Here’s the 16th edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa produced and presented by finance journalist Idriss Linge in Cameroon. Nous sommes fiers de partager avec vous cette nouvelle émission de radio/podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Impôts et Justice Sociale, édition 16:Des chefs d’Etats Africains en appellent à une solidarité plus juste dans le monde

Dans cette seizième édition de votre podcast dédié à la justice fiscale en Afrique et dans le Monde, nous avons capturé la voix de trois président africains, qui lors de leurs interventions respectives à l’occasion d’un débat organisé par le New York Forum Institute, ont souhaité voir se manifester une solidarité plus juste dans le monde, face à la pandémie de Coronavirus qui fait son chemin dans différents pays.

Alassane Ouattara de Côte d’Ivoire a indiqué que l’après Codid-19 sera marqué par un nouveau paradigme

Macky Sall du Sénégal, lui, a trouvé injuste le peu de considération fait à l’endroit des efforts de l’Afrique et plaidé pour un effort de solidarité plus grand

A la suite de ces Chefs d’Etats africain, Adama Coulibaly est l’invité du podcast. Cet économiste responsable pour l’Afrique de l’ouest et Centrale de l’ONG OXFAM, revient sur la décision du G20, de suspendre le service de la dette des pays pauvres de la planète, dont 40 sont en Afrique

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le lien suivant

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

the sector depends heavily on public support — from tax exemptions from VAT and kerosene tax, to state aid for airports, low-cost airlines and infrastructure linking airports with nearby cities. Airlines also get 85% of their allocated pollution permits for free under the EU’s carbon market. The kerosene tax exemption in Europe alone is valued at €27 billion a year. Other more sustainable transportation methods — such as rail — have not benefited from such generous tax treatment.”

The idea of “no state aid to tax havens” has received public support around the world and some parliaments – eg Denmark, Austria and Scotland – have excluded companies based in tax havens from receiving Covid-19 state aid. The German finance minister Olaf Scholz seems to take a similar view:

anyone (…) who has placed his company headquarters in a tax haven cannot expect that this is now the right corporate structure to be able to claim state and taxpayer money in a crisis. We are quite clear on that.”

The idea also received support from more than 280,000 Germans, who signed a corresponding call for action by the NGOs Finanzwende and Campact.

Because Covid-19 has brought air traffic to a worldwide standstill, the German airline Lufthansa is one of the first companies to need massive state aid or else it faces insolvency. In response to German press raising issues with Lufthansa’s subsidiaries in the Cayman Islands and Panama – two countries from the EU’s tax haven list – Lufthansa voluntarily published selected information on its six subsidiaries in those countries, but that failed to create real transparency because important information (turnover, profits, taxes) and activities in other tax havens (Ireland, Malta, Switzerland, etc.) was missing from the disclosure.

The German government has now approved €9 billion worth of state aid with few conditions regarding tax transparency, mainly requiring Lufthansa to provide its country by country reporting to the fund administering the state aid (Lufthansa still seems reluctant to accept). Meanwhile, an analysis of Lufthansa’s financial reporting reveals big risks for state aid ending up in tax havens:

In total, the airline has 92 subsidiaries in corporate tax havens (using the Tax Justice Network’s Corporate Tax Haven Index as benchmark). In Malta, a subsidiary with only two employees made a profit of almost €200 million. Nine other Maltese companies are run by six employees and manage assets worth more than €8 billion.

In the last ten years, the airline paid only €3 billion in taxes on a profit of €15.6 billion. This corresponds to a rate of only 19.4 per cent compared to 32.45 per cent due at the company’s headquarters. Lufthansa’s tax practices have repeatedly led to high back payments and legal disputes in the past.

The individual ownership structure suggests that they too are moving their profits to tax havens. German billionaire Heinz Hermann Thiele, who bought 10 per cent of shares in March 2020, is particularly noteworthy. He has, on several occasions spoken out against state influence and is himself engaged in aggressive tax “optimisation” using a family holding in an inner-German tax haven. In addition, many of the institutional investors are structured via the Cayman Islands or Delaware.

In order for the public to be assured that state aid does not end up in tax havens, Netzwerk Steuergerechtigkeit recently called on the German government to finally abandon its years of resistance to public country by country reporting in the EU. Tax Watch (UK) makes further good suggestions on how the idea can become more than symbolic politics – besides a repayment obligation if tax authorities find tax avoidance in the future, they demand more capacity for tax authorities, a black list to exclude tax avoiders from state contracts, as well as detailed public data on state aid.

Em meio à crise econômica e sanitária, o governo brasileiro anunciou uma injeção de mais de US$ 185 bilhões para ajudar o setor financeiro — cerca de dez vezes o orçamento do Ministério da Saúde. Enquanto isso, 87% das micro e pequenas indústrias do Estado de São Paulo, por exemplo, não conseguem acessar a linha de crédito pública de US$ 7 bilhões, segundo o sindicato do setor.

Esse é apenas um exemplo dos desequilíbrios que o Estado pode gerar em sua atuação vacilante na atual conjuntura. Mas pode ser bem simples para um governo fazer escolhas técnicas e apartidárias, que beneficiem a população como um todo. O episódio #13 do É da sua conta detalha uma ferramenta da Tax Justice Network que ajuda governos a fazer escolhas justas na hora de socorrer empresas. É uma espécie de vacina contra abusos tributários para um país se certificar que o dinheiro público que pode ser usado para salvar vidas e promover a retomada econômica não vá parar num paraíso fiscal.

E na reportagem você ouve que enquanto algumas organizações sociais e indivíduos se solidarizam com populações pobres afetadas pela pandemia, algumas empresas que doam para a luta contra o coronavírus fazem lobby para descontar o valor que estão gastando com doações do imposto que deveriam pagar.

Em www.edasuaconta.com, você tem acesso a todos os episódios e links para todas as plataformas de áudio digital onde você pode ouvir o É da Sua Conta. Confira!

Last week we published the second part of our Tax Justice Focus special on climate crisis and tax justice. This blog reproduces the article contributed by economist Daniela Gabor*, in which she pinpoints the dangers of allowing private actors to take the lead in financing the transition away from fossil fuels to renewables, arguing that private financiers will reap the rewards while passing the risks to states and the general public, and hiding behind ‘subsidised greenwashing’.

Please note that this article was written before the Covid-19 pandemic took off in Europe and North America, precipitating the deepest economic depression in over a century.

Click here to download the first and second parts of our Tax Justice Focus special.

By Daniela Gabor*

The transition to a low carbon economy can be organised in two distinctive ways.

The first way, widely known as the Green New Deal, outlines a radical program of ecological and economic transformation led by the state. This involves massive investments in low-carbon activities – green industrial policies backed by green fiscal and monetary policies – while ensuring that decarbonisation happens in a just manner.

Critically, this calls for demolishing the political order of financial capitalism: undoing its ideological aversion to fiscal activism and state intervention, its commitment to the ‘independence’ of central banks, and to the political power of carbon financiers.

In response, a second, status-quo option is rapidly emerging from the financial sector. Let’s call it the Wall Street Climate Consensus. It promises that, with the right nudging, financial capitalism can deliver a low-carbon transition without radical political or institutional changes.

The WSCC grows out of recent changes in international development discourse, as for instance promoted by the World Bank in its ‘Maximising Finance for Development’ agenda, whose mantra is ‘leveraging private capital for development’. It promises institutional investors $12 trillion in “market opportunities” in transport, infrastructure, health, welfare, and education, to create new investable assets via public-private partnerships in these sectors and deeper local capital markets (or, as the World Bank puts it in a slick video, “to help private finance tap into developing markets.”) They are pushing risky and expensive ‘shadow banking’ practices onto poorer countries, likely to encourage privatisation and usher in long-term austerity, ultimately threatening progress on the SDGs. Under this consensus, nation states are supposed to protect the financial sector from the risks of investing in developing markets. This would privatise gains for finance and push losses onto low-income governments and the poor.

Now, along similar lines, carbon financiers are increasingly seeing the climate crisis not as a threat, but as an opportunity to make high profits, via “subsidised greenwashing.” The idea is that states will subsidise and protect finance from climate risks. This is a great opportunity for finance – and poses great dangers to the wider public and to the climate.

The Wall Street Climate Consensus involves a two-step strategy to promote the creation of apparently ‘green’ asset classes, while also preventing the state from getting too heavily involved in reducing carbon-intensive activities.

