The Financial Action Task Force (FATF) is in the process of reforming Recommendation 25 on beneficial ownership transparency of trusts and other legal arrangements. The Tax Justice Network is publishing this report which explains the risks created by trusts and why these risks justify the call for increased transparency. The call for trust registration is supported by the findings from the 2022 edition of the Tax Justice Network’s Financial Secrecy Index which showed that more than 120 countries already require some type of trust registration, including 65 countries which require some type of beneficial ownership registration.

The Financial Action Task Force (FATF) is the inter-governmental body that establishes and assess compliance with Recommendations on anti-money laundering (AML) and the financing of terrorism. The organisation is in the process of reforming beneficial ownership transparency requirements. In March 2022, the FATF approved the reform of Recommendation 24 on beneficial ownership transparency for legal persons such as companies and foundations. The main improvement was the requirement for countries to set up beneficial ownership registries (or equally efficient alternative mechanisms). Although the FATF could have been much more ambitious in its reform – especially in terms of public access to beneficial ownership information or lowering thresholds used in the beneficial ownership definition – requiring a government authority to collect beneficial ownership data is a major achievement, especially for putting pressure on laggards including Switzerland and China. However, requiring beneficial ownership registration for legal persons is hardly “radical”. It’s quite mainstream actually. The Tax Justice Network found that by April 2020, more than 80 jurisdictions had already approved laws requiring beneficial ownership information to be filed with a government authority. By 2022, this number was closer to 90 jurisdictions including the recent approval of the Corporate Transparency Act in the US in early 2021.

In July 2022, the FATF started the process to reform Recommendation 25. It opened a consultation and published a white paper but gave little indication that “trust registration” will become part of Recommendation 25.

The problem with trusts

As described in the Tax Justice Network’s brief on the role of trusts in the Pandora Papers, trusts create three specific secrecy risks and one asset protection risk.

Secrecy risk 1: Trusts do not need to register to have legal validity

In many countries trusts don’t need to register with an authority to enjoy all the benefits conferred by the law. This means that governments do not know how many trusts exist in the world, how much they hold in assets or who is benefitting from them. Instead of this self-imposed secrecy on trusts, countries could follow the examples of Barbados (for purpose trusts), Czechia, France, Puerto Rico or St. Kitts where trusts must be registered to be legally valid.

Secrecy risk 2: Trusts can use murky roles and numerous parties to obfuscate control and benefit

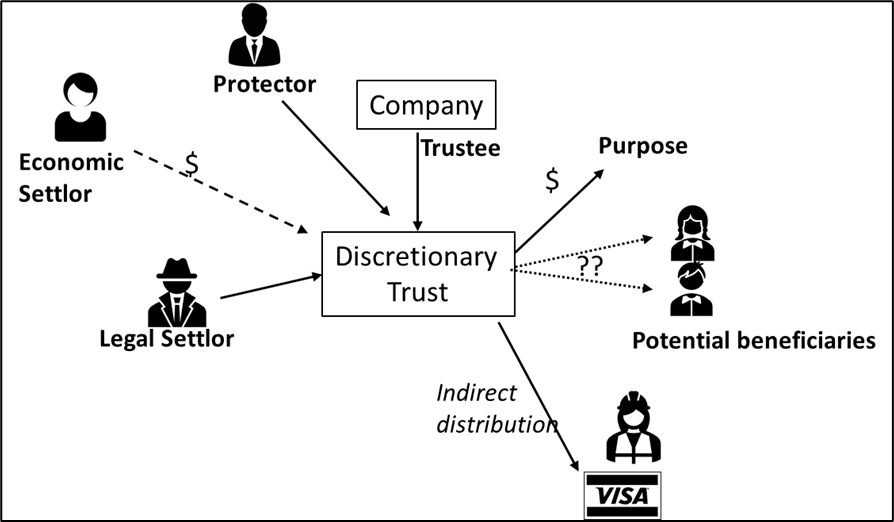

The classic example of a trust, where a parent (settlor) transfers assets to their sibling or lawyer (trustee) to manage the assets in favour of their spouse and children (beneficiaries), has a clear and straightforward delineation of roles and relationships. Modern trusts, however, can utilise a wide variety of increasingly complex and murky roles and relationships so as to completely obfuscate who has control or benefit over the assets. The reality of modern trusts is far more complex and hazardous than the fictional example often touted.

