New

publications in the US, the UK, Switzerland and Japan show that better statistics

on cross-border exchanges of financial information are possible and necessary

to hold governments and financial institutions accountable.

Large amounts of financial information are now being shared automatically across borders, to allow countries to find out where their (mostly wealthy) taxpayers have stashed their wealth and what income they are earning, for tax purposes. This is a great improvement on the situation just a few years ago, when wealthy folk could hide their money around the globe with almost complete impunity, safe in the knowledge that their secrets would be kept safe. This improvement is led by the OECD’s Common Reporting Standard (CRS) for automatic exchange of banking information, set up by the OECD, a club of rich countries.

It is still hard to know how well this system is working, however. We have been asking for statistics on automatic exchange of banking information since our first report in 2014 (see loophole 27), after the OECD trumpeted the “end of banking secrecy” but we showed that this was (and unfortunately still is) far from being real.

Publishing aggregated statistics on banking information shouldn’t be controversial. While banking information on specific account holders is of course confidential (for example, “John has $10 million in HSBC”), there is no legitimate reason why aggregate information – for example, “All Germans hold $100 billion in country X” should be kept under wraps. Aggregate numbers of this kind are already published by some countries’ central banks (such as those of the United States or Switzerland) and by the Bank for International Settlements. Similarly, information on the total number of foreign bank accounts that countries sent and received from each other (eg “Argentina received information about 20,000 bank accounts from country X”) should not be considered an existential threat either.

In essence, statistics on automatic exchanges of banking information are necessary to:

1) allow a wide range of interested stakeholders – citizens and governments in developing countries, academics, journalists, civil society organisations, and so on – to obtain essential information about the total holdings of their countries’ (wealthy) residents in financial centres. This statistical information would help measure capital flight, inequality and identify the most relevant financial centres chosen by a country’s residents to hold money and investments. In addition, for authorities in developing countries unable to join the automatic exchange system (to receive the specific bank account details), this statistical information would help cross-check information they receive from local taxpayers. For example, tax authorities could cross-check the statistical data (“our residents have X million in country Y”) against the data reported in the tax returns. Anti-corruption agencies could do the same in relation to asset declarations from high-ranking government officials.

2) hold to account banks and other enablers of the offshore secrecy system, and at the same time make sure the automatic exchange system is working

3) allow all interested stakeholders to hold public authorities to account, for subjecting their wealthiest citizens to the rule of law.

THE DETAILS

1) Basic information for developing countries

The CRS systematically shuts many developing countries out, thus removing a key tool they could use to stop the looting of their countries and the stashing of their national wealth offshore. The big problem is the principle of ‘reciprocity’, where countries must send information too. Many developing countries, especially the poorest and most vulnerable, simply aren’t equipped or resourced to collect banking information. So they aren’t allowed to get anything back. (Tax havens, by contrast, are allowed to implement non-reciprocity, albeit of a different kind: they can simply refuse to receive information from abroad, under “voluntary secrecy”.)

Statistics would provide at least basic aggregate data for these developing countries (for instance, “all Zambians hold $X million in Switzerland, $Y million in the United States, and so on.). Statistics are important even if a countries’ authorities aren’t asking for it – after all, they may have an interest in not receiving any information to protect their own corrupt officials. However, statistics would also give journalists and civic groups evidence to push their governments to investigate those offshore holdings, and to act.

2) Hold enablers to account and assess the exchange system’s effectiveness

The OECD’s CRS framework for automatic exchange of banking information lacks teeth to enforce its provisions on financial institutions, compared to the US domestic framework to exchange banking information automatically (called FATCA) that imposes a 30% withholding tax on non-compliant banks. However, even these high withholding taxes and other penalties seem to be little deterrent for banks. For example, in 2018 the US prosecuted an executive of Loyal Bank for failing to comply with FATCA. The US found out about this by using an undercover agent. Statistics comparing all banks with each other would allow the identification of outliers (eg most big banks filed X reports, but bank Z is saying they have no information to report). These statistics would be a much more efficient way to find non-compliant banks, in terms of time and resources.

As we described here (pages 37-52), and here, statistics are essential to identify avoidance schemes and to make sure that they system is working, and that banks are correctly filing information.

Some real-world cases illustrate how this can work.

