Co-organised with Gurminder K Bhambra, University of Sussex and Julia McClure, University of Glasgow

An analysis of inequality stemming from Imperialism and an exploration of reparation pathways

Colonial histories remind us, time and again, that the poverty of what comes to be understood as the global south and the wealth of the global north are intrinsically connected. That is, the very same historical processes that generated the wealth of European countries are the ones that made other places poor. During the phases of imperialism from the sixteenth century onwards, European countries extracted revenues and resources through formal and informal channels and spent this money often on domestic welfare and infrastructure. The precise value of the ‘colonial subsidy’ to European states and their citizens is incalculable or, at least, no attempt has been made at the global level to attempt to calculate it.

During the age of European global empires, European countries imposed tax regimes both nationally and across their imperial hinterlands that have also contributed to the establishment of trends of inequality that continue through till today. This conference will bring together leading academics to present new research highlighting the linkages between empires, nation states, taxation and resource extraction, and the resulting inequalities in polities and welfare systems experienced as a consequence of this mass extraction.

The conference will also explore where society and institutions can go from here to begin to address the centuries of damage and to investigate how reparations could begin to address some of this damage. This event will explore the following themes:

To what extent has the European project of public expenditure on welfare been made possible by imperial extraction?

What role has been played by promoting dependent territories as ‘tax havens’, in the more recent period of extraction, and how has this damaged those territories as well as others?

How do tax laws, which can themselves be understood as having imperial legacies, continue to shape inequality trends?

What sort of reparations could conceivably address the scale of damage created from imperial extraction, and how can taxes be collected and redistributed to begin to mitigate the economic damage created?

Call for papers:

This conference will focus on qualitative and quantitative research that explores the themes of empire, taxation, inequality and reparations. In addition to the range of papers already in preparation for a forthcoming volume, the organisers wish to invite original, high-quality papers for presentation in the following areas:

Reparations through taxation: the potential role of different types of taxation, for example on wealth or on financial transactions, to contribute to reparations

‘Plan B’: alternative development paths for UK territories and others where a ‘tax haven’ business model was effectively imposed by the imperial power, and potential reparations for the damage done

Tax, race and gender: to what extent are tax systems, now and historically, designed around a largely white, male landowning class, and what are the past and present implications? Are tax systems largely ‘colourblind’ and ‘genderblind’, or is disaggregated data used to inform policies and tax administration – and how does this affect inequalities?

Please submit abstracts of up to 500 words, along with the required supporting information, using our online application form. The deadline for submissions of abstracts is 11 September. The review panel will communicate decisions by 25 September. Full papers will be due by 30 October.

Registration will open when the preliminary programme is published in October 2020. More information will be published in due course on our website. For any queries, please email [email protected].

Blog by Neeti Biyani, Centre for Budget and Governance Accountability, New Delhi

Geopolitically, India is one of the most significant countries on the planet, with a GDP of almost $3 trillion and the fifth largest economy in the world. It is surprising, then, that the tiny island nation of Mauritius – with a GDP of approximately US $14 billion and a population of just 1.3 million – is the largest foreign investor in India.

The Mauritius Leaks, an investigation by the International Consortium of Investigative Journalists in 2019 offered clues as to why this might be the case. From being an idyllic island nation, Mauritius made a concerted decision to follow in the footsteps of numerous British Crown Dependencies and transformed itself into an offshore financial centre starting in 1989. Seeking to diversify its largely agrarian economy, Mauritius positioned itself as a jurisdiction of choice for multinational corporations and investors looking to invest in developing African, Asian and Arab countries.

Through the enactment of the Mauritius Offshore Business Activity Act (1992) to govern the country’s offshore financial services sector, it paved the way for foreign companies to incorporate subsidiaries with limited public disclosure, extremely low tax rates and a high degree of secrecy and asset protection. And by creating an intricate network of bilateral investment, tax and trade treaties with mostly developing countries, Mauritius proceeded to build one of the most aggressive offshore regimes in the region.

Along with offering low taxes, the network of Investment Promotion and Protection Agreements (IPPA), commonly known as Bilateral Investment Treaties, essentially protects and allows foreign-owned holding companies to become Mauritian resident companies. This incentivises businesses and investors to invest in other regions, mainly Africa and Asia, while operating under the garb of the Mauritian flag.

Often detailing taxing rights, these treaties constrict the taxing rights of developing countries, as profits are shifted to low-tax jurisdictions such as Mauritius – thus depriving developing countries of the revenue they rightfully deserve. The IPPA network provides measures against any efforts towards expropriation and nationalisation by partner countries. Due to the very nature of IPPAs, countries often end up losing money by way of litigation, penalties and compensation if the investors are unable to recover the investment made.

Despite evidence that double taxation agreements (DTAs) cause considerable and unnecessary loss of revenue from developing countries, resource-strapped low-income countries in particular are forced into entering unfair and unjust treaties to attract FDI in the absence of any alternatives.

India and Mauritius too had such a double tax treaty for many years, which proved irresistible to multinational corporations seeking to avoid paying their fair share of taxation. In the absence of a democratic global system of governance in this domain, most countries manage their tax relationships with other nations through bilateral agreements called double tax treaties. Indeed there are now over 3,000 of these agreements, ostensibly designed to prevent companies from having to pay tax twice in two different jurisdictions, in effect around the world. The proliferation of these accords has in turn fuelled the phenomenon of ‘treaty shopping’, through which multinational companies seek to exploit loopholes and inconsistencies by creating a fake paper trail for the goods and services they provide, and thereby pay less to government coffers. All too often, they succeed in paying no tax at all. In fact, research has shown that developing countries lose billions in tax revenues due to treaty shopping strategies employed by multinational corporations.

Until recently, the double tax agreement between India and Mauritius was notorious, with such vast revenue flows moving between the two countries that Mauritius became, on paper at least, India’s largest investor. At the same time, many Indian exporters were also invoicing their goods through shell companies in Mauritius, again to avoid tax liabilities in their home country.

For over 30 years, firms have been able to avoid paying capital gains taxes on sales using the Mauritius-India DTAA signed in 1982. Research by Centre for Budget and Governance Accountability, New Delhi has shown that between 2000 and 2017, Mauritius accounted for 34 percent of foreign direct investment into India. According to the Reserve Bank of India, in 2018, foreign direct investment from Mauritius accounted for US $13.4 billion, accounting for 36 percent of India’s total investments.

What was really happening was that investors were using Mauritius as a conduit, routing capital through shell companies in the country and then into India through a tax avoidance technique known as ‘investment round tripping’. In this context, it means that capital from India was usually routed to Mauritius, a jurisdiction with a lower corporate income tax rate. Indeed, the rate they paid could descend to zero if the money was held in special types of registered companies. Then the capital is sent back to India in the form of foreign direct investments and, thanks to the double tax treaty, an investor can claim she’ll pay tax in the conduit country (i.e. Mauritius). For the same reasons, the Mauritian route was also used by Indian companies that were investing outside of India.

In 2016, after years of negotiations, India managed to renegotiate its tax treaty with Mauritius and, by reimposing capital gains taxes on investors ‘from Mauritius’ who buy shares in Indian companies, it plugged one of the tax avoiders’ favourite loopholes. The treaty amendment went into force in April 2017 and applied half of the prevailing rate of capital gains tax until 1 April 2019, following which the full rate applied.

However, while the treaty amendment closed the benefit of zero capital gains tax, other vehicles used for avoiding taxation, including mutual funds and exchange-traded derivatives, were not adequately addressed in the renegotiation, so alternative channels for illicit financial flows remain in place. Furthermore, although both India and Mauritius are parties to the Multilateral Instrument (MLI) created by the OECD to prevent the abuse of double tax treaties in cases where the principal purpose of a business arrangement is to save tax, Mauritius has not included its tax treaty with India in its MLI commitments.

