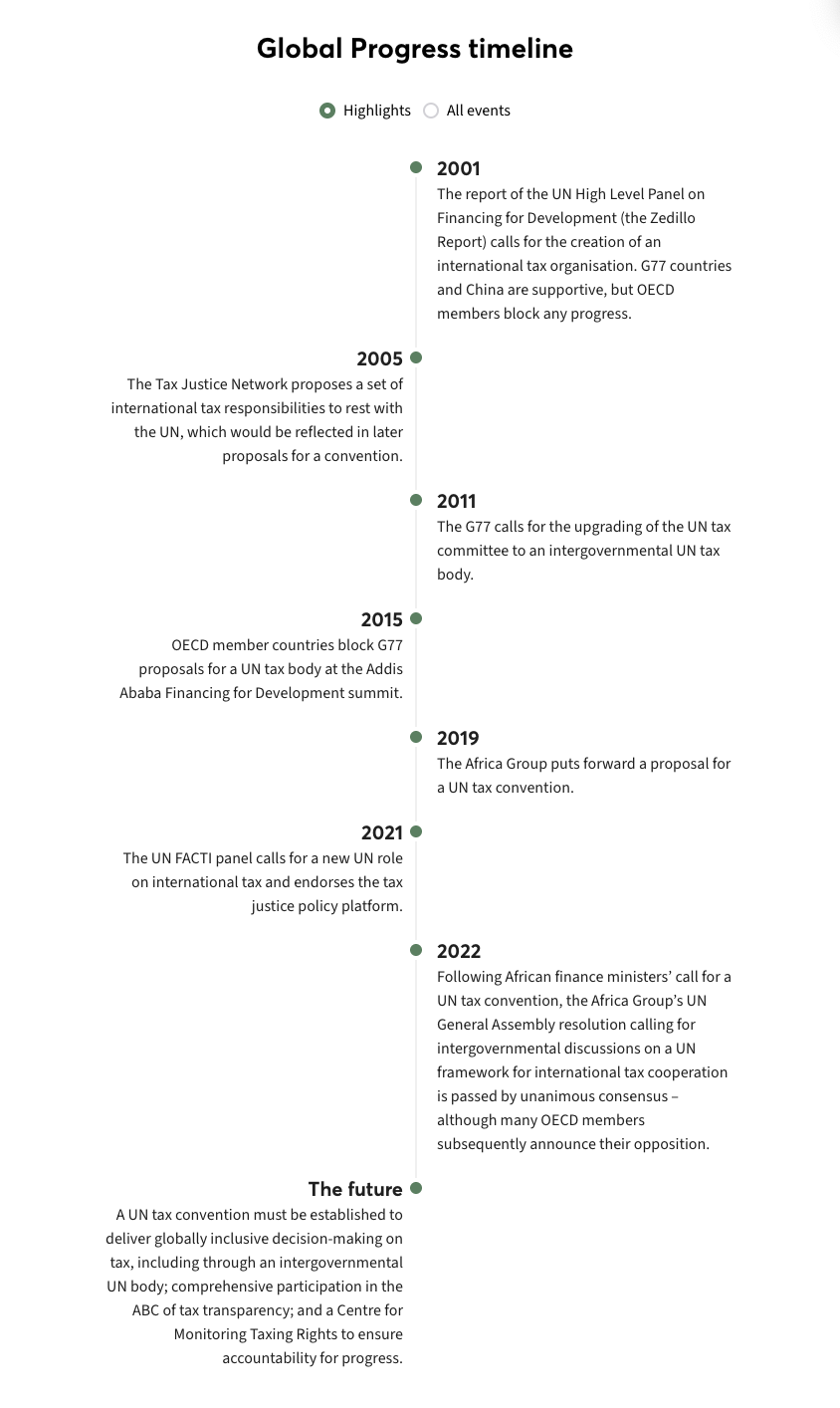

This year marked 20 years since the formal launch of the Tax Justice Network.

As part of our 20 year anniversary, we tasked On Think Tanks to conduct an evaluation of the impact we have had, the difference our research and activism have made, the policy changes we contributed to, and the broader benefit from our wins (and failures!) over the past 2 decades. The study by OTT presented an assessment of the Tax Justice Network’s 20-year history that highlighted our significant impacts in the tax justice space. The assessment highlighted how:

The Tax Justice Network places a strong emphasis on evidence-based outputs and advocacy, which are fundamental pathways towards sustainability, professionalism, and impact.

The Tax Justice Network has emerged as an accessible resource for media outlets, development organisations, government institutions, and grassroots movements seeking to interpret, substantiate, and assess arguments in the realm of tax justice, with the scope and reach of our media coverage having increased over the years.

The journey towards a UN tax convention has been significantly underpinned by arguments and evidence put forth by the Tax Justice Network, providing an important part of the empirical basis to substantiate the arguments for a revolutionary governance shift.

The Tax Justice Network has catalysed the movement through two primary channels. One avenue is diffusion, where staff or associates draw inspiration from the Tax Justice Network and establish their own tax justice initiatives or research agenda. The other involves providing support and convening global meetings primarily led by leaders from the global south and shaped by their agenda.

As in the two decades before, this work continued throughout 2023: deepening and expanding our research, analysis and advocacy, to secure narrative shifts, and bring about systemic change to challenge tax injustice.

Flagship publications and tools

Our work again reflected the impact that weak global tax policies are having, with countries being on course to lose US$4.8 trillion in tax to tax havens over the next 10 years. $311 billion of tax lost annually is lost to cross-border corporate tax abuse by multinational corporations and $169 billion is lost to offshore tax abuse by wealthy individuals. Lower income countries, which have historically had little to no say on global tax rules, continue to be hit harder by global tax abuse, with their tax losses of $47 billion being equivalent to half of their public health budgets.

Alongside work on our State of Tax Justice report, we also announced changes we’re working on in respect to the way we publish our Financial Secrecy Index and Corporate Tax Haven Index. The changes involve switching to sequential, rolling updates of partial sets of indicators, instead of large-scale updates of each of the indexes as a whole. This is intended to make the indexes more robust and impactful (while at the same time allowing for a more balanced spread of our workload.)

Importantly, 2023 also saw the launching of two new tools: our Data Portal, and the Tax Justice Policy Tracker.

Our Data Portal provides a convenient way for researchers, journalists, activists and the wider public to explore, download and use data produced by the Tax Justice Network and selected data from other sources. With the data portal, we aim to provide a one-stop-shop for anyone interested in working with indicators of tax havens and financial secrecy.

The second new tool we launched in 2023 is the Tax Justice Policy Tracker, which monitors and promotes progress on nine key policies that are important for reprogramming our tax systems for the better. The tracker grades each country’s laws on how well the country is implementing each of the nine policies, helping governments spot where they can improve. The tracker also reports each country’s public position on each of the policies. We kicked off the beta version of the tracker with one live-tracked policy, the UN tax convention, because this is the most critical question facing policymakers internationally today. The next policies will be incorporated gradually in the coming years.

Research

Over the course of 2023 we finalised a study that estimated the potential impact of a wealth tax in EU countries; closely followed and analysed the EU’s BEFIT proposal for corporate tax reform; assessed the impact of offshore leaks on bank deposits in tax havens; analysed country by country reporting data on profit shifting in Slovakia; worked on developing a conceptual framework for indicators of tax havens and secrecy jurisdictions and quantifying corporate profit misalignment at the company level; finalised a study on VAT fraud in collaboration with ECORYS; and worked on a research paper that develops a methodology to illicit financial flows using a bilateral gravity model. We also collaborated with government authorities around the world (eg Uganda, Nigeria, Slovakia, Ghana, and others) to analyse detailed administrative data and to provide granular policy recommendations for mitigating illicit financial flows.

Beneficial ownership

We have long advocated for the transparency of beneficial ownership information. Over the course of 2023 we conducted a review of the state of play of beneficial ownership in Latin America and Africa. We also provided extensive input into the Financial Action Task Force’s Recommendation 25 on beneficial ownership transparency for legal arrangements; looked at 30 uses for beneficial ownership beyond money laundering; and discussed the 10 targets every country’s beneficial ownership strategy should meet. Not surprisingly, our analysis also showed how the split among EU countries in respect of beneficial ownership mirrored their rankings on the Financial Secrecy Index. Our advocacy efforts were wrapped up with various workshops, training sessions and webinars on beneficial ownership.

Importantly, 2023 also saw the launching of our roadmap to beneficial ownership transparency (REBOT), offering a graduated framework with a series of steps governments can take on the road to achieving transparency.

We have also been actively participating in various fora around the world, from the IMF and World Bank spring meetings; testifying at parliamentary subcommittees; and moderating panels at conferences – all around securing greater transparency in global financial systems.

