Welcome to our monthly podcast in Portuguese, É da sua conta (‘it’s your business’) produced and hosted by Grazielle David and Daniela Stefano. All our podcasts are unique productions in five different languages – English, Spanish, Arabic, French, Portuguese. They’re all available here. Here’s the latest episode, Registro global de ativos pode acabar com sigilo financeiro #38:

De um lado 33 milhões de brasileiros passando fome. Do outro, pelo menos 558 bilhões de dólares de brasileiros no exterior. De um lado, a população de rua aumenta. Do outro, super ricos com medo da violência. Mas “a violência só existe porque o sigilo financeiro existe antes”, afirma Márcio Calvet Neves, do Instituto de Justiça Fiscal no episódio #38 do É da Sua Conta, que traz a possibilidade de solução para estes problemas: o registro global de ativos.

Se ativos financeiros, e também outras formas de acumular riqueza, como joias, obras de arte, pianos e relógios caros, criptomoedas, obras de arte virtual, patentes e softwares de empresas fizerem parte de um registro global, em que todas as pessoas “de carne e osso” estejam ali identificadas, seria possível saber quanto de riqueza existe, quem são seus proprietários e, consequentemente, criar um imposto sobre esses bens, para que assim aqueles que possuem mais, contribuam com mais. A boa notícia é que um registro global de ativos é viável e possível. Saiba como nesta edição do É da Sua Conta.

Você ouve no É da sua conta #38:

A relação entre desigualdades e sigilo financeiro.

Como funciona o mercado de obras de artes virtuais.

Como ampliar registros de bens já existentes para incluir ativos financeiros.

Como saber quem são donos de criptomoedas, obras de arte e ouro.

A implementação de um registro global de ativos, do nacional para o regional e do regional para o global.

O que precisa ser feito para identificar beneficiários finais.

Os resultados do registro global de ativos: melhor arrecadação tributária e distribuição de riquezas.

A tecnologia das criptomoedas dos block chains, dos NFTs ainda é muito jovem e como ela mexe diretamente com dinheiro, atraiu muita especulação desenfreada.” (Luciano de Maria, programador e entusiasta de criptomoedas)

Ao se determinar de quem é a riqueza, os países que teriam acesso a esse registro global de ativos teriam instrumentos para fazer uma política fiscal mais eficiente, pra reduzir a desigualdade social e tributar quem realmente tem capacidade contributiva para pagar o tributo onde este deve ser pago..” ( Márcio Calvet Neves, Instituto de Justiça Fiscal)

Se possuir algumas barras de ouro, um quadro caro, um apartamento, uma conta bancária, um piano muito caro, uma carteira de ações, tudo seria registado no registo global de bens; e seria acessível, no mínimo, às suas autoridades fiscais e policiais para ter a certeza de que a pessoa paga seus impostos.” (Nick Shaxson, Tax Justice Network)

É muito positivo usar intermediários pra reportar e implementar esses marcos de devida diligência, identificar por exemplo se a carteira está no nome de uma empresa, que seja necessário registrar também o proprietário final dessa empresa.” (Florencia Lorenzo, Tax Justice Network)

Há um processo: ao construir um banco de dados sobre o que já existe e expandir gradativamente, conectando os registros entre países e regiões , finalmente, chegaremos a esse objetivo de um registro global de ativos..” (Gabriel Zucman, ICRICT)

Se a gente conseguir as informações de beneficiários finais, será uma vitória mundial contra os evasores” (Marcio Verdi, CIAT)

~ Registro global de ativos pode acabar com sigilo financeiro #38

Participam desse episódio

Gabriel Zucman – membro da Comissão Independente para Reforma da Tributação Corporativa Internacional (ICRICT), professor da Universidade da California Berkley e diretor do Observatório Tributário da União Europeia

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa con Marcelo Justo y Marta Nuñez:

Más secretos del índice de secreto financiero global de la Tax Justice Network.

Las multinacionales y las pequeñas y medianas empresas en nuestro cuarto capítulo sobre qué son los paraísos fiscales. El ejemplo de Colombia.

Los bancos, grandes ganadores de estos años de pandemia en América Latina

Y el impacto social y la emigración en Ecuador, un país devorado por un sector financiero que hoy gobierna el país.

Invitados:

Ryan Gurule de FACT (Coalición estadounidense por la Transparencia Financiera y Corporativa)

Guillermo Oglietti, investigador del Centro Estratégico Latinoamericano de Geopolítico (CELAG) y co-autor del libro “La mano visible de la banca invisible”

Welcome to the 54th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

في العدد #54 من الجباية ببساطة سلطنا الضوء على نتائج مؤشر السرية المالية لسنة 2022 الذي تصدره شبكة العدالة الضريبية وإحتلت فيه الولايات المتحدة الأمريكية المركز الأول قبل أن نتطرق في حوارنا مع الصحفي التونسي عبد السلام الهيرشي لبحث استقصائي حول البنوك في تونس تحت عنوان “كارتيل البنوك في تونس: أثرياء الحرب في زمن البؤس”

For this month’s episode #54 of “Taxes simply”, we explore the latest results for the Financial Secrecy Index, which saw the US ranked first for offering financial secrecy to the criminal and corrupt. We then speak with Tunisian journalist Abd El Salam El Herchi, who recently published an investigative piece on the banking cartel in Tunisia and the corruption involved in establishing this cartel. We discuss the repercussions and the consequences for the Tunisian economy and the Tunisian people.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Le mois de mai 2022 a été marqué par la publication par Tax Justice Network de l’édition 2022 de l’Indice d’Opacité Financière. L’événement est intervenu en même temps, que l’appel lancé à Dakar au Sénégal le 17 mai 2022, par les ministres africains de l’économie pour un système fiscal international sous l’égide des Nations Unies. Pour la quarantième édition de votre podcast en français produit par Tax Justice Network, nous revenons sur le lancement en Afrique de l’indice d’Opacité Financière. Avec nos partenaires du CRADEC, nous avons échangé sur des questions comme l’échange automatique d’information, la propriété effective et le reporting financier des entreprises pays par pays. Les participants au regard des résultats présentés, ont soutenu l’idée de soutenir un système fiscal international sous le prisme d’une convention des Nations Unies.

Interviennent dans ce podcast :

Jean Mballa Mballa, Directer Exécutif du CRADEC

Eric Etoga, Chercheur Dynamique Mondiale des jeunes

Honorable Jean-Marie Pong Moni, Sénateur du Cameroun

~ Lancement en Afrique du l’Indice d’Opacité Financière 2022 : L’urgence d’un système fiscal international sous l’égide des Nations Unis #40

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le sous ce lien.

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Os Estados Unidos estão no topo do Índice de Sigilo Financeiro 2022 da Tax Justice Network. Isso significa que além de favorecer a corrupção, os EUA têm grande responsabilidade no saque das riquezas dos países, na redução da capacidade de arrecadar impostos e na desestabilização de mercados no mundo todo.

De acordo com este ranking, há o dobro de riqueza escondida em paraísos fiscais do que dinheiro circulando nas economias, entre pessoas e empresas. Mas, ha nouma boa notícia Índice: apesar das sabotagens de cinco dos países que compõem o G7, as reformas nas regras da transparência adotadas em mais de 100 países estão reduzindo o mercado para aqueles que buscam esconder suas fortunas. Os achados do Índice de Sigilo Financeiro 2022 e soluções apontadas por esse relatório da Tax Justice Network estão na edição #37 do É da Sua Conta.

Você ouve no É da sua conta #37:

Top 10 dos países que mais fornecem sigilo financeiro no mundo.

O que levou os EUA à essa vergonhosa liderança e o que precisa ser feito para o país diminuir a oferta de esconderijo para indivíduos ricos, de acordo co organizações que atuam por justiça fiscal.

EUA, Reino Unido, Alemanha, Itália e Japão: o mau exemplo das grandes economias como facilitadoras de sigilo financeiro.

A razão da melhora da posição das Ilhas Cayman, ainda que continue entre os 20 que mais oferecem serviços secretos.

Emirados Árabes Unidos, Singapura e Hong Kong: a tendência de indivíduos ricos em buscar autocracias para esconder suas fortunas.

Angola e Brasil: como estão no ranking e o que precisa ser feito para reduzirem a oferta de sigilo.

