Welcome to the 30th edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to share it. You can also join the programme on Facebook and on Twitter.

In the 30th edition of Taxes Simply:

Walid Ben Rhouma and Osama Diab discuss new statistics issued by the Central Agency for Public Mobilization and Statistics (CAPMAS) on the economic impact of the coronavirus on Egyptian households; the discussion focuses on the social groups most affected by the crisis and the unequal impact of the crisis.

Plus: we present a summary of tax and economic news from the Arab region and the world including: 1) A new agreement between Egypt and the IMF 2) The United States blocks a proposal to tax multinationals and 3) The fears for a Tunisian economic contraction.

الجباية ببساطة #٣٠ – الأثر غير المتكافئ لجائحة كورونا على الدخل

أهلا وسهلًا بكم في العدد الثلاثين من الجباية ببساطة. في الجزء الأول من هذا العدد يتناقش وليد بن رحومة وأسامة دياب حول إحصائيات جديدة صادرة عن الجهاز المركزي للتعبئة العامة والإحصاء المصري عن أثر فيروس كورونا الاقتصادي على الأسر المصرية، ويتمحور النقاش حول أكثر الفئات تضررًا من الأزمة والأثر غير المتكافئ للأزمة.

في القسم الثاني نتناول ملخص لبعض أخبار الضرائب والاقتصاد من المنطقة العربية والعالم، ويشمل ملخصنا للأخبار: ١) اتفاق جديد بين مصر وصندوق النقد؛ ٢) الولايات المتحدة تعطل مشروعا لفرض الضريبة على الشركات متعددة الجنسيات؛ ٣) توقعات بانكماش الاقتصاد التونسي.

Here’s the 17th edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa produced and presented by finance journalist Idriss Linge in Cameroon. Nous sommes fiers de partager avec vous cette nouvelle émission de radio/podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Pour cette 17ème édition de votre Podcast Francophone « Impôts et Justice Sociale », nous revenons sur l’outil de mesure du niveau d’exposition des pays aux Flux Financiers Illicites. Cette plateforme développée par Tax Justice Network, permet à diverses catégories d’utilisateurs, de mesurer le risque de fuite des capitaux qui existe entre les pays et leurs partenaires commerciaux. Nous revenons aussi sur les débats parlementaires au Cameroun, où un député interroge le gouvernement sur les cadeaux fiscaux faits aux entreprises du fait de la crise, alors que le pays a besoin de ressources. Nous interrogeons enfin divers acteurs de la société civile africaine sur les questions de transparence budgétaire en Afrique

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

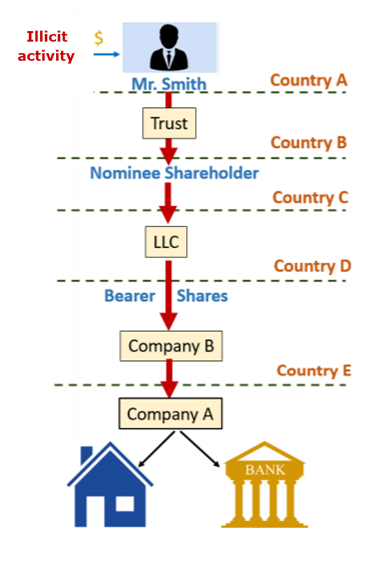

Leak after leak has confirmed what African citizens have long suspected: the elite hide their actions and identities to loot state resources and reduce taxes owed. A new study published today by the Tax Justice Network Africa and Tax Justice Network examines one of the steps African countries are taken to address this issue: beneficial ownership transparency.

Earlier this year, the International Consortium of Investigative Journalists investigated Africa’s wealthiest woman, Isabel dos Santos, who is the daughter of former Angolan President José Eduardo dos Santos, for allegedly moving millions in public assets and revenue out of Angola.

Comprising over 715,000 documents, the Luanda Leaks on the surface sounds like just another story of corruption in Africa. However, the leaked documents suggest that dos Santos and her husband were only able to move the ill-gotten gains thanks to a web of at least 94 secrecy jurisdictions across the world through an “archipelago of shell companies”.

“‘African corruption’ is only African as regards its victims, its perpetrators are institutions and individuals from across the globe who are willing to loot without conscience as they watch their offshore accounts grow.”

Financing Africa’s development is deeply undermined by global financial secrecy. Illicit financial flows exiting the continent dwarf overseas development assistance entering the continent, and erode the sovereignty of nations in raising revenues domestically for public expenditure and investment.

African countries are taking action to domestically address financial secrecy, including requiring the beneficial owners of companies, partnerships, foundations and trusts to register. Identifying, registering and disclosing the real people (beneficial owners) who ultimately own or control legal vehicles is a key policy for promoting and protecting domestic revenue mobilisation that may otherwise be eroded by illicit cross-border financial transactions including money laundering, tax evasion and avoidance, corruption and terrorist financing.

Beneficial ownership registration was placed squarely on the African agenda to address illicit financial flows in 2015, with the launch of the African Union and United Nations Economic Commission for Africa’s report of the High Level Panel on Illicit Financial Flows from Africa. The High Level Panel was emphatic that the year-on-year haemorrhaging of government revenues was a fundamental obstacle to achieving sustained human development, the fulfilment of basic human rights and the ending of poverty.

Beneficial ownership disclosure can allow better oversight by the public and their representatives, especially when entities are involved in extracting mineral resources that are vested in the state on behalf of the people or are bidding for public contracts. For example, beneficial ownership information is vital for monitoring compliance where countries have mineral and local content laws in place that require a certain proportion of mineral rights be held by indigenous groups, or nationally-owned or majority women-owned companies be prioritised in a mining company’s procurement of goods and services.

The state of play of beneficial ownership in Africa today

A new study published today by the Tax Justice Network Africa and Tax Justice Network examines the progress being made towards beneficial ownership transparency in 17 African countries. This draws on the data from the Financial Secrecy Index 2020 and complements a global study of beneficial ownership registration.

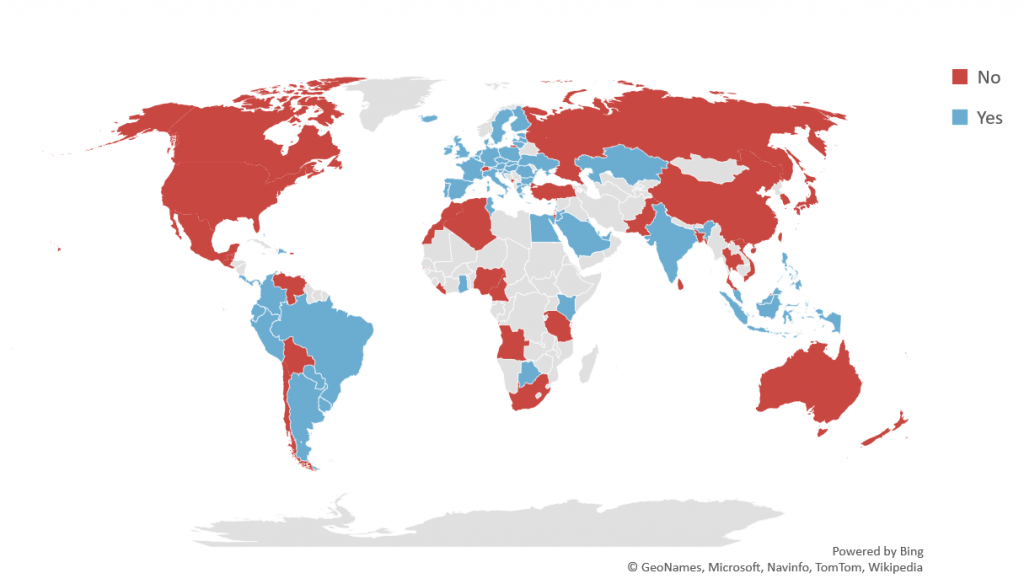

The study finds that seven jurisdictions have introduced legislation requiring the registration of beneficial ownership information. These are Botswana, Egypt, Ghana, Kenya, Mauritius, the Seychelles and Tunisia.

Botswana joins just three other countries worldwide (Argentina, Ecuador and Saudi Arabia) that have transparent measures for companies that can be interpreted as requiring all beneficial owners with just one share to register.

Across the world, 81 of the 133 countries assessed in the Financial Secrecy Index have laws and regulations for beneficial ownership registration. Of these countries, 68 countries have partial or complete registration of beneficial owners, and in some cases, this is not only for companies, but also for partnerships, foundations and trusts.

Jurisdictions with laws and regulations for beneficial ownership registration in 2020

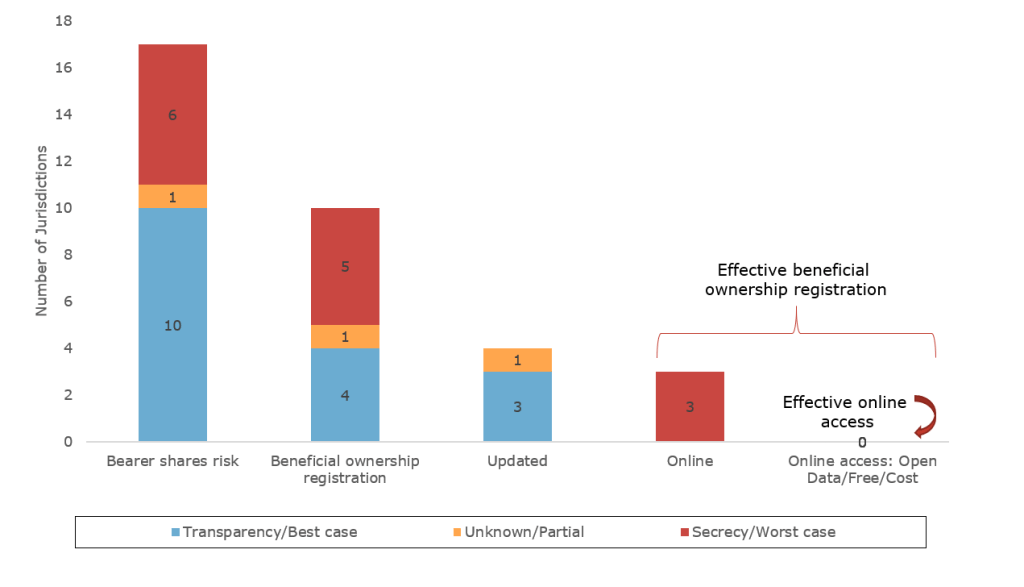

Effectiveness of laws is, however, limited in countries that continue to allow bearer shares and where updating information is not mandatory. No African country makes beneficial ownership information available online, for free, for all sectors, and for all legal vehicles.

