Illicit money flows are notoriously hard to track. According to a 2011 report from the UN Office on Drugs and Crime, less than 1 per cent of proceeds from criminal activity that are laundered via the financial system are detected. In efforts to overcome this, authorities have tried to improve customer due diligence requirements, increased transparency around legal vehicles, and engaged in automatic exchange of bank account information to prevent money laundering.

However, existing mechanisms still have several loopholes and are not sufficient to effectively map and counter illicit financial flows. For instance, financial account information that is exchanged based on the US Foreign Account Tax Compliance Act or the OECD’s Common Reporting Standard can only be used for tax purposes and might not be useful in detecting other financial crimes. Additionally, the automatic exchange of information only covers data on annual income and account balances, which can easily be manipulated and does not enable investigations of individual transactions.

The fight against money laundering requires law enforcement agencies to “follow the money”, and, as we have argued, financial transaction data could be a game changer for this. A new study, published by researchers from the Tax Justice Network (as part of the TRACE consortium), investigates the potential, shortcomings, reform options, and prevalence of the use of the SWIFT financial messaging data in countering illicit financial flows among European law enforcement agencies.

The central role of SWIFT for countering financial crimes

The Society of Worldwide Interbank Financial Telecommunications (usually simply referred to as SWIFT) is an association which, among other things, is responsible for providing a global messaging system of financial information. In 2021, over 11,000 institutions participated in the SWIFT network, and more than 10 billion messages relating to financial transactions were sent through this system1.

The interest in accessing SWIFT data for detecting and combatting risks of illicit financial flows is not new. The Financial Action Task Force has sought access to SWIFT data since the 1990s, but SWIFT resisted. Despite this, authorities around the world have gained some access to SWIFT data. The US used SWIFT data in its Terrorist Finance Tracking Program to map out terrorist networks, and the US, EU, and UK expelled some Russian banks from the SWIFT network in 2022 to enforce economic sanctions against Russia. Researchers have also used SWIFT data to estimate capital fleeing Ecuador, and to study the impact of anti-money laundering regulation on payment flows.

SWIFT data can be useful in financial investigations and supervision in two ways. First, law enforcement agencies could access batches of SWIFT transactions for specific cases they are investigating, to trace specific transactions. Second, broad access to SWIFT data could enable advanced analytics to identify suspicious transaction patterns, develop risk algorithms, and guide policy analyses. This could be done through financial intelligence units or anti-money laundering supervisory bodies in the financial sector.

Our new report suggests, however, that SWIFT data is currently not, or very seldom, directly used by law enforcement agencies and financial intelligence units in the European Union, due to obstacles such as low-quality data, data compatibility, the need for technical expertise to analyse data, and the incompleteness of data. Despite this, the report concludes that authorities would find access to SWIFT data useful for both preventive analytics and investigations.

Concerns related to the incompleteness and quality of the data, especially relating to the capacity to match financial transactions to specific individuals, call to attention a need to strengthen the messaging standards and the institutional frameworks that govern money transfers, both at the regional and international level.

Governing financial messaging: International standards, legal frameworks and their loopholes

In 2012 the Financial Action Task Force introduced the travel rule, which requires some information on the originators and beneficiaries of payments to be carried through the entire payment chain. The rule’s objective is to make basic information available to law enforcement, financial intelligence units and financial institutions, to facilitate criminal investigations and the analysis, identification, and reporting of suspicious transactions. At its heart, the travel rule aims to create an audit trail, allowing for information about where a payment came from to “travel” through the payment chain along with the payment. These rules do not directly apply to the SWIFT organisation providing the messaging system, but to the financial institutions handling the wire transfers and payments, and who in turn own and operate the SWIFT organisation and system.

The European Union incorporated the travel rule into law by means of the Regulation on Transfer of Funds in 2015. Since July 2021, the EU has been discussing a revision of the regulation as part of its 6th anti-money laundering package. That revision’s main aim was to bring crypto transfers into the scope of the regulation.

Our report shows that both the Financial Action Task Force recommendation 16 and the European Union version of the travel rule have severe shortcomings from the perspective of an ideal and consistent transparency framework for financial transactions. For example, the inclusion of beneficial ownership information on payers or payees is required under neither the Financial Action Task Force recommendations nor under European transfer of funds regulations. In this regard, the data on the originators and beneficiaries of payments can refer only to a legal entity, and not to the individual who is benefiting from it. Furthermore, consistent, structured and unique identifier information about relevant legal or natural persons would not always be required under either of the rules, evidencing important weaknesses of both the travel rule and the European regulation.

The regulation on the transfer of funds has an additional weakness in both its original and revised formats with regard to intra-EU transfers. While the Financial Action Task Force travel rule mandates the inclusion of a name for both the payer and payee, the European Union does not require this information for transfers within the European Union. Additionally, the EU falls short of always requiring the inclusion of additional personal identification information, such as address or birthdate, for the payer. Intra-EU transfers only require account numbers for the respective parties, with the remaining information being provided on request within three working days.

Furthermore, the 2021 proposed recast of the European regulation on the transfer of funds may remove the mandatory inclusion of all the identification criteria of the payers of bank transfers. The listing of criteria now omits the word “and” in article 4.1, which previously clarified that all three identifying attributes (1. name, 2. account number, and 3. address including name of country; official personal document number; and customer identification number, or alternatively, date and place of birth) needed to be included in a transfer message. The removal of the word “and” in articles 4.1 and 4.2 may lead to some ambiguity about whether to include all identifying criteria – or if only one is sufficient. We believe that this potential ambiguity is likely to be addressed and removed through a further revision of the proposed rewording of the transfer of funds regulation which is set to be voted on in April 2023.

Compared to already weak Financial Action Task Force and European regulations, the SWIFT messaging format is even weaker, with no consistent, uniform or mandatory data structure, and dispensing with hard-wired, coded, and mandatory information to be included about both the paying and beneficiary customers. This is a key shortcoming of the SWIFT messaging format, since the lack of consistency makes data matching and mining extremely challenging, hindering efforts by law enforcement agencies to detect, address and prevent illicit financial flows. As a consequence, enforcement agencies may need to rely on financial institutions to provide the requested transactions in manually collated excel files that have been extracted from the original SWIFT transaction records, creating a series of risks, including everything from simple errors in copying and transposition, to the potential manipulation of evidence.

Anticipated developments

Effective standards governing financial messaging systems are a crucial though sometimes overlooked element in combating illicit financial flows. However, there is growing recognition of the importance of this issue. The G20 Finance Ministers and Central Bank Governors Meeting of February 2023 in Bengaluru, India, included a reference to the “travel rule” in their final communique:

“We recognise the urgent need to establish effective anti-money laundering and counter-terrorism financing regulations and oversight of virtual assets, especially to prevent their use in money laundering and terrorism financing, in line with FATF Standards. We support the FATF’s efforts to speed up the implementation internationally of its standards for this sector and recommit to timely implementation of these rules, including the ‘travel rule’.”

While the travel rule is mentioned here in the context of money laundering risks relating to virtual or crypto assets, its mention in such a high-level policy document underlines its global and systemic relevance for countering illicit financial flows.

Another key future development is that, by 2025, SWIFT will have been phased out and replaced by a new financial messaging standard called ISO 20022, which opens a golden opportunity for reforming the global financial payment infrastructure to be better equipped to counter illicit financial flows. While the format appears to be much more structured, only global political standard setters like the United Nations, the G20, the Financial Action Task Force and/or the EU, will be able to decisively influence the suite of mandatory information to accompany transfers of funds in the decades to come. India’s chairing of the G20 could prove decisive in strengthening the minimal transparency requirements for legitimate cross-border financial transactions.

Recommendations

The main recommendations from the report include:

Requiring the mandatory inclusion of beneficial ownership data in transaction records for both the ordering and beneficiary customers.

Preventing the execution of any wire transfers if the identification and verification of the bank’s customers and their beneficial owners have not been fully completed.

Removing any exceptions and ambiguity about the necessity of including multiple identifiers on payers and payees, especially in the current recast of the EU transfer of funds regulation.

