Welcome to our monthly podcast in Portuguese, É da sua conta (it’s your business). All our podcasts (unique productions in five different languages – English, Spanish, Arabic, French, Portuguese) are available here.

É da sua conta#19: Carrefour e Pão de Açúcar: abusos em nome do lucro

Carrefour e Pão de Açúcar cometem diversos abusos – tributários, trabalhistas, com fornecedores e clientes – tudo para lucrar ainda mais, revela o livro “Donos do mercado”, dos jornalistas João Peres de Victor Matioli. Os abusos tributários e comerciais das duas maiores redes de supermercados que operam no Brasil estão no episódio #19 do É da Sua Conta. Ouça:

João Peres e Victor Matioli, autores de Donos do Mercado, contam como investigaram os dois hipermercados e trouxeram à luz as más práticas das empresas.

Carrefour e Pão de Açúcar exploram seus fornecedores, sobretudo os de pequeno porte, para maximizar seus resultados financeiros.

Envio de lucros a paraísos fiscais, organogramas complexos e não pagamento de multas relacionadas a impostos: manobras usadas por Carrefour e Pão de Açúcar para evitar o pagamento de tributos no Brasil

As medidas fiscais que podem acabar com estes crimes se colocadas em prática.

Como a financeirização atua no setorde alimentação

Você pode ganhar um livro “Donos do mercado”. Ouça o podcast e saiba como participar do sorteio!

Online conference: 3 and 4 December 2020– Register here

Co-organised with Gurminder K Bhambra, University of Sussex and Julia McClure, University of Glasgow, also based on a forthcoming book Imperial Inequalities: Taxation and Welfare across European Empires

In previous centuries European countries exercised the ‘aggressive extension’ of their authority. Their political interests extracted value and hardwired systems, culture and law to ‘lock’ colonised countries into debt and fiscal dependency. More recent decades, during ‘decolonisation’, saw the perfecting of this imperialist authority leaving a legacy of fiscal indenture.

Today defenders of imperialist systems – multinational companies and wealthy individuals – continue to exploit their powerful advantage leaving states impoverished and often democratically weak.

This conference will highlight the genesis of inequalities within countries and between countries. And in examining this, legacy contributors will explore directions for reparation and reprogramming global tax law and policy.

Questions we’ll be exploring:

To what extent has the European project of public expenditure on welfare been made possible by imperial extraction?

What role has taxation and welfare played in creating imperial inequalities? Do these challenge any pre-established theories about pathways to global inequality?

What role has been played by promoting dependent territories as ‘tax havens’, in the more recent period of extraction, and how has this damaged those territories as well as others?

How do tax laws, which can themselves be understood as having imperial legacies, continue to shape inequality trends?

What sort of reparations could conceivably address the scale of damage created from imperial extraction, and how can taxes be collected and redistributed to begin to mitigate the economic damage created?

How can we move reparations policy up the international political agenda and gain political momentum to move reparations forward?

A lot of people will be visiting our website today to read about the State of Tax Justice 2020 report that we’ve just launched globally. But the regular visitors among you will have noticed a second major launch today from the Tax Justice Network: our new website and branding.

What happened to the map?

The Tax Justice Network launched in 2003 after three Jersey islanders – Jean Anderson, Pat Lucas and Frank Norman – contacted former Jersey senior economic advisor and our founder-to-be John Christensen, asking him to help them save their island from the tax haven it had become. If you’re unfamiliar with the story of how a small group of school teachers and nuns baked and sold enough cakes to get the Tax Justice Network on to its feet and spark a global tax justice movement, the video below about the fire-starting trio and the annual award we named after them is well worth a watch.

With the launch of the Tax Justice Network came a logo that has served as the face of the organisation for nearly two decades. At the time, not many people knew about tax havens and their devastating impact on inequality around the world. The Tax Justice Network’s logo, just like the rest of our work at the time needed to draw attention to the globe-spanning nature and urgency of the problem.

Fast forward 17 years, and after numerous offshore scandals, tax havens are regularly featured in the news and tackling them is high on national and global agendas. Polling conducted this year in seven leading countries shows overwhelming public support for policymakers to crack down on companies using tax havens.

With the launch of the State of Tax Justice 2020 today, the debates about whether tax havenry is something that happens at the heart of the global economy, not its palm-fringed peripheries; and about whether global tax abuse is large enough to constitute a first-order economic problem; are over. The world’s biggest tax havens are OECD member countries: the UK (with its network of Overseas Territories and Crown Dependencies), the Netherlands and Luxembourg. Countries are losing over $427 billion to global tax abuse ever year. Losing a nurse’s yearly salary every second to a tax haven is very much a problem, especially during a pandemic.

The numbers are in. It’s time to act.

The way forward

The Tax Justice Network’s rebrand is characterised by a key pivot from drawing attention to the problem to pointing the way forward to the solution. While the Tax Justice Network has been proposing and successfully ushering in radical and imaginative polices solutions since 2003, we wanted our new branding itself to inspire people to reimagine the role tax plays in their life, and to reimagine a world where tax justice is realised.

The first step was to rethink the colours we use. Our red, black and grey colour scheme was good at communicating the gravity and urgency of the issue, which is why you’ll often find variations of this scheme used by NGOs. But what if we wanted more from our colour scheme?

After some brainstorming, we realised: what better colour to communicate both the possibility of a new world and the prosperity to be gained by all in a just society than a bright and warm yellow? The colour of both the sun and the simplest symbol for tax, a gold coin.

The second step was to find a design that could visualise what we want to say. In the end, the simplest symbol proved the best: an arrow pointing the way.

Putting it all together, we’re delighted to finally share with your our new Tax Justice Network logo.

Reprogramming our tax systems

A number of the Tax Justice Network’s policy proposals are global standards today. The data published by the OECD this summer which made our State of Tax Justice 2020 report possible was collected under country by country reporting, based on our original proposals and the draft international accounting standard published by Richard Murphy in 2003. Nonetheless, there’s still a long way to go to achieving tax justice.

For decades, our governments have been using tax policy as a tool to indulge the desires of the wealthiest and most powerful multinational corporations and individuals, instead of protecting people’s wellbeing. As a result, our societies are characterised by gross inequalities that deny us the opportunities to make a good life possible for everyone. This has dealt an ever heavier blow to women, people of colour and disabled people who already face systematically poorer prospects. Yet despite tax rates being cut down to the lowest levels of the modern period, multinational corporations and wealthy individuals are still short-changing people out of $427 billion in tax every year.

We must reprogramme our global tax system to prioritise people’s health and livelihoods over the desires of those bent on not paying tax. That means using tax policy as tool for making sure everybody has access to the opportunities that make a good life possible.

And so, to better equip people and governments around the world with the information and resources they need to reprogramme their tax systems, we’ve completely revamped our website to make it easier for visitors to find the content they need and to learn about the tax justice issues that impact them.

The new website we’ve launched today incorporates feedback we’ve received over the years from our website visitors, supporters and global network about what they want to get out of our website. Alongside a cleaner interface for more comfortable reading and a more intuitive organising of content, our new website packs a number of clever features we think you’ll find useful – like our country profiles. We’ll be launching more features in the coming weeks, including the ability to filter content and research by topics and region.

Our new report, rebrand and website launched today marks a new chapter for the Tax Justice Network. For those of you who have been with us on this journey for some time now, we thank you for your support and look forward to taking on the work ahead together. And for those of you joining us today for the first time, a big welcome from the Tax Justice Network team – there’s plenty of room for you in the fight for tax justice. We’re just getting started.

The equivalent of one nurse’s annual salary is lost to a tax haven every second

Countries are losing a total of over $427 billion in tax each year to international corporate tax abuse and private tax evasion, costing countries altogether the equivalent of nearly 34 million nurses’ annual salaries every year – or one nurse’s annual salary every second.1 As pandemic-fatigued countries around the world struggle to cope with second and third waves of coronavirus, a ground-breaking study published today reveals for the first time how much public funding each country loses to global tax abuse and identifies the countries most responsible for others’ losses. In a series of joint national and regional launch events around the world, economists, unions and campaigners are urging governments to immediately enact long-delayed tax reform measures in order to clamp down on global tax abuse and reverse the inequalities and hardships exacerbated by tax losses.2

The inaugural edition of the State of Tax Justice – an annual report by the Tax Justice Network on the state of global tax abuse and governments’ efforts to tackle it, published today together with global union federation Public Services International and the Global Alliance for Tax Justice – is the first study to measure thoroughly how much every country loses to both corporate tax abuse and private tax evasion, marking a giant leap forward in tax transparency.