Step 1: promote metrics and “taxonomies” to enable greenwashing

The Wall Street Climate Consensus sees it as essential to define metrics and standards that assess the environmental performance of economic activities and companies – and thus of the “green-ness” of loans and securities that finance them. Strategically, they are pushing for public and private taxonomies (classification systems) to allow a broad interpretations of what ‘green’ means.

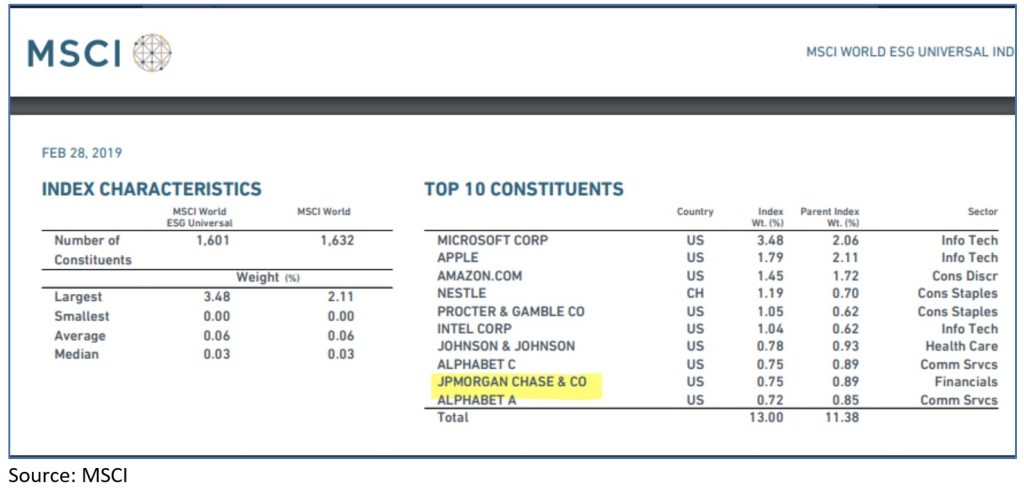

The most popular approach, pioneered by the private sector, relies on private Environment, Social and Governance (ESG) ratings, to evaluate companies and governments. Private ESG ratings are expanding fast, and are expected to apply to half of some $69 trillion assets managed in the US by 2025[1].

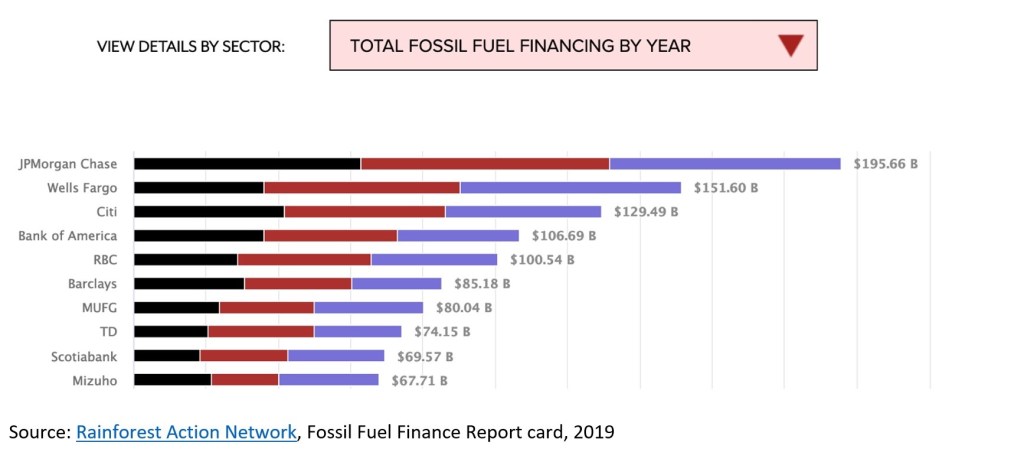

Private ESG frameworks are fertile terrain for greenwashing. For one thing, the various different frameworks offer confusing[2] and conflicting assessments of environmental performance, making it easier for borrowers to mislead investors about the greenness of the assets they purchase. For example, in February 2019 the ESG index run by MSCI, a big ratings agency, contained JP Morgan Chase in its top 10 constituents – in the same year that the bank was ranked (by the Rainforest Action Network) as the biggest financier of fossil fuels.

The multiplicity of private ESG frameworks also allows investors to shop around for the ESG ratings most favourable to themselves – and there is a wide divergence, allowing plenty of choice. (At one point, for instance, the FTSE’s ESG scored the car company Tesla at the bottom of its global auto ESG ratings, while MSCI ranked it as the best.)[3] Making matters worse, ESG rating companies face perverse incentives to award high ratings to firms.

For these reasons public ratings, by contrast, are potentially more effective than private ratings. However, carbon financiers have been successfully lobbying to water down one of the main public classification systems, the European Commission’s Sustainable Finance taxonomy. Originally, it identified “sustainable” economic activities as those that make a substantial contribution to at least one of six environmental objectives, and which cause no significant harm to the others[4], using quantitative thresholds[5]. But after heavy lobbying, the EU taxonomy has now expanded this to three separate categories: sustainable, “enabling”[6] and “transition”[7] activities. The two extra categories are supposed to encourage high-emitting companies to shift from ‘brown’ (polluting) activities to ‘green’ ones, by ensuring that enough financing is available. But in reality they open the door to greenwashing by introducing new complexities in setting and monitoring the quantitative thresholds, and also by restricting the scope for identifying “brown” (or polluting) activities.

Step 2: subsidies for ‘green’ products without penalties for brown

The financiers’ push to shape public and private classifications systems is not only about greenwashing. It is also about boosting profits, by channelling the growing political will to address the climate crisis into subsidies for green assets. For example, the European Commission is considering relaxing capital requirements for financial institutions holding green assets. Central banks, which are pioneers in the policy world in the climate change fight because of the financial-stability implications of extreme climate events, are also considering preferential treatment of green securities in their monetary policy operations (in their so-called ‘collateral frameworks.’). These may turn out to be very expensive for states and the wider public.

This nudging for green finance also seems to be accompanied by a low appetite for targeting ‘brown’ finance, even though penalties (via tougher regulatory requirements or via certain central bank operations) could rapidly accelerate the decarbonisation of the financial system, and shift capital flows away from polluting activities towards greener ones.

The success of carbon financiers in opposing “brown penalties” is partly a result of a long-running de-facto alliance between private financial sector players and central banks. The latter invoke ‘transitions risks’ to justify an incremental, green-subsidising approach, in line with what the Wall Street Climate Consensus wants. When they say ‘transition risks’, what they mean is that strictly regulating and curbing brown finance might result in stranded carbon assets which pose risks to financial stability.

Although central banks do not have the conceptual tools to adequately capture the mechanisms through which transitions risks may morph into financial stability risks, their emphasis on transition risks renders them critical allies for carbon financiers in the construction of the Wall Street Climate Consensus. For instance, Mark Carney’s speech for the COP26 hosted by the UK, and the COP26 private finance strategy, framed in the key of the Wall Street Climate Consensus, envisages a ‘3 R’ approach to leverage private finance for the climate fight: mandatory Reporting of climate risks, nudge private finance to improve climate Risk management via stress tests, and provide a better picture of Return opportunities from the transition to net zero, by moving from problematic ESG approaches to encourage investments in 50 shades of green[8].

While the nods to mandatory reporting and ESG weaknesses are commendable steps forward, the COP26 private finance strategy falls short on the truly transformative measures such as brown penalties or greening the operations of central banks.

Make no mistake: the Wall Street Climate Consensus will not turbocharge the climate agenda. It is designed to protect the status quo of financial globalisation.

Rapid decarbonisation can only happen if central banks and regulators convert to penalising brown rather than subsidising green, and use a credible definition of brown that minimises greenwashing. And states everywhere must take seriously the transformative power of green macroeconomic policies. This involves massive public investments in green sectors financed via ‘green’ coordination between fiscal and monetary policies. It should also include green safety nets to ensure a just transition, one that does not put the burden of decarbonization on the poor.

Furthermore, should governments fail to secure the cooperation of central banks for green macroeconomic policies, they could introduce a Green FTT on brown assets. This would be calibrated to (a) target brown assets and (b) remain in place until an adequately brown-penalising framework is wired into the operations of central banks and broader regulatory frameworks. Together with a carbon tax, this would ensure adequate financing for green public investments while simultaneously re-orient private capital towards private green investments.