Treating all cross-border transfers equally irrespective of regional economic integration.

To enhance data quality and consistency, SWIFT should hard-code basic data requirements for customers in their message standards and ensure that only structured data is allowed in message fields.

Additionally, SWIFT should develop and monitor a data validation standard for all banks using the network.

Lastly, jurisdictions should centralise data on all transactions through a domestic institution.

In conclusion, the report highlights that the SWIFT message data is currently not being effectively utilised by law enforcement agencies and suggests a need for significant reform in the SWIFT message format and regulatory framework. This would enable far more successful investigations of financial crimes by revealing networks and connections that would otherwise remain invisible.

La falta de transparencia en la titularidad de empresas, fideicomisos, sociedades y fundaciones es un importante impulsor de los flujos financieros ilícitos. Esta opacidad tiene consecuencias negativas en las economías y sociedades de todo el mundo, lo que resulta en una mayor inestabilidad financiera, desigualdad, y erosión de la confianza en las instituciones, en el estado de derecho y en la democracia. En colaboración con Tax Justice Network Africa y Fundación SES, Tax Justice Network publica hoy dos informes sobre el estado actual de la transparencia de beneficiarios finales en África y América Latina. La transparencia de los beneficiarios finales requiere la divulgación pública de las personas que en última instancia poseen, controlan o se benefician de un vehículo legal, como una empresa. Nuestros dos informes se basan en datos del Índice de Secreto Financiero 2022 de Tax Justice Network, cubren los últimos desarrollos y avances, y profundizan en la situación de países específicos a través de estudios de casos. A continuación, se presenta un breve resumen:

Transparencia de beneficiarios finales en África y América Latina

Los gobiernos africanos y latinoamericanos son conscientes de que la transparencia de los beneficiarios finales es una herramienta poderosa para combatir el lavado de dinero y el abuso fiscal. Nuestra investigación demuestra que se están realizando progresos en ambos continentes.

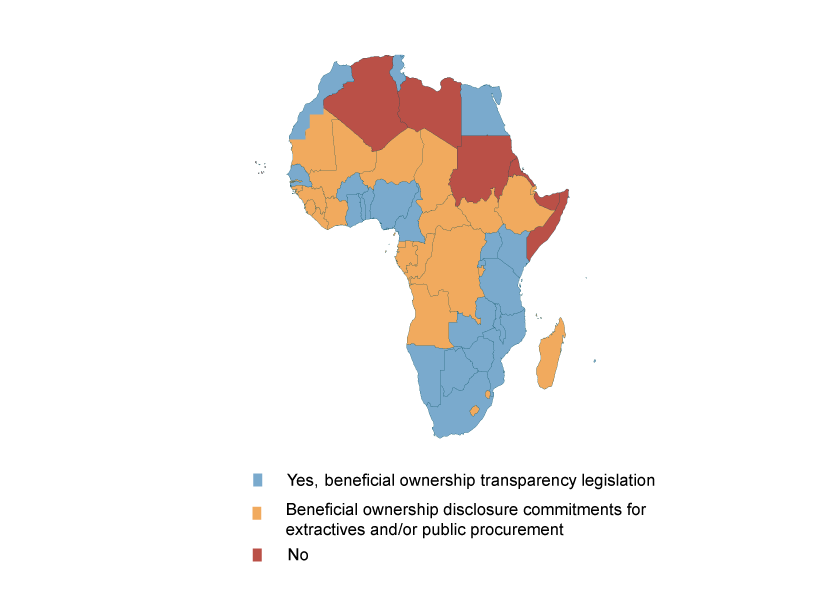

En África, 23 de las 54 jurisdicciones han implementado leyes que exigen que los beneficiarios finales de las empresas sean declarados o registrados ante una autoridad gubernamental. Nuestro informe Transparencia de beneficiarios finales en África en 2022 incluye casos reales que ilustran los perjuicios que causa el secreto financiero. En Camerún, por ejemplo, la malversación de fondos públicos destinados a responder al Covid-19 generó un debate entre la sociedad civil, los medios de comunicación y las autoridades públicas. Uno de los casos de fraude involucró a familiares del comité gubernamental responsable de las adquisiciones. Desde entonces, el país ha reconocido la necesidad de beneficiarios finales en su Ley de Finanzas de 2023, que exige que las personas jurídicas registren a sus beneficiarios finales ante una autoridad pública.

En América Latina, 10 de las 16 jurisdicciones analizadas requieren que la información sobre los beneficiarios finales sea registrada ante una autoridad gubernamental, lo que representa un aumento significativo desde 2018, cuando solo cuatro jurisdicciones lo requerían. El informe sobre “El estado actual de los registros de beneficiarios finales en América Latina” incluye una sección que explica cómo se pueden fortalecer aún más los marcos institucionales nacionales a través de estudios de casos.

A pesar de los avances, siguen existiendo importantes lagunas. Las acciones al portador, que son acciones representadas por certificados físicos que otorgan la titularidad a quien las posee, representan un riesgo significativo para la transparencia. Recomendamos que los países prohíban el uso de acciones al portador y eliminen gradualmente las restantes. La falta de acceso público a los registros también es una gran debilidad.

Los estudios también revelan los compromisos de los gobiernos con la transparencia de los beneficiarios finales en sectores específicos. Algunos países se han comprometido a divulgar información sobre beneficiarios finales para las empresas de las industrias extractivas como parte de la Iniciativa de transparencia de la industria extractiva. También se han hecho compromisos similares para aumentar la transparencia y la rendición de cuentas en la adquisición de bienes y servicios durante la pandemia, cuando varios países se comprometieron a publicar los beneficiarios finales de las empresas adjudicatarias de contratos gubernamentales como parte del acceso a la financiación del Fondo Monetario Internacional.

El camino a seguir

El progreso en la transparencia de los beneficiarios finales varía ampliamente entre países y regiones. Incluso en aquellos países que han implementado marcos sólidos, existen lagunas que pueden ser explotadas. Por ejemplo, la legislación debe cubrir todas las entidades legales (no solo las empresas, sino también asociaciones, fideicomisos y fundaciones). Una definición clara y completa de quién califica como beneficiario final y métodos eficientes para mantener esta información actualizada también son componentes cruciales para establecer un sistema sólido para la transparencia de los beneficiarios finales. Además, en el caso de incumplimiento de estos requisitos, son necesarias consecuencias y la aplicación de sanciones para impedir el abuso.

Cualquier progreso en la transparencia que un país haga siempre corre el riesgo de ser socavado por la opacidad en otros países. Es importante destacar la gran responsabilidad que tienen algunas de las principales economías del mundo para mejorar sus propios marcos. El sur global enfrenta enormes desafíos para responsabilizar a sus elites, dado que estos importantes actores internacionales les brindan ayuda y les permiten evadir el estado de derecho en sus países de origen. Los países de bajos ingresos son las principales víctimas del sistema extraterritorial mundial y sufren de manera desproporcionada los flujos financieros ilícitos. Si bien en gran medida no son responsables de permitir estos flujos, los acontecimientos recientes muestran que los países de bajos ingresos necesitan importantes actores internacionales para brindar transparencia, pero no pueden confiar en que lo hagan. Si bien Estados Unidos presentó recientemente una ley que regula la transparencia de los beneficiarios finales, el progreso logrado a través de la Ley de Transparencia Corporativa en 2021 es insuficiente. Por otro lado, la Unión Europea, que anteriormente tenía un régimen de transparencia relativamente avanzado, dio un gran paso atrás con un fallo judicial a fines del año pasado que aceptó el argumento de que la transparencia de los beneficiarios finales viola la privacidad personal. Este fallo llevó a los países a restringir el acceso a sus registros en cuestión de horas. Este revés destaca la necesidad de que los países del sur global implementen sus propias medidas de transparencia de manera unilateral para protegerse en la medida de lo posible de los daños del secreto financiero.

Para ayudar a los países a lograr una transparencia óptima, Tax Justice Network ha publicado una hoja de ruta que describe los pasos hacia las mejores prácticas para la implementación de registros de beneficiario.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast. (All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here.)

