For over sixty years, the Organisation for Economic and Cooperation has held dominion over the stewardship of international tax negotiations. In that time, progress achieved in putting a stop to crossborder tax abuse, which now costs governments around the world some US $480 billion a year, has been meagre at best.

With negotiations on a new framework tax convention now moving forward at the United Nations, the OECD’s leadership of standard setting on international taxation is for the first time in doubt. The move to initiate talks at the UN follows an historic resolution brought forward by the Africa Group, which was in turn motivated by frustration over the exclusionary dynamics of the OECD process. It can be argued that the OECD, as an institution mandated only to represent the interests of 38 advanced economies that make up its membership, was never an appropriate forum to tackle a problem which is, but it very nature, global. As demonstrated in the State of Tax Justice report, OECD member states are responsible for facilitating the vast majority of revenue losses to international tax abuse and, as such, have a vested interest in impeding the kind of radical reform that is so badly needed.

A new briefing produced by Tax Justice Network in collaboration with a coalition of allies systematically unpacks the various arenas in which the OECD has proven itself unfit to lead negotiations on international tax cooperation.

At the top of the list is the manifest inadequacy of its proposed ‘two-pillar solution’ to the problem. The first pillar aims to reallocate the profits of multinational companies to the jurisdictions where consumers are located, thereby countering the practice of profit shifting which lies at the heart of corporate tax abuse, while the second pillar sets a minimum corporate tax rate of 15 percent so as to prevent the ‘race to the bottom’ engendered by dysfunctional tax competition. Pillar One is limited to a tiny fraction of the profits of the largest multinationals, however, while the rate of 15 percent set by Pillar Two is likely to act as a ceiling rather than a floor, thereby exacerbating rather than redressing the very problem it purports to solve. Independent analyses have demonstrated that the ‘two-pillar solution’ would have little impact in real terms, while what benefits might flow from the deal would accrue almost entirely to the Global North.

The insufficiency of its proposed solution to international tax abuse stems from the failure to meaningfully incorporate the voices of Global South nations into the negotiating process. While the ‘Inclusive Framework’ mechanism was established in 2016, ostensibly to facilitate the participation of non-OECD members in the ‘Base Erosion and Profit Shifting’ initiative, proposals brought forward by the G24 in representation of developing nations were ignored in favour of an agreement negotiated bilaterally by the United States and France. It was against this backdrop that the Africa Group opted to table Resolution 78/230 for the commencement of talks on a more inclusive process at the UN.

Failures of inclusivity and effectiveness are not the only areas when the OECD has come up short, however. The existing regime of international taxation, which makes crossborder tax abuse relatively straightforward, was put in place as the major European empires were in decline and was designed to protect the economic interests of former colonial powers. As a result it has deeply racialised impacts, systematically constraining the fiscal space of majority non-white nations of the Global South and, in turn, their ability to fund fundamental public services. Moreover, despite the fact that the OECD counts most of the world’s most nefarious tax havens among its members, the only country it has targeted for sanctions on the basis of tax haven policies is the tiny African state of Liberia.

Unfortunately, this failure of accountability coheres with a pattern of conduct by the organisation in recent years, which has also seen repeated controversies over shortcomings in adhering to professional standards. Perhaps most notably, as the Africa Group’s initiative to pursue more inclusive negotiations at the UN gained traction, the OECD took the unprecedented step of writing to various of its member states’ ambassadors questioning the fitness of the UN to lead such talks and calling on them to block the proposals.

Several of the OECD’s leading figures have meanwhile been mired in controversies over questions of autonomy and independence. In 2022 the former head of the OECD’s Centre for Tax Policy and Administration, Pascal Saint-Amans, departed the organisation and immediately took up a position with lobbying firm Brunswick Group. During her time with KPMG, current head of tax policy Manal Corwin meanwhile co-authored a tax planning proposal for Microsoft that would lead to a major tax abuse scandal, while Secretary General Mathias Cormann has likewise faced controversy over allegations he profited from secretive dealings with Luke Sayers, who was head of Price Waterhouse Coopers Australia during the TaxLeaks scandal.

In a world of multiple enmeshed crises, from climate change and runaway inequality to the cost of living and recovery from the Coronavirus pandemic, the continued syphoning of revenue away from government coffers represents an urgent human rights concern. Modelling by the Government Revenue and Development Estimations initiative at the Universities of St Andrews and Leicester demonstrates that, were it not for the revenue lost to crossborder tax abuse each year:

15 million people would have their right to basic water.

32 million their right to basic sanitation.

2 million additional children would attend school.

101 additional children would survive every day: 36,900 each year.

11 additional mothers would not die during childbirth: 3,999 each year.

It is for the reasons set out in this briefing that the move to shift negotiations on international tax cooperation away from the OECD and to the more inclusive forum of the UN is so critically important. The most ubiquitous counterargument deployed by those nations that would seek to maintain the status quo is that the UN process would risk duplicating efforts at the OECD. While the latter organisation undoubtedly has valuable technical expertise and experience to offer, the United Nations is the only forum that can provide the legitimacy, inclusivity, transparency, and accountability that is a precondition to the just and comprehensive reforms that are so badly needed, however. The UN can and must provide a radically different process and outcome to that which has unfolded at the Organisation for Economic Cooperation and Development.

Litany of failure: the OECD’s stewardship of international taxation was produced by Tax Justice Network in collaboration with the Center for Economic and Social Rights, Centro de Estudios Legales y Sociales (CELS), the Economic Policy Working Group at ESCR-Net, the Global Network of Movement Lawyers at Movement Law Lab, the Government Revenue and Development Estimations project (University of St Andrews/University of Leicester), Minority Rights Group, Tax Justice Network-Africa, and Steven Dean, Professor of Law, Boston University School of Law.

Africa has contributed the least to global warming, yet millions of African people are facing the most severe impacts of the climate crisis. To combat these challenges – stopping floodwaters, feeding starving people, and increasing the resilience of the public sector – African governments need more finance.

Yet Africa loses around $89 billion each year due to illicit financial flows, according to estimates. The enabling nations of tax abuse are the richest countries in the world. Ironically, they are also largely responsible for the climate crisis.

Climate finance and tax abuse

Over a decade ago, rich nations pledged an annual US$100 billion for climate finance – a promise that has been unfulfilled. And even if they honoured their promise, this amount falls far short of addressing the world’s escalating needs. By 2030, the economic cost of loss and damage in poorer countries could be as high as US$1.8 trillion.

Fixing the international tax system could help plug this gap. The Tax Justice Network’s State of Tax Justice 2023 estimates that the world loses US$480 billion per year to corporate tax abuse and wealth tax evasion. This is nearly five times more than the unmet climate finance commitment. This stark discrepancy is why Africa is leading the charge for a UN framework convention on tax. A majority of the world is advocating for international rules that should have been in place years ago, had it not been for the influence of the richest nations within the OECD.

Fostering continental conversations on tax and climate

In the same year, the Special Rapporteur on the promotion and protection of human rights in the context of climate change urged the UN General Assembly to “Explore legal options to close down tax havens as a means of freeing up taxation revenue for loss and damage”.

We are now sharing insights from two roundtables and studies conducted in Mozambique and Tanzania. Drawing from these collaborative efforts, we adopted a framework of tax justice principles to direct future advocacy for climate action. This is known as the ‘5Rs of tax justice’, which include:

raising revenue,

redistributing wealth to create a more equal society,

repricing through higher costs to discourage activities that infringe on the rights of others,

improving representation to strengthen the social contract between citizens and their elected officials, and

supporting reparations to address harms from historical injustices and colonial legacies.

The briefing, accompanied by a pocket guide, includes a series of probing questions for each of the principles to enhance collaboration between tax and climate justice movements. You can download the briefing and the pocket guide from Tax Justice Network Africa.

