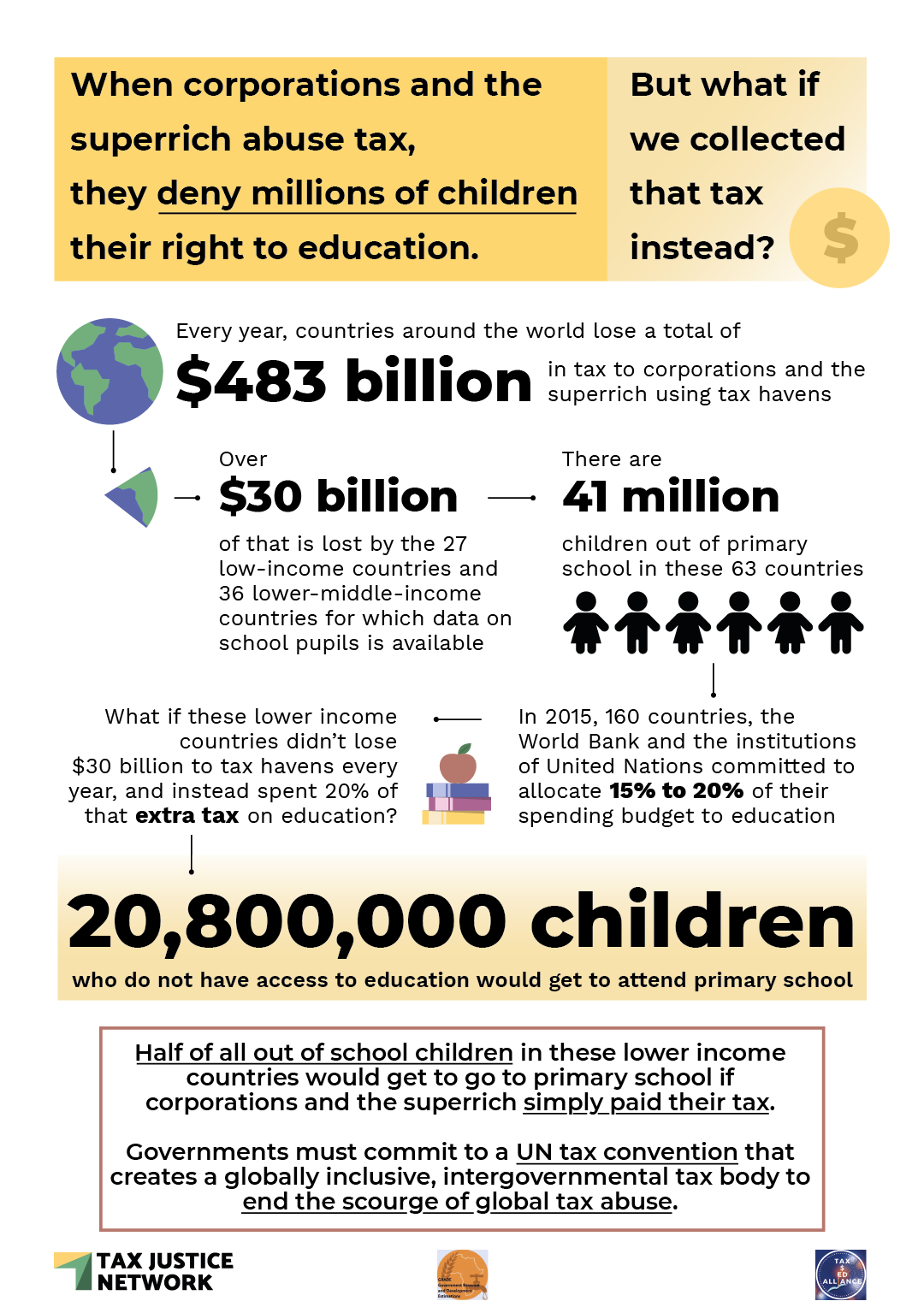

Every year millions of children are denied access to public education. Education is a child’s right, but government revenue budgets, especially in low income countries, are almost always insufficient to ensure all children have the opportunity to access publicly funded primary and secondary school.

In preparation for the United Nations Transforming Education Summit last week we prepared analysis on the impact of tax abuse on access to public education. The results were shocking. Of the $483 billion lost to tax abuse world wide over $30 billion is lost by the 27 low-income countries and 36 lower-middle-income countries for which data on government expenditure per school pupils is available. In these 63 countries there are 41 million children out of school. If each of these countries were to spend just 20 percent of the tax revenue they lose annually to global tax abuse, 20,800,000 children who don’t have access to education would get to attend primary school.

Our research with Dr. Bernadette O’Hare at the GRADE project used 2021 State of Tax Justice data to measure the impact of global tax abuse by multinational corporations and tax evasion by wealthy individuals on children left out of school. We specifically looked at the impact on education using data on ‘out of primary school’ children and ‘out of secondary school children’. The countries we analysed were: Samoa, Chad, Rwanda, Sierra Leone, Liberia, Malawi, Gambia, Cambodia, Mozambique, Madagascar, Uganda, Congo DRC, Kenya, Myanmar, Togo, Guinea-Bissau, Benin, Tanzania, Guinea, Afghanistan, Nepal, Ethiopia, Mali, Central African Republic, Burundi, Niger, Comoros, Burkina Faso, Georgia, Nicaragua, Vietnam, Sri Lanka, Egypt, Congo, Rep., Bhutan, Syria, Ukraine, India, Morocco, Timor-Leste, Zambia, Moldova, Cameroon, Armenia, Mongolia, El Salvador, Indonesia, Honduras, Vanuatu, Laos, Ghana, Senegal, Pakistan, Eswatini, Guatemala, Mauritania, Cote d’Ivoire, Paraguay, Guyana, Cape Verde, Sao Tome and Principe, Djibouti and Yemen.,

The Incheon Declaration (2015), adopted by 160 states, the World Bank, United Nations institutions and civil society presented a new vision for education and a commitment for governments to use between 15 to 20 percent of spending budgets on education. We cautiously assumed therefore that at most, governments would spend no more than 20 percent of any additional revenue found from curtailing global tax abuse on public education budgets.

At the United Nations Transforming Education Summit – the goal for the TaxEdAlliance, a global initiative that puts the spotlight on transforming education finance of which we are a member, was to urge a radical reframing in the way in which education is financed. Tax justice is central to this reframing.

The vision of Sustainable Development Goal 4 to ensure inclusive and equitable education continues to be thwarted by global tax abuse on a grand scale. Powerful actors whose interests lie in accumulating wealth are denying children throughout the world their right to education. As a consequence countries – economies and societies – that should prosper are out of pocket and without the means to provide inclusive and equitable public education.

It is shameful that those governments and financial institutions who have committed to Sustainable Development Goal 4 fail to make good on their commitments. It is shameful that the obligation to the right for each child to have education is deprioritised. More shameful is those governments and financial institutions who recklessly block progressive tax policy reforms. The time to transform the financing of education is long overdue and calls for a fair, equitable and truly intergovernmental approach must be heard. Such reform demands political leadership. The May 2022 ministerial declaration of the Economic Commission for Africa saw more than a quarter of United Nations member states call for negotiations to begin on a UN tax convention that could deliver comprehensive progress. Yesterday, the UN Secretary General António Guterres announced his readiness to support a UN tax convention.

Policymakers must join this call urgently, and commit to a UN convention on tax that creates a globally inclusive, intergovernmental tax body to end the scourge of tax abuse.

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

In this episode, Taxcast host and producer Naomi Fowler explores tax as a tool for racial justice and the launch of a new report by Decolonising Economics.

Links to past Taxcasts on reparational and tax justice, plus a video of the launch of new report: Tax as a Tool for Racial Justice and other useful resources available here.

There’s a real opportunity for mobilising towards transformative policies that’ll work not just for racialised communities in the UK and globally, but for everyone feeling the pains of this economic system”

Naomi: “On the Taxcast this month – racial injustice and how we end it. It’s not been central to tax and economic justice work and campaigning as it should have been. Especially in Europe. We’ve talked on the Taxcast before about the 4 Rs of tax, that tax isn’t just about the most well known R – Revenue. Because as well as raising revenue, tax has other Rs that are less well known but they’ll start making more sense as we hear why tax is a crucial tool for racial justice.

So, here’s the other Rs of tax – there’s Repricing – that’s essential in a world experiencing climate crisis, needing to limit carbon use. The next R of tax is Redistribution – fair taxes, so wealth is shared better. Then there’s Representation – which is all about how tax justice enhances democracy and accountability.

We could add a fifth R – Repair. And that’s something that reparational justice campaigners talk about – that’s about remedying the legacy of social and economic exclusion and ecological damage caused by exploitation, colonialism, patriarchy and structural racism.