While previous studies on the scale of global corporate tax abuse have had to contest with the fog of financial secrecy surrounding multinational corporations’ tax affairs, the State of Tax Justice analyses data that was self-reported by multinational corporations to tax authorities and recently published by the OECD, allowing the report authors to directly measure tax losses arising from observable corporate tax abuse. The data, referred to as country by country reporting data3, is a transparency measure first proposed by the Tax Justice Network in 2003. After nearly two decades of campaigning, the data was made available to the public by the OECD in July 2020 – although only after multinational corporations’ data was aggregated and anonymised.4

Of the $427 billion in tax lost each year globally to tax havens, the State of Tax Justice 2020 reports that $245 billion is directly lost to corporate tax abuse by multinational corporations and $182 billion to private tax evasion.5 Multinational corporations paid billions less in tax than they should have by shifting $1.38 trillion worth of profit out of the countries where they were generated and into tax havens, where corporate tax rates are extremely low or non-existent. Private tax evaders paid less tax than they should have by storing a total of over $10 trillion in financial assets offshore.

Poorer countries are hit harder by global tax abuse

While higher income countries lose more tax to global tax abuse, the State of Tax Justice 2020 shows that tax losses bear much greater consequences in lower income countries.6 Higher income countries altogether lose over $382 billion every year whereas lower income countries lose $45 billion. However, lower income countries’ tax losses are equivalent to nearly 52 per cent of their combined public health budgets, whereas higher income countries’ tax losses are equivalent to 8 per cent of their combined public health budgets. Similarly, lower income countries lose the equivalent of 5.8 per cent of the total tax revenue they typically collect a year to global tax abuse whereas higher income countries on average lose 2.5 per cent.

The same pattern of global inequality is also strongly visible when comparing regions in the global north and south. North America and Europe lose over $95 billion in tax and over $184 billion respectively, while Latin America and Africa lose over $43 billion and over $27 billion respectively. However, North America and Europe’s tax losses are equivalent to 5.7 per cent and 12.6 per cent of the regions’ public health budgets respectively, while Latin America and Africa’s tax losses are equivalent to 20.4 per cent and 52.5 per cent of the regions’ public health budgets respectively.

Rich countries are responsible for almost all global tax losses

Assessing which countries are most responsible for global tax abuse, the State of Tax Justice 2020 provides the strongest evidence to date that the greatest enablers of global tax abuse are the rich countries at the heart of the global economy and their dependencies – not the countries that appear on the EU’s highly politicised tax haven blacklist or the small palm-fringed islands of popular belief. Higher income countries are responsible for 98 per cent of countries’ tax losses, costing countries around the world over $419 billion in lost tax every year while lower income countries are responsible for just 2 per cent, costing countries over $8 billion in lost tax every year.

The five jurisdictions most responsible for countries’ tax losses are British Territory Cayman (responsible for 16.5 per cent of global tax losses, equal to over $70 billion), the UK (10 per cent; over $42 billion), the Netherlands (8.5 per cent; over $36 billion), Luxembourg (6.5 per cent; over $27 billion) and the US (5.53 per cent; over $23 billion).

G20 countries meeting tomorrow responsible for over a quarter or global tax losses

G20 member countries meeting this weekend for the Leaders’ Summit 2020 are collectively responsible for 26.7 per cent of global tax losses, costing countries over $114 billion in lost tax every year. The G20 countries themselves also lose over $290 billion each year.

In 2013, the G20 mandated the OECD to require collection of the country by country reporting data analysed by the State of Tax Justice 2020 – a measure the OECD had long resisted until then. In 2020, the OECD’s consultation on country by country reporting highlighted two major demands from investors, civil society and leading experts: that the technical standard be replaced with the far more robust Global Reporting Initiative standard, and – crucially – that the data be made public.7

The Tax Justice Network is calling on the G20 heads of state summit this weekend to require the publication of individual multinationals’ country by country reporting, so that corporate tax abusers and the jurisdictions that facilitate them can be identified and held to account.

Alex Cobham, chief executive of the Tax Justice Network, said:

“A global tax system that loses over $427 billion a year is not a broken system, it’s a system programmed to fail. Under pressure from corporate giants and tax haven powers like the Netherlands and the UK’s network, our governments have programmed the global tax system to prioritise the desires of the wealthiest corporations and individuals over the needs of everybody else. The pandemic has exposed the grave cost of turning tax policy into a tool for indulging tax abusers instead of for protecting people’s wellbeing.

“Now more than ever we must reprogramme our global tax system to prioritise people’s health and livelihoods over the desires of those bent on not paying tax. We’re calling on governments to introduce an excess profit tax on large multinational corporations that have been short-changing countries for years, targeting those whose profits have soared during the pandemic while local businesses have been forced into lockdown. For the digital tech giants who claim to have our best interests at heart while having abused their way out of billions in tax, this can be their redemption tax. A wealth tax alongside this would ensure that those with the broadest shoulders contribute as they should at this critical time.”

Rosa Pavanelli, general secretary at Public Services International, said:

“The reason frontline health workers face missing PPE and brutal understaffing is because our governments spent decades pursuing austerity and privatisation while enabling corporate tax abuse. For many workers, seeing these same politicians now “clapping” for them is an insult. Growing public anger must be channelled into real action: making corporations and the mega rich finally pay their fair share to build back better public services.

“When tax departments are downsized and wages cut, corporations and billionaires find it even easier to swindle money away from our public services and into their offshore bank accounts. This is of course no accident; many politicians have wilfully sent the guards home. The only way to fund the long-term recovery is by making sure our tax authorities have the power and support they need to stop corporations and the mega rich from not paying their fair share. The wealth exists to keep our societies functioning, our vulnerable alive and our businesses afloat: we just need to stop it flowing offshore.

“Let’s be clear. The reason corporations and the mega rich abuse billions in taxes isn’t because they’re innovative. They do it because they know politicians will let them get away with it. Now that we’ve seen the brutal results, our leaders must stop the billions flowing out of public services and into offshore accounts, or risk fuelling cynicism and distrust in government.”

Dr Dereje Alemayehu, executive coordinator at the Global Alliance for Tax Justice, said:

“The State of Tax Justice 2020 captures global inequality in soberingly stark numbers. Lower income countries lose more than half what they spend on public health every year to tax havens – that’s enough to cover the annual salaries of nearly 18 million nurses every year. The OECD’s failure to deliver meaningful reforms8 to global tax rules in recent years, despite the repeated declaration of good will, makes it clear that the task was impossible for a club of rich countries. With today’s data showing that OECD countries are collectively responsible for nearly half of all global tax losses, the task was also clearly an inappropriate one for a club heavily mixed up in global tax havenry.

“We must establish a UN tax convention to usher in global tax reforms. Only by moving the process for setting global tax standards to the UN can we make sure that international tax governance is transparent and democratic and our global tax system genuinelyfair and equitable, respecting the taxing rights of developing countries.”

Country cases of tax losses

Tax abuse in Vietnam causes as much economic loss as Typhoon Molave Typhoon Molave, described by Vietnamese Deputy Prime Minister Trinh Dinh Dung as “one of the two most powerful storms Vietnam has had in the past 20 years,” destroyed more than 700 houses and left 80 people dead and missing in October 2020. The Vietnamese government estimates Typhoon Molave to have caused $430 million in economic damage.9 Vietnam loses nearly as much tax, over $420 million (97 per cent of $430 billion), every year to global tax abuse.

