Published:

12 March 2018Reading time:

3 minOn February 19th, the OECD launched a consultation entitled “Preventing abuse of residence by investment schemes to circumvent the CRS”. It was about time. Since 2014, we have written several papers and blogs (here, here, here, here and here) explaining how residency and citizenship schemes offered by countries can be abused to avoid automatic exchange of bank account information established by the OECD’s Common Reporting Standard (CRS).

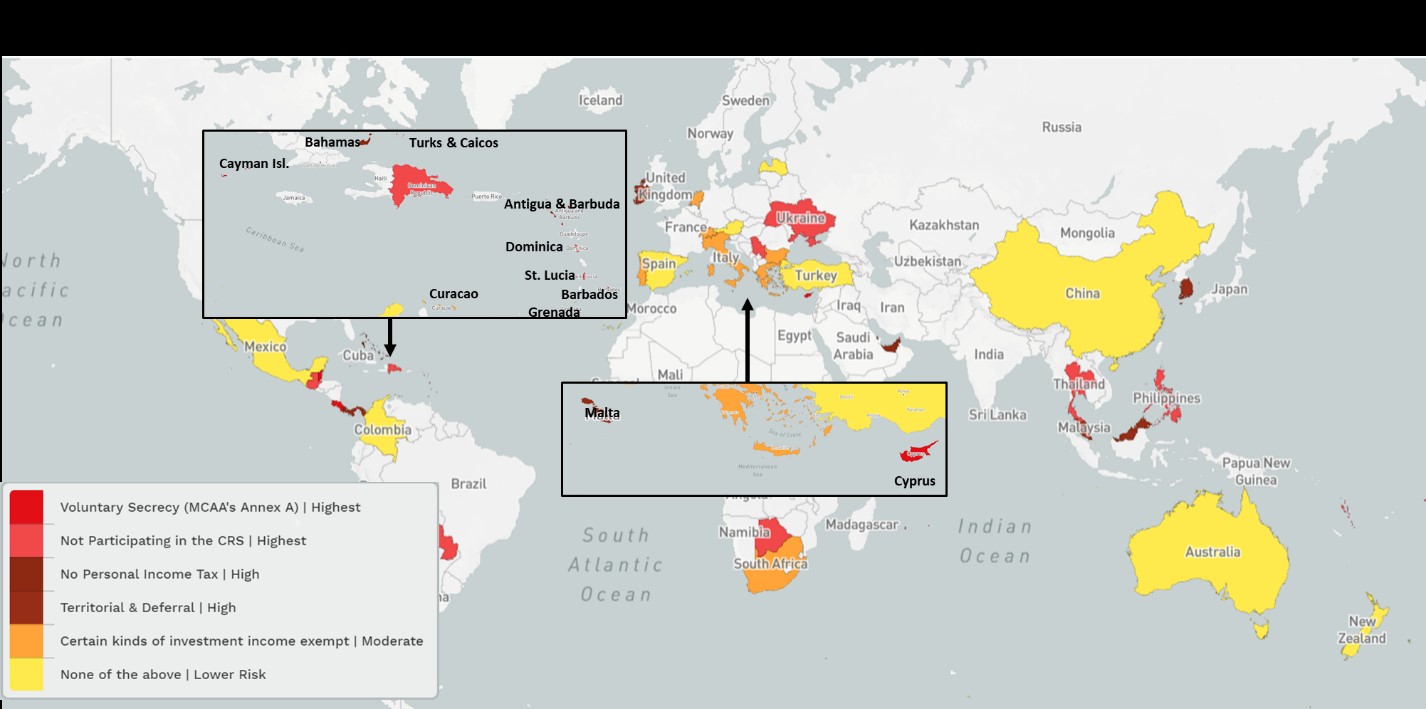

Today, we publish this brief report by myself Andres Knobel and Frederik Heitmüller with the list of countries presenting the highest risk to be abused for avoiding the CRS.

Image based on a map created by 23degrees.io

How does this work? In short, the CRS requires banks and other financial institutions to determine the residence of their account holders, so that their banking information will be sent to the corresponding country (where the account holder actually resides) so that authorities can check if the person has declared the foreign bank account and paid relevant taxes. However, if the account holder manages to trick the bank by pretending to be resident in another country, their banking information will be sent to the wrong country, or it might not be sent at all. Citizenship and residency by investment schemes can be abused for this precise purpose. An account holder may acquire one of these citizenships or residencies in exchange for money, not to migrate to another country, but only to trick their foreign banks about where they actually live.

TJN’s Financial Secrecy Index published last January assessed this under indicator 12. Based on this research, we now present a list with all jurisdictions offering residency or citizenship by investment schemes, considering their level of risk. For example, residencies or citizenships offered by countries who are not participating in the CRS or who have chosen “voluntary secrecy” (to send, but not to receive information under the CRS), present the highest risk because any person who is (determined by the bank to be) resident in one of these countries will become “non-reportable”: their banking information will not even be collected, let alone exchanged with other countries for CRS purposes.

You may be surprised to see that there’s one country missing from the list: the U.S. In principle, the U.S. should be included. After all, it has a residency by investment scheme offering green cards in exchange for USD 500.000, and the U.S. is not participating in the CRS. However, the U.S. is a major risk (probably the greatest) to the CRS, not because of its residency scheme, but because of its lack of participation in the CRS altogether.

Using the U.S. residency scheme to avoid CRS reporting is unlikely because anyone holding a green card would be considered reportable under the U.S. FATCA framework (the U.S. equivalent of the CRS). This doesn’t mean that the U.S. poses no risks for avoiding the CRS. On the contrary. While the U.S. residency scheme is unlikely to be used to avoid the CRS, a much cheaper option is offered: any individual can simply hold their money in U.S. banks and this way avoid the CRS altogether (given that the U.S. is not a participating jurisdiction, U.S. banks will not exchange any information pursuant to the CRS). The U.S. may still exchange information about non-resident account holders if it has a FATCA-based inter-governmental agreement with the country where the account holder is resident. However, since the U.S. will not send information to other countries at the beneficial ownership level, any individual could avoid being reported both under the CRS and under FATCA if he/she holds money in U.S. banks through an entity (not in their own name; see here and here for more details).

In other words, the U.S. represents a major risk to the CRS, not because of its residency by investment scheme, but because of its refusal to join the CRS or to exchange with other countries as much information as it receives from them under FATCA-based agreements.

The author

Related articles

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

Finally, the European Court of Justice cracks down on trusts

Financial secrecy has entered the EU AML rulebook. What comes next?