Call to action: registro global público dos proprietários “de carne e osso” e de bens e ativos e transferência das decisões sobre tributação internacional para a ONU.

“Os EUA são a única grande economia que ainda não adotou os padrões internacionais de transparência de informações.” ~ Florencia Lorenzo, Tax Justice Network

“A indústria de investimento privado dos EUA está perto dos USD 11 trilhões, o que ultrapassa qualquer mercado semelhante no mundo. É por isso que as reformas que os EUA precisam fazer para a transparência desse mercado são tão vitais.” ~ Ryan Gurule, FACT Coalition

“Mesmo nos países ricos dos paraísos fiscais, a maioria das pessoas são também vítimas das suas próprias elites corruptas. Portanto, é melhor ver este equilíbrio de forças como sendo entre uma pequena elite transnacional corrupta, por um lado, e os 99% de pessoas comuns em todos os países, ricas ou pobres, por outro lado.” ~ Nick Shaxson, Tax Justice Network

“Vemos os serviços de sigilo irem cada vez mais para esse tipo de jurisdição (autocrática), o que é um sinal positivo na medida em que reflete uma espécie de marginalização dos fluxos financeiros ilícitos. Já não é algo que se possa fazer através de Londres ou Delaware.” ~ Alex Cobham, Tax Justice Network

“(Levar a discussão para a ONU) permitiria a todos os países participar de forma igualitária, o que atualmente não é uma realidade com as regras tributárias globais sendo feitas na OCDE sem a participação de mais de um terço dos países do mundo.” ~ Lays Ushirobira, Global Alliance for Tax Justice

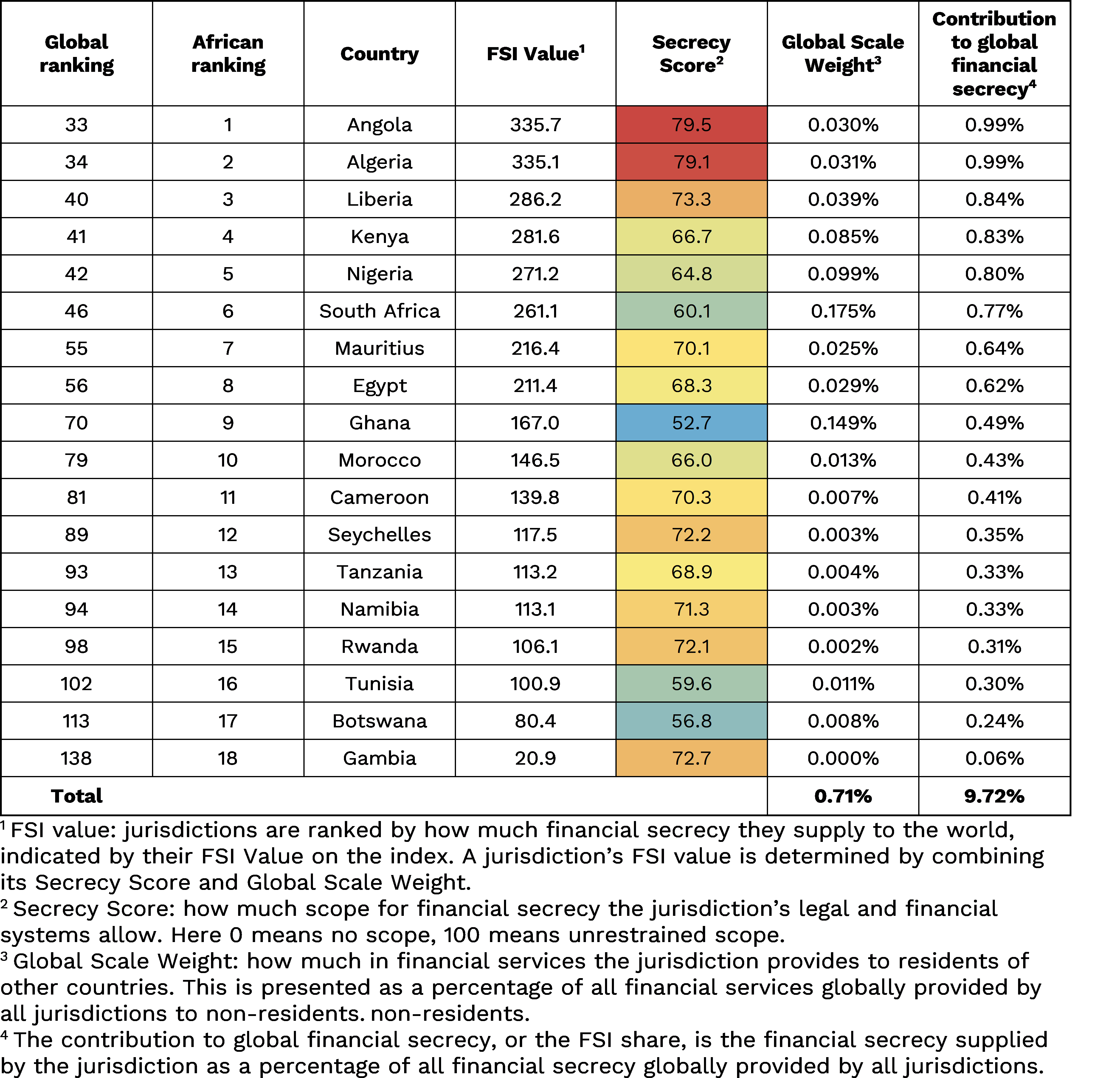

African Ministers call for UN tax convention to protect against financial secrecy supplied by the richest nations, as Africa improves in the Financial Secrecy Index 2022 – Tax Justice Network, Tax Justice Network Africa, Centre Régional Africain Pour le Développement Endogène et Communautaire

Yaoundé – Cameroon, 27th May 2022. Africa loses about US$ 90 billion per year in illicit financial flows, robbing the continent of resources to finance investment and development. Financial secrecy allows individuals to hide and move money out of the continent and the Financial Secrecy Index 2022, published by the Tax Justice Network, shows that the largest enablers of financial secrecy are some of the richest nations in the world, including the USA and Switzerland.

African leaders do not have an equal footing in setting international tax rules, which have been determined for over a century by a group of rich countries under the Organisation for Economic Co-operation and Development. This is why African Ministers of Finance, Planning and Economic Development adopted a resolution last week calling on the United Nations to begin negotiations on an international convention on tax matters.

The Financial Secrecy Index finds that all but 4 of the 18 countries assessed in the region – Rwanda, South Africa, Seychelles and Ghana – have made progress in improving financial transparency at home. None of the countries in the region is in the top 30 of financial secrecy suppliers in the world. On the contrary, several countries, such as Kenya and Nigeria, are in the top 20 of those that have improved their laws against the use of secretive financial practices by non-residents.

Half of the African countries assessed have also made significant progress in requiring disclosure of beneficial ownership of companies and more than half now have beneficial ownership laws in place. In addition, the capacity of tax administrations has improved or remained at the same level for all jurisdictions, and there are being great strides to improve international cooperation to prevent money laundering. Two countries – Ghana and Liberia – showed a worrying shift in the index, but this is mainly because they now offer more financial services to non-residents and not because they have introduced more secrecy services.

All African countries must take domestic action to prevent enabling illicit financial flows needed to finance sustainable development by improving corporate transparency obligations. This includes quick wins, like making all extractive industries contracts, tax rulings, and beneficial ownership information public. And requiring country by country reporting of multinational companies that are headquartered domestically and requiring subsidiaries of multinationals operating domestically to report on a country by country basis locally.

Most importantly, the index also reveals that Africa must continue its efforts to protect itself from its international partners. Five G7 countries alone – the US, UK, Japan, Germany and Italy – are responsible for cutting global progress against financial secrecy by more than half. African leaders must also continue to keep a close eye on Asian economic partners, including Singapore, Hong Kong, the United Arab Emirates and China, which have maintained or jumped up the rankings, both because of the increase in financial services they offer to non-residents and their financial and legal systems that enable financial secrecy.

The Financial Secrecy Index 2022 shows again that international tax rules cannot be set by the OECD, which members are some of the greatest enablers of financial secrecy. African leaders are right to call for a UN convention on tax to curb illicit financial flows and recover stolen assets. An inclusive, global approach to setting international tax rules is the only way Africa can stop its plunder from tax abuse.