[4] These are: Climate Change Mitigation; Climate Change Adaptation; Sustainable Use and Protection of Water and Marine Resources; Transition to a Circular Economy; Pollution Prevention and Control; Protection and Restoration of Biodiversity and Ecosystems. See more https://ec.europa.eu/commission/presscorner/detail/en/ip_19_6793

[5] The Technical Expert Group is in the process of identifying the list of activities and the attending quantitative standards across the six objectives.

[6] Enabling activities are defined as those activities that enable other activities to make a substantial contribution to one or more of the objectives, and where that activity: i) does not lead to a lock-in of assets that undermine long-term environmental goals, considering the economic lifetime of those assets; and ii) has a substantial positive environmental impact based on life-cycle considerations.

[7] Transition activities are defined as those ‘activities for which there are no technologically and economically feasible low-carbon alternatives, but that support the transition to a climate-neutral economy in a manner that is consistent with a pathway to limit the temperature increase to 1.5 degrees Celsius above pre-industrial levels, for example by phasing out greenhouse gas emissions.’ See https://ec.europa.eu/commission/presscorner/detail/en/QANDA_19_6804

Last week we published the second part of our Tax Justice Focus special on climate crisis and tax justice. This blog reproduces the lead article by famed German economist Peter Bofinger, in which he argues the case for a radical transformation of our understanding of how economics works, and why the state must take the financial lead in investing in a fossil fuel-free future. Please note that this article was written before the Covid-19 pandemic required neoliberal-leaning states to actively intervene to protect their economies from total meltdown. Click here to download the first and second parts of our Tax Justice Focus special.

To take climate change seriously, we must completely transform how we generate, transmit and store energy. We need to change the ways in which people and things move around. We must retrofit and refurbish our homes and offices and public buildings, to make them friendlier to the climate. As Jeremy Rifkin has rightly said, we need a Third Industrial Revolution.

This raises a big question. How can we pay for it?

To raise finance on the enormous scale required, only a few options are possible.

The first could be to tax carbon. But the big problem here is that this will tend to make fuel more expensive, which will in turn tend to hurt poorer sections of society the most. When French President Emmanuel Macron tried to impose new fuel taxes in 2018, protests by the Gilets Jaunes (or Yellow Vests) erupted on French streets, eventually forcing him to reverse course. The way around these potentially insurmountable political difficulties is to return the proceeds of carbon taxes (or the revenues from carbon trading schemes, as Prof. Jim Boyce argues elsewhere in this edition,) directly and equally to each citizen, as ‘carbon dividends’. So if such schemes are put in place, the revenues will likely have to flow back to the population, instead of being invested in green projects. Wealth taxes and higher corporate taxes can contribute, but to raise funds at the vast scales required are unrealistic.

Could we finance a third industrial revolution through public-private partnerships, where financial institutions raise the funds to finance green projects? This may help in some situations, but governments can generally borrow so much more cheaply than private sector actors can, so this is an extremely expensive option. (Elsewhere in this edition, Prof. Daniela Gabor raises additional warnings in about relying heavily on private finance.)

The only other solution that is big enough to address the challenge is for governments to borrow to pay for the green transformation. Interest rates are at historically low rates – bonds issued by some governments currently enjoy negative yields. There is no sign of inflation, and ample room for borrowing. So in this environment, government borrowing is by far the best way to pay for the green transformation.

But there is an obstacle. That obstacle is a mindset, which says that governments must not borrow, they must not add to the national debt, and they must not spend more than they receive in revenue. Budget deficits must be zero. We Germans call this Schwarze Null, or Black Zero.

And here is the crux of the current problem facing Europe. If Black Zero says you cannot borrow to invest, then we cannot pay for a credible green transformation, at least without savage, economy-damaging cuts elsewhere.

Yet in Germany there is a broad consensus that while climate change is important, Black Zero is much more important. We need Black Zero, the thinking goes, to protect our children and our grandchildren from large public debts. Black Zero first, climate second. And Germany is the most powerful country in Europe – so this way of thinking suffuses European policy-making.

Where does this bias against deficits come from? In Germany there are historical reasons for its existence: old memories of hyper-inflation, and more? But in fact, it is taught in standard economics textbooks around the world, and a generation or more of economists has fallen under its spell.

For instance, in his popular book The Principles of Economics, Greg Mankiw says that public debt “crowds out” private debt. That is in the main introductory text that millions of students have read, and it’s presented as a fact of life: that whenever a government increases its debt and runs a deficit, this reduces private savings and private investment. They do not qualify this in any way in this main text book.

But this argument is completely wrong. It rests on the outdated classical logic of a corn economy. The idea is that if a household saves corn, and the government grabs some of that corn, then there is less corn to plant or to eat. That may be true for a household that saves corn. But they are untrue if there is a financial system. The government does not absorb someone else’s money when it borrows and spends. As John Maynard Keynes explained, you don’t have to consume less to get financing: it comes from banks or from capital markets. The financial system creates money. And when the government borrows it spends the money into the economy immediately. (This idea is also embedded in Modern Monetary Theory, by the way.)

Another related theory, known as Ricardian Equivalence, says that the government is like a household, and if it borrows today it must repay it eventually through higher taxes in future years. So, this theory goes, it is kindest to our children to reduce government debt eventually to zero.

But again, this makes no sense. If you can to borrow money at a one percent annual interest rate, for example, and invest the proceeds in a project that will yield four percent returns, your economy – and likely your children – will be better off? The ensuing growth of your economy means that this productive borrowing could also reduce your debt as a share of your economy. And if you can borrow at negative interest rates – as you can now – this equation becomes even more attractive. Not only that, but government bonds are safe assets: people in the financial sector right now are worrying that there are not enough safe assets. And there is high demand for green bonds.

The money is there for the taking. Yet this anti-borrowing obsession has been embedded into German and European institutions for decades. For example, in the 1992 Maastricht Treaty that established the European Union, it was decided that governments should bring their debts down to or below 60 percent of GDP. But 60 percent is a totally arbitrary number! A doctor who tried to treat a patient on such a basis would be sued. It inflicts pain. If a debt limit means you spend less on the things that matter, then it is almost criminal.

Germany’s climate package approved in December last year is another case in point. It says that we do not want to tax carbon immediately: we can wait until 2021. If you subtract revenues from trading carbon certificates, Germany envisages spending just 0.2 to 0.3 percent of GDP. This is peanuts. It will not tackle climate change effectively.

China, by contrast, has been running double digit deficits for years (if you include national and provincial government budgets). It has borrowed enormous sums, spent more on renewable energy in the past decade than the United States, Japan and Germany combined, and enjoyed large economic growth at the same time. Especially for large economies, there are almost no limits to the deficits that countries can run.

Public debt is a bit like drinking. Excessive drinking is obviously bad. So what is the right amount?

A good way to decide is to avoid textbook theories and to follow the “Golden Rule” for fiscal policy. If governments make investments from which future generations benefit – as with green investments – why should it pay for those from current revenues? And green investments can be highly productive: if we retrofit the whole housing stock for energy efficiency, for instance, there can be major energy savings, potentially making these investments very profitable in economic terms.

There is more good news here. The Euro area could stabilise its current debt to GDP ratio at around 90 percent, while running a 2.7 percent fiscal deficit, assuming a reasonable nominal GDP growth rate of 3 percent per year. People are talking about a Green New Deal (GND) requiring €150-200 billion per year, which is worth just 1.3 – 1.7 percent of GDP. So we could finance the European GND, with plenty left over for other spending priorities, and without even increasing European debt levels. (And even if we did increase the debt, it would likely harm neither us nor future generations anyway.)

We could increase borrowing in several ways. One would be to exclude green investments from the European Stability and Growth Pact, which forces European governments to curb deficits and borrowing. Another way is to issue Euro-bonds with joint liability, justified by the fact that the climate isn’t a national issue but a European (and global) one. A third way, suggested by Paul de Grauwe, is for the European Investment Bank to issue bonds to finance green investments, and for the European Central Bank to then purchase these bonds as part of its long-term asset-buying programme.

I only see two potential constraints here. One is labour: massive green infrastructure investment requires a lot of labour that cannot be done by robots. But with widespread automation and digitalisation threatening many jobs, job creation is likely to be highly positive for Europe.

The second obstacle is Germany. The mindsets on debt in Germany are rigid, even if some economists are at last starting to think differently. This is the real constraint on financing the Green New Deal.

The money is there. The Golden Rule has never been more appropriate than today, when we have such low interest rates, and even negative rates. Almost nothing can go wrong if we borrow more to finance this productive investment.

[1]Peter Bofinger is a Professor of Monetary and International Economics at the University of Würzburg, and was a member of Germany’s five-strong Council of Economic Experts from 2004-2019.