Country by country reporting

This year saw our first country by country reporting webinar, focusing on the legislative process to explain the nature and politics of public country by country reporting by multinational companies in Europe, the United States, the United Kingdom and Australia. Policy changes secured by partners active in each location will begin to yield fruit in new public reporting requirements that kick in during 2024, as the shift to full transparency appears increasingly inevitable – while remaining a major struggle against the defenders of tax opacity.

Tying climate justice to our advocacy work on beneficial ownership, we also explored the link between beneficial ownership and climate crimes in the fishing industry in particular; and lifted the lid on who benefits from opacity in beneficial ownership in the fossil fuel industry.

This work on climate justice is rolling over into 2024, with our March 2024 Paris conference that will be focusing on historic global emissions and centile-level climate reparations.

Enforcement by well-resourced and independent tax authorities

Our illicit financial flows analysis has been finding application on a practical level with work being done to help various government authorities to analyse microeconomic data (at the entity- or transaction-level) to identify illicit financial flows and to effectively design mitigatory policies. In 2023 this included identifying illicit financial flows using customs data; and analysing micro-level data on intra-group transactions of multinationals to identify companies to audit and to estimate the scale of profit shifting.

Human rights

One of our primary objectives has been in articulating the impact that tax injustice has on the ability to secure and fund fundamental human rights. We continued to work on research collaborations with the Government Revenue and Development Estimation tool (GRADE) at St. Andrews University, exploring and illustrating the pervasive impact of tax abuse on rights to health, education and on climate justice.

Over the course of the year our human rights advocacy work also included making a number of submissions to UN special rapporteurs: on the importance of freedom of expression in sustainable development; the effects of foreign debt and human rights in Liechtenstein and the Bahamas; and fiscal legitimacy through human rights. As part of the Tax Ed Alliance – a network of global organisations advocating for transforming financing of public education – we are contributing to the development of a taskforce on tax justice and the right to education; and have been working on capacity building with the Global Campaign for Education on the UN Tax Convention and the effects on education financing.

Aside from this deeper focus on education, we have also expanded our work into exposing the effects of racism in tax systems and human rights; worked on a short documentary video and brief for the Demotrans EU consortium project on Ireland and Kenya’s lack of incorporation of taxation into their Business and Human Rights Action Plans; presented a webinar with more than 20 grassroots women’s organisations in Brazil; and provided expertise in support of the Global Alliance for Tax Justice Tax & Gender Working Group’s strategy and theory of change for a ‘feminist global, regional and national tax system that resources the full realisation of women’s human rights’.

We also worked with a range of human rights and economic justice partners to deepen analysis of the colonial nature of OECD dominance over international tax rule-setting; and participated in an Expert Group Meeting on the Accountability of Powerful Private Actors in Global Health convened by the UNU-IIGH. The inaugural meeting invited academics working on global public health and a small number of civil society organisations to consider collaborative responses to the threat posed by unaccountable actors in the sphere, including through unchallenged tax abuse.

Reaching people

Our monthly Tax Justice Network podcastscontinue to go from strength to strength. Completely separate productions in English, Spanish, Arabic, French and Portuguese, they are available on the dedicated thetaxcast.com website and on most podcast apps. In 2024 we will be rebranding all our podcasts, and are also planning a new India/Pakistan podcast and hope to launch a Small Island Nation podcast.

We are launching a new weekly Tax Justice Network podcast series starting in January 2024, called The Corruption Diaries. It’ll take listeners on a journey through the eyes of anti-corruption veterans, with perspectives on reform and key historical events you won’t hear anywhere else! In the first series we sit down with one of the heroes of tax justice over decades, leading white collar crime lawyer Jack Blum who tells us about his life’s work. You can search on your favourite podcast app for The Corruption Diaries and subscribe there, or find it here.

In addition to ongoing coverage of our flagship materials like the indices and our State of Tax Justice report, our letter to King Charles III prior to his coronation drew media attention to the role of the UK and its network in global tax abuse, as well as linking to the historic injustices behind the UK’s wealth. This builds on our continuing work to highlight the role of tax as a tool of colonial extraction, and also the scope for tax to play a significant role in necessary reparations and ongoing redistribution.

Over the course of 2023, we published 119 blogs (and still counting!). Alongside this, our work featured in more than 314 broadcasts, 2,745 online media mentions, and 246 print pieces in over 140 countries. In July alone, when we published the State of Tax Justice report, our research was covered in 602 articles with a reach of over 5 billion. Over 300,400 sessions occurred on the Tax Justice Network website and our social media posts on Twitter, Facebook and LinkedIn had a combined reach of over 1,545,958.

A changing landscape more than 2 decades in the making

No roundup would be complete without mentioning the significant shift in global tax policy development that 2023 brought with it.

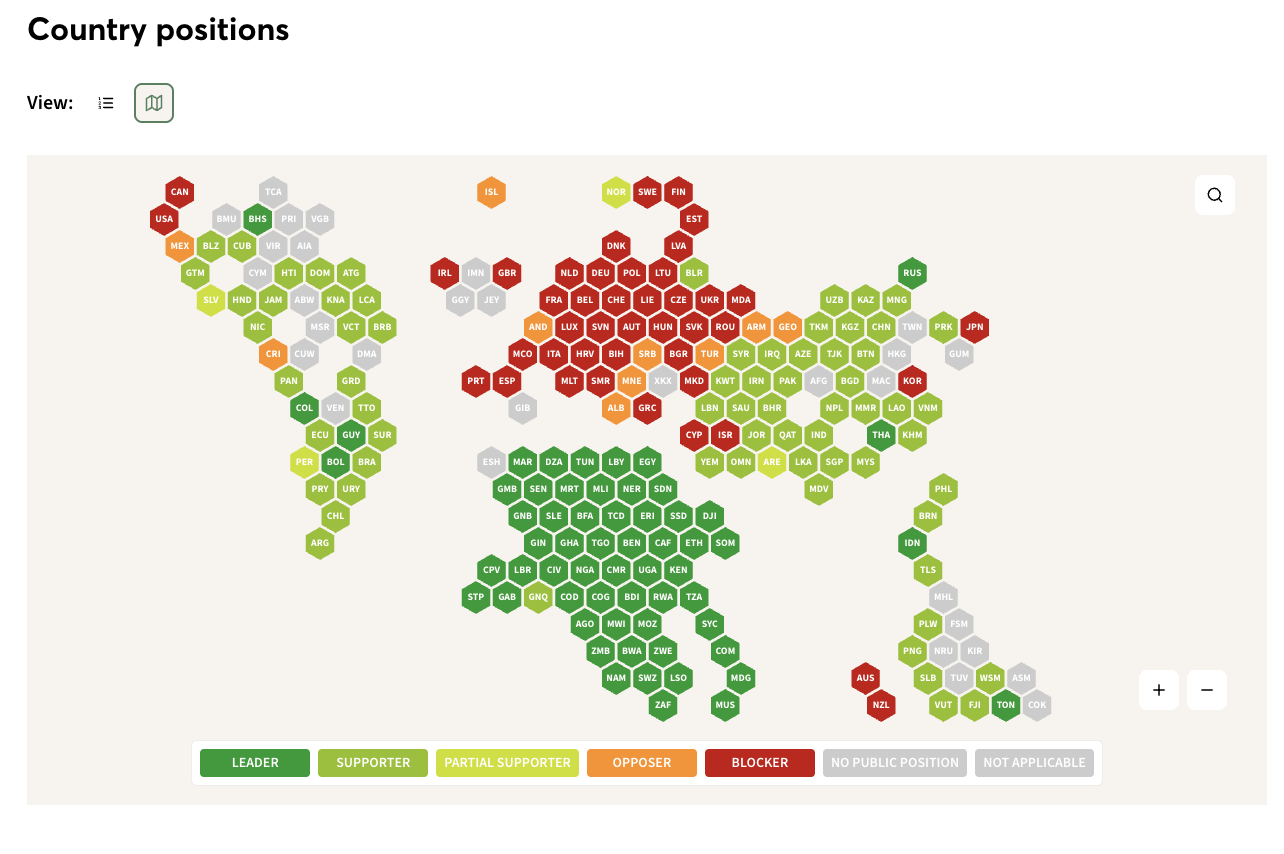

We have long advocated for a more representative, more transparent, and more responsive platform for the development of global tax policy. In November 2023, an overwhelming majority of countries took historic action towards making this a reality. Countries at the UN adopted by a landslide majority a resolution to begin the process of establishing a framework convention on tax, to completely change how global tax rules are decided. The success of the resolution despite the resistance from the world’s strongest economies is a rare feat, and demonstrates the overwhelming demand from countries outside the OECD for the meaningful voice on global tax rules which they have historically been denied.