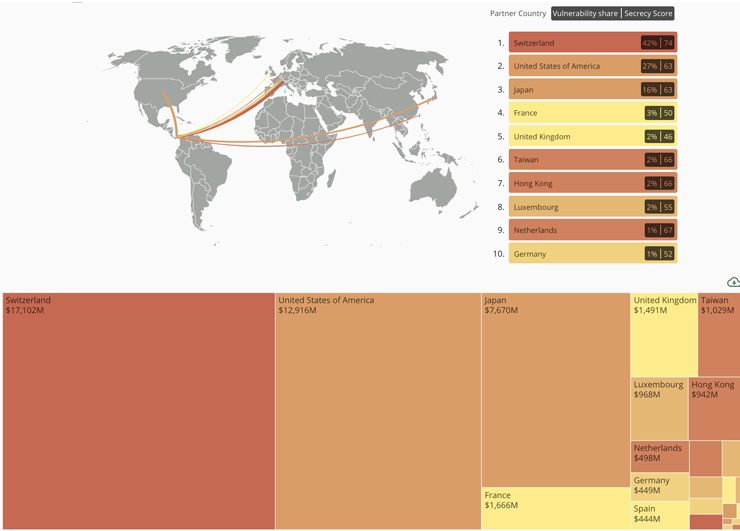

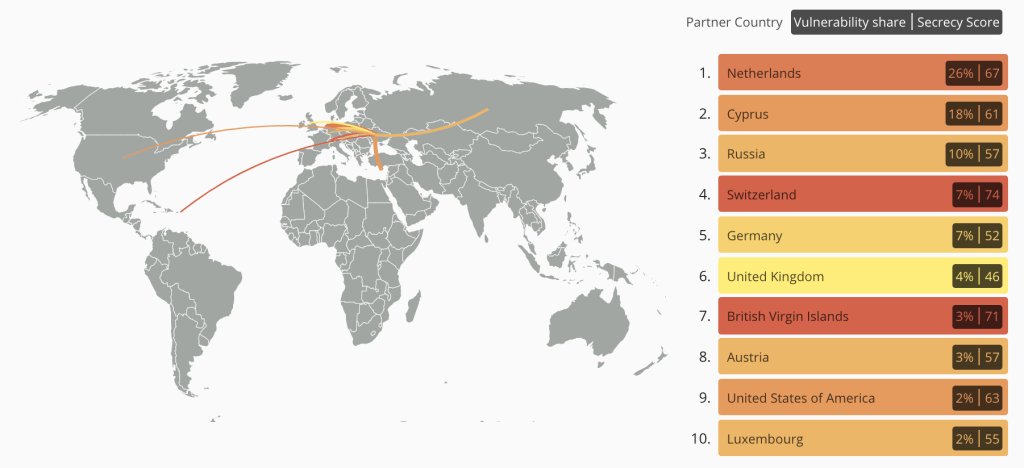

And as shown by Tax Justice Network’s new Illicit Financial Flows Vulnerability Tracker, Mauritius was still India’s number one source and destination for both inward and outward foreign direct investment in 2018. In fact, in 2018, the inward direct investment stock from Mauritius (estimated at almost US$ 126 billion) was even higher than such investment in 2015 (estimated at around US$100 billion).

India: FDI inward 2018

India: FDI outward 2018

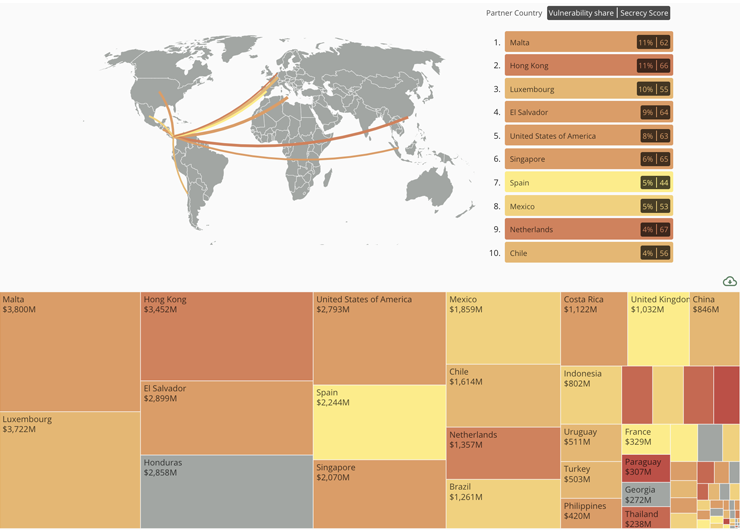

Despite a sudden and telling drop in direct investment from Mauritius to India in 2019, the corresponding figures for Singapore – the second most popular tax haven among India’s economic elite – have grown enormously in recent years. Indeed, the volume of investment from Singapore to India doubled from US $33.5 billion in 2015 to US $66 billion in 2018. The Netherlands is a close second in terms of acceleration of investment into India since the revision of the India-Mauritius treaty.

India: FDI inward 2015

It must also be underlined that, of the top ten destinations for direct investment in India, six are either corporate tax havens or financial secrecy jurisdictions (the United States, Switzerland, Singapore, Japan, The Netherlands, and the United Kingdom – which if considered together with its spider web of jurisdictions would have ranked first on both indices). This suggests that the Indian economy is severely exposed to international tax avoidance schemes, and other illicit financial flows, that are likely to be systematically draining state coffers of resources desperately needed to tackle both the ongoing Coronavirus health emergency and the concomitant economic crisis.

In this context, it is unsurprising that India has been one of the leading voices calling for developing countries to have a more meaningful role in negotiations on the international governance of taxation. Efforts to address the dysfunctional global tax system have thus far been led by the OECD under the Base Erosion and Profit Shifting (BEPS) process. However, this process, negotiated behind closed doors by rich countries, has largely excluded the voices of developing countries. Repeated calls from developing nations for a genuinely democratic, inclusive body under the auspices of the United Nations have likewise been thwarted by richer countries. With the US having now demanded the OECD process be put on hold, it is high time for the international community to work together for a radical reform of global tax rules through a genuinely inclusive process in which all can participate on equal footing. Such a process is only possible at the United Nations.

Image of Indian banknotes courtesy of Rupixen/Unsplash

Guest blog: Richard Christel, Program Associate at Transparency and Accountability Initiative

Recently, Transparency and Accountability Initiative was asked to prepare a presentation for a Tax Justice Network organised convening bringing together civil society, private foundation, and public aid agency participants. The focus of the presentation was on civil society funding for domestic resource mobilisation (DRM) efforts. Our research confirmed the challenge of getting reliable data on current level of support, but also brought home the limited levels of funding for non-state actors on tax. Given the bleak fiscal picture for countries around the globe exacerbated by responding to the coronavirus pandemic, mobilising engagement of all stakeholders in support of equitable and accountable tax system is all the more important.

Tax reform and subsequent revenue raising will be key in the recovery effort and now more than ever, civil society must be involved in reform discussions. If you are not at the table, you are on the menu. Civil society can play an active role in working with policymakers and tax authorities to remove inequities in current tax policy and administration and raise revenues for development priorities as the TAI-commissioned report on civil society engagement in tax reform points out, “CSOs tend to play three broad roles in tax debates, often in combination: analysis of tax policy, advocacy for or against policy proposals, and awareness raising on tax rights and obligations.”

Of course, civil society can only do this if they have resources to engage effectively.

To answer this question, we examined data from the OECD Creditor Reporting System (CRS) in April. We examined gross disbursement data from 2014 to 2018 from all official donors in sector code 15114 (domestic resource mobilisation). This data isn’t perfect and isn’t totally complete, as it lacks some European Commission funding, but of available datasets, it is the most complete and easiest to use.

Overall, civil society funding for domestic resource mobilisation has been on the upward trend, starting off at (2018 USD prices) $950,000 in 2014 and ending at $13.26m in 2018. Compare this figure to funding for public sector institutions, $10m and $260m in 2014 and 2018 respectively. As a percentage of all reported domestic resource mobilisation funding, civil society has received on average only 2.72 per cent of funding from 2014-2018. Of course, no one is arguing for parity in these numbers. Civil society cannot collect taxes or establish a tax administration office, nor can it issue subpoenas or conduct audits. However, given the importance and value of funding civil society efforts on domestic resource mobilisation, these are strikingly low figures.