En este programa con Marcelo Justo y Marta Nuñez:

El reino de los narcobanqueros en Ecuador: tambalea el gobierno de Guillermo Lasso

América Latina, la necesidad de un nuevo modelo y un pacto fiscal en entrevista con la CEPAL

La reforma impositiva de Gustavo Petro en Colombia y la pequeña y mediana industria

El debate sobre la moneda alternativa al dólar para los intercambios de América Latina

Invitadxs:

Andrés Arauz, economista y ex candidato a la presidencia ecuatoriana

Daniel Titelman, director de la división de desarrollo económico de la Comisión Económica para América Latina (CEPAL)

Oscar Ugarteche, Director del Observatorio Global Latinoamericano, OBELA, profesor de la Universidad Nacional Autonoma de Mexico, y autor de Historia Critica del FMI

~ Narcobanqueros, la reforma impositiva Colombiana, moneda alternativa

Welcome to the 63rd edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here.

في العدد #63 من بودكاست الجباية ببساطة استضاف وليد بن رحومة الباحثة مزن النيل لمناقشة ورقة بحثية بعنوان “السياسة اليومية للنظام الضريبي في السودان: تحديد ٱفاق الإصلاح” المنشورة ضمن مجموعة الصراع والمدنية البحثية التابعة لجامعة LSE بالمملكة المتحدة بالتعاون مع ماثيو بنسون ورجاء مكاوي. وتحدثت مزن النيل عن قصور النظام الضريبي السوداني في توزيع الثروة بشكل عادل سواء بين الأفراد أو الجهات زيادة على إعتماد الإقتصاد السوداني على الأنشطة الريعية دون إدماج لمختلف الفئات في العملية الإنتاجية.

In episode #63 of Taxes Simply podcast, Walid Ben Rhouma hosts researcher Muzan Al-Nil to discuss her recently published paper entitled “The Everyday Politics of Sudan’s Tax System: Identifying Prospects for Reform,” published within the Conflict and Civility Research Group of LSE University in the United Kingdom, in collaboration with Matthew Benson and Rajaa Makkawi. Muzan discusses the failure of the Sudanese tax system in distributing wealth fairly, and the dependence of the Sudanese economy on rentier activities.

~ السودان: سياسة الولاءات وتركيز الثروات عبر الضرائب

Secrecy surrounding ownership of companies, trusts, partnerships and foundations is a major driver of illicit financial flows. The negative consequences of this secrecy are felt across economies and societies worldwide and result in greater financial instability, increased inequality, and erosion of public trust in institutions, the rule of law and democracy. In collaboration with Tax Justice Network Africa and Fundación SES, the Tax Justice Network today publishes two reports on the state of play of beneficial ownership transparency in Africa and Latin America. Beneficial ownership transparency requires the disclosure of the individuals who ultimately own, control or benefit from a legal vehicle, such as a company. This data should be publicly available, free of charge. Our two reports draw on data from the Tax Justice Network’s Financial Secrecy Index 2022, cover some of the latest developments and progress, and dig deeper into the situation in specific countries through case studies. Here is a brief summary:

Beneficial ownership transparency in Africa and Latin America

African and Latin American governments know that beneficial ownership transparency is a powerful tool to combat money laundering and tax abuse. Our research shows that progress is being made on both continents.

In Africa, 23 out of 54 jurisdictions now have laws that require beneficial owners of companies to be declared or registered with a government authority. Our report Beneficial ownership transparency in Africa in 2022 includes real life cases of the damage financial secrecy causes. In Cameroon, for example, the misappropriation of public funds meant for responding to Covid 19 sparked debate among civil society, the media, and public authorities. One of the cases of fraud involved family members of the governmental committee responsible for procurement. Since then, the country has recognised the need for beneficial ownership in its Finance Act of 2023, requiring legal entities to register their beneficial owners with a public authority.

In Latin America, 10 out of the 16 jurisdictions analysed require beneficial ownership information to be registered with a government authority, a significant increase since 2018 when only four jurisdictions mandated this requirement. The report on the State of Play of Beneficial Ownership in Latin America includes a section explaining how national institutional frameworks can be strengthened further through case studies.

Despite progress, significant loopholes remain. Bearer shares, which are shares represented by physical certificates that grant ownership to whoever holds them, pose a significant risk to transparency. We strongly recommend that countries prohibit the use of bearer shares and phase out the remaining ones. The lack of public access to registries is also a major weakness.

The studies also reveal governments’ commitments to beneficial ownership transparency in specific sectors. Some countries have committed to disclosing beneficial ownership information for companies in the extractive industries as part of the Extractive Industry Transparency Initiative. Similar commitments have also been made to increase transparency and accountability in the procurement of goods and services during the pandemic, when several countries pledged to publish beneficial owners of companies awarded government contracts as part of accessing financing from the International Monetary Fund.

The way forward

Progress on beneficial ownership transparency varies widely across different countries and regions. Even in countries that have implemented strong frameworks, loopholes remain that can be exploited. For example, legislation should cover all legal entities (not just companies, but also partnerships, trusts and foundations). A clear and comprehensive definition of who qualifies as a beneficial owner and efficient methods for keeping this information up to date are also crucial components of establishing a strong system for transparency of beneficial ownership. In addition, consequences and enforcement of sanctions for noncompliance with these requirements are necessary to deter abuse.

Any transparency progress a country makes is always at risk of being undermined by secrecy in another country. It’s important to highlight here the great responsibilities on the part of some of the world’s major economies to do better. Given the help that these major international players provide in enabling elites in other countries to escape the rule of law in their home countries, the global south is faced with huge challenges in holding them all accountable. They are the primary victims of the global offshore system, suffering disproportionately from illicit financial flows. While they are largely not responsible for enabling these flows, recent developments show that lower income countries need major international players to deliver transparency but certainly cannot rely on them doing so. The US only very recently brought forward a law regulating beneficial ownership transparency, and even then, the progress made through the Corporate Transparency Act in 2021 is very weak. Meanwhile, the European Union, which previously had a relatively advanced transparency regime, has taken a major step back with a court ruling late last year that accepted the argument that beneficial ownership transparency violates personal privacy. This ruling led to countries restricting access to their registries within hours. This setback highlights the need for countries in the global south to implement their own transparency measures unilaterally to protect themselves as far as they can from the harms of financial secrecy.

To support countries in achieving optimal transparency, the Tax Justice Network has published a roadmap that outlines steps towards best practice for the implementation of publicly accessible beneficial ownership registers.

In the wake of the Covid-19 pandemic, the International Monetary Fund lent and gave money to governments to help save as many lives as possible. Governments bought equipment, drugs and test kits. Knowing that public procurement can be a hotbed for collusion and corruption in all countries, the International Monetary Fund asked governments to make special governance commitments. In Africa, 34 governments committed to register and disclose the real people behind companies awarded contracts.

Nevertheless, money meant for saving people had a funny way of growing legs in many places during the pandemic. Commitments to transparency may not have been put into practice or done so in time or effectively, given the ‘Covidgates’ that sprung up across the world – from Brazil to Malawi.

Cameroon’s ‘Covidgate’ sheds light on the problem of anonymous company ownership. In 2020, the government set up a Special National Solidarity Fund to finance the health sector to protect Cameroonians from the coronavirus. But social media users soon started to leak information about embezzlement and fraud involving the solidarity fund. The press picked these up, and President Paul Biya called for an investigation.

With over 120,000 recorded Covid-19 cases, the Audit Bench of the Supreme Court of Cameroon revealed serious problems with the procurement process for equipment and drugs needed to help Covid-19 patients. Irregularities resulted in inflated prices for Covid-19 test kits and stocks of drugs disappearing.

In many cases, the information about the real owners of companies that won government contracts was “uncertain”. The Ministry of Health had set up a working group to oversee procurement. The president of this group was Ousmane Diaby, who also headed a division in the ministry. According to the Audit Bench’s audit, companies owned by Diaby won contracts.