Guernsey

After sending banking information to the US (based on FATCA) and to other countries (based on the OECD’s CRS), the British tax haven of Guernsey reported that it received notifications from those countries indicating “record level errors”, requiring Guernsey financial institutions to make relevant corrections.

The UK

The Society of Trust and Estate Practitioners (STEP) showed how the UK found out that banks are wrongly identifying entities as beneficial owners:

“HMRC has identified the most common errors made by financial institutions (FIs) when filing their Automatic Exchange of Information (AEOI) returns… [including:] 5. The FI reports entities as controlling persons. Some FIs report entities as the controlling persons of entity accounts, resulting in trusts and companies being reported as controlling persons. However, entities cannot be controlling persons; under CRS and FATCA, ‘controlling persons’ means natural persons who exercise control over an entity.”

The US

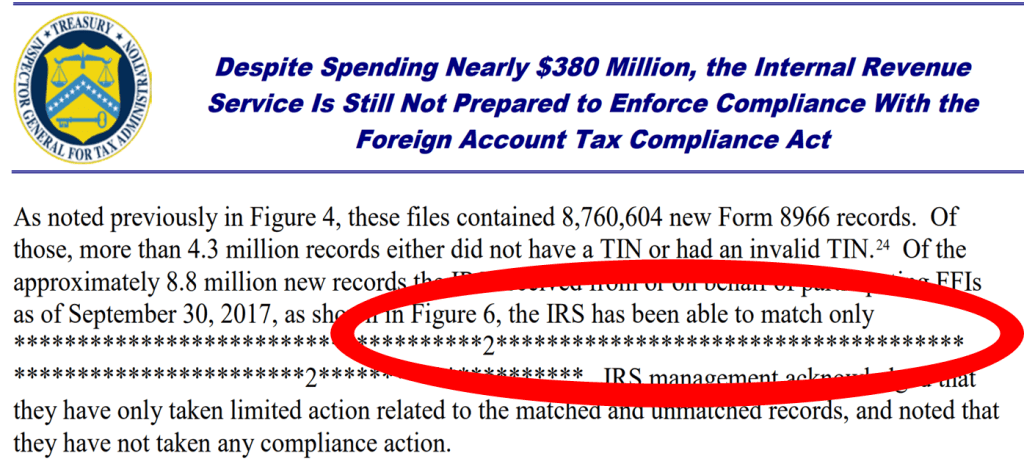

Banks are also reporting wrong information to the US. The US Treasury Inspector General for Tax Administration reported that in 2017, out of the 8.7 million forms received with FATCA information, 4.3 million (roughly half) didn’t have a tax identification number (TIN), including 3.2 million that had an invalid TIN, such as “000000000,” “111111111,” or “999999999,”.

If banks don’t report accurate information, or don’t report any information at all, there’s little that authorities can do to fight illicit financial flows, which takes us to the last point.

3) Hold authorities to account and make sure they are properly equipped

In March 2019, during the OECD Integrity Forum at a panel on exchange of information, Norway described that they had a matching rate of 90%, meaning that out of all the information received pursuant to automatic exchange of information, they could identify the correspondent Norwegian taxpayer in 90% of the cases.

The US Treasury Inspector General for Tax Administration report, in contrast, decided to redact information on the matching rates:

However, based on the Government of Accountability Office (GAO)’s report, we know that these matching rates are rather low:

Without valid TINs on Forms 8966 submitted by FFIs, according to IRS officials, IRS faces significant hurdles in matching accounts reported by FFIs to those reported by individual tax filers on their Forms 8938. As a result, IRS must rely on information such as names, dates of birth, and addresses that the filers and/or FFIs may not consistently report. Without data that can be reliably matched between Forms 8938 and 8966, IRS’s ability to identify taxpayers not reporting accurate or complete information on specified foreign financial assets is hindered, interfering with its ability to enforce compliance with FATCA reporting requirements, and ensure taxpayers are paying taxes on income generated from such assets. [emphasis added]

Given that in some cases roughly 50% of forms didn’t have a valid TIN (see point 2 above), it could be expected that the US matching rate is less than 50%…

And, as described in our blog, some EU countries didn’t even bother to open the data they received.

The staff of tax authorities shouldn’t automatically be blamed, however: the buck stops with government, which often under-resource tax authorities, sometimes based on political decisions not to intervene.

What do tax authorities say when asked to publish statistics about automatic exchange of banking information?