The chart below shows the state of play for beneficial ownership registration of companies in Africa. For beneficial ownership registration to be effective, bearer shares must be cancelled, be made unavailable or be immobilised. All domestic companies must be required to register all of their beneficial owners in all cases, except for common exemptions for state-owned companies and listed companies. The effectiveness of beneficial ownership registration is also dependent on the information being updated along with the threshold set for registration; it should not be higher than the “more than 25% ownership” threshold. For the greatest transparency, all information should be available online, ideally for free and in open data format.

Effective registration of company beneficial ownership information

In 6 of the 17 assessed African countries, bearer shares have not been immobilised as shown in the first column of the chart below (Angola, Kenya, Liberia, Morocco, South Africa, Tanzania). The second column shows that of the 10 countries where bearer shares do not pose a risk, only Ghana, Botswana, Seychelles and Tunisia require the registration of all beneficial owners of all types of companies with a government authority, like the Registrar of Companies. The next column goes on to show that in only three jurisdictions – Ghana, Botswana and the Seychelles – does this information have to be updated. In none of the assessed countries does this information have to be online.

This year progress is expected for ending anonymous companies extracting solid minerals, oil and gas in Africa. Countries participating in the voluntary Extractive Industries Transparency Initiative are required to introduce public registries for beneficial owners of mining, oil and gas companies. Yet beneficial ownership transparency is required for all sectors.

Recommendations

The study makes practical recommendations on how countries can implement beneficial ownership registration and improve the effectiveness of disclosure. In summary:

Beneficial ownership provisions should apply to all legal vehicles in all sectors, including companies, partnerships, foundations and trusts.

All bearer shares should be prohibited or at least immobilised by a government authority.

The definition of beneficial owner should not have a minimum threshold, ie, registration should apply to every shareholder holding at least one share.

Legal and beneficial ownership information provided should be comprehensive, accurate and up to date and for the full ownership chain.

Registered beneficial ownership information should be verified and non-compliance should be met with sanctions.

Registries housing legal and beneficial ownership information should be made publicly available.

Such domestic action is critical for African countries. Yet the main providers of financial secrecy lie outside the continent. Thus furthering the global movement towards greater public beneficial ownership disclosure is required. Making information public across all jurisdictions will provide African governmental regulatory authorities and watchdogs, financial institutions, investors, journalists and civil society groups with access to information for investigations, asset recovery, public contracting, entering mining contracts, improving tax compliance, and more.

The continent must continue to stand united in requiring those most complicit, especially former colonial powers, to make this information publicly available.

We recently published a two part Tax Justice Focus special on climate crisis and tax justice. This blog reproduces the article by Jacqueline Cottrell, in which she explains that while carbon taxes were once at the centre of discussions about tackling climate crisis, aggressive lobbying by fossil fuel advocates persuaded the public that they are regressive and would hit the world’s poorest hardest. In this article Cottrell calls for citizen’s assemblies to embed carbon taxes in a broader progressive agenda. Click here to download the first and second parts of our Tax Justice Focus special.

by Jacqueline Cottrell

Myth-busting

It is an old story of neoclassical economics that policymakers must be prepared to trade off positive environmental outcomes and GDP growth. Today, in the European Union at least, this myth has been overcome; policymakers now refer to green taxes as “growth-friendly” and are supportive of a European green deal. Myth-busting has been relatively successful – and for good reason. None of the huge body of scientific research conducted to examine the impacts of carbon taxation have produced any evidence that it has a negative impact on GDP growth. Instead, research has indicated that a carbon price is the most efficient and effective instrument to reduce GHG emissions, whether implemented by means of taxes or trading.

When it comes to carbon taxation and social equity, however, many myths persist. It is received wisdom that carbon taxes are unfair and inequitable and have a disproportionately negative impact on lower income groups. The reality is more complex. To understand it, we need to take a closer look at the different dimensions of inequity relevant to climate policy and carbon taxation.

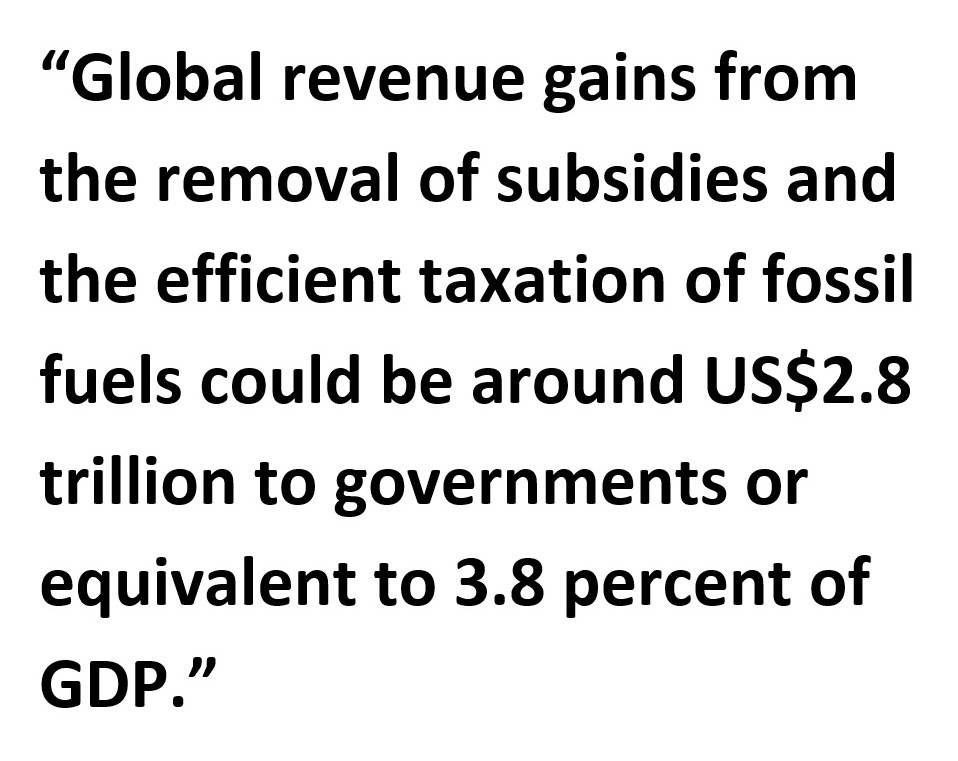

Let us look first at policy outcomes. Without additional welfare spending, carbon taxes may lead to price increases that have negative impacts on lower-income households. On the other hand, carbon taxes can raise really substantial amounts of revenue. A tax of US$70/tCO2 has the potential to raise revenues worth 1-3% of GDP in most countries, or 2-4% of GDP in major developing economies such as China or India. This implies that in low- and middle-income economies, with an average tax-to-GDP ratio of just 12%, carbon taxes can raise 25% more revenue.

In most of low and middle-income countries, the revenues a carbon tax of US$70/ tCO2 could raise dwarf current spending on health, education or welfare. Carbon taxes have the potential to act as a hugely powerful engine for change, reducing inequality and establishing targeted welfare programmes and free health and education systems, as well as funding the transformative changes required to tackle and adapt to the climate emergency.

The second dimension pertains to inequity of contributions to the climate crisis. In 2015, Lucas Chancel and Thomas Piketty found that just 10 percent of the global population – amongst the world’s wealthiest – emit 45 percent of global CO2 emissions. The bottom 50 percent of emitters, almost exclusively from developing countries, are responsible for just 13 percent of global emissions. If we do not implement a carbon tax for social equity reasons, we are letting these 10 percent of polluters get away without paying for the impact of their excesses on the global climate.

Seen in these terms, and assuming that appropriate redistributive mechanisms are in place – free installation of small-scale renewable energy such as rooftop solar, solar water heating or biogas, distribution of clean energy-efficient stoves, cash transfers, or a carbon dividend as proposed by James Boyce in this issue – a high carbon tax, of which 45 percent is paid by the top 10 percent of polluters, has an air of “Robin Hood” about it. The final dimension of inequity relates to climate change outcomes: the devastating impact of the crisis will be most felt by the poor and vulnerable groups, as they will be least able to adapt or respond.

So, why have we not reached agreement on a global carbon tax? The answer to this question is way beyond the scope of this article. But at least one of the reasons is also linked to inequity: in this case, inequity of representation in policy-making. Many industries and individuals have a strong financial interest in the status quo: oil and mining companies, energy-intensive industry, wealthy consumers (let me remind you: around 10 percent of the global population responsible for 45 percent of GHG emissions), to name but a few. These groups exert a great deal of influence in global policy debate, while the voices of the world’s poor and vulnerable are hardly represented.

In contrast to big business, which spends billions lobbying governments every year, civil society is underfunded and poorly organised in comparison, and up until now, has tended not to focus on tax policy.

The joy of tax?

Some citizens are passionately interested in taxes and recognise their potential to shape our societies, looking to Scandinavian countries as an example. All Scandinavian countries have a carbon tax: Sweden has the mother of all carbon taxes, at a rate of US£127/tCO2. Nevertheless, life in Sweden is relatively normal: there are no blackouts, people still drive Volvos, dance to Abba and shop at IKEA, while Sweden leads the way in decarbonising electricity, heating and transport.

