The upcoming 27th Session of the Committee of Experts on International Cooperation in Tax Matters, hosted in Geneva, is poised to continue a crucial discussion on net wealth taxes. This United Nations body, comprising specialists from diverse countries, will examine a report that elucidates the design and implementation mechanisms of these taxes.

In this significant moment, the Tax Justice Network, in collaboration with partner organisations including ActionAid International, Financial Transparency Coalition, Oxfam, and Patriotic Millionaires, is pleased to release a joint statement. Together, we acknowledge the Committee’s dedication to formulating practical guidance on wealth taxation policies, particularly with regard to net wealth taxes.

Our statement underscores the alarming reality of widening disparities, both between nations and within them. It highlights the intersections of multifaceted inequalities spanning gender, race, religion, disability and socio-economic class, emphasising the pressing need for structural reforms. The exponential surge of concentrated private wealth, shielded from equitable taxation by opaque financial systems, requires bold and effective responses.

The joint statement advocates for the implementation of a net wealth tax as a potent tool in the fight against inequality and the promotion of social justice, aligning perfectly with the Sustainable Development Goals. The revenue generated from taxing wealth can be vital for low income countries, strengthening fiscal capacity and enabling the provision of vital public services. We extend our commendations to the Subcommittee on Wealth and Solidarity Taxes for their efforts in providing guidance on a range of wealth taxation options. We call for the approval of the subcommittee’s recommendations on wealth taxes and urge the provision of additional guidance, including the formulation of model wealth tax legislation, to establish a unified approach worldwide, thus curbing tax avoidance.

In addition, we stress the importance of expanding the international framework for the exchange of information, essential for the efficient administration of wealth taxes. Recognising that net wealth taxes primarily target the wealthiest segments of society, we propose the establishment of a global asset registry. This would ensure comprehensive transparency regarding all relevant assets, thwarting attempts to conceal wealth offshore.

This pivotal report could mark a substantial step towards global equity. We encourage nations to work together and implement comprehensive wealth taxation policies, edging us closer to a more equitable future. The journey to tax justice is ongoing, and every stride in the right direction brings us nearer to a fairer world.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast. (All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here.)

En este programa con Marcelo Justo y Marta Nuñez:

Naciones Unidas da un paso por la justicia fiscal y social.

La situación en México y Brasil, las dos economías más grandes de la región.

En nuestra miniserie sobre los 10 mitos fiscales, el mito número seis y el número siete: mito número 6: para crecer hay que bajar los impuestos

Y mito Número 7: Las grandes corporaciones son las que pagan más impuestos.

Oscar Ugarteche director del Observatorio Económico latinoamericano, OBELA, profesor de la Universidad Nacional Autonoma de Mexico, la UNAM y autor de Historia Critica del FMI

Martin Mangas investigador Universidad Nacional General Sarmiento Argentina, miembro del Espacio de Trabajo para la Equidad fiscal (ETFE), y contribuidor a “Mitos impuestos: una guía para disputar ideas de lo fiscal”

Adrian Falco Coordinador del Programa de Integración Regional de la Fundación SES de Argentina. Miembro del Espacio de Trabajo para la Equidad fiscal (ETFE), y contribuidor a “Mitos impuestos: una guía para disputar ideas de lo fiscal”

Welcome to the 70th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here.

في العدد #70 من بودكاست “الجباية ببساطة” يستضيف وليد بن رحومة الباحث في العلوم السياسية ومدير منتدى البدائل العربي محمد العجاتي للحديث عن إجتماعات البنك الدولي وصندوق النقد في مراكش بالمملكة المغربية، ومدى تأثيرها في مآل عدد من القضايا الإقتصادية والإجتماعية التي تهم المنطقة العربية.

In episode #70 of the “Taxes Simply” podcast, Walid Ben Rhouma hosts social scientist and director of the Arab Forum for Alternatives, Mohammed El Agaty, where they discuss the upcoming World Bank and IMF meetings in Marrakech and their potential impact on the future of the major economic and social issues in the Arab region.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Dans ce nouvel épisode de votre podcast Impôts et Justice Sociale nous explorons les enjeux du changement climatique et comment les gouvernements africains financent leur réponse face à ses répercussions. Lors de la Semaine Africaine du Climat, nous avons eu l’opportunité d’échanger avec Nassim Oulmane. Expert en économie bleue, M. Oulmane dirige actuellement la division dédiée aux Technologies, au Changement Climatique et à la gestion des ressources naturelles au sein de la Commission des Nations Unies pour l’Afrique. Ensemble, nous abordons la crise climatique en Afrique et examinons comment les ressources fiscales internes peuvent contribuer à la mobilisation des fonds nécessaires à l’adaptation et à l’atténuation de ses effets.