Alvin Mosioma, Executive Director Tax Justice Network Africa:

“The results of this year’s Financial Secrecy Index highlight the problem of having the very same countries that are the leaders in the provision of financial secrecy be the very same countries that are spearheading the discussions on global tax reform. The Tax Justice Network Africa reiterates its support for the call by African governments for a tax convention that supports an intergovernmental tax body. Indeed, such a body is necessary to enable African countries to participate in global discussions on tax on an equal footing as all other countries.”

Alex Cobham, chief executive Tax Justice Network:

“The current international tax architecture is a disaster. It gives rise directly to needless inequalities between countries and within countries, denying everyone the chance for better lives. Lower income countries lose by far the largest share of their current tax revenues to cross-border tax abuse – the equivalent of nearly half their public health budgets. But lower income countries are also excluded from international cooperation and rule-setting. The Financial Secrecy Index 2022 shows the countries most responsible for enabling illicit flows, are the same countries setting the rules. The powerful joint call from African finance ministers brings the world a step closer to the international tax reforms that are desperately needed. It is crucial now that policymakers in other regions make their views clear, and that the United Nations accepts this mandate and begins negotiations urgently.”

Jean Mballa Mballa, Executive Director of CRADEC (African Regional Centre for Endogenous and Community Development):

“As a civil society active in the fight against illicit financial flows and tax justice, we are satisfied with Cameroon’s progress. We are particularly pleased by the efforts made with the ownership registration, the framework for more efficient tax administration, as well as the good behavior in international cooperation. However, we are still concerned about the management of transparency with respect to legal entities. Finally, we invite the authorities to be more vigilant, in view of the evolution of China, the country’s leading commercial partner, whose responsibility as well as that of two main jurisdictions affiliated to it (Hong Kong and Singapore) has increased sharply, with regard to the facilitation of financial secrecy.”

About the Financial Secrecy Index

The Financial Secrecy Index is produced biennially by the Tax Justice Network. It ranks each country based on how intensely the country’s financial and legal system allows individuals to hide and launder money extracted from around the world. The index grades each country’s financial and legal system with a secrecy score out of 100 where a score of 0 is full transparency and a score of 100 is full secrecy. The country’s secrecy score is then combined with the volume of financial services the country provides to non-residents to determine how much financial secrecy is supplied to the world by the country. The Financial Secrecy Index 2022 assesses 141 jurisdictions.

Contacts

Tax Justice Network

Tax Justice Network Africa

Centre Régional Africain Pour le Développement Endogène et Communautaire

C/O Godfrey Wilson Ltd,

5th Floor Mariner House,

62 Prince Street,

Bristol, England

BS1 4QD

[email protected]

African finance ministers have adopted a resolution calling for a United Nations convention to stop tax abuse earlier this week as some of the richest nations, including the US and Switzerland, continue to be the biggest suppliers of financial secrecy according to the Financial Secrecy Index 2022, published this week by the Tax Justice Network.

African countries lose about $90 billion in illicit financial flows each year. This underlines how inadequate rich-countries’ efforts are through the Organisation for Economic Co-operation and Development to redesign the rigged financial system. The Financial Secrecy Index 2022 reveals that five G7 countries alone—the US, UK, Japan, Germany and Italy—are responsible for cutting global progress against financial secrecy by more than half.

In the meantime, African economies are dealing with the Covid-19 pandemic’s impact, exacerbated by Russia’s invasion of Ukraine. Here in Malawi, the price of bread has more than doubled, now costing over half the minimum daily wage. This is why African leaders this week called for a United Nations Convention on Tax to curb illicit financial flows and recover lost assets, where financial secrecy is an accomplice lurking in the shadows.

The Conference of Ministers […] Calls upon the United Nations to begin negotiations under its auspices on an international convention on tax matters, with the participation of all States members and relevant stakeholders, aimed at eliminating base erosion, profit shifting, tax evasion, including of capital gains tax, and other tax abuses.

UN Economic and Social Council, Committee of Experts’ Resolutions for consideration by the Conference of Ministers, endorsed 17 May 2022

The African Union and UN Economic Commission for Africa triggered the global adoption of a target to curb illicit flows in 2015. This was through the High-level Panel on Illicit Financial Flows from Africa, led by former South African president Thabo Mbeki. This paved the way for concerted campaigning by African policy makers, parliamentarians and activists. And the resolution is a testament to their perseverance.

Financial secrecy at large

Financial secrecy is slowly shrinking the world over, despite some of the richest countries subverting progress. Total financial secrecy dropped by 2 per cent in 2022. This follows a 7 per cent reduction in 2020, according to the Financial Secrecy Index 2022. This is because of better international cooperation and more and more countries requiring beneficial ownership disclosure.

Yet the Financial Secrecy Index 2022 remains a warning of the divisive deficiencies in the global financial system. Every country loses. But the impact is hardest for lower income countries (or historically plundered states, as economic anthropologist Jason Hickel has called them).

In the wake of the Pandora Papers—the largest journalistic investigation of the biggest leak exposing the offshore world of finance—journalists Simon Allison and Sipho Kings asked:

What if, instead of giving money to the developing world, rich countries stopped money from leaving the developing world in the first place?

In the index, countries are assessed on how intensely its financial and legal system allows individuals to hide and launder money. The lower the marks of the secrecy score out of 100 the better. In the index, 100 is full secrecy and 0 is full transparency. The Financial Secrecy Index 2022 analyses financial and legal systems of 141 jurisdictions across four categories. These are: knowledge of beneficial ownership, the transparency requirements for legal entities, the integrity of tax and financial regulation, and international standards and cooperation.

The secrecy score is not just a report card, it’s a problem-solving manual. It shows policymakers the laws and loopholes to amend to become more transparent. But it’s not just how secretive a country is that matters, the index combines the secrecy score with the global scale weight. This is the volume of financial services countries provide to residents of other countries. Services like opening a bank account or setting up a company. The combination of the secrecy score and global scale weight into the FSI value paints a picture of how much offshore financial activity is put at risk by a country’s laws.

Africa in the Financial Secrecy Index 2022

Since the 2020 edition of the Financial Secrecy Index, all but four African countries—Rwanda, South Africa, Seychelles and Ghana—have made some progress improving financial secrecy at home. Two countries —Ghana and Liberia—made worryingly large leaps up the index, mainly because they now offer more financial services to non-residents.

Over the last two years, African countries have made steady progress in improving international cooperation on anti-money laundering efforts, information exchange and judicial cooperation. Several tax administrations are improving the way they operate. Half of the African countries also made great leaps in requiring the disclosure of beneficial owners of companies. More than half now have beneficial ownership laws for companies, requiring the real flesh and blood owners to be identified. Yet in most countries limited partnerships remain black boxes, making it possible for the real owners to avoid scrutiny.

All African countries have an alarmingly high secrecy score of over 90 points out of 100 when it comes to the transparency requirements for companies. This is an area with quick wins to stop the bleed. Jurisdictions should require companies to make public up-to-date beneficial and legal ownership information, publish all extractive industries contracts and tax rulings, and let the public have free access to the annual accounts that companies file.

No African jurisdiction requires multinational companies to publish public country by country reports. These reports shed light on where a multinational company books their profits and pays taxes, aiding tax collectors to make sure they are paying their fair share. Yet South Africa and Nigeria are home to some of Africa’s largest multinationals that should require their multinationals to publish these reports.

Taking on financial secrecy inclusively

This week has been monumental with African leaders calling for a UN tax convention because countries, like Malawi, have very little say over the current international tax regime. It has remained substantively unchanged since the early twentieth century. The rule-setter the OECD, has brought 140 countries together in its so-called “Inclusive Framework”, promising an “equal footing” in determining international tax rules. Even the African Tax Administration Forum criticised the pressure African countries were put under in the recent process to develop new tax rules for taxing the digital economy. The Professor of Law Yariv Brauner at the University of Florida has rightly described the forum as a “(not so) Inclusive Framework”, and the emerging reforms it is pushing appear massively favourable to rich countries.

Instead of the OECD’s piecemeal approach, a United Nations Framework Convention on Tax, just as the African finance ministers articulated, and a truly representative convening body, where the Malawian and other African governments have a say, are essential to fundamentally change the way all governments can tackle tax abuse. Financing our responses to the Covid-19 pandemic and its aftermath depend upon it.