Reporting Woes

However, this isn’t the full story.

When countries signed on to the Addis Tax Initiative (ATI), they pledged to increase funding for domestic resource mobilisation efforts. Part of this commitment is to report data on disbursements and countries do so when they report official aid statistics to the OECD and the Addis Tax Initiative. Unfortunately, we found anomalies in the data across reporting mechanisms.

One such anomaly was quality control in reporting. For example, one country government marked more than $10m in funding to the Kenya Revenue Authority as civil society funding, which appears a mislabeling. When we account for such apparent reporting glitches, this government’s civil society funding dropped from $16.49m from 2014 -2018, down to just $520,000 over the same period.

Similarly, for another donor government what was labeled as technical assistance to national and subnational government was categorized under civil society support. Upon recategorization, the civil society support drops from $3.5m to $100,000.

Indeed, original Creditor Reporting System data indicated civil society funding being $60.9m from 2014-2018. Upon closer analysis, I suggest that a more accurate figure is $36.64m, a difference of $24.26m.

Perhaps the targeted end users for these original disbursements were for civil society, however we could only analyze publicly available data.

Compounding the challenge of an accurate overview are differences between different data sources. For example, the Addis Tax Initiative’s public domestic resource mobilisationdatabase lists the Netherlands as having two total project disbursements in 2016, while the OECD data has six. Simultaneously, the Addis Tax Initiative 2016 data source lists the Netherlands having 11 projects, of which 6 had USD amounts extended. For their part, the Addis Tax Initiative says “…the data used in the DRM Database consists of OECD DAC data adjusted for the purpose of the ATI monitoring exercise.”

However, we don’t know the basis for differences between the two datasets. There is also value in having timely data available – currently the Addis Tax Initiative database only has data from 2015-2017 available.

Given that TAI members report grants data to the Secretariat annually, we try to create an accurate sense of domestic resource mobilisation funding from our members. However, finding an exact dollar amount for civil society domestic resource mobilisation funding is difficult due to some funding being core support to grantees working a range of issues including domestic resource mobilisation and as such isn’t broken down.

The Window

Investing in domestic resource mobilisation strategies now is what will help alleviate financial pressure and increase fiscal sustainability in the long run. Care should be taken however, to avoid levying regressive taxes on an already battered populace. A well-resourced civil society can garner political capital and harness citizen anguish to push for more progressive taxation, help assure that multinational corporations and the wealthy pay their fair share, that loopholes do not favour the well-connected, and in turn bolster treasuries and limiting more financial strain on the poorest. These initiatives can strengthen public budgets and help ease, however slightly, the economic devastation that is sure to linger.

But of course, that is only if organised civil society is left standing. As the next round of the Addis Tax Initiative begins to shape up, let us support taxation and civil society with dedicated targets of support to assure equitable and accountable tax systems and sound reporting to back it up.

Welcome to the 31st edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to share it. You can also join the programme on Facebook and on Twitter.

In the 31st edition of Taxes Simply:

Welcome to the thirty first edition of Taxes Simply. In the first part of this edition, we meet Nabil Abdo, regional policy advisor for Oxfam in the Middle East, on the structure of the Lebanese economy that led to the emergence of the severe economic crisis currently taking place in the country. In the second part, we meet with Tunisian journalist Khawla bou Karim about her investigation, “The missing million in oil taxes”, in which she reveals the disappearance of $53 million in oil taxes from the Tunisian government budget.

As for the third and final part, we cover a summary of the most important tax and economic news from the Arab region and the world, and our summary of news includes: 1) The automatic exchange of tax information covers assets worth $10 trillion; 2) The implementation of “country-by-country reporting” system may save EU countries $20 billion; 3) The IMF further reduces its forecast for the region.

الجباية ببساطة #٣١ – أزمة لبنان الطاحنة واختفاء ضرائب نفطية في تونس

أهلًا بكم في العدد الحادي والثلاثين من الجباية ببساطة. في الجزء الأول من هذا العدد نلتقي بالباحث الاقتصادي اللبناني نبيل عبدو مستشار السياسات الإقليمية لمنظمة أوكسفام في الشرق الأوسط في حوار عن هيكل الاقتصاد اللبناني الذي أدى لبزوغ الأزمة الاقتصادية الطاحنة التي تشهدها البلاد حاليًا. في الجزء الثاني، نلتقي مع الصحفية التونسية خولة بوكريم عن تحقيقها الصحفي “ضرائب المحروقات والملايين المفقودة” التي تكشف فيه عن اختفاء ضرائب نفطية بقيمة ٥٣ مليون دولار من ميزانية الحكومة التونسية.

أما في الجزء الثالث والأخير، نتناول ملخص لأهم أخبار الضرائب والاقتصاد من المنطقة العربية والعالم، ويشمل ملخصنا للأخبار: ١) التبادل التلقائي للمعلومات الضريبية يشمل أصول بقيمة ١٠ تريليون دولار؛ ٢) تطبيق منظومة “الإبلاغ عن كل دولة على حدا” (country-by-country reporting) قد يوفر ٢٠ مليار دولار على دول الاتحاد الأوروبي؛ ٣) صندوق النقد يخفض توقعاته بشأن المنطقة.

This time, the call’s presentations covered two main topics: how to share confidential information and how to apply advanced analytics to already collected data to detect red flags.

As we described in our paper on beneficial ownership verification, one of the steps to confirm the accuracy of the data involves cross-checking information against other databases. “Is John really called John and does he actually live on that street?” Countries are already required to ensure national authorities cooperate and share information with each other (eg the tax authorities and the financial intelligence unit which deals with money laundering). Achieving this at the national level is already challenging due to the lack of standardised data or interconnection of local databases, along with the refusal of local authorities to cooperate with each other by invoking fiscal confidentiality or other secrecy laws (they tend to forget that they all play for the same team, and that many of these financial crimes are related to each other, eg tax evasion may be a predicate offense for money laundering).

Sharing confidential information with other parties

Given the current freedom of establishment where anyone may have interests in a legal vehicle from any country, domestic cooperation is not enough. Countries need to verify information on any non-resident beneficial owner: “Hi Germany, is Friedrich really called that, and does he actually live in Berlin?” Cooperation at the international level may be even more difficult because countries would likely be unable and unwilling to share personal data of their citizens/residents with any foreign country. To address this, our paper had proposed zero-knowledge proof queries, where the beneficial ownership register of say, the UK, would automatically query Germany’s databases on the details declared by Friedrich to the UK register. German databases would only answer whether there was a perfect match (confirming that Friedrich didn’t lie to the UK). In case of a mismatch, Germany wouldn’t reveal the true answer. The UK would simply reject Friedrich’s registration until he declares information that results in a perfect match with Germany’s records.

An alternative to our proposed zero-knowledge proof queries was presented on the call by Jules Anthonia from FCInet. It suggested enabling cross-border checks without the need for foreign databases to be integrated. “FCInet is a non-commercial (government developed) decentralised computer system that enables FCISs (Financial Criminal Investigation Services) from different jurisdictions to work together, while respecting each other’s local autonomy. With FCInet, FCISs can jointly connect information, without the need to surrender data or control to a central database or authority, and without unlawful intrusion on privacy. A core functionality of FCInet that allows FCISs to jointly analyse information and to identify relevant information in real time, is ma3tch. Ma3tch enables distributed analysis without the need to bring data together in one central place.”

While this technology is meant for financial intelligence units and tax authorities, it could also be used by beneficial ownership registries, as the figure shows. Ma3tch agents (Agency A) would pseudonymise local data (Philip Tattaglia, Luca Brasi and Johnny Fontane) into match filters (zK4G). The receiving register (Agency B) matches its local data (Greene Moe, Adams Kay, Brasi Luca) against the received filter in FCInet. Only hits on information that both the sending FCIS and the receiving FCIS have in common are revealed (eg Luca Brasi). Subsequently, identified hits can be validated and followed up, so that Agency B only shares information about Luca Brasi.