South Africa’s tax losses could lift over 3 million people out of poverty Nearly half of South Africa’s adult population lives in poverty, with more women (52 per cent) in poverty, than men (46 per cent).10 The latest upper-bound poverty line published by the South African government in 2019 is ZAR 1,227 per month (almost $85 per month).11 If the $3.39 billion in tax that South Africa loses every year to tax abuse was instead given as direct cash transfers of $85 per month to people living in poverty, over 3 million people could be lifted out of poverty.

Greece’s tax losses equal to over a quarter of scheduled debt repayments Greece’s annual loss of nearly $1.36 billion in tax (€1.15 billion) to tax abuse is equivalent to over a quarter (27 per cent) of Greece’s scheduled debt repayments for 2020, which total €4.19 billion.12 Among the multiple debtors Greece owes, the country is specifically scheduled to repay €443.7m to Eurozone countries in 2020. Greece’s annual tax losses are over double this amount.

Responsibility for global tax losses

The UK spider’s web is responsible for over a third of global tax losses The jurisdiction that causes countries the most global tax losses is British Overseas Territory Cayman, which is responsible for other countries losing over $70 billion in tax every year. However, Cayman is just one jurisdiction that falls under UK’s network of Overseas Territories and Crown Dependencies, where the UK has full powers to impose or veto lawmaking and where power to appoint key government officials rests with the British Crown. Infamously referred to as the UK spider’s web13, extensive research has documented the ways in which this network of jurisdictions operates as a web of tax havens facilitating corporate and private tax abuse, at the centre of which sits the City of London.

The State of Tax Justice 2020 finds that the UK spider’s web is responsible for 37.4 per cent of all tax losses suffered by countries around the world, costing countries over $160 billion in lost tax every year.

The “axis of tax avoidance” is responsible for over half of the world’s tax losses The Corporate Tax Haven Index 2019 had previously estimated that the UK, together with its network of Overseas Territories and Crown Dependencies, Luxembourg, Switzerland and the Netherlands are together responsible for half of the world’s risk of corporate tax abuse, coining the label “axis of tax avoidance” for the group.14 The Tax Justice Network revealed in April 2020 that the axis of tax avoidance costs the EU over $27 billion in lost tax every year solely from US multinational corporations operating in the EU.15

The State of Tax Justice Network confirms today that the axis of tax avoidance is collectively responsible for over 47.6 per cent of global tax loss incurred from corporate tax abuse. When including tax losses to private tax evasion, the axis of tax avoidance is responsible for 55 per cent of all tax losses suffered by countries around the world, costing countries nearly $237 billion in lost tax every year.

EU blacklisted jurisdictions cause less than 2% of global tax losses, EU member states cause 36% Analysis of the jurisdictions on the EU tax haven blacklist found the cohort to be collectively responsible for just 1.72 per cent of global tax losses, costing countries over $7 billion in lost tax a year.16 In comparison, EU member states are responsible for 36 per cent of global tax losses, costing countries over $154 billion in lost tax every year.

The Tax Justice Network has long criticised17 the EU’s blacklist for ignoring major tax havens while focusing on jurisdictions that are secretive but play an insignificant role in the global economy. The State of Tax Justice 2020 reveals that two jurisdictions blacklisted by the EU, Palau and Trinidad and Tobago, while non-cooperative with international tax regulations, did not create any observable tax losses for other countries.

On the other hand, British Territory Cayman which was briefly blacklisted for the first time in February 202018 but removed from the list in October 2020 after it was deemed compliant with international tax rules, is responsible for the biggest share of countries’ tax losses (16.5 per cent of global tax losses, equal to over $70 billion a year). The Tax Justice Network argues that Cayman being deemed to be compliant with international tax rules despite being the world’s greatest enabler of global tax abuse is evidence that current international tax rules are not fit for purpose.

Three actions governments must take

The Tax Justice Network, Public Services International and the Global Alliance for Tax Justice, along with supporting NGOs, campaigners and experts around the world, are together calling on governments to take three actions to tackle global tax abuse:

Introduce an excess profit tax on multinational corporations making excess profits during the pandemic, such as global digital companies, in order to cut through profit shifting abuses. Multinational corporations’ excess profit would be identified at the global level, not the national level, to prevent corporations from underreporting their profits by shifting them into tax havens, and taxed using a unitary tax method.19

Introduction of a wealth tax to fund the Covid-19 response and address the long term inequalities the pandemic has exacerbated, with punitive rates for opaquely owned offshore assets and a commitment between governments to eliminate this opacity. The pandemic has already seen an explosion in the asset values of the wealthy, even as unemployment has soared to record levels in many countries.

Establish a UN tax convention to ensure a global and genuinely representative forum to set consistent, multilateral standards for corporate taxation, for the necessary tax cooperation between governments, and to deliver comprehensive, multilateral tax transparency.

The research will be presented at virtual event taking place from 1:00pm to 2:30 pm GMT on Friday 20 November 2020. The event will features speakers from around the world. Registration is available here.

Notes to Editor

The tax losses of countries around the world are equivalent to nearly 34 million nurses’ annual salaries every year. Instead of a blanketly applying one country’s average annual nurse salary to the world, the global number of equivalent nurses’ salaries lost is arrived at by first calculating how much each country’s tax losses is equivalent to in local average annual nurse salaries in the country. Each country’s equivalent in nurses’ annual salaries is then summed to produce a global total the reflects nurses’ annual salaries around the world. Countries’ average annual nurse salaries are sourced from OECD data. For non-OECD countries, we use the average salary in the country, as reported by the International Labor Organization. Missing values in the OECD and ILO databases were calculated using the relation between the country’s average salary and GDP per capita found in other countries.

A global virtual event launching the State of Tax Justice 2020 will take place at 1pm GMT on Friday 20 November 2020.

Country by country reporting is designed to expose and deter profit shifting, a practice that involves multinational corporations moving profits from the countries where they were generated to tax havens, where corporate tax rates are low to non-existent, in order to underreport how much profit they made outside of tax havens and consequently pay less corporate tax. By requiring multinational corporations to publish how much profit they made and how much cost they incurred in each country in which they operate, public country by country reporting makes it impossible for corporations to shift profit into tax havens for the purpose of warping tax obligations elsewhere without being detected. This also exposes the cost of corporate tax havens’ aggressive tax policies to other countries.

An international accounting standard for public country by country reporting was first proposed by the Tax Justice Network in 2003. Although initially resisted by the OECD the reporting method was eventually backed by the G20 group of countries in 2013, with the OECD producing a standard for use from 2015. After numerous delays, the OECD finally published partial data in July 2020. However, while the Tax Justice Network’s proposal called for multinational corporations to publicly disclose their country by country reports, the OECD required multinationals only to privately submit their reports to OECD countries’ tax authorities. Reports collected from multinational corporations were then aggregated and anonymised by OECD countries before the data was shared with the OECD body and published. As a result, while the Tax Justice Network’s analysis of the data published by the OECD shows that multinational corporations are paying $245 billion less in corporate tax than they should, it is not possible to identify which multinational corporations are responsible.

For countries that did not make country by country reporting data available, the State of Tax Justice uses information about the activity of multinational corporations within the non-reporting country from the data made available by other reporting countries. The more data coverage a country has – ie, the more countries whose country by country reporting cover a given, other country – the greater the accuracy of the estimates for the latter. Hence the importance of the transparency measure. As more countries get on board with country by country reporting in the coming years, the sharper the estimates will become.

Countries’ annual tax loss estimates are calculated using data from the latest year available as of time of writing. Corporate tax abuse estimates are based on analysing the latest country by country reporting data from the OECD, which are for 2016. Private tax evasion estimates are based on analysing data on bank deposits from the Bank for International Settlements from 2018. These estimates are representative of the tax losses countries incur on an annual basis.

The World Bank classifies countries on the basis of gross national income per capita as either low, lower middle, upper middle or high income. Roughly half the world’s population lives in the two lower income groups, and roughly half in the higher income groups. Accordingly, when referring to “higher income” countries in this press release and report, we refer to high income and upper middle income countries grouped together, and when referring to “lower income” countries, we refer to lower middle income and low income countries grouped together.