On the whole, however, interest in tax policy is limited, including carbon taxes. Josephine Public does not know much about carbon tax, and certainly does not appreciate its potential to raise revenue worth between 1-4% of GDP. Neither does Josephine know that these revenues could be redistributed in whatever way governments see fit, or that they have the potential to transform our societies and economies through redistributive mechanisms, increasing investment in health, education, jobs, low-carbon industries, and access to sustainable energy for all.

Josephine also doesn’t know the best news of all: carbon taxes are fair, as the wealthiest and the biggest polluters pay the most.

Unfortunately, in reality carbon taxes generally hit the headlines when they are perceived as being too high, unfair, or punitive. Articles in favour often cite policy wonks arguing about “externalities”, “the social cost of carbon” and “market failures”. Even if this jargon means something to tax justice campaigners and climate activists, it does not serve well as a call to arms for the typical wo/man on the street. How can we change this?

Mainstreaming

In the past, we did not take the climate crisis seriously enough. Initial responses to “global warming” were not proportionate to a threat to our continued existence on the planet.

In the Northern hemisphere, many joked about warming sounding quite promising. In the global South, governments prioritised GDP growth, calling on high-income governments to tackle climate change given their historical responsibility.

Climate scientists were rightly cautious about drawing a causal link between individual extreme weather events – hurricanes, typhoons, droughts, desertification, devastating floods – and the climate crisis, a reticence which has served as ammunition to climate deniers.

Today, our vocabulary and our understanding has changed. Where public discourse once referred to “climate change” or “global warming”, we now talk about the “climate crisis” or the “climate emergency”. The good news is that this reflects a growing shared understanding of the seriousness and immediacy of the problem.

All over the world, street protests are putting climate action centre stage: schoolchildren and students are participating in “Fridays for Future” strikes, while citizens old and young are joining the Extinction Rebellion’s calls for decarbonisation. In October 2019, 400 scientists joined protests on the streets of London, several of them contributors to IPCC reports on climate change.

Yet to go further and achieve decarbonisation, these movements need to identify and articulate specific policy demands. Policy wonks contend that the best carbon tax would be a global one – to prevent distortions between countries and keep decarbonisation as efficient as possible. The question is: How might a global carbon tax be achieved?

The Extinction Rebellion in the UK is calling for a citizen’s assembly. Taking a global approach and creating a number of citizen’s assemblies, one for each continent, or part of a continent, would take the instrument debate out of clandestine meetings between big business and policymakers and move it into the public domain, to a place where evidence is public and subject to scrutiny.

Citizen’s assemblies would put the evidence in favour of carbon taxation, alongside other instruments, before a wide audience. It would give experts the opportunity to explain why carbon taxes are a good thing, that they can be effective, fair and equitable, and that their revenues can be used to reshape the societies and economies we live in. I believe that under such circumstances, the case for a carbon tax would win out.

Mainstreaming climate policy discussions through citizen’s assemblies would create a platform for the planet’s inhabitants all to be vocal in our support of ambitious climate policy in general and carbon taxes in particular. The results could be fed into UNFCCC negotiations and drive the step change in climate policy which is both urgently necessary and sadly lacking. What a coup for the UK government at the COP26 in Glasgow if they could negotiate a global agreement to implement a series of global citizen’s assemblies in 2021?

Ultimately, we have to recognise that one way or another, we are all going to have to deal with the climate crisis. We can choose to address it now with a carbon tax, reducing GHG emissions and using revenues as an engine for enhancing social equity and transforming our economies and societies according to our democratic wishes. Alternatively, we can pass the problem on to future generations and leave them to look on, powerless, as the climate emergency transforms our societies and economies in ways that we cannot imagine. Putting this choice in the hands of global citizens now is the only equitable way forward.

* Jacqueline Cottrell is an environmental fiscal policy consultant active in the field of development cooperation for numerous international organisations. She is a Senior Associate at Green Budget Germany and a member of the international programme committee of the Global Conference on Environmental Taxation. Her publications include a study on fiscal policies to address the health impacts of the transport sector in Jakarta, Indonesia (UNEP, forthcoming), A Climate of Fairness: Environmental Taxation and Tax Justice in Developing Countries (VIDC 2018), andEnvironmental Tax Reform in Developing, Emerging and Transition Economies(German Development Institute, 2016).

Faulkner wrote: “The past is never dead. It’s not even past.”

As we discuss, the legacy of centuries of institutionalised racism is that a wealth chasm has been created between black and white communities.

We also know that the City of London in Britain built its wealth from slavery and empire. Still today, major finance sectors have extractive business models which impoverish some of the world’s poorest nations. And, financial secrecy is another form of empire.

So how can we think about combining tax justice and reparations? Keval Bharadia‘s work on a super tax on the $8 trillion a day financial markets could help show the way. And all financial institutions must have independent slavery money audits. For those financial institutions now coming forward and offering what they’re calling reparations funds, how do we ensure that these funds are large, they’re targeted to the right places, and they’re ongoing?

A transcript of the programme is available here (not 100% accurate)

Produced and hosted by Naomi Fowler of the Tax Justice Network

We’re recovering from many things. We’re recovering from COVID-19, we’re recovering from 400 years of oppression, and we are also recovering from a looming economic downturn. And one thing we know for sure, and we continue to learn with every economic downturn is that States have choices. They have a choice point and that’s to cut services and continue to cut their budgets that harm families that are in need – or raise revenue, raise revenue on corporations, raise revenue on those that are most profitable and the wealthy. And that’s a racialised choice, given the country’s history and ongoing biases.”

There needs to be a proper negotiation on what level of reparations should be paid and to whom and who will be responsible for holding reparations in trust funds for the genuine benefit of the descendants of slaves. What must not happen is that banks and other companies use tokenistic reparation payments as an exercise in white-washing while not disclosing the full history of their involvement in slavery or in imperial plunder and pillage.”

Want to download and listen on the go? Download onto your phone or hand held device by clicking here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher etc. Please leave us feedback and encourage others to listen!

Join us on facebook and get our blogs into your feed.

Existem “pílulas tributárias” para uma retomada econômica mais sustentável e redistributiva.

O episódio #14 do É da sua conta receita quatro “pílulas” que podem fortalecer o orçamento público para que governos tomem decisões justas no enfrentamento da crise, priorizando o combate à pobreza e à desigualdade, a manutenção de empregos e o resgate de pequenas e médias empresas.

Nosso colunista, jornalista da Tax Justice Network Nick Shaxson aborda a primeira “pílula tributária”, a taxação sobre lucro excedente de grandes corporações. A Comissão Independente para a Reforma do Imposto sobre Corporações Internacionais (Icrict) apresenta a “pílula” para adequar a tributação de multinacionais que operam em monopólios ou oligopólios. A terceira “pílula” é a taxação de grandes fortunas. Revisão de isenções e benefícios tributários a empresas e setores econômicos e transparência sobre esse tipo de decisão resumem os efeitos esperados pelo uso da quarta “pílula tributária”.

Our monthly podcasts are aimed at ordinary citizens, campaigners and practitioners, filling the gap in regional media coverage and analysis of tax, redistribution, financial secrecy and the global infrastructure of corruption, holding governments to account. The podcasts empower citizens to engage in and influence debates on these issues, and provide the solutions needed to support change. The podcasts are offered free to radio stations, as well as for downloading. They also reach key influencers: journalists, researchers, bloggers, tax and corruption experts, lawyers, policy makers, politicians and NGOs.

The Tax Justice Network is seeking a tax justice commentator and consultant for our Arabic podcast. Please find all details on the role and how to apply here.The deadline for applications is July 20th 2020.[Update: application deadline now extended to September 2nd 2020 with a new start date of September 7th 2020]

Our producer Walid Ben Rhouma has been producing and hosting the podcast for almost three years and, after a happy and fruitful relationship, our collaborating journalist and human rights expert Osama Diab is leaving our tax justice podcast family and handing on the microphone!

If you’re the right person to replace him, we’d love to meet you. You need to be an Arabic and English speaker who can continue Osama’s role of helping educate listeners in an accessible way on tax justice, helping source stories, great interviewees, compile headlines, always finding effective ways to explain to listeners about taxation, financial secrecy, tax havens, corporate tax cheating, and economic justice, communicating the global power aspects of who makes the rules, and how.

You will need to be very familiar with the Tax Justice Network’s solutions to all these problems and able to communicate them and ensure the programme is ‘on-message’. You will also appear each month on the podcast as a commentator discussing and analysing one or two agreed topics relevant to that month with Walid. You will be supported by me, Naomi Fowler – I produce the English language podcast, coordinate all our podcasts, and will have editorial oversight.

Please find all application details here. I look forward to hearing from you. Here’s the team you’ll be a part of, broadcasting tax justice in five languages:

Illicit financial flows are transfers of money from one country to another that are forbidden by law, rules or custom. They damage economies, societies, public finances and governance of countries around the globe. A key challenge to tackling illicit financial flows is the difficulty countries face in identifying which financial flows carry the largest risk to their economies. The Tax Justice Network is today launching the Illicit Financial Flows Vulnerability Tracker to help countries identify the trading partners and channels that pose the greatest risks to their economies.

Our previous research identified the eight main channels in which illicit financial flows take place: trade (exports and imports), banking positions (claims and liabilities), foreign direct investment (outward and inward) and portfolio investment (outward and inward).

For each of the eight different channels through which illicit financial flows operate, we calculated three measures.

Vulnerability captures how financially secretive the country’s trade, investment or banking partners are. Vulnerability reports the average financial secrecy level of all partners with which the country trades or invests for a given channel, weighted by the volume of trade or investment each partner is responsible. For example, if all the inward foreign direct investment a country receives comes from the Cayman Islands, one of the world’s greatest enablers of financial secrecy, the country would have a high vulnerability measure on foreign direct investments.

Intensity reports the share of national GDP that the channel makes up, helping capture the importance of the channel to the country. Intensity does not measure the secrecy involved in the channel nor the risks of illicit finanical flows the channel poses. For example, foreign direct investments may represent 10 per cent of a country’s GDP.