Invité de cet épisode :

Nassim Oulmane : Responsable par intérim de la Division Technologie, Changement Climatique et Gestion des Ressources Naturelles au sein de l’UNECA

~ Fortunes africaines: Une urgence pour les administrations fiscales #54

Vous pouvez suivre le Podcast sur:

Le télécharger pour l’écouter hors connexion sous le sous ce lien

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

The Tax Justice Network and Coventry University, partners in the EU 2020 Horizon TRACE project, have recently responded to a call for evidence regarding the Criminalisation of Money Laundering Directive, in which we highlighted critical loopholes and provided recommendations to improve the EU’s ability to combat money laundering effectively.

Here are our main recommendations which in our view can provide the EU with a roadmap for a more effective regulatory framework:

Harmonising taxcrime definitions

One key area of concern is the lack of harmonisation in the definitions of tax crimes among EU member states (see pages 236 onwards in this Oxford University Press Open Access Book). While tax evasion and fraud are criminal offences across the EU, there are significant disparities in how these crimes are defined and penalised. Definitional variations of tax offences serve as critical enablers of cross-border tax crime in the EU, as it frustrates investigation efforts.

We therefore recommend harmonising the definitions of tax crimes. By eliminating definitional inconsistencies, the EU can prevent dubious individuals and multinational corporations from exploiting legal loopholes to evade taxes and engage in money laundering.

Leveraging technological innovation

As technology continues to evolve, so do the techniques and tools employed by money launderers. The TRACE project has revealed that emerging technologies, such as artificial intelligence, have enabled increasingly sophisticated money laundering methods in various sectors, including art, gambling, and cryptocurrency.

To address these risks, the directive must be updated to account for the opportunities and challenges presented by technology including the use of artificial intelligence tools to track illicit financial flows more effectively.

Protecting whistle blowers

Whistle blowers play a crucial role in uncovering money laundering activities. Their actions enhance transparency and support law enforcement agencies in exposing financial crimes. While the EU has a Whistle-blower Protection Directive, this protection should extend to the directive on the criminalisation of money laundering. Incorporating whistle blowing protection provisions into this directive would highlight the vital role that whistle blowers play in the fight against money laundering and tax crimes.

Transparency of legal entities and arrangements

Identifying the individuals that ultimately control and benefit from legal entities is essential to preventing tax evasion, money laundering, corruption, and terrorism financing. To improve transparency, the EU should invest in a robust beneficial ownership framework, ensuring that information is accessible to the public.

While progress has been made in establishing beneficial ownership registries, challenges remain. Some countries have not effectively eliminated the use of bearer shares, which introduces secrecy risks. The EU should encourage member states to close these loopholes and prevent the use of bearer shares.

Enhancing public access to beneficial ownership data

Public disclosure of beneficial ownership information is crucial for preventing financial crimes. Accessible data allows civil society organisations, journalists, and authorities to hold individuals accountable for their actions. Up until October 2022, public access to such information had been gradually improving, and according to the Tax Justice Network’s assessment, laws requiring beneficial ownership to be registered with a government authority have been approved in a total of 97 jurisdictions. However, in November 2022, a ruling by the EU Court of Justice disrupted this trend by invalidating public access to beneficial ownership information for local legal entities within the EU in the context of combating money laundering. Nonetheless, as the Tax Justice Network reported in July 2023, some EU countries have chosen to maintain their public registers, a practice that should be encouraged throughout the Union.

Verification mechanisms for beneficial ownership data

Ensuring the accuracy and legitimacy of beneficial ownership information is vital. The EU should use interconnected government and public databases to verify and maintain consistent ownership data within and across member states. Implementing advanced big data analytics and automated IT systems can help detect suspicious cases and streamline the verification process (as outlined in the Tax Justice Network’s Roadmap to Effective Beneficial Ownership Transparency (REBOT) paper in greater detail).

Applying awhole of government approach to data and maximising synergies between policies

Illicit financial flows often intersect with multiple crimes and social issues. To address these challenges comprehensively, beyond the imperative of ensuring that authorities possess adequate and verified information, the EU needs legal frameworks and tools that ensure that once data is registered, it becomes accessible to all pertinent stakeholders. The absence of collaboration and a fragmented approach to tackling illicit financial activities can result in scenarios where critical information exists but remains unshared among relevant authorities, whether domestically or internationally. Applying a whole of government approach to data should also consider multiple angles, such as corruption, national security, tax abuse, and social inequalities. This is likely to facilitate more effective prosecution of money laundering offenses.