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

Which nations are the world’s biggest financial secrecy offenders? And what does it tell us about the world, about politics and about democracy? How high does your country rank in facilitating global corruption?

Allowing anonymous wealth is undermining for all of us. I think we’re going to see a bit of a separation and we’ll see who really needs the secrecy regardless of the reputational damage and who has some kind of slightly more genuine commitment to responsible financial services practice.”

~ Alex Cobham

Right now the US is itself a tax haven, it’s one of the biggest secrecy jurisdictions in the world. These results confirm that, and it’s no longer time for the US to pretend that it can enact and create a less corrupt global environment and foster democracy without looking internally and cleaning up its own house and catching up with global norms. It’s time to walk the talk.”

~ Ryan Gurule

The Taxcast, May 2022 summary on the Financial Secrecy Index 2022 results:

Naomi: “We’re hearing a lot from world leaders about sanctions against Russian oligarchs at the moment. We know financial secrecy is what the powerful, the corrupt, and criminals really love. With financial secrecy they can undermine the democratic will of any country’s government. They can drain the tax revenues that stop the rest of us living secure and happy lives. So which nations are the world’s worst offenders when it comes to financial secrecy? I’m going to tell you, because this month the Tax Justice Network’s released the latest results of the Financial Secrecy Index. Our specialist team ranks countries every two years on how secretive their financial and legal systems are. Then, they combine that with how big a financial secrecy global player they are – in other words, how much damage they’re doing in the world.

So, this isn’t a list of the world’s most secretive jurisdictions, as is sometimes misreported. It’s a list of countries ranked according to the level of secrecy services a country offers customers, combined withits size as a global player. I’ll give you an example – the very beautiful Maldives is a highly secretive jurisdiction – but it’s a really small player globally doesn’t have a significant impact on global financial secrecy – so it’s not at the top of the index. So it’s logical isn’t it, that the bigger a financial secrecy supplier a nation is, the more responsibility they have to reduce their secrecy services because they’re doing more damage. So…this is a ranking you don’t want to be at the top of. So, here’s the top ten – our 2022 roll call of shame…

At number 1 is the United States, with the worst rating ever recorded by the Financial Secrecy Index.

Number 2 is Switzerland

Joining the top 3 for the first time is Singapore

Number 4, Hong Kong

Number 5, Luxembourg

At number 6 is Japan, which increased its supply of financial secrecy to the world by 10%

Germany’s shot up to number 7 from 14th place last time, it’s increased its secrecy supply by a third, a very bad result for them – so much for all that cheap talk on sanctions on oligarchs!

And at number 8, the United Arab Emirates – at least they don’t pretend to care about oligarchs!

At number 9, the British Virgin Islands, a British Overseas Territory

And number 10, Guernsey, a British Crown Dependency

[Clip of the British national anthem and the Sex Pistols ‘God Save the Queen’]

And yes, don’t be fooled by the United Kingdom not being in the top ten. This time the UK is at the number 13 spot. BUT as is ALWAYS the case, I’m ashamed as a British person to tell you that when you combine Britain with all its satellite havens around the world, it is still the world’s worst offender. We’re gonna talk about Britain later, and of course the shockingly bad result for the United States and how other G7 states – Japan, Germany and Italy are holding back progress. By the way, when it comes to China it’s zoomed up to number 11 in the index. And what China does is extremely impactful on for example, Africa, since China is their biggest trading partner. Anyway, there are 141 countries assessed in the index, so there’s plenty more fascinating stuff there. I asked head of the Tax Justice Network Alex Cobham for his reaction to the 2022 Financial Secrecy results:”

Alex: “I guess the least surprising thing was the US actually getting to the top, as the biggest global threat, but the kind of the backsliding of the G7 was a bit unexpected. I hadn’t thought we’d see that across that set of the most powerful countries. But the biggest surprise was Cayman. Cayman has dropped from the top, out of the top 10, and surprising because of the reason for it, you know, they’ve, they’ve spent so long, I think Cayman Finance has put more money and more time than anyone in the world into criticising the index. And the index rightly judges them as highly secretive – to be fair, they have genuinely improved, this year their secrecy score is down from 76 to 72, mainly because the UK required it to join the UN conventions on terrorist financing and the convention against corruption. But the reason the rank has dropped so sharply is because all of this time they’ve been refusing to publish the information about their share of international financial services exports, and now they’ve finally done it and it’s revealed that, that their global role is actually much smaller than we, and pretty much everybody else had always estimated from the data that they do actually allow to become public. Now, what that means is that they must have known all of this time that their ranking in the index was seriously over inflated. And I suppose they took the decision that they’d rather look like they were the really really bad guys than actually come clean and tell people that they’re not quite such a big player in global finance as they were allowing people to think. So that’s, that’s the big surprise. Of course, you know, the UK and its set of dependent territories remains the biggest overall problem despite Cayman’s improvement.”

Naomi: “That’s interesting. I mean, when it comes to the G7 nations the Financial Secrecy Index points the finger really really strongly at the US, the UK, Japan, Germany and Italy and you know, they have been shouting the loudest about sanctions on Russian oligarchs yet we now know through the Financial Secrecy Index results that they’re responsible for cutting back progress on financial transparency that would have allowed sanctions to happen, I mean – complete hypocrisy, so I mean what’s going on with that?!”

Alex: “It’s kind of fascinating, isn’t it? Um, you know, these, this set of countries are not the most secretive jurisdictions in the world, not by a long shot, but they are big players. And so their secrecy matters, they have a big share of global financial services and so when they are more secretive it poses a bigger risk to everyone else. As you say, what’s happened this year is that the progress that would have been made if the G7 had just stood still has been cut by more than half because actually they’ve gone backwards. Then, uh, Canada, France, um, to round out the G7, um, actually both getting, getting slightly better, so well done them, showing it can be done, including within the EU, but it takes a bit of commitment. So it’s a slightly depressing picture. You know, these are the countries, as you say, in, in this moment of Russia’s invasion of Ukraine that are looking to make sanctions effective and they need to be looking at themselves and saying the way that we deny progress on financial transparency, doesn’t just deny the ability of other countries to tax fairly and to act against corruption, it also denies our own ability to impose effective sanctions if we want to. You have to hope that if there’s a silver lining to any of that, it’s a recognition including among these most powerful countries that allowing anonymous wealth is undermining for all of us, and we just have to finally push through and deliver on the beneficial ownership transparency, knowing who is behind companies, trusts, foundations, partnerships, and bank accounts so that we can all be broadly confident that uh, you know, that law and order is applied across the board and that the system works and that we can tax progressively.”

Naomi: “Yeah. And another trend, I mean tell me if I’m right or not in suspecting that when it comes to autocratic states there’s sort of a rise in the use of those states for financial secrecy, and surely oligarchs worldwide will be observing all this talk about sanctions against prominent Russians, now we’ve seen in this index, very interestingly rise of the United Arab Emirates. Um, Singapore has risen a lot too, which I know it’s, uh, a democracy, but it’s, uh, also described by many as a thinly veiled autocracy, Hong Kong also. Could this be a future trend in your view and what would that mean?”

