#27 Imposto de renda: empresas e ricos devem contribuir mais

Enquanto o mundo retoma o debate sobre a necessidade de taxar mais grandes empresas, e já tributa há anos a distribuição de lucros e dividendos, para distribuir a renda de uma forma mais justa, o Brasil segue na contramão, mesmo na recente proposta de reforma do imposto de renda.

“O local por excelência para lidar com a questão da desigualdade é a tributação de renda e patrimônio, em particular a tributação de renda.” – Rodrigo Orair, pesquisador e especialista em política fiscal, tributação e desigualdade

“Falar em queda de arrecadação no Brasil é muito complicado, porque vivemos uma crise fiscal expressiva e ao mesmo tempo precisamos garantir bens e serviços públicos e principalmente a proteção social para lidar com os efeitos da pandemia. Então, eu não vejo espaço fiscal para reduzir carga tributária no momento.” – Débora Freire, professora de economia da UFMG

“As grandes reformas da tributação não são feitas em momentos de paz e tranquilidade, mas em momentos de crise aguda. Nós temos uma janela de oportunidade histórica pra avançar efetivamente” – Paulo Gil Introini, diretor do Instituto de Justiça Fiscal.

Especialistas entrevistados no episódio #27 do É da sua conta defendemque grandes corporações e as pessoas mais ricas contribuam mais para que o país possa proteger sua economia, garantir direitos e reduzir desigualdades. Esses são também os objetivos de uma reforma tributária baseada em justiça fiscal.

Ouça no É da sua conta #27:

Mudanças no imposto de renda devem respeitar os princípios de direitos humanos para garanti-los e reduzir desigualdades

Detalhamento da proposta de reforma do imposto de renda em discussão no Brasil

Tributação de lucros e dividendos

Proposta para empresas contribuirem menos com o imposto de renda no Brasil na contramão da realidade internacional

Education provides the “foundations for individual autonomy, liberty and human dignity”. (1)

Yesterday marked the start of the Global Partnership for Education’s (GPE) two-day Summit, which is hosted by the Nigerian and UK governments. The Global Education Summit: Financing GPE 2021-2025, which you can join live (2:00pm BST), aims to explore “with key partners the role of education in the face of today’s key challenges”.

We’ll be listening carefully to the debates and most importantly the political commitments. Meaningful action is especially needed on two of the challenges to be explored in the Summit: financing education and advancing gender equality.

The Abidjan Principles underline states’ obligations to establish free, quality, public education systems for all. Public services, therefore, should be the central way in which governments support the realisation of the right to education, and thus open up lifelong opportunities in further education, training and access to paid employment. Access to education needs to be delivered consistently and sustainably. Schools and other centres of education along with the educators and support teams of carers, specialists, and technicians needed to operate them are critical to deliver the right to education. So too is the public transport and digital infrastructure to ensure all children have access to education.

Where resources are scarce, girls fare less well than boys in terms of opportunities and accessing education. This is because girls and women adult learners are disproportionately burdened by structural and systemic discrimination. Girls will be depended upon to undertake the burden of caring for others within the family and wider communities. Girls will also be expected to provide income to the household in many different ways including tending crops, small scale manufacturing, domestic labour and can become victims of trafficking.

Social and economic policies need to be dismantled and re-designed so that assumptions about the role of girls and the regressive impacts from the failure to fulfil the right to education are addressed in progressive public service policies. Policies, therefore, need to be effective instruments to ensure women and girls, in particular, enjoy the right to education. Social and economic policies need to ensure that women and girls have access to affordable digital services, to accessible public education services and to available social protections.

At the Tax Justice Network we approach the notion of sustainable financing for human rights, including the right to education, through our 4 R’s of tax:

Raising revenue progressively by broadening and deepening the tax base; redistributing income and wealth using taxation policy and so that those who have more contribute proportionately to their wealth and income; repricing market goods and services such as harmful tobacco good or carbon emissions, and strengthening the accountability of governments through the payment of taxes, which ultimately underpins the social contract and effective political representation.

The country profiles of our annual State of Tax Justice report, jointly published with the Global Alliance for Tax Justice and with Public Services International, report on the scale of revenue losses to cross-border tax abuse.

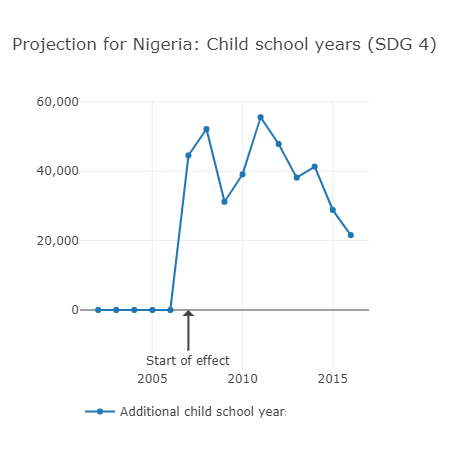

Consider the hosts of the GPE summit. Nigeria is estimated to lose US$10.8 billion a year, or 2.4% of the country’s GDP. For education, over a ten year period an increase in government revenue of 19.67% would be associated with 400,000 children receiving an extra year of education, or roughly 40,000 every year (2). With similarly dramatic losses projected in each other area of public services, it is unsurprising – but most welcome – that Nigeria has been at the forefront of demanding international progress against tax abuse. Nigeria is championing the important UN FACTI Panel recommendations for a new and fairer global architecture to fight illicit financial flows, for example, and standing against OECD proposals on corporate tax that would give the great bulk of new revenues to the richest countries.

The UK loses even more tax from corporate and individual tax abuse – an estimated US$10 billion lost to global tax abuse committed by multinational corporations, and nearly three times that to offshore tax abuse by individuals – roughly US$600 per person. As a high income country, however, the public financial constraint on access to affordable education in the UK is less binding when compared to lower income countries. And indeed, the UK’s losses are in no small part the result of the country’s deliberate strategy of positioning itself at the heart of a network of financial secrecy jurisdictions and corporate tax havens, the legacy of the British Empire. But that strategy means that the UK is responsible for imposing major revenue losses on other countries, with harsh impacts on the available resources for public services in lower-income countries – not least, public education.

The GPE Summit, continuing today, presents a real opportunity for governments, policy makers and a cross section of civil society groups to look hard at and address the financing of global education. As MaryJacob Okwuosa, National Coordinator at Activista Nigeria and Founder at Whisper To Humanity, said this week, “It is time for GPE to take tax seriously” and by implication the governments of the world. That seriousness must be reflected in an intersectional approach to substantive equality in education for girls and women learners.

The technical nature of tax issues may be seen or projected as problematic, but the decisions needed are political, and simple. The GPE should recognise explicitly that tax is the sustainable source of finance for public education, and lend its weight to international efforts to redress the global inequalities that face lower-income countries in exercising their taxing rights.

Sources: (1) Yoram Rabin, The Many Faces of the Right to Education, in D. Barak-Erez and A. Gross (eds), Exploring Social Rights Between Theory and Practice, 2007; (2) GRADE https://med.st-andrews.ac.uk/grade/research/

It’s been two weeks since our Annual Conference but the buzz and energy is still running through our heads and hearts. This year’s Annual Conference, the theme of which was Tax Justice and Human rights, was particularly special to many of us, not just because it marked a return after last year’s conference was cancelled due to the pandemic, but because it also exemplified the way in which tax justice over the past years has been widely adopted into so many spheres for social justice.

The conference launched a foundational report explaining the linkages between tax justice and human rights. In her Foreword, Irene Ovonji-Odida, Ugandan lawyer and women’s rights activist and also a member of both the High Level Panel on International Financial Accountability, Transparency and Integrity for Achieving the 2030 Agenda (FACTI Panel) and the Independent Commission for the Reform of International Corporate Taxation (ICRICT), explained how the report:

“navigates through some of the most salient issues and helps to map the alarming contours of the human rights impacts, [and]…at the centre of these abuses are high-income countries and their dependent territories, and the wide circles of tax and other professionals“

Supported and co-hosted by the Association of Accounting and Business Affairs (AABA); City University, London; and the Tax and Gender Working Group of the Global Alliance for Tax Justice (GATJ), this year’s conference fuelled an energy and a host of conversations which reflect the growth of influence of the global tax justice movement, and the credibility and relevance of tax justice positions for those advocating for human rights and ending inequalities.