The OECD’s blueprint for reforms published in October 2020 has been widely criticised by Joseph Stiglitz, Eva Joly, Jayati Ghosh and other leading economists and tax experts for failing to deliver meaningful reform. The Tax Justice Network criticised the OECD’s proposal for being a “tax haven lite” plan.

Approximately half (49.2 per cent) of the adult population in South Africa were living below the upper-bound poverty line in 2015. According to the government survey, there were 35.1 million adults (aged 18 years and older) under the upper-bound poverty line. Adult females experienced higher levels of poverty when compared to their male counterparts.

The South African government measures poverty by three threshold points. The upper-bound poverty line, the lower-bound poverty line and the food poverty line. The latest values for the poverty lines, among which upper-bound poverty line is the highest, were published by the South African government in 2019.

For a list of Greece’s scheduled debt repayments, see here.

Most of the UK’s Overseas Territories and Crown Dependencies ranked high on the Tax Justice Network’s Corporate Tax Haven Index in 2019, a ranking of how complicit countries’ legal and financial systems are in enabling global corporate tax abuse (see note 13 below). The Corporate Tax Haven Index previously estimated the UK and its network of Overseas Territories and Crown Dependencies to be collectively responsible for a third of the world’s risks for global corporate tax abuse.

While the index measured risks for corporate tax abuse, it could not directly measure corporate tax losses arising from those risks due to the difficulty in measuring corporate tax abuse prior to the publishing of country by country reporting data by the OECD this past summer.

The State of Tax Justice 2020 confirms that the UK spider’s web is responsible for 28.5 per cent of the tax losses countries incur from corporate tax abuse, in line with the index’s 2019 estimate. When including tax losses to private tax evasion, the UK spider’s web is responsible for 37.4 per cent of all tax losses suffered by countries around the world, costing countries over $160 billion in lost tax every year.

For more information about the UK spider’s web, please see Michael Oswald’s documentary “The Spider’s Web: Britain’s Second Empire”, produced by Tax Justice Network founder John Christensen. The documentary is available on YouTube in English, Spanish, French, German and Italian and has been viewed nearly 4 million times.

The Corporate Tax Haven Index ranks countries by their complicity in global corporate tax havenry. The index scores each country’s legal, tax and financial system based on the degree to which it enables corporate tax abuse. Each country’s corporate tax haven score is then combined with the scale of corporate activity in the country to determine the share of global corporate activity put at risk of tax avoidance by the country. The greater the share of global corporate activity put at risk of corporate tax abuse by the country’s tax and financial system, the higher the country ranks on the index. The following 10 jurisdictions ranked highest on the latest edition of the Corporate Tax Haven Index published in 2019: 1. British Virgin Islands (British territory), 2. Bermuda (British territory), 3. Cayman Islands (British territory), 4. Netherlands, 5. Switzerland, 6. Luxembourg, 7. Jersey (British dependency), 8. Singapore, 9. Bahamas, 10. Hong Kong. For more information on the index and the axis of tax avoidance, see here.

Analysis by the Tax Justice Network of country by country reporting data published in early 2020 by the US ahead of the OECD’s publishing of country by country data found that the axis of tax avoidance cost EU member states over $27 billion in lost corporate tax a year solely from US multinational corporations operating in the EU.

Of the 12 jurisdictions on the EU tax haven blacklist, data was only available for 8 jurisdictions for the State of Tax Justice 2020 to analyse: Barbados, Fiji, Palau, Panama, Samoa, Trinidad and Tobago, US Virgin Islands, Vanuatu, Seychelles. Due to the very small sizes of the economies of the four jurisdictions for which data is not available (American Samoa, Anguilla, Guam, US Virgin Islands), the absence of the jurisdictions from the analysis of the EU blacklist is not expected to have any material impact on the analysis.

Analysis by the Tax Justice Network in 2018 found that the EU tax haven blacklist blocks just 1 per cent of financial secrecy services threatening EU economies.

Analysis of the EU’s decision to blacklist British Overseas Territory Cayman in February 2020 is available here.

Under the excess profit tax, each country where the multinational corporation operates would have the right to tax a share of the corporation’s global excess profits according to the country’s local corporate tax rates. The size of the share of excess profits that is apportioned to a country to tax would be based on the share of the multinational corporation’s workforce and sales based in the country. Meaning, countries where multinational corporations hire employees, run factories and offices, and sell goods and service – ie, where they genuinely do business – will have the right to tax a bigger share of the corporation’s excess profit at local corporate tax rates than countries where the corporation only exists as rented mailboxes for profit shifting purposes. This method of taxing global profit is known as unitary tax.

Tax losses by regions and income groups:

Region or group

Total tax loss

Tax loss to corporate abuse

Tax loss to private abuse

Equivalent health budget

Equivalent nurses’ salaries

World

$427,782,662,532

$244,903,619,563

$182,875,735,367

9.22%

33,913,688 nurses

Higher income

$382,744,587,716

$202,166,248,454

$180,575,939,262

8.41%

16,289,176 nurses

Lower income

$45,021,135,653

$42,737,371,109

$2,282,856,942

52.36%

17,623,965 nurses

Africa

$25,775,160,683

$23,242,133,255

$2,532,717,666

52.46%

10,130,883 nurses

Asia

$73,372,803,475

$46,190,152,354

$27,182,053,281

6.48%

11,371,221 nurses

Caribbean/ American Isl.

$1,429,594,178

$642,376,849

$784,817,330

12.41%

182,632 nurses

Europe

$184,087,359,433

$79,529,965,976

$104,557,393,457

12.58%

4,636,180 nurses

Latin America

$43,111,038,773

$40,123,746,097

$2,987,292,676

20.41%

6,225,731 nurses

Northern America

$95,099,311,659

$52,551,805,288

$42,547,506,371

5.70%

1,252,972 nurses

Oceania

$4,907,394,330

$2,623,439,745

$2,283,954,586

4.79%

114,069 nurses

Tax losses inflicted on others by regions and income groups:

Region

Total inflicted tax loss

Inflicted tax loss due to corporate abuse

Inflicted tax loss due to private abuse

Share of global tax loss responsible for

Higher income

$419,574,170,899

$237,340,746,418

$182,233,424,481

98.08%

Lower income

$8,209,131,410

$7,567,170,747

$641,960,663

1.92%

Africa

$4,739,131,071

$3,582,718,497

$1,156,412,575

1.11%

Asia

$76,216,744,183

$67,520,067,437

$8,696,676,746

17.82%

Caribbean/ American Isl.

$115,808,151,640

$58,123,586,045

$57,684,565,595

27.07%

Europe

$187,962,465,805

$99,803,107,457

$88,159,358,348

43.94%

Latin America

$5,536,878,049

$3,447,622,190

$2,089,255,859

1.29%

Northern America

$31,497,411,993

$7,557,038,524

$23,940,373,469

7.36%

Oceania

$6,022,862,769

$4,873,777,015

$1,149,085,754

1.41%

Top 15 countries most responsible for global tax losses:

Country

Tax loss inflicted on other countries

Tax loss inflicted by enabling corporate tax abuse

Tax loss inflicted by enabling private tax evasion

Share of global tax loss responsible for

Cayman Islands

$70,441,676,611

$22,819,899,267

$47,621,777,344

16.47%

United Kingdom

$42,464,646,560

$13,671,390,701

$28,793,255,859

9.93%

Netherlands

$36,371,503,832

$26,593,707,934

$9,777,795,898

8.50%

Luxembourg

$27,607,634,145

$9,283,427,114

$18,324,207,031

6.45%

United States

$23,635,935,547

$0

$23,635,935,547

5.53%

Hong Kong

$21,047,358,012

$16,331,010,356

$4,716,347,656

4.92%

China

$20,045,803,268

$20,045,803,268

$0

4.69%

British Virgin Islands

$16,295,774,429

$10,405,615,250

$5,890,159,180

3.81%

Ireland

$15,830,940,779

$6,068,846,053

$9,762,094,727

3.70%

Singapore

$14,633,842,974

$12,221,060,747

$2,412,782,227

3.42%

Bermuda

$13,843,144,682

$10,860,143,218

$2,983,001,465

3.24%

Switzerland

$12,844,985,635

$10,953,644,082

$1,891,341,553

3.00%

Puerto Rico

$9,177,305,410

$9,177,305,410

N/A

2.15%

Jersey

$7,911,160,368

$4,465,999,479

$3,445,160,889

1.85%

About the Tax Justice Network

The Tax Justice Network believes a fair world, where everyone has the opportunities to lead a meaningful and fulfilling life, can only be built on a fair code of tax, where we each pitch in our fair share for the society we all want. Our tax systems, gripped by powerful corporations, have been programmed to prioritise the desires of the wealthiest corporations and individuals over the needs of everybody else. The Tax Justice Network is fighting to repair this injustice. Every day, we equip people and governments everywhere with the information and tools they need to reprogramme their tax systems to work for everyone.