It turned out that Diaby and his younger brother owned MG & Company, yet they managed to hide behind the manager. The company received nearly US $5 million, but there was very little work to show for it. This situation “is likely to be classified as a criminal offence”, according to the Audit Bench.

Spreading the spoils among family members didn’t stop there. The working group also awarded six contracts to three companies managed by Diaby’s older brother. Diaby did not notify the working group of the relationship. Here, the Audit Bench stressed that there is a “high risk of criminal liability associated with the award of these contracts”.

Despite the audit, there have been no sanctions or actions taken so far. Cameroon’s commitments on beneficial ownership transparency to the International Monetary Fund were a step in the right direction. Yet they appear not to have been put in practice in time or effectively, based on the Audit Bench’s findings.

Cameroon has taken further action on beneficial ownership transparency since then though. The new Finance Law of 2023 requires the beneficial owners of legal entities to register with the tax authority. This is an essential tool in addressing government procurement fraud which ultimately robs people of good healthcare.

Africa’s commitment to transparency

Cameroon is not alone in introducing laws for beneficial ownership transparency. At the start of 2023, 23 of 54 African nations required the human beings behind companies to register with a government authority.

More than half of the continent has specific commitments for sectors prone to risk: the extractive industries and public procurement. Governments in 28 African countries committed to disclose and make public the beneficial owners of companies in mining, oil and gas as part of the Extractive Industries Transparency Initiative. This is important as people can hide behind opaque and complex company structures to win rights to extract Africa’s precious, finite resources. In many countries, commitments to beneficial ownership transparency first made in the extractive industries have also sparked the introduction of laws for all companies in every sector.

Beneficial ownership transparency in Africa in 2023 (as of January 2023)

Botswana, Egypt, Ghana, Kenya, Mauritius, and Tunisia require the beneficial owners of companies to register with a government authority and companies must notify authorities of any changes. What sets Botswana apart is that every single beneficial owner of a company must register. There is no threshold of ownership share below which a person becomes exempt. In contrast, Kenya, for example, has a threshold of 10 per cent. Hypothetically, this means that someone could set up a company with equal division of shares or voting rights between 11 people and not one of them would need to register, since individually the people would not meet the 10 per cent threshold.

The route to effective beneficial ownership transparency

In the extractive industries and public procurement in response to the Covid-19 pandemic, African citizens, journalists and law enforcement agencies have the best access to data. And, of course, the best data is not worth much if law enforcement agencies do not have the political space to act against wayward companies. Still, loopholes in beneficial ownership registration laws remain, which unscrupulous actors can exploit.

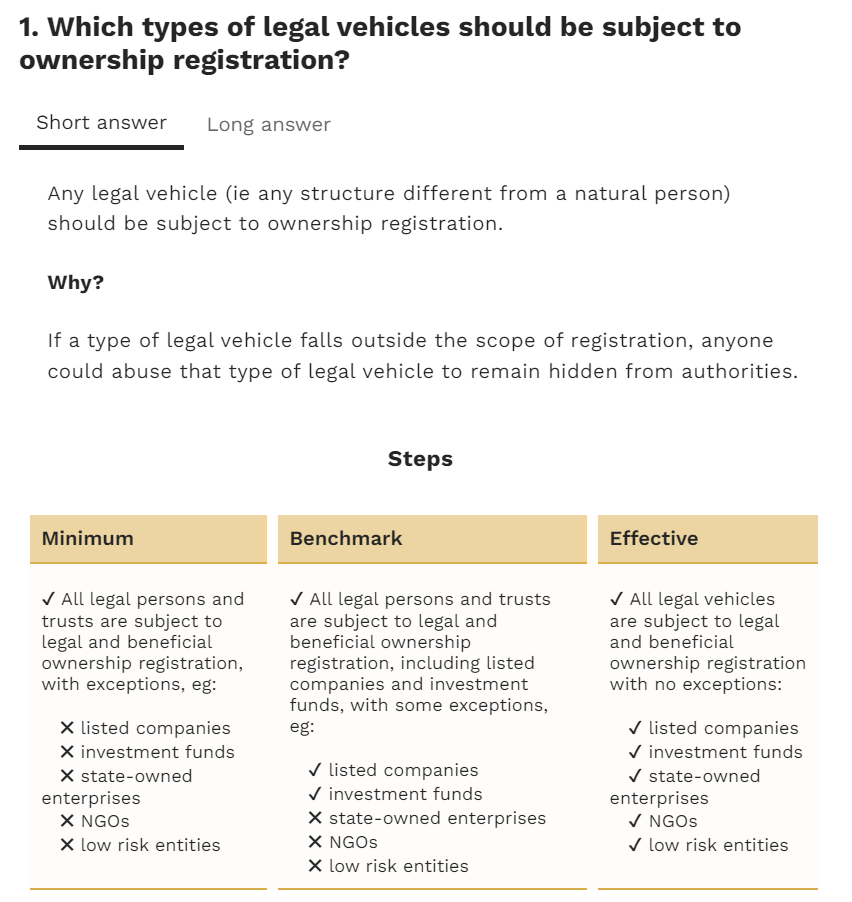

The Tax Justice Network has laid out its vision for effective beneficial ownership transparency in a Roadmap to Effective Beneficial Ownership Transparency. This is a blueprint for policy makers and citizens seeking to change legal frameworks. The roadmap sets out 10 targets that countries’ beneficial ownership frameworks should meet.

Scope. All legal vehicles should be subject to beneficial ownership registration requirements. This means any entity that is not a living and breathing person should disclose the natural person who owns, controls or benefits from it.

Definition of legal owners. All legal owners should register. This includes all who have a title or any direct interest in the legal vehicle.

Definition of beneficial owners.All beneficial owners should register. This includes any natural person who in any way owns, controls, or benefits from a legal vehicle.

Triggers for registration.All legal vehicles should be required to register beneficial ownership information if they seek to incorporate domestically, possess domestic assets, conduct domestic operations or have a domestic participant (eg a domestic legal owner, beneficial owner, settlor, director, etc).

Identification information for all owners. Legal vehicles should be required to provide all identification details about both legal and beneficial owners to ensure there is no confusion of identity. This includes full name, place and date of birth, address, national ID number, tax ID number, and nature of ownership. This also allows for special checks (eg status as a politically exposed person). Legal vehicles should also be required to disclose the full ownership or control chain (all intermediate layers). This illustrates how each beneficial owner benefits or has ownership or control over the legal vehicle.

Keeping information up to date. Legal and beneficial ownership registries should be updated annually, even if it’s just to confirm there were no changes, as well as updated when there is any change in the relevant information.

Access to information. Legal and beneficial ownership data should be available to the public for free. Ownership registries should be available online in open data format.

Verification of information. Beneficial ownership registries should automatically analyse data against other databases to check for consistency. For example, to confirm that all registered beneficial owners are alive. The online registry should introduce red flagging based on outliers and suspicious characteristics, such as a single person as a beneficial owner of thousands of companies.

Sanctions for non-compliance. Criminal and monetary sanctions are important alongside administrative sanctions. Administrative sanctions include removing non-complying legal vehicles from the registry and revoking any rights from non-complying beneficial owners (eg votes or dividends).

Special considerations. Countries should prohibit bearer shares, discretionary trusts and nominees. They should discourage complex ownership chains. Equally, countries should cover state-owned companies as well as listed companies and investment funds by applying even lower thresholds. In ideally, all countries should interconnect beneficial ownership registries with each other and with asset registries.

As the world commemorates this International Women’s Day, the Global Alliance for Tax Justice (GATJ) stands in solidarity with women’s rights organisations, movements, academics and activists, bringing the perspectives and contributions of the economic justice movement to advance the gender justice agenda. We are at a critical point in which a dangerous combination of fiscal policy and political choices continues to benefit a small yet exceedingly influential elite, increasing inequalities. Across the world, it is women who disproportionately bear the brunt of these fiscal policy failures through several layers of injustice.

In this scenario, GATJ invited eight women, who are members and allies of its Tax and Gender Working Group (TGWG), to reflect on the importance to call attention to the tax justice agenda as we commemorate the IWD, and how the demands for tax justice relate to women’s historical and present struggles for rights.