The conference opened with Prof Prem Sikka from AABA, founding partner of the conference, Member of the UK House of Lords and Senior Adviser to the Tax Justice Network, presenting a shameful picture of the scale of wealth and income inequality in the UK. While a tiny minority of citizens in the UK are enabled to compound their wealth to obscene levels many, many more live in poverty. Prof Sikka was quick to point out this pattern of wealth and income inequality is one repeated in every country across the globe.

Prof. Sikka took the opportunity, as is tradition at our annual conference, to recognise and honour individuals who have worked to support and promote the work of tax justice. This year, awards were given to Cathy Cross a longstanding Board member of the Tax Justice Network and to James Henry, a Senior Adviser to the Tax Justice Network.

Prof Anastasia Nesvetailova of the Political Economy Research Centre at City University of London (CITYPERC) opened her remarks by noting that the Biden tax plan, whatever its faults and there is indeed much that has been critiqued, is a compliment to the work of the Tax Justice Network and a recognition of the importance of the tax justice movement’s campaigning and analysis. Jeannie Manipon, from Asian Peoples’ Movement on Debt and Development (APMDD) and representing the Tax and Gender Working Group, concluded the welcome address by drawing attention to the opportunities and imperatives for a transformative agenda which places people and the planet at the centre of the movement’s thinking and action. Jeannie echoed a key message from the report launched as the centrepiece of the conference: “Tax justice is, very simply, a feminist agenda.”

Philip Alston, Professor of Law at NYU Law and Chair of Center for Human Rights & Global Justice, and until recently the UN Special Rapporteur on extreme poverty and human rights, encouraged everyone to read the report, and called on civil society to grasp the interconnectedness of tax justice and human rights. The reality, Prof Alston warned, is that any progress civil society organisations make on their issues can and will be “undermined or overturned by changes in the tax system”.

Attiya Waris, Deputy Principal at CHSS, Director Research and Enterprise and Associate Professor of Fiscal Law and Policy at University of Nairobi, and the newly appointed UN Independent Expert on the effects of foreign debt and other related international financial obligations of States on the full enjoyment of all human rights, particularly economic, social and cultural rights; and Steven Dean, Professor of Law at Brooklyn Law School, talked with Alex Cobham, chief executive at the Tax Justice Network, about subtexts and racial bias in tax systems; this theme eloquently and spectacularly built upon by Professor Dorothy A Brown, author of The Whiteness of Wealth, and our first keynote speaker at the conference. Later, the conference was honoured by a second keynote by Andres Arauz, Ecuadorian presidential candidate and tax and social justice campaigner, who framed his comments about efforts to bring back a ‘caring economy’ in Ecuador within the International Covenant of Economic, Social and Cultural Rights. Andres underlined how human rights depends on tax justice and debt justice to bring about the advancement of rights and curtailment of discriminatory policies.

Each year’s conference is marked by the Annual Lecture. This year we invited “a man known for standing with and for those who are perceived as weaker.” Dr Dereje Alemayehu, Executive Coordinator of the Global Alliance for Tax Justice, had a message that was clear and potent. Tensions between tax expertise and tax justice activism is a dynamic that “will always be there”. This is not a point of “discouragement” for activists. The focus of our activism is to mitigate the influence of past colonial powers and to address the “broken and outdated” global tax system they created. Politicking and power relations in the international arena determine our un-wellbeing and failure of rights. Dr Alemayehu warned that tax justice can’t be limited to technical solutions nor the notion that generating more revenue for countries represents justice – the 4 R’s of tax justice↪NOTEThe four “Rs” of tax refer to the key benefits that flow from taxation: Revenue, to fund public services, infrastructure and administration. Redistribution, to curb inequalities between individuals and between groups. Repricing, to limit public “bads” such as tobacco consumption and carbon emissions. Representation, to build healthier democratic processes, recognising that higher reliance of government spending on tax revenues is strongly linked to higher quality of governance and political representation. demand transparency, universality and equality. Delivered with characteristic compassion, Dr Alemayehu is clear that advancing human rights requires the creation of an organic link and alignment with the human rights movement in the struggle for justice.

On the final day there was a focus on the normative. Kate Donald moderated a session called ‘Going beyond the surface: translating human rights norms into concrete fiscal policy reforms’ and described the conference as a “milestone in bringing these issues [tax justice and human rights] together”. Kate shared encouraging examples of growing recognition of the fact that tax justice was crucial to the progress of rights, equality and sustainable development. Many more sessions also delved into normative approaches including a session on personal and political reflections on new constitutional developments to mitigate inequalities and strengthen rights in Chile.

It is fitting that this year’s spirited conference had a particularly animated conclusion. Pulling together a panel of legal, revenue, development and economic experts rooted in the global south, Irene Ovonji-Odida, lawyer, women’s rights activist, and UN High-Level Panelist, along with Logan Wort, Executive Secretary at the African Tax Administration Forum (ATAF), and Manuel F. Montes, Senior Advisor at the Society for International Development, considered what is next for the global taxing rights process, discussed how critical recommendations can be implemented to ensure tax justice and human rights are at the forefront of global policy making, and, crucially, reflected on the power imbalances and pressures that are imposed by the richest on the poorest.

Few can leave this conference without a sobering understanding of the powerful interests which tax justice and human rights campaigners, researchers and journalists are tackling head on. Their efforts to change structures and systems which fail the economic, social and cultural rights of peoples all over the world is exemplified in their courage, innovation, tenacity and hard graft. The realisation of rights is a collective struggle, as Jeannie Manipon said at the opening of the conference, to re-centre people and planet.

At this year’s conference we honoured the bravery and tenacity of one woman and her family. The Family of Daphne Caruana Galizia were awarded the Anderson-Lucas-Norman Award for Tax Justice Heroism. The award is named after Jean Anderson, Pat Lucas and Frank Norman, three Jersey islanders who were among the first to challenge the financial sector’s state capture of Jersey, sparking the global tax justice movement.

Daphne Caruana Galizia was a fearless investigative journalist. A native of Malta. She, like John Christensen, co-founder of the Tax Justice Network and native of the UK dependency Jersey, was driven by a sense of abhorrence towards the injustice that resulted from the self-interest, secrecy and illicit financial activity operating around her. Knowing that the patterns and scale of activity undermined democracy and the gulf between rich and poor, Caruana Galizia disrupted and frustrated the financially corrupt. She paid with her life. Her family honour her memory by continuing her investigative work and by bringing those responsible for her death to account. Their efforts are both a tribute to their mother, wife and sister, and to all investigative journalists who put themselves at risk.

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

In this episode Naomi Fowler speaks with Paul Caruana Galizia, one of the sons of Malta’s incredible investigative journalist and anti-corruption champion Daphne Caruana Galizia, who was assassinated in 2017. Paul Caruana Galizia discusses his mother’s legacy, the capture of Malta through an aggressive, over-sized finance sector with financial secrecy at its heart, and his hopes for the future.

You need to be very strong. To do the job that she did you really have to be your own person. You couldn’t be the kind of person who worries what people might think of you, And you really have to say, no, I’m not going to adapt, I’m not going to fall into that mould. I’m going to break it and keep breaking.”

~ Paul Caruana Galizia

The transcript is available here. (Some is automated and may not be 100% accurate)

The capture of Malta and the fight for justice #113

As mentioned in the show, here’s a video of the story of the ‘firestarters of the tax justice movement’ from the tax haven of Jersey:

A transcript of her edited keynote speech is available here.

You can subscribe to the Taxcast either by emailing naomi [at] taxjustice.net or find us on your podcast app.

Taxcast Extra: The Whiteness of Wealth (2)

You can download this podcast to listen offline here.

Regular listeners to our long-running monthly podcast the Taxcast will have heard episodes 102 and 103 where we looked at just some of the many complex issues around tax and race in the US and the UK context, the roots of structural racism and the lived experiences of people of colour today as citizens, taxpayers and economic actors.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa:

Semanas cruciales para el nuevo impuesto global para las grandes multinacionales.

La estrategia de los países en desarrollo para que se escuchen sus intereses en este nuevo impuesto internacional corporativo

Inflación global, ¿por qué los precios están subiendo en todo el mundo?

Y Chile, ¿podrá la asamblea constituyente lograr los cambios constitucionales que necesita el país?