While this vote was the focus of collective advocacy, important groundwork was also happening elsewhere. Our team members were heavily engaged in the Latin America Summit in Cartagena (working closely both with Ministerial officials in the region, civil society, and UN human rights officials) using Tax Justice Network tools and data to press home the importance of the shift of tax governance to the United Nations. A specific outcome of the Cartagena Summit was the establishment of a Platform on Tax which is chaired by the Colombian Government; and an invitation to join a dialogue with the Chilean Minister of Foreign Affairs, the UN High Commissioner on Human Rights, the UN office coordinator in Chile and the new member of the Committee on Economic, Social and Cultural Rights with a view to keeping the momentum going on truly securing global tax policy development.

The vote marked a turning point, and sets us on an exciting new course in 2024 and beyond, in pursuit of tax justice!

Looking ahead to the next 20 years, we also published our new strategic framework – beyond20. This was important, because – while the last two decades have seen some transformative steps forward – the world remains characterised by pervasive tax injustice. Our policy platform to curb this is summarised as the ABC DEFG₃ of tax justice:

The DE of domestic measures to ensure transparency results in effective accountability (Disclosure of sufficient public data, and Enforcement by well-resourced and operationally independent tax authorities);

The FG₂ of international elements (Formulary apportionment with unitary taxation, to end corporate tax abuse by ensuring that profits are taxed in the location of the real, underlying economic activity; Governance reform, centred on the establishment of a genuinely, globally inclusive process for the setting of tax rules and standards, under UN auspices; and a Global asset register (GAR), to connect and broaden the range of beneficial ownership registers across all legal vehicles and high-value assets, across jurisdictions, to provide a critical tool against abuse of tax, regulations and sanctions); and

G₃, Good taxes – a catch-all covering a progressive and effective overall tax system, and significant individual components of the tax justice agenda including wealth taxes, climate-related tax measures, excess profits taxes and minimum effective tax rates.

Global governance changes are crucial to the prospects of delivering policy changes in each area that can finally curb the scale of tax abuse, and address the global inequalities in taxing rights. Our 20th anniversary year was a good one, that has laid the groundwork for even more ground-breaking, paradigm-shifting work in 2024. We’ll see you there!

The holiday season is upon us, which for the millions of dust-covered board games that have spent the year hibernating in cupboards and cabinets means making the annual pilgrimage to the family dinner table to collect the biscuit crumbs and greasy finger stains they need to sustain themselves for another a year.

In honour of the annual cardboard migration, we’ve created the ‘Tax Dodgers Rules’ that you can play with using your own copy of a monopoly game. Cheat your way to extreme wealth and (hopefully) learn about how the rich and powerful abuse tax and hide their wealth from the rule of law. You can buy secrecy layers to hide your money from the players you owe money to and avoid paying tax. And you can establish beneficial ownership registers to expose your opponents’ secrecy layers. But be careful, there’s only so much wealth you can hoard for yourself before society collapses – and all players lose.

Of course, our suggestion is just to have some fun, and is nothing to do with the game Monopoly itself. The publishers of Monopoly have in no way endorsed this. Mind you, we’d like to think that Lizzie Magie – the original game designer, when it was first called The Landlord’s Game – might well have appreciated what we’re doing here. Magie was a feminist and a Georgist (a follower of Henry George, who had some interesting ideas about tax), and the point of the game was to make the case for land value taxes.

Here are the rules below (you can download these as a PDF – or as a word doc with working links). You can also download the printable ‘Tax cards’here, which you’ll need for the game. Have fun!

Download the rules as a PDF. Download the printable ‘Tax cards’.

A falta de transparência, a falta de abertura para participação social, as tentativas de suborno e corrupção, as brechas na legislação, além de algumas dificuldades bem visíveis, como a falta de equipamentos ou pessoal suficiente….

Como nossos heróis e heroínas invisíveis se preparam para enfrentar os desafios da administração tributária?

Esse é o tema do episódio #56 do É da Sua Conta, especial de fim de ano e em homenagem a auditores e auditoras fiscais das administrações tributárias do Brasil e dos países africanos lusófonos.

Qual o perfil ideal para trabalhar na administração tributária? Seleção, formação inicial e capacitação durante a carreira de auditoras e auditores com Márcio Verdi (CIAT).

Cabo Verde, Angola, Guiné Bissau e São Tomé e Princípe: os desafios dos profissionais da tributação nos países lusoafricanos, com Clair Hickman.

Fim da Escola Nacional de Administração Fazendária (ESAF), greve e falta de condições de trabalho: o que ocorre na Receita Federal? O Isac Falcão (Sindifisco Nacional) responde.

Justiça fiscal como princípio norteador da formação de nossos heróis e heroínas, com Florencia Lorenzo (Tax Justice Network).

“Defendo que deve sempre haver uma formação inicial. Por melhor formada que a pessoa venha, ela precisa ainda entender, por exemplo, dos aspectos éticos, morais e código de conduta.” ~ Márcio Verdi, secretário executivo do CIAT

“Quando o servidor da administração tributária ingressa através de um processo seletivo transparente, com provas e título, faz uma melhora sensível no corpo funcional, e depois, inclusive, no oferecimento do serviço público daquela instituição para a sociedade.” ~ Clair Hickman, consultora para administrações tributárias em países lusoafricanos

“Quando o presidente (Lula) falou que é preciso colocar o rico no Imposto de Renda, não é que o rico ia pular pra dentro do Imposto de Renda, precisa de uma administração tributária pra fazer isso.” ~ Isac Falcão, presidente do Sindifisco Nacional

“Um sistema tributário que foca naqueles que têm maior capacidade contributiva, é também um sistema mais eficaz.” ~ Florencia Lorenzo, Tax Justice Network

Participantes:

Beandrea Montoro, auditora fiscal em Guiné Bissau

Clair Hickman, auditora fiscal aposentada e facilitadora de treinamentos e consultoria fiscal em países lusoafricanos

Postos de fiscalização fechados à noite por falta de iluminação nos pátios, auditoras e auditores da Receita Federal em greve por mais de um mês em 2023, proposta do governo negada pela categoria. O que está acontecendo com a Receita Federal?

Neste episódio bônus, entrevista exclusiva com Isac Falcão, auditor da Receita Federal e presidente do Sindicato Nacional dos Auditores Fiscais da Receita Federal no Brasil, o Sindifisco.

After attending the United Nations Tax Committee meeting in October and participating in its deliberations, Professor Sol Picciotto reflects in his latest blog contribution on the history of the Committee and its role in international tax. (Shared with permission)

The meeting of the UN Committee of Experts in International Tax held in Geneva from 17 till 20 October 2023, took place at a time of historic developments in the international tax world. The previous week had seen the tabling at the UN, by Nigeria on behalf of the African group, of a resolution calling for the negotiation of a UN convention on international tax cooperation. This was subsequently approved by the General Assembly’s Second Committee, opening up new possibilities for international tax governance.

The same day was also marked by the publication, by the Organisation for Economic Cooperation and Development (OECD), of the full text of the multilateral convention (MLC) to address the tax challenges of globalisation and digitalisation, a key part of the two-pillar package negotiated through the OECD/G20 Inclusive Framework on BEPS (base erosion and profit shifting). However, the MLC remains stalled, and reports indicate continuing disagreements and political reservations, and above all serious doubts over the likelihood of US ratification, which is essential for the convention’s adoption.

The transition to a possible new global framework through the UN will take some time, but in the meantime the UN Committee has become increasingly active.

New Energy in the UN Committee

The October sessions of the UN Committee were crammed with discussions of detailed technical tax matters. There was little mention of the wider global developments, yet the meeting provided a fascinating counterpoint to them, particularly for those of us who have long supported and followed the Committee’s work. The current Committee is tackling an ambitious agenda with energy, efficiency, and determination, particularly among its members from low- and middle-income countries. This is in sharp contrast to its previous history, when it was almost entirely concerned with tax treaty issues and beset by continuing conflict about whether, and how far, the UN model should align with that of the OECD.

Now, halfway through the 4-year term of the current membership which runs to 2025, the Committee is well on the way to delivering reports covering a wide range of issues, including wealth and solidarity taxes, environmental taxation, indirect taxes, health taxes, and improvement of tax administration (including through digitalisation). This list adds to other important issues which fall within the Committee’s more accustomed areas of international tax, such as further refinement of transfer pricing guidance and updates to the UN model convention.

The Committee’s work in this more traditional area has also become bolder, with certain far-reaching proposals. Two can be singled out in particular:

1) Fast-Track Instrument

One is a proposed ‘Fast-Track Instrument’ (FTI) – a multilateral tax treaty aiming to streamline the adoption of selected key provisions of the UN model into existing tax treaties. These would strengthen the protection of the right to tax at source profits derived from activities in the country where they are performed.