There are more Rs actually that we could add to the list, including Reorganisation and Reclaim, all about building a caring economy that gives space for care and compensates those who care – but that’s for another day, that’s another podcast!

So, a couple of years ago now the Tax Justice Network and our sister organisation Tax Justice UK collaborated with Decolonising Economics. It’s an organisation dedicated to building a solidarity economy rooted in racial justice principles. They’ve launched a new report “Tax As A Tool For Racial Justice” this month. Here’s some quick highlights for you from the launch itself from panellists we invited to discuss it. Let’s start with Assistant Professor of Africana Studies Keston Perry:”

Keston: “To some degree I’m a bit sceptical about the idea of how do we decolonise the tax system – what does that mean for around sort of reforming aspects of the tax system which are actually rooted in enslavement, rooted in colonial subjugation? For me i think the report is really critical as the first of its kind I’ve seen, that is very much an important start for conversations around how the British empire and its legacies as well as the continuation of the fragmentation of that empire, what it means for trying to instigate action towards racial justice, and for me i think it highlights the ways in which tax and the financial system in general has been used as a tool for racial subjugation, extraction, continuation of racial disparities and hierarchies.”

Naomi: “That was Keston Perry. And here’s Stephanie Brobbey of the Good Ancestor Movement:”

Stephanie: “I was really excited to see this movement-centred research and really feel that it’s a road map to racial wealth equity, about just how far tax should be used as a tool to repair structural inequities specifically in the context of racial justice and the racial wealth gap and really how to leverage tax as a tool for systemic change and not just in and of itself to fix, you know, short-term issues with the economy. You know, enslavement and colonisation literally built the wealth of nations and created the architecture of a financial system which naturally concentrates wealth in particular geographies and across specific demographics. We know that the Bank of England financed colonial expansion, that merchant banks provided commercial credit to expand colonial activity but also to finance the buying and selling of slaves. And so we have this creation of a financial system which favours whiteness by default.”

Naomi: “That was Stephanie Brobbey, one of our panellists at the launch of the report Tax as a Tool for Racial Justice. And finally, here’s economist in economic development Priya Lukka:”

Priya: “For a whole body of thinking of this kind to be finally in the public space and for us to all be able to reference it and for it to hold weight and strengthen our arguments is so significant and i think it’s really going to shape where we can go next from here. We know that people living in poverty are not beneficiaries of the tax system but they are instead net payers so groups who’ve had their power taken away from them by colonialism such as indigenous groups, afro-descendant people, people living in segregated urban areas and landless people all pay disproportionately more tax than they should so there are certain structural inequalities such as racial and gender inequality that are the legacy of colonialism and its mechanisms of which the tax system is one, as established by this report and that’s really fundamental for it to be firmly established and argued and evidenced. And the uk has played a role in shaping not just the global tax system that stripped wealth from former colonised countries, but the whole financial system. Thank you for producing this work and I’m sure it’s going to lead to dialogue and more hopefully disrupt the current system.”

Naomi: “That was Priya Lukka. You can watch the whole session, the link is in the show notes, and I’ll put the link to the report in there too. So, we’re all hoping that this report Tax As A Tool For Racial Justice and the bringing together of people from so many different spheres will move us all together into the same space to take the next steps when it comes to campaigning and research. I spoke with Guppi Bola of Decolonising Economics, author of the report:”

Guppi: “We really saw it as an opportunity to finally put into place a map, I guess, of where some of that uncovering of evidence, as well as design and creation or creativity around new ideas and policies around tax and tax justice could exist. And I think I had an idea in my mind about this map for quite a long time, and it really felt like tax was a very useful place to focus on within the broader financial system and our thinking about the various financial instruments, because I guess of how quickly things in the tax world change, how easy it might be to implement policies, but also how transformative applying different taxes can be to the power across the economy. Um, I also think that there is a perception that tax is quite boring…”

Naomi: “Never!!”

Guppi: “Ha, never! But it’s, yeah, for me, it’s just like another mechanism that can steer us towards where we want to go and so Decolonising Economics, I suppose maybe like every good initiative started out as a bit of a frustration about the way things were happening in, I suppose, what Noni my organising partner and I refer to as the mainstream economic justice movement or NGO sector. And we both came from community organising and activism, but also had professional lives within the sort of economic justice sector. There was a lack of depth in the analysis of what the root causes of inequalities were, largely stopping at the point of sort of 1930s neoliberal thinking and not going past that. And for us, there seemed to be a real evident connection between the history of the colonial era and the establishment of the capitalist economy and the inequalities that were in existence today, and kept getting worse over the last decade. And so our desire to sort of have that analysis in some of that work that we were doing in designing campaigns and thinking about what kind of projects we could do to do further research in this area, because as we sort of ran workshops and explored this and wrote articles, we realised that there was little evidence other than in quite dense academic texts and not enough that translated to strategy. But the other thing also driving us was an understanding of the fact that the economic system can change, it can transform, it could really work for addressing racial inequalities.”

Naomi: “Right, so you’ve written this report, tax as a tool for racial justice, and what you say about the lack of work and attention on this area when it comes to racial justice and all sorts of campaigning and activism on economic justice, there’s been such a, a gap there in the UK particularly if you compare with the United States. That’s also something that’s been happening in the tax profession itself, economists, the mainstream media and working as I do for NGOs I know that they’ve been really, really slow to put that into the centre of their work. Lack of diversity is a big part of it but it goes way, way beyond that, to the narratives, the dominant narratives in society and you know, you do tend to get different professions simply reflecting inequalities in the societies they operate in and not pushing beyond those boundaries. So, what I wanted to ask you really is, in a way you’ve answered it, but why this report now?”

Guppi: “The thing that I was really keen to do with this work is think about actually what tax justice and equity means in terms of accelerating a design of a financial system that actually works towards repair. So just like pushing the vision of what we’re trying to do rather than, well let’s just try and rebalance how much money goes into the financing of fossil fuel industries versus renewables, or, you know, rebalancing inheritance so that things are redistributed better, but really like pushing the boundaries of what we perceive as fitting within the tax system, which also includes, okay, well, how are we applying reparations in this context? And what, what does that mean? And what does it look like to both those who are residing in the UK, but also outside who are impacted by the actions of British colonies and colonial Britain. And I think that desire to, I guess, show something structured on paper as evidence that there is a way in which organisations can undertake bits of research and campaign design that doesn’t feel too, sometimes can feel really overwhelming and complex. And there’s layers and layers and layers of complexity still within the report, but at least it offers a bit of a framework to begin thinking about how you would structure different sectors within the economy, think about the types of questions you might ask around land or finance systems or inheritance and immigration, and how they intersect with racialisation and racial identities. And then also encourage people to think beyond just racism as a structural oppression but go beyond that to thinking about disability and trans and queerness and how those also intersect with this economy as well. So hopefully it’s an opening for something much broader that works both at the depth of transforming the economy through taxation but also other forms of financial instruments that are in operation as well.”

Naomi: “For those who are listening who don’t live in Britain, and even for those who do, can you talk a little bit about some of Britain’s racial inequalities that exist today?”

Guppi: “Britain’s an interesting place, because in my perspective, whilst a lot of the inequalities are quite overt and obvious, they are actually also quite hidden, so what is perceived as the norm actually has a hidden dynamic behind it that is not seen, so you don’t really think about laws around policing, the housing market, immigration system. There is a deep racialisation within each of those systems that has a perception of fairness and objectivity, but definitely because of the roots of a lot of those structures in the colonial logic play out in ways that perpetuate racial inequalities. We do know that, of course, over the last 10 years inequalities have got much worse. One of the best reports to read and I reference it in the paper is the Colour of Money by Runnymede Trust, which looks at the wealth levels across different racialised identities. And it shows that for every pound of white British wealth in white British households, British Indians have 90p comparatively, and those who are worst off are often, uh, gypsy Roma, traveller, Bangladeshi, Pakistani, and black Caribbean, and black African.”

Naomi: “Yes, apparently families of Bangladeshi and Black African heritage in the UK have ten times less wealth than White British families. The UK’s Department of Work and Pensions has found that 60 percent of Black and Asian households have no savings at all, compared to 33 percent of white households. I mean there are historical reasons that are playing out right to the present day, going back centuries going on here, it’s something Britain’s really struggling with, and we hope this conversation is becoming safer to have for people who’ve been trying for a long time to have this conversation about Britain and how its systems have perpetuated racial inequalities coming from a violent and oppressive history that has real live repercussions to this day in the country itself but also overseas of course in terms of former colonies, and the role it plays in debt and other extractive processes, not to mention climate crisis that’s such a large part of the experience of some of those nations. There are so many things to talk about but Britain just hasn’t dealt with its history even remotely yet, has it, never mind its present?”