Exposure combines a channel’s vulnerability and intensity to estimate the share of a country’s GDP exposed to illicit financial flows by the channel. Comparing the exposure levels of different channels helps countries identify the channels that most expose their economies to illicit financial flows. For example, if a country’s inward foreign direct investment channel has a vulnerability of 76 and the channel accounts for 10 per cent of the country’s GDP, the country’s exposure score in inward foreign direct investment would be 7.6 per cent. This means 7.6 per cent of the country’s GDP is exposed to illegal transfers of money.

The Tax Justice Network’s new Illicit Financial Flows Vulnerability Tracker allows users to explore illicit financial flows data with interactive tools, and understand which countries are more vulnerable to illicit financial flows, and more importantly, why: which partner countries and which channels are responsible for the vulnerability in a country’s economy.

The tracker consists of three tools: map view, country profiles and country comparison.

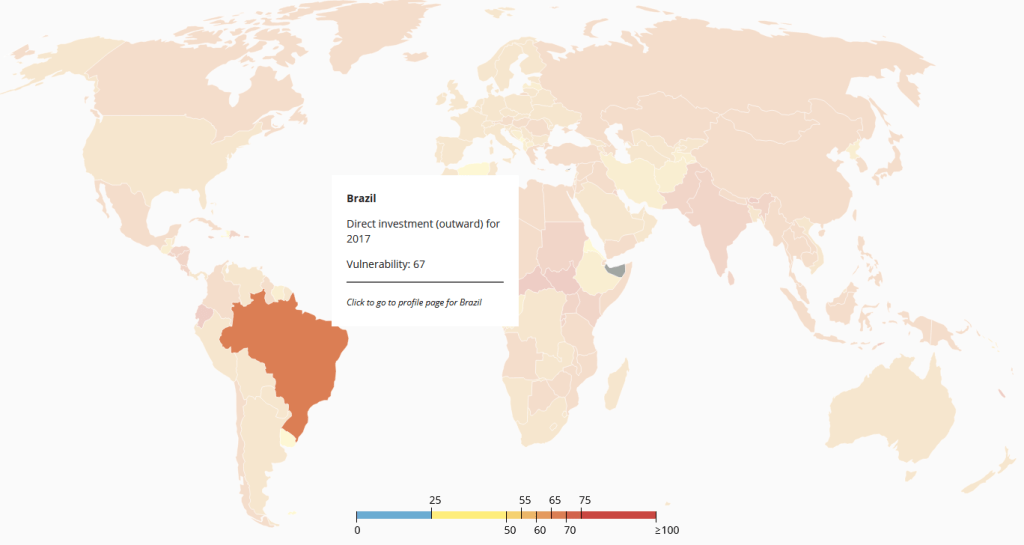

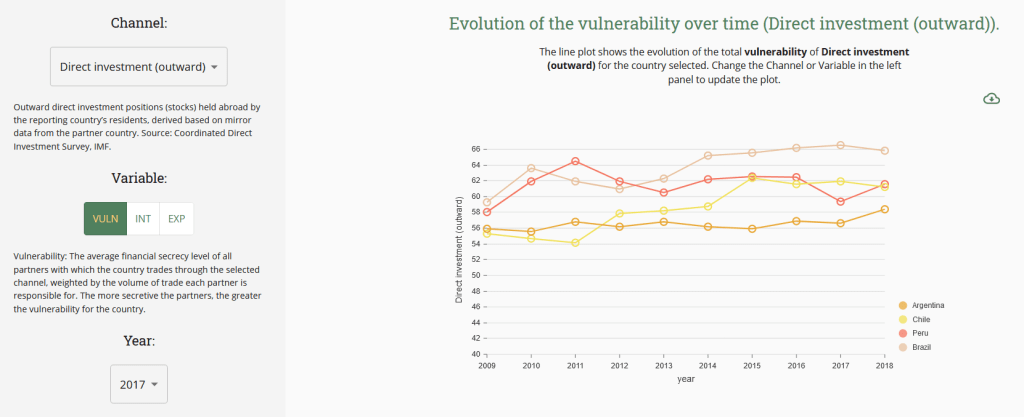

Tool 1: Map view

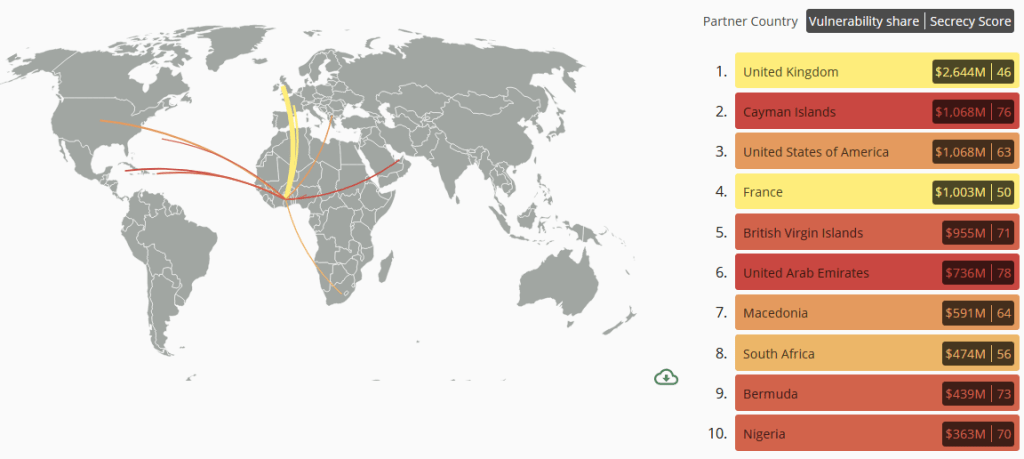

The interactive map allows users to understand which countries and regions are more vulnerable to illicit financial flows. For example, we see that the vulnerability of Brazil to outward foreign direct investment in 2017 is 67 (a very high score). This implies that Brazilian residents own many companies in places with high levels of financial secrecy, indicating high risks for illicit financial flows (and offshore tax evasion) to occur via direct investment.

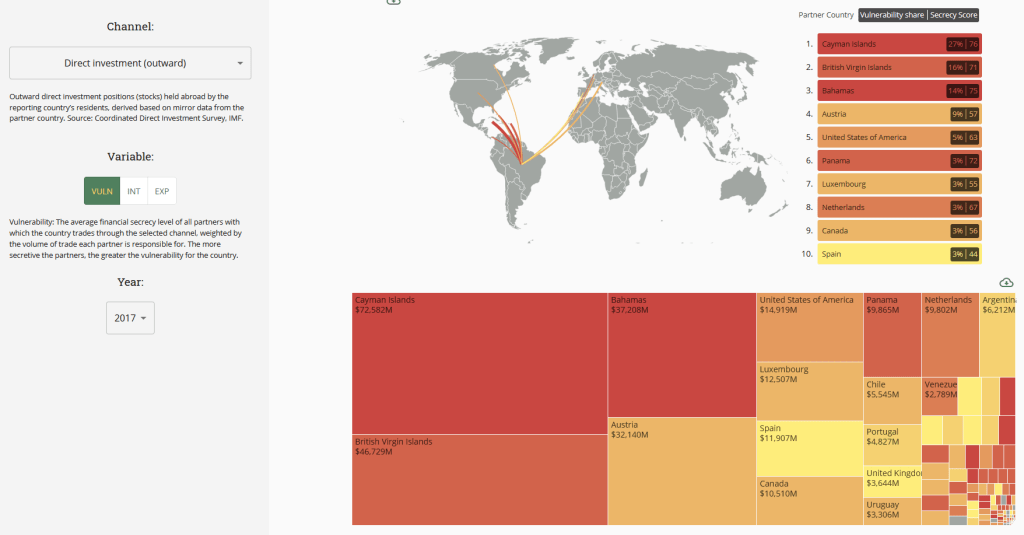

Tool 2: Country profile

Clicking on a country (or clicking on “country profiles” in the top menu) takes you to the country profile page of the country you selected. Each country’s profile page provides a detailed breakdown of the 10 trading partners that are most responsible for the country’s vulnerability, intensity or exposure for a given channel. Country profile pages also allow you to see year to year changes in a country’s vulnerability, intensity or exposure levels for all eight channels. In the case of Brazil’s country profile, the webpage shows that high vulnerability to outward direct investment is caused by the top three partner countries: Cayman Islands (responsible of 27 per cent of the vulnerability), British Virgin Islands (17 per cent) and Bahamas (14 per cent)). Cayman Islands—with a secrecy score of 76, British Virgin Islands—with a secrecy score of 71and Bahamas—with a secrecy score of 75— are three of the most secretive countries in the world. The left panel allows the user to easily switch between channels, variables and years.

Tool 3: Comparison tool

Finally, the comparison tool allows you to compare countries’ vulnerabilities, intensities and exposures across different channels. For example, comparing Brazil, Chile, Argentina and Peru, we can observe that Brazil is highly vulnerable to illicit financial flows. While Peru’s vulnerability has decreased over time, Brazil’s remained constant.

The rest of this blog provides three case studies we’ve compiled on Ukraine, Ghana and India by using the Illicit Financial Flows Vulnerability Tracker.

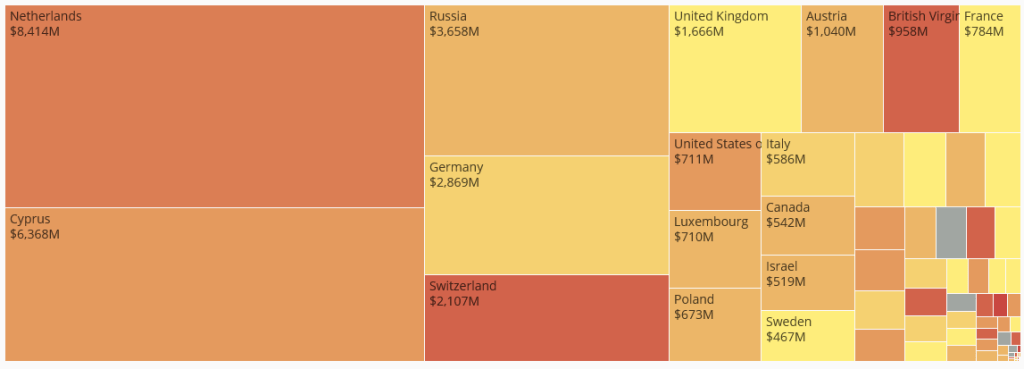

Case study 1: Ukraine

The majority of foreign direct investment entering Ukraine comes from three countries: the Netherlands, Cyprus and Russia. Other highly secretive jurisdiction, such as Switzerland and British Virgin Islands are also among the top investors in Ukraine.

