Guest blog by Professor Colin Haslam, Queen Mary University of London

In our working paper Safeguarding financial resilience for sustainability’ we argue that large companies listed on the European and the US stock exchanges have become financialised, leaving many with weak, financially exposed balance sheets and higher risk of insolvency. As the Covid-19 crisis hits, we are on the verge of a perfect financial storm as the European and US financialised corporate sectors have sacrificed financial resilience for shareholder value.

In response to the COVID-19 crisis governments are stepping up to underwrite company liquidity through wage and salary subventions. France, Spain and the UK, for instance, have unveiled emergency packages including direct pay-outs to employees as well as loans and guarantees for companies to mitigate the economic blow from the coronavirus. These economic interventions are about securing the financial stability of companies.

In accounting and auditing practice, company viability is tested by looking at both liquidity and balance sheet solvency. Companies need cash for liquidity to cover everyday business expenses. But to maintain balance sheet solvency, a company also needs a surplus of assets over liabilities, in the form of shareholder equity reserves. These reserves provide a critically important loss-absorbing buffer.

For example, when a company suffers a deterioration in income because of a downturn in product markets, any negative earnings need to be absorbed by shareholder equity reserves if that company is to remain a going concern.

In a financialised company, the primary modus operandi is asset value extraction for shareholders, through paying dividends and buying back its own shares. Aggressive distributions to shareholders can reduce retained earnings accumulated in shareholder equity, undermining the loss-absorbing buffer.

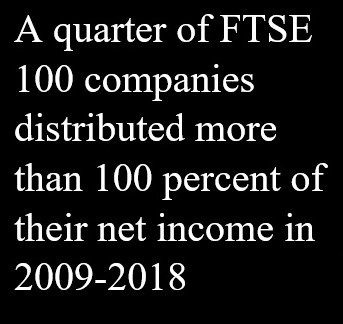

During the period 2009 to 2018 we estimate that net income earned by all FTSE 100 companies was £898bn, while dividends amounted to £571bn and share buy-backs £167bn. So in total, roughly four fifths of total net income was distributed. Nearly half of FTSE 100 companies distributed more than three quarters of their net income, while 25 distributed more than 100 percent of their net income!

This high distribution of earnings is a pattern that resonates across all the major European and US large company quoted stocks. To modify this behaviour, dividends could be added back to earnings for the purposes of calculating corporation tax. Where a company increases debt to fund distributions to shareholders the interest payments on this debt would be treated as being non-tax deductible. Stricter restrictions could include: stronger criteria for what constitutes realised earnings available for distribution to shareholders and changes to the UK companies act, that is, prohibiting company repurchases of their own share capital.

Table: Net income distributed to shareholders as dividends and share buy-backs[1]

| Dividends | Share buy-backs | Total | |

| % | % | % | |

| EuroStoxx 600 | 65 | 7 | 72 |

| S&P 500 | 36 | 51 | 87 |

| FTSE 100 | 64 | 19 | 83 |

Source: Thomson Eikon datasets

Financialised companies that have hollowed out their equity reserves are vulnerable not only to losses made in the normal course of business: they are also vulnerable to impairments of speculative asset values reported on their balance sheets.

The COVID-19 crisis will undermine company revenues and profits from selling goods and services as we now all lock down. But when company cash flows dry up there will also be a compounding negative impact on asset valuations that have been speculatively “marked to market” as part of fair value accounting (FVA) practices. The current market value of many assets recorded on a company’s balance sheet are speculative valuations. This is because these valuations are based on estimates about future cash flows that may or may not be realised by these assets.

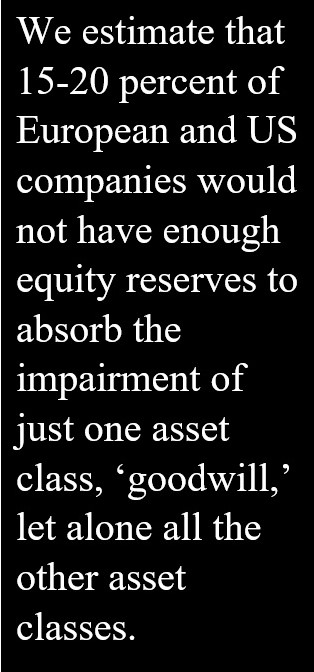

Assets adjusted to speculative market value include not just goodwill but also property, financial instruments, hedging products, pension funds, biological assets, brands, patent and licenses. These speculative asset valuations will also become compromised. Our working paper reveals that 15-20 percent of European and US companies would not have enough equity reserves to absorb just one asset class ‘goodwill’ being impaired – let alone all the other asset classes marked up to speculative market value.

So what’s to be done? A new social settlement.

The COVID-19 crisis has resulted in unprecedented state subvention of wages and grants to sustain our corporate sectors. When this crisis is over it will be necessary to demand corporate obligations, not just entitlements, attached to the granting of the social license of limited liability. A new social settlement will be required, as it will no longer be possible for corporate governance to operate solely for shareholders.

A starting point would be to restore prudential resource management, conservative accounting practices, and the preservation of capital and solvency for a going concern.

Policy interventions should now:

● Promote a default to historic cost accounting to limit speculative asset value impairment, and in the short run put in firebreaks to prevent asset value impairment and its transmission into the company equity funds.

● Restrict distributable dividends out of shareholder equity to accumulated realised earnings rather than realised and unrealised earnings that arise when asset values are inflated.

● Modify company tax law on dividends and tax deductible interest charges attached to debt finance used to fund distributions of all kinds to shareholders: adding these expenses back to compute corporation tax.

● Restrict the capacity of a company to convert other shareholder equity reserves, such as share premiums, into bonus issues for shareholders and other manipulations.

● Reform our company’s acts to stop companies from buying back their own share capital. We need to revert to the previous common law position prohibiting companies from buying their own shares.

In this time of crisis it is essential to ensure that, in the immediate short-run, companies do not liquidate assets because this will very quickly threaten company balance sheet solvency: a systemic Carillion effect.

In return for subvention, and beyond this current crisis, we should now all demand that companies fulfil broader obligations to society (not just shareholders).

This will require companies prudently safeguarding capital for a going concern in return for the social license granted by limited liability.

Company capital management: Safeguarding financial resilience for sustainability, Colin Haslam (Queen Mary University of London, George Katechos (University of Hertfordshire) Yuri Biondi (National Centre for Scientific Research, CNRS, Paris), 2020

[1] Over period 2009 to 2018

The author

Related articles

The Financial Secrecy Index, a cherished tool for policy research across the globe

New Tax Justice Network podcast website launched!

Como impostos podem promover reparação: the Tax Justice Network Portuguese podcast #54

Convenção na ONU pode conter $480 bi de abusos fiscais #52: the Tax Justice Network Portuguese podcast

As armadilhas das criptomoedas #50: the Tax Justice Network Portuguese podcast

The finance curse and the ‘Panama’ Papers

Monopolies and market power: the Tax Justice Network podcast, the Taxcast

Tax Justice Network Arabic podcast #65: كيف إستحوذ الصندوق السيادي السعودي على مجموعة مستشفيات كليوباترا

Remunicipalización: el poder municipal: January 2023 Spanish language tax justice podcast, Justicia ImPositiva