The Financial Action Task Force (FATF) in charge of the Recommendations on Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) has opened a consultation on the Guidance to Recommendation 25 on beneficial ownership transparency for legal arrangements (eg trusts). The Tax Justice Network has previously sent written submissions on the reform of Recommendation 25 and published a report showing the widespread use of trust registration around the world. Now, the FATF is inviting feedback on their proposed Guidance to Recommendation 25.

Our response addresses mostly the following questions (summary answers in bold, developed further in our response below):

ii. Are there other potential scenarios concerning beneficiaries that should be included in this Guidance?

Indirect beneficiaries (see more details in section 3.2.1 below).

iv. Are there other additional mechanisms available to ensure access to beneficial ownership information in the context of trusts?

Public access (see more details in section 4 below).

v. What are the suggested approaches to identify, assess, and mitigate the ML/TF risks linked with different types of legal arrangements (trusts governed under domestic law, foreign trusts administered in the country, and foreign trusts having sufficient links with the country)? What trends can be identified?

Demand registration as a precondition for trusts’ legal validity following the examples of Barbados (for purpose trusts), Czechia, France, Puerto Rico or St. Kitts (see more details in section 2 below).

vii. How can countries achieve the obligations on non-professional trustees more effectively?

Apply “constitutive effect registration”, suggesting that the trustee (as registered legal owner of the assets) will be the absolute owner and could defraud the settlor and beneficiaries, unless the trust and all details have been registered (see more details in section 2 of our response).

In conclusion, this Guidance is more comprehensive and ambitious than the actual text of Recommendation 25 which regrettably failed to implement a registry approach for trusts[1] (by requiring trusts to register their beneficial owners with a government authority). There are positive aspects mentioned by the Guidance that the Tax Justice Network has been warning[2] about for years, especially the risks of trusts’ asset protection, flexibility and lack of registration, or cases of trusts “declarative” registration (where lack of registration doesn’t affect the trust’s legal validity). The best solution in this regard is to consider as a “best practice” that trust registration should have a “constitutive effect” (where rights and legal validity start only after registration). Many countries already require registration for the trust’s validity, including Barbados (for purpose trusts), Czechia, France, Puerto Rico or St. Kitts (see the legal sources here[3]).

As for needed improvements, the Guidance should reinforce Section 5.2 on the registry approach by including as “best practice” the findings[4] that more than 120 countries already have some type of trust registration, including 65 jurisdictions which require some trusts to register their beneficial owners. More importantly, the Guidance fails to mention public access, even though some countries already offer free online public access to trusts’ beneficial owners. The Guidance should also review its language for possibly unintended meanings, as it currently appears to condone or even promote tax abuse (“tax minimisation, estate planning”) or fraud relating to creditors (“asset protection”). The Guidance should also clarify that private foundations are always legal persons subject to Recommendation 24 (and thus must follow the registry approach), even if the beneficial ownership definition that applies to these foundations resembles that of trusts, so that all parties to the foundation are registered. Finally, the Guidance should adopt as “best practices” more effective measures against discretionary trusts, expand beneficiaries to cover indirect distributions, and finally discourage complex structures by requiring that beneficial ownership rules should not apply thresholds whenever a party to the trust is a legal person.

The Tax Justice Network’s response

1. Trust registration: describe number of countries with trust registration

The Guidance Section 5.2 refers to the option of implementing the registry approach (ie trust registration with a government authority). It is relevant to include in this section, as a “best practice” the findings of the Tax Justice Network’s report[5] on trust registration: more than 120 jurisdictions already require some trusts to register with a government authority, 65 of which also require beneficial ownership information to be disclosed. In addition, while the Guidance refers to the obligation of the trustee to report information (paragraph 125), countries like Argentina have imposed that obligation on all parties to the trust.[6]

We welcome that the Guidance acknowledges that the lack of registration has many negative effects, such as not knowing how many trusts exist or determining their beneficial owners. Countries are therefore able to export their secrecy, by allowing trusts to be created according to their laws, but having no information about these trusts. Another major risk that the Guidance should include, is the risk to falsify or backdate documents, eg the trust deed or distributions, as these don’t need to be registered (as described by Australia’s tax authority[7]).