Alex: “I think it’s definitely crystallising as a trend and remembering that the index is in a sense backward looking because it takes a long time to, to bring together the data, the trends we’re actually seeing this year, aren’t yet reflected in the index and so it’s already going to go further than, than what we are, what we’re seeing in the index now. And I think the way you frame it is, is spot on. We are seeing a shift, which I think we can probably think is broadly positive, but with some caution, it’s a shift away from the secrecy jurisdictions, the tax havens that have sold themselves as offering good governance, tax neutral investment platforms for the concerned international investor, right? Where the key thing in a sense is that you are saying, you know, ‘if you have a dispute, our legal systems are absolutely straight and you’ll be appropriately protected. Your property rights will be protected. Now you may be doing all sorts of bad things elsewhere, but not to worry. we will look after you.’ What we’re seeing now, as you say, is a shift towards a set of jurisdictions that really don’t make those claims about good governance, or at least not with any seriousness because you know, the common thread, Hong Kong, Singapore, the United Arab Emirates is a pretty much complete disregard for human rights. Um, they may still claim that they’ve got systems in place to protect investors, but not as human beings, only as you know, the sources of money. And I think the fact that we are seeing that shift, we’re seeing secrecy services increasingly going to that sort of jurisdiction is a positive sign in that it, it reflects a kind of marginalisation of illicit financial flows. It’s no longer something that you can just do through London or Delaware. And you know, this is good business practice and everyone says, oh, that’s, that’s probably okay. Increasingly we’re seeing people, you know, not least Russian oligarchs in effect being openly in defiance of the application of, of laws or sanctions that others try to put on them, and going to these places where most other people are denied full human rights, as a choice. So this is not something you could defend as, as good governance or investment practice or anything else. This is clearly nothing more than an attempt to defy others making their own laws effective on you. And you are so keen to do that, that you are willing to hold your nose about whatever other practices that jurisdiction has. So I don’t think you could say, you know, this is anything like the end of the road, but I think we’ll look back in a few years and this might seem like a bit of a turning point when that kind of good governance investor protection argument for secrecy jurisdictions was finally nailed. And it became clear that, you know, this is about hiding, and cheating, and dodging, and abusing, and nothing else. And if you want to do it well, you do it over there. And the rest of us will make our own judgements about you, but let nobody pretend this is good investor behaviour or anything of the sort.”

Naomi:“That’s really interesting. Um, and I mean, we shouldn’t be that surprised because in the end, you know, tax havens and secrecy jurisdictions are fundamentally anti-democratic. But the G7’s gonna have to up its game, you know, a lot. And that’s what we are are getting strong and clear from the secrecy index, isn’t it? I mean, together they’ve increased their supplies of financial secrecy – Italy and Germany by a third, Japan by 10%, the UK by 2%, the US, well that’s the worst rating ever recorded since the ranking began in 2009!”

Alex: “Yeah. Look, it’s, you know, it’s an interesting time to see whether, or the extent to which the, the financial sector broadly defined takes heed of what’s going on. So, you know, I was looking at earlier this year, thinking about the British Virgin Islands. So here’s a jurisdiction, a UK, uh, dependency under investigation by the UK – and that takes a lot, you know, for the depth of its corruption – and the question you’re asking yourself is like, this is a major provider of anonymous companies used by investors of some description all around the world and a certain number of major multinationals and financial services firms too. Are those firms those kind of mainstream, responsible financial actors, are they gonna stay in the BVI or are they gonna say no? And you know, and now that the UK has confirmed in its findings the depth of the corruption, what’s their decision? Do you say, ‘okay, we, we can’t be there. It’s just, it’s so obvious that we are just there to cheat people and, and, you know, there can’t be any kind of good governance argument or anything.’ Or do you say ‘we don’t care. We need the secrecy, we need the ability to cheat, so we’re gonna stay anyway and we’ll take a bit of a reputational hit’ but now there’s a lot more of the financial services actors around the world finding that they’re in places that are really increasingly gonna be seen, or are seen as kind of beyond the pale. So what do you do? I think we’re gonna see a bit of a separation and, you know, it’s, I guess the, the tide going out to some extent, we’ll see who’s naked, you know, we’ll see who really needs the secrecy regardless of the reputational damage and who has some kind of slightly more genuine commitment to responsible financial services practice.”

Naomi: “Yes, the secrecy space is being squeezed, and the index team did identify a 5% global reduction in financial secrecy, although the increases in the G7 nations I mentioned really cuts that progress right back. But let’s look at the number one global offender, the United States. Wow! After all the Biden administration has said about tackling tax havens and about sanctioning oligarchs! I mean, they’ve increased their financial secrecy supply to the world by almost a third, the largest supply ever recorded by the index! That’s despite some fantastic anti-corruption coalitions in the States and achievements like the passing of the Corporate Transparency Act, finally passed after so many years. I spoke to Ryan Gurule of the FACT Coalition in the United States about the result for his country:”

Ryan: “I think that there are a lot of different factors that contribute to the score. The score itself is not surprising. Um, there are a couple of different factors that contribute to it and things that we’d seen as well. Um, first and foremost, uh, the US is behind in implementing transparency based reforms. And we know this, um, in fact, the US, which kind of kicked off the whole global transparency movement with FATCA, which is the US foreign account transparency mechanism in which US financial accounts held offshore are reported back to the US. That system is not reciprocal at all.”

Naomi: “He means that while the US insists on other countries sharing information on their citizens abroad, it doesn’t return the favour. So, information on the citizens of the world’s activities in the US remain locked in secrecy. Yes, really!”

Ryan: “And in the meantime, after the US kind of created that system, uh, it failed to engage with the world in making a more reciprocal information exchange system in tax. And it failed to keep up in other transparency reforms related to beneficial ownership of entities, real estate, private investment funds, and regulating the enablers that help potentially corrupt actors access the extremely enticing US financial system. And it’s enticing for a variety of reasons. The US financial system has very strong legal protection and it offers anonymity and complete secrecy.

I think it’s a bit of a wake up call, especially in light of what’s happening in the world right now. We’ve seen Russia invade Ukraine, we’re talking about an authoritarian nation invading a democratic country. And what we’re seeing when the United States is leading a global response in sanctioning the oligarchs that are part of Putin’s cadre, it’s difficult to do that if you don’t know where those oligarchs are keeping their money and, and hiding it. And from that perspective, I think that the Western countries are recognising that they’ve been playing a significant role in entrenching and empowering those regimes by allowing kleptocrats to pilfer from their own country and move that money back to secure, secretive Western jurisdictions, like US markets that are very attractive, and to do so on a completely anonymous basis and that has only entrenched their power at home, emboldened their actions and is resulting in a lot of the conflict that we’re seeing. So I think that wake up call, along with this score will be a real call to act.”

Naomi: “There are chinks of light though despite this disastrous scoring for the US which may not come into view until the next Financial Secrecy Index in 2024, I mean you’ve had the Corporate Transparency Act finally passed after so many years of trying. Once that’s fully implemented there should be some serious progress that should filter into the next results?”

Ryan: “Yeah, the United States has begun to act and the Corporate Transparency Act was passed in January of 2021. And for the first time that will require the disclosure of beneficial ownership of most legal entities in the United States, corporations, limited liability companies, we expect it to cover every limited partnership but we are waiting on finalised regs to confirm as much. However, there are a couple of things that are holding that up, especially as it relates to this score. For one thing that bill hasn’t been implemented, the Corporate Transparency Act passed in January 2021, but there’s a tremendous amount of regulatory work to stand up the rules around that statute and the framework itself, as well as to stand up the infrastructure from a tech and digital information perspective to make sure that the law works as intended but at the same time, the US regulatory agency responsible for setting those rules up and that infrastructure up is horribly underfunded. And they’re being pulled in a lot of different directions. And that’s the Financial Crimes Enforcement Network at the Treasury Department, or FINCEN. They’ve been called into action in connection with the aggression towards Ukraine in helping coordinate international sanctions, including to discover who actually owns these entities. But it would be a lot easier to do that if these structural reforms had been in place a long time ago.

The last thing I’ll say is the president, he has emphasised these things. Uh, he’s actually identified a lot of core tenants that would both address the financial secrecy index score, but more importantly, actually create a more transparent regulatory environment in the US that would not only help to enforce sanctions, but also to help prevent the need for sanctions in the future, because it would undermine the abuse of Western financial systems by kleptocrats. Those reforms include standing up and implementing the Corporate Transparency Act, bringing greater transparency to US real estate markets on a nationwide permanent basis with respect to commercial and residential real estate, regulating the enablers who bring and shelter assets within our financial system, bringing transparency to private investment funds, an $11 trillion industry in the United States that has no ‘know your customer’ or beneficial ownership rules, which is shocking, that would be the third largest economy in the world, and it’s a black hole of secrecy and finally, covering other areas that have been developing and that are of concern, including relating to luxury assets, bringing transparency to art antiquities and digital assets, making sure that those, you know, emerging categories of harms from a money laundering perspective are pulled into the traditional, anti money laundering frameworks. We don’t need to reinvent the wheel. We just need to make sure that they’re covered. You know, right now the US is itself a tax haven, it’s one of the biggest secrecy jurisdictions in the world. These results confirm that, and it’s no longer time for the US to pretend that it can enact and create a less corrupt global environment and foster democracy without looking internally and cleaning up its own house and catching up with global norms..and, uh, making sure that it’s rhetoric is more than just talk. It’s time to walk the walk.”