“Fiscal policy is shaped by the fallacy that revenue generated from monetized productive work within the market economy is mutually exclusive from women’s unpaid social reproductive work performed in the domestic sphere. And yet without the latter, the revenue from paid work with which macroeconomic policy preoccupies itself would suffer. This structuring of socio-economic relations has been a source of deep inequalities, such as limited economic opportunities for women, wage disparities, the devaluation of feminised labour, and women’s depletion. Organising around tax justice attempts to redress these inequalities by demanding a recognition of women’s indispensable labour. Recognition in this case not merely being the celebration of this unrewarded toil, but the actual rejection of the logics that construct social reproduction as women-only work, followed by appropriation of tax resources towards easing this burden.”

“International Women’s Day has its roots in women organising around labour. Women’s labour is inextricably linked to tax. When austerity and other failed measures defund and collapse public services, it is women who pay through increased unpaid care work, more precarious paid work and through out of pocket payments for privatised services. When you combine this with regressive tax measures such as high consumption taxes, it places extreme pressures on households. Tax raised and spent progressively can fund public services which are necessary to redistribute care, create decent jobs in the public sector and deliver on women’s rights. On this day, we need to amplify feminist calls for economies centred on care, and tax is a critical component.“

“Financing a country is a collective effort. Countries majorly finance their development through tax. This is why tax is an important tool for development. However, we operate within an unfair tax system in which those with the highest ability to pay do not pay their share, while those with the least ability to pay, pay over and above their ability. This is why as feminists, we demand a system change.

I have heard the world’s billionaires call on governments to tax them. For me, it feels like, particularly for governments in the global South, that they are being called to beard the lion in his den. Billionaires control the system. Through the global financial architecture they have determined whether they will pay their share of taxes or not; and when they choose to pay, how much they will pay. Thus, their call is only a mockery. If they had the willingness to pay, they would not need to ask to be taxed, they should pay! This is what tax justice is about.

African women have, because of systems such as colonialism, patriarchy, and imperialism historically been disadvantaged when it comes to access and control of productive resources. As such they have been marginalised within the economic and political field, and yet fiscal policies that govern revenue collection and distribution are influenced by and often favour powerful individuals and large companies, many of which are male, or male-owned respectively. To ensure tax justice, policy makers must be aware of how oppressive systems and policies can work against certain less privileged individuals and act as a barrier to their enjoyment of certain opportunities. Such differences include gender, socio-economic class (whether one is rich or poor), age, ethnicity, race, among others.”

The fight for tax justice is integral to the ongoing battles for women’s rights worldwide. Throughout history, women have faced various forms of exclusion from public life, including within decision-making processes related to the design and implementation of tax policies. This has contributed to women’s limited access to economic resources and created gender biases across tax systems that continue to ignore women’s lived experiences. Calls for tax justice aim to challenge these exclusions by advocating for equitable and transparent tax policies that benefit all members of society, including all women. Such policies have the potential to address the range of socio-economic and political barriers that women face and help to adequately resource gender-transformative public services and social protection programmes. Conversely, regressive tax policies can perpetuate gender inequalities and further undermine women’s rights. Therefore, demands for tax justice remain a critical site of struggle for women’s rights, connected to the need for equitable tax systems that eliminate both historical and ongoing barriers faced by women.

The subjugation of women is centuries old. The resulting inequalities have had, and continue to have, a profound impact on women and girls economically, socially and culturally. These persist today, in the fiscal and tax regimes and extractive economies and cultures that operate in high and low per capita countries. Not surprisingly, the burden and damage is disproportionately felt by women and girls in low income countries and in the households where regression and policy incoherence of unjust tax policies continue to marginalise by gender, race, disability and people of indigenous communities. The story of overlapping gender injustice must, then, turn its focus laser-like on the financial opacity and tax injustice that operates largely unfettered. Long awaited, much needed, is an intergovernmental agreement to ‘re-code’ international financial laws and tax policies to mobilise national revenue, redistribute revenue, and to use tax to incentivise or disincentivize public ‘bads’ , and establish greater representation between women and the state. The transparency, disclosure and enforcement needed to mitigate gender inequality depends on well-resourced institutions, and in turn such sustainable revenue requires ‘good’ taxes that target wealth. Both require a shift to inclusive and transparent governance of tax sovereignty.

“Women’s struggles for the right to the vote, equal pay, economic rights and bodily autonomy are historic, yet still very pertinent, as shown by the recent regression of hard-won women’s rights and gender equality since the start of the COVID-pandemic. For all women’s struggles how resources are used and who has the power to decide is critical. Women carry a disproportionate burden of unpaid care and domestic work, doing 76% of it worldwide. When public services are not available, inadequate or understaffed, this affects women most as shock absorbers of austerity and crisis; as we are most likely to pick up the gaps in care, lose the chance to decent work and have services cut that are relevant to us, such as maternal health or reproductive health rights. Tax systems and policies are at the heart of what resources are available for gender-responsive public services, but also shapes how resources are collected, used and (re)distributed – or as in the current system accumulated in the hands of a few. For all women to exercise choice and control over economic opportunities, outcomes and resources, and shape economic decision-making at all levels tax justice is key.”

“Women continue to be disproportionately negatively impacted by tax injustice, more so in the global South. Due to gendered norms in a patriarchal capitalist society, women shoulder much of the unseen work which capitalism cannot operate or thrive without. Despite this, they are still on the receiving end of increased austerity measures which impede their access to basic essential services such as health care and education. Women, historically, are the shock absorbers to the failed extractivist capital system, where tax injustice occurs women’s unpaid care work increases, the failures of the economic system, particularly a failure to implement progressive tax systems means the continuation of the externalisation of the gaps onto women’s work in the home and community. The demand for tax justice remains historically rooted in the demand for women’s rights.”

“The fight for women’s rights has always been closely linked to access to and control over economic resources. Historically, women were denied the right to vote because of their socioeconomic class and race. In the last thirty years, we know that the burden caused by the weakening of the fiscal state has been borne by women from lower income groups. How tax is raised and spent determines whether women fill the gaps in public services through unpaid or low paid care work and who accumulates wealth in a society. Higher rates of indirect taxes in countries or lack of funding for public services because of tax systems being poorly conceived or implemented have disproportionate impacts on women. Tax policies can also disincentivize women’s work and, along with a lack of adequate labour laws, force women into informal and precarious employment. Demands for tax justice must be based on and support the struggles for all women to realise their rights and achieve gender and racial equality.”

Global Days of Action on Tax Justice for Women’s Rights 2023

GATJ, its regional networks and partner organisations will hold, from 6 to 17 March, the 7th edition of the Global Days of Action on Tax Justice for Women’s Rights. The campaign coincides with the 67th session of the United Nations Commission on the Status of Women (UN CSW67), which is a key strategic advocacy opportunity and space to engage with policy-makers on tax justice issues affecting women.

This year, the campaign focuses on the call for the urgent adoption of wealth taxes to advance towards the realisation of women’s rights, gender equality, and the empowerment of women and girls. Throughout the two weeks of the campaign, there will be several virtual, in-person and hybrid events and activities across the world, calling on governments and multilateral institutions to make taxes work for women.

We’re sharing this excellent live discussion between Caribbean Economist and Advisor Marla Dukharan, Alex Cobham, Economist and Chief Executive of the Tax Justice Network, and Professor Steven Dean, Professor of Law at Brooklyn Law School, “to find out the truth about the world’s biggest financial secrecy jurisdictions, the racial bias behind the tax blacklisting of former European colonies and developing states, and the history behind the discrimination in a global tax system designed to favour wealthy states.”

You can read Marla Dukharan’s research on the EU Blacklist here and there’s more further reading on this below.