About Public Services International

Public Services International is a Global Union Federation of more than 700 trade unions representing 30 million workers in 154 countries. We bring their voices to the UN, ILO, WHO and other regional and global organisations. We defend trade union and workers’ rights and fight for universal access to quality public services.

About the Global Alliance for Tax Justice

The Global Alliance for Tax Justice is a growing movement of civil society organisations and activists, united in campaigning for greater transparency, democratic oversight and redistribution of wealth in national and global tax systems. We comprise the five regional tax justice networks of Africa, Latin America, Asia, North America and Europe, which collectively represent hundreds of organisations.

Produced and hosted by Naomi Fowler of the Tax Justice Network

This is what I can’t tolerate anymore, the lies by these people that all day long are talking about free speech and the fight against corruption. This cannot continue. Every story we are looking at now today in the Arab world will have a connection to one of those safe havens, and God knows how can you find the real owners if every jurisdiction says, sorry, we can’t give out any data, helping people that should be exposed. You know, your country and US and all these offshores are providing all the secrecy and the ability to shield the beneficial ownerships and the structures of these companies.”

~ Rana Sabbagh, OCCRP, the Organised Crime and Corruption Reporting Project and founder of the Arab Reporters for Investigative Journalism

It is not okay anymore in 2020 to own a business, to own a ship that you have deliberately hidden the ownership of through hugely complicated structures to either avoid tax or minimise your tax liability or reduce your safety standards.”

~ Thom Townsend, Open Ownership

Joe Biden and his team must address the colossal power of the corporate world, which after decades of mergers and acquisitions has become super concentrated into the hands of monopoly corporations in virtually all sectors…it ranks alongside all the other huge priorities facing the incoming administration, including climate crisis and tackling inequality and restoring trust in democracy.”

~ John Christensen, Tax Justice Network

Want to download and listen on the go? Download onto your phone or hand held device by clicking here.

Further Reading:

A Hidden Tycoon, African Explosives, and a Loan from a Notorious Bank: Questionable Connections Surround Beirut Explosion Shipment, OCCRP coverage

Beirut blast: a night of horror, captured by its victims

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher etc. Please leave us feedback and encourage others to listen!

Join us on facebook and get our blogs into your feed.

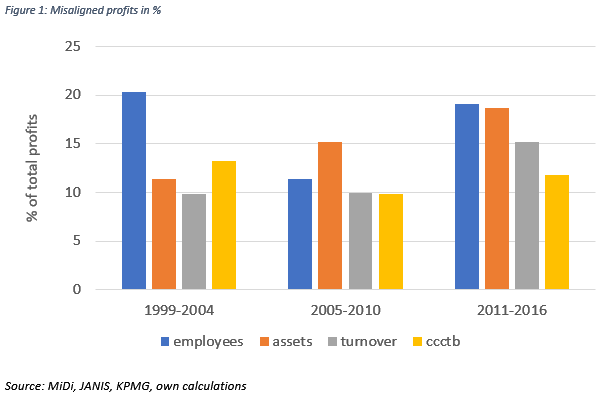

Despite numerous data challenges, economists have established that the multinational corporations’ reported profits are not well aligned with their economic activity across countries. However, uncertainties remain about the extent and patterns of this misalignment. In our recently published research article with Petr Janský, we analyse data on German-based multinational corporations and their foreign affiliates collected by the Deutsche Bundesbank. We find that the world’s tax havens attract a considerably higher share of German multinational corporations’ profit than economic activity, while in Eastern European countries, most developing countries and some big European countries reported profits are much lower than economic activity would suggest.

How do we measure corporate profit misalignment?

The term ‘misaligned profit’ describes the share of profits reported in a country that is not in line with the share of economic activity reported in the respective country. We compute each country’s share in the total profits of the sample and compare it to each country’s share in total economic activity measured in terms of number of employees, tangible and intangible assets, and turnover. We also use a measure of activity (‘CCCTB’) which is weighted one-third tangible and intangible assets, one third turnover and one-third number of employees. This is similar to the formula proposed by the European Commission for the Common Consolidated Corporate Tax Base (CCCTB). However, due to data limitations our CCCTB measure does not exactly correspond to the European Commission’s proposal. For example, we cannot split the factor ‘employees’ between remuneration costs and number of employees and we cannot distinguish between tangible and intangible assets in our data.

If actual profits are higher than what would be estimated based on the share of economic activity, this gives rise to ‘excess’ profit. If actual profits are lower than what would be estimated based on economic activity, this gives rise to ‘missing profit’. In order to measure the overall scale of misalignment, we compute how much profit is in the ‘wrong’ place by adding up the “excess profit” of jurisdictions where there is no concomitant economic activity.

For our analysis, we use data collected by the Deutsche Bundesbank, which include confidential data on foreign direct investments from the Microdatabase Direct Investment (MiDi) and a combination of confidential and publicly available balance sheet data from the JANIS database. Our main sample includes on average 1236 German parent companies per year with 5047 foreign affiliates in 178 jurisdictions for the years 1999-2016. About 60 per cent of observations stem from the manufacturing sector, and about 30 per centfrom the service industries.

How large is the misalignment of reported profits and economic activity in total and by country?

Figure 1 depicts the share of global profits that would need to be reported in other jurisdictions in order to be aligned with economic activity on average for the years 1999-2004, 2005-2010, and 2011-2016.

We find that the scale of misalignment varies depending on the factor that we use to proxy economic activity. Global profit misalignment has risen when measured in terms of assets and turnover but not in terms of employees. When we look at the yellow column which combines of all three factors, we see no clear trend of the scale of misalignment. It has rather remained stable over time at about 10 to 13 per cent of total reported profits.

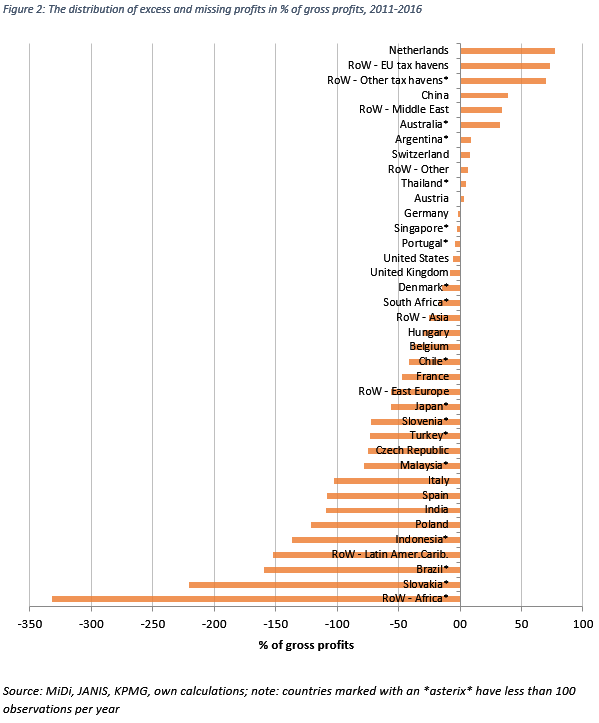

When we look at the distribution of misalignment across countries, our results are broadly in line with the literature: High-tax countries and most developing countries are missing-profit countries, while the world’s tax havens attract a considerably higher share of profits than economic activity. The Netherlands are the most notable example with about 80 per cent of reported profits being misaligned with economic activity, closely followed by the other tax havens which had to be grouped together due to the confidentiality requirements. Interestingly, the remaining EU tax havens are still more important for German MNCs than the rest of the world’s tax havens. The other excess-profit countries are mostly resource-rich countries from the Middle East, Australia and Argentina. The classification of China as an excess-profit country is puzzling. It might be explained by the exceptional combination of low cost of labour and capital combined with increasingly high value-added activities which we cannot control for in our approach. Another surprising result is the classification of all Eastern European countries as missing-profit countries despite their very low corporate tax rates.