The proposed FTI (Annex B, here) has the potential to transform key provisions of the UN model into a de facto global standard. These would mainly be provisions protecting source taxation, especially those adopted in the recent years by the Committee, namely:

taxation of capital gains relating to natural resources and offshore indirect transfers,

fees for technical services,

income from automated digital services,

the Subject to Tax Rule (a broader alternative to the one in Pillar Two),

capital gains from immoveable property.

It also proposes to include the UN model’s articles on Pension Funds and Arbitration.

Like the OECD’s Multilateral Instrument to implement tax-treaty related measures to prevent BEPS (the MLI), the FTI would operate flexibly with an opt-in approach and a matching mechanism, allowing states to decide mutually which treaties would be covered. Nevertheless, it would establish a gold standard, and could speed up the adoption of these key provisions.

A Shift in the Allocation of Taxing Rights

The FTI could therefore greatly facilitate a much-needed reversal of perspective on the tax treaties’ allocation between states of rights to tax. Tax treaties essentially operate to restrict the intrinsic rights of states to tax income at source, where the profit-generating activities take place, based on the view that countries should encourage foreign investment, particularly by multinational enterprises (MNEs). This was acceptable among OECD countries, which are generally both home and host countries for MNEs, but unfairly reduces the taxing rights of low- and middle-income countries, which are generally only hosts for foreign MNEs.

Despite the rhetoric about tax treaties encouraging investment, in reality, allowing non-residents to escape tax on profits from business in the country damages both tax revenues and the economy, by discouraging foreign firms from creating local jobs, and offering them tax advantages over local competitors. Moreover, residence-based taxation has propelled tax avoidance, especially since the 1990s, by incentivising MNEs to locate intermediary entities, especially those supplying services or licensing intangibles, in low- or no-tax jurisdictions. OECD countries finally decided to address proliferating tax avoidance in the BEPS project in 2012. However, that project was explicitly designed not to change the existing allocation of taxing rights.

Low- and middle-income countries have since the beginnings of international tax, sought to protect source taxation rights. However, the design of tax treaties, which form the skeleton of the international tax system, became dominated by experts from capital-exporting countries, particularly the US, known as the main home country of MNEs for most of the last century.

A key part in this history was played by Mitchell B. Carroll, who acted as a consultant for the US government, as well as a private practitioner and adviser to US industry groups such as the National Foreign Trade Council. He played a dominant role in the League of Nations Fiscal Committee (although the US did not join the League), as the US representative and then its secretary. He also helped found, and then became the first President of, the International Fiscal Association. A recently published history by Nikki Teo has helped document the key period witnessing the formulation of the ‘Mexico’ and ‘London’ versions of the tax treaty model, and the failed attempt in 1945-54 to establish a Fiscal Commission at the UN. Many followed in Carroll’s footsteps, so that the moulding of international tax rules became dominated by the perspective of tax advisers for MNEs and of capital-exporting country governments, institutionalised at the OECD.

It was not until 1967 that the UN came back into international tax, but only with an ‘Ad Hoc Group of Experts’, which was slightly upgraded in 2005 to a Committee of Experts. Its work remained narrowly focused on discussion of modifications to the OECD model convention to generate a UN version more acceptable for capital-importing countries. The Committee has also been greatly hampered by minimal resources, despite a boost in 2015 that enabled it to meet twice a year. This, combined with the growing frustration among middle- and low-income countries at the marginalisation of their perspectives during the OECD-led BEPS project, has led to the greater activism of the UN Committee.

2) Services Taxation Regardless of Physical Presence

The second bold proposal in the recent meeting resulted from these long-standing concerns about the restrictions on source taxation, accentuated by the emergence of e-commerce twenty years ago. This shift to a digitalised economy sparked discussions in the Committee back in 2004 that were initially radical, including talk of the possibility of defining a taxable presence test based on a threshold of sales revenue, and attribution of net profit to a non-resident using formulary apportionment. In fact, this approach has a long history, going back to the origins of the tax treaty system, and elements of it were included in the Mexico model and are still retained in the UN model.

The Committee was not ready to tackle such a comprehensive approach at that time, and in 2011 decided to focus on taxation of fees for services. Even so, it took another five years to agree on a new provision to be included inclusion in the model treaty (article 12A) for a withholding tax, and it covered only fees for technical services. Since these were defined to require human intervention, the measure did not extend to the digitalised delivery of services, although a broader provision was included as an option in the Commentary.

By this time, the BEPS project had completed its first phase, although work was still continuing on the main issue, namely addressing the tax challenges of the digitalisation of the economy. At this stage the UN Committee limited its role to following up on the outcomes of the BEPS project, while the non-OECD members of the Inclusive Framework had begun to act more cohesively in the BEPS project negotiations.

This was seen particularly when the G-24 group of developing countries put forward a radical proposal for taxing multinationals based on a new significant economic presence test, with an allocation of their consolidated global profits among countries where they have sales, using fractional apportionment. A consultation draft published by the OECD in October 2019, adopted the principles of this approach, but the proposals were complex and with a limited scope. This issue was highlighted in a paper submitted to the UN Committee by the Indian expert member, who proposed that the Committee should develop a simpler alternative. He therefore proposed a right to tax net income from ‘automated digital services’, even without a physical presence, through fractional apportionment, by applying the MNE’s global profit rate to local sales and attributing an appropriate share to the market jurisdiction.

Further work quickly produced a new article: 12B. This article took the more familiar form of a withholding tax on the gross payment amount, at a rate to be agreed between treaty partners. However, it included a provision (article 12B.3) for the recipient of the income to opt for taxation of the net income (at the country’s normal domestic rate) based on fractional apportionment, allocating 30% to the market jurisdiction. This proposal was then approved for inclusion in the UN model in 2021.

The Proposed New Provision for Taxing Cross-Border Services

The new model treaty article now proposed would combine and also extend the main articles in the UN model dealing with the taxation of cross-border services. It would integrate into a single provision articles 12A, 5.3.b (the famous ‘Services PE’ provision) and 14 (for independent professional services). This would ensure that a provider of services from outside the country could be taxed on payments received from residents in the country for any services, regardless of the nature of the service and without any need for physical presence, although perhaps subject to a revenue threshold. However, at present the proposal would not cover automated digital services, which would be dealt with separately by article 12B.

This new article, which the Committee at this recent meeting agreed to conclude, would provide helpful simplification of the right to tax at source payments for services, regardless of whether they may be classified as technical or professional, or delivered by an independent person or an enterprise. The application of a withholding tax on payments for services is justified because such payments are generally made by businesses, and deductible from their income, hence they directly erode the source country’s tax base. For this reason, the tax could apply regardless of whether the service is performed in the country. This type of tax is also relatively easy to administer.

Nevertheless, this is a blunt instrument, because this type of withholding tax applies to the gross amount of the payment. Although it is regarded as a tax on income, and so within the scope of the treaty, and hence eligible for a credit against any tax liability in the treaty partner, it is not calculated on the net income or profit, and the rate takes no account of the profitability of the transaction or of the MNE concerned. Although this is short of a satisfactory and comprehensive solution to the problem of a fair allocation of taxing rights over MNEs’ global profits, it is a practical immediate solution that can protect the tax base of middle- and low-income countries that are hosts to MNEs.

What Next?

It has become increasingly clear that effective and fair taxation of MNEs should be based on treating them in accordance with the economic reality that they operate as unitary entities, and that the rights to tax their global profits should be allocated by factors that reflect their real economic activities in each country. This approach was explored by an ICTD-supported research on unitary taxation of MNEs. Strangely, the BEPS project has now resulted in the acceptance of this approach in principle, as well as an agreement on the detailed technical standards needed for its implementation. However, the current proposals for implementation are inadequate and unfair, and the MLC is very unlikely to be implemented.

The time now seems right for a new initiative, which should be led by the middle- and low-income capital-importing countries. Such a proposal has now been outlined in a briefing by a group of authors, including two prominent members of the UN Committee.

The Shift to a Global Tax Framework

The new dynamic of the UN Committee has emerged in parallel with, and largely independent of, the political pressure for the UN to take on a much wider role through a multilateral convention which could create a new global institutional framework for tax. Yet the two processes are linked, due to their common underlying cause. The UN Committee’s long-standing preference for taxation at source, where activities take place, has been vindicated. Only a truly global tax body could finally achieve the radical reform needed to achieve a comprehensive, fair, and effective rebalancing of taxing rights over the global income of MNEs.

In the words of a foremost international tax specialist, who has frequently provided technical input and support to the UN Committee: “[i]n recent years, it has become increasingly apparent that the OECD – with or without the Inclusive Framework – is not an appropriate body to lead on international taxation”. As Philip Baker concludes, what is now needed is a “well-conceived and ordered transition of resources, functions, personnel and leadership to the UN.”