Guppi: “No, not at all. And there was a British attitude survey from 2020, so it’s quite recent that said that still 60% of the British public feel that those countries that were colonised were left better off than if they weren’t. And I still find that astounding, I think the only other country in Europe that has a better, you know, positive perception of their empire is the Netherlands, but most other European countries publics are broadly ambivalent about their empire or colonial past. And I’m not entirely sure that that is much better, I think that is another example of a hidden history, so we are having to contend with a perception of positivity. I’m very grateful to be able to have this conversation freely, but for sure there will be and will continue to be a real struggle in trying to find space to have a political conversation around the colonial history of Britain and its impacts and its relationships today. And that of course began more publicly during the Black Lives Matter mobilising and..the involvement of academic historians who became spokespeople for that relationship. But I do think that it now is the time for NGOs and campaigning organisations to begin thinking about solutions that embody that analysis. Because we have a responsibility in the process of designing transformative policies and campaign ideas to find ways to unite groups and I think there’s a real opportunity for mobilising towards transformative policies that will work not just for racialised communities in the UK or globally, but for everyone who is feeling the pains of this economic system.”

Naomi: “Yeah, absolutely, the conversation is not free and open still in Britain. So, how would you describe this report?”

Guppi: “The report is sort of broken up into about four sections, I guess. And we begin with a glossary of terms, which we find useful to understand the information that you’re then going to read, to understand and situate the practices of British, colonial economic policies in today’s context of racial inequalities and make that relationship about how you know, in the 1600s when Britain began exploring, and I say exploring it wasn’t exploring was it?! Invading and capturing land! See, even I’m just like in that mindset over the way that we talk about it – capturing land and killing people, and how the design of different institutions like the Bank of England and insurance companies enabled that exploitation and extraction and how their existence today connects us to that globalised economy and the dynamics of that globalised economy, so a little bit of that history. And then we move into I guess the meat of it, which is where I talk about the different structures in which tax plays a role in both boosting wealth in whiteness, that there is a history of policies that maintain the strength of certain institutions that try to ensure wealth in whiteness, whether it’s in white households or white dominant institutions. And when I say whiteness, I don’t mean just like skin colour, I mean the concepts and ideas around the economic system. Or block wealth to black and people of colour communities. And so we look at things like immigration and land, housing and many other structures, and how those dynamics play a part. And then the final bit explores the idea of what tax could be. And so how to think more intelligently about tax as a tool.”

Naomi: “Yeah. Right, and next steps, what do you want them to be? I mean, for me, I would want racial justice to be key to all social and economic justice campaigning and activism and research. I’m looking for practical policy that can be implemented, things like slavery and empire audits in particularly finance institutions, we’ve seen some institutions going that route, we need to see more, what what’s next for you?”

Guppi: “Very similar to you, uh, Noni and I would just like some evidence, some numbers that we can use about how much wealth was extracted, you know, by certain institutions at certain times during the colonial era, how that has created their political power today and what influence those institutions have had on our modern economy and design of public policies today. I’m also really keen for some of the communities that we work with to have the space to actually dream and reimagine about reparations and tax and what that could look like and to feel ownership and agency around issues of tax so that they feel that they’re able to give ideas that then are seen as legitimate and possible by the mainstream campaigning organisations and can be inbuilt into a long term strategy. And when I’m talking long term, I’m talking like 20 years, even if we’re obviously battling with the kind of tax politics that we have at the moment with our current government. We need to be able to give some positive direction to where we can go. And if we’re not laying vision, we’re really just going in cycles of where the politics is taking us and not moving forward in our own imaginations. And, and for me, that feels really important at this point, because of just the sheer level of despair that everyone is feeling.”

Naomi: “Yeah. I mean we’re at a stage of what feels like a real turning point in Britain actually. There’s a transition going on of all different kinds in the UK. There’s a sort of isolationist thing going on, some of the former colonies are probably finally about to make the break from the monarchy, there’s some pretty toxic things going on with the government. If we talk about what campaigners and researchers should prioritise in terms of solutions, wealth taxes and inheritance taxes are really obvious, land value taxes, you know, financial transactions taxes, we’ve talked and thought a lot about a plan B for small island nations to diversify from oversized finance sectors that are really fuelling inequality there, as I’ve mentioned, you know, slavery and empire audits that lead to real meaningful reparational justice. You know, the tax justice network works a lot on trying to change who decides on global tax rules to take that power away from OECD former colonial nations and put us in the hands of the United Nations, we need debt relief, we need climate crisis reparations. And in fact, plundered nations are asking the United Nations right now for a global tax to pay for climate loss and damage. There’s so much to work on, tax professionals – we need you! Where would you prioritise?”

Guppi: “I do think that there is traction, high levels of traction for climate reparations dialogue. Just thinking about just the sheer impact that is so evident on you know 2-300 years of just being under control by an economic system that has prevented countries that have been formerly colonised from being able to protect its own citizens. It feels very evident that that should be a place in which we should put all our efforts, just given the sheer scale of how destructive that history has been and is gonna continue to be, so protections in those areas are important. The other thing I think, beyond the public campaigning and influencing and advocacy work is feeling part of an organising space that is actually able to apply positive forms of tax that do instill repair. There is an emerging group of individuals who are privileged from the perspective of inheriting wealth and who recognise that inheritance is problematic and that them inheriting that wealth maintains a particular economic structure that perpetuates inequalities, and so there’s a questioning around what to do with that wealth and how to redistribute it. And there’s also wealth advisors who are now advising out of investment in the stock market and finding ways to put wealth into community control. And I’m interested in philanthropic organisations who have control over their wealth to really think about where their endowments lay, where their investments are, what they’re making their money out of. And everyone in the sort of NGO sector is part of that system, you know, we receive grants from philanthropic bodies and are in a way through that mechanism of need participating in an extractive economic system that is basically creating the problems that we’re trying to solve. So where we have some relationship directly with institutions, I think that there is a role for us to play in advocating internally as well.

And some of the other things that I would prioritise is in the US there is a voluntary tax called the Shuumi land tax, which recognises existence on indigenous lands. And I’m interested in how we could think about what a voluntary tax in the UK could be that recognises how much the racialised communities have upheld the economic system in the UK, from the NHS to our care workers and cleaners, and that kind of hidden part of the economic system that basically holds us up, and how we could create a voluntary tax to reparate for that and help move people from a place of oppression and marginalisation towards feeling liberated. And I think just to end that in the eventuality of some form of collapse, we will need to begin developing that community infrastructure, not relying just on State infrastructure to be able to do that distribution. I think that that’s hard work, but I think it’s really, really important because some of the more resilient nations are those that have that kind of diversity of systems at play, and we definitely don’t have that so much here in the UK.”

Naomi: “No, we don’t, and it’s often presented in a kind of a binary – either the State takes control of everything or you leave it to the markets, and that is a real problem and paucity of vision that we have in Britain for sure. And I mean it does seem like we are in a kind of capitalist death spiral at the moment, you know, nothing must interfere with the God-given right to make as much money as possible, no matter who you hurt, no matter what the cost, no matter what the damage is to people, to the planet, to biodiversity. But transition is happening already in many nations, it’s happening in the UK, we’ve just had the hottest summer on record. Whether we like it or not, we are in a transition era of all types. You’ve talked a bit about reimagining the commons and thinking differently about the nature of ownership and stewardship actually so that humanity can be compatible with the natural world instead of destroying everything that our lives actually depend on. So, it’s about visionary thinking because without it, it feels like we are really doomed!”

Guppi: “Well, you know, I had in the last 15 years of doing economic justice work to really dig deeper into the existence of other forms of economic practices, which is ultimately, you know, our relationship and management of resources and pulling in wisdoms of indigenous communities that are deeply connected with nature and nature’s resources, and communities as beings as kind of interdependence that we have with one another. And I do think that it is very challenging to look at politics today or look at people’s day to day and try to apply those practices, and imagine that those practices could be policy, but I do believe that it’s possible and I keep going back to this concept of community self-determination and organising.”

Naomi: “You’ve been listening to Guppi Bola of Decolonising Economics. And I’ll leave you with a pretty brutal example of how markets are perpetuating injustices, and profiting off misery. It’s not hard to see that it’s immoral. But also that it’s a continuation of a long history of subjugation, and that we can’t go on like this. After covid struck not so long ago, Zambia defaulted on its sovereign debt. Zambia’s been asking its creditors, including asset managers BlackRock to restructure the debt repayments they owe them. Even by IMF measures Zambia’s debt’s not sustainable. Here’s Stephanie Brobbey of the Good Ancestor Movement:”

Stephanie: “Blackrock holds about 220 million dollars worth of Zambian sovereign bonds and stands to generate in excess of 180 million dollars for its clients if those debts are paid in full, and Zambia has incurred crippling debt in order to try and build its infrastructure to protect its people from the climate emergency. And this is a classic example of how debt is preventing lower income, typically black and global majority countries from protecting themselves against the worst effects of climate change and this is a kind of double injustice the original extraction from colonial activity and enslavement, to kind of suffering from the emissions that have been caused by countries in the global North who are then continuing to extract from them and to amass wealth through their misfortunes and they are refusing to suspend interest payments, so that demonstrates the harm that is inflicted on black and global majority communities in this way which is rewarded in monetary terms. It really taps into the psyche of actually what we’re dealing with, wealth has been, and continues to be divided along racial lines.”