The CEDAW committee was formed in 1982, comprising 23 global experts in women’s issues. Its main role is to oversee progress for women in countries that are parties to the Convention on the Elimination of All Forms of Discrimination against Women. CEDAW monitors national measures to fulfil this commitment by reviewing reports state parties submit every four years. During the different sessions, the Committee engages in dialogue with government representatives and civil society organisations to provide feedback and seek additional information. It also issues recommendations on women’s rights-related issues, to which states parties should pay far more attention.

As part of its review process, the committee has previously requested Brazil to address “any disproportionately negative impact of austerity measures and tax policies on women” but the Brazilian government has failed to do so both in the State Party Report and its annex. Answering this silence, Tax Justice Network, INESC, Latindadd and Red de Justicia Fiscal para America Latina y el Caribe have worked together to shine a spotlight on the tax injustices directly affecting women’s rights in Brazil, particularly black women in low income backgrounds. Our joint submission elucidates why the Brazilian government needs to urgently address the issues of inequality and discrimination.

The group submitted a Shadow Report, with inputs from several feminist organisations in Brazil. We present a number of salient issues which provide indicators of gender inequality and human rights failures, for example, how women are likelier to work in the public sector and rely on crucial public services, but when public spending is cut, jobs disappear, salaries get capped, and essential services like childcare and healthcare vanish. This leaves women jobless or underemployed and burdened with even more unpaid care work. And on top of that, traditional gender roles at home and domestic violence make things worse. With little economic power or social support, these policies often keep women from accessing even their most basic rights.

Among the recommendations of the shadow report is the need to acknowledge the unequal impact of austerity measures on women, especially black women. We call for tax policies in Brazil to take into account gender and race issues, regulations that include subsidies for health and personal care products, and the implementation of tax refunds for the poorest. Our report also suggests implementing measures to reduce the prevalence of tax incentives for multinational companies that generate socio-environmental damage, in order to repay the affected populations, mainly black and indigenous women.

In this week’s session, representatives from both Tax Justice Network and INESC will attend in-person to present the report and deliver its key recommendations to the CEDAW committee and government officials. We will use this opportunity to also discuss with, and learn from, feminist civil society organisations about how tax justice plays a crucial role in women’s lives. We expect the Committee to use the information we presented to question the Brazilian government about their actions on austerity and tax, and demand the country implement tax justice measures and guarantee women’s rights.

Unprecedented, historic negotiations took place from 26 April to 8 May at the United Nations headquarters in New York. For the first time, the 193 Member States began discussing the parameters that will guide the negotiation of a United Nations Convention on International Tax Cooperation (UNFCITC). Civil society and other stakeholders were also able to publicly contribute their views to the negotiations under UN rules of procedure, bringing the winds of genuine democracy to international tax negotiations that have up until now taken place behind closed doors in spaces such as the OECD (see the Civil Society Financing for Development Mechanism’s comprehensive compilation of resources on these negotiations).

This blog summarises what happened in the first session of negotiations (from April 26 to May 8) and raises some considerations for the key decisions that the Ad Hoc Committee will have to make in the remaining period of its mandate. A second session of negotiations will be held from 29 July to 16 August on the final draft of the parameters, before they go to a vote at the UN General Assembly near year-end.

Why are framework conventions so important? Because they are binding instruments that provide the basis for the creation of a system of governance and an international legal regime in a specific field. Their nature can be better understood if they are thought of as a global constitution that serves as the basis for creating more detailed binding rules —called protocols— that make up an international legal framework. As such, the discussion on the terms of reference of a UN framework convention on international tax cooperation is a golden opportunity to lay the foundations for an international tax framework that overcomes the structurally embedded, racialised inequalities in decision making power that the world has inherited from the imperial and colonial dynamics with which the current rules were decided (see top-level UN experts formal communication to the OECD on this matter).

Resolution 78/230 adopted in 2023 by the General Assembly mandated an Ad Hoc Committee to finalise the terms of reference (ToR) that will govern the negotiations of a UN framework convention on tax by August 2024. This is as important a task as the negotiation of the United Nations Framework Convention on Climate Change (UNFCCC) was, whose provisions have laid the foundation for international climate cooperation with significant implications for present and future generations. As happened with the framework convention on climate change, the defining of the parameters of the UN framework convention on tax will have significant implications for the scope, speed and timeliness of international cooperation on global tax for the decades to come, ultimately shaping how the costs and benefits of international tax policy play out for future generations (see our previous blog on why the world needs UN leadership on global tax policy).

So how did the negotiations go?

A show of tactics lacking good faith

It’s important to emphasise that it took a historic, overwhelming, global south led victory at the UN last year for these negotiations to take place at all. That victory came in the form of legally binding decision taken by the UN General Assembly to begin these negotiations, starting first this year with negotiations on the terms of reference and culminating next year with a framework convention. The scope and focus of the negotiations were also agreed as part of this binding decision. A landslide majority of countries – home to 80 per cent of the global population – voted in favour of the decision, outnumbering those against by more than 2 to 1.

With a legal mandate now established to negotiate and pursue the adoption of a framework convention on tax, and clear decisions on what these negotiations should entail, pushback from countries who voted against the decision was expected to reasonably focus on watering down the terms of reference and securing the weakest version possible of a framework convention. Shamefully, pushback from some countries during the negotiations went beyond what could be considered in good faith. Several tactics were employed by some countries to negotiate not the terms of reference but to attempt to reopen, undermine and disregard the binding legal decision agreed last year.

In his 2023 report, the UN Secretary General presented to the UN General Assembly, as he was requested to do by the assembly, three options for making international tax cooperation fully inclusive and more effective. He noted that if the option of a framework convention (as opposed to a standard convention or a non-binding framework) was adopted by member states, it “would outline the core tenets of future international tax cooperation, including the objectives, key principles governing the cooperation and the governance structure of the cooperation framework”. The report also clarified that framework conventions “may also include institutional provisions for creating a plenary forum for discussion between States that is endowed with the authority to adopt further normative instruments to which States could then become a party”.

With the adoption of Resolution 78/230, the General Assembly opted to initiate an intergovernmental process that should culminate with the adoption of a Framework Convention, and as such it gave a precise mandate to the Ad Hoc Committee to elaborate the terms of reference for such an instrument. This mandate is binding for the 125 Member States that voted in favour of Resolution 78/230, as well as for the 48 that voted against and the 9 that abstained (see the positions that countries adopted on the Tax Justice Policy Tracker and the voting records here).

While states may have diverse negotiating positions and legitimate concerns about the process, the first round of negotiations that just took place shows that some states are still betting on carrying over into this stage discussions on issues that have already been decided, and as such should not be taking place if states are negotiating in good faith.

Among these obstructionist tactics that hinder the fulfilment of the Ad Hoc Committee’s mandate, and against which member states and other actors in the process must be vigilant, were:

Disregarding or generating confusion about the clear mandate to move towards a Framework Convention. This ranges from positions that still speak of a preference for a non-binding framework to those that disregard the constitutive character of a Framework Convention by restricting its ability to pursue its own objectives. The recurring argument by the minority that voted against Resolution 78/230 that the Convention should not duplicate or be inconsistent with existing instruments, for example, ignores that a Framework Convention, aims to “establish an overall system of tax governance” (see Secretary General’s report, par. 55) and as such can redefine the substantive and procedural pillars of existing and future instruments.

Limiting the scope of the task ahead and of the Convention to be negotiated to the point of disregarding the mandate of the Ad Hoc Committee. Advocating for a minimalist Convention with objectives such as “gather countries to exchange effective practices on mobilising domestic resources” (see several EU submissions) instead of outlining the core tenets of international tax cooperation, is also another way of ignoring the constitutive character of a Framework Convention and thus pushing for the definition of parameters for the stage that are contrary to the mandate of the Ad Hoc Committee.