We’ve written many times about the farce of the EU’s tax haven (and other) blacklists and how, if you want an objectively verifiable ranking, you need look no further than the Tax Justice Network’s Financial Secrecy Index. As Alex Cobham writes here, “There’s a long and largely ignominious tradition of tax haven blacklists, mainly at the OECD and IMF.They’ve tended to be subjective efforts, naming economically smaller jurisdictions with less political power, and steering well clear of major financial centres – regardless of their behaviour.” And incredibly, the EU’s tax haven list only applies to non-EU member states – and tortuously manages to not identify the US as non-cooperative, despite its well-earned #1 position on the Financial Secrecy Index. Well, how convenient…

The European Union saw several scandals recently that demonstrate corruption is a persistent problem in need of better regulation. The ongoing Qatargate scandal has highlighted the potential for corruption in the European Parliament, making clear it is high time for the EU to take action.

In January 2023, the European Commission opened a public consultation on its plans to adopt EU-specific anti-corruption rules and establish an EU policy on corruption. Working with leading academics and members of civil society organisations[i], we have submitted a response to the consultation which is available to read in full here.

Our response to the European Commission’s public consultation on corruption identifies 10 points that should inform future policy:

A directive on anti-corruption is urgently needed for legal clarity and to ensure harmonisation of efforts on countering corruption. We argue that the directive should contribute the best ways to regulate corruption at the EU and national levels, not only by adopting rules on bribery but also on undue lobbying, conflicts of interests, revolving doors, elite capture and dishonest practices in the public and private sectors. The EU has been inactive on this issue, despite the new legislative possibilities given to it by the Lisbon Treaty (Article 83 TFEU), and it is now the right time to address this phenomenon which harms societies and economies.

2. Anti-corruption strategies and agencies. We call upon the European Commission to put forward a clear strategy for countering political corruption and to adopt rules for anti-corruption agencies at the national level. These anti-corruption agencies should be independent, reporting to Parliament, and not to the government in power. They should also be provided with adequate personnel, budget and enforcement powers to fight corruption.

3. Whistleblowers have proven to be instrumental in discovering and reporting corruption. The long-awaited Directive 2019/1937 on the protection of persons who report breaches of EU law (the so-called Whistleblowers Directive) has not yet been transposed in most member states legislation, even though the transposition deadline has passed. Despite several advantages of the directive, there is still room for improvement. The directive’s transposition should be carefully reviewed and amendments should be proposed to ensure an appropriate reward/protection for all persons whose reports lead to successful revelation of wrongdoings that has an adverse impact on EU budgets.

4. Beneficial ownership transparency. Disclosing the beneficial owners behind legal vehicles is considered to be one of the most powerful transparency tools for tackling illicit financial flows related to corruption, as well as money laundering, tax evasion and the financing of terrorism. The EU had become a transparency leader with its 2018 amendment to the fourth Anti-Money Laundering Directive. However, public access to beneficial ownership information was recently invalidated by the European Court of Justice in relation to the cases WM (C-37/20) and Sovim (C 601/20) v Luxembourg Business Registers.

We believe that an EU anti-corruption directive should also require public access to information without needing to make a specific legitimate interest request. In addition, in order to better detect corruption and other crimes, the directive should require countries to establish asset registries for unregistered assets. Asset registers should collect information on the beneficial owners of the registered assets and cover a comprehensive range of assets, from real estate, yachts and private jets to crypto-assets, art works and jewellery.

5. Improved collection, access and use of banking information. The directive should require the SWIFT messaging system or any inter-banking communication within the EU to include beneficial ownership information.

6. Better risk indicators. EU member states should publish lists of the individuals who are politically exposed persons (PEPs) and asset declarations of Members of Parliament should include a comprehensive list of assets. Member states should also establish red flags or directly ban certain entities from entering into procurement contracts based on risk indicators from the entities’ country of origin.

7. Statistics on investigations and prosecutions. The EU should also develop a mechanism for independent monitoring of corruption and criminal law enforcement in the context of the member states. As part of this mechanism, the EU could establish a Corruption Observatory, which should perform and promote original research on corruption, create an open public repository of data on corruption and represent the EU as an active voice in countering corruption.

8. Monitoring of activities on corruption. We recommend that European agencies develop cyclical monitoring and evaluation of their respective and joint activities on corruption. Relevant European agencies, such as European Anti-Fraud Office (OLAF) and Eurojust, could closely work with relevant national authorities to more effectively operationalise a monitoring and evaluation mechanism that publishes annual reports on measures to combat corruption in the EU.

9. Training and learning. The EU should finance European exchange programmes between public officials, and, above all, train the younger generation of law enforcement officers.

10. Research on corruption. The Commission should also continue to promote advanced research on the criminological, sociological, economic, legal and behavioural dimensions of corruption to enhance effective harmonisation and cooperation within the EU and across its member states on corruption matters.

To conclude, the EU needs a comprehensive anti-corruption directive that is multi-pronged, as shown in our 10 points above. We believe these measures are necessary to meaningfully stamp out corruption in the EU.

[i] Prof. Umut Turksen, Dr Dimitrios Kafteranis, Dr Adam Abukari (Centre for Financial and Corporate Integrity – Coventry University), Dr Markus Meinzer, Moran Harari, Andres Knobel (Tax Justice Network), David Wright (Trilateral Research), Dr Wouter Wolfs (University of Leuven, Belgium), Ass. Prof. Aikaterini Pantazatou (University of Luxembourg), Dr. Erik Láštic (Comenius University, Slovakia) Pawan Kumar Sinha (International Anti-Corruption Academy).

É possível extrair minérios sem extrair vidas? Sim, mas é necessário cumprir e fortalecer as regulações e fiscalização do setor mineral, inclusive via tributação. As empresas de mineração são as que menos contribuem com impostos e o setor que extrai combustíveis fósseis é o que mais recebe subsídios governamentais no mundo.

Sobre a importância da tributação: 3,250 é o número de ambulâncias que poderiam ser compradas pelo município de Parauapebas (PA), na região amazônica, apenas se a Vale não desviasse lucros para paraísos fiscais e pagasse o que deve em Compensação Financeira pela Exploração Mineral, a CFEM.

Este é um dos dados de um estudo a ser lançado neste mês de março de 2023 sobre os abusos fiscais da Vale no Brasil e que é um dos destaques do episódio #46 do É da Sua Conta, que mostra que a tributação pode contribuir para que a mineração seja mais justa para as populações e o meio ambiente.

Tádzio Coelho, professor da Universidade Federal de Viçosa, coordenador do Estudo a ser lançado em março de 2023, em parceria com associação Justiça nos Trilhos e Rede Igrejas e Mineração.

~ É possível extrair minérios sem extrair vidas? #46

“Aqui no Malawi gostamos de falar que os minerais não são como milho ou mangas, porque não voltam a crescer. E é por isso que temos apenas uma chance de acertar os sistemas.” ~ Rachel Etter-Phoya, Tax Justice Network

“Pela Vale, houve um sub faturamento de CFEM de 1,8 bilhão de reais, o que vai dar, em dólares, 352 milhões de dólares. Mas a gente tem também as perdas que foram causadas à União, ao Estado do Pará, ao Estado de Minas Gerais e aos municípios das prefeituras onde a Vale mantém algum tipo de atividade mineradora referente à extração de minério de ferro.” ~ Tádzio Coelho, UFV

“O debate da CFEM é importante para pensar como essa contribuição se transforma em despesa e como ela pode estimular atividades econômicas que não são predatórias com os biomas onde esses territórios estão.” ~ Giliad de Souza Silva, Unifesspa

“A fiscalização, a monitoria, o controle são fundamentais em todas as fases – a descoberta, produção e exportação. Tem se garantir a presença do Estado e que haja monitoria nessas atividades.” ~ Inocência Mapisse, economista

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Pour cette 47ème édition de votre podcast en français sur la justice fiscale et sociale en Afrique et dans le monde produit par Tax Justice Network, nous partageons avec vous quelques réflexions qui ont été soulevées lors de la conférence alternative de la société civile africaine au Mining Indaba 2023. Il aura été question de transparence sur les bénéficiaires effectifs, ceux qui en dernier ressort profitent des retombés de l’exploitation des ressources minières. Il a aussi été question de la prise en compte des intérêts des communautés riveraines des projets miniers. Pour en discuter nous vous proposons une conversation avec deux acteurs importants de la société civile d’Afrique francophone

Maitre Jean-Paul Mulyanga : Directeur du Bureau de Liaison avec le Parlement pour la Conférence National Episcopale de RDC

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here. In this edition of the Taxcast:

After 30 years on the run, Italy’s most wanted fugitive Matteo Messina Denaro of the Cosa Nostra has been arrested in Sicily. We look at the costs of organised crime, both economic and societal, the contagion that financial secrecy facilitates, and how to reverse the rot.

