Our latest research published last week in the journal PLOS Global Public Health reveals the world has decided the educational rights of 2 Dutch children are more important than those of 24,000 Nigerian children.

This matters deeply when the world collectively loses an estimated $492 billion through multinational corporate tax abuse and society’s wealthiest people evading tax. The richest countries lose the most in absolute terms, but the poorest countries lose the most relative to their budgets since they’re more reliant on those revenues. Even though the richest countries lose in the billions, they are also some of the biggest global enablers of tax abuse, including Switzerland, Ireland, the Netherlands, and the UK, with its overseas territories and crown dependencies.

You may be asking yourself why this is happening when most countries, even the richest, desperately need more money for health, education, better transport connections, and more housing. You name it, the list is long.

So what do European tax havens stand to gain in terms of their ability to look after their own populations by providing access to fundamental economic and social rights through luring corporate profits made in other countries? And what’s the impact on rights in countries that are losing out on tax revenue on these shifted profits? A group of us—including child rights advocates, tax experts, and economists from the University of St Andrews, University of Leicester and the African Centre for Tax and Economic Studies—wanted to find out.

There can be ‘no rights without revenue’

Tax havens are an anathema to human rights. When tax havens enable companies and people to dodge paying their fair share of tax where they do business or where they live, governments have fewer resources to spend on making sure we have a healthy and safe environment, our children can go to school, and our mothers do not die in childbirth.

Over 70 years ago, the world agreed on the Universal Declaration of Human Rights, guaranteeing the right to education and health. Our national governments are primarily responsible for meeting those obligations. Still, every country also has extraterritorial obligations to mitigate the adverse impacts of its companies and domestic policies in other countries.

For this reason, multiple UN human rights bodies, including the UN Committee on the Rights of the Child, have called out countries such as the Netherlands and Ireland for the deleterious impacts of their cross-border tax policy. The Committee asked the Netherlands to

Conduct independent and participatory impact assessments of its tax and financial policies to ensure that they do not contribute to tax abuse by national companies operating outside the State party that lead to a negative impact on the availability of resources for the realisation of children’s rights in the countries in which they are operating.

United Nations Committee on the Rights of the Child

The problem is that estimating the money countries lose to companies that shift profits to tax havens, and the gains tax havens are making is notoriously tricky when so much tax abuse hides under a veil of secrecy. For our study, we used the only data available on profits shifted from source countries to destination tax havens, originally published by Thomas Tørsløv, Ludvig Wier and Gabriel Zucman. You can take a look around the world of Missing Profits for yourself.

We focused on Nigeria as an interesting case study and as one of the only African nations with this data. Multinationals shifted an estimated 26% of their profits out of Nigeria 2019, so the country lost over 3% of government revenue. Nearly one-quarter was lost to European tax havens. The largest tax loss, over $200 million, was to the Netherlands. Yet the tax revenue generated in European tax havens as a result of profit shifting from Nigeria was almost negligible: 0.01% of government revenue.

2:24,000

Large numbers are meaningless to most of us, so we used the Government Revenue and Development Estimations (GRADE) model to translate how many children live (or die) as a result of profit shifting, how many more (or less) people can access clean drinking water, and how many more (or less) children can finish primary and secondary school.

The GRADE model works by realistically assuming governments allocate additional revenue in the same way they have over recent decades. It takes into account the quality of governance, and incorporating the impact of additional revenue on governance it accepts that revenue increases take time to show impact.

500,000 more Nigerians would have access to clean water

800,000 more Nigerians would have access to basic sanitation

150,000 children would be able to go to school each day

11 more children would survive each day (totalling 4,063 children each year)

European countries tax corporate profits shifted to their jurisdictions at relatively low rates. Coverage of essential social and economic rights in European countries is almost universal. Therefore, their populations do not gain much in terms of essential rights from shifted profits from Nigeria.

Let’s take the Netherlands. If they stopped enabling profit shifting from Nigeria, an additional 24,000 Nigerian children would be able to go to school each day, and this would impact the educational rights of 2 Dutch children.

How do we fix this?

Thankfully, this situation is far from inevitable.

We need national and international action to close the loopholes for profit shifting—double tax treaties need rewriting, tax ‘incentives’ granted to multinationals need carefully evaluating, and governments must require multinational companies wanting to do business in a jurisdiction to publicly disclose their profits, taxes, and assets on a country-by-country basis.

Tightening the screws won’t be enough though, because the global tax system needs reprogramming. This is now possible with ongoing negotiations for the UN Framework Convention on International Tax Cooperation. The convention seeks to end tax havens, level the playing field so multinational companies pay their fair share of tax, and create the first truly inclusive global body to manage cross-border tax. This, instead of the current arrangement where the Organisation for Economic Cooperation and Development (OECD) decides the international tax rules—an organisation made up almost exclusively of the richest and most powerful nations, often former colonial powers, who are largely responsible for enabling global tax abuse.

A finalised UN global tax convention could be voted on by the 193 UN member states in 2027 and then, it’ll be open for signature and ratification.

Tackling threats to progress

It’s not all smooth sailing, though. While Nigeria has led the charge with the African Group for these structural reforms to end profit shifting, notorious tax haven countries, including the Netherlands, have hindered progress. Nonetheless, the majority of the world’s nations voted in favour of the convention’s terms of reference last year.

Now, however, governments need to find ways to increase extra-budgetary support for negotiations because the UN’s liquidity crisis has led to a hiring freeze for the already-agreed-upon secretariat, which is to provide the technical and operational backstop for negotiations.

Last month, the US delegation, under the new US presidency of Donald Trump, walked out of the UN tax meetings and also ended its support for the rich-country-led tax rule-making at the OECD. Now that the US will not be disrupting negotiations from within, and given its aggressive stance towards countries trying to assert their tax rights, countries that have until now been hesitant about or tried to block enhancing the UN’s role in this area, including the UK, Australia, Japan and European Union members, should seize the opportunity for global solidarity.

Countries must now decide if they will support the African Group and Global South bloc to collectively exercise their right to tax major multinationals or give in to the US administration’s coercive tactics, as we analysed last month. The lives and well-being of many children around the world depend on it.

We at the Tax Justice Network are calling on UN Member States to demonstrate their commitment to a more inclusive and effective global tax system by making immediate financial contributions to support the preparations for the intergovernmental negotiations of the UN Framework Convention on International Tax Cooperation (UNFCITC). This landmark convention has the potential to reshape international tax cooperation, ensuring it serves all nations equitably—but only if the UN is equipped with the resources to move forward.

Member States agreed in December 2024 a budget for the secretariat of the UN tax convention negotiations, with a trim staff of around 20 and a total cost of US$6 million – which is very low for such international coordination processes. Without the ability to contract these human resources because of the hiring freeze, the preparatory work risks stalling, threatening the momentum of this historic process.

For countries with the capacity to contribute, now is the time to prove your commitment to a more inclusive and effective tax cooperation. The UNFCITC represents a once-in-a-generation opportunity to create a truly inclusive framework that addresses the needs of all nations – and a timely chance to demonstrate the value of multilateralism. By providing the necessary financial support, Member States can ensure the UN has the staff and resources to conduct these negotiations effectively, paving the way for fairer tax systems that combat inequality, fund public services, and support sustainable development worldwide.

We urge governments to act swiftly and provide immediate, extrabudgetary funding to bridge this gap. The world is watching, and the stakes could not be higher. Let’s seize this moment to build a tax system that works for everyone.

This guest blog for the Global Alliance for Tax Justice isthe second in a series exploring the five demands of the 2025 Global Days of Action on Tax Justice for Women’s Rights.

This year, for the first time in history, all UN member states will come together to negotiate a legally binding tax instrument. The UN Framework Convention on International Tax Cooperation represents a historic opportunity to fundamentally change how global tax rules are decided and offers an opportunity to establish tax policy that works for all, including for women.

Getting to this point in the process is an enormous win already in terms of international tax governance, but it is not time to sit back just yet. Our work has only just begun to ensure that the UN tax negotiations result in a better tax policy that aligns with UN human rights conventions and previous human rights commitments that States have made, including commitments to furthering women’s rights.

Last year while negotiating the terms of reference for the framework convention, several organisations called for gender provisions to be included in the terms of reference. International human rights law was included in different iterations of the draft terms of reference. However at one point, the concept was removed entirely before international human rights law was once again re-incorporated into the text. This version was subsequently approved by the General Assembly in December 2024. As advocates of women’s and girls’ rights we must remain vigilant. As the negotiations begin on the text of the Framework Convention and two early protocols, we need to continue to safeguard and champion the rights of women and girls to ensure they are not forgotten voices in the reforms being developed.

Tax is our social superpower. Tax policy has enormous potential as a transformative instrument for the development and well-being of the population at large and women in particular, but instead the way that tax policy is currently designed and implemented contributes to the persistence of inequalities, including of gender inequality.

When states lack adequate resources to pay for public goods and services, women are disproportionately affected. As states eliminate and underfund social services, the impact of this loss is felt most acutely among low-income populations, among whom women are overrepresented. Additionally, institutions and programmes to promote gender equality and support women’s advancement also lose funding and thus are unable to carry out vital work. Inevitably, women fill in the gaps in caregiving, education, and other family support and care work left behind by dwindling and disappearing social programmes, typically without remuneration.

Due to a lack of revenue, States will also often increase their reliance on regressive forms of taxation, such as consumption or value-added taxes (VAT) on basic goods and services. These taxes may be easy to administer, but they disproportionately burden women, meaning that women become responsible for a disproportionate amount of the tax burden while receiving fewer benefits from tax-funded services, losing social protections and support, and taking on an increased workload without pay.