Mathew Gbonjubola, Director de Política Fiscal de Nigeria

Jayati Ghosh, comisionada de la Comisión Independiente para la Reforma del Impuesto Corporativo Internacional ICRICT y profesora de Economía de la Universidad de Massachusetts

“Tax justice is a feminist issue. Tax is a human rights issue.”

Today the Tax Justice Network publishes a new report Tax Justice and human rights: The 4 Rs and the realisation of rights. The report focuses on two main bodies of argument. The first addresses the failure of tax and broader fiscal systems to deliver intersectional equality and human rights. The second highlights how those failures are caused by illicit financial flows and the actors and structures behind them. Together, these arguments provide the backbone of the case for tax justice to be understood fundamentally as a feminist issue and human rights issue. They support the recognition of human rights’ dependence on tax justice to deliver rights and intersectional equality.

Our report, written with contributions from researchers at the Universities of Leicester and St Andrews School of Medicine (GRADE) in the UK and presented at the annual Tax Justice Network conference today (6th July), models the impact that the $427 billion lost globally could have if it went to governments rather than tax havens. GRADE modelling tells us that if there were an increase in government revenue equivalent to the tax abuse, for countries where there is data available, the additional numbers accessing their fundamental human rights projected over a ten year period would be as follows:

• Sanitation – 34 million people. • Drinking water – 17 million people. • An additional year at school – 3 million children. • Mortality reduction – 600,000 children and 73,000 mothers.

This shocking analysis reinforces previous research acknowledging the importance of revenue to make a well-functioning, democratic and accountable government that fulfils its obligation as a duty bearer of human rights. It also underlines that while the absolute scale of revenue lost from tax abuse in high income countries is greater than in lower-income countries, smaller losses have a more profound impact on improving the rights of people in low income countries.

Women and girls who make up over half of the world’s global poor can therefore disproportionately benefit from increased access to sanitation and drinking water, and to additional years in education. Through progressive advancement of these ‘gatekeeper’ rights, women and girls – especially those most marginalised, gain increased opportunities for greater well-being and development.

Finally, the report calls for a shift in power. It recommends an urgent step change in the reform of global tax rules. Specifically, the report calls on governments to establish an ABC of tax transparency and to support the FACTI Panel recommendations for greater fiscal accountability and transparency. Pivotal to this is the establishment of a UN Tax Convention that will set international standards of transparency and cooperation, a UN intergovernmental body to set global tax rules and a decisive shift of power away from the OECD, the existing tax ‘rule setter’ and widely acknowledged as a ‘rich countries club’. The establishment of a Centre for Monitoring Taxing Rights is seen as crucial in analysing and understanding the impact of the scale and distribution of tax and to ensure that structurally and systemically the approach to policy reform is both gendered and intersectional and can support the advancement of the full range of human rights.

Welcome to the 43rd edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available for listeners to download. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can join the programme on Facebook and on Twitter.

هل يحمي الحد الأدنى للأجور المصريين من التضخم؟

في حلقة هذا الشهر (# 43) من برنامج "الجباية ببساطة" ، نبدأ بتغطية آخر الأخبار المتعلقة بقضايا العدالة المالية على مستوى المنطقة العربية والعالم. في الجزء الثاني، كانت لنا مقابلة مع كريم مجاهد ، الباحث في الاقتصاد السياسي، ناقش فيها معركة تطبيق الحد الأدنى للأجور في مصر منذ عام 2011، ومدى إمكانية تطبيق القرار في القطاع الخاص بالإضافة لآثاره الاجتماعية والاقتصادية.

Pour l’Afrique, les pertes de ressources fiscales qui auraient pu renforcer les moyens de financer son développement, s’élèvent à 25,77 milliards $ chaque année, selon le rapport sur l’Etat de la Justice Fiscale (SOTJ) dans le monde publié par Tax Justice Network le 20 novembre 2020. Une réflexion et des campagnes sont menées tant au niveau de la région, que par des instances internationales, pour inverser la courbe et redonner une plus grande capacité financière aux gouvernements du monde entier, notamment ceux qui sont économiquement plus faibles. C’est dans cet ordre d’idée, qu’un Groupe de haut niveau sur la responsabilité financière internationale, la transparence et l’intégrité, connu sous le nom de Panel FACTI, a été mandaté le 2 mars 2020 par le 74e président de l’Assemblée générale des Nations Unies et le 75e président du Conseil économique et social pour réfléchir sur ces questions.

Le Panel FACTI a publié son rapport le 25 février 2021, dans lequel il formule une série de 14 recommandations. De manière générale, les différents points de revendication de la société civile internationale sont défendus par ce rapport. Par exemple, les objectifs de Tax Justice Network de promouvoir au niveau mondial des mesures telles que l’échange automatique d’informations, la communication d’informations financières pays par pays, la mise en place de cadres juridiques pour connaître les bénéficiaires effectifs et la mise en place d’un registre mondial complet des actifs sont pris en compte. Toutes les recommandations sont regroupées autour de trois pôles, comprenant les valeurs à mettre en œuvre, les politiques à entreprendre et les institutions qui accompagneront l’ensemble du processus. Elles plaident aussi pour l’adoption d’un modèle de convention fiscale international défini par les Nations Unies.

Ces recommandations du Panel FACTI reposent sur trois piliers, dont celui des valeurs, de la politique et des institutions qui seront au cœur de la réforme du système financier international. Pour ce qui est des valeurs, les pays et autres parties prenantes sont invités à faire preuve de plus de responsabilité, de légitimité, de transparence et de justice dans l’exécution des opérations financières. Par rapport à la politique, il est prescrit de mettre un accent sur l’identification des facilitateurs des FFI, l’inclusion de Société civile dans la recherche des solutions efficaces face au problème. Enfin le rapport plaide pour un cadre international de gestion de ce problème, avec un accent sur l’échange automatique des informations. Dans l’ensemble, la société civile africaine a accueilli favorablement ces recommandations. Certains, ont cependant émis de petites réserves sur le fait que le rapport de l’organe des Nations Unies ne donne pas une place plus importante au secteur du commerce international, qui est plus fondamental dans les flux financiers illicites en Afrique que l’économie numérique au cœur de l’attention des pays développés.

<< Les flux financiers illicites en Afrique proviennent principalement de trois sources. Blanchiment d’argent, flux financiers illicites fondés sur la fiscalité et enfin flux financiers illicites fondés sur le commerce. Selon le rapport du groupe de haut niveau de l’Union africaine Thabo Mbeki sur les flux financiers illicites en Afrique, la région est plus susceptible de souffrir des FFI à travers le commerce. Ce que nous constatons, c’est que ces questions étant à l’ordre du jour mondial, d’autres priorités sont maintenant mises en avant », a déclaré Chafik Ben Rouine, président de l’Observatoire de l’économie tunisienne, une organisation membre du réseau Tax Justice Network Africa, lors d’un récent échange entre les organisations de la société civile d’Afrique francophone et l’un des membres du Panel FACTI. L’Afrique ne rejette pas l’idée d’une taxation du digital. La question a d’ailleurs fait l’objet de discussion par ses experts, notamment dans le cadre de la conférence panafricaine sur les FFI Organisée par Tax Justice Network Africa en 2019.

Mais plusieurs parties prenantes de la région y compris la Commission Economique des Nations Unies pour l’Afrique, sont d’avis que les questions commerciales devraient être plus présentes, sur les débats internationaux, en matière de FFI. En effet, Selon un rapport de la Commission des Nations Unies sur le commerce et le développement (CNUCED) publié le 28 septembre 2020, l’Afrique a perdu chaque année 88,6 milliards de dollars entre 2010 et 2015 à travers la fuite de capitaux. Environ 40 milliards seraient liées au commerce. En ce sens, Tax Justice Network a développé des mesures de risques de flux financiers illicites via le commerce. La fuite des capitaux dans ce domaine peut prendre la forme de fraude fiscale à la douane, de surévaluation ou de sous-évaluation afin d’optimiser sa base fiscale ou de soustraire indûment des fonds à la corruption et au blanchiment d’argent. Outre les données sur le commerce des biens, les données sur les portefeuilles d’investissement publiées par le Fonds Monétaire International (FMI) sont également examinées, de même que celles de la Banque des Règlements Internationaux.