In relation to foreign law trusts with a link to a country (paragraphs 71-74), the Guidance could mention as a “best practice” that countries could expand registration triggers beyond having a local trustee. The Guidance could mention as a “best practice” the example of the EU, which requires registration when a trust acquires real estate or establishes business relations, although this should be expanded to cases where a trust has any interest in an entity or asset in the country. Another relevant example is Argentina[8], which requires trusts to be registered whenever any of its parties (not just the trustee) are located in Argentina.

The Guidance should describe as “best practice” all the countries that already have trust registration. Based on the Tax Justice Network’s Roadmap to Effective Beneficial Ownership Transparency (REBOT)[9], the Guidance should encourage countries as “best practice” to register trusts whenever they are created according to local laws, or when foreign trusts have assets, operations or parties located in the country in question.

2. Effect of registration: require constitutive effect where registration is a pre-condition for the trust’s legal validity

To make registration truly effective, especially in relation to local trusts that have foreign assets and parties, the Tax Justice Network has been advocating for a “constitutive effect”[10] for registration (where rights exist only after registration, while unregistered documents are legally worthless). The Guidance should propose as “best practice” to establish trust registration as a pre-condition for trust validity. Many countries already require registration for the trust’s validity, including Barbados (for purpose trusts), Czechia, France, Puerto Rico or St. Kitts (see the legal sources here[11]).

This way the country providing the source of law would be able to identify all its local trusts, even if all parties and assets are held abroad. In fact, many countries[12] already require all of their local trusts to be registered.

We welcome the Guidance recognising that enforcement may be impossible unless registration is a pre-condition for the trust’s validity:

“In the absence of registration requirements for express trusts and similar legal arrangements governed under a country’s law and where failure to comply with such registration requirements would lead to the failure of the trust, a country may find it difficult to establish the extent to which there is foreign use of trusts governed under its law.” (paragraph 78).

A “constitutive effect” approach would also incentivise accuracy and updating of information (addressed by the Guidance’s section 4.3 and 4.4). The effect would be that beneficiaries wouldn’t be entitled to receive a distribution, unless they are pre-registered. Likewise, an unregistered protector or trustee would be unable to make decisions, or veto measures.

This “constitutive effect” would also work to incentivise registration of non-professional trustees. The “constitutive effect” not only encourages trustees or protectors to register for them to be able to make valid decisions (such as investing in securities or purchasing assets on behalf of the trust.) It does more than that: settlors (the original owners of the assets settled into the trust) will also have the incentive to ensure that the trustee registers as “trustee” (disclosing their status as trustee, meaning as a mere “legal owner” of the trust assets).

When the trustee registers “as trustee”, the constitutive effect will have the effect of allowing the trustee to administer the trust’s assets, but also to prevent the trustee from stealing the assets (eg by disposing of them for their own benefit, against the settlor’s wishes). This protection would take place if the trustee disclosed: “I’m John Smith, I’m the trustee of trust X. I’m the legal owner of this house but as trustee of trust X. In reality this house belongs to the trust”. By contrast, if the settlor doesn’t demand that the trustee registers as “trustee”, and instead the trustee is registered as the owner of the assets without any reference to a trust (eg “I’m John Smith, the owner of this house”), then the constitutive effect would result in the law regarding the trustee as the real and absolute owner of the assets settled into the trust – allowing the trustee to keep the assets for themselves, and thus defrauding the settlor and beneficiaries. In this example, the trust deed, being unregistered, would have no legal validity. In conclusion, the constitutive effect encourages all parties to tell the truth to obtain protection of the law. The Guidance should mention as “best practice” that countries could establish “constitutive effect” for the registration of trusts.

3.1 Trust parties to be registered

3.1 Settlors

We welcome that the Guidance (paragraph 25) distinguishes between the legal settlor (a nominee) who appears on the trust deed and the economic settlor (the real but hidden settlor). As ways to identify the economic settlor the Guidance should propose as “best practice” the following. First, whenever authorities become aware of a settlor being just a nominee (legal settlor), they should ask them to reveal the identity of the real economic settlor. Second, authorities should use information on any identified nominee settlor to look for other trusts that this person may be associated with. This could reveal all other trusts where a nominee is potentially being used to hide the real settlor. Third, to detect legal settlors (nominees), the Guidance should require authorities/obliged entities to always obtain information on the transfer of assets to the trust, such as the originating account holder who transferred money to the trust, or details of the previous registered owner of any real estate settled into the trust.