Our results do not allow for a clear classification of Germany as an excess or missing-profit country. This is because the relative weight of misalignment is relatively low (only 2 per cent of total gross profits according to figure 2) and outcomes are not consistent over time, differ by activity factor and by the tax rate measure we use in order to compute the pre-tax profits. This is surprising as many studies find that multinational corporations shift profits out of Germany which would be consistent with Germany being a missing-profit country. However, note that we explicitly analyse a sample of German parent companies which does not include the German-based affiliates of foreign mutlinationals. Our results might thus be in line with a headquarter bias in profit shifting, in the sense that parent companies rather shift profits in between affiliates in order to minimize their global tax payments but do not necessarily shift profits out of headquarters or do so to a lesser extent. This would be in line with the results by other researchers who find that European multinational corporations are reluctant to shift profits away from their headquarters.

Our data suffers from several limitations. There is a lack of data on pre-tax profits and compensation of employees of foreign affiliates. As mentioned before, we are not able to distinguish between tangible and intangible assets which probably leads to an underestimation of misalignment. Further, our sample might not be representative of the whole population of German-based MNCs. Still, we think that – in the absence of representative data on MNCs and in particular on domestic MNCs – researchers can combine information from different pieces of data as a second best.

Conclusion

We analyse a sample of German-based parent companies and their foreign affiliates and find that about 10 to 13 per cent of reported profits are misaligned with economic activity. The distribution of „missing“ and „excess“ profits follows typical patterns: We find greater profits than activity reported in tax havens, and less profits than activity in developing countries, big high-tax countries and in all Eastern European countries despite their very low tax rates. Our results do not provide an indication of excessive profit shifing from German-based parent companies to their foreign affiliates but would be consistent with significant profit shifting activities between affiliates. This might indicate that foreign affiliates are more relevant in multinationals‘ strategies of tax minimisation. Due to our descriptive approach, we are not able to attribute the observed extent of misalignment to particular reasons. Profit shifting is only one of several possible explanations. Still, the outstanding role of the world’s tax havens in our sample points in this direction and thus requires further explanation.

The Transnational Institute has just published a report setting out ten proposals to mobilise resources to cover the cost of the global COVID-19 pandemic and to pay for the transition away from the fossil fuel economy. As the report points out in its conclusion, the multiple crises facing both the global North and the global South have shifted the Overton window of what is economically feasible. And as the report also makes clear, the means for building back better are readily available provided governments are prepared to take bold measures to, for example, tax wealth and corporate profits, reform fossil fuel subsidies, tax carbon, cancel debt, and achieve the UN sustainable development goals.

On the expenditure side the report identifies six priority areas of what might, in the words of economist Jayati Ghosh, shape “a global multicoloured new deal: red, green and purple.” These expenditures are summarised as follows:

To resource these expenditures TNI identifies ten proposals, most if not all of which will be familiar to readers of this blog, including a global wealth tax; a tax on income from wealth held through offshore structures; an excess profits tax; reforming corporate income tax; a financial transactions tax; removing fossil fuel subsidies, and so on. As the diagram below suggests, the potential revenues from these proposals are more than sufficient to pay for the expenditures identified above:

The core message of this report is that the gravity of the multiple crises facing humanity requires entirely new economic, political and cultural models that place care for humans, and for planetary life, above the pursuit of profit. If we are to meet the challenge of building back better, the resources to achieve this better future are to hand – “so long as the rich and powerful are made to pay”.

This new paper describes why beneficial ownership regulations shouldn’t exempt companies listed on a stock exchange. Securities’ disclosure regulations are not adequate for identifying beneficial owners. In addition, definitions are subject to loopholes that affect identifying all relevant end-investors.

As assessed by the Tax Justice Network’s Financial Secrecy Index and summarised by our paper on the 2020 State of Play of Beneficial Ownership Registration, more than 81 jurisdictions have approved laws requiring beneficial ownership to be registered with a government authority. However, many legal frameworks (including the EU Anti-Money Laundering Directive) exempt listed companies from the scope of beneficial ownership registration, based on what we consider to be a wrong interpretation of the Financial Action Task Force recommendations.

The exemption benefitting listed companies is usually based on the fact that some other regulator, eg the securities or financial regulator or the stock exchange, is supposed to already have that information. However, this brief looks at securities regulations available in some countries, eg the US and the UK, showing that securities regulation doesn’t necessarily cover beneficial ownership information.

In the case of the US, the Securities Exchange Commission (SEC) has form 13D which is even called “beneficial ownership report”. However, it doesn’t necessarily refer to a natural person (which is the key element of the beneficial ownership concept according to the Financial Action Task Force and the OECD’s Global Forum).

Other countries, eg Ecuador, India and the Philippines do cover natural persons when requiring listed companies to identify their beneficial owners. Nevertheless, thresholds are too high to be able to identify all relevant investors.

This brief explains why we need a comprehensive approach to beneficial ownership registration to ensure that all legal vehicles, including those involved in passive investments, are subject to proper transparency. The brief also proposes measures to address the challenges, including our previous paper on the secrecy that surrounds listed companies and investment funds.

The United States has long relied on informal agreements with private sector institutions to assert its interests in the global financial system. If we are to fight kleptocracy, we need to make this privately run plumbing more accountable to international institutions, argues Edoardo Saravallein this blog reproduced from a recent edition of Tax Justice Focus.

Getting a Grip on Global Financial Infrastructure

Edoardo Saravalle

When President Trump defied the international community and left the Iran nuclear deal in 2018, he had an unlikely partner: the Society for Worldwide Interbank Financial Telecommunication (SWIFT). The Belgian SWIFT provides the payments-messaging services that, in the words of Federal Reserve Chairman Ben Bernanke, are ‘part of almost every international money transfer.’[1] So when SWIFT decided to ban certain Iranian banks from its services—over the protests of European governments—it packed a major punch to Tehran’s economy.

Today, privately-controlled financial nodes like SWIFT are regular partners of U.S. foreign policy. This may soon change. As Washington focuses more on transnational economic threats like kleptocracy and tax evasion, infrastructure providers may consider their economic self-interest before eagerly cooperating. Public-private partnerships are a shaky foundation for U.S. foreign policy, and the United States should not let private actors control the plumbing of the international economy. Instead, it should seek global cooperation to create a better system.

SWIFT is just one of the services that make up the international economy’s plumbing. To make metals trading easier, there is the London Metal Exchange (LME) that enables futures trading and licenses warehouses around the world. To ensure the smooth payment and tracking of securities, there are Clearstream and Euroclear. To make investing in emerging markets easier, J.P. Morgan created the Emerging Market Bond Index which brings together securities across a wide swath of countries. And the London Inter-bank Offering Rate (LIBOR), a changing interest rate based on a survey of bank employees, is calculated to ensure adjustable interest rates that mirror market conditions.

These ‘infrastructures’ started as ways to make commerce easier, then became central to the functioning of global finance, and now are key components of U.S. power. The SWIFT threat is one of the strongest weapons in the U.S. economic arsenal. Even major players like Russia and China have come to fear a cut-off. But SWIFT is not alone. The LME magnified the effect of U.S. sanctions against Russian aluminum producer Rusal by suspending the company from its exchanges. Clearstream has blocked Iranian and Russian assets, and J.P. Morgan zeroed out Venezuela in its bond index, restricting capital flows to the country.