Similar technologies could be used to share information among private actors. Under the 5th EU Anti-Money Laundering Directive (AMLD 5), banks are required to report discrepancies to the public beneficial ownership registers. If company A registered John as its beneficial owner in the beneficial ownership register but then, when opening a bank account, company A tells the bank that Mary is its beneficial owner, the bank should report this discrepancy.

However, banks could report discrepancies not only with the beneficial ownership register, but among themselves, for example if company A told bank 1 that John is the beneficial owner, but when declaring to bank 2, it said that Paul is the beneficial owner. The UK Financial Conduct Authority (FCA) organised a TechSprint where different banks, compliance and data companies proposed frameworks on how banks could share customer information with each other in an encrypted way so as to detect discrepancies without disclosing their customers’ personal data.

Detecting red-flags using banking information

While reporting discrepancies in beneficial ownership between different data sets is useful, it’s not enough. After all, a company could have declared John as the beneficial owner to the beneficial ownership register and to all banks, when actually John is a de facto nominee and the real beneficial owner is Mary. There would be no discrepancies, but the data would still be wrong. More sophisticated checks are also necessary, especially in looking for patterns and red flags, as described in our paper on beneficial ownership verification.

On the one hand, outliers would be revealed if countries knew what their typical corporate ownership structure looks like. As example on how to do this, we undertook research using Orbis data to explore the legal ownership chains of UK companies.

There is significant scope, however, to look to internal information to verify accuracy of external information provided. Banks have key financial information that if examined in the right way could also detect money laundering schemes and enable real beneficial owners to be identified. Based on their experience analysing the Moldova Laundromat and other major money laundering schemes, Howard Cooper, Chris Ives and Matt Weitz from Kroll described how banks could enhance their analysis to detect sophisticated financial crimes.

Rather than analysing customers and their transactions in isolation – eg “has company X done too many transactions above $10,000?” – banks should look at the full customer profile across their full customer base to identify patterns and hidden relationships. This way it will be possible to determine whether apparently unrelated bank customers are linked to one another. These checks could include analysis to detect overlap in common customer information such as addresses, telephone numbers or IP addresses (from where remote bank transactions are carried out) as well as shared people – directors, shareholders, signatories, beneficial owners, people with power of attorney or professional service providers who opened the account on behalf of the company. Even more sophisticated analysis would involve analysing fund flows to detect undeclared links between customers and the ultimate beneficiary of transactions.

For example, in one Kroll investigation into a complex fraud and money laundering network, the analysis of internet banking IP addresses (in the middle of the picture below) revealed connections across a large number of purportedly unrelated customers (at the bottom):

Another example involved looking at apparently unrelated customers (in green, blue and pink) that shared the same corporate nominee directors and shareholders, which were owned and controlled by the same trust and company service provider:

On the surface, and in know-your-customer (KYC) files and the relevant corporate registry documents, all three of the customers had different beneficial owners. However, by analysing the transactions of the customers together rather than separately, it was quickly revealed that:

The three customers received funds from common external accounts and the onward movement of funds followed the same pattern, exposing an undeclared relationship between them.

One customer (in purple) transferred funds to the Trust and Company Service Provider for the incorporation of another apparently unrelated customer (in blue), indicating the know-your-customer (KYC) information may not have been accurate.

The end result of all the transactions was the transfer of funds to the account of an individual (in red) – indicating that this individual was the true ultimate beneficial owner of the companies and that the transfers were contrived for their benefit.

Looking at each transaction in isolation would not reveal any issues, it was only by examining the network of transactions did the discrepancies between the know-your-customer (KYC) data and the actual beneficiary of transactions become apparent.

Other red-flags that digitalisation makes possible to detect

By digitalising administrative procedures, countries may not only prevent corruption, because there is no paper file to be lost or changed, but they may also look for patterns and outliers to detect red flags.

Maria Jose Martelo and Eduardo Martelli, formerly at Argentina’s Federal Ministry of Modernisation explained how the digitalisation of administrative procedures in Argentina enabled two basic red-flags to be detected: one based on time and the other based on the responsible public officer.

Regarding time checks, two indicators can be constructed. The first one looks at compliance with “First in, first out” (FIFO). In principle, unless a procedure is categorised as urgent, chronological order should be respected. If John started the application to set up a company on 1 April, and Paul started another on 10 April, there should be no reason why Paul’s company should be ready first, assuming John’s application had no flaws. If this happens, it may be an indication that Paul bribed someone to get his company ready first, or that John was blackmailed by the public officer to pay a bribe, and upon his refusal, his application was put on hold (or “in a drawer” as the Argentine expression goes).

Similarly, by looking at specific procedures throughout the year, it is possible to determine the average time it takes to complete one. Applications (to set up a company, get a construction permit, etc) that are too brief compared to the average time may be an indication of corruption (eg bribe or conflict of interest). On the other hand, an application that is taking too long may be an indication of blackmail or the application being slowed down to encourage the applicant to bribe the public officer.

These time checks may be combined with an association check, to determine whether the same corporate user (or service provider) always gets the same public officer to process their application. This would be especially suspicious if that public officer also takes a record (short) time in approving the applications.

While none of these rules would confirm a case of corruption (after all, a fast public officer may simply be more efficient than the rest, or may be specialised to deal with specific types of industries or cases), at the very least such red flags should prompt an investigation to discount any collusion or corruption.

Importantly, these digitalised checks only work if absolutely all procedures are done digitally. By allowing any exception to the rule, a window for corruption is opened. Unfortunately, Argentina invoked problems with the IT platform at the beginning of the Covid-19 pandemic (after the platform exposed a scandal of overpriced contracts) to allow paper-based procedures to take place again.

Conclusion

Countries and policymakers should consider the following proposals:

Digitalised procedures and data (eg digitalised beneficial ownership registers) allow the cross-checking of information and the detection of red flags (eg based on time analysis and association rules).

By combining digitalised data and encryption, it is possible to share confidential information and detect discrepancies without disclosing all the personal details of shareholders, beneficial owners or relevant users. This would enable cross-checks among countries and among private holders of information.

Banks have a trove of data that should become part of systematic anti-money laundering checks so that they report not only basic discrepancies, but also other undetected cases of wrongful beneficial ownership information. These checks could include analysis to detect overlap in common customer information such as addresses, telephone numbers or IP addresses (from where remote bank transactions are carried out) as well as shared people – directors, shareholders, signatories, beneficial owners, people with power of attorney or professional service providers who opened the account on behalf of the company. Even more sophisticated analysis would involve analysing fund flows to detect undeclared links between customers and the ultimate beneficiary of transactions. While this analysis would be done at each bank, these checks should also be done at the global level, as we proposed in our recommendations for SWIFT to include beneficial ownership information in the messaging system and to run similar advanced analytics.

Pour cette 18ème édition de votre podcast « Impôts et Justice Sociale, nous revenons sur plusieurs actualités qui ont animé la justice fiscale et sociale dans le monde. Le programme débute sur la publication mi-juin 2020 d’un rapport concernant la transparence sur la propriété réelle en Afrique. Nous revenons ensuite sur la récente publication de l’OCDE, qui pour la première fois reconnait que la publication des données fiscales pays par pays, permet de mesurer l’ampleur des pertes fiscale pour les pays dans le monde. Le programme s’achève avec un invité, qui commente le dernier rapport Global Witness/PPLAAF sur les pratiques de corruption et de blanchiment d’argent présumés en RDC, impliquant l’homme d’affaires d’origine israélienne Dan Gertler.

Produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Diante de uma sinfonia de crises intensificada com a pandemia do novo coronavírus, o É da sua conta #15 segue a partitura das edições anteriores eapresenta mais instrumentos que, se bem afinados, podem ajudar países a financiar uma recuperação econômica.

