Published:

14 December 2022Reading time:

16 minThe Tax Justice Network’s proposed amendments to the open consultation on FATF Recommendations 25 on beneficial ownership for legal arrangements published in full below.

The Financial Action Task Force (FATF) in charge of the Recommendations on Anti-Money Laundering and Combating the Financing of Terrorism (AML/CFT) has opened a consultation on the reform of Recommendation 25 on beneficial ownership for legal arrangements such as trusts.

We have sent written submissions and participated in calls on Recommendation 24 and more recently on Recommendation 25 (on beneficial ownership for trusts and other legal arrangements). Now, the FATF is inviting feedback on their proposed amendments to the text of Recommendation 25.

The primary question the FATF is asking in its consultation is, “Are FATF proposals adequate to mitigate the risk of misuse of legal arrangements and to ensure access to BO information?”

To which we unfortunately answer, “No”.

The FATF reformed Recommendation 24 in March 2022 to require beneficial ownership registration from legal persons because the old requirements, which allowed, among others, a company to collect and keep beneficial ownership information to itself and only make the information available to authorities on request, were found to not be sufficient. In a dangerous undermining of its own conclusions, the FATF is now suggesting that when it comes to trusts, it is sufficient to ask the trust (or rather the trustee) to keep this information and only make it available on request. In other words, a transparency system that failed for companies is now being endorsed for trusts, which are even more secretive and complex than companies.

To answer the FATF’s third question, “What is the expected impact of the proposals on legitimate activity? In particular, what are the challenges for implementation?”, the answer is “Fortunately, there should be little technical challenge. Only political opposition.”

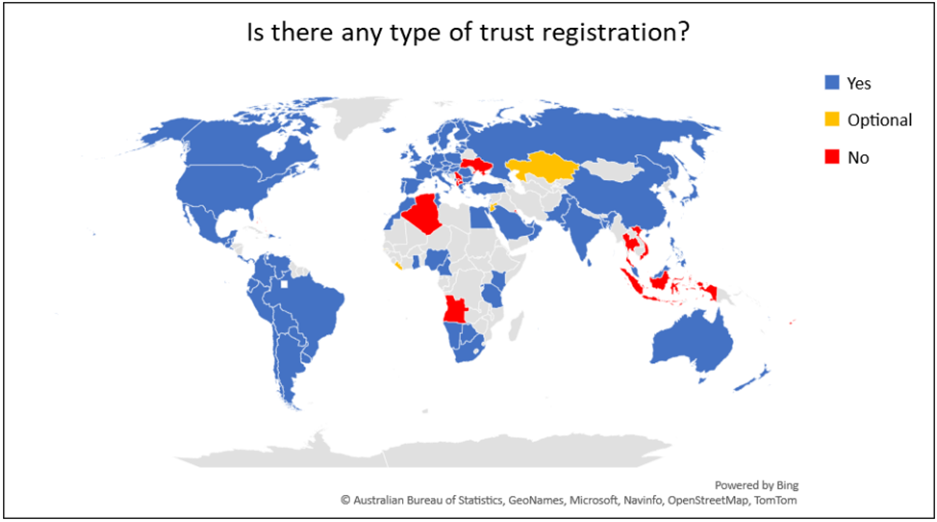

The only adequate measure is to establish central registries of beneficial ownership and to make information publicly available. As our paper on Trust Registration around the World shows, more than 120 countries already require registration for some types of trusts, proving that most countries already have the legal and technical infrastructure to require trusts to register.

You may find below our proposals to reform Recommendation 25. And further below, you may find our proposed amendments to incorporate these proposals into the text of the Recommendation. If you have any comments or feedback, please write to Andres Knobel at [email protected]

Proposals to reform Recommendation 25

1) Trusts should be required to register their beneficial owners with a government authority, just as legal persons are required to do so under Recommendation 24.

At the very least, the changes introduced by the March 2022 Reform to Recommendation 24 on beneficial ownership transparency for legal persons should also apply to trusts, especially the requirement to file beneficial ownership information with a government authority.