While these infrastructures do promote U.S. foreign policy, they further a limited vision of it: one where Washington enforces norms and goals against specific countries. But U.S. foreign policy is changing. During his campaign, Vice President Biden has promised a ‘foreign policy for the middle class,’[2] one that unites foreign and domestic goals, that combines economic and security goals, and that targets tax havens and corruption as ‘drivers of inequality.’[3] This would mean taking on a world where 8 percent of global household wealth hides in tax havens.

International financial infrastructures should be great partners in tackling these transnational problems. What better way to monitor and check international flows of money between shady jurisdictions than networks like SWIFT or ClearStream that make these flows possible? The NGO Tax Justice Network has called for ‘SWIFT statistics for all’ to track financial flows and tax evasion, and Georgetown Professor Stefan Eich has argued SWIFT contains an ‘an untapped utopian promise’ of ‘global monetary and financial regulation’ due to the fact that all financial transactions need to flow through it.[4]

However, past cracks in U.S. cooperation with infrastructures suggest that leveraging these privately-controlled choke points might not be so easy. First, these nodes did not help Washington out of altruism. It took years of fines and enforcement by the United States to ensure cooperation. Clearstream paid $152 million in fines over allegations that it held $2.8 billion in securities for the Central Bank of Iran. The board of SWIFT is made up of representatives for the world’s largest financial institutions, so it faced two layers of threats: enforcement against the board-member banks and against the company itself. This danger presented itself in 2018, when Iran hawks outlined the option of sanctioning member banks if SWIFT did not ban the Iranian banks.

Even more pressure will be necessary in the future. Faced with these legal costs and compliance headaches, the infrastructures limited their risk by cutting off Iran. The countries that enable tax evasion, though, are far more plugged into the global financial system. It will be harder for enforcement actions to convince infrastructures to cut off or pressure these countries or banks. Prosecutors’ nerve may fail before taking on major European jurisdictions, and U.S. policymakers may choose transatlantic conciliation over more friction regarding tax enforcement. Plus, it will be harder to count on the self-interest of the private sector: their financial interests will be far more at stake with tax havens compared to Iran.

Furthermore, successful coercion by the U.S. might not ensure consistent cooperation from these infrastructures. In the past, they have gone along with U.S. requests while also furthering other competing agendas. British banking giant HSBC has frozen the account of a Hong Kong pro-democracy activist and has come under fire, along with British bank Standard Chartered, for backing the region’s controversial national security law. These banks have acted even as U.S. sanctions forced financial services firms to cut ties with pro-mainland Hong Kong government figures.

In one extreme case these infrastructures enabled non-state actors to assert themselves over sovereign governments. Bond servicing infrastructures enabled hedge funds to enforce their will over the government of Argentina. Facing a court order, Buenos Aires discovered that it could not pay all other bondholders through the traditional payment infrastructures as long as it refused to pay the hedge funds.

Privately-controlled infrastructures’ cooperation with competing agendas could harm U.S. anti-kleptocracy and anti-evasion goals. Countries that currently benefit from tax evasion and the unfair financial architecture of the global economy, whether by offering exceedingly low tax rates or allowing owners of ill-gotten wealth to shield their identities, would fight these U.S. measures and try to sway the infrastructure providers. In the past, countries have protested, refused to cooperate, and (often rightly so) complained about U.S. hypocrisy. In 2014, the United Kingdom opposed Russia sanctions that would have harmed its financial sector and spearheaded efforts to build a relationship with Chinese finance. Still, in most of these cases, U.S. threats have convinced recalcitrant countries.

A transnational anti-evasion and anti-kleptocracy campaign would run into a new problem as well. The success of such an effort would depend on its ability to sway the private sector—giving added influence to the same entities it is trying to coerce. While a SWIFT board member or a securities processor is agnostic about Iran policy, as long as it does not have economic interests in play, it will have strong thoughts about continuing to serve the world’s wealthiest citizens—and in keeping its own tax rate low. This will make it more appealing for these infrastructures to form coalitions with like-minded countries bent on protecting their privileges in today’s unfair global financial system.

Finally, these privately-run infrastructures can be outright corrupt, so even if they were to cooperate they would be unsteady partners. The LIBOR scandal makes this danger clearest. The LIBOR is a number that is central to the functioning of global credit markets. Lenders adjust the rates they offer borrowers based on LIBOR. According to the New York Federal Reserve Board, there are about $1.3 trillion in consumer loans and $5.2 trillion in corporate loans and bonds based on LIBOR.[5] The number, soon to be shelved in light of its legal problems, shifts daily based on surveys of bankers. Following a major investigation, the U.S. Department of Justice and the U.S. Commodity Futures Trading Commission found that traders were cooperating to game these surveys. They would adjust their responses in order to make money on their positions. In the process, they shaped the cost of borrowing for borrowers all over the world. The LIBOR case highlights the underlying peculiarity of the infrastructures: though they are faceless and globally influential, they are usually made up of just a few players who can tilt the playing field. The incentive to tilt the field toward the private sector would be even more pronounced in this new foreign policy context.

Washington should not fight kleptocracy and tax evasion on such an unstable foundation. It should not rely on private partners that require constant coercion, that work with countries and private interests with competing agendas, and that allow corruption. Instead, Washington should ensure supranational control of these infrastructures so that they respond to the goals and wishes of the international community.

Turning the infrastructures of global finance into international organizations will have its costs. Today, sanctions often allow Washington to gets what it wants quickly and unilaterally, avoiding the diplomatic headaches that come with multi-lateral decision making. And indeed, making bond-servicing or payment processing plumbing the joint responsibility of international governments might entail more of the gridlock and international squabbling associated with the United Nations and other international organizations.

Still, this would be a far-sighted plan for the United States. States should not delegate key nodes of the global economy to private actors with their own agendas, particularly as they undermine states’ goals. As the undercutting of pro-democracy activists in Hong Kong suggests, private organizations can be untrustworthy partners. As the power-politics of the global financial system evolve, the United States might lose its uncontested influence as infrastructures hedge their bets by appeasing other countries. International control would therefore bring realpolitik as well as moral benefits.

As long as states are in charge, Washington will have a seat at the table. From this seat, it will be able to carry out a far-reaching and innovative foreign policy aimed at righting an unfair financial system. Internationally-controlled financial infrastructures will ensure that it is public goals, not private interests, that set the agenda.

Edoardo Saravalle is a former researcher at the Center for a New American Security. This article was first published in The American Interest on September 4, 2020.

[1] ‘Highlights: Bernanke’s Q&A testimony to House panel’, Reuters, February 29, 2012

[2] Joseph Biden, ‘Why America Must Lead Again’, Foreign Affairs, March/April 2020

[3] Jake Sullivan, ‘What Donald Trump and Dick Cheney Got Wrong About America’, The Atlantic, January/February 2019

[4] Stefan Eich, ‘SWIFT: A Modest Proposal’, The Nation, October 17, 2018

[5] ‘Second Report: The Alternative Reference Rates Committee’, Federal Reserve Bank of New York, March, 2018

The FinCen files leak disclosed information on “suspicious transaction reports” filed by banks between 2000 and 2017 to the US Financial Intelligence Unit (“FinCen”) in charge of monitoring anti-money laundering.

Although a lot could be said about this leak, there are many outrageous highlights: the leak refers to transactions of $2 trillion (twelve zeros: $2,000,000,000,000). Some banks kept on processing transactions on an account despite several red flags. And the worst part is it appears that both banks and regulators consider that to comply with the law and prevent risky transactions it’s enough just to file suspicious transaction reports, regardless of their quality or timing. That’s like saying that a company is complying with regulations on beneficial ownership registration even if they registered “Mickey Mouse” as the beneficial owner.