The UN Tax Convention represents a window of opportunity to break this cycle by delivering on progressive taxation to ensure that the tax burden is fairly distributed, combating illicit financial flows, and introducing transparency and accountability measures that ensure corporations and wealthy individuals pay what they owe in tax. The convention not only offers a promising moment to reform our broken international tax system, but also presents a once-in-a-century opportunity to set better normative standards for future social, economic, and environmental challenges.

Without clear and targeted gender-responsive considerations, though, gender blind tax policies will fail to address structural inequalities in the organisation of care work and undermine progress toward gender justice by replicating harmful cycles. We demand that the UN Tax Convention is aligned with established UN human rights conventions and includes gender equality considerations in all relevant provisions.

The negotiation of the UN Framework Convention on International Tax Cooperation kicked off this week in New York where all delegates who spoke, from every region of the world, affirmed their country’s commitment to the principles of the UN tax convention. The only objection made came from the United States, which urged delegates to walk out of the room with it.

The opening gambit backfired. No country answered the US delegate’s plea, who proceeded to walk out alone, leaving the US isolated.

UN Member States now have a golden opportunity to prove their stated commitment to the process by addressing, without the US disrupting negotiations, the key issues of the organisational session without delays.

In international relations, it’s often said that countries have neither friends nor enemies, only interests. With Trump back in the White House, the geopolitical arena is undergoing a seismic shift, compelling nations to rethink what defending their national interest truly entails. The realm of international taxation is caught in this upheaval, and the UN Framework Convention on International Tax Cooperation (UNFCITC) negotiations began with a failed attempt of the US to undermine this process. After delegations from all regions had expressed their interest in engaging constructively in the process, the United States arrogantly walked out of the negotiation arguing that it was not aligned with its priorities and called on other states to do the same.

Against this backdrop, the stage is set for negotiations this week to be the battleground where countries’ ability to grasp that cooperation is essential to enforcing their sovereign tax policies, and safeguarding their peoples’ interests will be tested.

What’s on the line? Roughly half a trillion dollars a year to be clawed back from cross-border tax abuse, as reported in our State of Tax Justice 2024 report (see the report for country level estimates). And that’s just what can be clawed back from direct losses – the IMF estimates countries’ indirect losses to cross-border tax abuse are three to six times larger than their direct losses.

The weeks leading up to the start of negotiations had been full of upheaval. Shortly after taking office, Trump issued a memorandum that dealt the death blow to the OECD’s Two Pillars agreement. He also instructed the US Treasury to develop “protective measures” against countries whose tax policies the new administration deems to have an “extraterritorial” or “disproportionate” impact on US-based multinationals. Essentially, this move by the new administration signals a potential retaliation against what was seen as a shared goal of the international community. The goal is to tax cross-border activities based on where real economic activity takes place, irrespective of the location of the multinational’s headquarters, in alignment with the sovereign decisions of individual states, and to address other shared global challenges through cooperation among states.

About a hundred years ago, agreement eventually emerged between the imperial powers at the League of Nations on the need for a set of tax rules that the imperial powers can use to divvy up taxing rights over one another’s companies when they operated within each other’s territory. It took another 90 years for agreement to emerge that these rules should more accurately divvy up taxing rights based on where real economic activity takes place, and must be enjoyed by all countries, not just now former-imperial powers. And another 10 years to arrive at a proposal to implement this new agreement, albeit one that was too weak and too biasedly in favour of rich countries to make a real difference.

It took Trump just a few hours into his second term to do away with all this. Not only did Trump withdraw the US from the OECD’s global minimum tax proposal, he signalled plans to question and take punitive measures against the right of any country to tax American multinational corporations, effectively turning US tax policy back to a pre-League of Nations standing – to a time when companies could only be taxed by the imperial power they came from, regardless of where they were making their money.

In effect, the Trump administration made it clear that it intends to demand that countries cede their tax sovereignty over multinationals operating within their own borders – or face economic siege.

In a context where the US administration appears to view its tax sovereignty as incompatible with that of other states, its withdrawal from the negotiation comes as no surprise. However, the UNFCITC negotiation emerges more clearly as the only viable option for achieving the multilateral agreements on international tax issues that the world urgently requires (see our historic coverage of the path towards this stage of the process in our rolling blog). Faced with a US administration adamant on a might-is-right attitude towards taxing rights, the UNFCITC is essential to protecting the tax sovereignty of all countries.

These negotiations aim to create a more inclusive and equitable framework for international tax cooperation, addressing challenges such as tax evasion, avoidance, and harmful tax practices, effective mutual administrative assistance in tax matters, the alignment of international tax cooperation with the economic, social and environmental dimensions of sustainable development, and a fair allocation of taxing rights, which are particularly pressing for developing nations but will reap benefits for all countries (see our analysis on the Terms of Reference adopted by the General Assembly in November 2024 that will guide these negotiations).

Countries such as the UK, Canada, Australia, New Zealand, Japan, and members of the European Union, which have so far been hesitant to fully support these negotiations, now face a critical choice. They must decide whether to work constructively with the African Group and the Global South bloc of countries, which have been instrumental in advancing this process, or to abandon any hope of exercising their taxing rights over major multinationals for at least another four years, effectively yielding to the coercive tactics of the US administration (see an analysis of the fallacies used by UN Tax talk detractors and how to counter them).

Trump’s actions over the past few weeks have put the US’s cards on the table for these hesitant countries – and their people – to openly see. While previous US presidents finessed a double game, promising to abide by the OECD outcomes they controlled but never doing so, Trump has clumsily given the game away by pulling the plug on the OECD process, walking out of the most important tax negotiations of our lifetime, and threatening tax war.

This double game didn’t just benefit the US, it allowed the governments of OECD countries to save face in front of their people, publicly feigning an equal footing with the US on OECD decisions that impacted tax policy at home. Trump has now ended the façade, and called out other OECD members’ new clothes.

He has made it clear that there is no fair negotiation table at which the US will sit, so countries should have no qualms about pressing on with negotiations at the UN without the US. The early US withdrawal shows that this is a position irrespective of the dynamics of the negotiations – in fact, in spite of parties beginning to show constructive flexibility in order to reach agreements.

This is a spectacular own goal for the US. It is a movement that negatively affects the interests of its own people and US multinationals. The impossibility for states to adopt common rules for multinationals, including those headquartered in the US, to pay taxes where their economic activities take place would mean, in practice, the surrender of state sovereignty. And without the OECD double game to save face, governments that have so far been hesitant to the UNFCITC will not be able to hide this surrender of sovereignty. The choice is clear, both to governments and their people: defend your tax sovereignty by cooperating at the UN or raise the white flag to the new bully.

It’s time for all countries to work together and make the most of Trump’s own goal.

Why would a UNFCITC benefit all states?

The lack of effective and inclusive international tax cooperation harms all nations. Despite differing views on the desirable distribution of costs and benefits of cooperation on tax matters, all countries and their citizens —including the US — would benefit more from full cooperation than from the limitations of the current standards. States have opted for cooperation on tax issues because, in today’s global economy, enforcing their own sovereign decisions on how to tax cross-border activity necessitates collaboration with other countries. The advantages of such cooperation would be significantly amplified if a multilateral tax treaty fit for present and future challenges were ratified by the vast majority of United Nations member states, a feat not yet accomplished by any other fora. The challenge lies in crafting an international agreement that is acceptable to as many parties as possible, thereby maximising the overall benefits of cooperation.

What’s wrong with existing standards? Why do we need to change them?

While significant strides have been made in international tax cooperation over the last decade, the current standards fall short of being inclusive and effective, as highlighted in the UN Secretary-General’s 2023 report. This has resulted in an asymmetric cooperation landscape, which is less beneficial compared to what fully inclusive and effective cooperation could achieve.

For example, an information exchange mechanism would yield greater benefits if all UN member countries participated. The exclusion of even a single member diminishes the accessible information and the potential for exchanges among all participants. When a large group is excluded, the scope of the mechanism for any participating country is significantly narrowed and the legitimacy and equity of the mechanism left open to question. Currently, 125 countries are signatories to the CRS Multilateral Competent Authority Agreement on Automatic Exchange of Information, but this falls short of the 193 UN Member States. Moreover, requirements like the immediate duty to reciprocate can pose significant barriers for countries with limited capacities, often those in greatest need of the benefits from international tax cooperation. The exclusion of these countries not only disadvantages them but also reduces the overall potential benefits for countries already participating under the current framework.

Although several multilateral tax agreements exist, none encompass all nations globally. The UNFCITC presents an opportunity to establish universal standards that are adaptable to the varying capabilities of different countries, thereby maximising the benefits of international tax cooperation.

Is the UNFCITC an instrument that is only of interest to low- and middle-income countries?

The UNFCITC is often viewed as advantageous for countries in the Global South, but it presents substantial opportunities for all nations genuinely committed to a fully inclusive and effective international tax cooperation. For example, Australia, with its recently adopted world-leading standard for public country-by-country reporting, could leverage the UNFCITC to push for global adoption of these practices, despite its opposition to the UN resolutions that opened the door for the negotiation of this instrument.

Similarly, most EU countries, which have struggled with the need for unanimity in tax decisions within the bloc, could collaborate with nations from different regions to push forward tax cooperation on a global level through the UNFCITC. Here, dissenters could voice their opposition but wouldn’t have veto power, allowing for broader agreement while giving countries the option to opt out of specific protocols.

Even the United States, ironically, might find that the scenario of widely accepted UNFCITC offers stable, uniform global tax rules beneficial for its companies. Currently, the US has withdrawn from these negotiations with a short-sighted view of its national interest, citing the objectives of the instrument as overreaching and potentially detrimental to all nations. However, it may be the case that in the future, the US corporate sector might pressure the administration to re-enter negotiations to safeguard their interests.