The main argument in favour of this equal treatment for any type of legal vehicle, be it a legal person or a trust, is two-fold. First, trusts are a type of complex legal vehicle subject to many types of abuses (as most recently highlighted in the Pandora Papers leak).Trusts should be subject to even more transparency (or at least as much transparency) as legal persons, not less. Second, private foundations share the same control structure and goals as trusts, and since they are considered legal persons, they are already subject to Recommendation 24, so there’s no reason why trusts should be considered special or different.

As described in our report on Trust Registration around the World, more than 120 jurisdictions already require some types of trusts to register with government authorities, including 65 jurisdictions which already require beneficial ownership information to be registered for some types of trusts. This proves that most countries already have the legal infrastructure to require trusts to register and to file beneficial ownership information.

While countries should be allowed to have as many local registries as they need (eg for federal purposes) all information should be centralised in a digital platform. This central platform should contain information on beneficial ownership and for all types of legal vehicles, and ideally also legal ownership information to avoid inconsistency problems. This way, it will be possible to know all the legal vehicles related to a beneficial owner, no matter which district or province a vehicle was incorporated in. Likewise, by having information on all legal vehicles as well as on legal and beneficial ownership in the same place, it will be possible to ensure consistency. For example, to prevent cases where the beneficial ownership register states that company A is owned by company B which in turn is owned by John, but the shareholder register states that company A is owned by trust X.

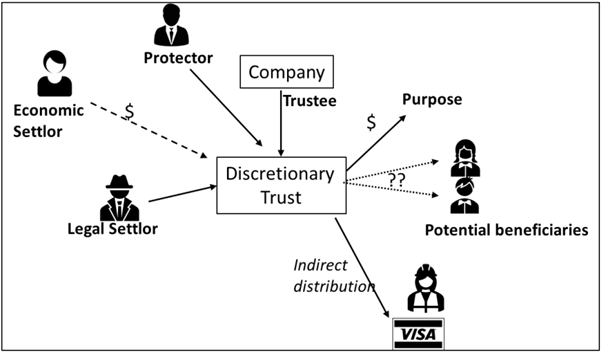

2) The beneficial ownership definition of trusts should include all parties, including protectors, purposes and indirect beneficiaries

Recommendation 25 only requires the identification of the settlor, trustee and beneficiaries. The Interpretative Note extends this to the protector and classes of beneficiaries, as well as “discretionary beneficiaries” (called object of a power) as well as any other individual with effective control over the trust.

The definition should be expanded to cover also:

- Legal and economic settlors (the legal settlor is the nominee who appears on the trust deed, while the economic settlor is the real owner of the assets settled into the trust)

- Purposes (in the case of purpose trusts)

- Indirect beneficiaries (as proposed by the OECD’s improvements to the Common Reporting Standard), which cover individuals or entities that receive indirect distributions, such as the payment of tuition fees or credit card expenses

- Any individual with any benefit from the trust assets or income (eg someone who uses any of the trust assets, such as a house or yacht)

Trusts involve very complex structures so all parties to the trust should be identified before they are allowed to control or benefit from the trust:

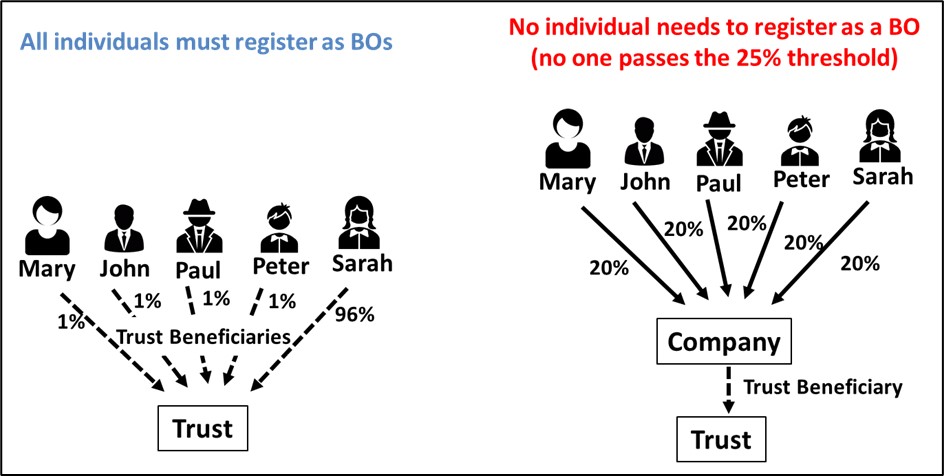

3) When legal persons are parties to the trust, no threshold should apply

The FATF imposes no thresholds on the beneficial ownership definition when it comes to trusts. However, the proposed reform would make it explicit that when a legal person is a party to the trust, then the beneficial owner of the legal person should be identified as a beneficial owner of the trust. Given that thresholds are applied for identifying the beneficial owners of legal persons, this allows individuals to artificially add thresholds into the beneficial ownership definition of trusts by interposing legal entities as parties to the trust. The result of this is that individuals with interests in the legal person below a threshold may remain hidden and unidentified, despite the fact that in the case of trusts all parties should be identified. This is illustrated by the next figure.

The solution is to require that, when a party to the trust is a legal person, then the beneficial owners of the legal person should be identified without applying any thresholds. (This should ideally apply to all legal persons, but especially when a legal person is a party to a trust).

4) Require beneficial ownership registration for trusts in any country where the trust has a link

Just as Recommendation 24 requires all locally incorporated legal persons to register their beneficial owners, so should Recommendation 25 cover all trusts created according to or governed by the laws of a jurisdiction.

While triggering registration (or availability of information) whenever a trustee is resident in the jurisdiction is important, this should be expanded to trigger registration whenever any party is resident in the jurisdiction as required by countries such as Argentina or France.

Lastly, registration (or at least availability of information) should apply to any trust with operations or assets in the jurisdiction.

5) Prohibit discretionary trusts

Discretionary trusts allow individuals to pretend on paper not to own, benefit or control assets in order to avoid creditors, asset recovery or transparency. As described by the paper “Beneficial Ownership Registration for Trusts – Gaps and Loopholes” from the Network of Experts on Beneficial Ownership Transparency (NEBOT):

“Trusts focusing on asset protection usually involve a discretionary component, where the trustee is given discretion (on paper) to decide on trust distributions. This means that the trustee may be able to choose when a distribution will be made, how much will be given, but more importantly, if a distribution will be made at all.

“Asset protection trusts use trustee’s discretion, rather than establishing distributions beforehand e.g. “distribute 50% each year to each of the two beneficiaries” to exploit circumstances…To avoid paying such tax, the beneficiary may choose to postpone distributions until a year with reported losses which could be offset, so as not to pay any personal income tax. An even more extreme is a situation where an insolvent beneficiary owes money to creditors… To prevent this, discretionary trusts usually include provisions to prevent distributions to indebted beneficiaries.

“Discretionary trusts also create secrecy. Being the beneficiary of a discretionary trust, a beneficiary could claim not to be a beneficial owner because they are merely ‘potential’ beneficiaries and may end up not receiving anything at all…”

The FATF should prohibit discretionary trusts or at least consider them to be high risk for secrecy, sanction avoidance and prevention of asset recovery.

6) Provide public access

Public access to legal and beneficial ownership information should become the norm. As described by our report on Trust Registration around the World, public access to trusts’ beneficial owners is available in 12 EU countries as well as in Ecuador. Other countries including Dominican Republic, Panama, Oman, Seychelles, Singapore and the US offer access public access to some trust information in certain circumstances.

Ecuador

Panama

Singapore

The US

Proposals to amend the Glossary

Given that the consultation also includes a proposal to amend the Glossary with the definition of beneficial owner, proposed changes should include:

7) Include all elements in the beneficial ownership definition

As we have proposed in the Roadmap to Effective Beneficial Ownership Transparency (REBOT) or explained in this blog, the beneficial ownership definition should include all elements: ownership, control or benefits. As described by the State of Play of Beneficial Ownership Registration in 2022 many countries are already establishing all three elements in the beneficial ownership definition in their laws, including with no threshold or low thresholds.

8) Measures against complex ownership structures

As we have explained in our report on Complex ownership structures, the more complex a structure (eg many layers up to the beneficial owner, foreign entities from tax havens, etc), the harder it will be for authorities to identify or to verify the beneficial owner. In most cases, creating complexity comes at little cost for the individual while transferring the burden and the cost to authorities. It is necessary to revert the formula, regulating or even prohibiting complex ownership structures.