Secrecy jurisdictions and tax havens have made it possible for mafiosi to progress from crossing physical borders with bank notes stuffed in suitcases, to being able to pour unlimited amounts of money into the financial system. Dirty money in, ‘clean’ money out. That money destabilises economies and corrupts democracies, while organised crime toxifies societies. The problem is that financial secrecy and tax havens are also the friend of commerce, multinationals and very wealthy, powerful people worldwide…

A transcript of the podcast is available here. (Some is automated)

Surgeon in Malta and opinon piece writer, Kevin Cassar

Hosted and produced by Naomi Fowler of the Tax Justice Network

“The mafia is not just a criminal phenomenon linked to money laundering, it’s a political, social and economic phenomenon. They interfere in the political process, they interfere in economic development. Ultimately we need State reform in all its parts. It really requires a fight against entrenched special interests.”

~ Professor Federico Varese

“Many banks and financial authorities don’t really care about who their customers are as long as they bring money in.”

~ Journalist, Stefano Vergine

“Some of these criminal organisations have a turnover every year which is basically the size of our economy…it is extremely difficult for journalists to do their job, it’s almost impossible to get clear answers.”

~ Surgeon, and opinion writer in Malta, Kevin Cassar

Naomi: “On this month’s Taxcast – the friend of organised crime and mafia networks is financial secrecy. Secrecy jurisdictions and tax havens have made it possible for mafias to progress from crossing physical borders with bank notes stuffed in suitcases, to being able to pour unlimited amounts of money into the financial system. Dirty money in, ‘clean’ money out. That money destabilises economies and corrupts democracies, while mafias toxify societies using force and fear. But the problem is that financial secrecy and tax havens are also the friend of commerce, multinationals and very wealthy, powerful people worldwide. That’s why the obvious solution of opening up secrecy jurisdictions is so hard to achieve.

I spend a lot of my time in Sicily, it’s a place that’s been limited for so long by the obsession people outside seem to have with the Sicilian mafia and the Cosa Nostra. Actually, the Cosa Nostra, as it once was, has been in decline for years, there’s been a lot of determination and bravery on the part of some Italian police and investigators. In my local town, the days when the judge had to have 24 hour guards with machine guns outside his house are long over. Actually he got sent to Calabria where the southern Italian mafias have become an even greater threat. Back on the island of Sicily though, something monumental just happened in January 2023:”

[Clips of shouts in the street as Matteo Messina Denaro is arrested, police sirens]

Naomi: “After 30 years on the run, Italy’s most wanted Cosa Nostra fugitive has been arrested. Matteo Messina Denaro boasted he could fill a graveyard with all his victims. You can hear the applause of passers by gathered on the street, some of them trying to hug the policemen, one of them is tearful.”

[Clip of applause from people in the street, and sirens]

Naomi: “Matteo Messina Denaro was sentenced in his absence for murders, including those of anti-mafia judges Giovanni Falcone and Paolo Borsellino in the 90s. That was a real turning point for many Sicilians, it’s a wound that goes deep to this day. Most main squares in Sicily are named after these two judges. In my local town square there’s a huge billboard with a famous photo of the two of them together. Written above it it says ‘citta contro tutte le mafie’ ‘city against all mafias.’ Back to the arrest of Matteo Messina Denaro:”

Professor Varese: “It’s wonderful news that he was arrested. He has been a fugitive for 30 years, he was the last big bosses to be a fugitive.”

Naomi: “This is Professor of Criminology and organised crime expert Federico Varese:”

Professor Varese: “It’s an amazing achievement, it was not easy to arrest him. The net was closing on him. People close to him had been arrested only a few months earlier..so you could somewhat imagine that this was coming, but it’s a fantastic news. It’s also symbolically very important because this man has been one of the most ruthless, violent, terrible killers in the history of the Sicilian Mafia, of course, he murdered women and children, he is one of the killers of Falcone. So it’s the end of an era.”

Naomi: “The end of an era for Cosa Nostra, I hope, compared to how it was in the past, but other mafia networks in Southern Italy like the Camorra and N’drangheta are still strong, still powerful and very dangerous. So if we look at the scale, just of all of the Italian mafias, I mean, it’s difficult to estimate these things as I know from the Tax Justice Network’s work, and the fact that transparency, and financial transparency isn’t there in so many places, but I’ve been looking at the estimated turnover of mafia business in Italy – according to the Bank of Italy it’s worth 2% of Italian GDP, that’s about 38 billion euros a year, that’s 104 million euros a day of dirty money washing through the system. I mean, can you speak to the scale and, you know, how big this is because 2% doesn’t sound like a lot, but it really is.”

Professor Varese: “Yeah, 2% is a lot. And the Bank of Italy is very reliable. There have been other numbers floating around like 7%, that’s I think, too much. It’s really important to see how this money, this figure is constructed. Uh, there is a lot of confusion over this because obviously what the mafia does, it extorts or ‘protects,’ depending on the point of view, businesses. So businesses pay a cut of their profit to the organisation mainly in Western Sicily, where the mafia is most rooted. And so we have to distinguish the business from the mafia income. So the business remains independent and makes money, but there is also often a tendency to confuse the turnover of the business with the profit of the business, with the profit of the mafia. And so it’s very, very hard to construct meaningful estimates. You can say that the Sicilian mafia is certainly in decline, partly because of this massive pressure from the police, and also because they have left the drugs trade. So they’re not any more involved in drugs as they used to be. Uh, now you can estimate the number of crime families, which are in Western Sicily and with some of them also in Eastern Sicily. And this is a number around 80 and the estimates of the membership is between one thousand and 400 ‘made’ members. So you can work out from that, but of course, not everybody makes all that much money, I mean, some are soldiers in the organisation who are probably just scraping through, and some, of course the bosses make much more. So it’s very hard to put a number to that. Certainly the Bank of Italy is a reliable source.

Another way to think about this is that there is an office, a procurator’s office in Palermo, which is responsible for managing property that are confiscated from people who are connected to the mafia, not necessarily mafia members, but also people connected to the mafia. So again, you can argue that maybe these confiscations happen very easily, but they estimate to have confiscated a third of the value of the Sicilian economy, so it’s a lot of money, so that would include items confiscated from people who are connected to the mafia, but not necessarily in the mafia so this goes also could be people who just pay protection money, which of course is illegal in Italy.”

Naomi: “So, you can see what a huge effect Cosa Nostra has had in Sicily all these years. As Professor Varese’s work has shown, Cosa Nostra tends to stay relatively local where they can maintain the tightest control with people they trust, but one of their favourite jurisdictions to launder money is in nearby Malta. Just one investigation not so long ago discovered people with links to Cosa Nostra were generating €14 million a month through illegal online gaming there. Some of that cash generated was being reinvested in legitimate businesses. But we’ll get back to Malta in a minute. This is journalist Stefano Vergine:”

Stefano: “What we know for sure is that over the last years, Italian authorities seized around 4 billion euros that allegedly belongs to Messina Denaro. It’s money that Messina Denaro invested through a number of his affiliates in legal businesses like supermarkets, wind farms, tourist companies, and also a lot of works of art. These assets were all in Italy, mainly in Sicily. The investments of course, were not done by him, they were done by people close to him. But of course, this might not be the whole wealth belonging to Messina Denaro. So, where could be the rest of his money? And for sure, we know that the global financial system provides a number of tools that help criminal organisations invest money. I’m thinking especially about tax havens and countries that guarantee the anonymity to beneficial owners of companies and of bank account holders. I’m thinking about Switzerland, for example, which borders Italy. Until a few years ago, bank secrecy was completely in place in Switzerland, and that means that if an Italian, for example, went to a Swiss bank with a bag full of cash, this person could deposit the money and no one would ever know this in Italy, neither judicial authorities. Now, things have partially changed and Switzerland started to exchange data of account holders with the authorities of countries that are part of the OECD. Still, hiding money, however is possible. And there are many places in the world that allow this to happen, officially or unofficially. One way is, for example, by using offshore companies linked to bank accounts that are based in a country where authorities don’t actually check properly who their client is. Let me mention some examples that I found out in my job – in 2016 on the magazine L’Espresso, along with a group of colleagues, part of ICIJ, we worked on the Panama Papers and we found out the names of dozens of offshore companies managed by a number of trusted men of mafia leaders. I’m talking about people like the Garabiano Brothers, Salvatore Riina, Bernardo Provenzano, who have been the absolute leaders of the Sicilian Mafia, the so-called Cosa Nostra. They were all sentenced to life imprisonment.