Hopefully, the negotiations over the proposals at the UN may lead to a new institutional framework, that can subsume the arrangements already achieved for international tax cooperation, for example through the Global Forum on Transparency and Exchange of Information for Tax Purposes, while creating a more conducive basis to take forward the substantive work on international corporate taxation. It is now time for government negotiators to lay aside considerations of narrow national self-interest and work together to create a truly global framework for tax systems that can help achieve sustainable development.

Further Reading

P. Baker (2023), ‘United Nations General Assembly resolution on the “promotion of inclusive and effective international tax cooperation at the United Nations”’. British Tax Review (1): 20-23, p.23.

Sol Picciotto (2013), ‘Is the International Tax System Fit for Purpose, Especially for Developing Countries?’ ICTD Working Paper 13.

Sol Picciotto (2021), ‘The Contested Shaping of International Tax Rules: The Growth of Services and the Revival of Fractional Apportionment’, ICTD Working Paper 124.

[Image credit: “UN Secretariat Headquarters, New York” by UN Photo/Manuel Elias is licensed under CC BY-NC 2.0]

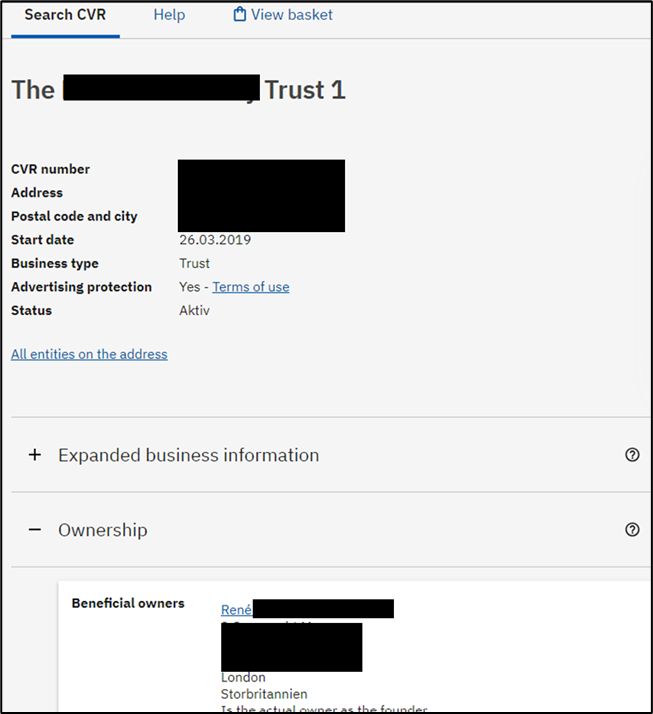

Close to 100 countries have approved beneficial ownership registration frameworks. Many of these countries will likely have to upgrade them after the recent reforms of the Financial Action Task Force recommendations 24 and 25 on beneficial ownership transparency for legal persons and trusts. And if not based on the reforms, then based on the pretty bad ratings given them by the Global Forum 2023 Annual Report:

We agree with secrecy supporters that beneficial ownership registries haven’t solved the issue of illicit financial flows. Tax evasion, money laundering and corruption keep flourishing unabated. However, this is not a reason to throw loophole-ridden beneficial ownership registries out with the proverbial bathwater. On the contrary, it just adds more urgency to get them right.

There are many things to fix. Applying verification and expanding access to all stakeholders (ie public access) so that beneficial ownership can serve multiple uses are obvious first steps. But our latest report deals more with the fundamentals: getting the law right to begin with. In this regard, complying with the weak standards of the Financial Action Task Force or the Global Forum won’t solve things either. As we’ve long warned, these standards have advised governments to build houses on sandy soil – it’s shouldn’t come as surprise then when walls begin to crumble.

Beneficial ownership vs legal ownership

Most companies have very simple structures where the legal owner (ie shareholder) directly owns and controls the company. In this scenario the shareholder is also be the beneficial owner. This information is publicly available in most commercial registries. That’s all good. The problem starts with complex ownership structures – ie where a company or legal entity is owned by many layers of entities spread across tax havens. These structures have been used by oligarchs, criminals and tax abusers to circumvent the rule of law. When it come to these structures, relying on just commercial registries is usually not enough to solve the problem.

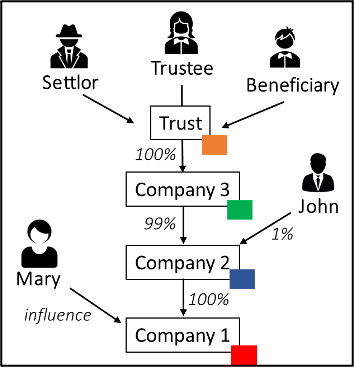

Consider the following complex structure, where each colour represents a different country of incorporation and where the real beneficial owners are Mary, John, the settlor and the beneficiary of the trust sitting at the top of the structure:

Relying on only legal ownership information held in commercial registries wouldn’t be enough to identify all these beneficial owners, even if (and this is a very big “if”) information on all the real owners was available in all relevant commercial registries.

The commercial register of country red would reveal that Company 2 is the legal owner of Company 1 (Mary wouldn’t appear in the commercial register). The next commercial register (country blue) would identify Company 3 and John as owners. The commercial register of country green would identify the trustee as shareholder (there might be no indication that the trustee is acting as a trustee on behalf of the trust, and could give the impression that she is the real beneficial owner). Even if the trustee declared the name of the trust to the commercial register of country green (which is unlikely), it would be even more unlikely that country orange has a trust register in which to find information on the settlor and the beneficiary. After a very time-consuming search, an investigating authority will at most identify just John and the trustee.

Current beneficial ownership registries aren’t that much better. Many of them include basic legal ownership information (eg Company 2) but not the full ownership chain (Company 3 and the trust) needed to confirm the declared beneficial owner on top. As for the beneficial owner information they hold, they would likely require the registering of the trustee, and in the best case scenario the settlor and beneficiary as well. But, Mary, who merely has influence (which may be hard to detect without advanced verification mechanisms) would likely avoid registration requirements, as would John. Only a truly effective beneficial ownership register would be capable of providing an overview of the whole ownership chain as shown in the figure.

Why beneficial ownership frameworks are flawed (even if in compliance with international standards) and how to fix them

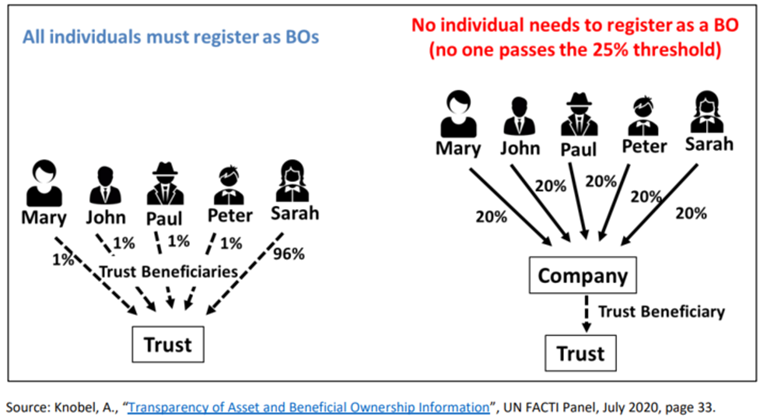

As the brief describes, following the Financial Action Task Force’s recommendations, most countries identify as beneficial owners only those individuals who hold more than 25 per cent of the capital in a legal entity, and where no one is identified, those with “control via other means”.

Based on the goal of saving costs for companies and for firms, financial institutions and other obliged entities that must undertake customer due diligence, countries take a “small” data approach (rather than the “right-data” approach), asking for as little information as possible and hoping that this makes it easy and cheap to collect and verify information. There’s perhaps also a naive hope here that that the catch-all phrase “control via other means” will capture all relevant individuals while asking for little. This supposedly cost-saving choice is a false economy and comes at a great cost: authorities are unable to obtain all the information they need, instead needing to spend considerable time to identify the real beneficial owners.

Instead, the brief explains that a no-threshold approach (ie requiring the identification of any beneficial owner with at least one share or vote), coupled with more extensive details to be collected (eg information on those with a power of attorney or with exposure to a company’s economic performance) is the only way to ensure that authorities will have all the beneficial ownership information they need when the need arises. This way, authorities can readily analyse the information they hold to reveal undisclosed relationships, properly conduct investigations into crimes, and detect crimes that might otherwise go unnoticed.

Importantly, as this brief will show, implementing a no-threshold approach does not add costs: even a framework with a 25 per cent threshold presupposes that anyone holding directly or indirectly at least one share has been identified. This is the only way to aggregate all holdings and determine which of those passed the threshold. Switching to a no-threshold approach would require no additional work in identifying direct or indirect shareholders.