Proposed amendments to FATF Recommendation 25 and the Glossary

Here are our proposed amendments to the Recommendation’s text to incorporate the above proposals.

The text that appears below in red are changes the FATF is proposing to make. Text that appears in bold are changes that we are proposing should be made. Text that is striked-through is text that is proposed for deletion.

Recommendation 25. Transparency and beneficial ownership of legal arrangements

Countries should assess the risks of take measures to prevent the misuse of legal arrangements for money laundering or terrorist financing and take measures to prevent their misuse. In particular, countries should ensure that there is adequate, accurate and up-to-date timely information on express trusts and other similar legal arrangements, including information on all the parties to the trust the settlor(s), trustee(s) and beneficiary(ies), that can be obtained or accessed in a timely fashion efficiently and in a timely manner by competent authorities. Countries should consider measures to facilitateing access to beneficial ownership and control information by financial institutions and DNFBPs undertaking the requirements set out in Recommendations 10 and 22.

Interpretive Note to Recommendation 25 (Transparency and Beneficial Ownership of Legal Arrangements)

1. Countries should require trustees of any express trust governed under their law, and persons holding an equivalent position in a similar legal arrangement, that are residents in their country or that administer any express trusts or similar legal arrangements in their country, to obtain and hold adequate, accurate and current up-to-date beneficial ownership information[1] regarding the trust or other similar legal arrangements. This should include information on the identity of: (i) the economic and legal settlor(s); (ii), the trustee(s); (iii), the protector(s) (if any); (iv), the each direct or indirect beneficiaryies or, where applicable, the class of beneficiaries[2] or objects of a power; (v) purposes (if any), and (vi), any other natural person(s) exercising ultimate effective control over or benefitting from the assets or income of the trust. For a similar legal arrangement, this should include persons holding equivalent positions.

Where the parties to the trusts or other similar legal arrangements are legal persons or arrangements, countries should require trustees and persons holding an equivalent position in a similar legal arrangement to also obtain and hold adequate, accurate, and up-to-date basic and beneficial ownership information of the legal persons or arrangements without applying thresholds. Countries should also require trustees and persons holding an equivalent position in a similar legal arrangement that are residents in their country or of trusts administered in their country of any trust governed under their law to hold basic information on other regulated agents of, and service providers to, the trust and similar legal arrangements, including investment advisors or managers, accountants, and tax advisors.

1*. Countries with express trusts and other similar legal arrangements governed under their law should have mechanisms that:

(a) identify the different types, forms and basic features of express trusts and/or other similar legal arrangements.

(b) identify and describe the processes for: (i) the setting up of those legal arrangements; and (ii) the obtaining of basic[3] and beneficial ownership information;

(c) make the above information referred to in (a) and (b) publicly available.

1**. Countries should establish public access via central registries as well as other sources described below to beneficial ownership information of assess the money laundering and terrorist financing risks associated with different types of trusts and other similar legal arrangements:

(a) governed under their law;

(b) which are administered in their country or for which the trustee or equivalent resides in their country;

(c) which have a trust party, e.g. settlor, protector, beneficiary or purpose located in the country,

(d) which have registrable or other relevant assets (e.g. real estate, bank accounts, vehicles, etc) or operations (e.g. provision of goods or services) in the country, and

(e) types of foreign legal arrangements that have sufficient links[4] with their country

and take appropriate steps to manage and mitigate the risks that they identify .

2. All cCountries should take measures to ensure that trustees or persons holding equivalent positions in similar legal arrangements disclose their status to financial institutions and DNFBPs when, in their function, as a trustee, forming a business relationship or carrying out an occasional transaction above the threshold. Trustees or persons holding equivalent positions in similar legal arrangements should cooperate to the fullest extent possible with, and not be prevented by law or enforceable means from providing, competent authorities with any necessary information relating to the trust or other similar legal arrangements[6]. Countries should also ensure that trustees or persons holding equivalent positions in similar legal arrangements should not be prevented by law or enforceable means from; or from providing financial institutions and DNFBPs, upon request, with information on the beneficial ownership and the assets of the trust or legal arrangement to be held or managed under the terms of the business relationship.