D’autres études sur les flux financiers illicites ont établi que l’Afrique se positionne comme une créancière nette du monde, et non la grande débitrice susceptible de constituer un risque pour ses investisseurs. Le rapport du Panel FACTI aborde également de manière pertinente la question des conventions fiscales en tant que source de flux financiers illicites, dans la mesure où elles sont parfois signées au détriment des pays les plus faibles. Mais cela ne semble pas lui donner une importance suffisante par rapport au rôle d’amplificateur de FFI que ces conventions ont dans le continent. Dans un rapport publié par le FMI en 2018, il est clair que les conventions fiscales dans plusieurs pays africains n’ont pas toujours permis d’attirer les investissements escomptés. Pourtant, des centaines de conventions fiscales avantageuses pour les pays riches continuent d’être en place en Afrique. Parmi les pays les plus agressifs du continent figurent la France, le Royaume-Uni, Maurice et les Émirats Arabes Unis.

Quelques possibilités en vue d’améliorer la situation actuelle

Ces considérations nous amènent à proposer une voie en avant pour une meilleure prise en compte des priorités des pays Africains dans le débat international concernant les flux financiers illicites.

Le rapport du Panel FACTI, dans le cadre de ses recommandations, suggère que la société civile soit impliquée dans l’élaboration des politiques internationales. Au niveau africain, les gouvernements devraient impliquer ces acteurs de manière obligatoire, lors de leurs discussions sur la fiscalité internationale, mais aussi dans la signature ou la gestion des conventions internationales, qu’elles soient fiscales ou commerciales.

Il serait également souhaité que les gouvernements africains, conformément à la recommandation du Panel FACTI sur la gouvernance nationale, créent une plus grande synergie entre les administrations fiscales, les douanes, les agences d’enquête financière et les banques centrales afin de mieux surveiller les flux financiers illicites à travers le commerce. Ces synergies permettraient d’améliorer l’efficacité des institutions, tout en permettant une meilleure qualité des données économiques permettant d’analyser ces flux.

Pour les sociétés civiles des pays africains qui ne disposent pas d’outils pour développer un plaidoyer solide, ainsi que pour les gouvernements en quête de mécanismes effectifs pour lutter contre l’évasion fiscale, et réaliser leurs ambitions de mobilisation de ressources, l’utilisation des solutions gratuites en ligne peut être décisive. En ce sens, Tax Justice Network dispose de plusieurs outils, tels que le Financial Secrecy Index, le CorporateTax Haven Index et le Illicit Financial Flows Vulnerability Tracker.

Whilst discussion and agreement on a global corporate minimum tax is historic, we consider it our job to challenge organisations like the OECD and to always push for better. We are sharing below our short statement on the OECD Inclusive Framework, supposed to be a space for all nations to contribute to developing tax standards and implementation.

But before that, it’s worth reading the Tax Justice Network’s Alex Cobham‘s thoughts which he shared on one of his famous long twitter threads:

OK, the OECD statement is out – and *now* it's clear why so many countries have expressed reservations. https://t.co/SiqWIXFSLB

— Alex Cobham @alexcobham.bsky.social (@alexcobham) July 1, 2021

Some commentators have been concerned about the risks of the very negative reactions to the OECD proposal, from a number of countries and groups, and from some activists – including us. Here’s another thread looking at the risks on each side:

If those of us who are fortunate enough to have a platform emphasise *only* the revenue grab of leading OECD members, and what that should mean for the legitimacy of the rich countries' club to set rules for the rest of the world, there is indeed a risk.

— Alex Cobham @alexcobham.bsky.social (@alexcobham) July 2, 2021

GLOBAL MINIMUM TAX CONFIRMED, BUT QUESTIONS GROW OVER OECD COMMITMENT TO ‘INCLUSIVE’ REFORMS

We note the statement from the Inclusive Framework, and the failure to acknowledge there the many countries that are known to have expressed serious reservations over the deal. After much speculation about concessions to lower-income countries, there is little progress here at all compared to the previous iteration.

‘Pillar 1’ remains a narrow reallocation only, of a small part of the global profits of the largest and most profitable 100 or so multinationals. Most countries, and especially lower-income countries, are unlikely to recoup the revenue they may lose from eliminating their DSTs if required to do so.

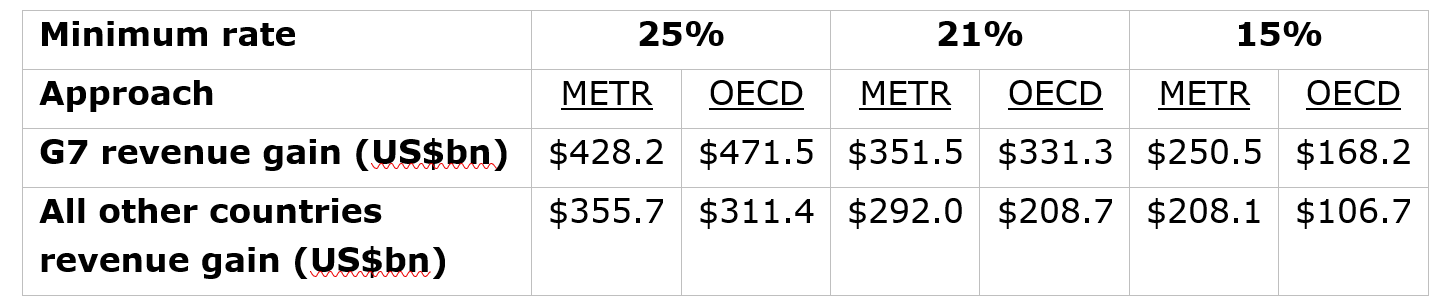

‘Pillar 2’, the global minimum corporate tax rate, remains of much greater importance, but deeply unfair. Even a rate as low as 15%, rightly decried by Argentina, by the Independent Commission for the Reform of International Corporate Taxation (ICRICT) and by many lower- and higher-income countries for the lack of ambition, could raise $275 billion of additional revenues if applied globally. That would make it the biggest change in tax rules for a century – but the G7 countries alone, with just 10% of the world’s population, would take more than 60% of those revenues.

Alex Cobham, chief executive of the Tax Justice Network, said:

“A higher effective global minimum tax rate, coupled with fairer distribution of the resulting revenues, would deliver greater benefits for almost every country – even including many of the OECD members which operate as corporate tax havens. But instead the OECD is forcing through a proposal that gives little to lower-income countries, and leaves much of the incentive for profit shifting intact.

“To force through such an unfair reform, giving the lion’s share of revenue to the largest OECD members when lower-income countries lose the greatest share of tax revenue to corporate tax abuse, is shocking. To do so during a global pandemic when the need for revenue to support public health, and economic recovery, is greater than ever, is unthinkable.

“The global minimum corporate tax rate can mark the beginning of the end of the race to bottom on corporate tax. But the OECD increasingly looks unable, or unwilling to deliver a fair and effective reform. Countries should take the opportunity to push ahead with their own reforms, and consider the possibility of future negotiations being held under UN auspices instead.”

Pour cette 29ème édition du podcast francophone édition de votre podcast en français Impôts et Justice Sociale avec Idriss Linge, nous revenons sur la fiscalité minimum des multinationales en rapport aux services du digital. 130 pays dans le monde ont finalement trouvé un accord pour un seuil minimum d’imposition de grandes entreprises, mais de nombreux défis demeurent. Du digital, il en a aussi été question lors des rencontres annuelles de la Banque Africaine de Développement, comme un levier pour l’amélioration des ressources domestiques. Toujours sur ce sujet, les mairies de la francophonie souhaitent tirer profit des activités commerciales digitales en les taxant, et on mené une réflexion y relative à Yaoundé au Cameroun. Enfin, le Cameroun est restauré dans le processus ITIE, mais les questions de propriétés réelles et de Publication de contrats sont encore de grosses préoccupations.

Interviennent dans ce programme:

Carlos Protto, Director of International Tax Relations, Ministry of Treasury, Argentina

Anicet Akoa, Président de l’Association des Maires du Cameroun

Alamine Ousmane Mey, Ministre en charge de l’économie, Cameroun

Le digital peut être au service de la Justice fiscale, mais des défis demeurent #29

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le lien suivant

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

It is Mansion House time again. Every year Britain’s Chancellor (finance minister) makes a speech at Mansion House, a spiritual home of Britain’s financial sector and the official residence of the Lord Mayor of London, where he (the Chancellor is always a ‘he’) declares his love and support for the country’s oversized financial sector, promises to tread lightly on tax and regulation, and urges it on to greater glories.