Busting the claims against a no-threshold approach

The sandy soil governments were advised to build their beneficial ownership frameworks on is the “25 per cent or more” threshold. The single most effective action governments can take to strengthen their beneficial ownership frameworks is switch to a no-threshold approach, following the examples of Argentina or Ecuador. This would identify as a beneficial owner any individual who has at least one share or vote in a legal entity – and eliminate the transparency escape hatch that is making beneficial ownership registers ineffective today.

Opponents to the no-threshold approach have made some arguments pushing back against the approach. The brief and the table below responds in detail to these.

Proportionality

Claim: Requiring “all” individuals to be registered (because no thresholds are applied) is by definition disproportionate.

Our response: There are plenty of cases where regulations apply to “all”: all legal owners must be identified with the commercial registry, all parties to a trust must be identified as beneficial owners. In many countries, all individuals must obtain a national ID, all taxpayers must file tax returns, all individuals wanting to drive must obtain a driving license, etc.

A measure should not be automatically considered “disproportionate” just because it applies to “all” people or companies rather than to specific ones. Collecting information about all individuals with a link to an entity (rather than only of those with more than 25 per cent of the shares) is not necessarily disproportionate.

The goal of beneficial ownership frameworks is to tackle illicit financial flows such as corruption, money laundering, the financing of terrorism, tax evasion, sanctions evasion, etc. Collecting beneficial ownership information for all owners regardless of the value of their shares does not impose a burden on an individual that is excessive in relation to the objective sought to be achieved. In fact, a no-threshold approach already applies in the case of legal owners of companies (all persons must disclose their direct shareholdings to a commercial register) and to beneficial owners of trusts (all parties to the trust must be identified as beneficial owners regardless of their interest or rights to the trust assets and income). In fact, for most companies with simple structures where the beneficial owner directly holds the shares, beneficial owners are already identified with a no threshold approach – eg in the UK more than 80 per cent of companies have simple structures.

The only ones who would be affected by a no-threshold approach are those who intentionally create complex offshore structures to remain below thresholds, as a way of avoiding transparency of their financial affairs.

In addition, most administrative processes involve an “all” approach. In many countries, all individuals must obtain a national ID, which may include providing their date of birth, address, signature and fingerprints. This does not mean that all individuals are regarded as potential criminals. This is simply information that the state needs to fulfil its obligations, including the prevention of crime, ensuring economic fairness, planning and budgeting for social services, identifying missing persons, etc.

In many jurisdictions, all taxpayers must file tax returns, not because they are all considered tax evaders, but because it is how tax authorities ensure and verify compliance. In addition, having information on all taxpayers, both honest and not, allows authorities to compare them, to find patterns or red flags to ensure a level playing field where everyone pays their fair share. All customers must provide a financial institution with information for the know-your-customer due diligence procedures, not because they are would-be money launderers but in order to apply proper checks.

A risk-based approach allows for additional measures to be taken, but for it to be effective in detecting anomalies and outliers it does require obtaining a minimum amount of information from all.

Claim: A definition without thresholds does not pass the necessity test because an individual with 1 per cent or less of the shares would not be in control of the company and would thus not be responsible for any crimes.

Our response: Thresholds are deliberately exploited by criminals and those who want to remain hidden from authorities, undermining the whole purpose of beneficial ownership transparency. A person with even a 0.01 percent interest in a listed company (eg Apple) would have no control whatsoever over the entity, but that that tiny percentage could be worth millions of dollars. Identifying this person could be relevant to money laundering, corruption, tax evasion, etc.

Criminals exploit loopholes, especially thresholds, to remain hidden from authorities.

Beneficial ownership transparency is about identifying the real owners and controllers of legal vehicles to prevent them from engaging in illicit financial flows such as corruption, money laundering, tax evasion, etc. Thresholds are deliberately exploited by criminals and those who want to remain hidden from authorities, undermining the whole purpose of beneficial ownership transparency. Thresholds allow individuals to remain hidden, either by distributing their interests so they are slightly below the threshold, or directly by not having any ownership interest but rather holding control through a power of attorney, financial instruments, etc. As visually illustrated in a publication on beneficial ownership and investment funds , a 0.01 per cent interest in Apple would give no control whatsoever over the design of the iPhone. However, that tiny percentage would be worth more than US$200 million. Identifying the beneficial owner of that 0.01 per cent would be relevant to determine whether taxes have been paid and how the beneficial owner afforded that interest to begin with, to dispose of cases of corruption or money laundering.

A no-threshold approach is the only way to ensure all relevant individuals are covered, no matter their circumvention attempts.

Claim: Preventive collection of data and pattern-finding violate criminal law principles. Looking for patterns to investigate specific individuals before suspicions exist violate the principle that “the suspicion leads to the investigation” rather than the other way around.

Our response: Crime prevention is just as important as its prosecution. There is no need to wait until a criminal act or wrongdoing happens in order to act. Crime prevention does not affect the presumption of innocence. Most legal frameworks put a lot of emphasis on prevention, not because they consider all individuals as future criminals or victimisers but to prevent them from becoming such.

All drivers need to obtain a licence to prove they know how to drive, where their sight and hearing is also tested. Seatbelts are compulsory. Drinking alcohol and the use of cell phones while driving is prohibited. Cars have licence plates so they can be identified. None of these rules can be interpreted as an infringement on the presumption of innocence. At the same time, all of this information could be relevant in case of a car accident. In the same way, obtaining information on all beneficial owners related to an entity, checking that they are not related to any criminal or that there aren’t other red-flags (similar to checking a driver’s sight and hearing) cannot be considered an infringement of the presumption of their innocence, or as impugning their good faith or honesty.

This is somewhat similar to how airport security helps to prevent acts of terrorism, except in this case by preventing the economic and human cost of financial crimes. Both airport security and beneficial ownership transparency apply to individuals who are not viewed as either criminals or terrorists. One of the arguments against public access and collection of beneficial ownership information on all individuals related to an entity is that it affects compliant and honest citizens who have done nothing wrong. A simple counterargument is that the vast majority of airplane passengers are not terrorists, but everyone is still required to go through airport security. This comes at some cost in terms of the additional time spent by passengers as well as the staff and infrastructure required – but the cost is offset by the prevention of greater, even more costly harms.

One of the likely reasons why millions of people agree to or at least accept the discomfort of airport security (which includes affecting their privacy as every item of their luggage can be checked) is the immediate relationship between terrorism and the loss of life. By contrast, beneficial ownership transparency is perhaps perceived as a less important, urgent or worthy “privacy-affecting” measure because it has a more indirect link to the violation of human rights. However, the fact that the link to beneficial ownership transparency is more indirect does not mean that it is irrelevant.

Although the link between beneficial ownership transparency and human rights violations is indirect, the consequences and effects can be much broader, when considering all the financial crimes and unfair situations caused by secrecy. In economic costs, the State of Tax Justice in 2023 estimated that countries will lose US$4.8 trillion in tax to tax havens over the next 10 years. The UN estimated in 2018 that the global cost of corruption was at least US$2.6 trillion, or 5 per cent of the global gross domestic product. All of these resources are critical to pay for fundamental human rights – health food, education, housing, a fair trial, and many others.

Although harder to quantify, financial crimes such as corruption also have a human cost. Corruption led to the deaths of 52 people in 2012 in a factory fire in Bangladesh, just as it did for almost 200 young people who were trapped at an illegally held music concert called “Cromañon” in Argentina in 2004. More than 40,000 people died in the 2023 earthquake in Turkey due to poor construction regulation and corruption, and Lebanon’s port explosion killed more than 200 people due to illegally stored chemicals.

Claim: Some human rights organisations and activists distrust what they believe governments will really do with the collected information, eg target vulnerable populations or political opponents.

Our response: State authorities aren’t necessarily the problem. Oligarchs, high net worth individuals and entities who are often more powerful than countries, pose a bigger risk to democracy, equality and the rule of law. A no-threshold approach is a way to protect minorities and vulnerable individuals by ensuring that powerful individuals won’t be able to escape the rule of law by creating complex ownership structures.

Criminal law, constitutions or human rights conventions are a way to limit state power. In the past, an absolute monarch could dispose of anyone’s life or property. Criminal law, or human rights law, limits absolute power. The former-king-now-democratic-state must now comply with a fair trial, equality before the law, prohibition of torture, access to information, etc.

From a historical perspective, the ruler had absolute power, while individuals who were vulnerable and powerless organised themselves to limit the King’s or state’s power.

The 21st century is complicated by the fact that there are high net worth individuals, oligarchs and multinational companies that have far more power than countries: they have more capital, more media power, armies of enablers to escape paying taxes, can bankroll violent actors and bankrupt journalists investigating their affairs, and lobby or bribe legislatures to engage in rent-seeking.