3. In order to ensure that adequate, accurate and up-to-date information on the basic and beneficial ownership of the trustsor other similar legal arrangements, trustees and trust assets, is accessible efficiently and in a timely manner by competent authorities, other than trustees or persons holding an equivalent position in a similar legal arrangement, on the basis of risk, context and materiality, countries should consider use ing any all of the following Countries are encouraged to ensure that other relevant authorities, persons and entities hold information on all trusts with which they have a relationship. Potential sources of information as necessary on trusts, trustees, and trust assets are:

(a) Registries (e.g. a central registry of trusts or trust assets), or asset registries for land, property, vehicles, shares or other assets

(a) A public authority or body holding information on the beneficial ownership of trusts or other similar arrangements (e.g. in a central registry of trusts; or in asset registries for land, property, vehicles, shares or other assets that hold information on the beneficial ownership of trusts and other similar legal arrangements which own such assets). Information need not be held by a single body only.[7]

(b) Other competent authorities that hold or obtain information on trusts/similar legal arrangements and trustees/their equivalents (e.g. tax authorities which collect information on assets and income relating to trusts and other similar legal arrangements).

(c) Other agents andor service providers including trust and company service providers, to the trust, including investment advisors or managers, accountants, or lawyers, or financial institutions, or trust and company service providers.

3* Countries should have mechanisms that ensure that information on trusts and other similar legal arrangements, including information provided in accordance with paragraphs 2 and 3, is adequate, accurate and up-to-date[8]. In the context of legal arrangements:

Adequate information is information that is sufficient to identify the natural persons who are the beneficial owner(s), and their role in the trust[9] .

Accurate information is information, which has been verified to confirm its accuracy by verifying the identity and status of the beneficial owner using reliable documents, data or information. The extent of verification measures may vary according to the specific level of risk.

Up-to-date information is information which is as current and up-to-date as possible, and is updated within a reasonable period following any change.

4. Countries should ensure that Ccompetent authorities, and in particular law enforcement authorities and FIUs, should have all the powers necessary to obtain timely access to the information held by trustees, persons holding equivalent positions in similar legal arrangements, and other parties, in particular information held by financial institutions and DNFBPs on: (a) the basic and beneficial ownership of the legal arrangement; (b) the residence of the trustees and their equivalents; and (c) any assets held or managed by the financial institution or DNFBP, in relation to any trustees or their equivalents with which they have a business relationship, or for which they undertake an occasional transaction.

5. Professional tTrustees and persons holding equivalent positions in similar legal arrangements should be required to maintain the information referred to in paragraph 1 for at least five years after their involvement with the trust or similar legal arrangement ceases. Countries are encouraged to require non-professional trustees and the other authorities, persons and entities mentioned in paragraph 3 above to maintain the information for at least five years.

6. Countries should require that any information held pursuant to paragraph 1 above should be kept accurate and be as current andup-to-date as possible, and the information should be updated within a reasonable period following any change. No direct or indirect distribution should be made unless the beneficiary and its beneficial owners has already been registered in the central registry.

7. Countries should consider establish measures to facilitate ensure access to any trust information on trusts that is held by the other authorities, persons and entities referred to in paragraph 3, by financial institutions and DNFBPs undertaking the requirements set out in Recommendations 10 and 22 as well as by civil society organisations, investigative journalists and the public in general.

8. In the context of the Recommendation, countries are not required to give legal recognition to trusts but should prohibit discretionary trusts and disregard any provision which gives discretion to a trustee or any other party on who is to be considered a beneficiary or receive a direct or indirect distribution. Countries need not include the requirements of paragraphs 1, 2, 5, and 6 and 11 in legislation, provided that appropriate obligations to such effect exist for trustees (e.g. through common law or case law).

[Other Legal Arrangements

9. As regards other types of legal arrangement with a similar structure or function, countries should take similar measures to those required for trusts, with a view to achieving similar levels of transparency. At a minimum, countries should ensure that information similar to that specified above in respect of trust should be recorded and kept accurate and current, and that such information is accessible in a timely way by competent authorities.]