Denying the motivation or other provisions of the resolution that has given rise to the work of the Ad Hoc Committee. As recognised in the UN Secretary-General’s report “existing international and multilateral arrangements […] do not satisfy the main elements for fully inclusive and more effective international tax cooperation”. Resolution 78/230 stated that an intergovernmental process at the United Nations for tax norm shaping and rule-setting would “leverage existing strengths and address gaps and weaknesses in current international tax cooperation efforts and arrangements”. While the Resolution mentions that this should be done “with full consideration of existing multilateral and institutional arrangements”, it also recognises that “inclusive and effective participation in international tax cooperation implies that procedures should take into account the different needs priorities and capacity of all countries to meaningfully contribute to the norm-setting processes, without undue restrictions”.

A corollary of this is that if Resolution 78/230 is motivated by the importance and timeliness of strengthening international tax cooperation to make it fully inclusive and more effective, both in procedural and substantive terms, then being faithful to that mandate implies overcoming the problem of the lack of both full inclusiveness and effectiveness of existing instruments identified by the Secretary-General’s report. In this vein, refusing to reform and reconsider existing rules on the grounds of avoiding duplication and complementarity, when they fail to meet the values put forward by the General Assembly, is to deny the motivation behind the mandate given to the Ad Hoc Committee.

Insist on changing well-established decision-making rules. All procedural provisions must be based on compatibility with the rules that are specific to the spaces where discussions take place. It is important to distinguish three distinct stages: 1) the Ad Hoc Committee’s decision-making rules for drafting the terms of reference (ongoing), 2) the Ad Hoc Committee’s decision-making rules for negotiating the Convention, and 3) the decision-making rules of the Framework Convention itself. In the first two cases, since the task will be performed by subsidiary bodies of the General Assembly, the established practice is that while consensus is sought, simple majority rule is not ruled out. A minority of states have argued that established practice should not apply when it comes to the Ad Hoc Committee’s decision making due to the alleged exceptionality of the nature of tax matters. Instead, they argued that decisions can only made on a consensus basis. The arguments for alleged exceptionality have not been convincing and either way would not be sufficient reason to modify the established practice in these bodies. The established practice is intended to ensure timely decision-making and to prevent a minority of states from obstructing progress by wielding veto power.

Restrict the participation of other stakeholders and limit their meaningful contributions to the process. At the first meeting of this negotiating session there was an incident that involved a lengthy discussion over Turkey’s objection to the accreditation of three civil society organisations. Fortunately, member states did not accept this objection and all organisations were accredited. A few days later, and less restrictive in nature, France requested that civil society organisations be heard only after all member states had spoken, if time allows. Although these are two very different actions, the two episodes reinforce the importance of all member states being on the same page in terms of valuing the opportunity that the UN rules of procedure offer to deliberate in a more informed manner with the input that civil society and other actors can bring to the process. The limited and precious time the Committee has for fulfilling its mandate should focus on using the input of all actors to jointly achieve the best outcome rather than on time-consuming discussions to restrict the existing participation mechanisms.

These tactics, coupled with silence as a strategy by the countries who voted against the resolution last year — which made the meetings particularly short during the last week of negotiations — led countries such as Nigeria to argue in its closing remarks on 8 May that good faith in negotiation must not only be preached but put into practice by all countries.

Country blocs around the main procedural and substantive discussions

Acknowledging the nature of the Ad Hoc Committee’s mandate by all countries should facilitate the task ahead: finalising the terms of reference in the indicated timeframe. What is the balance after the first session and what can we expect from the discussions to come?

Different views on the type of framework convention, its objectives and principles

The first days of deliberations focused on more general issues on what kind of parameters the terms of reference should set. That discussion showed stark differences in the type of framework convention that states are advocating for and varied views on what its general provisions should be. These different views of the type of convention desired, and on what the objectives of the framework convention should be, were also evident in the widely varying proposals countries submitted in writing ahead of the session.

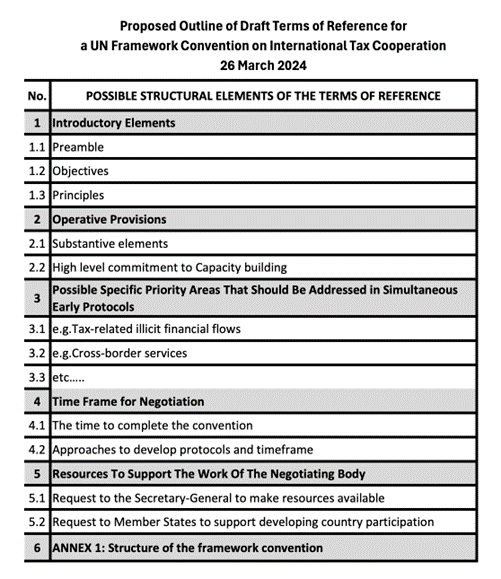

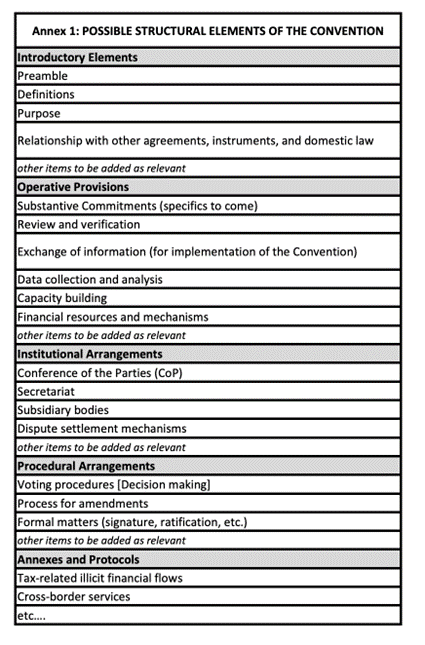

During the session, the positions on the type of parameters that the terms of reference should set were divided into two main blocs. A first group of countries – mainly those that voted against the resolution adopted last year – argued that the terms of reference should give very general guidelines and focus on the procedural aspects for drafting the framework convention – without prematurely addressing anything that could prejudge its content. A second group comprised of global south countries showed stronger support for an initial outline for the terms of reference and for an annex with the possible structural elements of the framework convention, both prepared by the Ad Hoc Committee’s Secretariat based on the inputs States submitted to the process (see images below). They later suggested the terms of reference should have a broad-based approach according to which all issues should be up for discussion, and that the terms of reference should include some substantive scoping along the lines of the draft outline of the elements of the framework convention proposed by the Secretariat.

Despite differences over the emphasis that the terms of reference should have, states adopted a working agenda that over several days addressed an exploration of substantive points that could be included as high-level commitments of the framework convention.

The issues that countries want the framework convention to address

The exploration of the issues identified an expanded but not exhaustive list of issues that the terms of reference should contain as a guide for the negotiation of the framework convention. States expressed different positions on the inclusion of these issues. Richer OECD countries, including several vocal EU countries, noted that the framework convention should focus on less controversial issues and not duplicate efforts with other fora (implicitly and at times explicitly, the OECD). Global South countries (including some OECD members) generally argued for the need to include all relevant issues, even if they had been addressed by other fora. It is the Tax Justice Network’s view that in order to incorporate the perspectives of all countries, an inclusive framework convention on tax should not exclude any of the issues discussed, and particularly those that lower-income states consider to be priorities.

Before reviewing states’ positions on specific issues, two more cross-cutting observations should be made. The first is about the language used. While states use similar terms such as “domestic resource mobilisation”, “capacity building” or talk about their commitments to “fully inclusive and more effective tax cooperation”, the scope of these terms can be very different. For example, for Global South countries it is key that domestic resource mobilisation is understood to include combating illicit financial flows, while for richer countries it is often associated with a capacity building agenda to enforce existing standards and improve the collection of specific taxes in lower income countries.