The proliferation of multiple, parallel international tax regimes would elevate compliance costs and complexity for companies, thereby highlighting the advantages of a unified framework. Whether the US adheres to its announced withdrawal of the negotiations or reconsiders its stance—as it has with unilateral recent tariff decisions against several countries in the past few days—it might come to appreciate the value of such an agreement. This would help in averting a patchwork of unilateral tax policies that could otherwise complicate international business operations.

This potential future scenario is reminiscent of the OECD’s Common Reporting Standard (CRS), which only gained traction after the US unilaterally implemented the Foreign Account Tax Compliance Act (FATCA), compelling other countries to adopt automatic information exchange. This action followed a decade after the EU had already promoted a multilateral approach with its own system for internal information exchange. That progress in harmonising international cooperation measures could take place along a similar path once the UNFCITC enters into force cannot be ruled out at this stage.

Why won’t the UNFICTC duplicate progress made in other fora?

As the crisis over the implementation of the OECD’s Two Pillar agreement deepens, the objection that the UNFCITC might duplicate work from other fora becomes increasingly baseless. In fact, the UN Framework Convention on International Tax Cooperation (UNFICTC) is emerging as a potent multilateral instrument to truly fulfil the original mandate given to the OECD by the G20, which the Two Pillars agreements, even if they had been universally adopted, would have fallen far short of due to their failed design.

For the coherence of the governance system created by UNFCITC, it is necessary that the standards adopted are compatible with the framework that is agreed in an inclusive manner in the context of a truly universal forum. This alignment is crucial to prevent fragmentation. While this approach does not dismiss the progress made in specific areas to date, it does mean that negotiations aren’t starting anew. Instead, countries should evaluate which standards best fit within the new framework, taking elements from other fora which can be validated through a truly inclusive and effective universal system.

Some states have voiced concerns about starting from scratch in a new negotiation forum, especially when discussions on similar issues within the OECD have been ongoing for years. However, paragraph 22 of the Terms of Reference addresses these concerns by mandating that the intergovernmental negotiating committee should consider work from other forums, explore synergies, and leverage existing tools, expertise, and strengths from various international, regional, and local tax cooperation entities.

Together with the inclusion of the principle of human rights and several other elements that were modified with respect to the initial versions of the zero draft of the terms of reference, these changes show that, contrary to the possible allegation by rich OECD countries, the views of the different states participating in the process have been included in the decisions made by the Ad Hoc Committee that drafted the terms of reference. Unlike what has happened in the OECD’s closed-door negotiations, the ability for anyone in the world to follow these public negotiations provides the information necessary to monitor and scrutinise the work of the chair or the bureau and thus provides a greater guarantee of inclusiveness and transparency for all states.

What will be decided in the organisational session and why is it important?

During organisational sessions of UN conventions, one can expect decisions that lay the groundwork for the work of the Ad Hoc Committee that will draft the instrument. These sessions typically involve setting the agenda for future meetings, which outlines the topics to be discussed. Key procedural rules are established, including how decisions will be made, and the selection of leadership roles like chairs, bureau members and rapporteurs. The modalities for stakeholder involvement, including how NGOs, private sectors, and civil societies can contribute, are also decided upon. Logistical arrangements, like the scheduling and location of subsequent meetings, are confirmed. Moreover, these sessions often address the review or adoption of key initial decisions that will set the tone for future negotiations. These decisions ensure that the convention operates smoothly, with clarity and direction, facilitating global dialogue and action on the convention’s core issues.

The organisational session of the Intergovernmental Negotiating Committee on the United Nations Framework Convention on International Tax Cooperation, scheduled from 3-6 February 2025, has focused on several critical discussions (see adopted agenda here). The session began with the election of officers as per rule 103 of the General Assembly’s rules of procedure, where the Committee will elect a Chair, 18 Vice-Chairs, and a Rapporteur, ensuring equitable geographical representation and gender balance as outlined in paragraph 6 of resolution 79/235. Following this, the Committee proceeded to adopt the agenda, in line with rule 99 of the rules of procedure, adopting programme of work as prepared according to Assembly resolution 79/235.

Other key decisions include the establishment of the negotiation modalities for the coming years, particularly emphasising the decision-making processes of the negotiating committee. Another pivotal discussion will involve the selection of the second early protocol to be negotiated alongside the convention until 2027. Options for this protocol include dispute resolution and prevention, addressing illicit financial flows, and the taxation of high-net-worth individuals, with the first protocol already set to tackle the taxation of income from cross-border services in a digital and globalised economy.

Why consensus as the sole rule for decision-making is inconvenient for the process?

Decision-making procedures in the United Nations are consensus-oriented, but do not exclude the possibility of majority voting when time requires it and the possibility of super-majority votes for the most important decisions. The rules of procedure of the subsidiary bodies of the General Assembly are well established and experience shows that it is not appropriate to grant any country veto power, which is what happens when consensus is adopted as the sole rule for decision-making. The US withdrawal from the negotiations clearly demonstrates why veto power may be at odds with the mandate of the Intergovernmental Committee. Under a consensus rule, the threat of a veto means that all states would have to give disproportionate weight to the demands of one state to prevent that country from blocking the entire process, which is not only unfair but may make it impossible to fulfil the mandate of the Intergovernmental Committee within the set period. The decision to operate so far under the rules of the General Assembly has been a wise choice.

While some UN Conventions have indeed been adopted by consensus, this has predominantly occurred during significant political gatherings, such as the Earth Summit in Rio de Janeiro in 1992. Here, landmark conventions like the United Nations Framework Convention on Climate Change (UNFCCC), the Convention on Biological Diversity (CBD), and later in similar contexts, the United Nations Convention to Combat Desertification (UNCCD), were all adopted by consensus. However, when it comes to Ad Hoc Committees or other subsidiary bodies of the General Assembly, the experience has been markedly different.

The United Nations Convention on the Law of the Sea (UNCLOS) provides a pertinent example. Despite starting with the aim of achieving consensus, the negotiations for UNCLOS were fraught with disagreements, particularly over issues like the deep seabed and economic zones. Ultimately, after years of negotiation, when consensus could not be reached at the Third United Nations Conference on the Law of the Sea, the convention was adopted by a recorded vote in 1982, reflecting the failure of consensus as a decision-making mechanism in this context.

Other examples are also illustrative in this regard. For instance, the Ad Hoc Committee for the Arms Trade Treaty (ATT) attempted to adopt the treaty by consensus in 2013 but failed due to objections from a few states, leading to the treaty’s adoption through a vote in the General Assembly. Similarly, the Ad Hoc Committee on Measures to Eliminate International Terrorism has often struggled with consensus to adopt a Comprehensive Convention on International Terrorism (CCIT), frequently resorting to alternative decision-making mechanisms. Another example of the failure to reach consensus at UN bodies is evident in the ongoing discussions surrounding the Convention on the Rights of Older Persons. Despite years of debate within the Open-Ended Working Group on Ageing, established in 2010 to strengthen the protection of older persons’ rights, there has been no agreement on creating a new, legally binding international instrument.

More recently, the experience of the Intergovernmental Negotiating Committee on Plastic Pollution illustrates similar challenges. This committee, tasked with developing an international legally binding instrument on plastic pollution, has faced significant hurdles in achieving consensus among member states. The negotiations, ongoing with sessions from 2022 to 2024, have shown that while there is a common goal to address plastic pollution, the diversity of interests, particularly around production, waste management, and binding versus voluntary measures, has made consensus elusive. Despite the ambition to conclude by the end of 2024, the process has seen multiple sessions where consensus was not achieved on key elements, suggesting that if a final agreement is reached, it might require reverting to majority voting or other decision-making methods.

Some countries have suggested that since taxation is a matter that touches on the core of state sovereignty, there can be no rule other than consensus. However, it should be stressed that with the adoption of the established rules of the General Assembly and its subsidiary bodies, which allow for decision-making by simple majority, no country will lose the sovereign prerogative to decide whether to ratify the Framework Convention. The final word on whether to keep engaged in the negotiations, or to ratify the instrument resulting from the process, will remain being a sovereign decision of each state.

Unblock the Future (Protocols): Your Pledge to Progress

In the negotiations surrounding the UNFCITC there is a clear mandate for the Intergovernmental Committee to deliver results within the next three years. This urgency necessitates prompt decision-making during the organisational session, including the selection of the second protocol without unnecessary delays. One potential tactic to obstruct progress could involve arguing that procedural decisions require further clarity on substantive issues. However, this is a misstep since organisational sessions are specifically designed to establish the basic operational framework for later substantive discussions. These sessions are not meant to define the scope or content of specific thematic areas or agree on the meaning of some terms but rather to set the stage for state members to have these conversations in the next sessions. The Secretariat has initiated the good practice of providing background documents with the necessary elements for states to make informed decisions (as in the case of the potential scope of the issues that the second protocol may cover). This strengthens confidence in the process and shows that the United Nations is an appropriate forum to properly conduct these negotiations. Thus, the focus during the organisational session should be on procedural clarity —such as selecting the subject matter of the second early protocol in the terms that the Terms of Reference set— to facilitate the substantive work ahead.

A call to choose cooperation

States are urged to engage constructively in the negotiations for the UN Framework Convention on International Tax Cooperation, adhering to the principles of negotiating in good faith. This means having a clear and well-supported position, being open to finding solutions rather than adopting an inflexible stance and moving forward without unnecessarily revisiting previously settled issues. It involves a readiness to compromise and support outcomes where they have had significant influence and avoiding tactics to obstruct progress. Such conduct not only upholds a country’s image but is crucial for establishing trust among nations. In a world that desperately needs multilateral solutions, choosing cooperation is not just a choice—it’s the right choice.