Secrecy risk 3: Trusts are often used in complex structures that create hurdles for authorities

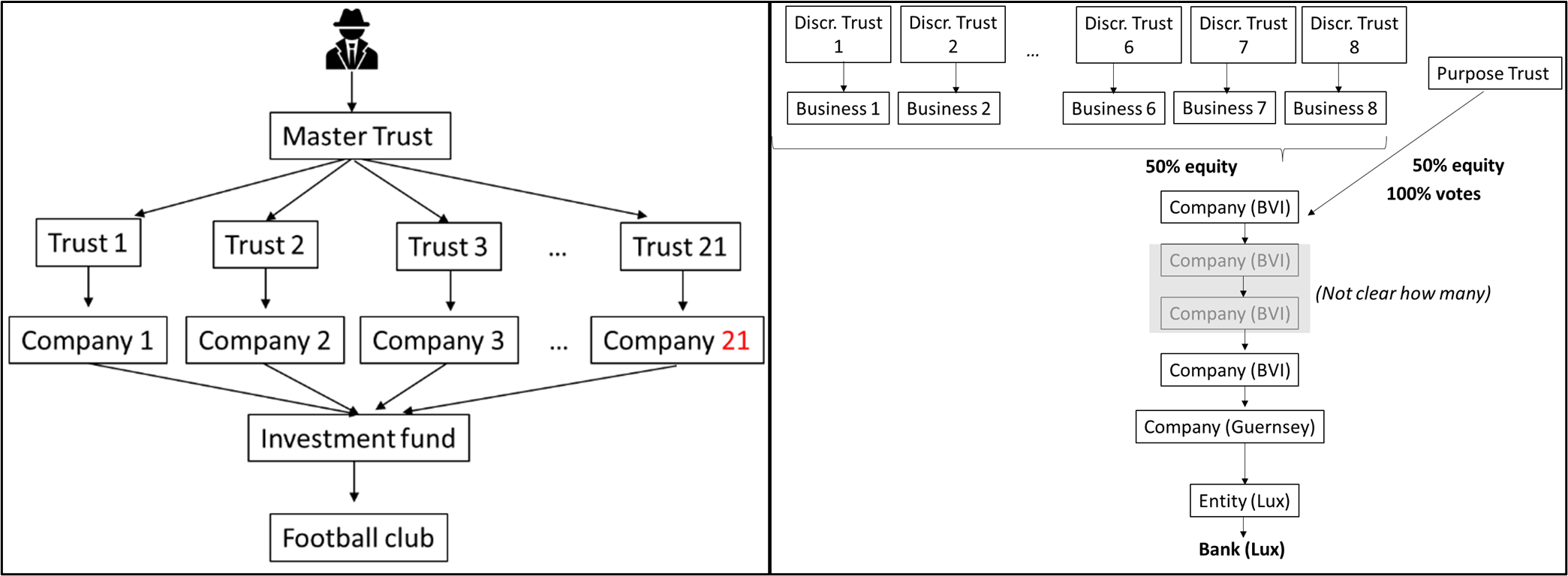

The combination of trusts and legal persons in complex chains can intensify secrecy. Even a two-layer chain involving one trust and one legal person can create impenetrable secrecy. The main problem occurs when countries’ beneficial ownership definitions are too limited to allow transparency on both layers in the chain.

Asset risk: Trusts shield assets against authorities and creditors

As explained in our paper “Trusts: Weapons of Mass Injustice?”, the subsequent “Response to the critics”, and many other blog posts, trusts have been abused to allow individuals to shield their assets when accused or found guilty of embezzlement, defrauding creditors, defrauding a spouse upon divorce, avoidance of sanctions, money laundering, murder and sexual abuse against a minor.

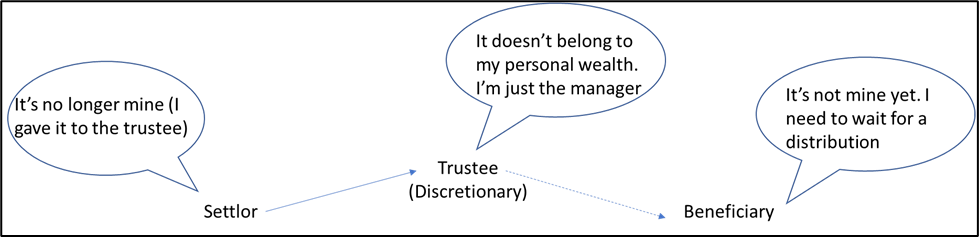

As the image below demonstrates, trusts can put assets in an apparent “ownerless limbo” where – on paper – no one owns the assets when it is convenient to not own the assets (eg when the personal creditors of the settlor, the trustee or the beneficiary come knocking). Of course, all parties can still conveniently use and enjoy the assets when no one is looking.