Naomi: “Stephanie Brobbey there. I’d add that Blackrock has clashed over the years with various tax authorities over its tax contributions, including in the UK. There’s so much reform and rethinking to be done. And all our lives depend on it.”

Durant le mois de mai 2022, le Cameroun a connu une polémique à propos d’une convention d’exploitation de fer signée entre son gouvernement et Sinosteel, une multinationale chinoise. Des députés rejoints par une partie de la société civile ont dénoncé ce contrat et exigé son annulation, expliquant que cet accord était désavantageux pour le pays. Dans une interview accordée le 23 mai 2022 à la chaîne de radio BBC Afrique, le ministre camerounais en charge des mines a démenti l’ensemble des craintes soulevées par l’opinion publique. Le gouvernement par la suite a décidé de publier ladite convention sur le site officiel du Ministère des Mines de l’Industrie et du Développement Technologique.

Sur un tout autre plan, Glencore, la multinationale anglo-suisse qui domine dans le secteur du trading des matières premières, a reconnu parmi plusieurs autres infractions, avoir effectué des paiements de l’ordre de 79,6 millions $, via des sociétés écrans, pour obtenir des contrats avantageux dans les secteurs du pétrole et du gaz, y compris au Cameroun.

Cette polémique ainsi que le cas de corruption de Glencore au Cameroun, rappelle qu’il existe un besoin des populations d’en savoir davantage sur les conventions qui donnent le droit à des entreprises étrangères d’exploiter et d’effectuer des transactions sur des ressources appartenant à leurs pays. Les caisses de l’État et donc, les citoyens, sont toujours perdants en raison d’accords cachés, de lois peu rigoureuses et de pratiques fiscales agressives des entreprises. Dans la plupart des juridictions, les ressources minérales non renouvelables sont gérées par l’État au nom du peuple. Les États accordent généralement aux sociétés le droit d’explorer, d’extraire et souvent de vendre des ressources minérales en échange de revenus ou d’une part du minerai. Le contrat décrit les droits, devoirs et obligations des parties, y compris les conditions et dispositions fiscales. Ces contrats peuvent s’étendre sur des décennies et entraîner des répercussions importantes et durables.

Contrats extractifs : Pourquoi la transparence compte

La transparence des contrats dans le secteur extractif est un élément essentiel de la lutte contre les flux financiers illicites. Dans son rapport de suivi pour l’année 2022, l’Initiative qui est le fruit d’une volonté globale pour la Transparence dans les Industries Extractives (ITIE) a rappelé l’importance de la transparence pour les contrats extractifs. « En faisant la lumière sur les règles et les termes qui régissent les projets extractifs, la transparence des contrats peut aider à lutter contre la corruption et donne aux citoyens les moyens d’évaluer si les recettes obtenues pour leurs ressources sont justes. Ces informations peuvent être cruciales dans des contextes où de précieuses recettes sont impactées par la volatilité des marchés et les politiques émergentes de transition énergétique », peut-on y lire.

Il est généralement admis que la divulgation des contrats extractifs implique que les fonctionnaires et les entreprises feront l’objet d’une surveillance accrue. Cela peut dissuader d’introduire des conditions fiscales faibles ou médiocres. Cela permet aussi de comparer les gouvernements quant à la qualité de leurs négociations avec les entreprises. Finalement, la divulgation permet aux agences gouvernementales autres que le responsable signataire, et à la société civile de surveiller l’exécution des contrats.

L’opacité sur le cadre dans lequel les ressources sont exploitées constitue en effet un risque de perte de revenus. Dans un rapport qu’il a publié en 2021, le Fonds Monétaire International montre comment les budgets des pays d’Afrique Subsaharienne ont subi de fortes contraintes en raison des efforts fournis pour gérer la Covid-19, alors que l’évitement fiscal des multinationales extractives leur fait perdre des sommes allant jusqu’à 750 millions $ par an.

En 2021, le rapport sur l’Etat de la Justice Fiscale publié par Tax Justice Network a mis en évidence le fait que l’Afrique avait perdu 17,1 milliards $ du fait majoritairement des abus fiscaux des multinationales. Pour la région, cela représentait en pleine crise de Covid-19, l’équivalent d’un tiers des budgets de la santé publique. Ainsi les pertes de revenus pour les pays Africains sont les plus importantes en proportion des ressources dont ils ont besoin pour financer leurs objectifs de développement.

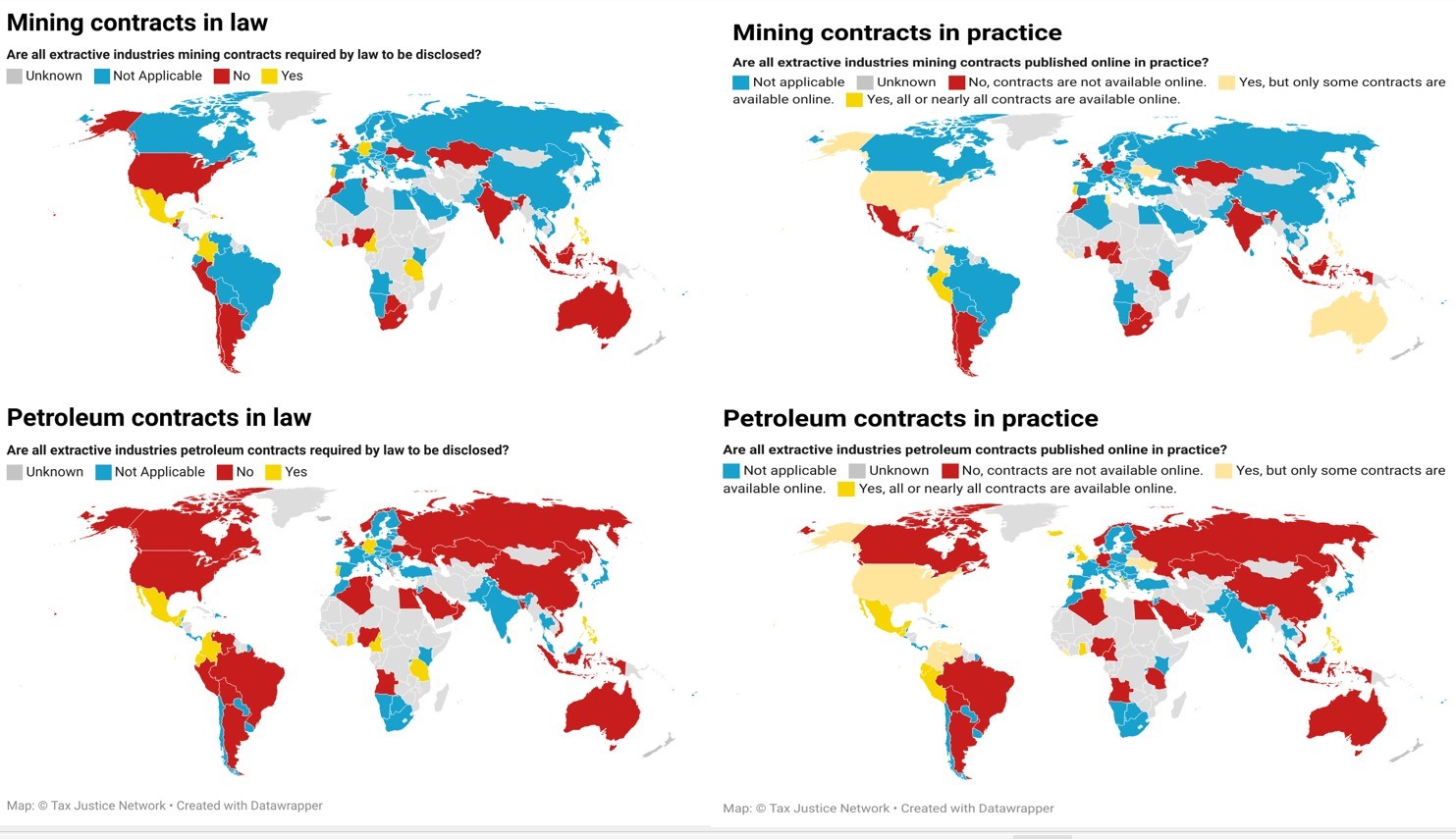

Publication des contrats extractif : Tendances dans le monde et en Afrique selon l’Indice d’Opacité Financière