As 2024 wraps up, it’s time to reflect on the impactful work and achievements of the Tax Justice Network over the past year. From groundbreaking initiatives to significant policy wins, this year has been a testament to the power of collective action in advancing tax justice. While we’ve celebrated important victories, looming challenges remind us of the critical work still ahead. Here’s a look back at the key moments and milestones that defined our work in 2024.

The year 2024 has seen both the biggest leap forward for tax justice – but also a setback that could prove catastrophic.

The huge leap forward is the overwhelming General Assembly vote on the terms of reference for the UN Framework Convention on International Tax Cooperation. Tax is fundamental to effective and responsive states that can deliver for their people, and so it is perhaps appropriate that tax is now seen as leading many other areas in moving beyond colonial governance mechanisms (in this case, the OECD) and instead towards globally inclusive decision-making. Delegates now have until 2027 to shape the new governance collectively. The opportunity to end decades of tax abuse and to re-establish the scope for progressive taxation is within reach.

The setback this year is the dismal failure of the climate COP in Baku to deliver meaningful climate finance. The refusal, on the part of the countries with historic responsibility, threatens to ensure that the human-made climate crisis becomes truly catastrophic. The next few months will tell if the situation can be recovered. Evidently, the tax tools are there to deliver the minimum necessary of US$1.3 trillion per year, in ways that ensure progressive outcomes both within and between countries. The tax justice movement has become increasingly engaged in climate policy over the last few years and may have a critical supporting role in 2025.

The EU Directive 2021/2021 This directive, which entered into force in December 2021 and applies to fiscal years commencing on 22 June 2024, has already been transposed by nearly all EU member states. As a result, these countries will soon have legislation in place for a wide-scope public country-by-country regime that applies to all sectors.

Australia’s new legislation: On 29 November 2024, the Australian Parliament passed new legislation. Under the new Australian requirements, large multinationals with substantial activities in Australia will soon begin disclosing comprehensive tax and operational data for a range of jurisdictions, some of which are highly ranked on our Corporate Tax Haven Index , including Singapore (ranked 5th) and Hong Kong (ranked 6th), none of which are currently subject to reporting requirements under any other legislation [The legislation is the Treasury Laws Amendment (Responsible Buy Now Pay Later and Other Measures) Bill 2024, available here. The specific element, ‘Schedule 4: Country by country reporting’, is detailed here].

U.S. submissions: In the United States, the first submissions of public country by country reports that apply to companies active in the extractive industries are expected to be filed by the end of 2024, including by the Big Oil companies. This comes after nearly 14 years of US Big Oil companies successfully preventing the reporting (included in the Dodd-Frank Act of 2010) by repeatedly challenging its implementation rules, both in court and in Congress. The required data includes information on mining royalties, dividends, fees, and a few other types of payments made to governments, as well as information on the amount of tax paid per country. The ICIJ details the long fight here.

Corporate Tax Haven Index

In October, we launched a redesigned website for our Corporate Tax Haven Index, which ranks countries based on their level of complicity in helping multinational corporations underpay corporate income taxes in other countries. The latest update to the Index shows that three British tax havens – the British Virgin Islands, the Cayman Islands, and Bermuda – retain the top three positions, respectively. The British Crown Dependency of Jersey ranked 8th once again, maintaining its position among the top ten.

One positive development this year, however, was the approval of the EU AML Package which, limited by the European Court of Justice ruling on public access, still tries to expand and facilitate access to Beneficial Ownership information for many stakeholders, including journalists, civil society organisations and academia, by recognising their “legitimate interest” to get access to info.

Tax Justice Network Research

Several of our research streams have seen significant developments in 2024. These include:

As part of the State of Tax Justice 2024 report, we published estimates of the scale of corporate tax abuse and tax abuse related to offshore wealth for the six years of data that is currently available (2016-2021), highlighting the sad upward trend in the tax losses incurred due to these practices.

We provided estimates of the potential tax revenues stemming from wealth taxes implemented at the national level, including a calculator that allows everyone to design their own wealth tax.

Continued collaborations using administrative-level data with government authorities around the world – we ran capacity-building meetings within our existing work in Uganda, Nigeria, and Slovakia, and established new research collaborations in Honduras, Czechia, Zambia, Benin, Ghana, and Tanzania.