The latest speech just given by the current Chancellor, Rishi Sunak, was no exception, praising ‘ground breaking’ new financial services deals with the tax havens of Singapore and Switerland, defending “the global norms of open markets,” and “sharpening our competitive advantage in financial services.”

The words ‘competitive advantage,’ or ‘competitiveness’ when applied to a financial sector, are clear warning signals for those of us who look closely at these things. To be precise, they are signals of a dangerous ideology, one that prioritises the interests of mobile financial capital over those of broad populations and democracies. And since Britain formally exited from the European Union last December 31st, these signals have been coming thick and fast.

In January, for instance, Greenpeace UK launched a petition containing this:

“Bee-killing neonicotinoids have been banned across Europe since 2013, but the UK government has just approved these deadly chemicals.”

“UK workers’ rights at risk in plans to rip up EU labour market rules.”

Soon afterwards, Big Four accounting firms appeared to be delighted about plans to opt out of certain EU transparency rules about abusive tax arrangements. There has been talk ofloosening stock market listing regulations. We hear that the UK is relaxing regulations on ‘dark pools’ – profitable trading platforms for investors, away from scrutiny, and potentially cutting back on various other finance-related rules and regulations. The government has announced plans for “freeports” (or “sleazeports,” hat tip) which have a record around the world for hothousing criminality and abuse and failing to boost even local economic growth. The UK is stepping outside an EU ban on exports of potentially toxic plastic waste to lower-income countries. Fears are rising that the UK may position itself as a “data haven” of lax standards, to attract predatory data-hungry businesses. The Penrose Report, an official review of UK competition policy released in mid-February, looks like another deregulatory push in a “power to the people” packaging. Forces are now pushing hard for a new super-regulator to ensure that UK finance regulators are more “supportive” of the City of London.

Inside the ruling Conservative Party there has been a clamour for a wider “bonfire” of regulations and tax cuts, even as they continue to pursue broad austerity for the majority of the population. As one wag put it on twitter:

“We have a rather crap car in this race, so we can make it ‘competitive’ by removing the roll cage, fire extinguisher, mirrors, brake lights etc.”

It’s a strategy to win a supposed race, that carries, shall we say, risks.

Power struggle

The deregulators don’t have it all their own way. Many remember the carnage of the last global financial crisis, spurred in large measure by “competitive” deregulation of this kind, much of it happening in London under a Labour government. (There are voices among the ruling Conservatives urging caution too.)

Even Chancellor Sunak seems divided, up to a point. He has joined the arsonists in advocating a “Big Bang 2.0” for the City of London – a reference to Margaret Thatcher’s explosive deregulation of finance in the late 1980s, which helped lay the conditions for the global financial crisis and the rise of finance into a near-invincible position of power in the UK. On the other hand, the same Chancellor Sunak recently hiked headline corporate tax rates significantly and admitted – shockingly to many Conservatives – that:

“Over the last few years haven’t seen that step change in the level of capital investment that businesses are doing as a result of those corporation tax reductions.”

UK Chancellor Rishi Sunak

Many bosses of big businesses and even finance companies are saying they don’t want to slide further along this slope either. More striking still, even the tax directors of major multinationals are saying that tax cuts hardly influence investment decisions, and that they largely support higher taxes on multinationals as part of wanting to “do the right thing.” This line of thinking is the opposite of the race-to-the-bottom “competitive” mentality, and there are extremely welcome signs coming from the United States now, where the Biden Administration has made some profound philosophical shifts in this area, as we’ll see below.

But in the UK, the deregulators have the upper hand

Yet in terms of public policy, the overall direction seems to be downwards, into a post-Brexit race to the bottom, as we have warned before.

Britain is walking further along the tax haven road – a strategy of degrading taxes, rules and enforcement in the hope of luring money from the oceans of mobile capital that roams the world hunting for kid-glove treatment, secrecy and handouts. Brexit, according to this model, ‘frees Britain to compete’ without burdensome EU regulations to hold it back. This would, as the Tax Justice Network’s John Christensen said in a speech to the European Parliament in 2019, “give the fox full access to the henhouse.”

The EU is taking a dim view of this broad direction, with almost no current prospects for the City of London to be granted “equivalence” status which would recognise the UK’s regulatory regime to be good enough to allow UK-based financial firms to sell services seamlessly across the EU. In the absence of equivalence, significant financial activity has already migrated to Europe.

This article will explore four big questions. Where does this “competitive” model come from? Was Brexit “caused” by tax haven actors and the City of London financial centre? Who will win, and who will lose, specifically, if this bonfire of financial regulations goes ahead? And how could Britain channel this momentous rupture in better, healthier directions?

Along the way, this article will expose the great ‘national competitiveness’ hoax and show why a strategy of pursuing this rootless global capital does not just hurt other nations: it harms Britain too.

Once we understand this we can see how Britain can act unilaterally in its own interest, doing exactly the opposite of what a supposedly “competitive” strategy would entail, and without needing to be part of a collaborative international project like the EU. A clear alternative path would re-invigorate British democracy and boost prosperity at the same time. This path lies in actively seeking to shrink the financial sector back to its useful core, and to implement “smart capital controls” in particular ways to exclude harmful financial activity from the UK.

How did we get here? Empire 2.0

Was the City of London financial centre and the “offshore interest” in Britain behind Brexit?

Not exactly. Many if not most people and institutions in the City of London actively opposed Brexit. Most of Britain’s large banks, law firms and insurance businesses had long grown used to the rules of the EU Single Market, which granted them “passporting rights” allowing them to establish branches in and do business across the zone with minimal cross-border kerfuffle, while being regulated and supervised in their home country. British tax havens like Jersey and Guernsey were mostly not cheerleading the Brexiteers: although they were previously locked out of the Single Market for financial services, suggesting that Brexit may not be such a rupture for them – it will be hard, because without Britain to lobby for them in Brussels, they are now more vulnerable to things like EU blacklists.

No, the British rupture with Europe has many fathers: Europhobic media barons; genuine anger at distant and élite EU technocrats (and at a mostly pro-EU British élite establishment that helped deliver the global financial crisis and other marvels); billionaires buying influence or mis-direct public anger about inequality and deprivation towards “wokeness” and other cultural memes; or dark-money funding for Brexit politicians who then lied about the benefits of Brexit, and more.

But finance, and especially offshore finance, certainly played a big role. To grasp this, it is necessary first to understand how finance gained such a grip on British politics, society and even culture – and how the “offshore interest” became so powerful within the financial establishment.

The City of London skyline

The City of London, (or “The City,” the colloquial term for the UK’s financial services sector,) was the “governor of the imperial engine,” as the historians Cain & Hopkins put it in their seminal title British Imperialism: it was the big global turntable for loans and finance across the colonies and beyond. The City grew rich and powerful, and became the dominant political force in Britain, particularly since the 19th Century.

After the finance-induced Depression of the 1930s, the world began to appreciate more keenly the dangers of letting finance become too dominant, or flow freely across borders. After the Second World War governments implemented progressive economic policies: eye-wateringly high taxes on rich people; nationalisations, powerful antimonopoly stances – and stringent controls over finance, including very tight curbs on cross-border financial flows.

This financial ‘repression’ and progressive policy-making lasted for a quarter-century after the War. The City and Wall Street loathed it – but it fostered what is now called the “Golden Age of Capitalism”: economic growth was higher, and more broad-based, than in any period of world history, before or since. (For more on all this, read this or watch this.)

As prosperity spread widely, however, powerful forces were already massing against the controls.

The first happened around the time of the Suez crisis of 1956, when Britain and France lost control over the Suez canal in a humiliating defeat. Colonies saw how weak the war-shattered imperial powers now were, and a wave of decolonisation followed. Britain’s dominant élites were doubly horrified because of their double sense of entitlement: first, that Britain should “rule the waves”, and second, that a certain class of finance-focused, overseas-looking ‘gentlemen’ should rule Britain. These people began looking for a grand new post-imperial role – and they found it in a new offshore model.