To resolve these differences, we believe it is necessary to build on the most comprehensive definitions adopted in the most universally accepted fora. This can help overcome discussions in which states should avoid becoming embroiled. For example, in the discussion on the issues that should be addressed as part of the simultaneous development of early protocols, the United States raised that the term “tax-related illicit financial flows” was ambiguous, and noted its concern that certain tax avoidance practices might not be considered illegal in certain countries and as such should not fall under that definition. This objection was raised despite the fact that UN’s formal statistical definition already includes cross border tax abuse by both multinational companies, through profit shifting, and wealthy individuals hiding assets and income streams offshore whether illegal or not. Considering such established definitions, therefore, there should be no doubt as to the extent to which some terms should be interpreted. Furthermore, the whole purpose of covering “tax-related illicit financial flows” is to develop rules that are less prone to aggressive tax avoidance to the detriment of global south countries. As such, whether these practices are legal in the United States or in other high-income countries, is irrelevant.

A second observation has to do with the information used for resolving controversies in the negotiations. If one starts from different premises or a different diagnosis of the problems of the current tax architecture, states may entrench themselves in rhetorical positions that do not address what other countries are calling for. For example, African Group countries have insisted that there are structural problems with the standards decided in other fora such as the OECD because these standards fail to consider the realities of African countries and because they were decided in a forum without meaningful and equal participation — facts on which ample evidence can be provided. In contrast, richer countries, and in particular OECD countries, repeatedly cite the risks of duplicating what already exists, including these problematic standards, thereby ignoring objections to the legitimacy and effectiveness of existing instruments without providing any evidence base to address the concerns of other countries. The search for a common understanding implies approaching the process in a way that genuinely addresses the concerns of other parties.

With these two observations shared, we now provide summaries of the positions that were expressed on specific issues.

Domestic resource mobilisation and capacity building

A first discussion was on the scope of the concept of domestic resource mobilisation (DRM). In written submissions the term was mostly used by countries from the global north, as the following table shows.

During the sessions, there were two main positions on this issue (see statements on the matter here). A first group of countries argued that domestic resource mobilisation should be the priority issue to be addressed by the framework convention, with an emphasis on capacity building in lower income countries. A second group of countries pointed out that domestic resource mobilisation must be understood beyond capacity building measures and include issues of fair allocation of taxing rights and progressivity of tax systems. Hence, according to the second group, domestic resource mobilisation and capacity building should be addressed separately (recognising the importance of capacity building under an approach that addresses the needs of Global South countries). The chart below summarises how positions were aligned during the session.

The Chair concluded this agenda item by acknowledging that domestic resource mobilisation would need to be understood as having at least two components: one related to capacity building and the other including fair allocation of taxing rights and broader issues.

Effective taxation of high-net-worth individuals, including wealth taxation

Several states raised demands in their written submissions in relation to the inclusion of taxation of high-net-worth individuals, as shown in the table below.

During the session, there was a broad agreement on the importance of this issue for combating inequality and achieving other aims, but positions on how to include it in the framework convention varied. On the one hand, Brazil stressed that it considered this to be a crucial issue, for which it had made a proposal in the context of the country’s G-20 presidency. Brazil pointed out that the United Nations would be the most inclusive forum to discuss this issue. Spain and France indicated their support for Brazil’s proposal to the G-20 and suggested that the modalities for inclusion in the framework convention could be defined at a later stage. Colombia, Morocco, Belgium and Austria were more in favour of referring to the taxation of very high-net-worth individuals as a high-level commitment under the framework convention.

A second bloc of countries noted that the taxation of wealth was an issue of domestic tax policy to be decided by each country individually. But these countries were still open to considering options for including it as a high-level commitment, although some more open than others. These countries insisted on the need for a flexible approach that recognises the diverse circumstances of each country. Interventions from Japan, Canada, China, Germany and Sweden fell within this view. The United States, the United Kingdom and Korea more strongly emphasised that this was a domestic taxation issue and were more sceptical about its inclusion in the framework convention. However, they did not raise insurmountable objections in principle, and Korea and the United Kingdom indicated that they were open to considering it. Mauritius and the Bahamas raised some technical doubts about design of wealth taxes and how to include it in the framework convention.

A third bloc argued that the issue was indeed very important but suggested including it either under the high-level commitment on domestic resource mobilisation (Nigeria, Jamaica, Singapore, Chile), the high-level commitment on combating illicit financial flows (India, Kenya) or under a new high-level commitment on combating inequalities (Japan).

Given that there was broad consensus on the importance of the issue, the Chair noted it should be included in the negotiation, although the specific modalities would have to be defined at a later stage.

Making sure tax measures contribute to addressing environmental challenges

On this issue, there was broad agreement on its importance and urgency and no objections to its inclusion were heard from any member state (except a call for caution from Korea).

There were different emphases on the measures that could be considered. Argentina, India, Mauritius, Bahamas and Kenya highlighted the principle of shared but differentiated responsibilities. The latter two argued that careful consideration should be given to the way this issue is addressed with a view to avoid restricting lower income countries’ policy space to exploit their natural resources.

Singapore, South Africa and Kenya focused more on the issue of carbon taxes, while Japan, France and Sri Lanka spoke of a wider range of instruments. Colombia raised the issue in connection with the need to mobilise more resources and fill the climate finance gap.

Spain, Norway, Austria, Italy and France spoke about the importance of the issue, and France mentioned the joint initiative they launched with Kenya on the Taskforce on International Taxation and Climate as a benchmark that could help the UN to give greater political relevance to this issue.

Equitable taxation of multinational corporations

One of the most controversial moments of the first round of negotiations occurred on the morning of 1 May. The agenda item to be addressed was the inclusion of the issue of equitable taxation of multinational corporations as a high-level commitment. The positions of the countries were divided into two blocs. A minority bloc expressed concern that the inclusion of this issue would erode the progress made in other fora, and particularly regarding the two-pillar agenda of the OECD’s Inclusive Framework. They insisted on the alleged risks of “duplication” and argued that any discussion of these issues would have to be consistent with ongoing work in the OECD framework.

A second bloc, representing a majority of countries, advocated for comprehensive inclusion of the issue as part of the high-level commitments. Within this group, some pointed out that a forum such as the OECD’s Inclusive Framework could be considered neither transparent, nor equitable, nor inclusive, and as such it was a distortion to say that all countries had already reached agreement in this area in reference to the two-pillar agenda. The expression “140 is not 193”, referring to the number of jurisdictions that are part of the Inclusive Framework as opposed to the number of UN Member States, was heard on several occasions. They also pointed out that the Inclusive Framework was hardly a forum in which its member states could participate on an equal footing. It was also raised that the risk of fragmentation would arise from not including this issue as part of the framework convention on tax. Other states argued that including this issue would not lead to the erosion of work already done in this area but rather consolidate that work.

In his closing remarks on this agenda item, the Chair acknowledged that there are different views on the matter. He acknowledged that a group of countries were concerned with duplication but as this concern connected more with how the work would be done rather than about whether it should be added or not, he concluded the corporate taxation issues will be included to be discussed as high-level commitment in the terms of reference.

Additional topics that can be included as high-level commitments

As part of the agenda, member states suggested additional issues to include as high-level commitments in the terms of reference. These included:

Indirect taxation to contribute to domestic resource mobilisation

Institutional capacity of revenue administration

Assistance in revenue collection

Country by country reporting (the Tax Justice Network intervened on this matter)

Taxation of extractive industries

High-level commitment on fairness

Dispute prevention and resolution mechanisms (a presentation by the Secretariat was made on this)

Certainty, equality and predictability as high-level commitments.