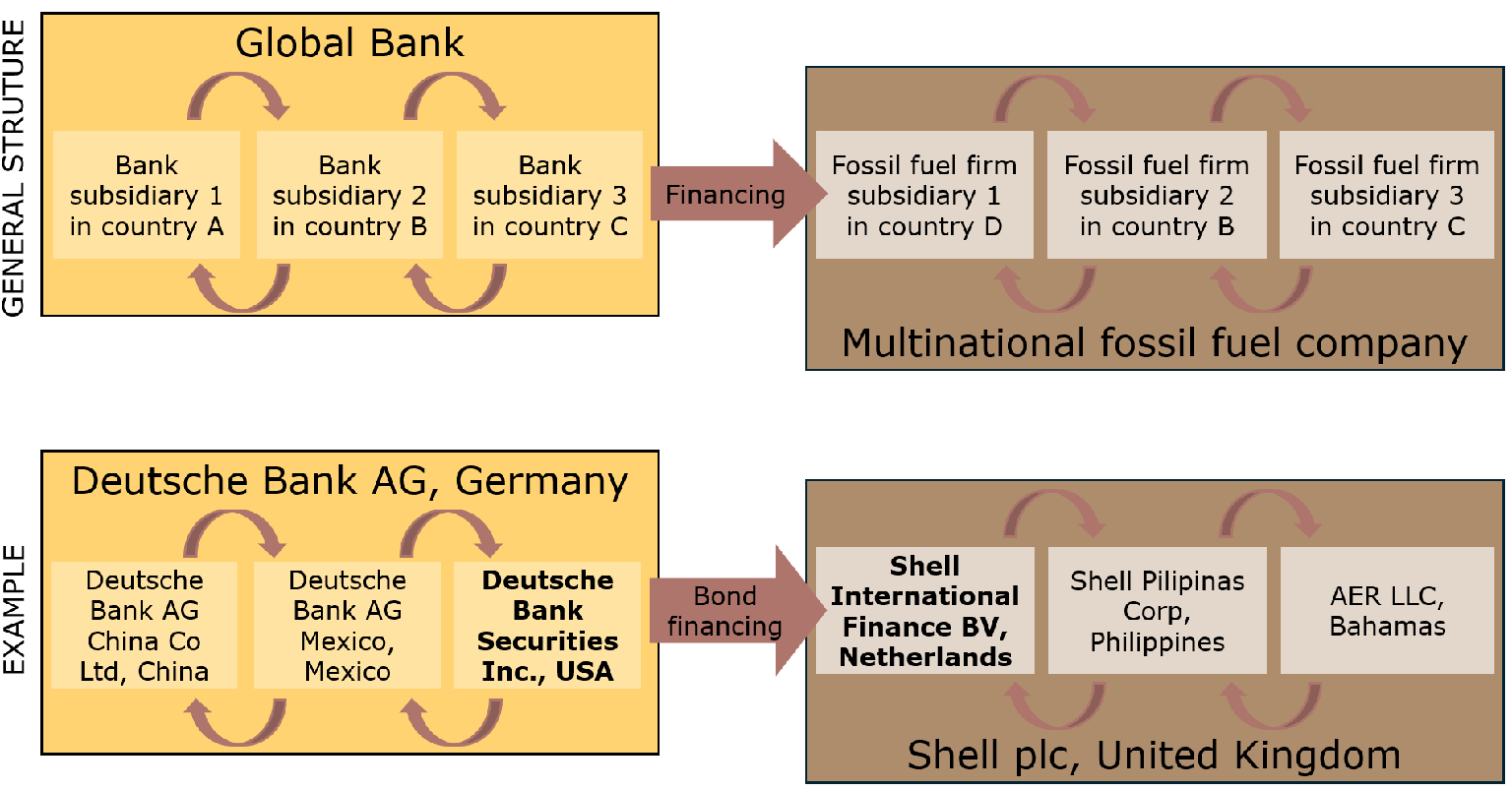

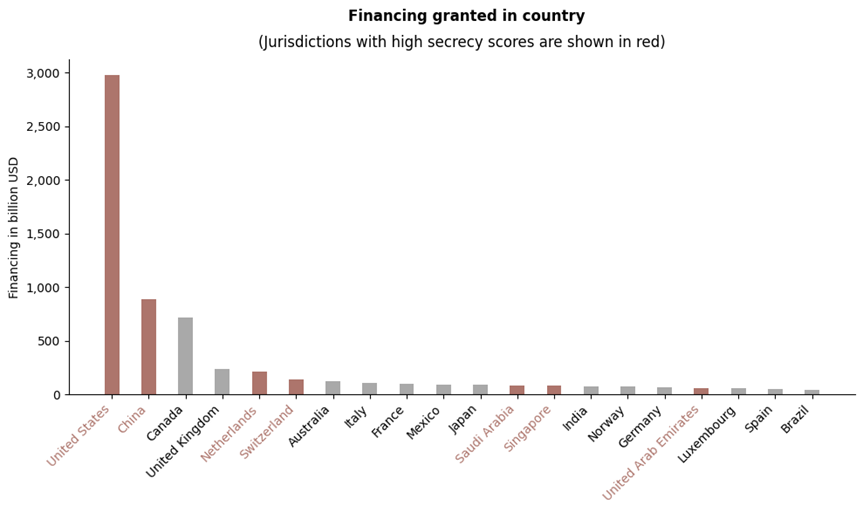

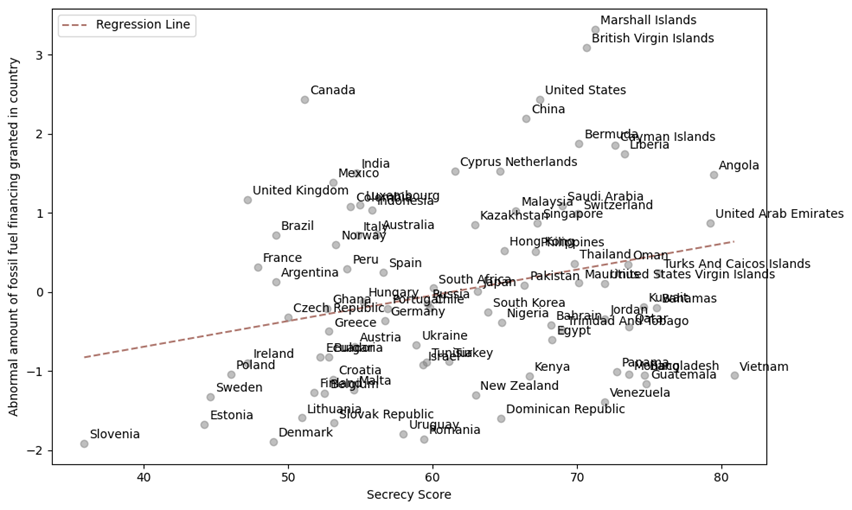

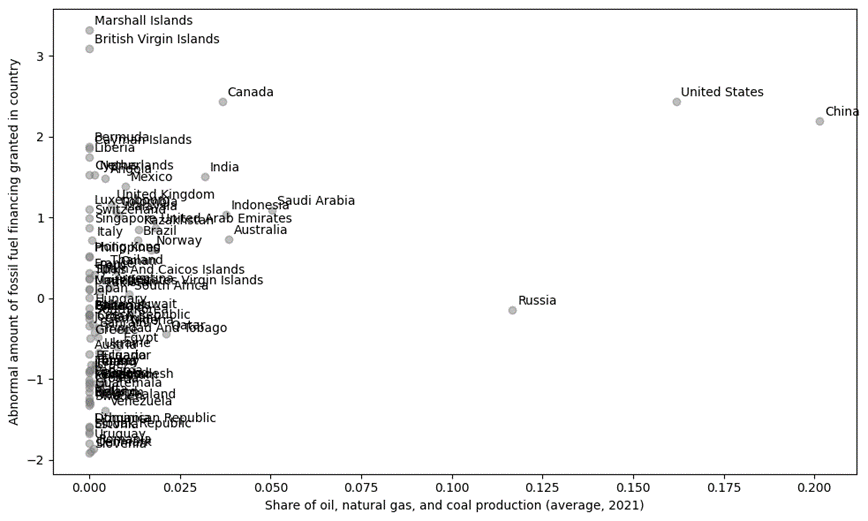

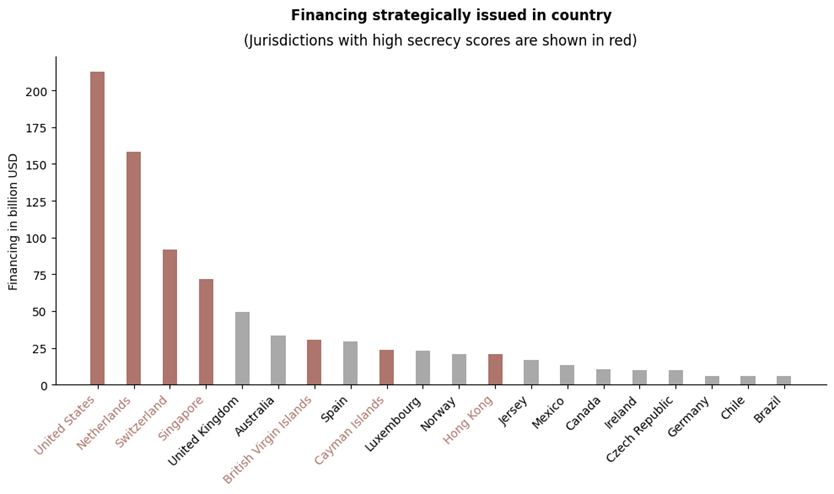

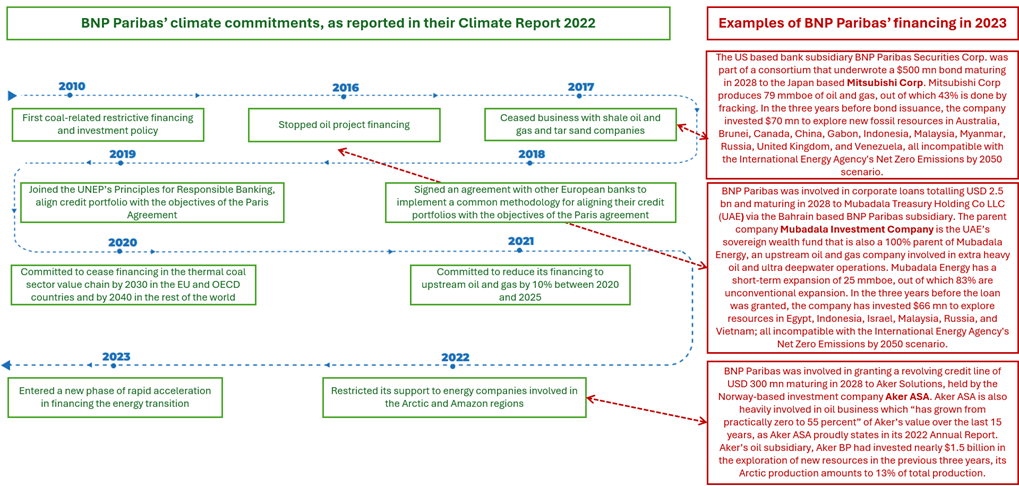

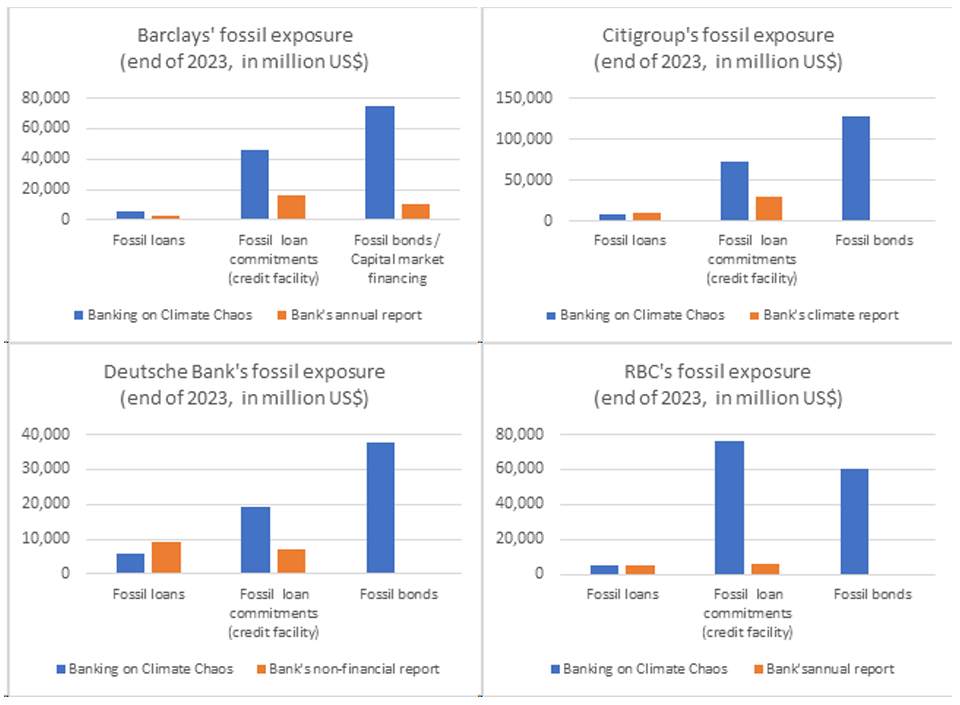

We published a report that examines the fossil fuel financing provided by the 60 largest global banks, exploring how funds are strategically channelled through high-secrecy jurisdictions.

We also continued to actively participate in the academic research environment. Some of our research outputs are now being published as part of the new Tax Justice Network Working Paper Series and we have presented papers at a number of international academic conferences.

The State of Tax Justice

Our annual State of Tax Justice 2024 report, launched in November, revealed countries are losing US$492 billion in tax a year to multinational corporations and wealthy individuals using tax havens to underpay tax. Nearly half the losses (43%) are enabled by the eight countries that remain, as of writing, opposed to a UN tax convention: Australia, Canada, Israel, Japan, New Zealand, South Korea, the UK and the US. (Argentina has recently become the ninth). The 2024 edition of the report is available here.

Tax Justice and Human Rights.

International advocacy – UN Framework Convention on International Tax Cooperation

The United Nations Framework Convention on International Tax Cooperation (UNFCITC) intergovernmental negotiations have continued to be an important focus of our advocacy work in 2024. We have actively contributed, in collaboration with a range actors, to shaping civil society engagement through both written and oral contributions. Our advocacy efforts extended beyond the tax justice movement (e.g. biodiversity, land use, human rights, climate, digital economy) to raise awareness of the UN Tax Convention and the relevance of our policy framework. [UN Tax Subtopic] – Statements & Interventions

We have tried to ensure that crucial issues like our ABC…G3 of tax transparency, the fight against illicit financial flows, and the recognition of human rights as a foundational principle remain central to the negotiations. Read more about CSO statements and interventions here.