Complete beneficial ownership information is about obtaining information about these powerful individuals who set up complex structures to escape the rule of law. It is a way to give more tools to authorities and to everyone else with access to beneficial ownership information, in the process helping to protect minorities and vulnerable individuals.

Even if there is mistrust on how authorities will use the collected beneficial ownership information, the beneficial ownership data will mostly refer to the (more powerful) individuals who are able to afford setting up companies and trusts, not vulnerable and discriminated populations on low incomes.

Some argue that some states are corrupt, or are dictatorships or autocracies, and that a beneficial ownership definition without thresholds would give them even more power to be abused. Unfortunately, those states are most likely already (legally) allowed to collect beneficial ownership information without applying thresholds, or to use other ways to obtain confidential information or coerce their citizens.

Major financial centres where the rule of law is respected and where democracies do work, should start collecting complete beneficial ownership information. This way, democracies will be able to prevent oligarchs and dictators from creating entities and holding assets in these democratic financial centres, or will at least be aware of their interests and control, in case sanctions are to be enforced.

Claim: All databases can be hacked. Collecting and centralising a trove of personal data on individuals related to legal vehicles creates a high hacking risk.

Our response: Although all systems could possibly be hacked, this has not stopped people from using banks, apps or password storage services. There are multiple privacy enhanced technologies that could be applied to reduce the risk of hacks or misuse, and to run analytics without sharing confidential information.

Data obfuscation tools such as zero-knowledge proofs, differential privacy, synthetic data, and anonymisation and pseudonymisation tools which alter, create noise or remove identifying details.

Encrypted data processing tools, such as homomorphic encryption, multi-party computation, private set intersection and trusted execution environments, which allow data to remain encrypted while being used.

Federated and distributed analytics, which allow data to be pre-processed at the data source so that only the summary statistics or results are transferred.

Data accountability tools such as threshold secret sharing, and personal data stores.

The Bank for International Settlements Innovation Hub’s Nordic Centre in 2023 published a report on Project Aurora, a proof of concept that explored new ways of combating money laundering with a combination of payments data, privacy-enhancing technologies, artificial intelligence and enhanced cooperation across institutions and borders.

Claim: Authorities are already overwhelmed with data and are often unable to process it effectively. There is no point in filing even more data with authorities because they won’t be able to use it.

Our response: The complete collection of beneficial ownership data is supposed to be handled by technology, algorithms, big data analysis, etc, and not necessarily through manual analysis. Complete data would create a deterrent effect, just as the implementation of automatic exchange of bank account information did.

The potential availability of complete data on all foreign bank accounts led to more tax revenues in many countries through voluntary disclosure programs (taxpayers voluntarily declared their foreign accounts and paid reduced fines, before the information was exchanged). Apart from the deterrent effect, even if data isn’t processed immediately, it could also be used in the future – many financial crimes have a statute of limitations of 5 or perhaps even 10 years, giving enough time for authorities to make use of it.

At the same time, there is an exponential growth in technological capabilities around data storage, data matching and mining, and the processing of big data – all the while often becoming more cost-efficient. Just because an authority cannot afford data management functionalities today, does not mean they won’t be able to do it tomorrow. The prevalence of under-resourced authorities is not necessarily an argument against the collection of beneficial ownership information without thresholds, but rather an argument in favour of giving public access to information so that other stakeholders, including financial institutions, journalists, civil society organisations, researchers and foreign authorities can also use and process the data.

An effective beneficial ownership framework would secure sufficient information to identify all individuals who may turn out to be relevant, after running advanced analytics to detect undeclared relationships and other red flags. Most of the proposals of this brief originate from the Tax Justice Network’s Roadmap to Effective Beneficial Ownership Transparency. This new report explains why these proposals are necessary.

In a nutshell, the proposals include the following:

1. All legal vehicles should fall within the scope of registration – without exceptions.

2. A “necessary” data approach should be applied, rather than a “small” data approach. This would ensure that all individuals who are related to a legal vehicle are identified whenever they:

a) Have control, ownership or derive benefits from a legal vehicle;

b) Have at least one share, vote, right to benefits, interests or exposure through financial instruments (ie without applying thresholds); or

c) Have control via other means based on a non-exhaustive list such as power of attorney over the entity or its assets.

3. All “necessary” details should be required. In addition to basic identity details (name, address, nationality, date of birth), more details should be collected, such as: politically exposed person (PEP) status, tax residencies and nationalities (eg based on golden visas), identity of direct family members, price or value or reason for becoming a beneficial owner (eg price of transfer of shares), source of beneficial ownership (eg transfer of shares, apportionment as trust beneficiary.)

4. The full ownership chain should be obtained and verified, up to each individual with at least one share.

5. Charge fees for verification of complex structures. As a way to discourage complex ownership structures with too many layers and shareholders (which may increase costs for those collecting beneficial ownership information), financial institutions and beneficial ownership registries should be allowed to charge fees per layer and per shareholder for any entity that wishes to be incorporated or open a bank account.

6. Proper verification responsibilities. Countries should take an active role in beneficial ownership registration and verification by having the beneficial ownership register collect information on the full ownership chain down to each beneficial owner with at least one share, as well as cross-checking data and applying advanced analytics to detect red-flags (eg based on individuals’ declared income, income patterns for the neighborhood where the person is based, etc). This would reduce costs for financial institutions, which should be required to conduct some additional verification (not generally available to authorities) such as checking who administers the bank account, withdraws money from an ATM or from whom and to whom bank transfers are made.

This year our work featured in more than 314 broadcasts, 2,745 online media mentions, and 246 print pieces in over 140 countries, and saw more than 300,000 visitors to our website.

To help you catch up on everything you may have missed through the year, we’ve compiled a quick list of our most read pieces in 2023.

Not surprisingly, our most read report was the State of Tax Justice 2023 report, which shows countries will lose US$4.8 trillion in tax to tax havens over the next 10 years if they stay the course on global tax policy.

Our most viewed country profiles are perhaps no surprise: the United Kingdom, followed closely by Mauritiusand Switzerland. Indonesia made a surprise appearance in fourth place, while the Netherlands was our fifth-most viewed country profile.

Three of our cornerstone topics also saw significant interest:

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here. We’ll soon be launching our new podcast website, so look out for that!

In an extended Taxcast edition this month, a century of tax rule setting by the former imperial powers has been overturned: we look at the UN vote on global tax reform. Taxcast host Naomi Fowler follows events at the UN, the failed efforts to block it and explores what it all means with Alex Cobham of the Tax Justice Network.

~ #138 Overturning a 100 year legacy: the UN tax vote

“If the time of crisis imposes the time of change, then it’s time for cooperation to take precedence over competition. It’s time for international solidarity to take precedence over particular and selfish interest in the short term. African people are tired of numbers about assistance for development. They do not request more assistance. They request every partner running business, the physical or digital, individuals and companies making profit should pay the right price, the fair and just percentage in terms of tax. Then we could keep our promise to transforming our world, to ensuring the world we want, the future we want is a reality.“

~ UN Representative from Cameroon

“It’s a century waiting to have a globally inclusive body to set tax rules to throw over the decisions made by the League of Nations in the 1920s and 30s that we’re all stuck with the consequences of today. We don’t actually need tax rules that were set by the imperial powers, honestly, we can do better.”

You can WATCH the vote at the UN here (the discussion on tax matters starts around 35 minutes)

Here’s a summary of the podcast:

Naomi: Hello and welcome to the Taxcast, the Tax Justice Network podcast. We’re all about fixing our economies so they work for all of us. I’m Naomi Fowler. On the Taxcast this month:

Clip 1: “African people are tired of poverty, they do not request more assistance. They request every companies making profit should pay the right price, the fair and just percentage in terms of tax.” Clip 2: “The committee is now voting on draft resolution L18 Rev 1 entitled Promotion of Inclusive and Effective International Tax Cooperation at the United Nations.”

Naomi: It may not sound like it, but this is a historic vote at the United Nations on where the power lies for global tax rulemaking.

Clip 3: “The voting has been completed. Please lock the voting machine. The result of the vote is as follows: in favour 125, against 48, abstentions 9. Draft resolution A/C2/78/L18 REV1 is adopted.”

Naomi: Some nations tried their best to block it, but a landslide majority of nations voted to catapult the world into the next steps for fairer rulemaking on global tax. It’s all about who gets to decide, and how, and where.

UN representative from Nigeria: For developing nations this resolution represents a beacon of hope.

Naomi: This is the UN representative from Nigeria introducing the draft resolution before the vote on behalf of the Africa Group.

UN Representative from Nigeria: By standing together today, we commit not only to fairer tax systems, but also to a collective future where economic justice are not mere aspirations but achievable realities. The path is clear and the benefits are manifold.

Naomi: And here’s the South Africa representative.