3.2 Beneficiaries

3.2.1 Indirect beneficiaries

Indirect beneficiaries involve schemes where persons can avoid being identified as beneficiaries of a trust but still receive distributions, by masking these distributions as trust expenses (eg paying a person’s credit card or tuition fees as if they were real trust expenses). The Guidance fails to include the requirement to identify “indirect beneficiaries” as beneficial owners, meaning those persons who received disguised indirect distributions. The Guidance could directly refer as “best practice” to the 2022 amendments[13] to the Common Reporting Standard (CRS) on automatic exchange of information, which incorporated indirect beneficiaries:

“Indirect distributions by a trust may arise when the trust makes payments to a third party for the benefit of another person. For example, instances where a trust pays the tuition fees or repays a loan taken up by another person are to be considered indirect distributions by the trust. Indirect distributions also include cases where the trust grants a loan free of interest or at an interest rate lower than the market interest rate or at other non-arm’s length conditions. In addition, the write-off of a loan granted by a trust to its beneficiary constitutes an indirect distribution in the year the loan is written-off. In all of the above cases the Reportable Person will be person that is the beneficiary of the trust receiving the indirect distribution” (p. 94)

The Guidance could include as “best practice” that indirect beneficiaries should also include any individual with a right to, or who actively uses or enjoys, the trust assets, such as a house, yacht or private jet that is settled into the trust.

3.2.2 Discretionary beneficiaries (“Object of power”)

The Guidance effectively rewards complexity by allowing beneficiaries of discretionary trusts not to be registered or identified until the time when they receive a distribution (paragraphs 46, 90). This benefit can be exploited to prevent any registration, given that it may be impossible to find out that a distribution has taken place, especially if it refers to an indirect distribution (see above). It would make more sense to mitigate the risks associated with the complexity of discretionary trusts by requiring as “best practice” that all potential beneficiaries to be pre-identified and registered, both as a way to hold information on all potential beneficiaries and to discourage discretionary trusts altogether.

By discouraging, or directly prohibiting the existence of discretionary trusts, trusts would be treated similar to companies. Companies allow shareholders, directors and other parties to change, but these changes must be registered. As “best practice”, the same should apply to trusts to ensure authorities will always hold information on trusts’ beneficiaries. To enforce this, as proposed above, registration should be considered to have constitutive effect (meaning that rights, eg to receive a distribution) only exist upon registration. As “best practice”, any distribution to an unregistered beneficiary would be considered as a breach of the trust, somewhat equivalent to a company paying dividends to individuals who aren’t shareholders.

By the same token, another best practice is that letters of wishes or any other trust documents with instructions for the trustee should be considered as having no legal validity (and therefore being unenforceable) unless they have been registered with authorities.

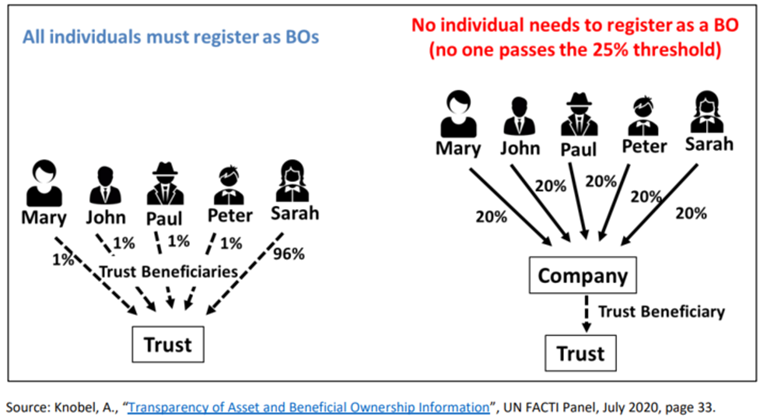

3.2.3 Complex structures: legal persons as parties to a trust result in increased secrecy

The Guidance refers to cases where a legal person acts as a party to the trust, eg a corporate trustee or beneficiary (eg paragraphs 23, 89). In such cases, the Guidance (paragraph 84) merely suggests applying the corresponding beneficial ownership rules that apply to legal persons.

As described in our paper on complex ownership structures[14], while beneficial ownership rules for trusts don’t apply thresholds, by adding an entity as a party to the trust and applying the corresponding rules for legal persons, thresholds can de facto be applied in trusts. As we had warned (and as illustrated in the next figure), this could allow the real parties to a trust (or a similar structure, like a private-interest foundation) to avoid registration.