Tax authorities usually invoke “confidentiality” to resist requests to share information. Of course, most of the information they hold may indeed be confidential by law (this depends on the country: some Scandinavian countries even make tax returns of regular citizens available to the public). However, central banks routinely publish aggregate data, while keeping specific bank account details confidential. By the same token, aggregate statistical information doesn’t violate any taxpayer’s confidentiality (no single taxpayer’s foreign banking information would be disclosed, only the total of all residents). So, if it’s not about the taxpayer, whose “rights” would tax authorities be breaching if they published statistics such as “our residents hold $100 million in country A”? Apparently, the rights of country A, as explained below.

Under the OECD’s Common Reporting Standard (CRS,) it is the Multilateral Competent Authority Agreement (MCAA) that determines the scope and process for exchanging banking information. The MCAA states:

Section 5. Confidentiality and Data Safeguards

1. All information exchanged is subject to the confidentiality rules and other safeguards provided for in the Convention…

(The “Convention” refers to the Multilateral Convention on Administrative Assistance in Tax Matters, which is the legal basis for exchanging information automatically.) The Convention states:

Article 22 – Secrecy

2. Such information shall in any case be disclosed only to persons or authorities (including courts and administrative or supervisory bodies) concerned with the assessment, collection or recovery of, the enforcement or prosecution in respect of, or the determination of appeals in relation to, taxes of that Party, or the oversight of the above. Only the persons or authorities mentioned above may use the information and then only for such purposes…

One could argue that the above provisions seem to refer to a taxpayer’s information, not to statistics that involve aggregate data on all taxpayers. However, the main argument against ‘publishing statistics’ comes, in fact, from the Commentaries to the Convention’s Article 22.2, which expand the meaning to include also not disclosing information even if “not-taxpayer-specific”:

…Furthermore, the information received by the competent authority of a Party, whether taxpayer-specific or not, should not be disclosed to persons or authorities not mentioned in paragraph 2, regardless of domestic information disclosure laws such as freedom of information or other legislation that allows greater access to governmental documents. (emphasis added)

But this shouldn’t in fact be an obstacle. Even in light of Article 22.2, countries should be free to publish statistics about the information they received (“we received information about 1000 accounts held by our taxpayers in country X”), because in this case they wouldn’t be disclosing the “information received”: they would be disclosing the calculations (aggregation) they made about the information they received.

Indeed, some countries are already publishing statistics based on automatic exchange of information.

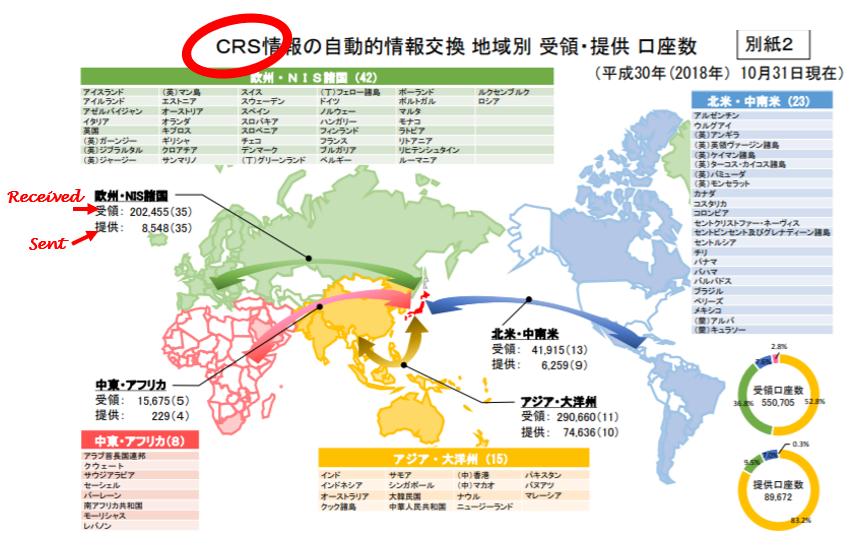

Here are Japan’s, for instance:

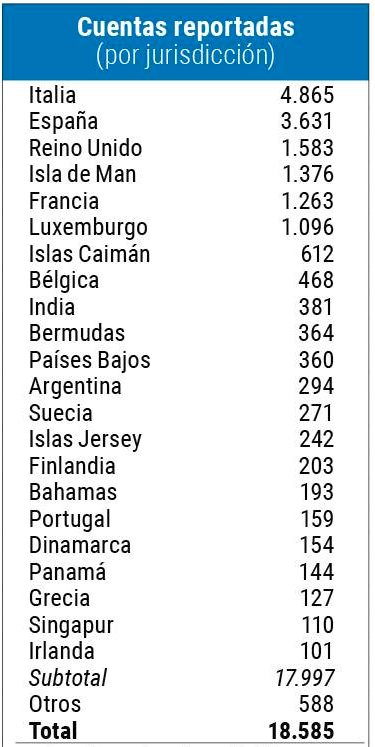

Uruguay’s news outlet Búsqueda published that in 2018 Uruguay sent information to other countries on 25.085 accounts held in Uruguay (half of which belong to Argentine residents), and that Uruguay residents hold 18,585 accounts in the following countries:

Switzerland’s statistics were published by Der Bund (“Bank accounts abroad. In which foreign states, Bern taxpayers hold the most bank accounts”):

The Swiss newspaper Blick also reported on 4.744 requests for administrative assistance on tax matters received by Switzerland from other countries. Leading the requests were Ireland, Denmark, France, the Netherlands and India.

Argentina’s La Nación published that in 2018 the country received information about 175.000 foreign accounts. The top financial centres used by Argentine taxpayers to hold their accounts were Spain, Italy, Uruguay, the UK and Germany.

The UK published that in 2018 they received information on 5.7 million accounts – compared to just 1.6 million accounts in 2017 (1.3 million of those held by individuals). The jump is likely to be because more countries joined automatic exchanges in 2018.

Even the OECD said they will publish statistics: not about banking information, but about another type of information that is shared among countries via automatic exchange of information: country-by-country (CbC) reports on multinationals’ activities, income employees, assets and taxes paid in each jurisdiction. Unlike banking information, we at the Tax Justice Network believe that country-by-country reports should be public and published online by every multinational. However, the OECD established a complex framework for it to be exchanged automatically, limiting the access and use that countries can give to these CbC reports. But at least there will be statistics about these country-by-country reports, as described by the OECD in its 2019 report to the G20:

In addition, the first aggregated and anonymised statistics prepared from data collected on CbC reports have now been prepared by OECD/G20 Inclusive Framework members and provided to the OECD for processing. The statistics are being provided for CbC reports relating to fiscal years beginning between 1 January 2016 and 1 July 2016, preserving the anonymity of MNE groups and the confidentiality of individual CbC reports. In total, there were 58 OECD/G20 Inclusive Framework members that had implemented CbC Reporting or had voluntary parent filing for the 2016 fiscal year, and it is estimated that only around 35 of those member jurisdictions received sufficient numbers of CbC reports to provide aggregated and anonymised statistics. Of those 35 jurisdictions, 26 jurisdictions have currently provided aggregated and anonymised statistics to the OECD covering around 4 100 CbC reports overall

How to ensure that all countries publish statistics about automatic exchange of information?

Some countries may disagree with our view and consider instead that the Convention’s current text doesn’t even authorise the publication of statistics. In relation to this, a few weeks ago we published another blog on automatic exchange of information, looking at why the international protocols only allowed this information to be used for tax purposes, even though many others (such as authorities fighting corruption and money laundering) had a legitimate and often urgent need to access the information. We recommended that countries sending the information sign a declaration authorising recipients to use the data beyond tax collection, based on another Article of the Convention. We believe the same could apply for publishing statistics.

The Convention does authorise these extra uses (beyond tax purposes) and sharing of information (beyond tax authorities), if a country’s domestic laws allow this extra use, and if the jurisdiction sending the information authorises this too.

The Convention’s Article 22.4 states:

information received by a Party may be used for other purposes when such information may be used for such other purposes under the laws of the supplying Party and the competent authority of that Party authorises such use…

Countries could thus sign a declaration stating something like “We declare in relation to the Convention’s Article 22.4 that, since our domestic laws allow the publication of statistics, we also authorise the recipient country to publish statistics on the information that we sent them pursuant to the OECD’s Common Reporting Standard for automatic exchange of information.”

A silver bullet that circumvents the legal obstacles

Yet there is an even stronger solution allowing countries to publish statistics without other countries’ authorisation.