Foreign direct investment (inward flow)

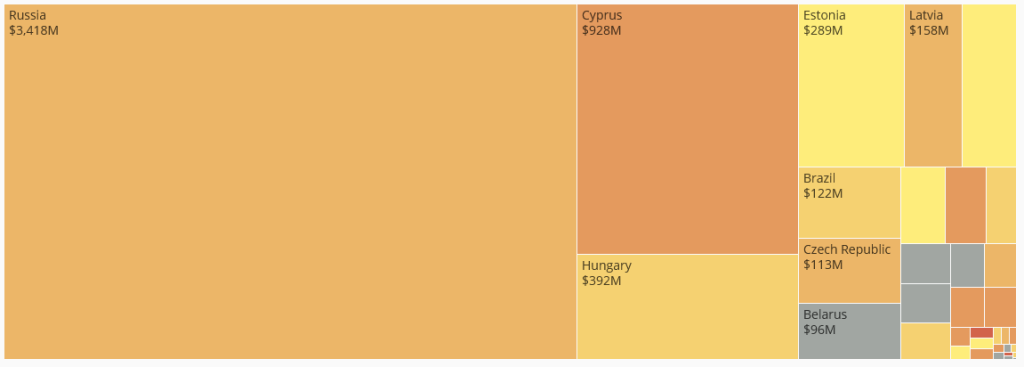

Foreign direct investment exiting Ukraine is primarily destined for Russia and Cyprus.

Foreign direct investment (outward flow)

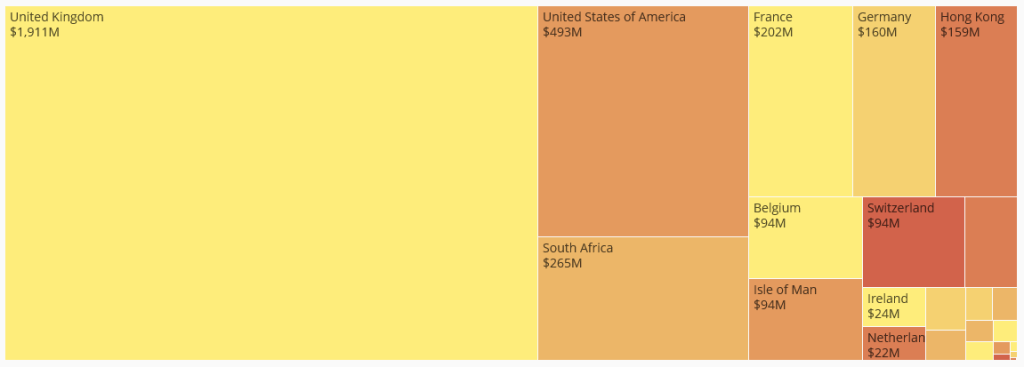

Case study 2: Ghana

Ghana gained independence from the United Kingdom in 1957. However, the influence of the former empire is still highly present. Outward bank deposits are often situated in the United Kingdom and British Crown Dependencies Jersey and the Isle of Man.

Bank deposit (outward flow, claims)

A large share of inward foreign direct investment comes the United Kingdom, and, concerningly, from highly secretive British Overseas Territories: the Cayman Islands, the British Virgin Islands and Bermuda.

Foreign direct investment (inward flow)

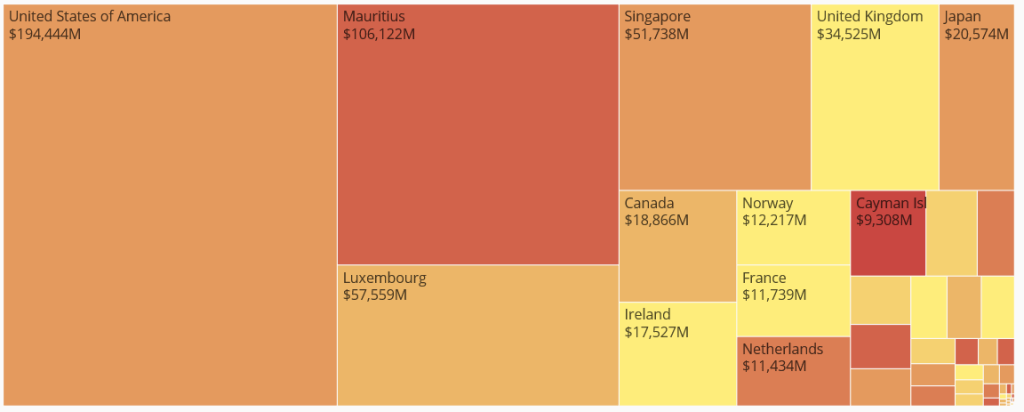

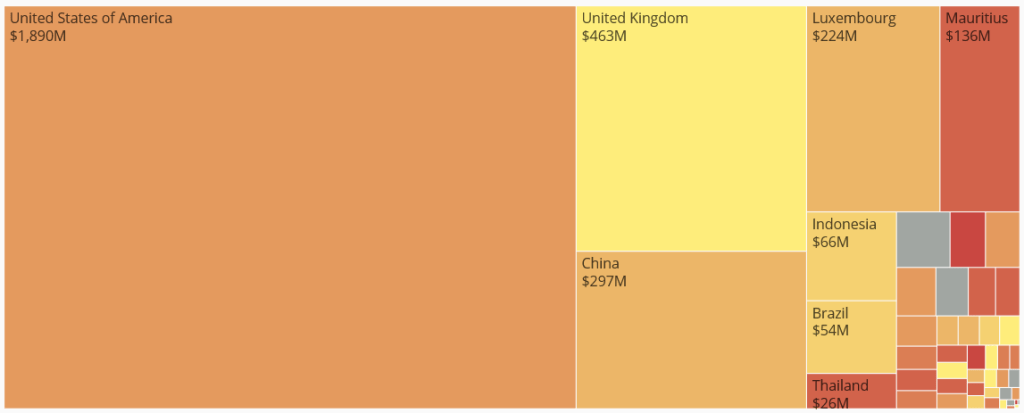

India: The Mauritius connection

A large fraction of India’s inward foreign portfolio investment (non-controlling investment in equity and debt securities) enters the country via Mauritius, Luxembourg and Singapore, notorious corporate tax havens known for their roles as conduits. This is not so evident for outward foreign portfolio investment, dominated by flows to the United States and the United Kingdom.

Portfolio direct investment (inward flow, liabilities)

Portfolio direct investment (outward flow, assets)

“(Other nations) had all come together” via the OECD to “screw America and that’s just not something we’re ever going to be a part of”.

~ US Trade Representative Robert Lighthizer addressing Congress, 17 June 2020, per Sydney Morning Herald.

Boom. The US has blown up ‘BEPS 2.0’, the OECD’s tax reform process with the Financial Times reporting that US Treasury Secretary Steve Mnuchin has written to four European finance ministers to say that the US was “unable to agree even on an interim basis changes to global taxation law that would affect leading US digital companies.”

US Trade Representative Robert Lighthizer told the US Ways and Means Committee, in response to a question about the letter, that the intention was to block any further progress at the OECD. “We were making no headway and [Mnuchin] made the decision that rather than have them go off on their own, you would just say we’re no longer involved in the negotiations.”

The finance ministers of France, Italy, Spain and the UK responded to the letter – per Belgium’s Le Soir – to say that “the positions and proposals of the United States have always been respected and taken into account”. Although they couldn’t resist a little dig, noting that this included an important US proposal that had never been “fully explained“.

The Trump administration then added the now-traditional confusion, with Treasury spokesperson Monica Crowley tweeting a one-line statement that contradicted Lighthizer on both the nature of the US decision and the reason for it: “The United States has suggested a pause in the OECD talks on international taxation while governments around the world focus on responding to the COVID-19 pandemic and safely reopening their economies.” (Italics added.)

The OECD hit back with its own statement, not from the tax team but directly from the Secretary-General Angel Gurría. His threat was clear: “Absent a multilateral solution, more countries will take unilateral measures and those that have them already may no longer continue to hold them back. This, in turn, would trigger tax disputes and, inevitably, heightened trade tensions. A trade war, especially at this point in time, where the world economy is going through a historical downturn, would hurt the economy, jobs and confidence even further.”

A strong response, effectively arguing the US is irresponsible to undermine talks. But in truth, the process was already in disarray, with the non-OECD members of the Inclusive Framework – that is, the lower-income countries that have typically been rule-takers as far as the OECD is concerned – openly calling out the institution’s failure to take meaningful account of their views. More than that, the OECD had already abandoned – at the behest of the US – most of the original ambition. While still paying lip service to the pledge to go ‘beyond the arm’s length principle’, the secretariat had tried to impose a US-French deal that did little of this at best.

Our research with the Independent Commission for the Reform of International Corporate Taxation (ICRICT) showed that the OECD proposal would have moved few of the profits declared in tax havens back to the countries where the real economic activity takes place; and would have primarily benefited a few OECD members, including the US, over all others. (Incidentally, we published the full model and the full dataset; sadly, the OECD has still to publish their data or any replicable model, providing only top line numbers that are hard to square with any others).