Falamos de emissão monetária e de títulos da dívida, sempre em harmonia com medidas tributárias justas e progressivas, focadas na tributação dos mais ricos e das grandes corporações.

Entenda o que é emissão monetária e os impactos na taxa de juros, na inflação e no endividamento. Saiba também como usar a dívida pública interna para financiar a solução dos problemas atuais e futuros. Enquanto países lusófonos africanos ainda sofrem com a dívida externa, lembramos como o Brasil superou o fardo de décadas de dívida externa e a dependência do FMI.

The UN high-level panel on Financial Accountability, Transparency and Integrity (FACTI) is moving fast. Following its launch earlier this year, the Panel has consulted widely with member states, civil society and experts from all areas of its broad mandate, the global architecture within which illicit financial flows take place.

Now FACTI has published a series of background papers laying out the key conclusions from expert assessment in each area. Below, colleagues from across the Tax Justice Network have summarised the main technical findings of each paper. We draw out the potential outline of the FACTI Panel’s final report, were they to follow the logic of this body of work.

As I said in invited remarks to the FACTI Panel’s ‘virtual global town hall‘ meeting, the problems the panel are addressing may be technically complex, but they are fundamentally political in nature:

Thank you co-chair, and panel, for the opportunity to speak. Your work is crucial, and most timely.

The Tax Justice Network was formed nearly two decades ago, and put forward then what remain the key elements to fix the global architecture for tax and financial integrity – motivated by the recognition that tax injustice does systematic damage to human rights, especially women’s rights and across a whole range of intersectional inequalities. The technical fixes include a shift to unitary taxation for multinational companies, and the universal introduction of the ABC of tax transparency: A for automatic exchange of information on financial accounts; B for beneficial ownership transparency, through public registers joined up into a Global Asset Registry; and C for public country by country reporting from multinational companies.

But while detailed, technical solutions are required, the question of whether the world chooses to implement these is fundamentally not a technical one but a political one.

For decades, the former imperial powers that dominate the OECD have set the rules for international tax and the architecture for financial transparency. The position in which we now find ourselves is the position that these rich countries have created. And that position is one in which tax abuse by multinational companies, and other forms of corruption, are not marginal activities, but are central to the global economy. All serious estimates, whether from researchers at the Tax Justice Network, UNCTAD or the International Monetary Fund, show that the costs of tax abuse are disproportionately high for lower-income countries – the very ones that are denied an effective voice at the OECD, and the right to participate fully in both rule-setting and information exchange.

And so the FACTI panel has one clear challenge: to outline the truly global governance alternative at the United Nations which can oversee effective responses to tax abuse and illicit financial flows, in the form of a new UN tax convention and rule-setting forum. Genuinely multilateral information exchange and rule setting has the potential to eliminate the grave inequalities in taxing rights between countries, to curb gross inequalities within societies, including those rooted in gender and racial injustice, and to empower the type of revenue raising for public spending that the pandemic has highlighted is crucial for all of our health.

As the review of the background papers confirms, the expert authors have identified exactly the political dynamics at play, and recommend a set of important and powerful reforms.

Summary of technical papers

The first of these, ‘Tax information production, sharing, use and publication’ underscores the importance of recent key steps towards transnational tax information cooperation. However, it criticises the established legal framework as not being universal, since it overlooks the needs of developing countries. For that reason, the paper emphasises the need to revise the existing legal frameworks and calls for public availability of certain tax information as a key policy tool.

The analysis by Professor Leyla Ates considers a number of proposals for improving existing legal frameworks of taxation. First of all, the existing international institutional framework should be improved through the creation of a global body with responsibility for collating and analysing tax data (including gender-disaggregated data) under the umbrella of the UN. Data should cover, inter alia, automatically exchanged financial account information and country by country reporting by multinational companies.

Moreover, countries should enjoy the full benefit of automatically exchanged financial accounts and public country by country reporting. To achieve this, Prof Ates argues, all jurisdictions must commit to fully inclusive and multilateral information exchange, to publish aggregate and detailed data, and to make detailed data available for analysis. To underwrite these processes, an international tax convention, led by the United Nations, is required.

In their paper on ‘The appropriateness of international tax norms to developing country contexts’, Martin Hearson, Joy Ndubai and Tovony Randriamanalina examine the extent to which six sets of international tax norms (including tax treaties, transfer pricing rules and mutual assistance agreements between states) hinder or help developing countries in enforcing their tax laws and preventing tax avoidance by multinational enterprises. The authors argue there is an institutional deficit in international tax norm setting and point out the need for an international body which can reconcile competing interests between lower-income and more powerful states.

In an attempt to address the disadvantages that developing countries currently face in global tax negotiations, the paper recommends the FACTI Panel employ a combination of short, medium and long term interventions. Among the short-term measures are that the Panel should urge governments to promote local filing legislation for country by country reporting, and adopt unilateral measures for taxing the digital economy that are better-suited to resource-constrained contexts. Medium term interventions include that the Panel should reexamine the purpose of tax treaties as a tool to maximise the gains for developing countries and explore a more radical approach; strengthen developing countries’ participation in international tax cooperation and capacity building, inter alia through investigating potential changes to the institutional design of the UN Tax Committee and the OECD’s Inclusive Framework.

Most importantly, the authors urge the Panel to pursue longer-term reforms by evaluating the replacement of the arm’s length principle with unitary taxation with formulary apportionment; investigating alternative instruments to current blacklists, peer review mechanisms and trade investigations, that better meet developing counties’ needs and available resources; and considering the call for a global tax body.

In the next paper in the series, ‘Transparency of asset and beneficial ownership information’, the Tax Justice Network’s Andres Knobel describes how financial secrecy is achieved in order to engage in illicit financial flows. To address and reveal these tax and financial crimes and abuses, beneficial ownership transparency entails identifying the natural persons who ultimately own, control or benefit from legal vehicles such as companies and trusts. This transparency provides a way to prevent abuses and to “anchor” legal vehicles to the limits and responsibilities of a natural person so that no one stays above the law. While the Financial Action Task Force (FATF) and the Global Forum on Exchange of Information for Tax Purposes allow countries to implement three different approaches to ensure availability and access to beneficial ownership information, the paper identifies the many gaps left in place, and recommends that all countries establish a centralised register of beneficial ownership for all legal vehicles.

Setting up registers does not guarantee that information will be accurate and up to date. Countries should also close the many loopholes in the legal framework (eg narrow scope of legal vehicles subject to registration, high thresholds in the beneficial ownership definition, lack of effective sanctions) and properly equip the beneficial ownership register. The paper weighs the privacy risks and economic costs, and concludes that giving online public access to beneficial ownership information will have significant benefits, by ensuring that all relevant users are able to access, use and verify the data. While most of the recommendations involve legal changes (which are economically ‘free’), the digitalisation, online disclosure and automated cross-checks or interconnection of registries may involve economic costs. Countries should see these improvements in beneficial ownership transparency for assets and legal vehicles as a strategic investment. High-income countries (especially major financial centres where most offshore legal vehicles are incorporated and where most of the cross-border wealth is located) should assist lower-income countries, because global beneficial ownership transparency is an important public good from which all stand to gain.

In their paper, ‘Anticorruption measures’, Michael Findley, Dan Nielson and Jason Sharman emphasise the need to increase efforts in law enforcement, as well as assessing risks and effectiveness of anti-corruption policies. The paper sheds light on the role of corporate service providers in international corruption and exposes the problem of misidentification of haven countries: the symbiotic relationship in which high-income havens, often OECD members, receive illicit flows from lower-income countries. The authors further note – as our Financial Secrecy Index has long demonstrated – that corruption perception rankings may capture some risks in source countries, but systematically ignore the havens that shelter the proceeds.

The authors recommend refocusing the fight on haven countries, and changing both the metrics and the policy responses in order to spotlight them. And while the authors are less convinced of the value of beneficial ownership registries, arguing for a focus on regulating, licensing and auditing corporate service providers, they concur with Andres Knobel on the crucial role of verification of beneficial ownership.