Naomi: “Ryan Gurule of the FACT Coalition. Ok, let’s talk about the UK. As I’ve said, combined with all its satellite havens it’s still the worst offender even though taken alone it’s ranked number 13. Unlike the United States, there aren’t encouraging signs at all. Alex Cobham again of the Tax Justice Network:”

Alex: “Ah, you can, you can say that Britain is eating itself, you know, it’s slightly sad. You know, we’re sitting here as as two Brits and, you know, on the one hand look, I think the world is increasingly aware that the UK is the biggest driver of financial secrecy, of tax havenry. The UK is the UK. And I think, let’s come back at the next index and see where the UK is. The UK government at present is absolutely not committed to transparency in almost any dimension, whether that’s freedom of information requests from journalists or the public, or it’s transparency about public procurement and public contracts, or indeed a great many other things, including financial secrecy. They haven’t delivered, in fact they’ve, u-turned on a set of commitments that the predecessor, but still Conservative government made including around country by country reporting, and the UK’s corruption is becoming both more pervasive and more visible, which is what you’d expect with a country that sits at the centre of this spider’s web of secrecy. We know financial secrecy corrodes, and it corrodes in the secrecy jurisdiction as much as it does damage to others. The UK is responsible for very serious revenue losses for other countries, but it also suffers very serious revenue losses itself. It is increasingly finding it difficult to make progressive taxation effective because the tolerance of anonymous wealth and opaque corporate accounting is so high and it’s so embedded politically that we don’t regulate this stuff properly. And even if we pass the laws, we don’t enforce them. The cost now to the British society is becoming increasingly clear. There will be a moment in UK politics when people say ‘we have to try something else.”

Naomi: “Yeah. Yeah. I mean, it’s like a lost a lost nation at the moment, a pariah nation even, and there’s this ongoing race to the bottom going on between New York and London, which is, also you can throw into the mix, but speaking about how to tackle long term these problems, I mean the Tax Justice Network and, and other anti-corruption campaigners want a Global Asset Registry and a United Nations Tax Convention. I know these are big subjects, but, can you briefly explain how the global asset registry would work practically?”

Alex: “Sure. So, you know, we already have registries of a lot of assets, you know, so a lot of countries have a land registry that records, depending, either the legal owner or ideally the ultimate warm blooded beneficial owner. And then a lot of countries have that for companies and an increasing number of countries have that for trusts and foundations as well. Then if you look at kind of high value assets like yachts and private aircraft, you often have registers sometimes international of who the owners are. And then even thinking about works of art in some cases and other assets we see similar types of registers. Now, not all of them are perfect. Not all of them identify the beneficial owner or don’t do it entirely effectively, but there’s a lot of information there. Most of it public, some of it held privately that could be joined up. And that’s really what a global asset registry is. The idea that you could actually put together the company ownership register for all jurisdictions, and then the same for other types of assets, other types of legal vehicles. And you’d end up with an overall structure that let’s say law enforcement would be able – imagine, for example, that you wanted to sanction some very rich oligarch or, you know, some major criminal, you could look through the global asset registry and effectively see every element of their ownership, every structure and every ultimate asset, and that would allow you equally to do things like taxing wealth effectively, if you wanted to. Not all of the information would be in public domain, as it’s not now, some of it would be private, so I don’t think anyone’s saying we should have information about people’s financial accounts in the public domain, but where you’ve created a legal vehicle to do business, then that’s, I think generally held should be, should be a factor of public information. So you’d have both public and private elements, and it would basically be a tool for different types of, uh, law enforcement, but also civil society, journalists, and so on, for all of us to understand really the distribution of wealth in our countries and internationally. And if we wanted to decide to tax it, um, or at least if we’re not gonna tax it, to make that decision actively and with the power to do so and be choosing democratically not to, if that’s a choice that’s made. So it’s really about empowering people both to make sure that laws and taxes are applied fairly, but also to allow us to curtail inequalities.”

Naomi: “OK. And the UN Tax Convention? So important to enshrine tax rights in a legally enforceable way to protect citizens. That’s another longer term thing we’d like to see happen right?”

Alex: “Yeah. I mean, look, I’m not so sure it’s long term anymore. I think we’ve had a shift. There’s been a sense that you know, the OECD has actually had 10 years on corporate tax and it’s failed, you know, nobody, including the bigger OECD members, nobody is happy with what the OECD’s put on the table after 10 years of trying. That’s on the corporate tax side. Meanwhile, on the transparency side, you know, we have the Financial Action Task Force whose former long standing head has just come out and, you know, really ripped them apart and highlighted just how much they have failed to achieve things like beneficial ownership transparency among more than a, you know, a handful of members and how actually there’s a small group of major members who really control it, and stop it delivering high standards for everyone. We know the UN tax committee already has kind of delivered on digital taxation in a way that the OECD is failing. It’s kind of obvious that this stuff should be done at the UN.

My feeling is we might see negotiations on a convention begin within a year. It really feels, you know, we could be that close and there’s still a long way to go even if we get started. But I think there’s just this general sense that the architecture doesn’t work. It doesn’t work for lower income countries, in fact, it never has done, but even for OECD members, I think there’s a frustration that they’re not getting the kind of effective, uh, changes that they need. And something like the, you know, the failure of the G7 to be able to make sanctions effective in the case of Russia because of their own failure to be transparent, I think is shifting the dial on what might be acceptable as, as global standards. So, I feel pretty positive at the minute. I think it’s not such a long term ambition after all.”

Naomi: “And very interestingly, just in a short time since I spoke to Alex, the African Union has just passed a resolution calling on the UN for a tax convention. Alex, I’m cheered to see that the financial secrecy index 2022 finds that global financial secrecy actually shrank by 5%, so it is going down. But, once you factor in the G7 countries I mentioned earlier, they increased their secrecy services by so much it whittled that global percentage down to 2%. But there is an ongoing reduction, which is encouraging, even though in the last index it was down by 7%. I know that enforcement is a whole other question, but the secrecy space is being squeezed and it’s a very important ongoing shift right?”

Alex: “Yeah, absolutely. You could say the continuing improvement in global transparency is really a reflection of the kind of the normalisation of the tax justice policy platform. There is much more automatic exchange of information about financial accounts, there is much more transparency of beneficial ownership, and there is continuing progress towards country by country reporting being transparent, there’s a lot of progress being made. So we should feel pretty positive stuff is being delivered in legislation, but it’s also being delivered in practice. The fact that the G7 as a group is dragging the needle back the wrong way is a definite cause for concern. But that global trajectory is positive. And it feels like the momentum will continue.”

Naomi: “So, I’ve given you just some of the highlights here, there’s so much more to discover. There are 141 countries in the index, find out about your country on fsi.taxjustice.net. That’s it for now from the Taxcast. Thanks for listening, we’ll be back next month. Bye for now.”

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa:

Estados Unidos se convierte en el primer proveedor de secreto financiero a nivel global.

EL camino a la Transparencia financiera para América Latina

En nuestro tercer capitulo de qué son los paraísos fiscales, sus grandes protagonistas, las miultinacionales.

Y ¿por qué Londres es el mayordomo mundial del dinero sucio?

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Pour cette 39ème édition de votre podcast francophone produit par the Tax Justice Network, nous partageons avec vous une partie des échanges qui ont eu lieu lors de la diffusion par TaxEd Alliance des notes d’informations sur l’état de la mobilisation des ressources fiscales au profit de l’éducation. Deux pays africains ont fait partie de l’analyse de référence, à savoir le Sénégal et la Zambie. Nous vous proposons de suivre la réaction d’un membre du Forum Civil, une organisation leader de la société civile sénégalaise.

Dans cette édition, nous revenons aussi sur l’indice d’opacité financière qui est en cours de finalisation, avec un jeu de question réponses, pour comprendre comment le lire. Aussi, nous parlons de l’accord fiscal international de l’OCDE, dont la mise en œuvre est menacée par de nombreux points de désaccord.

Pour écouter le lancement officiel des notes d’information de TaxEd Alliance, cliquer ici.

~ Financement de l’Education: Quel justice fiscale pour l’Afrique? #39

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le sous ce lien.