Figure. De facto application of thresholds to trusts’ beneficial owners

This is precisely what happened in an investigation on Russian oligarchs, as described by the BBC[15]:

“The ownership of Biniatta could be structured using a Seychelles foundation with five nominee councillors ‘so as to not declare a controlling person’. This would give the appearance that no one person had control over 25% of the company, the threshold under UK law for the requirement to name a person of significant control. Biniatta followed the advice and no person of significant control was declared.”

For this reason, in case a party to the trust is a legal person, the Guidance should mention as “best practice” that beneficial owners of that legal person should be identified without applying thresholds (anyone with at least one share, voting right or right to dividends should be identified as a beneficial owner of the corporate-trust-party).

3.2.4 Same beneficial ownership definition for foundations.

We welcome that the Guidance refers to the similarities between foundations and trusts (paragraph 21). However, the Guidance should also clarify that private foundations are always legal persons subject to Recommendation 24 (and thus must follow the registry approach), even if the beneficial ownership definition that applies to these foundations resembles that of trusts, so that all parties to the foundation are registered. The Guidance should mention as “best practice” the EU anti-money laundering Directive which establishes precisely this: legal persons (including foundations) are subject to beneficial ownership registration, but the beneficial ownership definition of trusts applies to foundations..

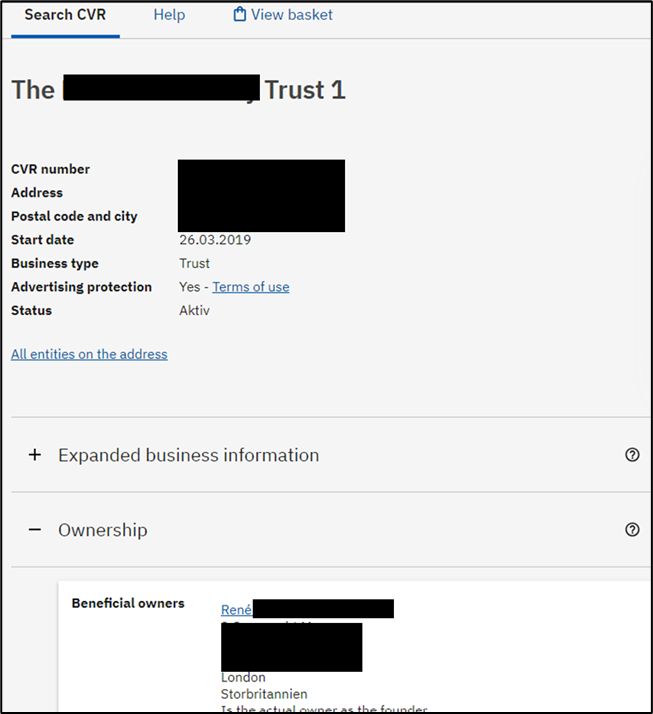

4. Access to information

The Guidance’s section on access to information (Section 5.5) refers only to access by competent authorities and by obliged entities (eg financial institutions). However, the Guidance should mention as “best practice”, or at least as an option, that there is widespread legal practice going beyond this level of access. Many countries allow direct public access to full beneficial ownership (Denmark or Ecuador), access to the parties to the trust when the trust is involved in real estate (eg Panama) or to some trust information (eg Singapore)[16]. Another option the Guidance should mention is to enable public access based on legitimate interest (eg the EU anti-money laundering directive of 2018, known as AMLD 5).

Figure. Denmark’s public registry

Figure. Ecuador’s public registry

It is not clear why the Guidance fails to mention those cases. It should include these other examples of public access alongside the current reference to more restricted access.

5. Acknowledgement of trusts’ risks

5.1 The privacy nature of trusts (ie their secrecy) makes them vulnerable to misuse.

We welcome the fact that the Guidance describes that the secrecy surrounding trusts makes them vulnerable to misuse (paragraph 52).

5.2 Trusts’ flexibility and asset protection are abused in many money laundering cases.

We welcome the fact that the Guidance acknowledges (paragraphs 57-58) that trusts’ flexibility and asset protection can be abused for money laundering and other cases. The Guidance explicitly mentions the ability to shield assets from creditors (what we call the “ownerless limbo”[17]), the possibility to change names of beneficiaries, or for the settlor to retain control. However, the Guidance should also mention the worst risks of all: the possibility of the trustee to have “discretion”. After all, all legal vehicles allow changes. The shareholders and directors of a company can also change over time. The main difference is that in a discretionary trust the change can happen based purely at the trustee’s discretion without anyone being alerted (without even needing to amend the trust deed).