Dans son édition la plus récente publié le 17 mai 2022, l’Indice d’Opacité Financière produite par les experts de Tax Justice Network met une fois de plus un accent sur la nécessité de transparence en matière de contrats extractifs. L’indicateur clé N°9 qui est exploité dans cet outil, évalue si les lois d’un pays permettent aux citoyens et à toutes les parties intéressées, d’accéder aux conventions signées entre les Etats et les sociétés extractives, et prendre librement et totalement connaissance de leurs contenus

Pour vérifier cela, l’indice examine plusieurs niveaux de transparence sur les contrats pétroliers et miniers. L’aspect sans doute le plus important est celui de savoir si une juridiction a adopté une loi qui impose la publication sans exception de tous les contrats extractifs. Le deuxième aspect de l’analyse concerne la publication effective de ces contrats. Selon qu’ils sont totalement rendus publics et accessibles ou publiés en partie et dans certains cas avec un accès limité ou complexe, un pays recevra une note spécifique. Pour la collecte et l’analyse des informations, l’équipe qui travaille sur l’Indice d’Opacité Financière au sein de Tax Justice Network sert de la mise à jour la plus récente de l’indice de gouvernance des ressources naturelles (pétrole et gaz), qui est produite par l’ONG Natural Ressources Gouvernance Institute (NRGI), et est librement accessible

Parmi les 141 pays analysés par l’Indice d’Opacité Financière, 29 pays sont considérés comme étant des pays miniers et ce nombre atteint 47 pour ce qui est des pays qui produisent le pétrole. Sur les pays concernés par l’exploitation minière, seulement 9 ont adopté des lois qui prescrivent et rendent obligatoire la divulgation des contrats miniers, dont trois en Afrique (Cameroun, Libéria et la Tanzanie). En matière de contrats pétroliers 12 pays dont 4 africains (Ghana, Cameroun, Tanzanie et Libéria) ont des lois qui prescrivent la publication des contrats entre le gouvernement et les multinationales pétrolières.

Cette tendance n’est pas très différente pour ce qui est de la publication effective des dits contrats. Sur les 29 pays analysés qui possèdent des ressources minières, seulement 4 publient la totalité de leurs contrats, 7 le font partiellement, 17 ne le font pas du tout et pour 1 pays cette information n’a pas été recoupée. En matière pétrolière, le nombre des pays qui publient les contrats dans la pratique est de 12, et ceux qui le font partiellement sont au nombre de 6 et enfin, 27 ne le font pas du tout (Pour 2 des pays analysés les informations n’ont pas pu être confirmées).

Transparence des contrats pétroliers et miniers selon les lois et en pratique dans le Monde Source: Financial Secrecy Index 2022

En Afrique, les tendances ne sont pas très différentes. Sur les 18 pays de la région évalués dans le cadre de l’Indice d’Opacité Financière, 9 possèdent du pétrole, et seulement 2 (Ghana et Tunisie), publient la totalité de leurs contrats pétroliers. Le Libéria publie partiellement et des pays comme le Nigéria, l’Angola, et l’Algérie qui sont les trois plus grands producteurs de pétrole de la région, ne publient rien du tout. Dans le secteur des ressources minières, aucun pays ne publie totalement ses contrats. 2 pays, notamment le Libéria et la Tunisie en publient une partie et 7 pays miniers africains ne produisent aucun contrat.

Sur la base de cette analyse, on peut déduire que le Libéria est un exemple de bonnes pratiques en Afrique, pour ce qui est de la divulgation des contrats sur les ressources extractives. Même s’il ne publie que partiellement ses contrats, les autorités y ont adopté des lois qui imposent la publication des contrats miniers et pétroliers. La Tunisie et le Ghana auraient aussi pu être des exemples de bonnes pratiques. Mais le premier ne dispose pas de loi précise en la matière, même s’il publie ses contrats extractifs. Le deuxième est producteur historique d’or en Afrique mais ne possède pas de loi sur la divulgation des contrats dans ce secteur, bien qu’il ait récemment adopté une loi qui prévoit la publication des contrats pétroliers.

Le Cameroun a progressé, mais il doit se hisser au niveau des meilleures pratiques

Dans le cas du Cameroun, il ressort de l’évaluation faite par l’indice d’opacité financière 2022, qu’il existe une loi qui favorise la publication des contrats extractifs. En effet, selon l’article 6 de la loi 2018/011 du 11 juillet 2018 portant transparence et bonne gouvernance dans la gestion des finances publiques, « Les contrats entre l’administrations et les entreprises publiques ou privées, notamment les entreprises d’exploitation des ressources naturelles et les entreprises exploitant des concessions de services publics sont clairs et rendus publics. Ces principes valent tant pour la procédure d’attribution du contrat, que pour son contenu »

Malgré l’existence de cette loi, le Cameroun n’a pas été bien noté dans la publication des contrats. Au moment où l’indice d’opacité financière 2022 était publié et malgré des échanges avec les autorités camerounaises, il n’a été démontré nulle part que le pays publiait ses contrats pétroliers et miniers. Dans sa nouvelle Stratégie Nationale de Développement, les autorités ont pourtant placé le secteur extractif (Gaz et Mines solides), comme un levier de son développement, pour la deuxième partie de sa Vision 2035. Il n’existe aucune plateforme librement accessible au public, où on retrouve les différents titres d’attribution des exploitations extractives.

A la suite de la pression de l’opinion publique après l’initiative d’un membre du parlement, le ministère en charge des mines a décidé de publier la convention d’exploitation de minerai de fer avec le groupe étatique chinois Sinosteel. L’analyse de cette convention révèle que certaines de ses dispositions sont contraires à l’esprit de la loi sur la transparence et la bonne gouvernance au Cameroun, mais aussi en dessous des standards de transparence qui sont fixé par Tax Justice Network, Tax Justice Network Africa, Natural Resources Governance Institute (NRGI), la coalition mondiale Publiez Ce Que Vous Payez, ainsi que d’autres acteurs e la société civile qui plaident pour une plus grande transparence dans le secteur. A l’article 27 de ce document, il ressort que certaines informations sur l’exécution du contrat minier sont frappées de confidentialités et ne peuvent être rendue public. L’article 44 donne la possibilité que soient négociés des accords spéciaux, qui ne sont pas intégrés dans la Convention et qui ne sont pas rendus public. Ces dispositions sont de nature, à favoriser que des avantages soient accordés au partenaire, à la défaveur des intérêts du peuple camerounais et des populations riveraines du site d’exploitation de la ressource. Aussi, des négociations secrètes pourraient négativement affecter la capacité du gouvernement à générer des revenus consistant sur l’exploitation de la ressource.

La transparence sur les contrats extractifs s’applique en partie

La question de la transparence des contrats extractifs est un élément essentiel de l’objectif visant à réduire les abus fiscaux en Afrique et dans tous les pays en voie de développement. De nombreuses juridictions ne sont pas forcément dotés de ressources naturelles, mais sont le lieu d’incorporation de multinationales actives dans le secteur. On peut citer ainsi l’Union Européenne dans son ensemble, ou encore des pays comme la Suisse. La France et l’Italie par exemple, sont les sièges de plusieurs importantes sociétés énergétiques dans le monde à savoir les groupe Total, Areva, ou encore ENI, qui ont des opérations dans le secteur des mines et des hydrocarbures en Afrique. Ainsi, le Parlement et le Conseil européens ont adopté la directive sur la comptabilité et la transparence en 2013, qui contraint les entreprises minières, pétrolières et gazières et les sociétés d’exploitation forestière dépassant une taille définie à déclarer leurs paiements aux gouvernements respectifs des pays où ils sont actifs. Les 27 États membres ont transposé cette directive dans leurs lois internes.

Le 19 juin 2020, le Parlement suisse a révisé son Code des Obligations relatif aux droits des sociétés et de nouvelles dispositions imposent aux entreprises extractives suisses actives dans le domaine du pétrole, du gaz et des minéraux de divulguer les paiements qu’elles effectuent aux gouvernements du monde entier. Cette loi est alignée sur les règles relatives aux industries extractives déjà en place au Canada, dans l’Union Européenne, en Norvège et au Royaume-Uni. Elle s’applique à l’activité des entreprises extractives pour des paiements effectués au-delà de 100 000 francs suisses par an et est en vigueur depuis le 1er janvier 2021.

Bien qu’importantes, ces avancées ne représentent qu’une petite partie des besoins de pleine transparence dans les contrats extractifs. Les entreprises minières et pétrolières sont aussi citées comme apportant leurs soutiens à l’Initiative Pour la Transparence dans les Industries Extractives. Le Conseil International des entreprises du secteur de la Métallurgie et des Mines a aussi fait savoir que l’ensemble de ses membres sont favorables à une plus grande transparence dans les contrats extractifs, et ils s’alignent pour cela sur la mise en pratique du principe de l’ITIE allant dans ce sens.