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to the 53rd edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

الإعلان عن إفلاس لبنان: أين الحقيقة؟

في العدد #53 من الجباية ببساطة نستضيف الخبير في التنمية الإقتصادية هاني السلموني لتحليل خبر إفلاس لبنان بعد إعلانه من طرف نائب رئيس الوزراء اللبناني سعادة الشامي قبل نفيه من رئيس الوزراء نجيب الميقاتي الذي صنفته مجلة فوربس مع شقيقه طه كواحد من أكبر اثرياء المنطقة العربية في مفارقة صارخة مع تدهور الوضع الإقتصادي اللبناني.

هل يمكن للحكومة اللبنانية التوصل الي حلول لتفادي الافلاس؟ وهل يساهم الإتفاق مع صندوق النقد الدولي حول برنامج تمويل جديد في إخراج لبنان من ازمتها؟

أسئلة نطرحها على ضريفنا د. هاني السلموني.

In episode #53 of “Taxes simply” we provide a recap of the key economic events globally and in the Arab region in April 2022. We then speak with Dr. Hany El Salamony, an expert in economic development who discusses the latest developments in Lebanon and the news of the country going bankrupt, while the country’s Prime Minister is named one of wealthiest Arabs on the Forbes list for the richest Arabs in 2022. Can the Lebanese government find a way to avoid going bankrupt? Can the agreement with the IMF for a new loan help mitigate Lebanon’s crisis? These are some of the questions we’ll discuss with our guest.

Sobe o preço do barril de petróleo, sobem os custos de produção e os preços de quase tudo para os consumidores finais, trabalhadores e trabalhadoras. O É da sua conta #36 é sobre essa maldição e como se livrar dela.

Cloviomar Cararine e Juliane Furno explicam como acontece a formação do preço do petróleo e de seus derivados no Brasil e no mundo, o peso da pandemia de covid-19 e da guerra na Ucrânia nessa dinâmica, como as empresas petroleiras se beneficiam desse cenário e os impactos sobre a inflação. Suzana Ruiz e Juliane apontam também as medidas de justiça fiscal que podem ser tomadas para minimizar esse problema global.

Ouça no É da sua conta #36

A inflação dos derivados de petróleo no Brasil e por que o petróleo produzido pela Petrobras acompanha o valor do produto no mercado internacional.

Os fatores que influenciam a formação do preço do barril de petróleo no mundo.

Empresas de energia e do setor petrolífero recebem subsídios governamentais. Isso é necessário?

É possível reduzir a dependência do petróleo, a exemplo de países que já fizeram a transição para fontes de energias renováveis?

Taxação de lucros extraordinários das empresas petroleiras como medida complementar para combater os efeitos da inflação dos derivados do petróleo.

Call to action: justiça fiscal como forma de combater os efeitos da inflação, reduzir desigualdades e fazer a humanidade se livrar da maldição do petróleo.

O combusivel está subindo adoidado. No dia 8 de abril o álcool estava R$ 4,60. No dia 11 custava R$4,80 e no dia 14 já estava 5,10 em alguns postos.”

~ Umberto Stefano, aposentado

A população brasileira hoje paga por um preço de um produto que ela produz e que vem reduzindo seu custo de produção, mas não conseguimos absorver esse ganho, que se reflete no aumento no lucro das empresas de petróleo e no pagamento de dividendos a seus acionistas.”

~ Cloviomar Cararine, economista do Dieese

Hoje em dia o fenômeno da financeirização impacta muito a precificação do barril de petróleo no mercado internacional. Nesse sistema há comercialização futura de barris de petróleo com um tempo bastante alargado. As expectativas sobre a produção futura e a especulação [sobre a variação de preços do barril] têm o poder de determinar o preço no presente.”

~ Juliane Furno, economista-chefe do Instituto para Reforma das Relações entre Estado e Empresa

Podemos aplicar uma taxa adcional a empresas energéticas que tiveram um crescimento muito alto e inesperado de seus resultados empresariais por causa da guerra na Ucrânia. Esses recursos podem ser usados para baixar as contas de energia ou investir em programas sociais —uma espécie de renda básica universal — para famílias que mais sofrem com os atuais efeitos inflacionários.”

~ Susana Ruiz, coordenadora de justiça fiscal da Oxfam Internacional

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

In this Taxcast episode we ask – do politicians believe in the societies they serve or not? Are they really a part of them, or do they live in a parallel world with different rules to ordinary people? The so-called ‘NonDom’ scandal goes all the way to Downing Street, the heart of the British government and the UK Chancellor/Finance Minister whose wife is taking advantage of an archaic tax status that leads to reduced taxes on her inherited fortune – just as her husband raises taxes on everyone else.

Transcript of the podcast (some is automated), you can read a summary of the Taxcast below.

What we see is that we have a regime that explicitly encourages people not to bring their money onshore. And there are lots of other things in the system that need fixing.How does one get reform of these kinds on the agenda?“

The nondom rule epitomises the sense of fracture of the social contract and the gradual erosion of commitment to democracy. And that’s why we need this whole new set of governing principles to re-establish some sense of a social contract here in Europe and elsewhere in the world where similar tax breaks have been given to the super rich.”

Taxcast interview with journalist and anti-corruption campaigner in Pakistan, Umar Cheema, on his inspirational achievement in making Pakistan only the fourth country in the world to publish the tax returns of its Parliamentarians.

Summary of this month’s epsidoe of the Taxcast, with Naomi Fowler:

“We have oligarchs behaving badly, governments behaving badly – this time, the scandal goes all the way to Downing Street, the heart of the British government and the UK Chancellor – the Finance Minister – & his wife’s extraordinary wealth. We all knew she had enormous inherited wealth – £11.5 million a year in dividends from her stake in her father’s IT business, based in India. But it turns out she opted to minimise her taxes using an archaic status to do so – she’s a nondom. So, what is a non-dom?

‘Non-dom’ status refers to a person who is not domiciled in the UK. That doesn’t mean they don’t live in the UK, it means that if one of their parents was born overseas they can choose to claim this status – which saves them lots of tax. The UK Finance Minister’s wife could well be avoiding 2 to 5 million a year in taxes because of the nondom status she’s opted for. Unlike most UK residents, nondoms don’t pay UK tax on their worldwide income and capital gains. (If you’ve got any worldwide income!)

The outrage of even this Conservative MP in this Parliamentary Committee hearing pretty much sums up the anger of voters – bear in mind it’s his party’s Finance Minister’s wife – just as her husband is currently raising taxes on the poorest people especially, as they face a cost of living crisis:”

“I mean it’s extraordinary, frankly. And you wonder why people –“

“It’s a policy issue –“

“Yeah, I know it’s a policy issue and it’s nothing to do with you, you’re just the bloke in charge, I realise that, but in all honesty you’re surprised that people think there’s one set of rules for rich people and one set of rules for someone else, when you’ve just told us that that’s exactly what there is!”

Naomi: “Not only that but both the Finance Minister and his wealthy wife “pledged permanent residence” to the United States as “Green Card” holders, while he was a Member of Parliament and Finance Minister. I mean, we can legitimately ask – do politicians and their families believe in the societies they serve – or not? Are they a part of it? Or not? So far in the UK, only 5 of the 22 cabinet ministers are willing to confirm publicly whether they or their families benefit either from offshore holdings or from non dom status. Back in 2015 I interviewed the amazing, award winning journalist and tax justice campaigner from Pakistan, Umar Cheema. We spoke about his inspirational achievement in making Pakistan only the fourth country in the world to publish the tax returns of its Parliamentarians. This is what he told me at the time:”

Umar Cheema: “Interestingly, a senior Finance Ministry official told me that when the government of Pakistan decided to make tax data public, they got to hear from the UK authorities that now we will come under pressure to do the same in the UK. I don’t know when they do, but one should hope for the best and the Tax Justice Network must use the example of Pakistan for pressuring the authorities in London.”

Naomi: “Ha! Britain today, and many other nations are still light years away from following Pakistan’s example and putting the tax affairs of their elected representatives into the spotlight. I’m going to speak with one of the co-authors of a new report which for the first time, unmasks the kind of people who are using this archaic non dom status in the UK – they released their report just as the scandal about the finance minster’s wife broke, happy timing to get major attention on to something fundamentally unjust. But first I’m going to speak with economist John Christensen.”