For this reason, the Guidance could propose as “best practice” that discretionary trusts should be outlawed (see section 3.2.2 above). Changes should only become enforceable and legally valid only upon registering the new beneficiaries or trustees with government authorities.

5.3 Abusive trust regimes

We welcome that the Guidance (paragraphs 61-62) also describes other abusive features that we have written about in our review of some of the most abusive trust jurisdictions[18]. For instance, the limitation of the time to initiate anti-fraud actions, the application of criminal burden of proof (“beyond reasonable doubt”), as well as the non-recognition of foreign laws and judgements. In addition to warning about these features, the Guidance could propose as “best practice” that these jurisdictions offering abusive legal frameworks should be considered high-risk by countries (eg add them to the national tax haven list). Alternatively, countries could disregard or invalidate any trust created according to the laws of these jurisdictions.

6. Understatement of trusts’ abusive purposes

The terminology used in the Guidance (eg page 3 and Annex) often appears to resemble that of enablers rather than an international organisation fighting anti-money laundering, especially the euphemisms for tax abuse practices (some of which would constitute a predicate offense for money laundering). The most acute cases of these are discussed below.

6.1 Describing trusts as a mere “relationship” (as opposed to an “entity”) supports trusts’ secrecy

The Guidance reads “[i]t is important to bear in mind that trusts are not a type of legal entity or corporate vehicle but a relationship between the principal parties to such arrangement.” (p. 3). However, unlike the relationships between parents and children, or parties to a commercial contract, eg to paint a house, this “trust relationship” has effects identical to a legal entity – which the Guidance acknowledges. Trusts are usually assigned a tax identification number for the trust (like any company) to pay taxes, and trusts (as an entity) can open bank accounts. Very importantly from a justice perspective, the assets held in the trust are separate from the parties to the trust (settlor, trustee, beneficiary) and in principle cannot be reached by their creditors, even if they are held under the trustee’s name. This is similar to a company benefiting from separation of assets and the shareholder benefitting from limited liability. Even an EU Court of Justice ruling in 2017 described that trusts are in essence an “entity”.[19]

For this reason, the Guidance should warn that although trusts are often viewed as relationships or legal arrangements (as opposed to legal persons), the legal effects of their creation (eg separation of assets, and their complex control and benefit structures) can be similar to, or even riskier than those of, legal persons.

6.2 “Asset protection”, “tax planning and optimisation”, “estate planning”

The Guidance describes as “purposes” for trusts (page 4 and Annex) a mix of legitimate and illegitimate goals. It could be true that most trusts engage in legal and legitimate endeavours, although the lack of registration prevents us from knowing how many trusts exist in the world and to assess their legitimacy. Trusts have been abused[20] many times to engage in tax evasion[21] and avoidance as well as to defraud creditors[22] or circumvent sanctions[23] and prevent asset recovery (using the “asset protection” features of trusts). However, the Guidance uses terminology used by professional enablers[24], such as “tax planning, estate planning”, that have served as euphemisms for tax abuses and fraud. “Asset protection” is defended by the Guidance as a way to protect assets against outsiders, although many times it is abused to defraud creditors (including former spouses in divorce proceedings) because trusts’ asset protection can shield assets beyond the protection of private property or even beyond the protection of limited liability that applies to most legal persons.

For this reason, instead of referring to “tax and estate planning” or “asset protection”, the Guidance should refer to, or at least also mention, the risks of tax evasion, tax avoidance and fraud against legitimate creditors.

6.3 Charitable trusts

We welcome the Guidance’s Box 2.1 on charitable trusts that warns that,

“while pursuing public good objectives sets charitable trusts (and similar legal arrangements such as Waqf) apart from other types of trusts, it is not possible to conclude in absolute terms that they present a lower risk. Indeed, some of their features may create an enhanced risk of misuse for ML/TF.”

We believe that this is the right approach, rather than to follow positions mentioned in the public call of November 27 which suggested that charitable trusts present less risks or that there should be different registration requirements based on the types of trusts. We welcome the Guidance’s warning that charitable trusts can also be abused and should not be subject to any less transparency requirements.