Throughout the year we provided key data and analysis to strengthen accountability for multi-stakeholder monitoring of the UN Tax Convention. Our figures, databases and summaries were used as a reference by other civil society organisations, journalists and negotiators. Here

Allied to our work on the UN Tax Convention has been an important collaboration with human rights advocates. With our Litany of Failure briefing, we have turned the spotlight onto OECD failures in global tax governance. The briefing catalogues the various problematic issues that have emerged through the OECD’s leadership of standard-setting in international taxation. Working closely with the Centre for Economic and Social Rights, the Minority Rights Group and other partners, we have also published this letter exchange with Manal Corwin, Director of the Centre for Tax Policy and Administration at the OECD cataloguing concerns regarding the impact of OECD tax policies on human rights.

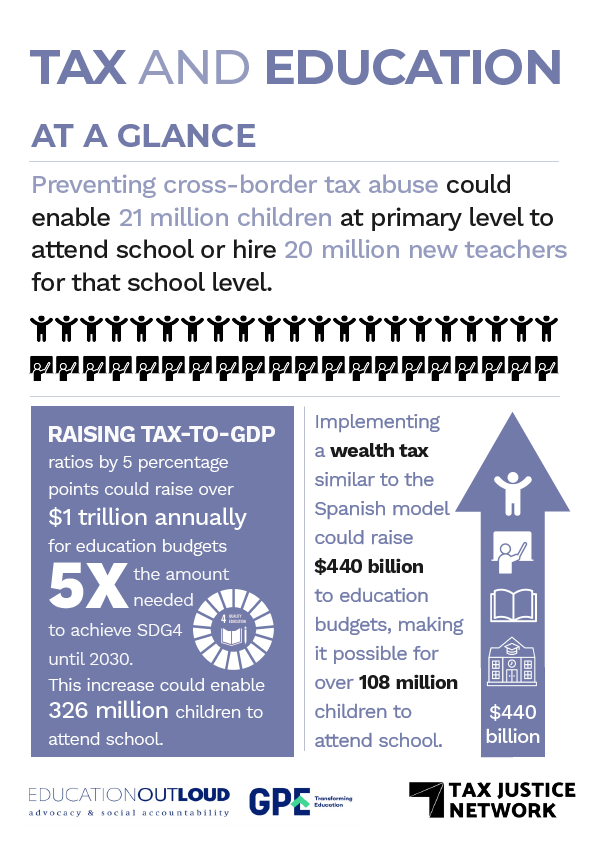

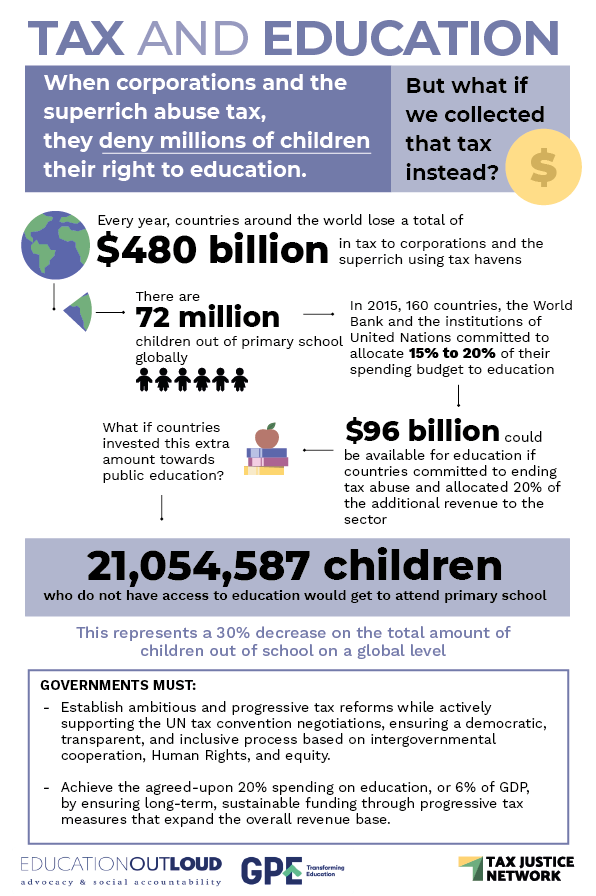

Right to Education

In October, we published our Stolen Futures: The Impacts of Tax Injustice on the Right to Education report. The report investigates how revenue lost to tax abuse reduces funds available for education systems worldwide and explores how measures such as wealth taxes and raising tax-to-GDP ratios could unlock significant resources for education budgets. We presented our findings in November 2024 at the Global Education Meeting in Fortaleza, Brazil, a high-level gathering of Ministers of Education, Ministers of Finance, thought leaders, and advocates addressing sustainable strategies for education financing. (See also the Fortaleza Declaration). In preparation for the event, we also participated in UNESCO’s webinar on education financing, where we shared preliminary findings and contributed to discussions on the critical role of tax justice in ensuring sustainable and equitable education financing. For more on the Stolen futures report, please read: Press releaseLaunch blog

We also published a collaborative C20 Education Working Group final paper that prioritises tax justice in the education agenda. Key opportunities emerging after the Stolen Futures publication include the Financing for Development 2024 and the Second World Summit for Social Development. Additionally, we engaged with the Global Education Monitoring countdown to 2030, addressing gaps in SDG4 implementation, including education financing.

Our contributions have highlighted the importance of aligning tax justice with education financing and the need for progressive tax measures to achieve equitable and sustainable development outcomes .

Gender equality and women’s rights: CEDAW Brazil review (May 2024, Convention on the Elimination of All Forms of Discrimination against Women)

The Tax Justice Network, Institute of Socioeconomic Studies (INESC), Latindadd and Red de Justicia Fiscal para America Latina y Caribe successfully finalised and submitted a Shadow Report focusing on tax justice and women’s rights in Brazil. Together with Institute of Socioeconomic Studies representatives, we participated in the 88th CEDAW session in Geneva, including a meeting with the Minister of Women and engaging with Ms Marion Bethel (CEDAW Committee chair), who utilised proposed questions and data to question the Brazilian delegation. We welcomed the opportunity to join a panel event with Geledés (Black Women Institute) to discuss the intersections of tax justice, gender, and racial inequalities. Additionally, the group published an op-ed in Carta Capital, participated in episode 62 of the É da sua conta podcast, and released several blog posts emphasising the Shadow Report’s recommendations. A post sessional feedback workshop with Civil Society Organisations involved in the 2023 consultation was organised by the group. Those who connected up during the CEDAW review provided an exciting opportunity to collaboratively plan the next steps, including the development of a booklet on tax justice and women’s rights, capacity-building sessions for feminist organisations, and joint advocacy efforts in the Brazilian Congress, plus international events (this year around G20, and starting preparations for next year around the Beijing Declaration anniversary, the Brazilian presidency of the BRICS and COP30).

Participating in the Inter-American Commission on Human Rights in Washington, DC was a humbling experience. The event centred on the voices and experiences of communities directly impacted by financial secrecy and Special Economic Zones, highlighting their efforts to advance climate justice (you can view that here). Additionally, we strengthened our connections within the global climate movement through the FAIR convening in Istanbul.

Events

In March, we collaborated with a number of civil society organisations to host an international policy and research conference at the Paris School of Economics, to explore the question ‘How can a UN Tax Convention address inequality in Europe and beyond?’. The two-day conference brought together academics, journalists, policymakers and activists to consider the potential of a UN Tax Convention to support meaningful progress against tax abuse, reduce inequalities within and between countries, and to strengthen the ability of states to respond to the climate crisis. The conference featured keynote speeches from Gabriel Zucman, Economist and Director of the EU Tax Observatory, Bjørg Sandkjær, State Secretary of Norway, and María Fernanda Valdés, Deputy Minister of Finance of Colombia.

The Tax Justice Network reaching people.

Communications and media

The Tax Justice Network continued to bring tax justice issues to more people through our media and online work in 2024. Our research and commentary was featured in over 3,200 media and press articles in over 120 countries with a reach of over 30,011,600,000. Over 319,000 sessions occurred on the Tax Justice Network website in 2024.

Our podcasts (advocating for tax justice in five languages)

Tax Justice Network podcasts are available wherever you get your podcasts or on our podcast website. They’re all productions by different teams focused on their regions. To give you a little taste, here’s just a few of the highlights in our podcasts this year:

On the Taxcast (in English) we kicked off 2024 with inspiring stories on campaigns for tax reform from around the world: strategies, successes, limitations, and what we can learn from the first in-depth studies of their kind. We also provided some in-depth coverage on crypto risks, looking at blockchain havens and crypto heists, as well as presenting our research on the international scandal of Greenlaundering, following the money which shows how financial secrecy is allowing banks to hide the true scale of their backing for activities that are accelerating the climate crisis. Our Taxcasts have also followed the successes of negotiations at the United Nations progressing towards a UN Tax Convention, as well as looking at potential corruption of the global rule maker on tax, the ‘rich country club’ of the OECD. We also provided analysis on the world’s moment of clarity regarding Donald Trump’s election win, All’s Not Lost and ended the year with a look at a $6.2 million banana artwork purchase (a sad illustration of the urgent need for wealth taxes) and how governments can apply our wealth tax proposal which could help governments increase their national budgets by 7 percent a year, a potential global revenue of more than 2 trillion US dollars annually.

And finally, in 2024 we launched and concluded Series 1 of The Corruption Diaries, an easy listening podcastwith 44 episodeswhich takes you on a journeythrough the eyes of anti-corruption veterans with their unique perspectives from a lifetime spent combating the most compelling ethical challenges of our time. Series 1 features conversations with Jack Blum, one of the US’s leading white-collar crime lawyers, specialised in investigating money laundering, financial crime and international tax abuse. Series 2 is coming in 2025.

This year our work featured in more than 80 broadcasts, 2,978 online media articles, and 223 print pieces in over 120 countries, and saw more than 230,000 visitors to our website.

To help you stay up to date with everything you might have missed this year, we’ve put together a handy list of our most read pieces from 2024.