Naomi: “OK John, nondom status is something we’ve spoken about quite a few times on the Taxcast and as is so often the case with these things this is yet another example of how oligarchs behave, and we can apply that term to all the super rich, it doesn’t just apply to Russians – they just live in a parallel universe where taxation applied to ordinary people doesn’t apply to them, and borders don’t apply to them. Now it looks like the UK finance minister’s wife, the chancellor’s wife has pretty much damaged her husband’s political career because there’s a lot of anger from ordinary people about the hypocrisy of tax minimisation by the family of the man who’s setting our tax policy in the UK and has done absolutely nothing to help citizens in the cost of living crisis they face. She’s now said she’ll pay tax voluntarily in the UK. And it’s important to make clear that she can say hand on heart, that she’s paying all taxes that are due completely legally, partly through her non dom status, but also interestingly, she’s got the payouts on her huge inherited wealth routed..through the tax haven of Mauritius, so she’s likely to be paying zero tax there, and this is very much what we call unearned income, so that’s a thing that’s so undertaxed compared to what we all work to earn.”

John: “Yeah, so look, we’ve discussed the non dom rules many times, and we’ve also campaigned for its abolition, but bear in mind the following: firstly, domicile has nothing to do with citizenship. You can hold an Indian passport as Ms. Murthy does, but live and work in London and pay UK taxes on your income. Secondly, being non domicile is a personal choice. You actually need to apply to her Majesty’s revenue and customs to be deemed to be non domiciled in the UK. And equally, if you want to pay taxes in the UK in the same way as the vast majority of ordinary people do, then you can give up your non dom status and you can do this without in any way undermining your Indian citizenship. And thirdly, when Ms Murthy’s spokesperson claims as they did that, she has been paying all the taxes used legally liable to pay, this statement needs to be unbundled very carefully, indeed, because it is almost certain that most people won’t understand the implications of being of what is being said, because most people are used to being taxed on pay as you earn basis, and they don’t receive unearned income from wealth held in an offshore holding company! So, in light of the scandal that blew up especially after her husband went ahead with increasing the national insurance contribution rates, which apply to most workers, Ms. Murthy has reportedly chosen to give up her nondom status and will henceforth be paying UK tax on all her worldwide income. But unfortunately for her and for her husband, the reputational harm caused when her non dom status was revealed is probably irreversible and her husband’s long held ambition to be prime minister of the United Kingdom has probably been hulled below the waterline. That’s because if there’s something the wider public really hate, it’s the notion that there’s one rule for super rich people and another rule entirely for ordinary people.”

Naomi: “Yeah. And especially while he was raising taxes on everybody else!”

John: “Yeah.”

Naomi: “So, the UK’s kind of really archaic nondom status has influenced other nations, I mean, Italy, where I am at the moment, they introduced something that was inspired by the UK, just as, at the same time political opposition in the UK did actually persuade the government to scale it back a bit. Um, and I do mean a bit, uh, because they put a 15 year time limit on it and they made it more expensive after a while, so the cost of 30,000 pounds a year fee, which is over 37 and a half thousand dollars a year to 60,000 pounds a year, and that’s about $75,000 a year. Um, again, more than most of us earn in a full year, so it’s obviously well worth it for these nondoms, um, and tax havens elsewhere also have all kinds of unjustifiable assorted advantages, and really all of this means that we must redefine the principles that should govern us all equally, right?”

John: “Oh, absolutely because you see, the nondom rule and the equivalent rules in many other countries come out of a particular ideology, a tax haven ideology, and it’s worth just to look at that ideology and understand why politicians think it’s worthwhile targeting tax breaks at the super rich people. The argument goes that super rich people are super mobile. They can choose to locate themselves anywhere Monaco one month, Palm Beach the next, they choose to locate their financial assets and their wealth anywhere, Cayman islands, Mauritius, wherever. So paying tax for the super rich is entirely a voluntary matter. There’s a perceptible public sense that the rules essentially the tax rules are biased to the interests of the very wealthiest people in society and the wider public, especially in Britain, but I think the same can be said in Italy and in France, are paying high levels of tax whilst receiving increasingly poor quality of public services. So the nondom rule, as far as I’m concerned, epitomises the sense of fracture of the social contract and the gradual erosion of people’s commitment to democracy. And that’s why we need this whole new set of governing principles to re-establish some sense of a social contract here in Europe and elsewhere in the world where similar tax breaks have been given to the super rich.”

Naomi: “Yeah. And what – definitely – and what governments everywhere always say to justify these kinds of privileges for the very wealthy is it encourages investment. And, uh, I’m gonna speak in a minute to the co-author of a really important report on nondom status about how much that really is a load of nonsense, but when it comes to the term investment, that’s a really, really tricky word, isn’t it? Because actually, well, it’s worthy of an entire Taxcast in itself, which is something I’ve intended to do for a while.”

John: “Yeah, well, the word investment as far as I’m concerned, it’s just a catch-all word used by lazy economists and politicians to confuse the public and obfuscate. As far as I’m concerned, much of what is termed investment, particularly inward investment doesn’t flow into new facilities or researching new technologies. Instead it goes into acquiring or merging with existing businesses, often leading to job cuts and often consolidating the market power of major companies, who might already have monopolistic powers in that market. So, yeah, absolutely, let’s go ahead, let’s have that edition of the Taxcast, let’s discuss this matter because we need to bring pressure to bear on the economists and national statisticians who provide the data on so-called investments, which we need to have a much better understanding of whether all these tax breaks to super rich people are actually leading to real investment in new jobs and new ideas and new services. Are they actually helping just the super rich and everyone apart from the super rich find their situation being eroded by the lack of investment into new wealth creating activities?”

Naomi: “Thanks John! Economist John Christensen. Now it’s time for the Taxcast special feature. The UK’s ‘non-doms’: Who are they, what do they do, and where do they live? What does it tell us about wealth and fairness? Now we have a new report just out – for the first time the data on nondoms has been mined by a team of economists and data specialists. We now have a picture of the UK’s ‘non-doms’ – these are people who are paying a nondom fee from £30,000 to £60,000 a year – that’s more than most of us earn in an entire year. It helps us definitively answer the question – what is the point of nondom status? Who does it serve? I’m speaking to Arun Advani of the University of Warwick, one of the report’s authors. So, hi Arun, so the most obvious question is how do you get non dom status?”

Arun: “You’re non dom just as a fact of your existence so you either are, or aren’t a non dom and that just is a function of whether your permanent home is the UK or not the UK. So if you were born here, brought up here to a British parent and you expect to live here the rest of your life, you’re a UK domiciled person. This, this is your permanent home. If however, you come from another country and you intend potentially to go back there, then you would be a non dom, and that will apply to, you know, many, many people.

Then there’s the separate question that’s been coming up recently which is about whether you are sort of a non-dom for tax purposes and this is really a question about whether you choose to tick a box on the tax form that says, ‘I wish to benefit from the remittance basis,’ which is a particular status that you get if you’re a non dom. So if you’re a UK Dom, you don’t have the option of that box, but if you’re a non dom, you can tick that box and ticking that box says, ‘I don’t have to declare or pay tax on foreign investment income until such time as I bring that income into the UK. And if I never bring that income into the UK, then I will never pay tax on that income.’ And so that’s kind of what all the recent debate has been about has been about, has been there are people who tick a box on the tax form that gives them this particular benefit that says, ‘if I keep my income from investments offshore, I won’t have to be paying tax on it in the UK. And potentially I may not be paying tax on it anywhere in the world.’”

Naomi: “Right, it’s the first time that the data on non doms has been analysed like this in, in Britain, so I, I just wanted to ask you, if you can describe the data that you’ve had access to, the data you used and why you wanted to do this?”

Arun: “So the data that we are using is from the UK tax authority, we go and sit in a secured room in the what’s called the data lab in her majesty revenue and customs and sitting in that secure room where we have no access to our phones or computers or anything else, uh, of our own computers. We can use a secured set of computers that give us access to completely anonymised data. So I can’t see anything about individuals in their personal capacities, their names or dates of birth or anything like that, but I can see anonymised data on all of the details you’d basically see on the tax form so I can see what they filed as their level of income and what all of those, like sub-components on different boxes of the tax form are. So that’s what we can see.”

Naomi: “And why did you want to analyse this data?”