Digital services taxes? No thanks

Again, what next? The obvious outcome is that a whole slew of countries will now introduce their own digital services taxes (DSTs), to claim some revenues from these major tax-avoiding multinationals. No bad thing, you might think, and perhaps a small step to reduce tax injustice…

But: Digital services taxes are bad taxes. There, I said it. They don’t deal with profit shifting. They don’t ensure a level playing field between businesses (quite the opposite). They don’t address the global inequalities in taxing rights between countries. Digital services taxes don’t address the issue of unearned rents in the pandemic. And they don’t build towards the broader reforms of corporate tax that are now urgently needed (again, quite the opposite).

What do digital services taxes do? They may raise some – typically small – amounts of additional revenue, at a time when it is much needed. They may reduce the effective policy bias to a sector that has been particularly aggressive in its tax dodging. OK. Digital services taxes allow governments to respond to public pressure to do something about tax dodging – without actually doing very much.

The threat of countries going their own way on this added pressure for some international progress at the OECD, but that’s done now. And the threat of digital services taxes certainly did nothing to prevent good proposals like that of the G24 being ditched in favour of the limited, highly complex alternative negotiated bilaterally by the US and France (until the US today threw its toys out of the pram).

Priorities for countries

The ideas that drove the original optimism around BEPS 2.0 have not gone away. And nor, despite the pandemic, has the systemic tax abuse of multinational companies or the role of their advisers at the big four accounting firms. There is an urgent need for reform – and revenue. If countries are to take unilateral action, here are three options – all ultimately consistent with the broader reforms needed:

1. Countries should introduce excess profits taxes. These will allow states to capture a share of the large unearned profits of those companies that are benefiting from the massive state intervention of lockdowns, while all others suffer. But these must be based not on the declared local profits of multinationals, but on a fair share of their global profits. Take the global profits above, say, a 5% return; then apportion to the country a share in line with their share of the multinational’s global sales and staff. The country can then tax these exceptional, unearned, locally generated profits, at a rate of say 75%-95%.

[If all countries do this, there is no double taxation and the multinationals even get to keep a bit of their unearned profits. Not bad for a pandemic when so many are losing so much, so let’s not take any complaints too seriously.]

2. Countries can introduce formulary alternative minimum taxes. Leave the OECD’s failed rules in place for now, awaiting some global negotiation, but draw a line on the extent to which profits can be shifted. If the declared profits after transfer pricing, thin capitalisation and all the other manipulations end up being less than, say, 80% of the country’s fair share of the global profits under a unitary tax approach, the tax authority should simply draw a line there and claim that as the minimum tax base.

[Again, this approach will not lead to double taxation unless other countries are taxing far more than their share – in which case multinationals should be encouraged to address any complaints there instead.]

3. Countries could move unilaterally to a full unitary and formulary approach. There’s no reason, in fact, not to just go the whole way. There’s no need for global agreement, and no reason for this to cause double taxation unless, again, other states are taxing more than their fair share.

Whichever path countries or regional blocs like the EU choose, they should ensure that multinationals are required to publish their country by country reporting. This will confirm to the world that the country is not taxing more than its fair share; and reveal if other countries are continuing to procure profit shifting. And of course, country by country reporting shows the public which multinationals – and which tax advisers – are most aggressively flaunting their social responsibilities to pay tax fairly, like the rest of us. What’s not to like?

Where now for the OECD?

At one level, the OECD faces a simple choice. While it has said that the show must go on, there is presumably a more thoughtful process happening behind closed doors. They could opt to complete the exercise, in the hope that Trump will be replaced and a new administration willing to get on board with the outcome will be along shortly. But this would be an EU deal, with few other countries able or willing to engage fully during the pandemic, and OECD members unwilling to cede real power. And in any case, how likely is it that global corporate tax reform would head the action list of an incoming Biden administration facing a twin crisis of corruption and COVID?

Would the EU want to bother, or instead push ahead itself and finally bring in the Common Consolidated Corporate Tax Base (CCCTB) – ideally on a full unitary basis? It’s hard to see how the OECD could regain any credibility with the Inclusive Framework after putting a red line through their work programme at the behest of the US, so the only argument would have to be ‘come on back, the big bully has gone’. Tricky, although it could perhaps work a bit if the EU was willing to see a more ambitious outcome internationally – something closer to the Common Consolidated Corporate Tax Base for all. But given the EU’s difficulties in dealing with its own tax havens, no one should hold their breath.

Alternatively, the OECD could do what we asked them to do a few months ago: accept that this process is toast, and unconscionably unfair to non-OECD members, and abandon it. It should be painfully clear to all that the negotiation of international tax rules is political, not technical; and the OECD’s legitimacy, such as it is, is technical and not political. This is not the right forum.

The OECD’s future role on tax could be in providing technical support to its members in a global tax negotiation. That negotiation must be at the UN – not because it is perfect, but because that is what it is for: to provide a forum for global political negotiations. The OECD has recently inveigled its way into UN processes, seeking a role to guide some kind of ‘BEPS 3’ for lower-income countries. This too is clearly illegitimate; but hints perhaps at a technical role on the fringes of a political process.

There are many good people working at the OECD to make international tax better. But the organisation has confirmed once again, for what should be the very last time, that it is a members’ club only and cannot be trusted to run a genuinely inclusive process.

Where now for the excluded of the ‘Inclusive Framework’?

It is not coincidental, of course, that OECD members are primarily countries that have had empires and/or are ‘settler nations’ – while those in the ‘Inclusive Framework’ are primarily the colonised, the ‘settled’. If ever there was a time to leave this behind, it’s now.

Three options stand out.

1. The possibility of meaningful, regionally led reforms. A combination of the technical group and the political (the African Tax Administration Forum working with the African Union, say); or a technical group working with a regional power (CIAT, the Inter-American Center of Tax Administrations, with Argentina, perhaps).

2. The UN might finally take on its role as the global forum for the global negotiations over global taxing rights that must, eventually, come to pass. A critical decision facing the high-level UN Panel on Financial Accountability, Transparency and Integrity (FACTI), when it reports in January 2021, is whether to put its full backing to the proposal for a UN tax convention. Such an instrument is intended to deliver fully multilateral commitments to tax transparency measures, and at the same time to establish the forum for such negotiations.

OECD members have already indicated their opposition, following their longstanding blocking of a meaningful role on tax for the UN. If the OECD is a busted flush, even this could perhaps shift; but for now, the third option may be the best bet:

3. This would be process-led by the G24 or G77 groups. The idea would not be to move immediately to a formal, global negotiation. Instead, the groups could convene an open discussion among states, with strong technical support, to allow exploration of the options and likely revenue and broader economic impacts. In effect, the idea would be to convene the sort of process that the Inclusive Framework had set out in its work plan, but with genuinely open participation.

This would allow the potential for consensus to emerge over time, but also provide technical support for countries taking more immediate measures – of the sort described above, for example – in the face of the pandemic and other revenue pressures. The Tax Justice Network stands ready to assist with technical support to any such process, as undoubtedly would the wider global tax justice movement.

Everyone knows the global economic system isn’t working in the interests of most of us. In our new video series the Reboot we talk about how to fix it. From lockdown because of covid19 Naomi Fowler speaks to John Christensen and Nicholas Shaxson of the Tax Justice Network.

In this second episode of the Reboot: the big question people are asking as many governments are busily ‘printing money’ to tackle the coronavirus is – how can we afford this? We talk about wealthier. economically powerful countries with strong currencies and independent central banks and why they absolutely can afford this. And then we’ll look at the situation for countries which don’t have strong currencies or powerful central banks, many of whom are already seriously indebted to the IMF, World Bank and private creditors.

Naomi Fowler is the host and producer of the Tax Justice Network’s monthly podcast The Taxcast which is available on most podcasts apps.

John Christensen is co-founder of the Tax Justice Network and is a forensic auditor and economist. His research on offshore finance has been widely published in books and academic journals, and John has taken part in many films, television documentaries and radio programmes.

Nicholas Shaxson is a journalist and writer with the Tax Justice Network. He is author of the book Poisoned Wells about the oil industry in Africa, Treasure Islands: Tax havens and the Men who Stole the World and The Finance Curse: how global finance is making us all poorer.

This statement from Tax Justice Network-Africa, reproduced below, can be accessed in pdf format here.

The COVID-19 pandemic has exposed systemic inequalities in the current social, political and economic systems. African countries are disproportionately bearing the brunt of the impacts of the pandemic as a result of decades of privatisation and austerity measures resulting in underfunding of social sectors. The crisis has also exacerbated the weak monetary and fiscal systems, with a limited fiscal capacity to respond. African countries are now also experiencing reduced tax revenues due to reduced economic activities as a result of the loss of export earnings and commodity price collapses.

The differentiated COVID-19 impacts in Africa as in many countries in the global south are as a result of neoliberal, neo-colonial and patriarchal economic systems of oppression through decades of structural adjustment programmes of the 1980/90s. The main political mantra of the Structural Adjustment Programme was to minimise the welfare state by reducing the involvement of State in socio-economic programmes. These policies focused on unviable capital-intensive industries often in commodity sectors, instead of promoting competitive labour-intensive industries. Africa’s low average annual growth of 3.3% in 2014-19 has in turn constrained public finances, leading to underfunded social sectors including health and education systems, weak governance, rapid increases in public debt, and large infrastructure deficits. This neoliberal system continues to entrench a broken international financial architecture that enables illicit financial flows, tax evasion and avoidance by the rich and MNCs. This broken tax system allows transnational corporates to minimise their taxation by shifting their profits to offshore tax havens.

Additionally, the MNCs lobby and obtain low or zero corporate income tax rates from governments growing use of generous tax giveaways aimed at attracting foreign investments. The private sector-led growth policies have resulted in severely undermining the capacity of the State to generate domestic resources required to invest in social sectors and made African countries largely reliant on extern aid to support government programmes. Trade liberalisation has also reshaped economies and relegated developing countries to mainly producing and exporting primary commodities and importing manufactured goods and now impacted by the drop in the price of commodities in the context of a global recession.