A good example is the use of data collected as part of the common reporting standard. While this has improved data sharing for tax purposes, limitations prevent broader use of this data (eg for preventing money laundering). The EU should ensure that data shared for tax purposes can also be accessed by authorities responsible for preventing, investigating, and prosecuting money laundering offenses.

Publishing common reporting standard data and other statistics

Making data publicly available and interconnected is a powerful tool in preventing financial crimes. Public access to anonymised statistics, such as those collected through the common reporting standard, can help stakeholders identify potential offences and anomalies. The EU should consider publishing common reporting standard data and other statistics to improve transparency and understanding of money laundering patterns.

An ongoing battle

The fight against money laundering is an ongoing battle that requires constant adaptation to evolving techniques and technologies. In closing these critical loopholes, the EU can strengthen its fight against money laundering, protect its financial system’s integrity, and contribute to a safer and more transparent global economy.

You’re likely reading this using technology containing minerals that once lay far below Africa’s mineral-rich soils. For the African continent is home to almost one-third of the world’s mineral reserves.

If you dig a bit deeper though, you’d find there’s some healing needed in the relationships between extracting minerals and society across the continent, and the world. Although natural resources account for almost one-third of total government revenue in some African countries, tax avoidance by mining multinational companies may cost sub-Saharan Africa as much as US$730 million per year in corporate income tax, according to the International Monetary Fund. The resulting inadequate funds means our public services – our schools, hospitals, and roads in Africa – don’t serve us as well as they could. It also hampers governments in introducing more progressive tax systems.

Government coffers are emptier than they should be, and as if this wasn’t enough, African governments are also grappling with the impacts of the climate crisis on their people. They’re coping with the fallout from flooding and droughts, sometimes within the same national borders, sometimes only months apart.

Current global carbon emissions reflect the deep inequalities in and across nations. Southern and Eastern Africa have the lowest emissions in the world. Sub-Saharan Africa could increase its per capita emissions by 20 per cent and still be in line with the agreed 1.5 degrees Celsius ceiling of the global pact for climate change, the Paris Agreement. Unfortunately, other regions have far exceeded their fair share. Scientists have issued a wake up call that we have already transgressed six of nine planetary boundaries and so we know what’s been agreed in itself isn’t enough.

Africa’s resource futures

The future of Africa’s extractive industries hangs in the balance as the demand for fossil fuels dips with international efforts to keep global warming below the 1.5 degrees Celsius. For almost half of African countries, two fossil fuels—petroleum and coal—are the most plentiful resources. African nations facing the risk of stranded assets, such as Chad, the Republic of Congo, Gabon, Mozambique, and Nigeria, may be counting on these resources for revenue and to meet domestic energy needs.

Yet new markets and greater demand for metals and minerals needed for low-carbon technologies – of which Africa has many – are promising. As Marit Kitaw, Interim Director the African Minerals Development Center (AMDC), writes

As global demand for batteries, electric vehicles, and renewable-energy equipment surges, African countries could harness their large deposits of minerals for the goal of fostering green industrialization. This would enable the continent to meet development objectives while also tackling climate change.

Marit Kitaw, September 2023, ‘Making the Most of Africa’s Strategic Green Minerals’, Project Syndicate

However, simply transitioning from fossil fuels to “green” minerals without accompanying systemic transformation to international tax rules and African industrial policy would enable ongoing corporate tax abuse and raw-material exports.

The Africa Mining Vision – adopted by all African Union members in 2009 to tackle “the paradox of great mineral wealth existing side by side with pervasive poverty” – seeks to transform mining from primarily export-driven extraction traded on markets outside the continent, to more extraction integrated into industrial policy, including domestic value addition and deliberate linkages to other sectors.

We, the writers of this article – Mukupa and Rachel – took these intersecting, complex conditions to heart and thought about how one treatment, tax, can help in the healing.

The 5 principles of tax justice include raising revenue, redistributing wealth to create a more equal society, repricing to make activities that infringe on the rights of others more costly, improving representation by reinforcing the social contract between voters and representatives, and supporting reparations to redress historical and colonial legacies.