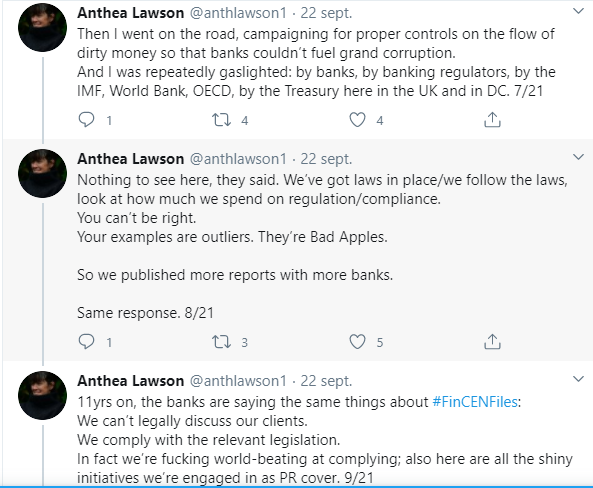

But no one is surprised. As described by anti-corruption campaigner Anthea Lawson:

If banks are sometimes complying, and many times only formally “complying” (by filing low-quality or outdated suspicious transaction reports), but money laundering schemes keep popping up (Azerbaijani Laundromat, Moldova Laundromat, Danske Bank, etc.), it’s quite clear that money laundering isn’t being prevented (and even when it’s discovered, it’s very hard to recover any of the money). It’s clear that the system is part of the problem. David Lewis, the Executive Secretary of the main international body in charge of anti-money laundering regulation, the Financial Action Task Force (FATF), confirms this. As reported by the International Consortium of Investigative Journalists (ICIJ):

Although most countries now have dedicated laws and regulations to combat money laundering, Lewis said: “they are rarely being used effectively, or to the extent that we would expect….

‘I would sum up the results as ‘everyone is doing badly, but some are doing less badly than others,’ Lewis said…

Lewis said many countries had only shown a last-minute commitment to tackling money laundering because they faced an upcoming FATF evaluation. “You see a sudden uptick in money laundering investigations and activity as they prepare to compensate for [past inaction], or to tell a good story to the assessors,” he explained.

As Lewis suggests, part of the problem may be on enforcing current laws.

However, ensuring governments properly resource authorities tackling financial crimes, given countries’ lack of interest or their need to face with multiple challenges, including urgent matters (eg Covid-19), is a long shot. The question is how serious governments really are about tackling corruption and money laundering, as the Hudson Institute and Kleptocracy Initiative’s Nate Sibley tweeted:

Before dunking on FinCEN, remember the tiny agency tasked—effectively—with policing the integrity of the global financial system has an annual budget of just $120 million. That’s less than the US government accidentally sends in benefits to dead federal employees each year.”

This blog post has some ideas on what we think should happen to improve the system without merely hoping that current laws will one day be enforced. Of course, part of the problem would be solved if banks and other enablers directly involved with customers and their money were to do a proper job. This would require going beyond asking customers for information and just believing everything they say. After all, a lawyer from Cyprus may (legally) be the beneficial owner of an entity that opened a bank account, but that doesn’t explain the source of the funds, let alone why millions of dollars are being channelled through that account. Banks are already required to apply enhanced due diligence and other measures if they have suspicions, so this is a matter of enforcement.

This blog post proposes new objective measures that would help different players obtain information while discouraging illegal schemes. To put this in perspective, a regulation could say “check that the customer isn’t lying”. While this is a matter of effort and enforcement, our proposed measures neither contradict nor modify that main goal, but try to impose new provisions – for example – “ask for a copy of their ID” which may be easier to enforce or at least to monitor, than the rather general goal of ‘detecting lies’.

First, countries should apply these things, which we’ve been calling for for years:

A: Availability of relevant ownership data

Beneficial ownership of account holders: Banks should not be allowed to open accounts, hold them or do any transaction if they haven’t determined the beneficial owner of the account holder (beyond doubt). Ideally, determining the beneficial owner of an account should go beyond asking for corporate information proving that ‘John’ is the beneficial owner because he is the shareholder of Company A, which opened the bank account. Banks should try to determine whether John is really benefitting, controlling and able to justify the source of funds and the movement of money through that account.

SWIFT messages with beneficial ownership data. The SWIFT messaging standard used to communicate international bank transfers among banks should be upgraded to require data on the beneficial owner of the sender and recipient account to be included in the SWIFT message, to enable the sending bank, the recipient and any intermediary (eg correspondent bank) to run proper customer due diligence checks. We have written more on this in this blog post. Alternatively, until SWIFT upgrades its standard to add beneficial ownership data, correspondent banks should require beneficial ownership data from any sending and recipient bank before they allow a transaction to take place.

Just as the US obliged SWIFT to hand in information for anti-terrorism purposes, the US and the EU should now require SWIFT to upgrade the standard to include beneficial ownership data. As discussed in point 9 below, the US and the EU could also require all local banks which are members of SWIFT to request that SWIFT upgrades the standard in this way.

3. Public beneficial ownership registries: Governments should make beneficial ownership information publicly available in open data format for all types of legal vehicles, including trusts, so that banks all over the world may cross-check the beneficial ownership information declared by their customers.

5. Involvement of banks in verifying registered beneficial ownership data: Banks (and enablers in general) should report discrepancies between the information declared by their customers and the information contained in beneficial ownership registries, as already required under the EU Anti-Money Laundering Directive.

6. Banks detecting discrepancies amongst each other: In addition to banks reporting discrepancies to the beneficial ownership register, they should be able to exchange customer information in a confidential way so they can detect cases where the same customer has given inconsistent information to two different banks. The UK’s financial intelligence unit (FCA) has been working on pilots for this purpose. If mismatches are detected and persist beyond mere simple errors, authorities should automatically be required to investigate.

7. Beneficial ownership registries as sources of compliant customers: Beneficial ownership registries should warn users about any legal vehicle (eg company, trust) with redflags, for example if a vehicle failed to register or update information, if its information doesn’t match other government databases, or if discrepancies have been reported. Banks shouldn’t be allowed to operate (open an account or do a transaction) with any entity marked with a redflag warning on the beneficial ownership register. We described how this could work in the Annex of our paper on beneficial ownership verification.

C: The specific role of bank

8. Systematic analysis to detect money laundering: As presented by Howard Cooper and Chris Ives from Kroll, banks should do much more than just ask information from each customer and analyse transactions on an isolated basis. Instead, they should analyse their full customer base to detect cases of connections between apparently unrelated customers. For instance, customers who share the same legal owners, beneficial owners, director, power of attorney, addresses, IP address, or whose transactions are highly related (either because they mirror each other or because transactions only take place among the same accounts). This has been described further here.

9. SWIFT as a source or centralisation of global anti-money laundering detection: While banks should do more systematic analyses of their customer base and transactions (see point above), this will only detect transactions involving each particular bank. However, money laundering schemes may involve many banks from many countries. For this reason, we have proposed that SWIFT, which already provides money-laundering services to some banks, should help detect or red-flag global money laundering schemes. Alternatively, if SWIFT is unable or unwilling to do this, governments should oblige SWIFT to hand over raw data for the Central Banks or financial intelligence units to conduct those checks, just as SWIFT provides transaction data to the US for the detection and prevention of terrorism.

If SWIFT refuses to do this claiming that it can only implement changes based on what its member banks require, the solution may be for each government to demand any local bank (that is a member of SWIFT) to require SWIFT to implement this centralisation and monitoring work (as well as to update the SWIFT system to include beneficial ownership data, as mentioned in point 2 above).

A first partial solution would be for banks to report all of their transactions on a daily basis to a government authority, eg the Central Bank or the Financial Intelligence Unit, so that analyses can be run at the national level. This wouldn’t be as good as centralising and analysing information at the global level, but it would be a very good start. For instance, banks in Australia must report the equivalent of SWIFT data for every international bank transfer to a central authority.

Now some new ideas we haven’t discussed before:

10. Checking the ownership chain up to the beneficial owner. Banks should refrain from opening accounts unless they can directly check the ownership of every entity integrating the ownership chain of the customer, in the corresponding commercial register. For instance, if the customer is Company A from the UK, owned by Company B from Delaware and allegedly owned by John, a bank should be able to obtain legal ownership information from the registries available in the UK and the US to confirm that John is the beneficial owner. If any of the country links fails to provide this information, the bank shouldn’t open the bank account, regardless of the information self-reported by the customer. This would put pressure on jurisdictions to establish public registries of legal ownership and beneficial ownership.