As we noted here and here, statistics don’t need to be about the bank account information received from other countries, but about bank accounts held by foreigners in each country’s banks. In other words, the countries sending the information should publish aggregate data (statistics) about the information they are about to send. They hold the information in the first place, so they don’t need to ask permission from any foreign country. This is also better, because it is more comprehensive. Instead, statistics only on information being exchanged exclude data from residents in developing countries that aren’t able to join the system (because their information won’t be exchanged yet).

In Point 1 about “basic information for developing countries,” we were referring to statistics on the accounts held by non-residents in each financial centre. We mentioned that the Bank for International Settlements as well as the US and the Swiss central banks already publish this kind of data. Even so, their data may still be misleading because they refer to the “legal owners” who hold the accounts, but not to the “beneficial owners” (the real individuals who ultimately own or benefit from the accounts). For example, if an Argentine individual held an account in a Swiss bank through a Panamanian company, the central bank’s statistics would show that account as owned by Panama (the legal owner), but not Argentina (where the beneficial owner resides).

On the other hand, information collected by banks and sent to tax authorities for the purposes of automatic exchange of banking information do contain details on the beneficial owners of the accounts. Therefore, statistics on these data would be more relevant. Statistics published by Switzerland’s tax authorities would show, in the above example, how many accounts (and how much money) held in Swiss banks are owned by Argentine individuals, even if they held them via Panamanian companies.

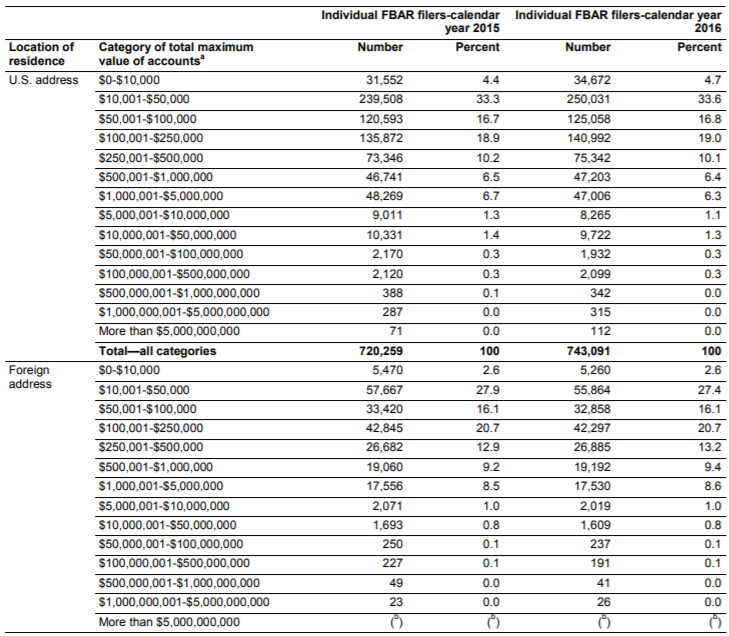

To grasp how useful statistics may be, look for instance at these US statistics published by the Government Accountability Office (GAO), based on American taxpayers who self-declared their holdings, classified by the value of their holdings – sometimes as high as more than USD 5 billion:

Imagine if we had the same information but about non-residents holding assets in US banks. Illicit financial flows and inequality would then be much easier to measure and combat.

Conclusion

Tax authorities should publish statistics on banking data received from local

financial institutions for the purposes of automatic exchange of information.

These statistics would enable developing countries, civil society organisations

and journalists to know how much money is held in each financial centre by the

residents of each country. This statistical information would help

measure capital flight, inequality, identify the most relevant financial

centres chosen by a country’s residents, and also allow authorities in

developing countries unable to join the automatic exchange system to do basic

cross-checks against information reported by local taxpayers. Statistics would

also allow authorities to hold financial institutions to account and make sure

that they are complying with the system. If the statistics also covered

information being exchanged, they would also show whether authorities can use

and are using the information they received from other countries.

The author

Related articles

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

The Financial Secrecy Index, a cherished tool for policy research across the globe

Did we really end offshore tax evasion?

The State of Tax Justice 2024

Submission to Special Rapporteur on the independence of judges and lawyers on undue influence of economic actors on judicial systems

New Tax Justice Network podcast website launched!

Overturning a 100 year legacy: the UN tax vote on the Tax Justice Network podcast, the Taxcast