Abiola Makinwa’s paper, ‘Foreign bribery investigations and prosecutions’,shows that illicit financial flows and foreign bribery rely on difficulties in effective prosecution because of the obscure transacting environment where it takes place, which is delocalised and has no central nexus of governance. Furthermore, the monopoly of the state to initiate criminal law enforcement often translates into a reluctance to prosecute domestic companies or persons, and, paradoxically, the criminal justice system may in such circumstances provide a layer of protection to wrongdoing corporations. State actors are often among the primary beneficiaries of contracts facilitated by foreign bribery; while the primary enforcer of anti-foreign bribery laws is the state itself. Finally, information asymmetries represent a great challenge since few countries have the critical capacity to uncover and discharge the traditional burden of proof with respect to foreign bribery activities that are shrouded in secrecy and concealed with the best expertise money can buy.

The author argues that the FACTI Panel should promote non-trial resolutions (NTR), whose growth and spread has focused on crime prevention ex ante, and which outperforms traditional (ex post) criminal prosecution. Dr Makinwa proposes structurally integrating victims’ compensation into NTR regimes, while in the long-term she advocates for linking supply-side NTRs to demand-side foreign bribery prosecution, in order to develop a prosecutorial framework that leverages voluntary disclosures from supply-side NTRs to support the development of a demand-side NTR process.

Fatima Kanji and Richard Messick in their paper ‘Accelerating the return of assets’ criticise approaches to stolen state assets that have been largely centered on the malfeasance of government officials from lower-income countries, while ignoring richer countries’ centra role in hiding the proceeds. The authors note that Sustainable Development Goal target 16.4 calls for more effective recovery and return of stolen assets, whereas the United Nations Convention Against Corruption requires states to assist in locating and returning stolen resources but all too often through processes that are painstakingly slow and prohibitively expensive.

In order to streamline asset recovery procedures, Kanji and Messick argue that barriers to the exchange of information should be addressed urgently and that states themselves should be required to disclose how long they take to respond to relevant requests. They also propose a crackdown on professionals who facilitate the hiding of assets, through the deployment of anti-money laundering laws and the strengthening of penalties. Such legislation should also be used to confiscate stolen assets and ensure their prompt return to victim states.

In the final paper, ‘Peer review in financial integrity matters’, Valentina Carraro and Hortense Jongen examine the role of peer review mechanisms – the most prevalent form of monitoring in the field of international financial integrity, but characterised by serious gaps and vulnerabilities. The authors evaluate six international review mechanisms: on tax, those mandated to monitor the OECD’s Inclusive Framework on Base Erosion and Profit Shifting, and the Global Forum on Transparency and Exchange of Information for Tax Purposes; in the area of corruption, the oversight mechanisms of the UN Convention Against Corruption, the OAS Inter-American Convention Against Corruption, and the OECD’s Working Group on Bribery; and in the field of money laundering, the monitoring of the Financial Action Task Force.

The authors identify five key institutional weaknesses that are currently limiting the effectiveness of these mechanisms: (1) the frequency with which they are conducted; (2) the lack of systematic follow-up monitoring; (3) exclusion or lack of participation by civil society and other key stakeholders; (4) power imbalances and political bias; and (5) problems arising from the existence of partially overlapping monitoring systems. They also emphasise that, at the domestic level, implementation of standards promoted through peer review mechanisms is often hindered by lack of political will and lack of technical expertise and resources.

Potential recommendations from the UN FACTI Panel report

The FACTI Panel has an important opportunity to lay out the path forward, identifying the changes in global rules and rule-making that will give the world at least a chance of curbing illicit financial flows, including the great scourge of corporate tax abuse. The central recommendations from the Panel’s background papers offer a clear roadmap, should the Panel choose to take it.

Running through all the papers is the core point that current structures are flawed politically: that power imbalances result in bad policies, with OECD members preventing effective scrutiny and accountability of their own actions (and often those of their dependent territories), thereby blocking globally effective action. The focus of current instruments and policy fora is consistently put on actions to be taken by lower-income countries and small jurisdictions, when it is high-income countries and major financial centres, along with their multinational companies and professional enablers, which are the consistent actors in all illicit financial flows.

The papers make a clear case for a UN convention, on which negotiations could begin immediately. This could address each of the three key thematic areas of the Panel’s work, providing the fully supportive context for additional, national actions and for a globally inclusive and effective response to the grave threat posed by illicit financial flows.

Corporate tax

In 2013, the G20 countries established a consensus – since joined by many more countries at all income levels and from all regions – that the single goal of corporate tax reforms should be to reduce (or indeed eliminate) the misalignment between the location of multinationals’ real economic activity, and where their profits are declared. In successive processes (2013-15, and now 2019-ongoing), the OECD appears to have failed to make significant progress. A convention can create the basis for, and the expertise in a secretariat to support, genuinely inclusive negotiations to deliver the necessary reforms. As noted in the background papers, this is likely to include a shift to unitary approach with formulary apportionment.

Financial transparency

The key elements identified in the Panel’s discussions and confirmed in their background papers are the ABC of tax transparency. The convention could include a comprehensive set of commitments to ensure comprehensive, multilateral, automatic exchange of financial information, including the publication of aggregate data; set the standard for beneficial ownership registers for all major asset classes, with a technical basis in open data allowing their combination into a global asset register; and the full publication of country by country reporting by multinational companies.

Institutional effectiveness

The convention should set standards for issues of cooperation and process raised in the background papers – notably, with regard to the speed and power relations in asset recovery processes; and to non-trial resolutions in foreign bribery and other illicit flow cases. In addition, and importantly, the convention would address the key failure of current arrangements in respect of peer review of compliance with international instruments – and specifically, would establish a comprehensive and inclusive mechanism of peer review for the convention itself.

Conclusion

There is no guarantee that the FACTI Panel will follow the advice of the chosen experts – and there has already been fierce resistance to the entire process from a number of OECD member states, and of course the corporate lobby – eg the International Chamber of Commerce arguing that the “Confidentiality [of multinationals’ country by country reporting data] is critically important”.

At the same time, many in civil society have expressed scepticism about the Panel’s willingness to take their own logic to its necessary conclusion, and to make the case for the full reforms that their analysis confirms to be urgently needed. With the publication of this important set of background papers, the world now awaits the FACTI Panel’s findings.

In this episode of the Tax Justice Network’s monthly podcast, the Taxcast we bring you part 2 on how tax justice can help address systemic racism in the US:

Plus: how muchwealth is stashed offshore?!! We speak to Tax Justice Network Senior Advisor and economist Jim Henry and John Christensen on why our estimate of $21 to 32 trillion has been vindicated by new figures released by the OECD: “it means we’ve discovered an eighth continent of wealth”

Produced and hosted by Naomi Fowler. Transcript available here (not 100% accurate) Never miss an episode – subscribe by emailing naomi [at] taxjustice.net

As we continue to ignore the racist history of the tax code, ignore the fact that policy is not race neutral and that the tax system is not immune to racism then we will continue to see the impact of black and Brown communities and communities of colour worsen in the most negative way.”

How is it that after 400 years over 40 million African Americans only own about 2% of US wealth? Normally when we talk about discrimination we talk about it from the perspective of the injustice or the immorality associated with it. I wanted to look at things a little differently. I wanted to look at what is the financial cost associated with it and more importantly what does research say that those costs are?”

For a very long time here, we’ve had a sort of a rising tide lifts all boats point of view in this country and saying, okay, well, you know communities of colour will benefit if we just invest in broad based policies. And I think this is a moment where people are saying, okay, we know that’s not true, right? It doesn’t mean we shouldn’t invest in these broad-based policies. And it doesn’t mean we shouldn’t push for things that benefit everyone, but communities of colour have been specifically and explicitly pushed behind and disenfranchised. And to address those harms are going to have to have explicit policies that benefit them.”

It means we’ve discovered an eighth continent of wealth. It’s important, especially for developing countries because [it] shows that they’re basically a net creditor of the rich world, ‘cos most of this money is not invested in Cayman islands or Panama, it’s basically invested in London and New York and Zurich.”