La transparence est nécessaire, mais elle n’est pas suffisante

Ces avancées demeurent toutefois limitées face à l’objectif de réduire les abus fiscaux dans les industries extractives. Déjà le standard de l’ITIE, ne concernera que les contrats qui ont été signés après le 1er janvier 2021. En Afrique, l’essentiel des contrats d’exploitation datent parfois d’il y a plus de 30 ans. Comme on a pu le voir avec l’indice d’opacité financière, de nombreux pays s’engagent en adoptant des lois favorables à la publication des contrats extractifs. Mais dans la pratique ils sont nombreux à ne rien publier du tout, ou à ne publier que partiellement les contrats concernés. On constate aussi, qu’une fois les contrats publiés, les autres éléments essentiels comme les mises à jour sur les bénéficiaires effectifs, les annexes aux contrats, la gestion environnementale, le financement de l’exploitation du projet, la gestion de la sous-traitance et d’autres informations ne sont pas toujours rendus publiques.

La Vision Minière Africaine qui a été adoptée par l’ensemble des pays du continent met elle aussi un accent sur la transparence dans le secteur extractif, parallèlement à un besoin de changements structurels économiques profonds, pour faire en sorte que les ressources servent les intérêts des populations. La Vision prescrit notamment, que les lois doivent autoriser de bien connaître les personnes derrière les multinationales extractives ainsi que leurs projets. Les conventions doivent aussi faire l’objet de validation par les parlements.

Ainsi, pour promouvoir la transparence fiscale et lutter contre les flux financiers illicites dans le secteur extractif:

Les pays doivent mettre rapidement un cadre qui assure une plus grande transparence sur l’exploitation des ressources extractives, afin de permettre à leurs administrations fiscales d’accéder à des meilleures informations et collecter plus de revenus. Ces dernières ainsi que d’autres institutions de contrôle devront être impliqués dans les processus d’attribution et d’exécution de ces conventions.

Les pays doivent exiger aux multinationales de communiquent périodiquement sur les techniques de planification fiscale qu’elles utilisent.

Les pays doivent adopter des lois qui assurent la disponibilité des informations sur les propriétaires effectifs de toute entreprise minière locale ou étrangère. Ces informations doivent être mises à jour et vérifiées à l’aide de logiciels de traitement automatique des données.

Les pays doivent publier toutes les dépenses fiscales liées aux industries extractives avec des objectifs politiques clairs et évaluer leur efficacité.

Il est important de mettre en place des dispositifs efficaces pour la taxation des plus-values que réalisent les entreprises sur les matières premières en faisant des transactions offshores. Ces transactions sont souvent effectuées entre entités d’un même groupe à des prix arbitraires. Il est aussi commun pour ces multinationales de faire des transferts d’actions à l’étranger, qui cachent effectivement l’acquisition des ressources par une nouvelle entité.

Il est aussi crucial de s’assurer que les zones et entrepôts francs ne soient pas instrumentalisés pour des transactions non contrôlées sur les minerais. A cet effet, les administrations doivent renforcent la coopération et l’échange d’information avec les autorités douanières pour faire en sorte que la valeur des ressources qui transitent par le port correspond aux activités et ressources déclarées.

Il est enfin important que la transparence sur les contrats extractifs, soit au-delà de l’exploitation des ressources, applicable sur les conventions qui sont signées tout au long de la chaîne logistiques, en faisant particulièrement attention aux intermédiaires (sous-traitants, traders, et autres). Ces derniers devraient être soumis à des conditions de transparence sur leurs contrats, et aux mêmes exigences de transparence fiscales et autres différentes législation anti-blanchiment de capitaux.

A mining contract signed by the Government of Cameroon with Sinosteel, a Chinese multinational, for an iron ore project was the centre of controversy in May 2022. Parliamentarians and some activists denounced the contract and demanded its cancellation because the agreement was disadvantageous for Cameroon. In an interview with BBC Africa, the Cameroonian mining minister swept aside all concerns, and the government decided to publish the contract online.

In the same month, Glencore, the Anglo-Swiss multinational that dominates commodities trading, admitted to paying USD $79.6 million through front companies to obtain advantageous oil and gas contracts, including in Cameroon.

These are reminders that people need to know more about the agreements that give foreign companies the right to exploit and trade resources belonging to their countries. State coffers and therefore citizens, always lose out because of hidden deals, weak laws and aggressive corporate tax practices. In most jurisdictions, non-renewable mineral resources are managed by the state on behalf of the people. States typically grant companies the right to explore, extract and often sell mineral resources in exchange for revenue or a share of production. Contracts describes the rights, duties and obligations of both companies and the state, including the fiscal regime. These contracts can span decades and have significant and lasting impacts.

Extractive contracts: why transparency matters

Contract transparency in the extractive industries is essential for fighting against illicit financial flows. In its 2022 Progress Report, the global Extractive Industries Transparency Initiative (EITI) stated: “By shedding light on the rules and terms that govern extractive projects, contract transparency can help fight corruption and empower citizens to assess whether they are getting a fair deal for their resources. This information can be crucial in contexts where valuable revenues are impacted by market volatility and emerging energy transition policies”.

Contract disclosure means that officials and companies will be subject to increased scrutiny. This can deter contacts with weak or poor fiscal terms. It also allows governments to compare the quality of contracts with other jurisdictions. Disclosure allows government agencies other than the agencies that formally enter the contract, and civil society, to monitor contract compliance.

Opacity increases the risk of revenue loss. In a report published in 2021, the International Monetary Fund shows how the budgets of sub-Saharan African countries have been severely constrained by efforts to manage the Covid-19 pandemic, while tax avoidance by multinational extractive companies is costing them up to $750 million a year.

In 2021, the Tax Justice Network, Public Service International and Global Alliance for Tax Justice’s State of Tax Justice report found that Africa had lost USD $17.1 billion, mostly to multinational tax abuse. For the region, this represented the equivalent of a third of public health budgets in the midst of the Covid-19 pandemic.

Disclosure of extractive contracts: global and African trends in the Financial Secrecy Index 2022

In the Tax Justice Network’s Financial Secrecy Index 2022, jurisdictions are assessed for contract transparency. Secrecy Indicator 9 examines whether domestic laws provide for online access to mining and petroleum contracts signed between governments and extractive companies.

To verify this, the index examines several levels of transparency in mining and petroleum contracts. Perhaps the most important aspect is whether a jurisdiction has adopted a law that requires the publication of all extractive contracts without exception. Yet policy is only as good as practice. The analysis reviews whether contracts are actually published. Countries are given scores depending on the level of disclosure in practice, ranging from all/most contracts being made public and accessible, to no contracts being disclosed online. For the collection and analysis of information, the Financial Secrecy Index uses the most recent update of the Natural Resources Governance Index (oil and gas) contract disclosure tracker, maintained by the Natural Resources Governance Institute.

Of the 141 countries analysed by the Financial Secrecy Index 2022, 29 are considered mining countries and 47 are oil producing countries. Of the mining, only 9 have adopted laws that mandate the disclosure of mining contracts, three of which are in Africa (Cameroon, Liberia and Tanzania). With regard to oil contracts, 12 countries, including 4 in Africa (Ghana, Cameroon, Tanzania and Liberia), have laws requiring contract disclosure.

Fewer countries actually publish contracts in practice. Of the 29 mining countries, only 4 publish all of their contracts, 7 do so partially, 17 do not do so at all and for 1 country this information has not been cross-checked. In petroleum, 12 countries publish contracts, 6 publish only some contracts, and 27 do not publish at all (2 countries could not be confirmed).

In Africa, of the 18 countries in the region assessed by the Financial Secrecy Index, 9 have oil, and only 2 (Ghana and Tunisia) publish all their oil contracts. Liberia publishes some contracts and countries like Nigeria, Angola, and Algeria, which are the three largest oil producers in the region, do not publish contacts at all. In the mineral resources sector, no country fully publishes its contracts. Two countries, notably Liberia and Tunisia, publish some contracts and seven African mining countries do not publish any contracts.

Based on this analysis, it can be concluded that Liberia is an example of good practice in Africa in terms of disclosure of extractive resource contracts. Even if it only publishes some of its contracts, the authorities have passed laws that require the publication of mining and oil contracts. Tunisia does not have specific laws for disclosure but it publishes its extractive contracts. While Ghana is a historical gold producer in Africa and has no contract disclosure for mining, it has recently passed a law that provides for publishing oil contracts.