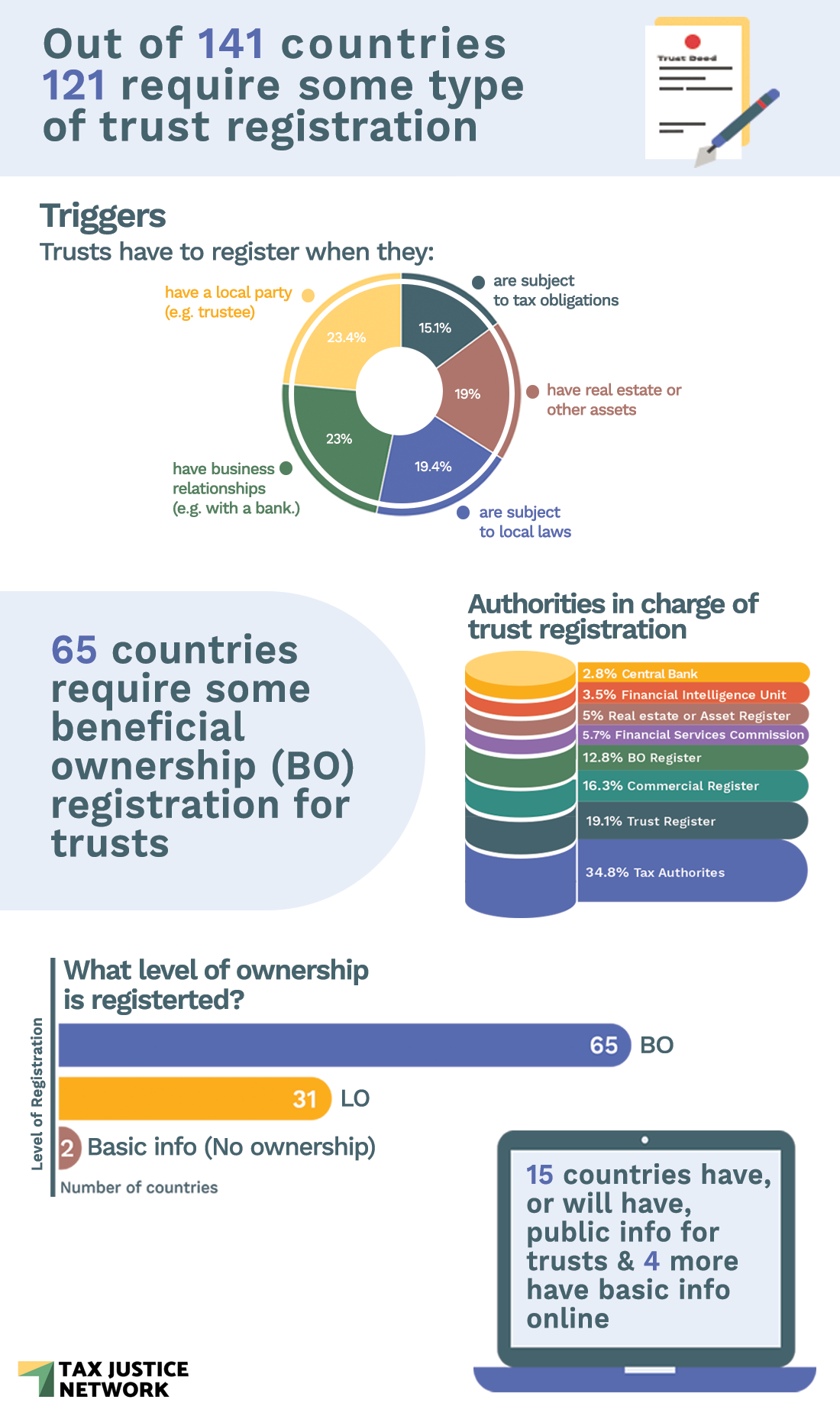

Trust registration around the globe

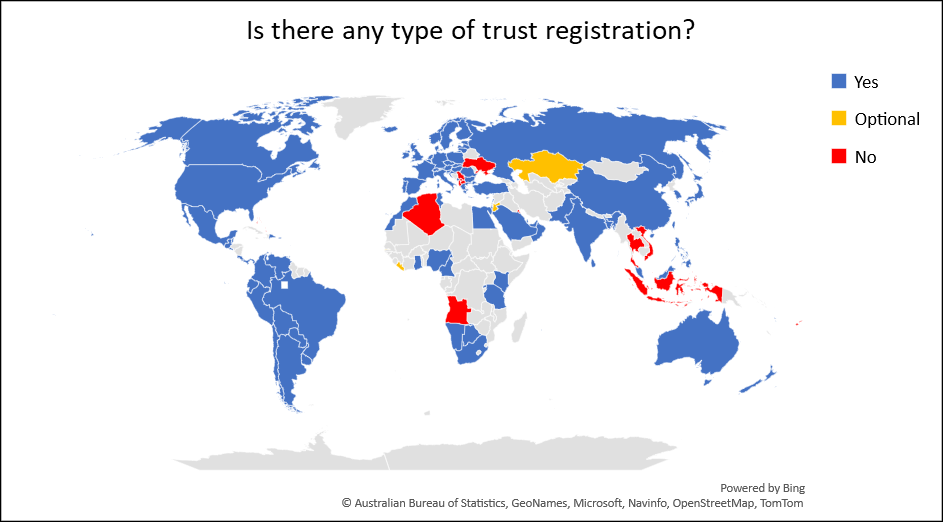

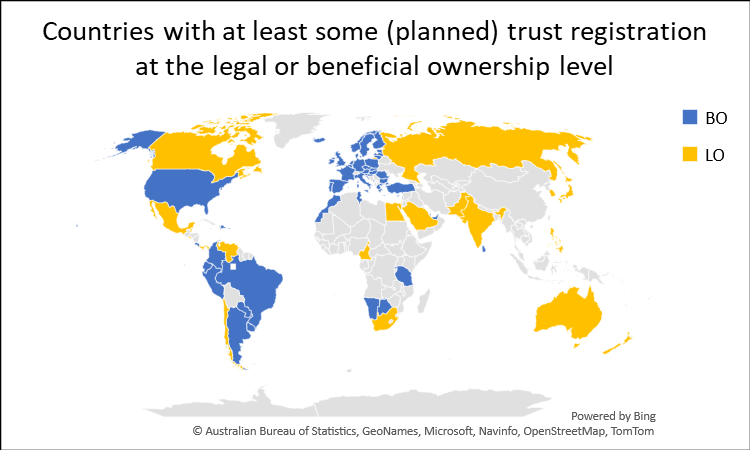

According to the 2022 edition of the Financial Secrecy Index, which assesses, among many things, legal and beneficial ownership registration for 141 jurisdictions, there are 121 countries that have some type of registration for “trusts”. By “trusts”, we include in our reference similar structures such as fideicomisos, fiducie, Treuhand or waqf. By “registration”, we refer to any situation in which a trust (or a trustee on behalf of the trust) must file information about the trust to a government authority (eg the tax administration, a trust registry or the land register).

Out of the 121 countries with some type of trust registration, 65 countries require (or plan to require) some type of beneficial ownership registration for trusts. This number includes:

- All 27 EU countries. The 5th Anti-Money Laundering Directive requires EU countries to set up central beneficial ownership registries for trusts.

- The US and four US territories (American Samoa, Guam, Puerto Rico and US Virgin Islands). The Corporate Transparency Act will apply to all US territories and, according to the proposed FinCen regulations (as of July 2022), “business trusts” (and other entities typically created by a filing with a secretary of state or similar office) will be covered by beneficial ownership registration.

- 11 countries in Latin America and the Caribbean: Antigua & Barbuda, Argentina, Brazil, Colombia, Costa Rica, Dominican Republic, Ecuador, Paraguay, Peru, St. Kitts and Uruguay.

- 9 jurisdictions in Europe: Andorra, Gibraltar, Iceland, Liechtenstein, Monaco, Montenegro, Norway, San Marino and the UK.

- 7 countries in Africa: Botswana, Morocco, Namibia, Rwanda, Seychelles, Tanzania and Tunisia.

- 5 countries in Asia (mostly in the Middle East): Lebanon, Qatar, Sri Lanka, Turkey and the UAE (for trusts created under the laws of the Abu Dhabi Global Market free zone).

- 1 country in Oceania: Nauru.