In the Tax Justice Network’s monthly podcast, the Taxcast:

we cover the story the mainstream media aren’t telling you – how governments around the world are undermining our tax collection services. We look at how the South Africa Revenue Service was established in very challenging times to become a world class institution. Yet also how quickly such achievements can be set back…

Also, as all eyes turn to Central Banks during this coronavirus pandemic, we ask who are they serving? And how do people forge a new relationship and a new role for them that fits modern times? We look at the profound implications of a little-known court ruling this month in Karlsruhe by the German Constitutional Court concerning the actions of the European Central Bank – the second-most important central bank in the world

A transcript of the programme is available here (it won’t be 100% accurate)

Presented and produced by Naomi Fowler of the Tax Justice Network.

It was known as the higher purpose…it was certainly one of the reasons why I think the revenue service was able to over the years grow and develop and become this world class institution that it did ultimately become. It was not just a job. It was a heart and mind labour of love.”

This court ruling coming out of Karlsruhe might lead to a rethink about the role of central banks in the 21st century. To whom should they be accountable, whose interests are being served by the charade of political independence and how can we make central banks accountable to the public they notionally serve?”

Want to download and listen on the go? Download onto your phone or hand held device by clicking here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher.

Join us on facebook and get our blogs into your feed.

WATCH: Cuts to tax office workers: a global trend:

This video shows tax office workers from Ealing tax office in the UK protesting against the closure of their tax office, also featured in this month’s Taxcast. They’re supported here by PCS (Public and Commercial Services Union) and several MPs, all questioning the commitment of the government to efficient tax collection services run by people with decades of experience. Unfortunately this is a trend worldwide, just when we need tax the most.

I’m working on a project to understand women’s attitudes towards, and knowledge of tax and I’ve designed a short survey of eleven questions which takes about two or three minutes. There are no ‘right’ or ‘wrong’ answers. No one will know who you are – it’s completely anonymous. The survey focuses on what tax means to you and to those you care about and it doesn’t matter if you know a lot, a little, or nothing.

I want to get a clearer picture of women’s understanding of tax and how they see it impacting on their lives. There are lots of words and technical language used to describe what tax is, what it does, why it matters. But its’s often difficult to grasp how it affects our lives on a day by day basis.

I specifically want to survey women over the age of eighteen years old, women from different backgrounds, women on low incomes or no income and those living on their own or caring for others.

An interview

The final question in the survey asks if you’d consider talking to me in more detail about your understanding of tax. The information I collect would be recorded but no one will be able identify you. I’d conduct the interview online. I’ll provide you with instructions on how to set this up. You just need access to a computer, a lap top or a smartphone, using Skype, Zoom, or WhatsApp, whatever works best for you.

I know many people are under a lot pressure and facing multiple difficulties at the moment during the COVID pandemic. An interview is not for everyone. If you indicate you’d like to undertake the interview with me, you can change your mind at any time, it’s completely voluntary.

If you opt for an interview I’ll record it and would need your permission to do this. I’d then save the recorded interview on a password protected site.

If you would like to volunteer for an interview and English is not your first language let me know.

My survey is available here. Thanks for your help.

As the economic shock of the pandemic deepens, hunger stalks the streets of supposedly rich countries, revealing the deep inequalities that existed even before Covid-19 struck. In the second of our two part Tax Justice Focus edition on financing the climate transition, we explore the links between economic justice and climate justice, and argue that the two struggles are inseparable. In the coming weeks we will be blogging all the contributions from our guest writers. Today we start with Nicholas Shaxson’s editorial. The first part of this edition is available here.

The world is divided between those who worry about the end of the world and those who worry about the end of the month, a French “Yellow Vest” protester said in 2018. That is a starting point for trying to understand how to pay for two emergencies: the huge costs of the unfolding economic shock of the Covid-19 lockdowns, and the even bigger long term costs of re-engineering our economies and our lives needed to stop potentially catastrophic global heating.

According to the International Energy Agency, the world needs $3.5 trillion in global energy-sector investments alone every year until 2050, if we are to limit global temperature rises to 2.0 degrees centigrade.

Many people think that the fight to protect the world’s climate is separate from the struggles to tackle inequality, oligarchy, or racial or gender injustices. This is a dangerous delusion, for – as this edition of Tax Justice Focus shows – the two struggles are inseparable, and each will fail without the other. This is for several reasons.

First, we face many of the same enemies, such as Charles Koch, Rupert Murdoch and other powerful interests who have financed both climate denialism and campaigns to persuade voters to cut taxes and deregulate our economies – with the Trumpian aim to override democracy and build oligarchic power at all costs. It is hardly surprising that their campaigns go together: according to the French economist Thomas Piketty, the richest 1% of the planet emit more carbon than the poorest 50%. Meanwhile tax havens reduces states’ ability to address environmental threats, while also providing safe havens for fossil fuel wealth looted from the environment.

A second reason was articulated by the Yellow Vest protesters in France, furious that ordinary folk are asked to pay new carbon taxes while unaccountable elites engorge themselves on state largesse. If the gigantic costs of the carbon transition are shouldered by lower-income groups, their rage at being shafted – again – will create fertile ground for demagogues and conspiracy theorists to recruit them in their millions and overturn the climate movement. This is already happening extensively in the United States, Brazil, and elsewhere, and it is also a reason why the climate movement is struggling to emerge from what one of its leaders has called its “white, middle class ghetto.”

The Taiwanese academic and author CHIEN-YI LU outlines a third reason why the two struggles are inseperable, in her article for this edition of Tax Justice Focus. Neoliberalism, an organised programme to usurp democracy by replacing political decision-making with economic calculations, is the bedrock of the climate crisis, she explains. Neoliberalism was always a strategy that used deceit to undermine progressive Keynesian economic ideas, just as climate denialists have undermined climate science. The trick has been to give people the appearance of empowerment through individual choice and freedom – but in the process atomising and dividing them and thus dismantling and discrediting the idea of society, government and the common good. That common good includes the climate, of course. To tackle global heating, or economic inequality, using any approaches based on individual empowerment and freedom will fail.

So economic justice is not just a nice add-on to climate justice: we must join forces. This must not be a story of environmentalists against workers, or of poor nations against rich ones. It is a battle to organise to rebuild the common good, against the tax haven-using carbon elites and economic elitists. There is no other way to proceed.

So: how can we pay for the climate transition in a progressive way?

Part One of our edition on tax justice and the climate, published last month, provided some answers: removing $400 billion in annual fossil fuel subsidies; transparency through new climate-friendly accounting standards; activism from groups like Extinction Rebellion; and a scheme to auction carbon permits and redistribute the proceeds equally to all citizens. In this edition, JACQUELINE COTTRELL now shows that carbon taxes can be progressive – if governments step up and design the policies in the right way.

Leading this edition, PETER BOFINGER, arguably Germany’s best known economist, kicks back against a deadly German consensus known as Black Zero: the idea that governments must always match spending with tax revenues and not borrow or run budget deficits. His article Black Zero against the Climate, written for us just before the Covid-19 crisis erupted in Europe, unpacks the “corn economy” fallacies and misunderstandings that underpin Black Zero and shows why states can and must borrow (and use central bank intervention) to pay for the transition. But German thinking has infected the European Union through mechanisms such as the Stability and Growth Pact, and now risks sabotaging the possibility of climate funding.

If states cannot finance the climate transition, then the financial sector will do it.

This would pose immense dangers, not just because states can borrow to spend far more cheaply than private actors can, and because states are accountable to citizens whereas financiers are not.

Financial sector players will also use an array of tried and tested mechanisms to shift the risks of investment onto the public, and shift the rewards to themselves. They specialise in creating and occupying economic choke points through which the vast sums must pass, from which they can milk great wealth that would otherwise be spent on the climate, or on softening the economic blow of the transition (or of the Covid-19 crisis). As former Bank of England Governor Mark Carney crowed earlier this year, the immense sums required to finance the climate transition “could turn an existential risk into the greatest commercial opportunity of our time.”

This is an existential danger to us all. It is the climate version of the Finance Curse, and the subject of our next article, The Wall Street Climate Consensus by DANIELA GABOR, a world expert on finance and shadow banking. The transition can be financed in two ways, she writes. The first would follow a Green New Deal logic, with state-led green industrial policies and monetary policies, and strong penalties for polluters. The other, status quo route, sees private actors providing the financing: they will harvest the rewards while states and taxpayers take on the risks, in a dangerous game of “subsidised greenwashing.” She outlines just how to confront the Wall Street Climate Consensus.