Cameroon has made progress, but needs to catch up with best practice

For Cameroon, the Financial Secrecy Index 2022 shows that the law favours the publication of extractive contracts. Indeed, according to Article 6 of Law 2018/011 on transparency and good governance in the management of public finances, “Contracts between the administration and public or private companies, particularly companies exploiting natural resources and companies operating public service concessions, shall be clear and made public. These principles apply both to the procedure for awarding the contract and to its content”.

Despite the existence of this law, Cameroon has not been rated highly on the publication of contracts by the Financial Secrecy Index 2022. At the time the index was published, and despite exchanges with the Cameroonian authorities, no evidence was provided that the country is publishing its oil and mining contracts. In its new National Development Strategy, the authorities have placed the extractive sector (gas and solid minerals) as a lever for its development in the second part of its Vision 2035. There is also no publicly accessible platform where the different licenses/contracts on extractive operations can be found.

Following pressure from the public after the initiative of a parliamentarian, the Ministry responsible for mining decided to publish the mining contractof iron ore with the Chinese state group Sinosteel. An analysis of this contract reveals that some of its provisions are contrary to the spirit of the law on transparency and good governance in Cameroon, and it also falls short of the transparency standards promoted by the Tax Justice Network, Tax Justice Network-Africa, the Natural Resources Governance Institute, the global Publish What You Pay coalition, as well as other civil society actors who advocate for greater transparency in the sector. Article 27 of this document states that certain information on the execution of the mining contract is confidential and cannot be made public. Further, article 44 provides for the possibility of negotiating special agreements, which are not integrated into the main contract and are not made public. These provisions are likely to favour the company, to the detriment of the interests of the Cameroonian people and the populations living near the mine. Secret negotiations could also negatively affect the government’s ability to generate consistent revenue from the exploitation of the resource.

Transparency in headquarter jurisdictions

The issue of transparency of extractive contracts is key to reducing tax abuse in Africa and all developing countries. Many jurisdictions are not necessarily endowed with natural resources, but are home to multinational companies active in the sector. These include European Union countries as a whole, and countries such as Switzerland. France and Italy, for example, are home to several of the world’s leading energy companies, including Total, Areva, and ENI, which have mining and hydrocarbon operations in Africa. The European Parliament and Council adopted the directive on accounting and transparency in 2013, which obliges mining, oil and gas companies and logging companies above a defined size to report their payments to the respective governments of the countries where they operate. All 27 Member States have transposed this directive into their national laws.

On 19 June 2020, the Swiss Parliament revised its Code of Obligations relating to company rights and new provisions require Swiss extractive companies active in oil, gas and minerals to disclose payments they make to governments around the world. This law is aligned with the extractive industries rules already in place in Canada, the European Union, Norway and the United Kingdom. The law applies to companies’ extractive activity for payments above 100,000 Swiss francs per year and runs from 1 January 2021.

While important, these advances represent only a small part of the need for full transparency in extractive contracts. Mining and oil companies are also cited as supporting at the Extractive Industries Transparency Initiative. The International Council of Mining and Metals Companies has also indicated that all of its members are in favour of greater transparency in extractive contracts, and are aligned with the implementation of the EITI principle .

Transparency is necessary, but not sufficient

Yet advances remain limited where the objective is to fundamentally reduce abuse in the extractive industries. The EITI standard on contract transparency, for example, only applies to contracts signed after 1 January 2021. In Africa, the bulk of contracts are more than 30 years old. And as the Financial Secrecy Index shows, while many countries adopt laws for contract disclosure, in practice, many countries do not publish at all, or only some contracts. Further, once contracts are published, other essential elements such as updates on beneficial owners, contract annexes, environmental management, project financing, and subcontracts are not made public.

The Africa Mining Vision, which has been adopted by all African countries, also places an emphasis on transparency across the mineral value chain, alongside deep economic structural changes to ensure resources work for the people. In particular, the Africa Mining Vision states that laws should allow for a clear understanding of the people behind multinational extractive companies and their projects. Contracts must also be approved by parliamentarians.

Further, to promote fiscal transparency in the extractive sector and tackle illicit financial flows:

Countries need to rapidly put in place a framework that ensures greater transparency on the exploitation of extractive resources, to enable their tax administrations to access better information and collect more revenues. Tax authorities and other oversight institutions should be involved in the awarding and implementation of these agreements.

Countries should require multinationals to report periodically on any tax avoidance schemes they use.

Countries should adopt laws that ensure the availability of information on the beneficial owners of all legal entities. This information should be updated and verified.

Capital gains must be effectively taxed, so that, for example, when junior exploration companies sell rights, often through offshore structures, profits are not shifted.

Countries should publish all tax expenditures related to the extractive industries with clear policy goals and evaluate their effectiveness.

Production transparency and monitoring is necessary to prevent under-declarations which can undermine the collection of royalties and be used to shift profits out of the source country.

Contract transparency must go beyond the primary contracts. It should be applicable to the agreements that are signed along the supply chain, paying particular attention to intermediaries (subcontractors, traders and others). They should be subject to contract transparency, and also to the same requirements of fiscal transparency and different anti-money laundering legislation.

The etymology of tax is “to fix”, and so…we ask ourselves “how can tax help address racial wealth inequality[and] repair the harms of structural racism that are embedded into our economic system?”

These are crucial questions. And it’s taken many of us involved in movements to tackle the world’s inequalities far too long to engage with them.

In partnership with our sister organisation Tax Justice UK, we at the Tax Justice Network collaborated with Guppi Bola of Decolonising Economics who has written a report which is the first of its kind in the UK:“Tax as a Tool for Racial Justice”. Decolonising Economics works to build a solidarity economy rooted in racial justice principles and you can read more about the organisation and its work here.

As it begins, the report “is intended to be a framework for future research, organising and campaigns for racial justice.”

To discuss the report, first presented by Guppi Bola, and next steps for campaigners and researchers, we brought together a panel of experts: Keston K. Perry Assistant Professor of Africana Studies, Williams College, Stephanie Brobbey Founder and CEO of the Good Ancestor Movement and Priya Lukka Economist in International Development. You can watch the launch of the report here:

You can also listen to Guppi Bola of Decolonising Economics speaking with Naomi Fowler on the Tax Justice Network podcast the Taxcast in more depth about the report here:

~ Tax and Racial Justice, Taxcast, September 2022

While in Britain there’s a big knowledge and research gap (as is unfortunately the case in many countries), in the United States there’s been some great work on tax histories and tax justice principles as they apply to racial justice, notably the work of the excellent Center on Budget and Policy Priorities and Professor Dorothy Brown’s The Whiteness of Wealth:how the US tax system impoverishes black Americans – and how we can fix it’, plus so much more.

You can hear Professor Brown’s keynote speech here at the Tax Justice Network 2021 conference. You can also hear her in conversation on our podcast the Taxcast, where she explains how the doors weren’t open to her work in this area: “Let’s be clear – when I started writing about race and tax, I was not – my scholarship nor I were welcomed by the white male law professor tax gatekeepers.”

Here’s a great twitter thread from Brakeyshia R. Samms listing US research:

I know it's not as popular as #EconTwitter, but the silence of #TaxTwitter on systemic racism is equally as disturbing & disappointing. We all know the tax system is not immune to racism.

Here's some research that should be required reading for all, not just tax experts:

— Brakeyshia R. Samms (she/her) (@BrakeyshiaSamms) June 1, 2020

Below is a list of resources which may also be of interest, some of which were shared during the launch. Please do add your suggestions in the comments section, we’ll be happy to have them.

Firstly we’re sharing links to the Taxcast, some of our monthly podcast editions which explore this area. All previous episodes are available here. (You can also find podcasts on that site in Spanish – Justicia ImPositiva, French – Impôts et Justice Sociale, Portuguese – É Da Sua Conta, and Arabic – الجباية ببساطة)

Decolonising Economics event looking into racial hierarchies, enslaved labour and indentured labour, reparations and wealth disparities: watch it here.

A report that aims to reclaim the educational space from the market

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa con Marcelo Justo and Marta Nuñez:

El nuevo discurso en América Latina sobre la evasión fiscal y el mundo offshore

Chile: ¿Qué va a pasar con la constitución?

América Latina y Estados Unidos en el nuevo contexto global

Y en nuestra miniserie sobre que son los paraísos fiscales, analizamos el impacto del Crimen Organizado

Ireland’s long-running battle with the European Union over Apple’s unpaid taxes has more than demonstrated the country’s dogged determination to continue facilitating massive levels of corporate tax avoidance. Pressure for reform in the ‘land of 100,000 welcomes’ is building, however. Next month in Geneva, Ireland’s tax policies will once again come under the spotlight when the United Nations Committee on the Rights of the Child considers evidence from civil society organisations. The meeting comes ahead of Ireland’s appearance before the Committee in early 2023, at which its compliance with the Convention on the Rights of the Child will be formally interrogated by a panel of UN experts.