International Cooperation

10. Countries should rapidly, constructively and effectively provide international cooperation in relation to information, including beneficial ownership information, on trusts and other legal arrangements on the basis set out in Recommendations 37 and 40. This should include (a) facilitating access by foreign competent authorities to any information held by registries or other domestic authorities; (b) exchanging domestically available information on the trusts or other legal arrangement; and (c) using their competent authorities’ powers, in accordance with domestic law, in order to obtain beneficial ownership information on behalf of foreign counterparts. Consistent with Recommendations 37 and 40, countries should not place unduly restrictive conditions on the exchange of information or assistance e.g., refuse a request on the grounds that it involves a fiscal, including tax, matters, bank secrecy, etc. In order to facilitate rapid, constructive and effective international cooperation, where possible, countries should designate and make publicly known the agency(ies) responsible for responding to all international requests for BO information, consistent with countries’ approach to access to beneficial ownership information. To this end, countries should consider keeping information held or obtained for the purpose of identifying beneficial ownership in a readily accessible manner.

Liability and Sanctions

11. Countries should ensure that there are clear responsibilities to comply with the requirements in this Interpretative Note; and that trustees or persons holding equivalent positions in similar legal arrangements are either legally liable for any failure to perform the duties relevant to meeting the obligations in paragraphs 1, 2, 5 and 6 and (where applicable) 5; or that there are effective, proportionate and dissuasive sanctions, whether criminal, civil or administrative, for failing to comply.[10] Countries should ensure that there are effective, proportionate and dissuasive sanctions, whether criminal, civil or administrative, for failing to grant to competent authorities timely access to information regarding the trust referred to in paragraphs 1 and 5.

Recommendation 25. Glossary

Amendments to the Glossary here: Glossary – Proposals to reform Recommendation 25.

[1]Beneficial ownership information for legal arrangements is the information referred to in the interpretive note to Recommendation 10, paragraph 5(b)(ii).

[2] Where there are no ascertainable beneficiaries at the time of setting up the trust, the trustee should obtain and hold information on the class of beneficiaries and its characteristics, or object of a power. Following a risk-based approach, countries may decide that it is not necessary to identify the individual beneficiaries of certain charitable or statutory permitted non-charitable trusts.

[3] In relation to a legal arrangement, basic information means the identifier of the legal arrangement trust (e.g. the name, the unique identifier such as a tax identification number or equivalent, where this exists), the trust deed (or equivalent), the residence of the trustee/equivalent or of the place from where the legal arrangement is administered.

[4] Countries may determine what is considered a sufficient link on the basis of risk. Examples of sufficiency tests may include, but are not limited to, when the trust/similar legal arrangement or a trustee or a person holding an equivalent position in a similar legal arrangement has significant and ongoing business relations with financial institutions or DNFBPs, has significant real estate/other local investment, or is a tax resident, in the country.

[5] This could be done through national and/or supranational measures. These could include requiring beneficial ownership information on some types of foreign legal arrangements to be held as set out under paragraph 3.

[6] Domestic competent authorities or the relevant competent authorities of another country pursuant to an appropriate international cooperation request.

[7] A body could record beneficial ownership information alongside other information (e.g. tax information), or the source of information could take the form of multiple registries (e.g. for provinces or districts, for sectors, or for specific types of legal arrangements), or of a private body entrusted with this task by the public authority.

[8] For beneficiary(ies) of trusts/similar legal arrangement that are designated by characteristics or by class, trustees/equivalent are not expected to obtain adequate and accurate information until the person becomes entitled as beneficiary at the time of the payout or when the beneficiary intends to exercise vested rights.

[9] Economic and legal Settlor(s), trustee(s), protector(s) (if any), direct or indirect beneficiary(ies) or class of beneficiaries, purposes and any other person exercising ultimate effective control over the trusts or who benefits or could benefit from any of the trust assets or income. For a similar legal arrangement, this should include persons holding equivalent positions. Where the trustee and any other party to the legal arrangement is a legal person, the beneficial owner of that legal person should be identified.

[10] This does not affect the requirements for effective, proportionate, and dissuasive sanctions for failure to comply with requirements elsewhere in the Recommendations.

The author

Related articles

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Fiscal hell or mirage? What Spain’s wage debate gets wrong

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

What we learned from three years of conversations on poverty beyond growth

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026