A new strain of finance emerged in London in 1956, the year of the Suez crisis. Essentially, banks began doing international business in London that wasn’t denominated in the Pound Sterling currency and was thus not plugged into the British economy. This wasn’t allowed under the international “Bretton Woods” rules to curb cross-border financial speculation, but the Bank of England decided to treat the activity as if it were happening “elsewhere” (which meant, in effect, nowhere) and opted not to regulate it.

Foreign banks, especially American banks, noticed fast: operating in this libertarian “offshore” zone was far more profitable than under the tight “onshore” controls, and this so-called “Eurodollar” market grew explosively. Meanwhile, a string of British “Overseas Territories” and “Crown Dependencies,” the residue of Empire, still substantially under British control, began to carve out niches as tax havens, offering secrecy and an almost complete absence of rules. Bankers in these territories – including Bermuda, Cayman, the British Virgin Islands and Jersey – began gleefully hoovering up drugs money and the proceeds of all sorts of other nefarious activity. This “Spiderweb” of British tax havens got plugged into the London-based Eurodollar market, while other non-UK tax havens joined in, from Switzerland to Panama, creating a rather seamless offshore zone where money could flit across borders at the click of an accountant’s pen (and, later, at the click of a computer mouse.) This system for escaping the Bretton Woods controls became the silent, hard battering ram of global finance, which from the 1970s onwards began punching ever bigger holes in the leaking international controls that had underpinned the Golden Age of global prosperity and stability.

Along with this battering ram came a story, a complementary ideology: a globalised version of what gets called neoliberalism. Neoliberalism is the idea that anything that isn’t nailed down should be sold off to the private sector and thus shoveled into the price mechanism and the rigours of “the market,” which would constantly sort everything into winners and losers and thus deliver the best and most efficient possible world. A wave of think tanks and academics, often based in Chicago, began to wield clever models full of mathematics, to push the idea that universities, hospitals, train networks – even the office buildings under the feet of Her Majesty’s tax inspectors – should be sold off, to be sorted by the hyper-efficient sorting machine of the market.

But it wasn’t just people and things and public life that needed to be judged by “the market”. Under a vision first formally theorised by the US academic Charles Tiebout – who first offered his theory up as a joke – it was whole countries too, which could “compete” heroically in a Panglossian market-based global sorting machine. Each nation would offer bundles of tax rates and regulation, together with packages of infrastructure and educated and healthy workforces, for the delectation of rootless capital. Investors would flit from one jurisdiction to the next in great shoals, ripping their kids out of schools and uprooting their factories, at the drop of a tax inspector’s hat.

In this formulation, society was absent and financial capital, picking and choosing from this global smorgasbord, was firmly in the driver’s seat. Countries had no choice but to be “competitive”: low taxes, loose regulations, an absence of “red tape,” and no ‘snooping’ on the activities of clever people by clod-hopping government bureaucrats. Financial secrecy was all the rage.

The Competitiveness Agenda

British Prime Ministers, from Margaret Thatcher to Tony Blair to Boris Johnson, fell under the sway of this “Competitiveness Agenda.”

To foreign audiences, as the historian Matthew Watson put it, Blair spoke of the opportunities from globalisation and from investing in Britain, managing expectations upwards; while to domestic audiences, he managed expectations downwards, couching globalisation as more of a threat: that business interests needed to win out over workers, taxpayers, and the general public (p103).

This wasn’t just a British agenda: a raft of “Third Way” politicians around the world had similar views that rootless global capital must be pandered to. Witness US President Bill Clinton’s belief in kow-towing to finance for “competitiveness’” sake, or Germany’s Harz reforms to underpay German workers in order to promote German exports, for example. What set the British model apart from many others was the focus on finance: the most dangerous of all the sectors to play around with.

In 2005, just ahead of the global financial crisis, Blair urged that we “roll back the tide of regulation,” decried “over-zealous enforcement,” and advocated that “those doing well get a light touch approach.” He attacked financial regulators for being “hugely inhibiting of efficient business by perfectly respectable companies that have never defrauded anyone.”

UK Prime Minister Tony Blair and US President Bill Clinton in September 1998

The global financial crisis that erupted soon afterwards, and the public anger that followed, should have consigned this Competitiveness Agenda to the dustbin of history. After all, it merely gave substance to what every sane economist has always known, that this kind of “competitiveness” is, as the economist Jonathan Portes put it, “meaningless fluff. . . a distraction from what is really going on” (p106). We will explore this, further down.

The zombie agenda lives again

Such was the idea’s potency, however, and its deep grip on Britain’s politics and culture, not to mention its convenience to the finance-heavy ruling classes, that it survived – softened after the crisis somewhat, but still very much alive today.

Before the global financial crisis, UK financial laws referred to the “desirability” of maintaining Britain’s competitiveness in financial regulation. The word was expunged from the lexicon after the crisis, and in particular from the 2012 Financial Services Act, amid a widespread recognition that it was a ‘competitive’ race on laxity between New York and London in particular that caused so much of the damage. Yet although the c-word was mostly expunged from public discourse after the crisis brutally exposed its bankruptcy, it was merely driven below the surface, waiting, hoping, to return.

Like mushrooms that are merely the surface fruitings of giant underground fungal organisms, a host of dog-whistle phrases signified the survival of the Competitiveness Agenda: “open for business;” “global, free-trading Britain;” “freedom to compete;” “top-ranked financial centre;” “proportionate financial regulation.” and still, at times, despite everything that happened in the crisis, a “competitive” tax system or financial sector” (e.g. Section 2.44) Some talk of a “Singapore on Thames” model, with the Asian tax haven as being something to aspire to, without thinking too hard about the parallels.

The concept is now, post Brexit, rallying for a comeback. A new Financial Services Bill, now being processed, has snuck worrying clauses back in, with a proposed duty for regulators to “have regard” for the attractiveness of the UK as a place for “internationally active investment firms to be based or to carry on activities.” That is the competitiveness agenda, by stealth, right there. More openly, a new report from a Task Force for Innovation, Growth and Regulatory Reform calls repeatedly for using regulatory laxity, and shows that people are becoming bolder about using the c-word again, with sentences like: “UK regulation can be a significant driver of our international competitiveness.” (Watch a data privacy expert skewer the report, here.)

Brexit, in this view, has been a chance to let Britain stride forth in the world, unburdened by Brussels’ red tape, and to “compete” again with the greatest, putting British businesses on their toes, spurring them to ever greater feats of dynamism and innovation.

This Competitiveness Agenda dovetails with another alluring idea, again broadly supported by the general public because it sounds reasonable and most people haven’t thought too hard about it. This is the idea that Britain’s route to national prosperity is through growing the City of London financial services sector. As in, ‘More finance makes us rich: and too much tax and regulation here will make the City ‘uncompetitive’ so we’ll hurt the country. So we must swallow our envy and just let those clever rich people do their thing and generate the wealth and the jobs and take the tax revenues where we can.’

The leading proponent of this Big-City ideology is TheCityUK, a peculiar public-private lobbying force, “directed, organized, co-ordinated and encouraged by a state agency as a matter of strategic national importance,” whose speciality is to publish glowing but utterly twisted assessments of the “contribution” of the finance centre to the UK economy – reports that are often regurgitated by busy (or craven) finance journalists.

The essence of this idea – that the financial sector is Britain’s goose that lays the golden eggs, and must be treated deferentially –well, who questions it? Former Bank of England governor Mark Carney pursued it, gushing in 2017 about the prospects of a City twice its size if Brexit goes well. The link between this idea and the Competitiveness Agenda is simple: if a bigger City makes Britain more prosperous, and mobile finance can flee elsewhere if it doesn’t get what it wants, shrinking the City, then Britain has to pursue ‘competitiveness’ in financial services, to make financial services bigger, in the national self-interest.

We will soon explore why the very foundations of this vision rest on elementary fallacies and intellectual quicksand. But first, it is worth briefly side-tracking into a darker, crystallised version of this vision: a mini-ideology held by a small but powerful vested interest, with its own élite sub-culture and its own outsized impact on Brexit.