Public access

In order to facilitate access to information by all relevant stakeholders (including both local and foreign authorities, obliged entities such as banks in charge of customer due diligence, investors and businesspeople, journalists and civil society organisations), there should be public access to information on trusts. Public access is also the only way to hold authorities to account and to check the quality of the register.

Fortunately, countries in Europe and Latin America are going beyond the standards and are offering (or plan to offer) public, online access to beneficial ownership information:

- 12 of the 27 EU Members already offer, or plan to offer, public access to trusts’ beneficial ownership information: Austria, Bulgaria, Croatia, Czechia, Denmark, Estonia, Germany, Netherlands, Poland, Portugal, Slovenia, and Sweden.

- The remaining 15 EU Members will have to ensure access to competent authorities, obliged entities and those with a legitimate interest. South Africa also offers access based on a legitimate interest.

- 3 more countries either plan to provide public access to beneficial ownership information on trusts (Norway) or already offer it for legal owners (Ecuador and Panama).

- 4 countries offer public online access to basic information on trusts: Dominican Republic, Oman, Seychelles and Singapore.

Best cases of public access

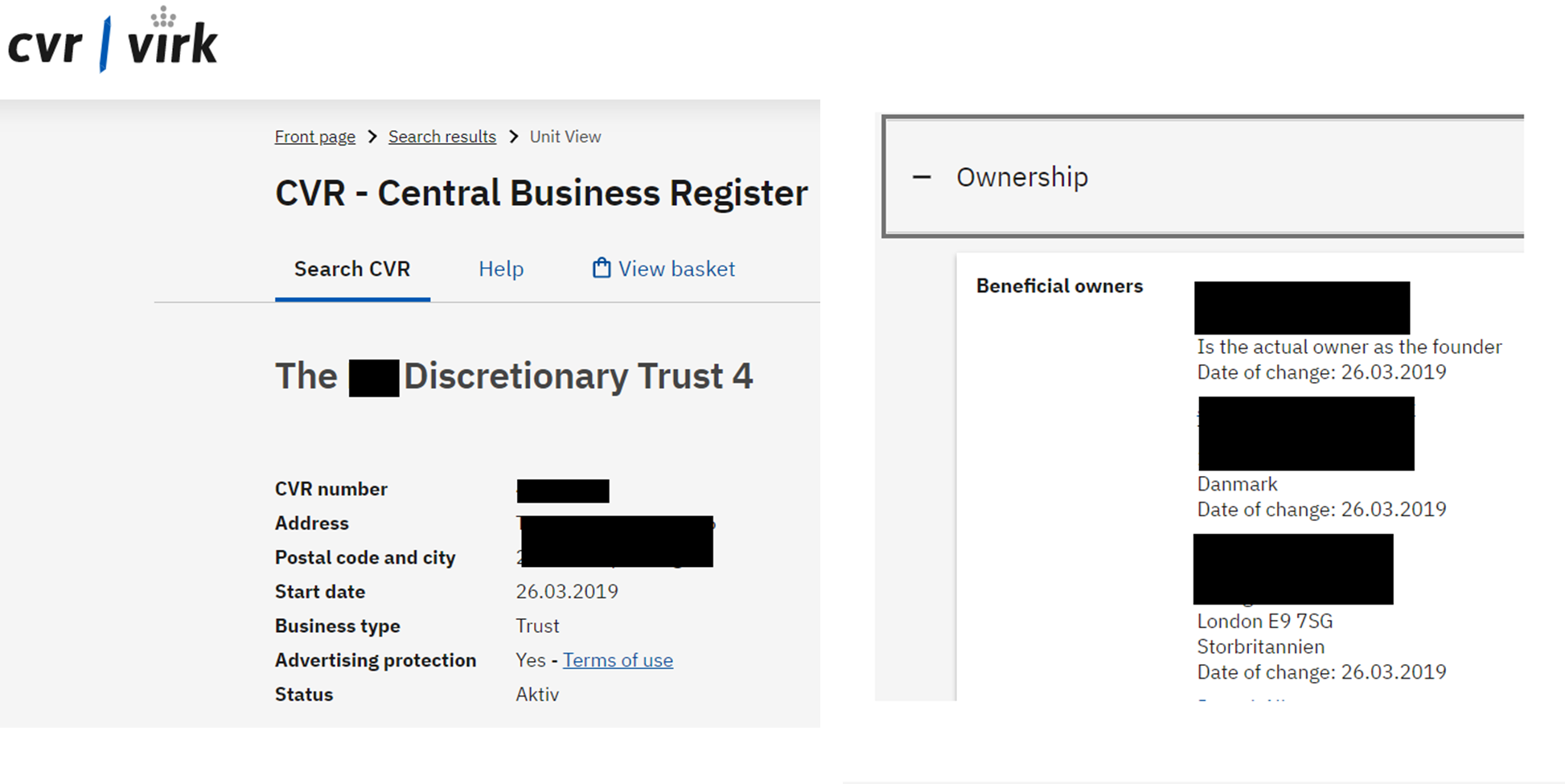

a. Denmark

Denmark offers free and public online access to information, allowing users to filter for only trusts in searches.

b. Ecuador

Ecuador allows users to search trust by name and tax identification number, including cancelled trusts. A wide range of details are available including settlors (constituyentes) and beneficiaries (beneficiarios)

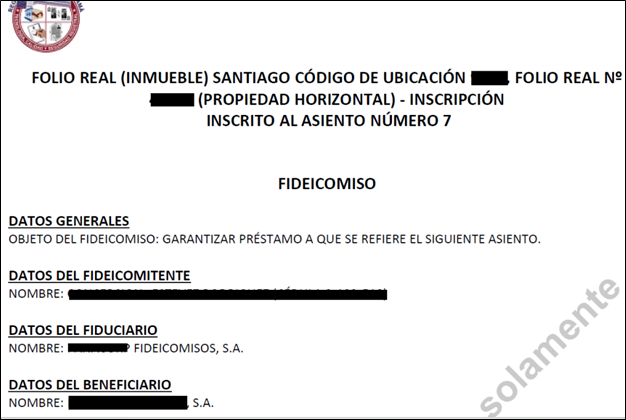

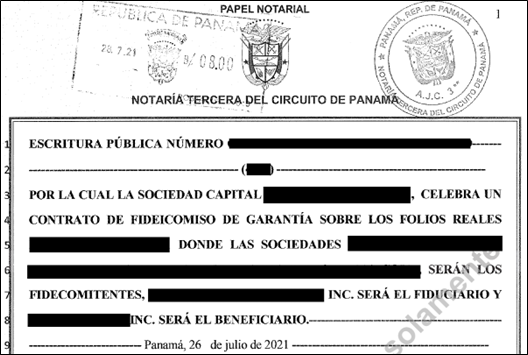

c. Panama

Of all places, Panama allows free online searches for trusts that are involved in real estate (inmuebles). Users can search specifically for trusts (fideicomisos) involved in real estate, and can also searching by name of settlor (fideicomitente), trustee (fiduciario) or beneficiary (fideicomisario). Information sometimes includes a summary of trust’s purpose (eg guarantee) and the name of the settlor, trustee and beneficiaries. More impressively, in some cases a free online scan of the full public deed creating a trust (fideicomiso) or a private foundation (fundación de interés privado) is available.