Eradicate economic imbalances between nations

The Tax Justice Network proposed the inclusion of measures related to the ABC of tax transparency, including the proposal to create a Global Assets Register and a Centre for Monitoring Taxing Rights.

“Protocols to the framework convention could provide additional, “regulatory” aspects, with more detailed commitments on particular topics, giving countries the ability to opt-in and opt-out on the basis of their priorities and capacities. If there is sufficient agreement on certain action items, some of these protocols could be negotiated at the same time as the framework convention. This might include, for example, a protocol on measures to address the problem of illicit financial flows”.

In addition, Resolution 78/230 required the intergovernmental committee, in elaborating the draft terms of reference for a framework convention “to consider simultaneously developing early protocols, while elaborating the framework convention, on specific priority issues, such as measures against tax – related illicit financial flows and the taxation of income derived from the provision of cross-border services in an increasingly digitalized and globalized economy”.

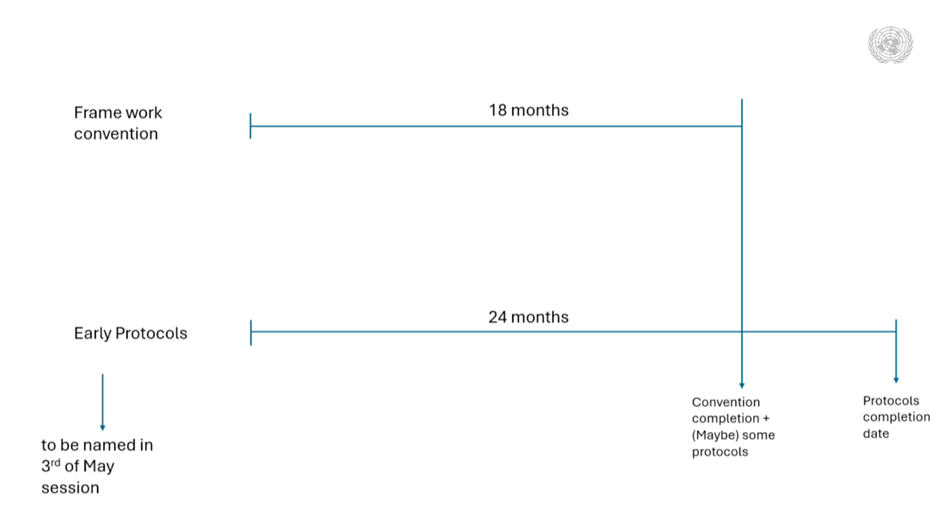

With this framework for discussion, negotiations on the 2nd and 3rd of May focused on addressing the issue of the simultaneous development of early protocols to the negotiation of the framework convention. Countries came to the session with various proposals on the issue of protocols in their written submissions. During the session on 2 May, two main blocs emerged. A first bloc proposed a sequential approach: first the framework convention, then protocols. A second bloc proposed to develop simultaneous protocols on urgent issues to respond to the needs of member states, even if they were controversial. An intermediate proposal came from the United Kingdom delegation to combine simultaneous and sequential work. The Chair summarised the proposal with the chart below.

This was followed by a discussion on the ambition of the proposed timeline, in which the African Union, India, Chile, China and others raised their support for the proposed approach, while other countries such as Sweden, Germany and Austria raised that there were still too many unknowns to make an informed decision. Argentina, Switzerland and the United Arab Emirates raised doubts as to whether simultaneity was feasible in terms of the resources that needed to be allocated. The conversation on the proposed timeline was followed by a presentation by the Secretariat on dispute prevention and resolution that some countries welcomed for providing clarity in terms of how the Framework-Protocol approach might operate.

On 3 May, the session started with a discussion of possible issues that early simultaneous protocols could address. Global south countries led with strong interventions aligned on the need to have simultaneous early protocols, with some range of issues discussed, but mainly mentioning the topics of tax-related illicit financial flows, information exchange, and taxation of cross-border services. There was some noteworthy pickup of civil society demands. For instance, India called for progress in tackling illicit financial flows by means of beneficial ownership and legal ownership registration, and Brazil suggested considering public country by country reporting.

This was countered by many OECD countries with a strong pushback against simultaneous early protocols, justified by resource constraints for parallel negotiations and the resulting need to prioritise, and by the desire to better understand how the framework convention would work and how everything would fit together,etc. In this context, controversies emerged over the understanding of some terms, including the definition of illicit financial flows.

The US took the floor and poured a bucket of cold water on the negotiations, speaking directly against three of the most frequently mentioned issues for consideration for early simultaneous protocols: tax-related illicit financial flows, information exchange and the taxation of cross-border services. The US specified that the term illicit financial flows should be interpreted to apply to criminal proceeds not only from tax crimes, but also from corruption and organised crime, and remove from scope tax avoidance which may not be illegal but “lawful” (here is why we beg to differ).

On exchange of information, the US expressed concerns that the existing international standard may be duplicated, in conflict with or eroded by any action by the UN framework convention on international tax cooperation in this area. Specifically, the US defended the standard of “foreseeable relevance” of requested information, which is the threshold for a country to exchange tax information under bilateral tax treaties and the Convention on Administrative Assistance in Tax Matters. It’s worth keeping in mind here, however, that neither the overwhelming majority of UN members nor the overwhelming majority of Global Forum members had any say in designing this standard. The standard has proven to be very cumbersome to adhere to in lower income countries, drastically reducing the effectiveness of the whole exchange of information regime in the global south.

Since the US does not participate many of the international standards it tries to defend (e.g. the US has not signed the Amended Convention on Administrative Assistance on Tax Matters; it also does not participate in the automatic exchange of financial account information under the Common Reporting Standard for Automatic Information Exchange; and often the country fails to live up to promised reciprocity under its own system of obtaining foreign account information, known as ‘FATCA’.), the US’ statement is a remarkable feat in hypocrisy.

With the US not walking the talk on tax information exchange, and oblivious to the democratic deficit in bringing about a standard for information exchange that is largely ineffective especially for lower income countries (as Tax Justice Network has explained in this briefing), designing better rules on global exchange of information can hardly be seen as an erosion of current standards. The ineffectiveness of the current standards was highlighted by Senegal by mentioning and acknowledging that information exchange is already happening, yet then emphasising how it would need to be improved for it to work for Senegal and similarly situated countries. Requests for information exchange would for example often not be answered, so at the UN, there should be a binding obligation to respond to requests with the requested data or with a valid reason why the data was not obtainable.

The discussion continued between a bloc of Global South countries arguing for the urgency of early action and prioritising the most pressing issues for resource mobilisation, and a group of higher income countries continuing to argue for the desirability of the sequential approach and the need for further analysis. Korea and Norway suggested that a Commission of International Organisations working on the Platform for collaboration be invited to provide further analysis on specific issues. Nigeria, on behalf of the African Union, made a compelling case to explain that existing rules are not catering to the needs of all countries and, therefore, urgent action is required in key areas that early protocols should address for mobilising resources to tackle poverty and other pressing challenges.