The offshore vested interest

Britain’s government, and to a degree its political system, media and even society, has come significantly under the thrall of a loose, rather libertarian alliance (or “solar system”) of influential people plugged into offshore tax havens. The players in this ‘offshore’ interest nursed a mix of reasons, personal, political and ideological, behind their support for Brexit. Some, like tax haven financier Arron Banks, funded key Brexiteer lobby groups, with money from often murky sources, with connections from people linked to the disastrous corruption-fueled mass privatisations after the collapse of the Soviet Union, including Boris Johnson’s former “Rasputin,” Dominic Cummings. This loose offshore interest group also includes Jacob Rees-Mogg, an upper-class pro-Brexit politician who has been co-owner of a major offshore investment firm; Richard Tice, leader of the Brexit Party whose family has deep offshore links, and a few others.

These people, and the often mysterious money behind them, were a significant factor behind Brexit: it is quite easy to argue, given the narrowness of the vote, that their influence flipped the vote from Remain to Leave.

If there is an ideology for these hardliners, it was perhaps first espoused by Rees-Mogg’s father William, author of a book called The Sovereign Individual, a favourite of Silicon Valley libertarian times. The book foretold ever greater difficulties financing welfare states as mobile capital increasingly escaped the grubby bonds of the democratic state. Subscribing to the fictional Littlefinger’s “Chaos is a Ladder” theory of getting rich, the book urged the talented, privileged “sovereign individual” to thrive by embracing the offshore mystic, by cheerleading chaos, and by advancing the offshore project itself.

Many adherents of the offshore world view are, like the Rees-Moggs, associated with the ruling Conservative Party. The essential idea is that Britain, broken free from the tiresome “shackles” of Europe would be “free” to deregulate, cut taxes, facilitate financial secrecy, and generally become more of a tax haven than it already is. One could argue that theirs is the freedom of the fox in the henhouse: for the “sovereign man” to better exploit the rest.

Does this “competitive” approach work? It certainly does for them. But for the country as a whole, it is a different – and widely misunderstood – story.

Upgrade for productivity, downgrade for “competitiveness”

“Competitiveness” – as in a ‘competitive’ country, or tax system, or financial regulatory system – sounds great. But it is a fools’ (or a knaves’) errand.

A couple of examples illustrate the fallacies that lie at the heart of this Competitiveness Agenda.

First, consider the near-impossibility of prosecuting crimes and abuses by major financial actors in London. In the words of Liberal Democrat peer Baroness Kramer last February:

“One of the most damning descriptions I ever heard of UK regulators … is that when a US regulator comes to an institution, that institution is in fear; when a UK regulator comes to an institution, people go and make tea.”

Make no mistake: this is the “competitiveness agenda.” Give mobile capital an easy ride, by weakening and removing laws and rules, then not enforcing them. Kramer’s is just one in a long line of warnings about this. If you want more detail on this laxity, perhaps look at this litany of British crime-friendly laxity, or read this 2019 research report comparing US and UK enforcement of financial crimes and misdemeanours, which concluded that “The UK is effectively outsourcing its corporate financial crime enforcement to the US.”

These British failures aren’t a weakness or aberrations of a system designed by benevolent government to deter bad actors: they reflect a deliberate strategy to entice – and consequently to encourage – abusive, and even criminal actors to operate in (or via) Britain’s financial system, often via its tax havens. Once you start looking for this Competitiveness Agenda, you’ll find it everywhere.

Tax authorities have been quietly, steadily defanged: so have financial regulators, competition authorities, and others.

On tax, recent history illustrates again why this competitive strategy does not work. Britain’s policymakers long boasted of seeking “the most competitive tax system in the G20” and slashed its headline corporate tax rate, from 30 percent for most of the 2000s, to 19 percent. On the government’s own figures, each percentage point cut in the headine rate cost an estimated £3.4 billion in lost corporate taxes, equivalent to the annual salaries of over 100,000 teachers.

Is this trade-off good? Does shifting £3.4 billion (or over £37 billion, given the 11 percentage point cut) to multinationals each year somehow make Britain more ‘competitive,’ given the losses elsewhere? With that much money, you could run 20 Oxford Universities, or send a million British children to the elite Eton College, at least if you could fit them all in. And that’s not to mention other damage from these cuts: higher inequality, greater monopolisation as highly profitable giants thrive at smaller businesses’ expense, and more.

Those are quite some costs to the UK. What are the benefits to the UK? Well, all the non-partisan evidence shows that the direct benefits of these cuts generally flow to shareholders. In addition, around 55 percent of UK quoted shares are owned by non-residents, so those tax cuts aren’t just shuffling money about inside the UK from poorer to richer sections of the population: most of the benefits leak overseas.

In terms of the indirect benefits, well, this tax-cutting is supposed to attract foreign “investment” to counteract the costs. We have explained on severaloccasions why these tax-cut lures just don’t work. Chancellor Rishi Sunak, as a reminder, admitted that these swinging UK corporate tax cuts didn’t attract useful investment; those tax directors we mentioned just admitted the same; and survey after survey of business leaders shows that their top priorities are good infrastructure, the rule of law, healthy and educated workforces, and access to vibrant local markets – most of which require good tax revenues. In these surveys, tax cuts and lax regulations are a low priority.

So a “competitive” tax strategy has delivered a raft of costs to the wide UK population and economy, and any benefits have flowed to a far small section of people, including accountants who do very well out of the system themselves and yet are allowed to advise the government on policies. Tom Bergin’s excellent new book Free Lunch Thinking explores the cost-benefit imbalances in great detail.

So what does it mean for a country to be “competitive”?

Policies on investment and national development can take different approaches. One is “upgrading” – for example, strong public investment to improve education or infrastructure, or strong public interest regulation to shepherd and select for businesses acting in the public interest. If Germany successfully upgrades its education, that may well make Britons better off, as richer Germans buy more UK goods. Similarly, if Britain regulates to improve its own financial stability, Germans will be less likely to be impacted by financial crises. Upgrading improves one’s own long term productivity and has nothing to do with “competitiveness” relative to other countries. Everyone wins. Indeed, in a seminal 1994 article “Competitiveness: a dangerous obsession” – the US economist Paul Krugman described competitiveness as just “a funny way to say ‘productivity’.”

A second, “competitiveness” approach, involves “downgrading”. Financial capital flows freely across borders, and countries dangle incentives or subsidies to attract it. Examples include relaxing capital requirements for banks; reducing enforcement of criminal behaviour by financial actors, creating tax loopholes for billionaires or multinational corporations, eliminating minimum wages or crushing trade unions, relaxing environmental laws, or having weak competition policies that let dominant firms exploit British consumers, workers and taxpayers more easily.

A delivery worker delivering an Amazon package

These ‘competitive’ policies are always harmful in the long run. Worse, if Britain downgrades to stay internationally “competitive,” tax havens and other jurisdictions will respond in turn, provoking a race to the bottom. UK taxpayers must continually fork out ever greater subsidies to those capital owners, just to stay in the race. Downgrading regulation selects for the worst firms, most willing to exploit. Inequality and public anger inevitably rise. So does corruption, as firms jostle and lobby to access and expand the growing train of “competitive” subsidies.

The winners in this “competitive” race are – always –large monopolising multinationals and wealthy individuals, while the losers are small businesses, local communities and the general public.

One of the most significant statements on ‘upgrading’ versus ‘downgrading’ comes from the Biden administration, which has made very clear which side of the divide it stands on, in a statement on April 7 announcing a new tax package.

And this world view seems to be reflected across many policy areas. Here’s Katherine Tai, U.S. Trade Representative:

“This inequality isn’t fair or sustainable. It didn’t happen overnight. It is the result of a long pursuit of tax, trade, labor, and other policies that encouraged a race to the bottom.”

The way forward in international tax negotiations spurred by a recent meeting of G7 leaders will be messy and full of pitfalls, but this is a profound philosophical shift. Crucially, these approaches are popular. Majorities vote heavily against the ‘downgrade for competitiveness’ version because they are fundamentally anti-democratic.

In short, this ‘competitive’ race harms the countries that engage in it, and it is unpopular too. So it is worrying that in post-Brexit, Britain, as explained above, and in the words of this excellent analysis of UK financial services by Chaminda Jayanetti, “Competitiveness is making a comeback.”

And this brings us to the finance curse.

Brexit and the Finance Curse

Britain’s public, media and political classes have long been gripped by an idea that the City of London financial centre is the goose that lays our golden eggs. Organisations like TheCityUK put out streams of reports, often repeated by journalists without serious question, apparently showing the scale of the City of London’s “contribution” to the UK economy, showering jobs, investment and tax revenues on the rest of the country.