~ Tax Justice Network Senior Advisor and economist Jim Henry on why our estimate of $21 to 32 trillion offshore wealth has been vindicated by new figures released by the OECD

Want to download and listen on the go? Download onto your phone or hand held device by clicking here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher etc. Please leave us feedback and encourage others to listen!

Join us on facebook and get our blogs into your feed.

Guest blog: Nick Mathiason, founder and co-director of Finance Uncovered

The global economic crisis sparked by Covid-19 means governments urgently need additional revenue as emergency stimulus packages taper.

Capital gains tax – a tax on the profit from the sale of assets such as oil blocks and telecom licences – should be a reliable pot of revenue for countries, particularly poorer, resource rich nations.

However where there’s a tax there’s an avoidance trick. With capital gains tax, the trick is relatively simple.

In Britain, for instance, while the highest rate of personal income tax is 45 per cent, the average capital gains tax rate is 15 per cent according to analysts at financial adviser firm, AJ Bell.

Now the UK Treasury has just announced a capital gains tax policy review which may see the wealthy contribute more to offset huge public spending.

But it is in the corporate sector where capital gains tax avoidance could make a material difference to helping to rebuild shattered economies. Not just in the UK, but throughout the world.

This is because when private equity firms, hedge funds and multinationals sell profitable businesses, they very often pay zero capital gains tax in the countries where the principal, relevant economic activity takes place.

Though most attention among tax justice campaigners has been on corporation tax avoidance, capital gains tax avoidance has largely gone unreported. Until now.

Lightbulb moment

You know how you always remember where you were when you stumbled on a systemic tax dodge that costs developing countries tens of billions of dollars?

Well, I was near Geneva “on a job” for Finance Uncovered. It was May 2017 and our task was to find tax dodging stories.

We’d been asked to spend three days with Public Services International union officials from Ghana, India, Malaysia, Nigeria, Norway and Uganda poring over the accounts of six companies.

My lightbulb moment came when I sat with Ugandan academic, Everline Aketch from Public Services International. Everline wanted to know the extent of profits made by Umeme, Uganda’s monopoly electricity distributor.

Immediately, the news antennae went up: we could see that a controversial British private equity firm called Actis based on London’s South Bank had recently sold Umeme.

Actis had a chequered history as readers of the British satirical and investigative magazine Private Eye will know.

Once owned by the Department for International Development and charged with building growth businesses in Africa, Asia and Latin America, Actis was privatised in 2004 at a knockdown price making its managers extremely wealthy. The deal was widely regarded as having short changed the taxpayer.

So had Actis made a windfall profit from its sale of Umeme, and if so had Uganda received any capital gains tax from it?

Here’s what we found out.

Lucrative exit

In 2004, Umeme had been privatised. The Ugandan government issued Actis with a licence to run electricity distribution.

After eight years, in 2012 Actis plotted its lucrative exit. Over a four year period, the central London based firm sold blocks of Umeme shares onto the Uganda stock exchange. By 2016, it had completely exited.

By examining company disclosures, combing notes in Umeme’s accounts, examining arcane tax treaties between Uganda and Mauritius, and through discussions with Actis itself, we estimated the British financiers had made a $129m capital gain. It was a figure Actis did not dispute.

We also established that Uganda, where that vast profit was made, had not received a shilling in capital gains tax.

How was this done?

Well Actis deployed a simple technique – one that is used by many other major overseas investors when they buy assets in another country.

The private equity firm had placed its shares in Umeme in a Mauritius company. The shares it sold over a four year period were Mauritian. So no capital gains tax was due in Uganda, which charged capital gains tax at 30 per cent. It meant that Uganda missed out on $38m in capital gains tax – then equivalent to 6 per cent of its health budget.

This technique – using a tax haven company to own shares – is called an Offshore Indirect Transfer.

“Capitulation”

Over the next two years, Finance Uncovered pieced together three further examples in Germany, Namibia and Vietnam in which more than €2bn in tax was avoided.

In Vietnam, our story combined with civil society campaigning contributed to “a capitulation” by US oil giant, ConocoPhillips which had previously refused to pay an estimated $179m in capital gains tax to the south Asian nation.

This week, a new report we helped write with Oxfam Novib referred to other documented Offshore Indirect Transfer disputes in India, Peru, Uganda together with stories we had previously investigated. Our report found that in just six cases alone, developing countries missed out on $2.2bn.

The past 40 years has seen a tsunami or corporate activity with valuable assets traded. Even in our post Covid economy it is impossible to imagine an end to the profitable trading of businesses.

Attention is now growing on this simple ruse which denies tax revenue to in particular developing countries. We at Finance Uncovered are proud to have built an evidence base in this section of the tax avoidance forest. It is imperative that policymakers close the offshore indirect transfer loophole.

There are definitely policy remedies. Countries can use national legislation to prioritise their capital gains tax taxing rights if investors move shares of an asset to a tax haven. Countries can also ensure double taxation agreements between it and another jurisdiction also reflect this priority. There is no question bombed out Covid economies need these types of measures to come into play.

Nick Mathiason co-directs Finance Uncovered which trains journalists and activists to investigate tax abuse, money laundering and corruption and then helps participants get stories into the public domain.

Most beneficial ownership definitions are based on ownership thresholds or voting rights. But there are ways to control a company without holding any shares. This brief explores some of these gaps and proposes ways for authorities to address them. This brief is also available to download as a PDF.

The ownership bias

The Glossary of the Financial Action Task Force (FATF) Recommendations related to anti-money laundering and combating the financing of terrorism (AML/CFT) defines a “beneficial owner” as the natural persons who ultimately own, control or benefit from a legal vehicle such as a company, partnership, trust, foundation, etc, or who have effective control over them. It is clear that the definition refers both to “ownership” or “control”, however, in the past few years since the Financial Action Task Force published its recommendations, a warped implementation of this definition has taken hold of beneficial ownership registers in many countries. That implementation warps “ownership” or “control” into “controlling ownership”.

While most countries’ laws use the Financial Action Task Force’s Glossary definition, the process of identifying a beneficial owner in practice can differ. Based on the Financial Action Task Force’s Recommendation 10 (which refers to how financial institutions should undertake customer due diligence), mechanical tests are often incorporated in regulations, such as the need to identify any individual who directly or indirectly owns shareholdings above a certain threshold as a “beneficial owner”. One widely used threshold to determine who a beneficial owner is, is the “more than 25 per cent” of ownership or voting rights, which we’ve criticised in previous research and blogs.

However, returning to the original definition, beneficial ownership is not about having a level of ownership that is substantive or large enough to be considered a controlling ownership, but merely about having ownership in the first place or control or benefit. We thus understand that there should be no threshold and anyone holding at least one share should be identified as a beneficial owner. As the paper on the updated state of play of beneficial ownership registration reveals, based on the findings of the Financial Secrecy Index published in 2020, four jurisdictions are already requiring beneficial ownership registration whenever anyone holds at least one share: Argentina, Botswana, Ecuador and Saudi Arabia.

One argument in defense of the “more than 25 per cent” threshold is that only ownership that meets this threshold classifies as “controlling ownership” and so is worth registering. But simply implementing the threshold itself shows how the logic of arbitrarily distinguishing and registering “controlling ownership” falls apart in practice. If Paul owns 30 per cent of a company and Mary owns the remaining 70 per cent, both of them would have to register as beneficial owners (because both pass the 25 per cent threshold) despite Paul having no control at all. Mary has the majority of the votes and so all of the control. In the case of trusts all parties have to be identified as beneficial owners, including the settlor and the beneficiaries, even though neither may have any control over the trust and the trustee (at least on paper, since trusts can easily be abused).