African nations have been tackling the challenges posed by the existing international tax system for decades. For the last 60 years, decision-making on international tax has been confined to the Organisation for Economic Co-operation and Development (OECD), a membership body of the world’s richest nations, where no African nation is a member. In a historic move in 2022, Nigeria, on behalf of the Africa Group, put forward a resolution at the United Nations to start intergovernmental discussions on international taxation with a view to setting up an intergovernmental tax body within the UN. It was adopted by unanimous consensus.

The road to recovery

Last year’s UN resolution is good news for all. But OECD member states and their dependencies – responsible for almost 7 in every 10 dollars lost to corporate tax abuse – are not going to accept the necessary transformations easily, even though most of their citizens are also adversely affected by an unfair international tax system. These are the very same nations that are historically and currently most responsible for the climate crisis because of their greenhouse gas emissions.

The next months are pivotal. António Guterres, the Secretary-General of the UN, published a ground-breaking report in August 2023, which confirms much of the analysis by members of the Global Alliance of Tax Justice, setting out three options for progress on international tax within the auspices of the UN.

At the UN General Assembly last week, the moderator of the debate concluded that a consensus had emerged around the central option of the three proposed in his report: a framework convention on tax. This is the longstanding aim of tax justice campaigners. Yet the UK, the US, and the EU with its powerful members, countries most responsible for enabling much of the tax losses – and yet suffering themselves in terms of absolute losses – were conspicuously silent.

Tax justice is a deeply needed planetary salve. As Guterres wrote,

The present report comes amid increasingly urgent concerns that the international financial architecture, and with it the international tax system, have not sufficiently supported the post-pandemic economic recovery, financing of the Sustainable Development Goals and climate action.

Report of the Secretary-General ‘Promotion of inclusive and effective international tax cooperation at the United Nations’, 2023

We hope our brief here sparks further thought for the role of tax in Africa’s resource-rich nations in light of the climate crisis. Given their shared vision and common objectives with Guterres’ report, we join the call for greater collaboration between the feminist, tax justice and climate justice movements.

You can download the brief The Principles of Tax Justice and the Climate Crisis in Africa’s Resource-Rich Nationshere.

Poluição por combustíveis fósseis; contaminação do solo, rios, animais e vida humana por agrotóxicos. Tabaco, bebidas alcoólicas e ultraprocessados que prejudicam a saúde. A tributação pode colaborar para desincentivar estas e outras práticas nocivas.

O episódio #53 do É da Sua Conta explica como funciona a reprecificação com o imposto seletivo, ferramenta que, se bem desenhada, pode diminuir o efeito da crise climática, melhorar a saúde das pessoas e combater desigualdades. Grandes corporações, que contaminam mais, devem contribuir mais!

Reprecificação: Florencia Lorenzo, da Tax Justice Network, explica como a reprecificação, um dos 5 “Rs” da justiça fiscal pode contribuir no combate à crise climática, na promoção de uma alimentação mais saudável e no desincentivo de outras práticas que fazem mal à saúde e ao meio ambiente.

Bob Michel da Tax Justice Network traz evidências científicas de que imposto seletivo desincentiva práticas nocivas, como o tabagismo, na Europa.

Reforma tributária no Brasil deve ser sustentável e prever transição para economia menos poluente através de impostos seletivos para combustíveis fósseis e agrotóxicos, comenta Mateus Fernandes, do Instituto Democracia e Sustentabilidade.

Imposto seletivo para bebidas alcoólicas e ultraprocessados devem constar da reforma tributária brasileira. A proposta é da ACT Promoção da Saúde e Marcello Baird acredita que o projeto de lei que tramita no congresso nacional pode estar entre os pioneiros no mundo se for aprovado com estas medidas.

“Trata-se de tentar mudar o comportamento de grandes empresas, de grandes fundos de investimentos, para reorientar a economia para que quando façam suas decisões econômicas, levem em conta também o custo social dessa decisão de investimento.” ~ Florencia Lorenzo, Tax Justice Network

“Nos países europeus, a introdução do imposto seletivo sobre o consumo de cigarro onde esse tipo de imposto era uma novidade reduziu nitidamente o número de fumantes.” ~ Bob Michel, Tax Justice Network

“Qual é a nova revolução verde que a gente precisa fazer? Vai continuar sendo baseada em agrotóxicos, que recebem algo em torno de R$ 350 bilhões de incentivos por ano?” ~ Mateus Fernandes, Instituto Democracia e Sustentabilidade

“Imposto seletivo é uma medida super importante para desestimular o consumo de ultraprocessados. Há inúmeros dados que mostram como esses produtos são prejudiciais à saúde das pessoas, causando mortes e adoecimentos” ~ Marcello Baird, ACT Promoção da Saúde