The final meeting of the first week closed with a recap by the Chair on the issues raised by delegations as priority issues for the development of early simultaneous protocols:

Cross-border services

Illicit financial flows

Digital economy

Dispute resolution

Taxation of high-net-worth individuals

Environmental and climate challenges

Exchange of information

Tax incentives

In line with the joint submission of the Global Alliance for Tax Justice and the CSO Financing for Development Mechanism that the Tax Justice Network endorsed, we believe that any elements to be developed by protocols should be covered by strong provisions in the negotiation of the framework convention itself. In our own written submission, and in line with what has been raised by several countries in the global south, the Tax Justice Network believes that an early protocol on illicit financial flows should be part of the list of protocols to be prioritised, incorporating the ABC of tax transparency – i.e. automatic exchange of information, beneficial ownership transparency and (public) country by country reporting – and the creation of a Centre for Monitoring Taxing Rights. Whether negotiated simultaneously with the framework convention or under other arrangements, these elements, as well as others that countries may wish to develop further through protocols, should be included as part of the core content of the framework convention. Capacity issues need to be carefully considered by countries in a simultaneous negotiation of early protocols from a strategic standpoint, but far from being a zero-sum game many of the bottlenecks in the more general discussions could be resolved by parallel technical negotiations on more specific issues that early protocols can address.

Roadmap for second session, preparatory work and timeline

The second week of negotiations proceeded at a slower pace, with several countries refusing to make additional interventions on substantive or procedural issues in the absence of a zero draft that captured the earlier discussions. In this context, the final days focused on reaching agreement on the way forward, as summarised in the timeline below (prepared by our partners at the Center for Economic and Social Rights).

This ambitious roadmap implies several challenges for the different actors involved in the process. For UN member states, it will involve preparations for the decisive negotiations between July and August, which given the events of the first session are expected to be very tough and complex. For countries in the global south, the stakes are measured in terms of the resources that states lose every day to respond to the climate and other interrelated crises, and to build schools, hospitals, sustainable infrastructure and to mobilise the resources with which the realisation of people’s rights can be financed. For high-income countries that until now have been in the driver seat of global tax governance, it is a simple matter of accepting that international tax norms need global support, a fair distribution of benefits and a special reckoning of the needs, priorities and capacities of global south countries. But also, a matter of recognising that universally accepted rules that correct the flaws in the current tax architecture are beneficial for all countries. Such highly needed rules might contribute to put an end to the astronomic losses that richer countries suffer from tax abuses to the detriment of their own population (which are greater in absolute terms than those of lower income countries).

Achieving a shared understanding to focus everyone’s energies on agreeing terms of reference that enable the negotiation of an ambitious convention is critical for the process. However, discussions are tough, and the negotiation issues are sensitive. Continued leadership, unity and perseverance by Global South countries – the kind that brought us to these negotiations in the first place – will be required to see this process out in a successful way.

Evidently, it will be a major challenge for countries to achieve a successful negotiation in the short time ahead. For other stakeholders involved, ranging from the Secretariat facilitating the discussions to civil society observing the process, it will therefore be key to assist countries in drawing the right conclusions to make consensus achievable. As such, the Tax Justice Network will continue to provide tools and analysis to support the negotiations, and to collaborate with partners within the tax justice movement and beyond so that the world seizes this historic opportunity for change.

Beneficial ownership transparency is a crucial tool to fight illicit financial flows. It involves identifying the real individuals who ultimately own, control or benefit from legal vehicles such as companies and trusts. Although this sounds rather simple, getting it right is a whole different story. Standards by international organisations (watered down by powerful countries) tend to be quite weak and unambitious. Even then, countries fail to meet these low standards as they lack understanding, resources or interest (or all of the above).

Against this gloomy context, a technical note published by the IMF in January 2024 on “Resolving Opaque Bank Ownership and Related-Party Exposures” is a much welcomed breath of fresh air. It is also an encouraging sign of what the IMF’s new AML strategy is capable of. The technical note deals with an issue very dear to the Tax Justice Network on who “controls the controllers”. Financial institutions are frequently bestowed with obligations to prevent money laundering, determine the tax residence of account holders, withhold account holders’ taxes or report their banking information for automatic exchange purposes. However, this system which relies on the private sector to self-supervise and to assist competent authorities often results in awful consequences (as can be expected of any system with the wrong incentives). For instance, there have been several cases of banks turning out to be complicit, or even initiators, of the wrongdoing they are meant to guard against. The Swiss leaks is one prominent example.

The IMF technical note is not just interesting for its subject matter. It also made us here at the Tax Justice Network realise that we need to update our paper on uses and purposes of beneficial ownership data to include another very important reason to provide public access to beneficial ownership information: bank stability and bank failure. Lack of beneficial ownership transparency can have an impact on the (illegal) transactions carried out by the bank’s owners, which in turn can have serious financial stability and macroeconomics effects for a country. As the technical note describes:

“If not managed properly, related-party transactions can quickly become a source of bank weakness and a threat to financial stability…Most of these [bank] failures (16 out of 22) were largely attributed to extensive abuses by beneficial owners of bank resources in a manner affecting viability….In Indonesia, excessive related-party exposures were one of the key contributors to the country’s banking crisis in the late 1990s… the channeling of funds to finance beneficial owners was a common practice” (pp. 22 and 34).

Some could argue that if public access to beneficial ownership information is needed to prevent bank failures, then it should only apply to the banking sector rather than generally. However, the same counter-argument (that we’ve repeated many times) applies: if you don’t cover absolutely all companies, then secrecy (for corruption, fraud or bank failure) will move up the chain, to the contractor or supplier. Indeed, the same happens with banks where secrecy is not present in the bank itself, but in the secretive entities engaging in (undisclosed) related-party transactions:

“[…] the experience of some jurisdictions with material related-party problems shows that although the banks’ immediate related parties, such as managers or controlling shareholders, were mostly known to the authorities, numerous borrowing entities that were de facto connected to these related parties were not reported as such.” (P. 26)

Apart from offering us a new purpose and case for public access to beneficial ownership, the technical note offers several recommendations that are completely aligned with the Tax Justice Network’s position on beneficial ownership transparency. The following table presents a summary of our papers and proposals compared to extracts from the technical note pointing to the same ideas.

The Tax Justice Network’s proposals compared to the IMF paper’s proposals

The Tax Justice Network

IMF technical note on banking ownership (extracts)

As proposed for instance by our roadmap to effective beneficial ownership transparency (REBOT), all countries should establish public access to beneficial ownership information. We have published a report addressing the privacy, data protection and human rights perspective in favour of public access to beneficial ownership information.

“It is good practice to require public disclosure of a bank’s beneficial owners.” (p. 9)

“Common characteristics of opaque ownership structures include (1) excessive layers of ownership (for example, chains of holding companies)… (2) owners’ residency in foreign jurisdictions… (3) complex usage of available legal persons and arrangements (for example, special purpose vehicles, trusts).” (p. 9)

“A common problem relates to narrow or unclear definitions of … “significant ownership,” or other relevant terms; for example, exclusively based on quantitative indicators such as ownership thresholds. Definitions may fail to capture voting rights being exercised without legal ownership (for example, under a collateral arrangement) or preferential voting rights (for example, veto rights).” (p.11)

Some of our policies in our roadmap focus on addressing complex ownership structures and incentivising compliance go way beyond international standards. These include proposals to reduce the number of allowed ownership layers, lowering (or eliminating) thresholds, prohibiting discretionary trusts, disallowing foreign entities based in secrecy jurisdictions from owning local assets or entities, and applying the “constitutive effect” so that registration is a pre-condition for having or exercising rights.

Additional legal amendments, beyond international standards, may need to be considered… examples of enhancements include (1) restricting the complexity of bank ownership, for example, by limiting the number of ownership layers; (2) lowering the threshold for direct and indirect “significant ownership,” to enable the supervisor to deal with opaque ownership structures and concerted actions that were designed to keep the relative share of individual shareholders just below preexisting regulatory thresholds… that full disclosure of beneficial ownership.… is a precondition for exercising their shareholder rights;… (6) explicitly empowering the supervisor to declare a specific ownership structure as “nontransparent” and, thus, in breach of licensing requirements; (7) explicitly stipulating in law that bank owners or shareholders from jurisdictions that are uncooperative for the purposes of prudential supervision, or are considered to have strategic AML/CFT deficiencies, do not meet suitability requirements” (p. 11 and 13)

Our roadmap together with our papers on trust registration around the world and abuses of offshore trusts describe the risks of trusts (especially discretionary trusts) and propose ways to disallow them or counter their harmful effects.Our roadmap and paper on why beneficial ownership registries aren’t working also recommend identifying those with a power of attorney as beneficial owners with control.One of our first papers on beneficial ownership, published back in 2016, proposed identifying the 10 or 20 biggest shareholders in cases where no individual passes the threshold to become a beneficial owner (instead of following the Financial Action Task Force’s requirement to identify a senior manager).