In one case, for example, we revealed offshore companies doing business in Africa with gold and diamond mines. These companies based mostly in the British Virgin Island were owned by the sons of Vito Palazzolo. We’re talking about mafia organisations that are based on familiar ties. It’s their strength. So Palazzolo was sentenced for being one of the biggest money launderer of Cosa Nostra when the Mafia organisation was led by Toto Riina, we’re talking about the nineties and its main business was trafficking heroin around the world. Palazzolo was sentenced for mafia back in the eighties, but the public didn’t know about these offshore companies owned by his sons until we revealed them in 2016. And this means that in the British Virgin Islands, no one raised a red flag on these companies, although the shareholders were sons of one of the biggest money launderers of Cosa Nostra.

There are a number of cases like this and in the Malta files, we also find cases like this, and this shows that you don’t necessarily have to go that far, you don’t have to go to the Caribbean, you can stay close to Italy and go to Malta. Uh, in 2017, we revealed that some mafia organisations opened companies in the island. I’m talking about Sicilian mafia, Camorra, N’drangheta, the Calabrian mafia. For example, we found a company based in Malta whose director was the heir of an important mafia clan based in Calabria, the so-called N’drangheta, the family is a big family specialised in cocaine trafficking with the South American cartels. So this is another example that shows how easy can be for a criminal organisation to open a company. Why is that? Even in countries where beneficial owners are not secret and where authorities officially collaborate with other countries, this is the case of Malta for example, many banks and financial authorities don’t really care about who their customers are as long as they bring money in. So this is, I think, what actually help criminal organisation to invest money overseas.”

Naomi: “And sometimes the best investigations that have given us the most information were only because this information was leaked, right? And not because it’s actually possible for somebody like you sometimes, a journalist, to actually get behind the wall of secrecy to be able to report on who’s behind a particular crime or a company involved in a crime right?”

Stefano: “That’s true. I mean, most of the times, yes, the best investigations are coming from a leak or let’s say from an internal source. It doesn’t have to be, you know, a huge leak like Panama Papers, which, which was a very good investigation and brought a lot of results. But still, yes, let’s say one way is to have a police source that is telling you things that have been already uncovered. Uh, the other way is to have an internal source or a whistleblower that can take you, that can bring you a lot of data or data concerning his company’s specific field of activity.”

Naomi: “Yeah, otherwise it can be like coming up against a brick wall. Let’s have a look at Malta as one of the favourite jurisdictions for Cosa Nostra money. The harm Malta’s done to itself and its people because of its oversized financial sector and offshore secrecy services is obvious. It’s not exaggerating to say it’s become a criminal state. Dirty money has undone the rule of law there, almost every check and balance. But it doesn’t stop there because once dirty money’s gone into their financial system, it washes into the global economy. This is Kevin Cassar. He’s a surgeon in Malta, who’s spoken out about how Malta has become a mafia paradise:”

Kevin Cassar: “Malta is just 60 miles south of Sicily. We can actually see Mount Etna on a clear day. So we are extremely close. We have regular ferries going across, which takes about just two hours by ferry. If you take a plane, it takes you 20 minutes to get to Sicily. The big advantage to mafiosi and other people in organised crime in Sicily is that Malta joined the European Union and we’re also, of course, we’ve got the Euro and we are part of Schengen, so there is free movement. So it’s extremely easy to get in and out of Malta and into Europe and from Sicily into Malta with very little or no checks at all. Now, in addition to that, Malta is the tiniest country in the European Union, which means that some of these criminal organisations have a turnover every year which is basically the size of our economy. And therefore, in a small place like this, it is extremely easy to pay your way into whatever position you want to get to.”

Naomi: “Dirty money is also what led to the murder of Maltese journalist Daphne Caruana Galizia, to shut down her investigations. And the mess the police made of that case, and allegations about politicians connected to it tell you everything about the state of justice in Malta. And just as telling, not long ago in Malta the post of Deputy Police Commissioner became vacant. No one applied for it and for me, that speaks very strongly about what a kind of a failed state Malta actually is.”

Kevin Cassar: “Yeah. It definitely is a failed state, and the problem is that the Prime Minister has almost absolute powers. So the Prime Minister appoints the police commissioner. The problem with that is that people who are deeply involved in gross corruption, who are involved in, you know, illegalities who are close to the Prime Minister, were never prosecuted. Um, so we have, for example, magisterial inquiries related to Pilatus Bank for example, which specifically said that the chairman of Pilatus Bank, which is this money laundering enterprise for the Azerbijanis, and for people close to former Prime Minister Joseph Muscat should be prosecuted. This man has never been prosecuted. We had another magisterial inquiry which looked into allegations that one of these secret financial structures set up by Mossack Fonseca belonged to the Prime Minister’s wife, former Prime Minister Joseph Muscat that is, and one of the accountants who was part of the same company that was working very closely with the Prime Minister, the conclusions of the inquiry was that this man should be prosecuted for perjury. This man was never prosecuted. So we have a state of impunity, which was one of the main conclusions of the Daphne Caruana Galizia inquiry.

So in answer to your question, why do people not want to join the police force in any, even almost at the, the lowest levels, let alone at the higher echelons? And the reason is that this is a completely corrupt institution. The police commissioner himself was finally removed when there was an order by the court that he should be investigated. That was months, if not years ago. No action has been taken against the former police commissioner.

There is also huge pressure, of course, on people who are in the police force who try to do their job. So we’ve had people, for example, like a chap who was investigating these people close to politicians and politicians themselves was basically hounded out of the force, and he’s now suing the government for discrimination and for basically not reintegrating him into the police force. We had another gentleman who was in the FIU, that’s the Financial Investigative Authority, who was basically kicked out when he started to work on these cases of corruption involving politicians. So it’s no surprise that nobody wants to get into a police force like that.”

Naomi: “No, no surprise at all.”

Kevin: “You know, we live in a country where we’ve had several bombings people killed with car bombs, the same type of bombs that killed Borsellino and Falcone. In a small country like this where you have bombs exploding and killing people, none of those bombings has been solved. The only one that has partially been solved is the Caruana Galizia bombing, and that’s because of the involvement of the FBI. So, can you imagine a small country like ours where we have multiple people killed from car bombings and nobody ever arraigned? And I tell you possibly why, because the people who are now under arrest, finally, the Maksar Brothers, they were clients of our current Prime Minister. So our current Prime minister was the lawyer defending the Maksar Brothers. So this is the sort of network that we have, which is, to me, it is far worse than what is happening in Sicily, because in Sicily, there is some rule of law, the state is trying to protect the citizens. In this country, our government, our authorities, our institutions, the police are all part of this criminal network.”

Naomi: “So, however bad things have been, and can be in Sicily, Malta is a classic captured state because of its big financial secrecy sector. And looking the other way when it comes to criminal money coming in extends to everything. It undermines fair public procurement in the public interest, which Sicilians know all about too. All of this erodes people’s trust in the State to provide for their needs. Kevin Cassar, as a surgeon, has seen this for himself only too plainly in Malta:”