While “control” may be relevant to finding the responsible individuals who controlled a legal vehicle (eg company) involved in a financial crime, ownership (regardless of the threshold) is relevant for other purposes. A 0.01 per cent of a listed company may be worth millions of dollars despite giving no control over it. Knowing the beneficial owner of that 0.01 per cent may be important for asset recovery, but also to determine if the person could explain how they purchased those assets in the first place or whether they have paid corresponding wealth tax, if applicable. Unfortunately, listed companies and investment funds enjoy a high degree of secrecy, either because they are exempted from beneficial ownership registration laws or because the high thresholds mean that hardly any individual will pass the 25 per cent threshold. Therefore, only the manager or CEO will be identified. While these entities may have to disclose some information to the securities regulator, usually at 5 per cent thresholds, that is still not enough. An example of this relates to a study that was unable to find the beneficial owners of Berlin real estate through investment funds.

In any case, the disclosure of the beneficial owners holding directly or indirectly at least one share is a very important step, but it is not enough. The legal owners and the full ownership chain should also be disclosed to detect other abuses, eg circular ownership. Moreover, the key point is not to stop the analysis once a person having ownership above a certain threshold was identified (either one share or more than 25 per cent), but to go further until every individual with control through other means is also disclosed.

How to find those individuals with control through other means (different from ownership)?

The UK and then the 5th EU Anti-Money Laundering Directive (AMLD 5) include in their beneficial ownership definitions those individuals with more than 25 per cent of the voting rights or the right to appoint or remove the majority of the board of directors. “Influence” or “effective control” is also mentioned. In principle, it is good to leave the door open with these general provisions such as “anyone else with effective control over the legal vehicle”. This allows the staff at a registrar or bank in charge of assessing a legal vehicle’s beneficial ownership structure to dig further and to try to understand the control structure. However, for those without the will, time or experience, it would be good to have some more “mechanical” approaches.

For instance, there are low-hanging fruits as we proposed in our checklist for beneficial ownership registries. Those with power of attorney or any similar right to administer the legal vehicle or its bank accounts (transfer or withdraw funds) should also be registered. Given that since 2020 the EU requires financial institutions to report discrepancies between the information declared by their customers and the information available in beneficial ownership registries, reported discrepancies should detail whether those managing the bank accounts are also mentioned in the beneficial ownership register.

However, it is not enough to register those with a power of attorney or those who manage bank accounts. There are more complex cases of control or influence through means different from ownership. These cases create loopholes which individuals case use to avoid beneficial ownership registration. We will discuss these cases here so that government can take action to safeguard against them.

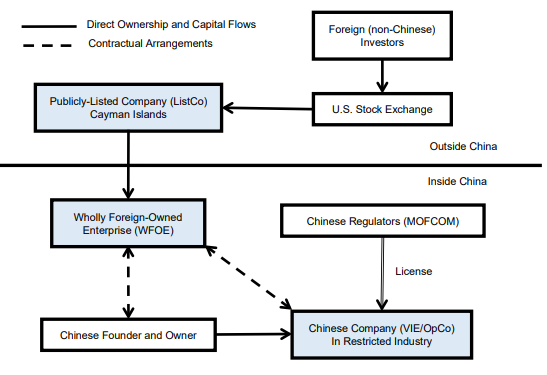

a) Combination of commercial contracts. The case of the VIE structure for foreigners to “own” Chinese strategic assets meant for Chinese owners

The Chinese Variable Interest Entity (VIE) achieves the same effect of ownership and control, not through holding shares or votes, but through different commercial contracts.

As Whitehill and Coppola describe, China has restrictions on foreigners owning or investing in strategic industries (eg internet platforms, financial services, telecommunications, energy, agriculture). To avoid these restrictions the VIE structure works as follows:

The Variable Interest Entity (VIE) is the legal vehicle engaged in the strategic industry which can only be held by Chinese owners. Another company, the Wholly Foreign Owned Enterprise (WFOE) is created in China. As its name indicates, it can be owned by foreigners because it is not related to a strategic industry. Foreigners may invest in the WFOE through a listed company, which may be in Cayman or anywhere.

What we care about are the dashed arrows between the WFOE (foreigners) and the VIE (strategic industry). They show how it is possible to have control and all the economic benefits of ownership, without actually owning the VIE.

Whitehill describes the necessary contracts and agreements involved:

A loan agreement and equity pledge agreement: WFOE (foreigners) transfers money to the VIE (strategic industry) as an interest-free loan and gets as collateral all of VIE’s assets and liabilities.

A call option agreement: WFOE (foreigners) has the right to purchase the VIE at a pre-determined price, usually the amount of the loan agreement.

A power of attorney in favour of WFOE (foreigners), granting it shareholder rights such as voting, attending shareholder meetings and submitting shareholder proposals.

A technical services agreement and an asset licensing agreement designating WFOE (foreigners) as the exclusive provider of services. These “services” justify why WFOE may get all of the VIE’s pretax income (as payment for those services).

In essence, a few contracts may replace ownership by giving control (through a power of attorney) and rights to all income and assets (through service agreements).

b) The use of derivatives and other financial instruments

If the Chinese VIE structure sounded complex, at least it was possible to understand it. In 2006 Henry T. C. Hu and Bernard Black published “The new vote buying: empty voting and hidden (morphable) ownership” describing that “hedge funds have been especially creative in decoupling voting rights from economic ownership. Sometimes they hold more votes than economic ownership – a pattern we call empty voting. In an extreme situation, a vote holder can have a negative economic interest and, thus, an incentive to vote in ways that reduce the company’s share price. Sometimes investors hold more economic ownership than votes, though often with morphable voting rights – the de facto ability to acquire the votes if needed. We call this situation hidden (morphable) ownership because the economic ownership and (de facto) voting ownership are often not disclosed.”

Some of these “simple” strategies involve lending shares for the day in which there is a vote and then returning them. This strategy is very similar to the Cum-Cum tax fraud, where shares were borrowed not to vote, but to defraud tax authorities. In the tax fraud, the holder of shares lends them before dividends are distributed to a party entitled to dividend tax reimbursement, eg based on their residence. After dividends are distributed, the tax paid and reimbursed, the shares can be returned to the original owner (who shouldn’t have benefitted from the reimbursement). Both parties agree to share the “windfall profit” from the evaded tax.

Instead of a loan, shares could also be sold with a right to buy them back either by contract, or by buying a “call” option from someone else, which is a financial instrument giving you the right to purchase a specific share at a given price.

Other strategies are much more complex and unless you have a very strong knowledge of finance, you’ll need to read the 99-page paper by Hu and Black and look up all the finance jargon (of which there’s a lot!) to be able to fully understand the strategies. As even the authors acknowledge, “the variety of decoupling strategies can be overwhelming”. They list some of them. For example, “empty-voting” strategies (more votes than economic ownership) include “share ownership hedged with equity swap” or “share ownership hedged with options”. Basically, voting rights are kept because shares are kept, but economic benefits are transferred by giving someone else a right to the share value. Another strategy, “insider hedging” refers to founders or CEOs who reduce their economic exposure without selling their shares (so as not to alert anyone). They keep their shares and votes, but they reduce their economic exposure by limiting losses and reducing potential gains. They do this by engaging in “zero-cost collar” which involves buying a put option (right to sell at a specific price) while simultaneously selling a call option (allowing the counterparty, the buyer, to purchase the share at a specific price). These strategies may also be reversed, where a player doesn’t have any votes (or shares), but is still exposed to the shares’ performance through financial instruments. This would have the same economic effect as holding those shares directly themselves. The authors described that based on market conditions, hedge funds engaging in these strategies may have a de facto voting right at their discretion (by unwinding the financial contract). They gave an example of hedge fund P: “[P] held ‘morphable’ voting rights – which could disappear when [P] wanted to hide its stake, only to reappear when [P] wanted to vote.” (page 837)

All of these hedge fund strategies may have more to do with securities law (and hopefully are understood by securities regulators to prevent abuses and more financial crises). For our purposes, financial instruments such as derivatives used and abused in the financial industry show that it is possible to own shares but give economic rights to someone else, or vice versa: having exposure to a share’s performance as if you owned it, without holding it. The same applies to voting rights.

c) Trusts