Box 3 on Ukraine’s indicators on non-transparent ownership:“* Trust: Presence of a discretionary trust in the ownership structures* Power of attorney: Issuance of power of attorney…* … For shareholder structures with more than 20 natural persons, the largest 20 individual shareholders were defined as ‘key participants.’” (p. 12)

Our paper Rethinking limited liability: beneficial ownership transparency to reform the liability system proposed ways to ensure beneficial owners or ultimate shareholders are held liable. This liability should also apply to any earnings that shareholders, beneficial owners or directors obtained from the company, even if they are no longer related to the entity by the time the liability arises (within some reasonable timeframe). In other words, if John as a shareholder got dividends worth $10 million from company A, then sold his shares to Mary and after a few months company A cannot repay its debt, then at least part of $10 million previously paid out to John should be used to repay current creditors, even if John is no longer a shareholder or beneficial owner. In essence, if there’s a cap in losses, there should be a cap in gains.

“The civil liability of beneficial owners and other related parties for a bank’s failure may be based on a combination of general and specific rules. The bank can pursue its claims from related parties on different legal grounds, for example, contract, tort, or unjust enrichment.” (p. 35)

Our roadmap as well as our paper on beneficial ownership verification proposes sophisticated checks to detect registered owners who are actually nominees serving as owners. These checks include checking whether the registered owner could have afforded acquiring their shares to begin with, based on their declared income or wealth.Likewise, our paper on complex ownership structures recommended reversing the cost equation. As things stand now, complexity is free for those who create it and costly for authorities and investigators who seek to identify the beneficial owner hiding behind the complicity – a task that often proves impossible. Our recommendation was to reverse this situation, and make it costly and burdensome (or even forbidden) to create complex ownership structures. This would be similar to how Dutch banks started charging higher fees to customers with complex ownership structures because of the extra costs the banks incurred when performing due diligence.

“verify that beneficial owners have no record of criminal activities or involvement in illicit activities or suspicious practices. It should also assess their financial soundness, that is, the sources of funds for the acquisition of bank shares… The financial soundness assessment is a key tool to identify potential “strawmen” (that is, nominal shareholders that lack financial strength and act in the interest of an undisclosed beneficial owner). In jurisdictions with legacy opaque shareholder structures of systemic proportions, this assessment may call for identified beneficial owners to submit audited financial statements, tax returns, bank account statements, independent personal asset valuations, and other documents.” (p. 16)

Our paper on beneficial ownership verification delves into the risks and challenges of verifying beneficial ownership information and proposes various methods for verifying that information and detecting red flags. One challenging example is detecting cases where trusts disguise distributions to beneficiaries (eg paying their tuition fees or credit card expenses) as if they were expenses belonging to the trust. The IMF paper proposes additional, very good ideas on how to detect undisclosed relationships between entities and how to identify nominees and shell companies.

“*Exclusivity: For example, no other financial institution unrelated to the bank is lending to the party, and the amount and type of loans do not justify it from an economic point of view.

*Economic dependency: For example, most of the party’s revenues come from the bank or its related parties …

*Common infrastructure: For example, common or very close business addresses (physical or virtual) with the bank and its related parties; common operational structural elements; common managers or staff; and common suppliers, service providers, or customers.

*Underwriting standards: For example, material disproportion between proceeds, tenor, and terms and conditions; legal form of transaction differs from their economic essence; and the terms and repayment conditions differ from the current market conditions.

(…)

*Indebtedness and creditworthiness: For example, at the onset, the loan is unlikely to be repaid as stipulated in the contract, given creditworthiness and available repayment sources; and credit rating below the minimum considered acceptable by the bank.

*Interest rates, fees, and prices: For example, interest rate and fees to be paid to the bank are substantially lower than for clients with similar economic and financial characteristics, and prices paid by the bank for assets or received services differ from market prices. (p. 27)*Loan transactions in the weeks prior to material capital injections (for example, those exceeding a certain percentage of total capital during the past five years) should also be reviewed to ensure that the injections have not been effectively funded by the bank itself.

*The sample should also include some transactions that do not directly involve credit exposures, for example, purchase and sale of financial instru¬ments and nonfinancial assets, acquisition of assets in lieu of loan repayment, and service contracts, such as for asset management, advice, and other major professional services (for example, information tech-nology development, database management, auditing, and loan workouts).” (p. 30)

Conclusion

This technical note is an excellent example of the role that the IMF can and should take to bring about real progress on beneficial ownership transparency. For instance, the IMF could start requesting major financial centres to publish beneficial ownership information of their banking sector. This would allow beneficial ownership transparency to move beyond the weak international standard set by the Financial Action Task Force. We hope to see more of this ambitious approach when the IMF engages with countries on capacity building and financing, and when the IMF give feedback on current international standards. In this regard, a protocol on beneficial ownership transparency to the UN Framework Convention on International Tax Cooperation (the UN Tax Convention) would also ensure more transparency for all countries.

Countries at the UN are currently negotiating the parameters of a UN framework convention on tax, which could deliver the biggest shake-up in history to the global tax system. The final parameters – aka the “terms of reference” – will be published in draft form in August, and voted on by the full General Assembly, likely in November.

We’ll be sharing rolling updates on this blog here over the coming months in the run-up to the UN vote on the terms of reference.

Countries voted by a landslide majority last year to begin negotiations on establishing a UN tax convention. The convention has been heralded as countries’ best chance to avoid losing nearly $5 trillion to tax havens over the next decade.

What makes a UN tax convention so game-changing isn’t just the changes it would make to existing global tax rules, but the way it would dramatically change how global tax rules are decided. For over 60 years, global tax rules have been decided behind closed doors at the OECD, a small club of rich countries whose members include some of the world’s most harmful tax havens. A UN tax convention would require global tax rules to be decided democratically and transparently at the UN, where all countries can be heard on global tax rules that affect us all.

26 April – 8 May: The committee will hold its First Session, where all countries will have an opportunity to inform the provisional work of the committee on the terms of reference.

29 July – 16 August: The committee will hold its Second Session, where all countries will have an opportunity to input and negotiate on the final draft of terms of reference before the terms go to a vote near year-end.

November/December TBD: The UN General Assembly will vote on whether to accept the terms of reference prepared by the committee for a UN framework convention on tax. If passed, countries will negotiate the content and meat of the framework convention in 2025, with a view to put the convention to a vote near year-end in 2025.

Positions raised at First Session of the Ad Hoc Committee, 26 April – 8 May 2024 Positions submitted in writing ahead of the First Session of the Ad Hoc Committee.

Transcripts of the First Session of the Ad Hoc Committee, 26 April – 8 May 2024

Please note that these transcripts are automatically generated by transcribing software and may contain errors.

The Tax Justice Network ran similar live rolling blogs in 2023 and 2022 on the previous stages of the UN process leading towards a UN framework convention on tax. The 2023 blog is available here. The 2022 blog is available here.