Participantes:

Antonia, agricultora ribeirinha brejeira no Sul do Piauí

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here. In this edition of the Taxcast:

The US government has spent an estimated $1 trillion on their ‘war on drugs.’ But, in more than 50 years, the cross-border flows of illegal drugs, arms and money have increased. It’s a mess. And it didn’t need to be this way. In part one of a two part series, we look at the failed so-called ‘war on drugs’ and how to stop wasting precious lives. We start with the supposed ‘goodies’ and the ‘baddies’ and the real crime story…

“The toughest laws created the toughest criminals. The only thing we’re doing is increasing the violence. And at this point, where we are now, only the most violent will survive. We have to ask about political will here. What are the interests of the countries and other major players involved?”

~ Karina Garcia-Reyes

“It was always about the US and the UK in particular, protecting and leveraging their own national trading interests on both sides of the Atlantic. Western countries were never going to put the trillions used on the war on drugs into combating financial secrecy havens.”

~ Dr Mary Young

“The tools of tax avoidance are the same tools that enable the illicit drug trade’s extraordinary resilience to prohibition.”

Here’s a summary of this Taxcast edition, part 1 of Drug War Myths:

Naomi Fowler: On the Taxcast this month, and in next month’s episode, we’re going to look at the so-called ‘war on drugs’ and how to stop wasting precious lives. In part one, the supposed ‘goodies’ and the ‘baddies.’

Here’s President Nixon more than 50 years ago, back in 1971:

Nixon:America’s public enemy number one in the United States is drug abuse. In order to fight and defeat this enemy it is necessary to wage a new all-out offensive. I’ve asked the Congress to provide the legislative authority and the funds to fuel this kind of an offensive. This will be a worldwide offensive. If we’re going to have a successful offensive we need more money. If this is not enough, more will be provided.

Naomi Fowler VO: Since that announcement, the US government has spent an estimated $1 trillion on their ‘war on drugs.’ But the cross-border flows of illegal drugs, arms and money has increased steadily. There are contradictions everywhere you look along this chain of misery: it’s the United States that’s the biggest consumer country of illegal drugs and not really the producer countries like Colombia, Afghanistan and Jamaica.

In Mexico alone, an estimated 80% of the weapons used by organised gangs are manufactured in the United States – that’s a common story in many countries.

And as for money-laundering from the illegal drug trade, the two biggest facilitators and end destinations are the US and UK financial systems.

It’s a mess. And it didn’t need to be this way.

Karina Garcia-Reyes: I had a normal life… when the war on drugs started in Mexico in 2007, the beginning of 2007, and I witnessed how my hometown completely changed because of this war. Our lives were so affected by this war.

Naomi Fowler: This is Criminology lecturer and writer Karina Garcia-Reyes of the University of the West of England, where she now lives.

Karina Garcia-Reyes: I cannot explain to you the fear, you know that started spreading. And in two years I saw lots of businesses had to shut down because of the violence. Me, my friends, my family had to witness different shootings between the military and organised crime groups. We stopped going out. I didn’t feel safe in my hometown. this is the main reason why I started doing research on organized crime.

There’s a big narrative of, you know, the war on drugs, a binary narrative, right? The good guys, the bad guys, you know, the good guys being the government, the police, the military – starting with the United States. And then in Mexico, we kind of bought this idea. We actually appropriated this narrative and I have to say, I admit, I admit that I actually reproduced that in my mind when I started my research.

My original research focus was exploring the effect of this war on vulnerable groups like children and young people. So with this in mind, I contacted this rehabilitation center in my hometown because I knew I was so affected by this violence and I lived in a very safe place, middle class, I wanted to know how exactly these groups were being affected.

I did four months of field work in this rehabilitation centre. I have to be honest, I was not looking for them. It would have never, ever crossed my mind to do interviews with criminals, especially with, with this type of criminals, to be completely honest. Um, but I bumped into them and you know, I think they found me.

Naomi Fowler: Karina ended up hearing the testimonies of 33 men – former hitmen, drug dealers and getaway drivers.

Karina Garcia-Reyes: at the beginning, I just listened to their testimonies out of curiosity. But after two weeks of listening to very similar stories, I decided to change my focus. I thought, okay, instead of interviewing what I, at that point I saw the victims of drug trafficking violence, now I’m gonna interview the perpetrators. I think one of the most important things that I learned is that there is a very fine line between victims and perpetrators.