UN representative from South Africa: For many Africans, fulfilling the UN Sustainable Development Goals is a matter of life and death. Unfortunately, their ability to meet these aims is hobbled by illicit and hidden movements of capital that amounts to vast billions each year. It is high time that the international community addresses this injustice in global taxing rights that is impoverishing millions, which goes back to the days of the League of Nations, when most member states were colonies and which has been perpetuated by the monopoly that rich country clubs have held over international tax rulemaking.

Naomi: We know that if we continue on our current trajectory where the ‘Club of Rich Nations’ at the OECD wields the power on tax rules in their own interests, countries are on course to lose 4.8 trillion US dollars to tax havens over the next decade. This vote aims to avoid those kind of astronomical losses by doing things differently through the United Nations and establishing a UN Tax Convention. Taxcast listeners will remember that in 2022 countries at the UN agreed by consensus to the preparations that have led up to this UN vote. So what have 125 nations just voted for? Alex Cobham of the Tax Justice Network:

Alex: So look, what’s happened, you know, last year there was agreement to move forward with intergovernmental discussions, so the real thing that it required was this report from the Secretary General to look at the options and then a debate in the General Assembly this year. Naomi: Yes, and I covered that in the Taxcast. It’s the one called the day global power shifted. I’ll put that in the show notes. So the report was done, yeah.

Alex: Right, so that’s happened, and off the back of that a new resolution was brought forward by the Africa Group. And this resolution really does two things. So it sets the commitment to work towards a framework convention on tax. And in the immediate period, really from January to August, it says we will create, basically a committee of all of the UN member states in order to create the terms of reference for those negotiations. So it’s all of the countries of the world agreeing the terms of reference for the negotiation on a framework convention. And the idea is that will then be brought back to the General Assembly in September, and then the negotiations would go forward. So last year was kind of creating the context, saying this is what we’re looking at. And this year is, we’re kind of into the hard and fast steps, this really concrete committee to take it forward, to create the terms of reference. So we’re on the road, you know, we have a resolution now that commits absolutely and without equivocation to negotiating a framework convention, a legally binding outcome.

Naomi: Okay. We’re going to look at the no voters and their motivations in a minute. But why did nations agree by consensus last year, but this time it went to a vote?

Alex: Yeah, so, this is sort of UN technicality, last time they didn’t vote so it’s UN consensus, so nobody objected hard enough to say, let’s take this to the vote. So there were some objections, registered or reservations from some OECD countries but nobody wanted to resist enough to have a vote so it passes by consensus and that’s effectively as close as you get to unanimity. This year they wanted to stop it. And they fought really, really hard all the way through trying to stop it and only the almost complete unanimity of the G77 countries made sure that we had such an overwhelming result in favour.

Naomi: Right, and the G77, that’s a coalition of so-called ‘developing’ countries, so it was a landslide really, those 125 nations voting in favour of the resolution represent 80 percent of the world’s population. It’s a historic vote too, the last attempt to address global power imbalances through the United Nations was spearheaded by Jamaica in the 1970s, along with other newly decolonised nations. Back then, they passed the UN Declaration on the Establishment of a New International Economic Order, and the aim of that was to reinforce the rights of all national governments to control multinational capital and specifically exercise democratic power over multinational corporations. The backlash against it from the most powerful nations dissuaded any similar attempts for nearly 50 years, until now. Here’s the representative from the Bahamas at the UN:

UN Representative from the Bahamas: This resolution is an important step towards an inclusive and equitable global tax system. For over six decades, the international tax policies formulated and dictated by the OECD neglected or failed to address the inherent challenges and the differences in development dynamics faced by the global south. Throughout these decades, developing countries have grappled with the disequilibrium of the international financial architecture, coupled with inconsistent contradictory tax and financial services policies, which have stifled economic growth. Mr. Chair, this resolution envisions a future where services and trade benefit all countries fostering true inclusivity and cooperation. It will enable countries, particularly in the Global South, to actively participate in shaping international tax norms, while creating equity and development capacity where it did not exist before. It will also ensure the development of protocols to combat illicit tax related illicit financial flows, which cause the loss of hundreds of billions of dollars in tax revenue annually. By addressing this issue we are taking a significant step towards preserving the financial integrity of vulnerable countries while generating more revenue to finance development. Mr. Chair, the overwhelming support for this resolution is a clarion call, indicating that the majority of the world recognises the inequalities of the current international tax regime and are victims of its arbitrary and inconsistent rules. In this vein, the Bahamas welcomes the passage of this resolution as an aspiration for equity, inclusivity, sustainable development and tax cooperation.

Naomi: The Bahamas co sponsored the draft resolution and we’ll talk a bit about their position later, which is interesting. Before the main vote happened on the draft resolution, Promotion of Inclusive and Effective International Tax Cooperation at the United Nations, the United Kingdom proposed an amendment to that draft resolution. Here’s the UK representative.

UN representative from the UK: During negotiations, the UK and others have sought to engage constructively to bridge the range of views and find a way forward that is in line with the ambition and which commands consensus. That is why we are now proposing an amendment to the resolution, which would change the text to just refer to a framework, rather than a framework convention.

Naomi: OK. So, what was the UK up to there? And why did they want to change the text to refer to a framework rather than a framework convention? What were they doing?

Alex: So, the UK brought forward this amendment. It’s not quite clear why it was the UK who brought it forward, because it was really the European Union’s position but I think just, you know, some OECD members trying to block things together. So the UK brought forward an amendment to strike out the word convention, basically from the resolution, in order to kind of get to a position where you have no legally binding outcome at all. Naomi: Right, so in a way they were happy to talk shop, but not if it actually meant it was legally binding?!

Alex: I mean, that seems to have been the position, which is remarkable. Because bearing in mind, these are countries that sometimes complain that the UN is a talking shop, and they use that as an argument for why they shouldn’t do things at the UN. And in this case, they were demanding that the UN be a talking shop and have no possibility of being anything else so, yeah, it wasn’t, it wasn’t a very compelling position, I think, and certainly the Africa Group gave it very short shrift, and rightly so. Naomi: Yeah, here’s the Nigerian representative’s response to that and there’s not much doubt what he thought about the UK’s intervention! UN representative from Nigeria: Thank you very much, Chairman, and I would like to thank the UK delegation for its engagement and for its, uh, approach of trying to alter the resolution. The position of the African Group is that the amendments being proposed by the UK delegation aim to, or would certainly preserve a restrictive status quo where developing countries remain marginalised in terms of international discourse. This approach denies us a voice in vital areas of agenda setting, norm creation, and decision making. The African Group, therefore, categorically rejects these amendments and strongly encourages all delegations to vote against them. We instead invite you to support and vote in favour of the draft resolution as it is, affirming our commitment to equity, inclusiveness and a global tax system where every member has an equal say.

Naomi: Well, that attempt by the UK to amend the draft resolution didn’t work. It was heavily defeated. Listen here to the results of the vote on their amendment.

UN representative: Delegations are kindly requested to indicate their votes. Those in favour of the proposed amendment contained in document A/C2/78/CRP 7, please signify. Those against and abstentions. The committee is now voting on the proposed amendment to draft resolution L 18 REV 1, as contained in document A C2 78 CRP 7. Will all delegations confirm that their votes are correctly reflected on the screen? The voting has been completed. Please lock the voting machine. The result of the vote is as follows in favour 55 against 107 abstentions 16. The proposed amendment contained in document CRP 7 is not adopted.

Naomi: So, that amendment got nowhere. Next, the United Nations voted on the Africa Group’s now unamended draft resolution. Just before that, the US representative gave a statement on why the US was going to vote against it. Let’s listen to a bit of that.

UN Representative from the US: The United States regrets that it cannot join consensus on this resolution and wishes to explain the reasons for this decision before the vote. The content of the resolution and the process followed over the course of negotiations have resulted in outcomes that are likely to duplicate and undermine existing intergovernmental negotiations on international tax cooperation.

Naomi: Duplicate and duplication are words you hear a lot from the no voting countries.

UN Representative from the US: The resolution has failed to achieve the consensus necessary to strengthen international tax cooperation for the benefit of all countries. Without broad consensus among countries, any process is unlikely to strengthen international tax cooperation or achieve meaningful results.

Naomi: Hmm, well, the United States has often opted out of international agreements on tax rules as they’re decided currently, so, yeah..! Next, the US representative went on to claim that tax rulemaking as it’s done now is all just fine. Nothing to see here!

UN Representative from the US: Negotiations of the Inclusive Framework occur in a setting in which 145 jurisdictions provide input and decisions are made by consensus. This approach affords every member a real voice in negotiations and decision making, which allows for the development of solutions with broad consensus that have a better chance of standing the test of time.

Naomi: So she’s sort of saying 145 jurisdictions agree tax rules together and it’s all great?!