Economic crisis is an opportunity for deep-seated change. The Covid-19 crisis seems unlikely to melt away with a V-shaped recovery, and a return to the status quo. The time to push new ideas is NOW.

The 18th Century political philosopher Edmund Burke summed up how to proceed –

When bad men combine the good must associate; else they will fall, one by one, an unpitied sacrifice in a contemptible struggle.”

If we do not unite climate justice with economic justice, tax justice, racial justice and gender justice, those worried about the end of the month will become the enemies of those worried about the end of the world. The result will be an environmental, economic and political catastrophe.

Download and read the full edition of this round of essays here.

Download and read the first part of this edition here.

By Tommaso Faccio, co-founder of Tax Justice Italia

With the support of, and in partnership with the Tax Justice Network, Tax Justice Italia was launched today with the aim of adding a credible voice for tax justice in Italy. Tax Justice Italia will work to change the debate around taxation in Italy, counter the prevailing narrative that taxes need to be cut and dispel the misconception that it is legitimate to avoid or evade taxation. The new organisation aims to raise awareness among people across the country on the importance of tax for a strong economy and a healthy society.

More than €100 billion in tax is evaded in Italy each year and 15% of corporate tax obligations in Italy go unpaid each year through the use of tax havens. The amount of private wealth held offshore is estimated to be 8% of Italy’s GDP. These are just some of the reasons why a tax justice organisation is needed in Italy today.

Tax abuse deprives Italy of much needed revenues to boost investment in public services, such as health and education, and to finance sound anti-poverty measures. Furthermore, tax evasion severely hampers the redistributive function assigned to the progressivity of the Italian tax system, especially in personal income tax. This is a major problem for a country that displays a high level of pre-tax income inequality and one of the lowest levels of inequality reduction through taxation in the EU.

With the G20 presidency looming in the distance and the revived debate around tax havens within the EU, the time is ripe for a new organisation.

Our first work “Paradisi Fiscali: il caso Eni” analyses country-by-country data published voluntarily by the Italian major oil firm Eni, which is effectively controlled by the Italian State, analysing its presence in a number of tax havens and its approach to taxation. Given the Government’s recent strong rhetoric against EU tax havens, the report provides an opportunity to hold the Government accountable for the tax policies adopted by its state-controlled companies.

You can follow the work of Tax Justice Italia on our website or on twitter @taxjusticeIT.

Welcome to this month’s podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! (Ahora también estamos en iTunesy tenemos un nuevo sitio web.)

En este programa:

La pandemia y una nueva explosión de deuda mundial

¿Qué pasa con la deuda de los países pobres y en desarrollo? ¿Cancelación, suspensión o reestructuración?

Un viaje alrededor del mundo con las nuevas iniciativas para que las corporaciones y las grandes fortunas aporten al financiamiento de esta crisis.

Y cómo la falta de inversión previa en salud, está impactando a Centroamérica.

INVITADOS:

Andres Arauz, ex director del banco central de Ecuador, y economista hoy de la UNAM, la Universidad Nacional Autónoma de Mexico

Powerful shocks like pandemics, wars or financial crashes have an impact on society, but the nature of that impact depends on the theories people hold about history, society, the balance of power – in a word, ideology – which varies from place to place. It always takes major social and political mobilisation to move societies in the direction of equality.”

The Financial Transparency Coalition (FTC), a group of civil society organisations from around the world, invites you to a virtual conference on 28 May from 13:00 to 15:30 CUT. Drawing upon their deep expertise and influential network, the Coalition will consider how to prioritise reforms and policy innovations on tax and transparency that can secure greater revenue and ensure that less is lost to secrecy and abuse. This an important opportunity to understand the contributions needed for systemic change that can point us “in the direction of equality.”

Speakers including world leading economist Professor Jayati Ghosh, Jawaharlal Nehru University; Logan Wort, executive director of the African Tax Administrators Forum; Alex Cobham, chief executive of the Tax Justice Network; Professor Emmanuel Saez, director of the Center for Equitable Growth at at the University of California Berkeley (invited).

For anyone who cares about beneficial ownership transparency the spotlight should be on the EU – where public beneficial ownership registers became mandatory in 2020 – and Germany, which is struggling with the issue of anonymous real estate ownership in the face of a looming review by the Financial Action Task Force and a public alarmed by rising prices, which have exploded, in part due to an influx of anonymous international investment.

Just in time for the EU directive – but later than the UK, Denmark or Luxembourg – Germany made its beneficial ownership register public at the beginning of 2020 and has become one of the first countries worldwide to oblige foreign real estate buyers to register in the local beneficial ownership register.

A new study by the Rosa Luxemburg Foundation traces the ownership of more than 400 companies owning real estate in Berlin through public and commercial registers worldwide – including the German and other European beneficial ownership registers – concluding that nearly a third remain anonymous and transparency remains an illusion. It takes 15 examples and shows how implementation and enforcement of beneficial ownership transparency has failed in Germany (and other European registers) and why the EU definition of beneficial ownership remains fundamentally flawed.

When the German parliament debated the implementation of the EU’s 5th anti money-laundering directive most politicians, experts and the public agreed it should go ahead. The national risk analysis and the financial intelligence unit had identified real estate as a major risk area for money laundering and the Finance Ministry’s Secretary of State asked parliamentarians for additional ideas, in particular in the area of real estate. A prosecutor from Berlin pointedly reminded the parliamentarians that anyone who buys a house in Berlin using a company from any secrecy jurisdiction stays beyond the reach of law because prosecutors have no way of determining the real owners. And last but not least, due to soaring purchase prices and rents, many tenants are no longer willing to accept anonymous investors and dirty money. The press took notice. Everyone wants to know: Who owns our cities?

Besides opening the beneficial ownership register to the public (as foreseen in the EU directive), parliament passed one amendment that obliges any company from outside the EU wanting to buy real estate in Germany to register, and another allowing – or obliging – notaries and real estate agents to increase scrutiny of real estate transactions.

But despite all these efforts the study by the Rosa Luxembourg Foundation shows that answering the question of who owns Berlin remains impossible for two reasons:[1]

The German beneficial ownership register was badly designed and is not effectively enforced.

The concept and definition of beneficial ownership in the EU and FATF guidelines is seriously flawed.

Anonymous companies owning Berlin real estate

135 of 433

Missing entry in the transparency register despite compulsory registration

83 of 111

No beneficial owner according to current definition (25%)

82 of 135

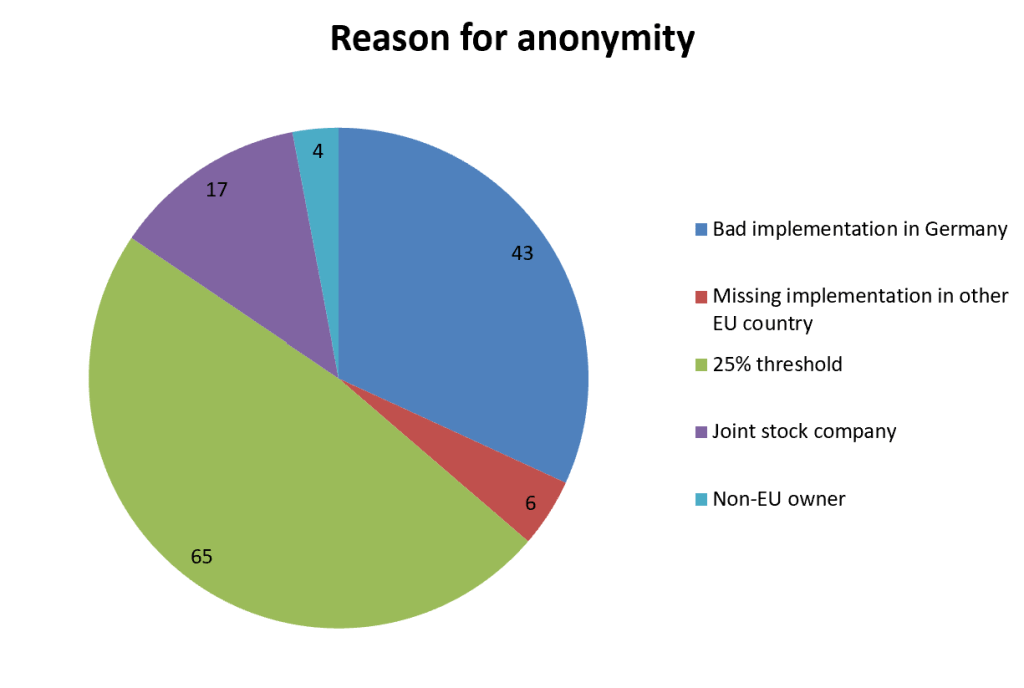

Under these circumstances the new rule forcing foreign companies to register in the beneficial ownership register is purely symbolic and easily circumvented. Out of 433 companies owning real estate in Berlin that were analyzed for the study 135 remained anonymous. Of 111 relevant cases – i.e. where the beneficial owner was not already known through the German company registers – there was no entry in 83 cases and a real beneficial owner in only 7. In at least 82 out of the 135 cases the real owners remained anonymous, using joint stock companies and investment funds to ensure they didn’t surpass the 25% threshold to register as a beneficial owner.