The Committee has already set its sights on the human rights impacts of Ireland’s fiscal regime, particularly as they pertain to lower income countries, having raised the issue in November 2020. A coalition of Irish and Ghanaian organisations fighting for tax justice has now made a follow-up submission to the Committee setting out in detail the manifold ways Ireland siphons revenue away from poorer countries and the devastating human rights impacts this incurs.

Perhaps the best-known aspect of Ireland’s role in international tax abuse is its facilitation of profit shifting by multinational corporations. As the submission demonstrates, the legal structures offered by the country in order to enable such practices have evolved over time, but progress in putting an end to profit shifting has remained meagre at best. The government has used superficial reforms to argue it has closed loopholes, but the notorious ‘Double Irish’ tax avoidance structure has simply given way to the ‘Single Malt’ which allows companies to achieve the same result through alternative channels.

Ireland’s extensive network of 73 bilateral tax treaties, in combination with these ignominious fiscal structures, make it a prime destination for companies seeking to shift their profits out of other countries and thereby avoid paying their fair share of tax. What’s more, the country has been specifically targeting emerging African economies for such agreements in recent years, despite serious concerns that its aggressive negotiating tactics have led to deleterious outcomes for partners such as Ghana. Indeed, research carried out by the Government Revenue and Development Estimations (GRADE) initiative at St Andrew’s University shows that revenue lost to corporate profit shifting from the West African country in a single year would otherwise have saved the lives of 170 children. The Tax Justice Network’s State of Tax Justice report meanwhile estimates that Ghana loses US $166 million a year – the equivalent of 19% of its health budget – to cross-border tax abuse. In total, Ireland imposes revenue losses of some US $19 billion a year on other countries, according to our calculations.

When challenged about the nefarious impacts of its tax havenry, Ireland’s government has generally pointed to a 2015 spillover analysis commissioned by its Department of Finance which, the country argues, shows it has no negative impact on developing countries. Said analysis is seriously flawed however; it only examined 13 of the developing countries which receive investment flows from Ireland, and only 4 percent of the available data on Irish overseas investment.

Moreover, Ireland’s role in undermining human right in other countries is not limited to its direct facilitation of international tax abuse. Like all states that have signed up to the major UN human rights agreements, it is also subject to extraterritorial obligations to respect, protect and fulfil human rights through its participation in institutions of international governance.

These principles appear to have been ignored when Ireland fought hard to water down proposals at the OECD for a global minimum corporate tax rate, and thereby helped ensure the final agreement – ostensibly intended to end the ‘race to the bottom’ in corporate taxation – would bring little or no benefit for poorer nations.

Similarly, the country continues to resolutely oppose proposals for international tax talks to be moved from the OECD to the UN, and for the creation of a new global tax convention under the auspices of the same body. Both of these measures represent long-standing demands of civil society organisations and governments across the Global South, as lower income countries could participate on a more equal footing at the United Nations.

Having always valued its reputation as a champion of human rights and solidarity on the international stage, Ireland needs to deliver a sea change in both its policy positions and its comportment in tax negotiations if these values are to be reflected in its fiscal regime and relationships.

Welcome to the 57th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

أزمة الديون المصرية والخصخصة المتسرعة

في العدد 57 من الجباية ببساطة سلّطنا الضوء على أزمة الديون الخارجية في مصر وما يرافقها من خصخصة “متسرعة” ومدى تأثير ذلك على حياة المواطن البسيط وهل من تشابه مع السيناريو السيرلنكي من خلال لقاء مع الباحثة الإقتصادية والصحفية بموقع مدى مصر بيسان كساب.

In episode #57, we interview Egyptian economic journalist and researcher Beesan Kassab, and discuss Egypt’s current foreign debt crisis, how it is affecting citizens’ livelihoods, and how it compares to the ongoing crisis in Sri Lanka.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Pour cette 43ème édition de votre Podcast en français sur la justice fiscale et la justice sociale produit par Tax Justice Network, nous revenons sur les exonérations fiscales en matière de dépenses financées par l’Aide Internationale au Développement. La question a fait l’objet de discussions dans le cadre des « Journées pour la Fiscalité du Développement » organisées il y a quelques temps par l’OCDE. Plusieurs experts ayant pris la parole ont partagé les réflexions les plus récentes sur cette problématique. Sont intervenants dans ce podcast:

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to our monthly podcast in Portuguese, É da sua conta (‘it’s your business’) produced and hosted by Grazielle David and Daniela Stefano. All our podcasts are unique productions in five different languages – English, Spanish, Arabic, French, Portuguese. They’re all available here. Here’s the latest episode, CARF permite sonegações bilionárias no Brasil #40:

Cerca de 1 trilhão de reais (USD 192 bi) está para ser julgado no CARF, o Conselho Administrativo de Recursos Fiscais. Mas o que é CARF? O que está sendo julgado? De quem é esse dinheiro? E se grandes corporações e super ricos não pagam impostos, de onde vem o dinheiro para políticas públicas? Tem solução? Essas e outras questões estão respondidas do episódio #40 do É da Sua Conta.

Você ouve no É da sua conta #40:

CARF é órgão público a serviço de grandes corporações e super ricos: metade dos conselheiros é indicada por confederações de empresas.

Herança patrimonialista: não há nada como o CARF no resto do mundo.

CARF favorece desigualdades: se os que mais têm não pagam seus impostos devidos, sobra para quem menos tem pagar mais tributos. Exemplos são o aumento de impostos sobre bens e serviços e a não correção da tabela do imposto de renda, fazendo com que mais assalariados de menor renda tenham que pagá-lo.

Exemplos positivos: saiba como se recorre a uma decisão tributária nos países nórdicos.

Há saída: Instituto de Justiça Fiscal propõe alterações no CARF que favorecem toda população.

Ricardo Fagundes da Silveira, auditor fiscal da Receita Federal e membro do Conselho Consultivo do Instituto de Justiça Fiscal

“ O Itaú deixa de recolher 60 bilhões. A Ambev, 30 bilhões. Aquilo que deixa de ser recolhido ao cofre público vai estar amanhã remunerando, na forma de dividendos, os grandes acionistas.” (Ricardo Fagundes Silveira, Instituto de Justiça Fiscal)

“Os pequenos contribuintes serão sacrificados porque serão chamados a cobrir o rombo deixado pelos grandes sonegadores. É um código que nada ajuda os contribuintes, em nada ajuda a sociedade brasileira.” ( Isac Falcão, Sindifisco Nacional)

“Quando o próprio Estado toma posições mais agressivas do que um consultor tributário, acende um alerta em relação às atittudes anti-republicanas, em relação ao futuro. Isso é sair muito da estrada do caminho do desenvolvimento.” (Marcio Calvet Neves, Instituto de Justiça Fiscal)

Welcome to the 56th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

في هذا العدد السادس والخمسون #٥٦ من الجباية ببساطة نقدم موجز للحلقات التي قام البودكاست بإذاعتها في النصف الأول من عام ٢٠٢٢

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa:

La asunción de Petro en Colombia y el nuevo equilibrio geopolítico en sudamérica.

Estados Unidos contra China, Occidente contra Oriente, ¿quién está ganando la batalla económica?

Los billonarios y la evasión fiscal en un nuevo capítulo de la miniserie qué son los paraísos fiscales.

Edmund Fitzegerald, miembro de ICRICT, la Comisión Independiente para la reforma de la Fiscalidad corporativa internacional (Twitter: https://www.twitter.com/icrict)

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Pour cette 42ème édition de votre Podcast en Français produit par Tax Justice Network, nous revenons sur la publication par l’OCDE et l’ATAF du rapport annuel sur la transparence fiscale en Afrique, en vous proposant de reécouter certains aspects spécifiques.. Selon la méthodologie de ce rapport, les pays africains continuent de fournir des efforts dans ce domaine et les choses évoluent. Mais de nombreux défis subsistent encore pour parvenir à un niveau pertinent de transparence dans le secteur de la fiscalité sur le continent. Nous revenons aussi sur un séminaire de formation mené en fin juillet 2022 par l’Organisation Africaine des Institutions Supérieures de Contrôle. Lesdits travaux étaient menés en préparation à la réalisation d’un audit général sur les Flux Financiers Illicites en Afrique. Nous avons discuté avec quelques responsables de cette organisation.

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

The Tax Justice Network made an intervention at the European Parliament’s Expert meeting on the Unshell Directive on 12 July 2022. The intervention was presented by Moran Hariri, lead researcher indices at the Tax Justice Network, on the behalf of the organisation. The full text of the intervention is shared below.

First of all, we would like to thank you for the invitation to speak at this important meeting and present our views regarding the Unshell directive.