Our most viewed country profiles saw some surprising shifts, with Indonesia unexpectedly rising to the top spot, followed by Switzerland. The United Kingdom dropped to third place, while the Netherlands climbed to fourth. The United States rounded out the top five as our fifth most viewed country profile.

Reforming the international tax system is our only shot to find the means to mobilise missing climate finance in the necessary order of magnitude. The current international tax regime leaves trillions of dollars of tax revenue on the table because of its inability to eradicate tax abuse and its under-taxation of wealth. The current regime also fails to help Global South countries maximize their potential for domestic resource mobilisation, which is much needed to finance their fight against climate crisis. The persistent problem of financial secrecy further worsens the climate crisis problem, and thereby increases the climate finance bill.

In this blog, we’ll show that the future of inclusive tax cooperation on the interface of tax and climate lays with the United Nations Framework Convention for International Tax Cooperation, negotiations on which will start in 2025.

Along with this blog, we’re publishing today a new briefing on seven principles of good taxation for climate finance.

The climate crisis is a story of inequality that comes with a daunting price tag

There is inequality of responsibility for the climate crisis: to this date, the Global North is estimated to have contributed 92% of cumulative greenhouse gas emissions. Yet the Global South faces the brunt of the consequences, while having contributed the least to the problem.

On top of that, the means to finance a way out of the crisis are deeply unfairly distributed: the Global South, having the least blame and most burden to bear, has dramatically far less financial means than the Global North to put towards mitigating the climate crisis.

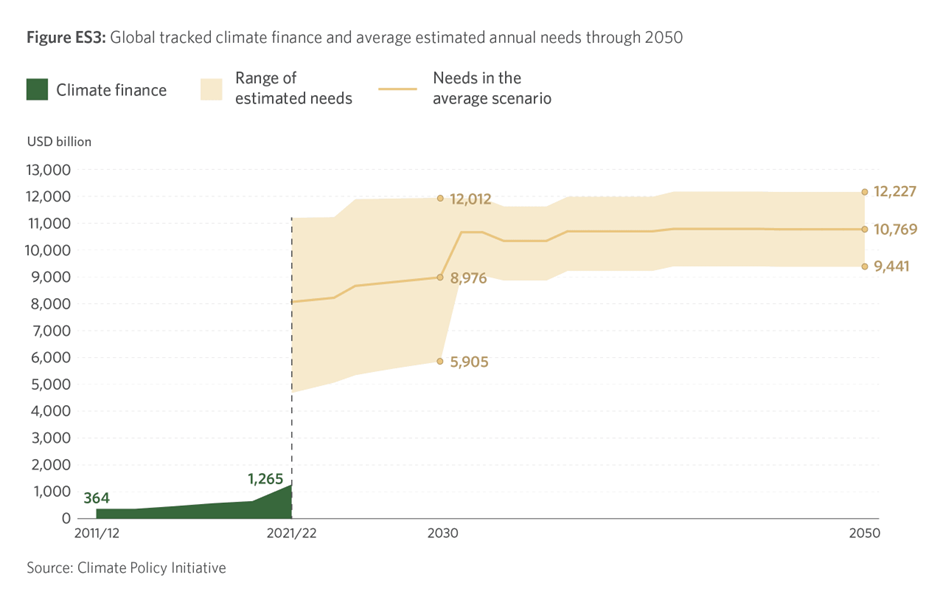

Let there be no mistake: a lot of money is required to deal with the climate crisis. Estimates by the Climate Policy Initiative show that the combined annual cost to deal with the climate crisis in all countries around the globe will reach $9 trillion by 2030. Every moment of in-action increases this bill further. Currently, the annual amount dedicated to climate finance hovers below US$1.5 trillion – negligible compared to what the world really needs.

Climate finance: money for what and how much?

What exactly are these mindboggling sums needed for? Climate finance essentially serves three purposes:

Climate mitigation, or measures to reduce the sources of greenhouse gas emissions or increase storage of emitted gases (eg the establishing of a cleaner transportation system or the increasing of forest sizes);

Climate adaptation, or measures to adjust society to the current and future effects of climate crisis (eg the building of flooding walls);

Loss and damages, or funding to deal with the negative economic consequences of climate crisis that go beyond what people can adapt to (eg the cost to repair damages resulting from extreme weather events)

It is clear that the richer countries of the Global North need to pick up a large chunk of the South’s climate finance bill. This is needed not just to aid these countries’ mitigation efforts, but also to assist in climate-proofing societies and paying for climate damages suffered by those that bear little responsibility.

But how much external financing from Global North to Global South is enough to give developing countries a chance to adapt, mitigate and pay for ongoing loss and damage? These dimensions of a new collective quantified goal (NCQG) for climate finance were the topic of negotiations in Baku during the latest Conference of the Parties to the Paris Agreement (COP29).

Prior to the COP, UN Trade and Development (UNCTAD) released new estimates which reveal that developing countries would need about $1.1 trillion in annual climate finance from 2025 and some $1.8 trillion by 2030. Developed countries would need to fund at least three quarters of the funds required by their developing counterparts. Alarmingly, only one-fifth of developing countries’ financing needs is expected to come from domestic resource mobilisation (DRM), leaving around up to $1.3 trillion a year to be derived from developed countries.

Importantly, the climate finance should also meet certain qualitative standards. Currently, over 3.3 billion people live in Global South countries that spend more on interest than on education or health. Climate finance to Global South countries only makes sense if it expands the fiscal space of those countries rather than stifling development any further be increasing countries’ level of indebtedness. As such, the goal of climate finance should be rights and needs-based, and allocated primarily in the form of grants rather than loans. There must also be no double-counting: the funding should be additional to the existing official development assistance (ODA).

That time of the year: post-COP disappointment

At COP29, not much came to fruition of the ask for a strong commitment from the Global North to fair climate finance of an amount upwards of $1.3 trillion a year by 2035. In Baku, developed countries agreed to channel ‘at least’ $300bn a year into developing countries by 2035 to support their efforts to deal with climate crisis, a fraction of the expected real needs. The underwhelming, new climate finance goal has left developing countries bitterly disappointed. As Panama’s climate envoy put it: “this very low level of finance … means death and misery for our countries.”

There is, of course, another way.

Instead of rich countries essentially claiming they cannot afford to deal with the climate crisis they created because public finances are tight, public finances themselves need to be reformed. That means looking at the elephant in the room of climate finance diplomacy: the international tax system.

What’s tax got to do with it? Everything.

Tax is our social superpower. Not only does tax generate the revenues needed to fund public goods, it also provides a tool to correct societal wrongs and correct inequality in society. And it provides the main way to redistribute means among citizens.

This is not different in the case of climate finance.

Whether funds are raised through domestic resource mobilisation in the Global South or via public financing in the North, nearly all of it originates as tax revenue. Given the magnitude of the climate finance gap, our tax systems need to perform to serve climate mitigation and adaptation efforts.

Because of climate crisis, we cannot afford to play fast and loose with tax and financial transparency.

Currently, we play loose.

In our recent State of Tax Justice 2024 report, we show that countries lose US$492 billion of tax revenue a year o multinational corporations and wealthy individuals using tax havens to underpay tax.

US$492 billion from corporate and private cross-border tax abuse is of course a far cry from the US$9 trillion needed for global climate finance. However, if these losses were to be eliminated, revenue gains would be much higher because if the loopholes through which taxable profits leak to tax havens are closed, countries will no longer feel pressured to keep tax rates low.

This pressure and the knock-on effects of corporate tax abuse in particular additionally cost countries what gets called the “indirect costs” of cross-border corporate tax abuse. The IMF estimates that these “indirect costs” are three to six times greater than the “direct costs” of corporate tax abuse. Of the US$492 billion countries lose a year, two-thirds (US$348 billion) is due to corporate tax abuse – this is the “direct costs”.

Eliminating global tax abuse would mean both direct and indirect costs, so tax revenues from multinational corporations wouldn’t rise by hundreds of billions a year but potentially by trillions. A global increase of the average effective tax rate on corporate profits by the biggest multinational enterprises by few percentage points would likely result in additional revenue gains in the hundreds of billions. Such a ‘climate finance corporate surcharge’ should be earmarked to serve countries’ climate finance obligations.

If, in addition to closing the loopholes for offshore income tax abuse, countries would introduce a progressive net wealth tax on the richest taxpayers, trillions of additional revenue can be gained. As pointed out by Oxfam, the richest 1% emit as much planet-heating pollution as two-thirds of humanity.

According to our recent calculations, a net wealth tax, based on the one implemented in Spain, of roughly 2% to 3% on the richest 0.5% would yield an annual revenue of US$2.1 trillion a year. Not only would a climate finance solidarity surcharge address this rampant inequality, it would also be the ultimate implementation of the polluter pays principle.

Tax havens not only help drain critical public resources from countries, they also conceal fossil fuel financing and enable environmental crimes. Unless we address ‘greenlaundering’ and the financial secrecy which hampers mitigation efforts through fossil fuel divestment, much of climate action is nothing more than rearranging the deckchairs on the Titanic. To put things in perspective, last years’ numbers show that tax havens cost governments as much tax revenue as the yearly global cost of climate losses and damages.

The mutual finger pointing of tax v. climate

The price tag of the climate crisis makes it so that we have little choice than to make fundamental changes to the current architecture of international tax and architecture. We simply cannot afford the massive corporate tax abuse, the undertaxed private wealth and the financial secrecy that hinders the green transition. But to make change happen, we should be able to rely on global tax governance structures that are inclusive and effective, and accept the premise that tax policy and climate action are two sides of the same coin.

At the moment, such structures do not exist. The OECD and G20 – limited membership organisations that have monopolised global tax governance – are shockingly masterful in entrenching the separate silos of tax and climate. The OECD’s global minimum tax regime under Pillar Two is a case in point.