Germany vs. EU – the state of play of beneficial ownership registers

Even though beneficial ownership registries have been obligatory in the EU since 2017 and their publication was due at the beginning of 2020, only six countries (UK, Denmark, Luxembourg, Latvia, Slovenia, Bulgaria) made their register freely accessible by then. Seventeen countries either don’t even have a beneficial ownership register (such as the Netherlands and Cyprus) or haven’t made it public (such as France and Spain).[2] Germany created the register in 2017 and made it public by 2020 but there are two big issues that hamper its usefulness:

First, Germany is one of only four countries (with Malta, Sweden, Norway) that don’t make the register mandatory. On top of that, instead of integrating the beneficial ownership register with existing ones (like Denmark, the UK or Malta) Germany (like Austria or Luxembourg) opted to create a separate register that is badly integrated. In theory, companies that already register their beneficial owners in Germany are spared additional bureaucracy. In practice this doesn’t work. As limited companies already have to publish all shareholders in the company register, typical real estate owners – Germans owning real estate through German companies – are fully transparent. But there are also many foreign companies that hold shares of German real estate companies and whose beneficial owners consequently can’t be found in the German registers. Nearly all of these German companies failed to register in the German beneficial ownership register and, because of the poor integration of the two registers, the oversight body is unable to efficiently identify companies with foreign shareholders that should register in the beneficial ownership register.

Second, a significant share of Berlin real estate is owned by joint stock companies, investment funds or companies claiming to have no beneficial owner above the 25% threshold set by the EU definition. As German joint stock companies, they have to disclose anyone owning more than 3% of their shares and record ownership in the internal, non-public shareholder register – but they often record and know only the name of the wealth manager or the bank administering their shares, rather than the beneficial owner. Many of the investment funds are structured as a combination of Cayman Island partnerships and Luxembourg SCSp – which means they don’t register their investors in any of the existing registers. Likewise the Seychelles LLC owning German real estate via Luxembourg can easily claim to have no beneficial owners under the existing criteria without much chance for verification – especially considering the absence of proper registration, the missing international cooperation and the existence of vehicles such as protected cell companies in many of these secrecy jurisdictions.

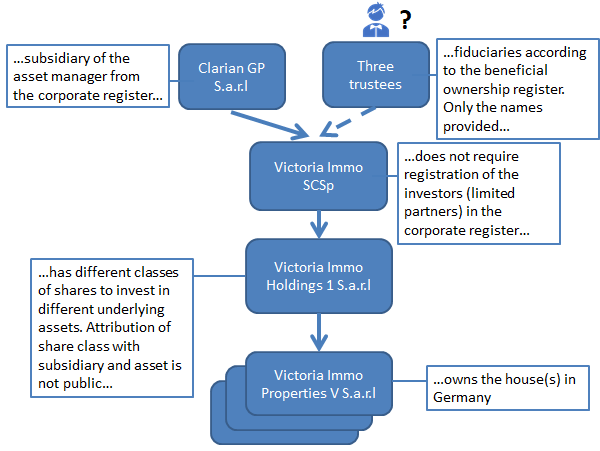

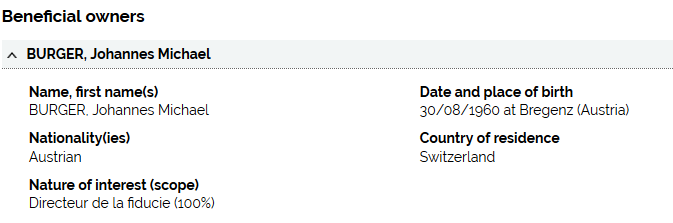

The cases analyzed in the study show the potentials and limits of beneficial ownership registers in various ways. One particularly instructive case revolves around a traditional book shop in Oranienstraße (Kreuzberg) fighting against eviction by an anonymous owner that might well turn out to be the heirs of the Tetra Pak fortune – mostly philanthropists with a reputation to lose.[3] While the owners use an SCSp to avoid registering the shareholders in the normal corporate register, the beneficial ownership register contains the names of three lawyers working for Liechtenstein’s biggest multi-family office.

But the beneficial ownership register doesn’t contain the name of the trust or vehicle they are representing nor of the final beneficiaries (which would remain unknown anyway because Liechtenstein hasn’t adopted a beneficial ownership register yet).

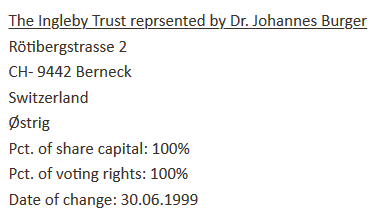

Extract from the Luxembourg beneficial ownership register

In contrast the Danish beneficial ownership register (concerning an unrelated company) lists the same three lawyers as representatives of the Ingleby trust connected to the Tetra Pak heirs. Because of this ambiguity the owners of the bookshop in Kreuzberg continue to wait for the confirmation of who is trying to evict them and whom to appeal to.

Extract from the Danish beneficial ownership register

The examples and results of the study show – creating a new and parallel register and trying to avoid double-entries by exemptions for beneficial owners already registered in traditional registers was a very bad idea. To fulfill the FATF requirement of effective beneficial ownership transparency Germany will have to ensure proper integration and consistency of the registers or learn from its neighbors and change the approach. The German case is also a perfect case example to demonstrate that without public scrutiny completely dysfunctional registers can proliferate for years – something that is hopefully going to change now that the register is public. And finally the study shows that through the EU and worldwide a lot of work remains to make existing beneficial ownership register work and to eliminate the limitation that allow the proliferation of anonymous ownership.

[1] In addition, German land registers are accessible only after proof of a legitimate interest. That’s why – instead of doing a full analysis or a random sample – the study was based on owners identified through a crowd-based collection of ownership data from tenants, journalists and local politicians.

N.B.The Tax Justice Network apologises for the use of an image of a palm tree in this article to represent tax havenry. The palm tree trope is widely used across media to associate international tax abuse largely or exclusively with small tropical islands whose populations are predominantly non-white and/or Black-majority. Evidence shows that the vast majority of international tax abuse is driven by rich OECD countries like the UK, US, Switzerland, Luxembourg and the Netherlands – yet it is small island nations that are often targeted by international policymakers while rich OECD countries are afforded exemptions. This colonial and structurally racist situation is bolstered by the use of the palm tree/island trope in media coverage of tax abuse. While the Tax Justice Network took the internal decision years ago to ban the use of the palm tree trope in our publications, we have kept our past uses of the trope up in order to be transparent about our past actions, rather than erase them, and to reaffirm our commitment to reject the trope going forward.

Acknowledgement: The Tax Justice Network is grateful for the information provided by India’s Self Employed Women’s Association (SEWA).

The COVID 19 pandemic has ‘flipped’ our understanding of many things which we took for granted pre-lockdown. One of these is the role of the state.

States have needed to act to protect our health, our incomes, our industries. This has restricted freedoms and invested powers in institutions that we might not have thought sanctionable only a few months ago. While the picture and level of intervention varies from country to country, questions about the obligations and responsibilities of the state and commitments made by the state under inter-governmental and in international law are important – including with respect to the role of tax and financial transparency in relation to human rights obligations.

The many reports of death, hardship and distress mean that governments will need to think carefully about how they can, and should, meet social and economic rights. Part of these political debates will need to include how resources are distributed and what policies are needed for their redistribution to protect the vulnerable and most marginalised from further inequalities and discrimination.

The impact of COVID-19 on informal women workers is especially hard. Many of us will remain ignorant of how women’s lives are torn apart by the COVID-19 pandemic. Knowing begs the question: what should be our response? How best to alleviate hardships born by women working in the informal economy; the most marginalised in societies? What should our governments, our intergovernmental institutions, do to mitigate the extreme impact of insecurities – food, income, housing, water, sanitation which have been triggered and exacerbated by the pandemic?