To support this box, there are two warnings that the Guidance could add. For instance, the largest tax evasion case against an individual in the US involved the tax evader renaming his trusts as “charitable” to confuse authorities on the real purpose of those trusts[25]. In other cases, charitable trusts or foundations may include many legitimate beneficiaries (eg the Red Cross or Unicef) to prove that they are “charitable” although no distribution in favour of these legitimate beneficiaries actually takes place, as happened in the case of Northern Rock bank’s trust in favour of Down Syndrome North East[26]. Instead, the capital is concentrated in the trust, undistributed, or de facto distributions are made in form of indirect distributions or salaries.

[1] https://taxjustice.net/2022/07/28/reforms-to-fatf-recommendation-25-should-reflect-fact-not-fiction/

[2] https://www.taxjustice.net/wp-content/uploads/2017/02/Trusts-Weapons-of-Mass-Injustice-Final-12-FEB-2017.pdf

[3] See page 7 in: https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[4] https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[5] https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[6] Art. 1.c of Resolution AFIP 3312/2012 as amended: https://servicios.infoleg.gob.ar/infolegInternet/anexos/195000-199999/196461/texact.htm

[7] https://www.ato.gov.au/about-ato/research-and-statistics/in-detail/general-research/current-issues-with-trusts-and-the-tax-system/

[8] Art. 1.c of Resolution AFIP 3312/2012 as amended: https://servicios.infoleg.gob.ar/infolegInternet/anexos/195000-199999/196461/texact.htm

[9] https://taxjustice.net/2023/02/07/roadmap-to-effective-beneficial-ownership-transparency-rebot/

[10] https://www.taxjustice.net/wp-content/uploads/2017/02/Trusts-Weapons-of-Mass-Injustice-Final-12-FEB-2017.pdf

[11] See page 7 in: https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[12] https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[13] https://www.oecd.org/tax/exchange-of-tax-information/crypto-asset-reporting-framework-and-amendments-to-the-common-reporting-standard.pdf

[14] https://taxjustice.net/wp-content/uploads/2022/02/Complex-ownership-chains-Reduced-Andres-Knobel-MB-AK.pdf

[15] https://www.bbc.co.uk/news/uk-67276289

[16] See more details on pages 25-31 here: https://taxjustice.net/wp-content/uploads/2022/07/Trusts-FATF-R-25-1.pdf

[17] https://www.taxjustice.net/wp-content/uploads/2017/02/Trusts-Weapons-of-Mass-Injustice-Final-12-FEB-2017.pdf

[18] https://www.taxjustice.net/wp-content/uploads/2017/02/Trusts-Weapons-of-Mass-Injustice-Final-12-FEB-2017.pdf

[19] ECJ 646-15, where the ruling described: “That concept of ‘other legal persons’ extends to an entity which, under national law, possesses rights and obligations that enable it to act in its own right within the legal order concerned, notwithstanding the absence of a particular legal form, and which is profit-making. In this case… under the national law concerned, the assets placed in trust form a separate fund of property, distinct from the property of the trustees, and that the trustees have the right and the obligation to manage those assets and to dispose of them in accordance with the conditions laid down in the trust instrument and in national law. (…) That being the case, such a trust should be considered to be an entity which, under national law, possesses rights and obligations that enable it to act as such within the legal order concerned.”

[20] https://www.taxjustice.net/wp-content/uploads/2017/02/Trusts-Weapons-of-Mass-Injustice-Final-12-FEB-2017.pdf

[21] https://taxjustice.net/2020/08/13/judge-ruling-you-are-no-mother-teresa-and-no-one-goes-to-cayman-for-philanthropic-reasons/

[22] https://taxjustice.net/2017/11/08/enough-evidence-trusts-states-actions/

[23] https://taxjustice.net/2022/03/31/no-trusts-are-not-impenetrable-shields-for-oligarchs-assets-here-is-how-to-pierce-them/

[24] https://www.oecd.org/tax/crime/ending-the-shell-game-cracking-down-on-the-professionals-who-enable-tax-and-white-collar-crime.pdf

[25] https://www.justice.gov/opa/press-release/file/1327921/download

[26] https://www.theguardian.com/business/2007/nov/28/northernrock.subprimecrisis

The author

Related articles

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

UN Tax Convention: Summary of the Tax Justice Network’s stakeholder input after the Fourth Session of negotiations

After Nairobi and ahead of New York: Updates to our UN Tax Convention resources and our database of positions

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

")