Show less ▲

🔴 – Live updates

Wed 27 Nov 2024

17:45pm GMT: Alex Cobham covers the live vote via Bluesky

Here’s the resolution on ‘Promotion of inclusive and effective international tax cooperation at the United Nations’, put forward by Nigeria on behalf of the Group of African States: undocs.org/A/C.2/79/L.8

Bizarre first contribution from Argentina, whose delegate explains the country has embarked on ‘a new model’ and therefore has marked a set of paragraphs in the text from which it disassociates itself, including the 2030 Agenda, SDGs, climate change(!), and introduces its own definition of gender…

Russia next, also supports the resolution and also disassociates itself from some paragraphs- in Russia’s case, those referencing the Pact for the Future

The Nigerian delegate now introduces the motion, summarising the path through agreement on the draft terms of reference by which the countries of the world have arrived at this point

“The Africa Group believes that achieving an equitable and inclusive framework (for tax) will benefit all… We must seize this moment to strengthen cooperation… Only together can we pave the way for a fairer and more sustainable future.”

Hungary, speaking for the EU, is raising a ‘technical clarification’. It’s not a good sign that Hungary is speaking – they and France are understood to be the main opposition to the resolution, within the EU.

The Nigerian delegate explains that the change was a technical one to address a redundancy in the text (a repetition of language on geographical scope)…

Hungary says that they are not fully satisfied, and that this change undermines consensus. (This seems petty…)

Nigeria’s delegate explains that OP2’s language reflects the consensus from the ad hoc committee, and that reopening this would undermine and delay the process. On OP5, the Africa Group believes that the organisational session of the negotiations in 2025 must determine decision-making rules.

UK delegation speaking to its abstention on OP5, and the importance of consensus – but note “the openness to progress”, opportunity to agree at the organisational session, and stresses its commitment to work with all partners. Interesting shift – might UK reverse its opposition on main vote?

US – a leader of the opposition – now speaks, to call a vote on the whole resolution. “We would have preferred to join consensus” but refuse because the text does not require full consensus. Ignoring the earlier discussion…

The Nigerian delegate emphasises that voting *against* the resolution would be a vote against multilateralism, and against the interests of developing countries in particular.

15:00pm GMT: Second Committee, 26th plenary meeting – General Assembly

Today, the UN General Assembly votes on the UN Tax Convention Terms of Reference.

13:00 pm : Sergio Chaparro-Hernandez update ahead of the todays vote at the UN on Adoption of the #UNTaxConvention Terms of Reference.

📢Today, the United Nations will take the final step to begin negotiations on the most important international tax treaty in history: the #UNTaxConvention 📃 What to expect from the vote today? What is the value of this process in the current international context? 🧵👇#VoteYespic.twitter.com/9xi9UPtOm3

— Tax Justice Network @TaxJusticeNet.bsky.social (@TaxJusticeNet) November 27, 2024

This year the Ad Hoc Committee worked on the drafts terms of reference that set the parameters for the negotiation of the #UNTaxConvention in the next three years. The vote at the Ad Hoc Committee showed opposition softened as only 8 countries (#TheHarmfulEight) voted against. pic.twitter.com/a0lCE6m7WT

— Tax Justice Network @TaxJusticeNet.bsky.social (@TaxJusticeNet) November 27, 2024

What to expect ahead of the vote? The South bloc (G77 countries) with a few exceptions will likely remain solid in its support to the process. The question is if rich countries will understand this is the best chance to reform international tax rules in the current context. pic.twitter.com/nVZpKwE6RO

— Tax Justice Network @TaxJusticeNet.bsky.social (@TaxJusticeNet) November 27, 2024

👁️Don’t miss our live blog tracking developments on the road to this critical UN vote towards a #UNTaxConvention. 📺Follow the vote in our live blog today at 10am (EST) 👇https://t.co/Q0TTNfGkKG🔴live-un-tax-negotiations/ @SergioChaparro8

— Tax Justice Network @TaxJusticeNet.bsky.social (@TaxJusticeNet) November 27, 2024

Fri 16 Aug 2024

9:45pm GMT+1:Countries ‘bash open’ door to historic tax reform at UN

Countries have just voted by a landslide majority to adopt an ambitious scoping document for a UN tax convention, after months of negotiation. The document1, referred to as the Terms of Reference, sets out ambitious parameters and a clear roadmap for the next stage of negotiations, to being next year, on a framework convention and early protocols. The parameters secured set a strong enough basis for countries to deliver the biggest shakeup in history to the broken tax system.

7:33pm GMT+1:The ICRICT commission’s statement calls on UN member states to vote YES on terms of reference

The Commissioners state:

“The vote today on the ToRs provides an historic opportunity to advance international tax cooperation in an inclusive and sustainable manner and we encourage Member States to vote YES to the draft as it stands.”

12:15pm GMT+1: Countries to vote today on ambitious scope for UN tax convention after months of negotiations

Economists, civil society organisations and campaigners from around the world are calling on countries to back the ambitious scoping document for a UN tax convention that emerged yesterday after months of negotiations at the UN. The document1, referred to as the Terms of Reference, sets out the principles and protocols that will inform the framework convention, and has retained enough of its original ambition to deliver the biggest shakeup in history to the broken global tax system, the Tax Justice Network says.

10:00am GMT+1: Tax Justice Minute: Sergio Chaparro-Hernandez wraps up the second week of the final negotiations.

Wed 7 Aug 2024

The second week of negotiations on terms of reference for the UN Tax Convention is in full swing. Having stormed through discussions on the objectives and preamble of the draft ToR, vying national interests are now on full display as countries debate the principles that will underpin the Convention.

Of critical importance to tax justice advocates is the incorporation of strong human rights language into the terms of reference. On Monday and Tuesday, an arduous debate ensued on the exact function and location of such language in the ToR. Broadly speaking, countries’ opinions were divided across three positions. Colombia and a number of other Latin American countries fought compellingly for human rights obligations to be included in the principles section the preamble. Embedding human rights standards in the operational part of the document as a principle means they can serve as one of the concrete guidelines of the work under the Convention besides other principles like ‘transparency’ or ‘the fair allocation of taxation rights’. Inserting human rights as a principle aims to ensure the Convention meaningfully advances the wellbeing of ordinary people in all countries. It would also require a specific focus on the needs of marginalised sectors, such as women, minority ethnic groups, persons with disabilities and other discriminated-against groups.

As things currently stand, the principles section of the ToR states that efforts to achieve the objectives of the Convention should “be fully aligned with international human rights law and States’ existing commitments under human rights conventions to respect, protect and fulfil all human rights for all people in all countries”.

Perhaps surprisingly, the position of including human rights as a principle was strongly and repeatedly opposed by the African countries and by India. As explained by the African Group, not including human rights as a principle does not equate to the continent dismissing human rights obligations. On the contrary, efforts to mobilise domestic resources to increase living standards and human rights adherence are the key priority for Africa. But in their view, this will be achieved by fair and equitable tax rules between countries. India agreed, but not without calling a cat a cat: if a general reference to human rights is adopted as a general principle, it could be used to block things like effective exchange of information.

The African and Indian position needs to be understood in relation to the third position, that taken by many of the countries in the Global North. Having voted against the process towards a UN convention on tax last year, these countries were quick to support the inclusion of a general human rights principle which – in their view – mostly serves to anchor the protection of taxpayer rights. After all, it is these individual human rights – the right to privacy, the right to property – which tend to be most enforceable (or most frequently enforced, at least).

As illustrated in recent jurisprudence by the European Court of Justice (see here and here), individual human rights like the right to privacy do not always align with progressive tax agendas. On the contrary, wealthy global North taxpayers aiming to stretch the scope of these rights in local courts may altogether hinder progress. Hence, the African and Indian skepticism and the grim realisation for all others involved that even a seemingly obvious reference to universal human rights – core values on which the UN forum is built – can be weaponised against a progressive agenda or, at least, is perceived by a large part of the Global South as entailing such risk.