This byzantine tangle of rules implements the fundamentally good idea that corporate profits should be taxed at a minimum level. The new rules include a provision which essentially allows certain profits to be taxed below the minimum level if they reflect economic substance in the form of real assets and employees. A laudable idea, but in light of the climate crisis, can the world afford this type of neutrality? Implementing a global system which incentivises oil business to grow their business because bigger and more oil rigs means a larger allowance for undertaxed profits seems absurd.

The cross-border effects of the minimum tax rules have triggered a never-before-seen global review of corporate tax incentives. The fact that the climate crisis is completely ignored as a parameter for these reviews is a huge, missed opportunity to unleash the power of corporate taxation for the sake if climate action.

Unsurprisingly, the recent Rio G20 Declaration of November 2024 is similarly disappointing on the links between tax and climate. For example, the G20 ‘reiterates its commitment’ to the Two-Pillar Solution, including the (climate crisis ignoring) minimum tax regime. As for climate action itself, the G20 leaders do not raise the tax topic and simply ‘encourage each other to bring forward net zero greenhouse gas emissions and climate neutrality commitments’.

This lack of ambition by the self-proclaimed leaders of the world is unacceptable, especially to those (unrepresented) countries most affected by climate crisis. It is to this backdrop that a number of small developing island states are currently requesting the International Court of Justice to formally condemn the lack of climate action as a violation of international law.

Unfortunately, the Paris Agreement is also not very helpful to further the ‘tax meets climate’ agenda. The Paris Agreement is obviously a landmark in the multilateral fight against climate crisis as it sets all-important carbon emission-reduction goals. But these so-called nationally determined contributions (NDCs) are non-binding pledges and do not come with concrete agreements on coordinated action to meet these national targets.

The Paris Agreement also doesn’t sufficiently address the issue of unequal burdens faced by the Global South and historical responsibility. In recent negotiations by the conference of parties, additional goals like the loss and damages fund (COP28 in 2023) and the new collective quantified goal (NCQG) for climate finance were partically agreed. But the outcomes are too little, too late and too unambitious.

To make things worse, tax is not mentioned once in the text of the Paris Agreement, nor has it ever been the dedicated focus of any COP, nor will it likely be in the future. Just like the G20 points to the Paris Agreement to deal with climate, the Paris Agreement essentially points to elsewhere when it comes to tax in relation to climate. That’s a shocking reality, given tax’ crucial role in climate action and climate justice, whether through domestic resource mobilisation in the Global South, efficient and equitable revenue raising for climate finance in the North or effective climate mitigation and adaptation efforts in all countries south, north or in between.

It’s clear that at the intersection of tax and climate, the world is currently missing an important piece of the global governance puzzle. But change may be within reach.

A new dawn: the UN Framework Convention on International Tax Cooperation

On 27 November 2024, the world may have given itself a lifeline when it comes to solving the tax and climate governance issue. On that day, a landslide majority of countries voted in favour of the adoption of a UN General Assembly Resolution which formally kicks off, as of 2025, the negotiations for a United Nations Framework Convention on International Tax Cooperation (UNFCITC).

The Resolution also adopted the draft Terms of Reference (ToR) that were developed by an Ad Hoc Committee over the course of 2024 and which will guide the upcoming negotiations. The terms provides that ‘a holistic, sustainable development perspective that covers in a balanced and integrated manner economic, social and environmental policy aspects’ is one of the principles and commitments that should be included in the Convention. The terms lists ‘tax cooperation on environmental challenges’ as one of the explicit topics that could be considered for a substantive protocol under the Convention.

Even though nobody doubts that the upcoming negotiations of the Convention will be extremely tough, the inclusion of the climate related elements in the Terms of Reference is a hopeful first step to push for a new approach to tax and climate.

Some countries, like Spain, Colombia, Pakistan or the Bahamas would have preferred for the terms to go further and strive for a much more comprehensive integration of tax policy and equitable climate action. These countries should be supported to not give up on their agenda in the upcoming negotiations.

Inspiration can be drawn from the Agreement on Climate Change, Trade and Sustainability (ACCTS). In this first-of-a-kind hybrid trade and environment agreement signed in 2024, four otherwise unrelated countries – Costa Rica, Iceland, New Zealand and Switzerland – agreed to live up to their climate ambitions and only wield their national power to create trade rules if consistent with climate targets. This includes the formal commitment to remove fossil fuel subsidies.

The ACCTS is purposely designed as an open plurilateral agreement, meaning that it’s agreed by a select few countries who are betting on the fact that other countries will join later, which they can do under the agreement at any stage. A ‘sustainable climate tax protocol’ in which an ever-expanding group of countries commit to creating national tax policy in line with pre-agreed principles of good taxation for climate finance may very well follow a same path.

The adoption of the UNFCITC along the lines set out in the terms of reference will be a massive boost in the race to meet the US$9 trillion climate finance challenge. Filling the climate finance gap requires uprooting the current system of international tax governance centred around the OECD/G20. It also requires urgent and universal progress in the fight against corporate tax abuse, the eradication of financial secrecy, the effective taxation of extreme wealth and the increase of cross-border assistance to enforce tax laws. These elements are front and centre in the terms and are expected to form the main focal point of next year’s negotiations.

At the same time, inclusive tax cooperation also implies establishing a fair and equitable international tax system which strengthens the Global South’s potential for domestic resource mobilisation, and, as a consequence, the reduced reliance on external climate financing pledges by the countries in the North.

A successful UNFITC negotiation can make this happen.

And, to be frank, it has to make it happen. The world has few options left to successfully face the climate challenge ahead. Countries must seize next year’s lifeline opportunity with everything they’ve got.

The UN General Assembly is expected to approve the terms of reference for negotiation of a Framework Convention on International Tax Cooperation (UNFCITC) in November. This will be the latest milestone in an historic initiative to shift global standard setting on tax cooperation from the Organisation for Economic Cooperation and Development (OECD), which only represents the interests of the 38 most industrialized nations, to the UN, where all countries have a voice.

As a civil society collective working towards social, economic, racial and climate justice, we call on the OECD to support the UN process and to provide a meaningful response to the concerns raised by both UN experts and civil society that its proposed ‘two-pillar solution’ to cross border tax abuse would prejudice human rights in developing countries.

In December last year, a group of eight UN human rights experts, including the Independent Expert on Foreign Debt and Human Rights, the Special Rapporteur on Racism and the Special Rapporteur on the Right to Food, made a historic communication to the OECD warning of the negative human rights impacts of its ‘two-pillar proposal’. The experts warned that the OECD’s reforms would widen racial and gender inequality both between and among countries whilst robbing the already impoverished countries of the Global South of much needed revenue to resource economic, social and cultural rights. The communication further laid bare how the OECD’s reforms would prejudice the predominantly non-white nations of the Global South, thus impeding their right to development and exacerbating poverty and inequality.

In August, an Ad Hoc Committee established in accordance with a resolution brought forward by the Africa Group adopted the terms of reference for negotiations by landslide majority, with 110 nations in favour, 44 abstentions and 8 countries voting against. The terms of reference are notable for including adherence to human rights principles as an objective of the Convention. Most OECD states abstained from the vote whilst several opposed the motion. The OECD had previously sought to undermine rights-aligned reforms through the UN process. Throughout the sitting of the Ad Hoc Committee, OECD countries have argued that the UN process should remain complementary to parallel OECD reforms; that the UN process amounts to duplication; and that agreement should be achieved by consensus – a criteria that would allow veto power for OECD countries through the back door.

As a collective of organizations working on social, economic, racial and climate justice, we wrote to the OECD in May, demanding that it meaningfully respond to the arguments and evidence presented by the UN human rights experts and that it commits to carrying out human rights impact assessments – including the potential of racial and gender impacts – of the ‘two pillar proposals’.

We received an unsatisfactory response from the OECD in which they insisted that they are “fully committed to UN human rights mechanisms”; “supporting gender equality” and “fighting all forms of discrimination”. Without substantiating its claim, the OECD alleged that its global corporate minimum tax would be beneficial to countries in the Global South. The OECD also alleged that because every country has the “sovereign choice” to decide whether to participate in its tax reforms it is unfair to accuse it of any kind of wrongdoing.

In August, we responded to the OECD reiterating the deleterious effects of its ‘two pillar proposals’ for countries in the Global South. Chief amongst these concerns are how its global minimum corporate tax would result in a race to the bottom, how any revenues raised would be miniscule and that the OECD has failed to counter evidence of the negative racial and gender impact of its proposals.

We also strongly raised our concerns about how undemocratic the OECD’s tax reform processes have been, repeatedly sidelining the distinct interests of countries in the Global South on numerous occasions. For instance, Global South countries have pushed for different approaches to international taxation such as unitary taxation and a higher threshold for a minimum corporate tax which would ensure a more equitable allocation of taxing rights and address inequities baked into the international financial architecture. We also highlighted examples of how the OECD has overridden the sovereignty of states especially in the Global South and used coercive tactics to ensure that compliance with its standards are inescapable.

To date, the OECD has failed to respond to our second letter, thus prompting us to make this correspondence public in accordance with universal principles of transparency and accountability.

The OECD has held stewardship of global tax reform processes for over six decades, having been handed this responsibility by a small number of powerful nations during the era of decolonisation. We have elsewhere laid bare how the establishment of tax havens, which are part and parcel of a system of international tax abuse that siphons $492 billion from tax authorities each year, were also prompted by decolonisation.

The time for this neocolonial approach to global tax governance is over. UN human rights experts were correct when they said that the UN-led process represents a “once-in-a-lifetime opportunity” to reform the international financial architecture so that it is fit for purpose and can address the polycrisis of our times – including the debt, climate, poverty and inequality crises – all of which disproportionately impact the countries of the Global South.