The Financial Times reports:

The Bank of England’s pressure on HSBC to cancel its dividend for the first time in 74 years has reignited a debate at the top of the bank over whether it should redomicile to Hong Kong.

This is shocking, on several levels.

First, that’s a direct threat by HSBC against UK policymakers – in the middle of a pandemic and a global economic shock. Classy timing.

Next, the Bank of England’s gentlemanly discouragement of dividend payments to help tackle the Coronavirus crisis is far too timid: we (and many others) have recently encouraged permanent bans on share buybacks (which used to be illegal) and temporary bans on dividends – especially banks which should now be ploughing money into shoring up their capital safety cushions in the current environment.

Furthermore, we have seen exactly this intimidation before, from exactly the same global bank, deploying the very same kinds of anonymous whispers, to favoured journalists who the bankers judge will put the “right” spin on the story.

This is, once again, the Competitiveness Agenda. Threaten to relocate elsewhere if you don’t get what you want — knowing all along that you’re not going to carry through on this threat. Talk, after all, is cheap. (HSBC is going to throw itself decisively into the arms of the Chinese Communist Party? Really?)

The same FT story cites an anonymous HSBC director accusing the Bank of England of “put[ting] a gun to the head of the board of directors . . . the calls for redomiciling will increase”.

No, it’s the other way around: HSBC is trying to put a gun to Britain’s head. Here’s how this game tends to pan out: Large multinational threatens to relocate, knowing secretly it has no plans do so. Yet an obsequious British state gratefully hands over goodies, extracted from current and future taxpayers and other sections of society. The bank then piously decides, after “careful consideration”, not to relocate. We described it thus, after the last big round of empty threats in 2016:

The bank’s been conducting a ‘review’ of its operations, and constantly drip-leaking panic-inducing details about these supposed internal deliberations, as a way of maximising pressure on British politicians to relax regulations and minimise pesky things like criminal probes, capital requirements, bank levies, and plenty more. And boy, have some concessions been made . . .

Those concessions alone have since cost the UK an estimated billion pounds a year, equivalent to the cost of educating 200,000 schoolchildren. HSBC didn’t, of course, relocate. (This kind of game happens all the time: it’s the same basic ploy as Amazon’s widely-reported efforts to engineer a “Hunger Games environment” to create ‘competition’ between US states to host its second headquarters, in which it sought to squeeze maximum subsidies and tax breaks out of the states. As one analyst put it, “Amazon already knows where it wants to be” – and in the end, his prediction proved exactly right.

To be fair, this time the FT journalists didn’t let the bank have it all its own way, pointing out that HSBC originally relocated from Hong Kong to London after Britain handed its colony Hong Kong to China in 1997: as an investor put it:

“it’s the price to pay if you’re going to domicile in the UK with all the protection that gives you.”

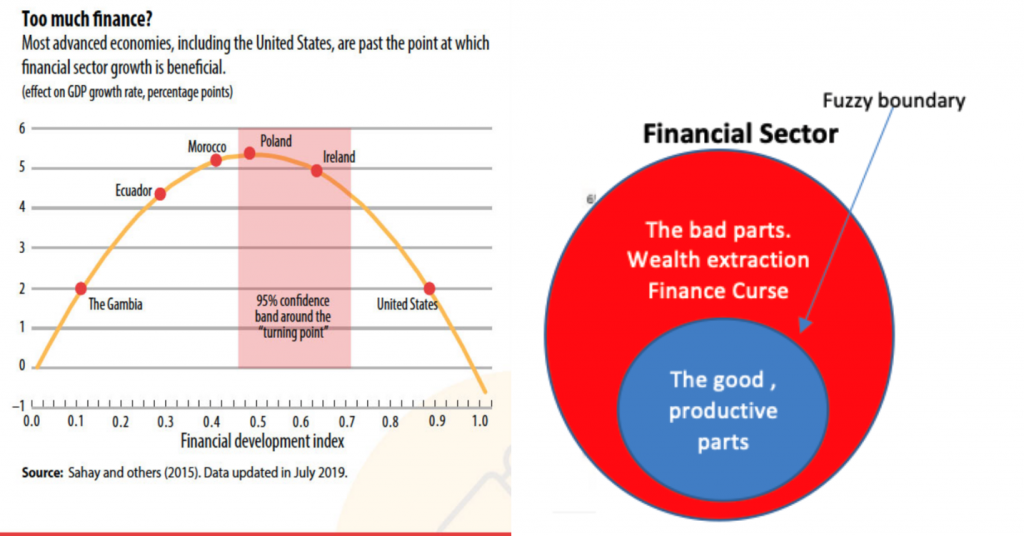

But here’s an even more important thing. The British financial sector is too big – much too big. There’s an ocean of research out there now, showing that countries with oversized financial sectors tend to become less prosperous as a result. Shrink the financial sector, for prosperity. Two images, the first from the IMF, and the second from us, show the basic issue, which is the Finance Curse.