The Covid-19 pandemic has created an opportunity to address some of the underlying principles of neo-liberal economic theory and demand structural and systemic reforms for redistributive justice including progressive taxation reforms, and where the wealthy elite and multinational companies pay their fair share. It’s about creating an opportunity to re-examine the continent’s fiscal and economic-policy priorities and creating alternatives to the current structure’s economic model that is fit for purpose and reinvigorating the role of the State.

The impacts of the global pandemic in Africa are not limited to health; it has also affected peoples’ lives socially and economically. Firstly, the pandemic has exposed weak public health systems which are understaffed and poorly resourced due to decades of underfunding and privatisation. Africa is witnessing the vulnerability of privatised and discriminatory health systems, and COVID-19 is increasing the pressures on the already unresponsive public healthcare systems. Secondly, reduced economic activities as a result of lockdown containment measures have led to a reduction in tax revenues despite the increased spending in the health sector. Fewer exports from African countries due to reduced demand and less economic activity has the probability of leading to a substantial economic recessionrequiring governments to inject money into the economy for survival. However, Africa’s ability to use monetary and fiscal policies to mitigate the pandemic’s economic impact is limited. African countries’ governments and central banks lack the fiscal policy space and capacity to adopt robust and often unprecedented short-run stimulus measures. Governments are constrained by monetary arrangements that prevent them from implementing national strategies. Besides, many African countries have unsustainable sovereign debt levels. Currently, the continent has a total external and domestic debt stock of $500 billion, and the median debt-to-GDP ratio had risen from 38% in 2008 to 54% in 2018. By causing a collapse in exports and terms of trade, the COVID- 19 pandemic is pushing African countries into negative per capita growth.

The effects of the coronavirus are also being felt disproportionately by the poor and the working class. The ILO estimates that more than 72% of total employment in sub-SaharanAfrica is in the informal sector. Despite this sizeable informal economy of up to 90%, African countries do not have social welfare systems to cover those without jobs as a result of lockdown measures. The pandemic has led to massive layoffs and non-payment of wages, pushing many workers into unemployment, poverty and starvation. The pandemic has also revealed and deepened existing gaps in social protection systems and has also translated into an intensified care burden for women. This has resulted in increasing the underpaid and unpaid care work and reinforcing patriarchal norms because women, on average perform 76.2 per cent of total hours of unpaid care work, more than three times as much as men. Lastly, most African countries are agriculture-based, and the GDP is primarily built upon agricultural services. However, food sovereignty and security is threatened as food supply chains are disrupted.

We urge African governments to:

Repeal value-added tax and consumption taxes and provision of tax credits to SMEs, and low-income earners.

Support greater investment in publicly funded, quality, universal public services and universal social protection systems. Prioritising well-staffed and resourced public health systems, equipped to respond to public health emergencies.

Ensure food sovereignty and security during this crisis and post-crisis

Urge IFIs to cancel sovereign debt for debt-distressed African countries to give governments sufficient fiscal space to respond to the current crisis, in compliance with human rights standards.

Progressively raise and spend tax revenues to address the impacts of the crisis, including by gender-responsive budgeting (GRB).

Evaluate and assess tax incentives and exemptions being given to non-essential corporations using a cost-benefit analysis to scrap any wasteful tax breaks that are a drain on public coffers.

Raise corporate income taxes (CIT) rates. – a “race to the top” targeting profitable businesses, and incorporating progressivity in the CIT, by taxing highly profitable companies at a higher rate while promoting tax transparency and a reform of the international corporate tax rules.

Promote domestic and regional tax transparency measures to identify and curb illicit financial flows (IFFs) by promoting Public country by country reporting (CBCR) for multinational corporations. (public information); Public registers of beneficial owners of legal entities and arrangements automatic exchange of information

Scale-up multilateral cooperation in combating illicit financial flows (including tax evasion and corporate tax abuse) and ensure that multinational corporations pay their share of taxes where they do business by rethinking and reinforcing the reform of the global corporate tax system and supporting the establishment of a global tax body to establish global norms on tax rules.

Welcome to this month’s podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! (Ahora también estamos en iTunesy tenemos un nuevo sitio web.)

En este programa especial sobre el coronavirus:

Los ganadores de la pandemia a nivel mundial.

¿Quiénes son los acreedores de la deuda global?

La Organización Mundial de la Salud dice que el foco mundial de la pandemia es el continente americano. Analizamos la respuesta en tres países: Bolivia, Chile y Perú.

y Costa Rica ingresa a la OCDE: ¿paso adelante o condena?

Several months into the COVID-19 pandemic people are bracing themselves. ‘Build back better’ is the mantra, but what does that mean in terms of tax justice and human rights? How should governments respond in the face of anticipated economic and social hardships?

Like many others we are concerned governments’ policies should not deepen inequalities or negate many of our fundamental rights. In the wake of the 2008 financial crisis, many governments ran roughshod over their human rights obligations, insisting that such considerations could not be priortised in the context of such a calamity. This perverse logic had devastating impacts for many millions of people. Indeed it is precisely in the face of a global emergency that human rights norms and standards should be given the highest priority.

This time we want to see a way forward which is both progressive and sustainable. The Center for Economic & Social Rights (CESR) shares this vision. Many of the public clearly share it too.

To find the right solutions we need to untangle ‘progressive’ rhetoric from ‘regressive’ policies. It’s important we establish which are the policies that will make a positive change to people’s lives. And which are the harmful ones which will fail you because, for example, of the country you live in, your race, or your gender.

CESR is publishing a series of straightforward issue briefs which aim to unpack the human rights principles that must be taken into account in policy responses to the pandemic and what social activists need to know. We are delighted to collaborate with CESR on this their latest briefing Progressive Tax Measures to Realize Rights. The full briefing is available as a pdf here in English and in Spanish here.

You can find CESR’s published and forthcoming briefings here.

The killing of George Floyd by US police in Minnesota, on 25 May 2020, has sparked a public response both more powerful and more international than almost any of the previous cases in a very long line – including Breonna Taylor in Kentucky, 13 March 2020. The demands for justice extend far beyond the specifics of the individuals involved, and instead reach deep into the structurally racist inequalities embedded in countries all around the world.

Reparations for slave… owners?

In the UK, welcome attention is being paid to the typically whitewashed history of the British Empire. As statues of (white, male) slave traders tumbled, Naomi Fowler (the Tax Justice Network’s creative strategist and presenter of the monthly Taxcast) reported on a long-running investigative project. This focuses on the financial institutions and others who benefited from the unrivalled generosity of the British government, which in 1835 recompensed the slave owners who were to be ‘dispossessed’ by the abolition of the legal right to hold title to other human beings. Such was the scale of the repayment, at around 40% of annual revenues, that UK taxpayers continued to service the resulting debt until 2015.

The UK Treasury’s bizarre, tone-deaf decision to celebrate the final payment being made prompted a wave of revulsion at the idea that taxes paid by UK tax residents in this century could have been used, in effect, to make good an imagined debt to those who profited from human misery in one of the most shameful elements of an imperial history not lacking in competition. That response included a petition, now reopened, calling for the government to return to taxpayers these illegitimately raised revenues.

The notion that we as tax payers in Britain, including those whose ancestors were subjected to the horrors of enslavement, have by your own admission, financially contributed to such payments, is totally unjust and abhorrent to us… We at no time consented to the misuse of our tax monies to reward such abominable crimes. We therefore demand refund in full so that such funds can be put to better use in repairing the harms done and paid for not in our names.“

– Cleo Lake, petition to HM Revenue and Customs.

‘You broke the social contract’

As both the petition and Naomi Fowler’s piece note, the sums extracted globally by the British empire were much bigger than the compensation paid to slavers – running easily into the trillions of dollars, rather than the few tens of billions associated with this debt. What sort of reparations could conceivably address this scale of damage?

And the human costs of the structurally embedded racism, in both former imperial powers and in settler/colonial states, run far higher. The racial wealth gap is extraordinary, is not closing and will not do so under the types of policies typically considered. White power didn’t just push Black people and others behind, as if stealing some money in a game of Monopoly – as Kimberly Latrice Jones lays out here, ‘you fixed the game… you broke the social contract.’

Two recent papers from Dr Trevon Logan, the Hazel C. Youngberg Distinguished Professor of Economics at the University of Ohio, show one role of tax in how white people broke the social contract. First, in ‘Do Black Politicians Matter? Evidence from Reconstruction’ (March 2020, Journal of Economic History), Logan shows that after the American Civil War,

“an additional black official increased per capita county tax revenue by $0.20, more than an hour’s wage at the time. The effect was not persistent, however, disappearing entirely once black politicians were removed from office at Reconstruction’s end. Consistent with the stated policy objectives of black officials, I find positive effects of black politicians on land tenancy and black literacy. These results suggest that black political leaders had large effects on public finance and individual outcomes over and above electoral preferences.”

Effective taxation supports the 4 Rs: revenue, redistribution, re-pricing (of public bads) and political representation. Attempts to include freed slaves in public services for the first time required new revenues, to complete a broader social contract, and Black politicians were more likely to pursue this aim. But resistance was often violent – aiming, almost literally, to break that social contract before it could be embedded.

Second, in ‘Whitelashing: Black Politicians, Taxes, and Violence’ (June 2019, NBER), Dr Logan finds that successful revenue-raising was also associated with a higher likelihood of (white) political violence against Black people:

A dollar increase in per capita county taxes increases the likelihood of a violent attack by more than 25%. The result is robust to numerous economic, social, historical, and political factors. I also find that counties where black officeholders were attacked had the largest negative tax revenue changes between 1870 and 1880 and that violence against black politicians is unrelated to other forms of post-Reconstruction racial violence. This provides the first quantitative evidence that political violence at Reconstruction’s end was related to black political efficacy.”

How would one go about establishing an appropriate level and means of reparation for the scale of damage done – not only the outright theft of lives, but the burning down and looting of possibilities for political, social, economic, human development? There are many great resources out there to help think about what this could mean, and this white British male blogger is in no way qualified to opine on right ways and wrong. What does seem clear, however, is that while a monetary aspect is likely necessary, it could never be sufficient. That which must be repaired is also social and political, not purely economic.