Recommendations

Based on the Tax Justice Network’s previous recommendations on how to prevent trusts from being abused to avoid sanctions against oligarchs, we propose the following recommendations.

The Financial Action Task Force (FATF) should:

1. Require the “registry approach” for trusts under the Reform of Recommendation 25.

All countries should:

2. Require trusts to register to have legal validity.

3. Establish central registers to collect beneficial ownership information on all trusts that: (a) are created according to, or governed by local laws; (b) have any asset or operation in the country; or (c) have any party who is resident in the country.

4. All parties (settlors, trustees, protectors, beneficiaries, and any other individual with control or benefit) to a trust (including unit trusts used for investment funds) should always be required to be identified as beneficial owners before they are allowed to enjoy any power or control, or receive a distribution.

5. When a trust owns a company, all the parties to the trust should be considered the beneficial owners of the company (not just the trustee or “any person with control over the trust”)

6. When a party to the trust is a legal person (eg a company), all the beneficial owners of the company should be identified as beneficial owners of the trust, ideally without applying any threshold. Even if the beneficial ownership definition for companies usually applies thresholds, eg “anyone with more than 25 per cent of shares”, no thresholds should be applied when a company is a party to the trust.

7. Provide public access to information on trusts, just as is done with legal persons similar to trusts such as private foundations. Public access should ideally be online, free and in open data format.

8. Prohibit discretionary trusts.

Download the report

The author

Related articles

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

The Financial Secrecy Index, a cherished tool for policy research across the globe