India’s Self Employed Women’s Association (SEWA) have documented, and continue to document the extreme hardships of women working in the informal economy. According to SEWA, 93 per cent of India’s workforce is in the informal economy. In the short term, the state and international financial institutions need to step in to shield informal women workers from the shocks of crisis.

Establishing progressive tax systems and developing robust global financial transparency is key to anticipating the effects of social and economic crisis, and to protecting the rights of gender and race. Doing so, for signatory states such as India, also opens both the possibility of “leaving no one behind” as Agenda 2030 (the Sustainable Development Goals) intends, and to meet obligations set out by human rights instruments including the Convention on the Elimination of all Forms of Discrimination Against Women (CEDAW) and the International Covenant on Economic, Social, and Cultural Rights (ICESCR).

The right response?

The COVID-19 crisis exposes long term political, social and economic ‘rights’ failures. The plight of many millions of informal workers is an injustice and a rights failure – and a failure to repay the social and economic value that is extracted from women’s informal labour in agriculture, food production, caring, and domestic work.

In India one response to COVID-19 has come in the form of a World Bank loan. Immediate relief is critical as the International Labour Organisation (ILO) has underlined, but this is also a time to underline the need to act for systemic and sustainable change.

21-day curfew – devastation for women

While the COVID-19 pandemic has already led to the loss of jobs and incomes for millions of workers around the world, for millions of poor women agricultural workers and small farmers in India, the 21-day curfew announced on March 22nd has been devastating. Living on the edge of poverty and hunger even before the disease, people now face a ban on movement and transport which has crippled the harvesting, distribution and sale of fresh produce and winter crops. The economic threat for many women and their families is grave.

Failing to recognise the reality – Banks’ loan

moratorium

The winter harvest includes crops such as wheat, barley, mustard, canola, sesame, peas, etc. and fresh produce. Many women small farmers had finalised the trade of their produce. They were hoping to pay off their agricultural loans using the income from the sale of their harvests. However, due to the lockdown traders could not pay the farmers. While the Reserve Bank of India announced that all lending institutions should institute a 3-month moratorium on loan repayments, it did not waive the interest on the loans; thus, poor women farmers will have to pay a higher interest. Additionally, as many small farmers borrow from local moneylenders the moratorium does not include them, leaving many women workers without the income to pay back their loans. The government’s deferral of payments on credit card dues[1] will, similarly, yield little or no benefit to poor women in the informal economy.

More than 10,000 small and marginal farmers and vegetable growers from Gujarat as well as farmers in the states of Kerala, West Bengal, Rajasthan, and Punjab could not take their fresh produce such as tomatoes and cabbage to the market. The income they generate from the sale of fresh produce has dropped to almost half. For example, tomatoes should sell for Rs.5 per kg but the women are only receiving Rs.1 to Rs.3 per kg.

Many small farmers had harvested their cotton and wheat and had stocked it in their homes waiting for traders to pick-up the harvest. But due to the COVID-19 crisis, migrant workers are moving back to their homes in villages. However, the homes are full of harvested crops and there is no room for returning family members who are migrants.

Prime Minister Modi made the drastic decision about the 21-day curfew without any considerations for the daily lives of millions of poor women and men and their families. For women and men who live on the margin of daily wages and daily purchase of food, the restrictions on movement mean they are closer to hunger and death even before getting sick with the Covid-19 virus.

Eye catching vs sustainable

In the short-term, social and economic crises require a rapid response. So far the eye-catching responses and “beacons of better” are few and far between. Viet Nam, South Korea and New Zealand appear to have minimized the impact of the COVID-19 virus, for now at least. Denmark and Poland have caught the public mood and imagination on corporate greed with plans to exclude tax haven registered companies from public bailouts (although we have argued that a somewhat broader approach will be needed to ensure benefits).

Responses to COVID-19 in many OECD countries are operating upon the foundations of “austerity” policies, a deliberate shrinking of the state through ideologically led social and economic policy. Not surprisingly, the most aggressive countries in this aspect have found themselves floundering – either reversing economic stance quickly but finding the underlying structures unprepared (by policy), as in the UK for example, or continuing to struggle with the intellectual dissonance between ideological stance and evident need, as in the USA. Most importantly, many of the most marginalised groups suffer and are left behind to fend for themselves. Short-term actions are needed, but based on a progressive systemic, long term approach.

In India, the Tax Justice Network’s Financial Secrecy Index 2020 has documented the progress made in recent years, in terms of addressing financial secrecy. This has included important revisions (2016) to the damaging double tax treaty arrangement with Mauritius. But there remain ongoing problems including “unnamed” ownership.

The transparency of India’s financial architecture is at best partial. Enactment of a Prevention of Money Laundering Act and the establishment of an Financial Intelligence Unit made for an early engagement in, and signature to, the OECD’s Multilateral Competent Authority Agreement (MCAA) for Automatic Exchange of Information (AEOI) in 2015. All this has helped to tighten up on “unnamed” money – money laundering and tax dodging. The 53 active Automatic Information Exchange Agreements India has in place will help to curb illicit finance flows and tax dodging, but more could be done.

Building

foundations

Most countries are “guilty” of systemic tax and financial transparency failures. If addressed, such failures could create opportunities to strengthen rights protection and build formidable social and economic foundations.

A progressive tax regime, as the tax justice movement has long argued, is critical to halt the tide of so called profit shifting by multinational corporations and cement the possibility of taxing rights, in particular, in developing countries. As well as being recognised by experts around the globe as an essential element for clamping down on huge tax dodging it is a critical part of a financial transparency policy platform needed to address inequalities and human rights failures.

Governments need to match their domestic actions to the strength of their voice on the international stage. While India continues to take progressive positions in international fora such as the G24 – by advocating for more taxing rights for developing countries and pushing for unitary tax approaches – the same cannot be said for its national positions and political bent which has favoured bailouts while leaving the most vulnerable to suffer.

On 24 April 2020 the US Court of Appeals for the fifth

circuit ruled

that a US law firm must disclose to the US tax authority (the Internal Revenue Service)

the names of requested clients in connection to an investigation. Specifically,

the Internal Revenue Service (IRS) had asked for documents identifying any US

clients at whose request or on whose behalf the law firm had acquired or formed

any foreign entity, opened or maintained any foreign financial account, or

assisted in the conduct of any foreign financial transaction, including records

or other data relating to setting up offshore financial accounts and the

acquisition, establishment or maintenance of offshore entities or structures of

entities.

The issue at stake was whether attorney-client privilege

would allow the law firm to reject the summon. It didn’t.

The law firm, however, wasn’t picked at random. The ruling

describes that the investigation arose because during the audit of a US

taxpayer, it was revealed that the taxpayer hired the law firm for tax

planning. This was accomplished by establishing foreign accounts and entities,

and executing subsequent transactions relating to said foreign accounts and

entities. Specifically, from 1995 to 2009, the taxpayer engaged the law firm to

form eight offshore entities in the Isle of Man and in the British Virgin

Islands and established at least five offshore accounts, so the taxpayer could

assign income to them and, thus, avoid US income tax on the earnings.

The case is interesting, but it reflects that enablers’

secrecy tools won’t be easy to dismantle. This ruling doesn’t suggest at all that the IRS can send fishing

expeditions to any law firm to find tax abusers. Instead, it appears that the

fact that there was a possibility – but not certainty – that these (unknown) US

clients had violated tax regulations is what allowed the IRS to overcome

attorney-client privilege.

Lawsuits require judges to interpret and apply the law to one

particular case. But we should take a step back and ask ourselves whether the

law itself makes sense, or if it needs to be reconsidered.

As we have recently written in an earlier

blog on this case, attorney-client privilege is just the tip of the iceberg

in facilitating illicit financial flows. Attorney-client privilege is abused not

just for tax abuse purposes, but for money laundering as well, as warned by the

Financial

Action Task Force.

Today we are delighted to support the launch of a new and critically important website: ‘a volunteer online data repository of information on feminist principles and actions, as well as policy responses to the COVID crisis.’

After the 64th UN Commission on the Status of Women in March 2020 was cancelled, feminists came together within days to share, support and to continue strategic work that couldn’t wait. They worked ‘across global movements centered on human rights, sustainable development, and economic and social justice’ to launch this vital resource. As Emilia Reyes and Bridget Burns explain in introducing it, “Working at the intersections of multiple forms of crisis is not a new task for feminist advocates”.