Reparations—by which I mean the full acceptance of our collective biography and its consequences—is the price we must pay to see ourselves squarely… What I’m talking about is more than recompense for past injustices—more than a handout, a payoff, hush money, or a reluctant bribe. What I’m talking about is a national reckoning that would lead to spiritual renewal.“

On the other side of one of empire’s many coins, we find the UK’s network of small islands operating as financial centres. Nick Shaxson’s book Treasure Islands and Michael Oswald’s film, The Spider’s Web, document how the UK turned away from its responsibilities to its remaining territories. Instead of making the financial commitment to support their development as the sun set on the British Empire, successive governments chose instead to encourage them down the road of tax havenry – attracting dirty money from all over the world, and channelling it into the City of London.

The intention was to engineer a ‘win-win’: providing a development path for the territories that would ‘save’ the UK from providing aid funds on an ongoing basis, while at the same time ensuring the continuing pre-eminence of the UK as a global financial centre.

The actual effect, arguably, was lose-lose. Many of the UK’s dependent territories saw a sharp and sustained rise in inequality, as foreign financial services professionals entered and captured the greater share of any subsequent benefits in economic growth. At the same time, a predictable Dutch disease played out, from Jersey to Cayman, with agriculture, tourism and other alternatives largely squeezed out by the new industry, making both the economies and the politics of these islands increasingly dependent on the whims of accounting and international law firms – rather than democratic preferences. This capture, part of what we have labelled the Finance Curse, further deepens the inequality and corruption facing islanders.

Meanwhile, at an international level, the emergence of the UK’s network of secrecy jurisdictions has been a central driver in the process of global extraction that has followed the period of formal Empire. The UK and its network, if taken as a single entity, would consistently be at the top of both the Financial Secrecy Index and the Corporate Tax Haven Index – in other words, the network is the greatest threat facing the world in all aspects of illicit financial flows, from tax abuse to grand corruption.

As we show in a new book with Petr Janský (now free to download in open access, from Oxford University Press), these illicit flows undermine the 4 Rs of tax in countries all around the world. In simple monetary terms, corporate tax avoidance is estimated to cost some $500bn a year in lost revenues, and offshore tax evasion a further $200bn – but as with the pattern of racist political violence that Prof Logan documents in the US, the governance damage is likely to be far greater than the simple loss of immediate revenues for public services.

It is difficult to imagine the means and level of reparations by which the UK might begin to make amends for the global extraction it has driven during decades, and continues to drive today. A very first starting point would be to bring the UK and the network into line with the ABC of tax transparency – committing fully for all of the jurisdictions to participate in Automatic, multilateral exchange of financial account information; to deliver public registers of verified Beneficial ownership information for all companies, trusts and foundations; and to require public Country by country reporting from all multinationals.

In terms of the UK’s territories and the islanders themselves, the position is perhaps more straightforward. The UK has, in effect, saved money year on year by promoting their tax havenry rather than supporting broad-based, sustainable human development strategies. The City of London too has benefited, by receiving a greater stream of (partially laundered) dirty money; although of course this has also contributed to the UK’s own finance curse, driving the governance and inequality problems it now faces.

These funds, in effect taken from the territories by the UK’s failure to meet its responsibilities, should now be provided as the basis to support that permanent transition – away from tax havenry, with both the global and local costs that it imposes, and towards alternative strategies: the ‘Plan B’ that islands should have been supported to develop since the 1950s, instead of pursuing financial secrecy. This is a topic about which the Tax Justice Network has been involved in discussions with partners in many of the jurisdictions over a number of years, and we are cautiously optimistic now about policy ideas beginning to come forward. We’re always interested to hear from others on this, and to support where we can, so do get in touch if that’s you.

Update: you can hear Naomi Fowler and John Christensen discussing this research in edition 102 of the Taxcast, our monthly podcast, starting about 2 minutes in:

It’s hard to believe but it was only in 2015 that, according to the Treasury, British taxpayers finished ‘paying off’ the debt which the British government incurred in order to compensate British slave owners in 1835 because of the abolition of slavery. Abolition meant their profiteering from human misery would (gradually) come to an end. Not a penny was paid to those who were enslaved and brutalised.

The British government borrowed £20 million to compensate slave owners, which amounted to a massive 40 percent of the Treasury’s annual income or about 5 percent of British GDP. The loan was one of the largest in history.

We wanted to find out which financial institutions were involved in this loan, so I sent two Freedom of Information requests to the UK Treasury and the Bank of England about it. I received two responses, which I’ll detail later, but the names and details of those creditors and investors remain frustratingly out of sight. If you feel you have the skills and time to help us continue the search, please get in touch.

legacies of slavery continue to shape life for the descendants of the formerly enslaved, and for everyone who lives in Britain, whatever their origin. The legacies of slavery in Britain are not far off; they are in front of our eyes every single day.”

Kris Manjapra‘s article, along with the work of historian David Olusoga inspired this blog, our investigations, and our Freedom of Information requests on this subject.

We recently published a two part Tax Justice Focus special on climate crisis and tax justice. This blog reproduces the article by Richard Murphy, in which he outlines how radical changes to accounting rules would require companies to comprehensively disclose their carbon emissions. Sustainable Cost Reporting, Richard argues, would put company directors into a position where they must accept responsibility for the harm caused by ‘externalities’. Click here to download the first and second parts of our Tax Justice Focus special.

by Richard Murphy *

Accountancy was established to protect investors from fraudulent managers. As the activities of companies now exceed planetary limits accountants must think much more carefully about their public interest responsibilities. Here one of the discipline’s most original and influential thinkers sets out the role new reporting standards could play in aiding a swift and just transition away from fossil fuel dependence.

The climate crisis is real: it is settled science that we must take immediate action to address its consequences. Across the world there has been a response that few in any activist community can ignore. There have been demands for a Green New Deal. Extinction Rebellion has led protests that have revealed the power of civil disobedience. Greta Thunberg has become a global figurehead for creating school strike protests.

The demands have, however, been primarily aimed at governments, which is reasonable given their responsibility for setting environmental policy. Governments will also be responsible for delivering the new public infrastructure needed to support the different types of economic activity that we now require. But we should not ignore the fact that as few as twenty oil and coal companies may ultimately account for one third of greenhouse gas emissions,[1] and just one hundred companies may account for seventy per cent of these emissions.[2]

What does this have to do with tax justice? In practice, quite a lot, since one of the possible reactions to the climate crisis is to tax the use of carbon-based fuels and another is to provide tax incentives to business to change their behaviour. Both might have a

significant impact on corporate tax bases and we need to understand what this might mean. However, we have almost no reliable data from most businesses on their carbon emissions; nor do we know enough about the economic impacts of any major policy proposals to be in a position to take decisions on such matters . As significantly, when it comes to the corporate tax base, we have almost no idea about which businesses might survive the transition to a net-zero carbon world, and which might not.

That said, moves are underway to address this issue. Former Governor of the Bank of England, Mark Carney, is promoting voluntary accounting standards created by a Bank for International Settlements initiative called the Task Force on Climate-related Financial Disclosures (TCFD).[3] Carney is to be commended for getting this ball rolling, but what he proposes is inadequate. The TCFD standards are voluntary and current rates of compliance are lamentably low.[4] Worse, TCFD standards do not require businesses to account for the carbon emissions that the products they create or sell give rise to when used by a customer, which means that the downstream environmental externalities businesses create in pursuit of their profits will go unreported. Given that the climate crisis has arisen because of businesses failing to take responsibility for the externalities of their activities, it is unacceptable for the TCFD standards to omit these downstream externalities.

For this reason the Corporate Accountability Network is developing what it calls sustainable cost reporting (SCORE), a new, mandatory accounting standard which will require businesses to disclose their greenhouse gas emissions (GHG) under four categories:

Scope 1: The GHGs the reporting entity creates itself;

Scope 2: The GHGs produced when generating the electricity the reporting entity consumes – the upstream externalities;

Scope 3: The GHGs arising from the manufacture and use of products and services over which the reporting entity has some contractual control e.g. within outsourced manufacturing processes (incorporating both upstream and downstream externalities);

Scope 4: The GHGs arising from the manufacture and use of products and services which the reporting entity buys in for resale essentially in the state in which they acquired them (also incorporating upstream and downstream externalities).

As is apparent, remoteness from control increases as the Scope number rises, but in each case the reporting entity facilitates the emission. In Scopes 3 and 4 the disclosure has to be split between upstream supply and downstream customer chains so that these can be fully understood. All disclosure will be on a country-by-country reporting basis to both reveal the geographic spread of the impact and to curtail carbon dumping.

Once this information has been disclosed, the reporting entity has to prepare a plan to become net carbon zero, as is necessary if the impact of climate change is to be managed. Crucially, SCORE requires that this plan be published and the cost to the reporting entity of its achievement must be estimated.

The most radical requirement of SCORE is that this cost has then to be included in the accounts of the reporting entity – in full – at the time of adoption of the SCORE standard. The logic is simple: SCORE recognises that the cost to the business of tackling climate change increases if action is deferred, therefore recognition of this cost in the accounts will encourage early action to minimise the final cost to the business of eliminating carbon emissions from its production and consumption chains. That this reverses the traditional accounting approach of discounting future costs is beside the point: nothing is normal about climate change and its impact.

Some important issues should be noted. The first is that SCORE does not put a cost on carbon usage: it covers the cost of removing it, making it far more robust than any alternative approach. SCORE also enables appraisal of each reporting entity on its own terms.

Second, the cost must be based on known technology: a precautionary principle must be applied, meaning that unproven technology cannot be assumed to deliver net-zero carbon, although investment in such technology to reduce the cost provision required (and so, in effect, declare a carbon cost reduction profit) is encouraged.

Third, the provision for costs will need to be reappraised annually and reported upon as a key accounting issue, thus enabling stakeholders to appraise companies’ commitment to their plans, and whether or not those commitments are being delivered on within the cost target. This will allow investors to identify companies that are best able to eliminate GHG emissions.