This pervasive idea has a dangerous subtext: that if this is our Golden Goose, then we need to feed it and pamper it. That is, feed it with “competitiveness” – tax cuts, deregulation, lax antitrust policies, and all that downgrading, effectively shifting wealth from ordinary people in the UK to owners of mobile financial capital, in pursuit of “competitiveness.”

This narrative is, once again, founded on elementary economic confusions.

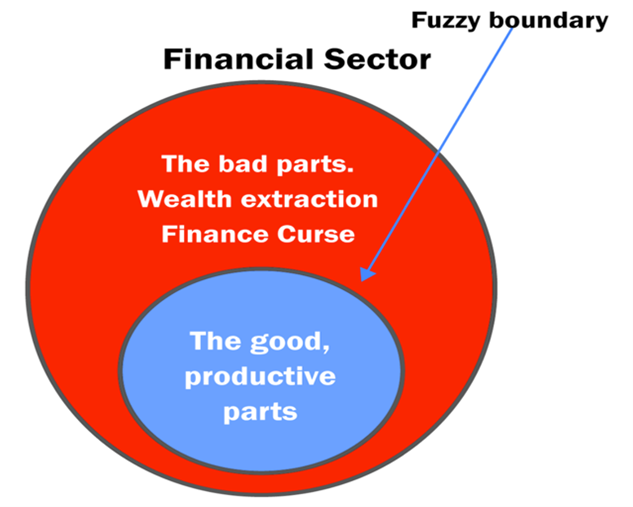

The first fallacy is those supposed “contributions” in terms of jobs and tax revenues are gross benefits, with the costs stripped out. Once you add in the costs, a very different picture emerges. This can be illustrated with two images, which we’ve used before.

The picture on the left is uncontroversial: it shows how any financial sector contains useful parts, which support the economy of the country that hosts it, and harmful predatory parts, which extract wealth from it. Clearly, there are large grey areas that are a mix of both.

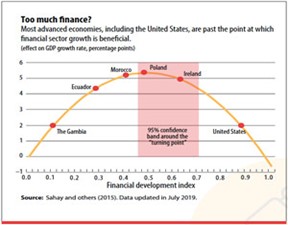

The IMF graph on the right, complementing this, reflects the findings of a growing strand of the academic literature, known as “Too Much Finance.”

Countries with underdeveloped financial sectors can usefully expand them to support their economy. But there is an optimal point, where a financial sector provides the useful services the underlying economy needs: and if it expands beyond this optimal size this reduces economic growth in the country that hosts it. Data suggests that the UK’s financial sector passed its optimal size some time in the 1980s, and just kept growing – inflicting terrible damage on the UK.

Again, we stress, excess finance does not just redistribute the pie unfairly: it shrinks the overall pie too. (There are other reasons for the apparent paradox that “too much finance makes you poorer” beyond predatory rent-seeking: see our first co-authored academic paper on this, from 2016.)

This leads to a simple proposal or slogan: that for countries past the optimal point, like the United Kingdom, we should “shrink finance, for national prosperity.” Shrink the harmful parts, in red in the left hand image, and keep hold of the good parts.

None of this should even be controversial: the only real argument is about the relative size of each part. As explained above, the “competitive” policies to attract mobile capital to the UK are harmful, because they are of the ‘downgrading’ kind (and anything that might get called “competitiveness” which is beneficial is “upgrading” – so it isn’t “competitiveness.”

Putting all this together, we can rephrase this slogan as “oppose competitiveness, for prosperity.” (We have said this all before, on tax: this is the finance version.)

This broad analysis has profound and optimistic implications for democracy, because it opens up a world of political possibilities for tackling some of the great problems of our age.

Currently, voters and politicians are hamstrung by the Competitiveness Agenda: they may want higher taxes on rich people or on big banks, or stronger regulations to curb financial scandals and abuses – that is, upgrading — but they fear that these people and organisations will disinvest and run away to Geneva, Singapore or Panama, where regulation is lighter. Businesses wield this threat all the time. So nothing gets done, and standards slip.

The race, to many people, looks like a collective action problem, where it is everyone’s shared interests to collaborate, but in the interests of each individual player to cheat. The classic solution to a collective action problem is to co-ordinate and co-operate. Governments get together to agree common thresholds, beyond which they won’t sink, or downgrade. This can work: the OECD programs such as BEPS (to tackle multinationals cheating on their taxes via the international system) or the Common Reporting Standard (CRS) where countries agree to share information on the wealth holdings of rich folk, to improve transparency.

But international collective action is weak medicine. Countries feel the incentive to cheat, it’s also hard to mobilise powerful domestic coalitions to support complex international collaborations – and try getting China or Russia or Luxembourg or Ireland on board in any case.

The finance curse analysis provides a clear and powerful route out of the collective action problem. If we should “shrink finance, for prosperity” – then we can step unilaterally out of the race. We need not wait for international collaborations, in the meantime downgrading our tax laws and financial regulations to stay in the race. The finance curse tells us to do exactly the opposite. Upgrade, chase away the bad actors, and even though the financial sector as a whole will be smaller, the wider economy will be more prosperous.

We can just upgrade, in our own domestic self-interest. This is a far more potent political proposition that can mobilise powerful domestic coalitions behind it.

Has Brexit helped, by shrinking the City of London?

Brexit certainly isn’t the way we would have shrunk the City of London, to boost Britain’s prosperity. But amid all the dark clouds of Brexit, this could be an unintended positive outcome, depending on how this all shakes out. From the EU’s perspective, Brexit also removes a powerful lobbyist that has done much to create harmful regulation in the EU. Europe, too, should take on board the finance curse analysis, as we argued in the Financial Times in2018, and strenuously avoid trying to lure financial activity away from London using ‘competitive’ lures.

Post-Brexit Britain: a global builder or berserking destroyer? The latter currently looks likely. But it is not inevitable.

Much will depend on which faction in the British ruling establishment gets the upper hand, in the years to come.

Written by Leyla Ates, Andres Knobel, and Markus Meinzer.

One of the most powerful tactics a multinational corporation can use to abuse tax is to secure a tax ruling in one country that gives the corporation written permission to exercise an abusive interpretation of the country’s tax law in a way that ultimately enables the multinational corporation to underpay tax in other countries where it operates. While in recent years countries have started privately exchanging or publishing some information on the tax rulings they issue to multinational corporations, these partial disclosures are not enough to stop the use of tax rulings for corporate tax abuse. Even if the full text of tax rulings were disclosed, it can still be impossible to understand how much corporate tax is being underpaid.

We propose here a number of measures to address this. In summary, each ruling should:

1. Be published online 2. Identify the legal person(s) involved and their tax advisers 3. Include the multinational’ country by country reporting data 4. Include a description of the full tax scheme, including any other rulings or schemes involved 5. Include an assessment of the tax impact

States should also commit to:

6. Protect and reward whistleblowers who reveal undisclosed tax rulings 7. Allow anyone to challenge the validity of a ruling

Tax rulings as tools for tax abuse

In essence, tax rulings are resolutions by a tax administration that give some level of certainty to taxpayers about how the tax administration interprets a specific regulation or transaction. Usually, a tax ruling on its own isn’t enough to enable tax abuse, but it can be a crucial part of a larger tax abuse scheme. When used constructively, tax rulings may help taxpayers understand and properly apply an ambiguous regulation, saving both taxpayers and the tax administration time and resources. However, over past decades tax rulings have increasingly been used as powerful tools for tax abuse. This is especially the case with “unilateral cross-border tax rulings”, where the tax administration of one country “unilaterally” issues a tax ruling that will have effects on the tax obligations of a taxpayer, such as a multinational corporation, in many countries. Due to the international or “cross-border” nature either of the taxpayer (eg a multinational corporation operating in several countries) or the transactions (eg interest payments on a loan a multinational corporation lent itself from a subsidiary in one country to a subsidiary in another country), a unilateral cross-border tax ruling can give a multinational corporation legal cover in one country to undermine the rule of law in other countries.

Abusive tax rulings can sometimes be unintentional consequences of a lack of capacity in a tax administration to understand the effects of a ruling, or of recklessness and corruption in a tax administration. At other times, abusive tax rulings can be part of a tax haven’s wider, deliberate efforts to attract multinational corporations by enabling them to reduce their tax liabilities in other countries.