The new website provides a set of principles to outline a feminist response to COVID 19, which involves a ‘paradigm shift’ – a different financial model – that relies ‘on adequate and equitable financing.’

You’ll also find on the Feminist Covid Response website:

Response Tracker. This marks policies or laws, temporary measures, or observed responses by country and by theme (for example, education).

Online Dialogues. This is a repository of online dialogues and webinars that have been held to discuss the intersections of gender, feminism, care, women’s rights and COVID-19.

Resources. This section contains a collection of feminist statements and analyses, mutual aid resources and organising tools.

This is an important opportunity to map the impact of COVID 19 and to ensure feminist solutions prevent a return to ‘business as usual’ once the crisis is perceived to be ‘over’, so please contribute with your own resources on tax justice, your experiences and your responses to COVID 19. This video below from the Womens Budget Group in the UK demonstrates how different elements of gender inequality are connected, and how unpaid care lies at the centre of this spiral. The experience of the pandemic is highlighting how deeply unequal women and girls are worldwide and we must now ensure these brutal lessons result in good policy.

We congratulate and are grateful to the twenty five volunteers from across the world who have worked so hard to publish this website. Please share widely, social media hashtags are #FeministResponse #COVID19

Here’s the 15th edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa by finance journalist Idriss Linge in Cameroon. Nous sommes fiers de partager avec vous cette nouvelle émission de radio/podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

IMPOTS ET JUSTICE SOCIALE #15 : L’aide hypocrite du G20 à l’Afrique face au Coronavirus

Dans cette quinzième édition de votre podcast « Impôts et Justice Sociale » nous revenons sur le Coronavirus, et les actions en faveur de la justice sociale au profit de l’Afrique et des Africains. De nombreux gouvernement ont pris des mesures pour limiter les conséquences économiques sur les personnes actives. Mais ces mesures reposent sur de faibles moyens et ne parviennent pas à toucher tout le monde.

Aussi, les pays riches du G20, dont plusieurs sont des paradis fiscaux ou des experts des stratégies agressives pour obtenir des avantages fiscaux avantageux, ont annoncé de grandes mesures d’aide à l’Afrique, mais il n’en est rien, Au contraire, le continent noir risque de payer plus cher cette suspension du service de la dette.

Pour en parler

Ali Idrissa, il est basé au Niger, où il occupe les fonctions de Coordonnateur du ROTAB (Réseau des organisations pour la transparence et l’analyse budgétaire)

Broulaye Bagayoko, qui est basé au Mali. Il est le Secrétaire Permanent du CADTM Afrique / Comité pour l’abolition des dettes illégitimes

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le lien suivant

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to the twenty-eighth edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to post it. You can also join the programme on Facebook and on Twitter.

In the 28th edition of Taxes Simply: can the accumulated wealth in tax havens be taxed in order to mitigate the economic and health crisis that the world is facing?

In the second part of the programme, we present our summary of the most important tax and economic news from around the world, including:

Denmark says it won’t consider companies registered in tax havens for bailouts

The Netherlands disrupts European solidarity in facing the coronavirus – twice

The IMF urges Kuwait to increase taxes and reduce its dependence on oil

Prices for US oil contracts go negative due to lack of demand

أهلا بكم في العدد الثامن والعشرين من الجباية ببساطة. نتناول في هذا العدد مشكلة الملاذات الضريبية، وهل يمكن إخضاع الثروات المتراكمة هناك للضريبة من أجل التخفيف من حدة الأزمة الاقتصادية والصحية التي يعيشها العالم حاليا. في الجزء الثاني من البرنامج نعرض كالعادة ملخص لأهم أخبار الضرائب والاقتصاد من حول العالم، ويشمل ملخص الأخبار: ١) الدنمارك لن تدعم الشركات المسجلة في ملاذات ضريبية؛ ٢) هولندا تعطل التضامن الأوروبي في مواجهة كورونا مرتين؛ ٣) صندوق النقد الدولي يحث الكويت على زيادة الضرائب وخفض الاعتماد على النفط؛ ٤) عقود مايو/آيار للنفط الأمريكي تصل سعرها إلى سالب في ظل نقص الطلب على الوقود الأحفوري.

Quais são os rumos para a sociedade global, vencida a pandemia? Como não repetir erros de outras crises e apostar em novos paradigmas? Estas reflexões são feitas por uma diversidade de economistas: Laura Carvalho, Pedro Rossi, Áurea Mouzinho, Marco Antonio Rocha, Inocência Mapisse, Thomaz Jensen, Marilane Teixeira, Guilherme Mello e também pelo nosso colunista, o jornalista Nick Shaxson.

Nossos entrevistados contemplam que após a pandemia é possível o ressurgimento de Estados mais fortes, focados em investimentos públicos em saúde e proteção social; uma economia baseada em cuidados, no papel das mulheres e no consumo consciente; um mercado de trabalho mais inclusivo e a reinvenção de movimentos de trabalhadores; e, sobretudo, a ascendência da solidariedade e do coletivo como alicerces de uma sociedade global mais ambientalmente sustentável. E o dinheiro para financiar a nova economia pode vir com a aplicação de medidas como um maior controle dos fluxos financeiros de paraísos fiscais e um sistema tributário mais progressivo.

E uma novidade: completamos um ano de podcast e o presente para todos os ouvintes é um site novo. Em www.edasuaconta.com você tem acesso a todos os episódios do podcast e a todas as plataformas digitais de áudio. Confira!

Participantes desta edição:

Pedro Rossi, professor do Instituto de Economia da Unicamp

Nick Shaxson, colunista do É da sua conta, jornalista da Tax Justice Network

How UK civil servants tailored US anti-money laundering policies to suit Britain’s financial services industry…

Amid the global crisis emanating from the spread of Covid-19, those of us who advocate for tax justice have seen our objectives sharpened as the already huge gulf between the living standards of the “poor” and the “rich” seemingly widens every day. The fight for tax equality concomitant with the wider notion of equality in terms of access to public services (including healthcare) for everyone has never been more pressing. As already noted by the Tax Justice Network and its contributors, the coronavirus pandemic is shining a light on the wealthy fat cats who are shoring up money in secrecy jurisdictions while asking for bailouts and the devastating impact of tax avoidance on EU states, including the effects on public services spending.

But the voices of tax advocates will not be silenced. As stated by Nick Shaxson, while some “Important People” may think that “our ideas were utopian, even crazy” the reality is that in the post Covid-19 world, the likes of the UK’s Chancellor, Rishi Sunak, and others who hold the budgetary keys in OECD countries, will need to sit up and take notice of the need to rewrite national tax laws and thereby help to undermine the financial bases of criminal organisations and also those businesses operating at the murky end of legitimacy – rather than rejecting calls to bar tax haven companies from bailouts. Bureaucratic law makers should not be able to draft legislation in a way that benefits the wealthiest (whether professional criminal entrepreneur or savvy tax avoider), while demonising those whose lives are enveloped by persistent financial hardship. Laws which undermine genuine law enforcement concerns to tackle crime, corruption and inequality. Laws which continue to support the threats posed by financial secrecy jurisdiction to the world’s poorest countries. Laws, which when all is said and done, allow criminogenic environments to flourish with the support of the British government.

Along with Dr Michael Woodiwiss (History, University of the West of England), we have this week published an article with the journal Trends in Organized Crime, on anti-money laundering law-making by some of the policy makers operating in Whitehall and Threadneedle Street in the late 1980s. Our research focused on the retrieval and analysis of a substantial, previously secret, UK Treasury file from 1987, which contains the letter writing correspondence between Thatcherites based at Whitehall and Threadneedle Street at a time when the UK felt under pressure to conform to US policies emanating from the “war on drugs”. Correspondence evidences the ways in which the UK and US were able to quietly manipulate anti-money laundering policies to suit the economic priorities of the banking and finance sectors on both sides of the Atlantic; for example flatly rejecting calls for increased vetting of bank customers, retaining secrecy jurisdictions as prominent financial centres, and shooing away the efforts of Interpol to highlight financial crime in the banking sector. Simply put, the existing international anti-money laundering framework – which, let’s not forget, generally falls under the heading of criminal law, given the crimes it covers – has been created and developed by bankers and Treasury civil servants, with minimal input from law enforcement. Some such as Rachel Lomax (who later became Deputy Governor of the Bank of England), Graham Kentfield (who later worked as the Chief Cashier at the Bank of England), and Colin Gregory (promoted to Deputy Director, Government Legal Department) progressed to work in high profile positions within the banking sector and government.