The right hand graph is pretty much unarguable. Shrink the red, and keep the blue, seems to be a sensible approach. The left hand graph – an upturned banana shape (repeated in study after study) shows that we all need a functioning financial sector, and countries with underdeveloped financial sectors need to expand them to support prosperity. But there is an optimal point — the UK and the UK probably passed it some time in the 1980s – when the sector is providing the services an economy needs. Further growth of a financial sector beyond that optimal point starts to damage economic growth.

Why? For a number of reasons, most important of which is that once a financial sector has (to put it crudely) set up the useful services an economy needs, it finds that there are further profits to be mined by penetrating into other parts of the real economy – from agriculture to healthcare to the film industry to tourism – and finding ways to extract wealth from those parts. Frequently, it’s done by financial sector players buying up perfectly good companies then financially engineering them – running their financial affairs through tax havens, say, or by increasing their debt, or sitting astride and milking some sort of monopolistic choke point — to extract more wealth from them, and in aggregate this leaves behind a more fragile corporate landscape. This is in essence what private equity and a lot of merger and acquisitions do – or it could happen in a related guise, public-private partnerships (see the Private Equity and the March of the Takers chapters here).

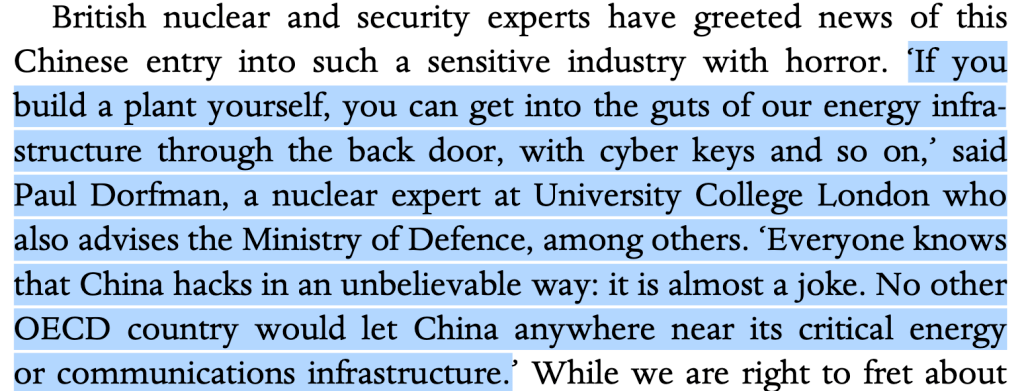

These pigeons will soon come home to roost: after which we might get a better idea of the costs. It’s impossible to estimate the scale of the damage from oversized finance with any degree of accuracy, but the best estimates suggest it is very large indeed. Much is not measurable: such as the fact that in 2013 and 2015 when Britain signed a series of deals with the Chinese Communist Party to give the City of London financial sector access to lucrative financing, the quid pro quo was that Britain would have to allow the China General Nuclear Power Corporation (CGN) to take a large stake in Britain’s mega-nuclear power station, Hinkley C. Here is one reaction to that:

What the UK should be doing is taxing and regulating this rather lawless global bank, and taking a very hard line — so that it either shrinks its operations to the useful core of services it provides, or the bank relocates to Hong Kong, taking its political, economic and democratic damage with it.

The author

Related articles

🔴UN tax convention hub – updates & resources

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

A 500-billion-dollar decision for the world: the revenue impacts of global unitary taxation

2 August 2026

Detecting Profit Shifting in Administrative Data: A South African Perspective

28 July 2026

A heartfelt farewell to our dear Óscar

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

Nonsense. Regulators are here to determine outcomes not set specific actions. HSBC is not lawless and this article shows the worst in irresponsible and dumb “journalism”. Shrink UK the financial sector and what do you have? Higher taxes for all. Dividends help pay pensions and support tens of thousands of individual investors. They also support the economy. Shame on you for such a poor, inaccurate and misguided article.

Comments are closed.