Idid life story interviews, meaning that I was listening to these men’s whole life stories since they were children. If you just actually look at their childhood stories, they’re really tragic, I still cannot believe how these individuals survived in the middle of so much violence because they were victims of, you know, horrible things like child abuse, child trafficking, neglect in the best case, some of them had to survive in the streets, which is really hard. And when I was listening to these stories, you know, these adult men crying you know, remembering how, for example their fathers used to beat their mums, how they were subjected to the most horrible types of violence and abuse, then I was able to understand, and I want to clarify, never to justify the violence that they engaged with later on in their lives, they learn to be violent. So, if we want to stop this type of violence, we have to start by the roots.

Naomi Fowler: Karina’s book is called ‘Morir Es Un Alivio’ (- Dying Is a Relief). We can’t hear the testimonies directly from the men she spoke with because she gave her word that no one but her would ever hear them, but she writes about them.

What was really interesting was that you said 28 of the 33 men you spoke with said at some point in their lives their greatest aspiration was to kill their fathers because of the experience they’d had in the home.

Karina Garcia-Reyes: It is shocking, but also very telling in terms of how violence is, is learned and taught, you know, if you want to be a real man, this is how you have to be a man, you’re violent, people have to be afraid of you, they conflate respect and fear. And they, they spoke about feeling so hopeless because they were little, but once they grew up and they were old enough, strong enough to actually confront their fathers they did become like them. Violence was everywhere, within their homes, but also in the streets, because most of them joined a street gang since they were little. What they learned there was the law of the jungle, you know, the law of the fittest, right? You had to be violent in order to survive. This toxic masculinity is a common thread in their narratives.

Naomi Fowler: You also connect that in your book with the sort of the consumerist individualistic culture that came along with neoliberalism in the 80s, which is really interesting.

Karina Garcia-Reyes: Yes. Remember that Mexico is a huge country. We are like 130 million people and half of the population at least is living in conditions of poverty. So what I’m trying to say here is that we have a really big, big breeding pool, so to speak for these different types of violence to happen. I’m not saying that being poor makes you violent, but what I’m saying is that unfortunately, poor neighbourhoods living in the margins of society with little or no access to the most basic services, they, they are so vulnerable because they’re isolated, basically they rule themselves somehow. They feel that their lives are not worth because nobody’s paying attention to them, if they die, nobody cares. So again, it’s like a jungle. All of them repeated these words a lot. We live in the jungle.

Naomi Fowler: You also said that there’s a kind of moment of realisation where you say ‘I will never forget his words because it was then I understood who the real villains are’ and then you started to see your participants, your interviewees as secondary in this whole industry, and as scapegoats and ‘the perfect enemy that every war needs’, is how you described it.

Karina Garcia-Reyes: Yes, because some of my participants were sicarios or hitmen. And one of them was telling me about erm, because one of my questions was, you know, what was your daily job, what you used to do, and one of them, he said that, you know, they, they were given the names of people they had to kill and they never knew why. But he, by chance I guess he mentioned that he killed a journalist and I said, why would you kill a journalist? And he said, well, I don’t know, you know, I would never ask my boss why am I killing this person, I would just do the job. But then he complimented his answer by saying that journalists usually uncover links of corruption between organized crime groups and important people. Could be local politicians, important politicians at the national level, but not only politicians, it would be important people in the industry, like, you know, entrepreneurs, lawyers. And this is something that I, I wouldn’t never forget because he said, we have nothing to lose. As criminals, we don’t have a reputation. If anything, we want people to be afraid of us. They’re killing journalists to protect the reputation of these people because they actually do have something to lose.

Another one told me that part of his job was he was a bodyguard for an accountant in Texas and you know, he never knew what he was doing. Again, you know, these people don’t ask questions, they are the very base of the pyramid here, and I asked, okay, so what was the link between this accountant and, you know, the organisation? What did he do? And again, no idea, I mean, his job was to keep this man alive. And I can give you so many examples like these.

This is something that really frustrates me because in, you know, cultural products like movies or TV series, you see, for example, Narcos, either in Colombia or Mexico, which are the trendy ones at the moment, I guess. You know, you see them sometimes as powerful and of course, you know, of course, there is hierarchy within organized crime organizations. But when you look into it, you will always find that there’s always somebody in the legal world, making decisions, not them. And this is something we rarely see in these shows or these movies. They’re reproducing this very binary narrative of the good guys and the bad guys. I’m trying to remind people that there’s a blurred line, you know, we don’t have two separate worlds, we don’t have the legal world and the illegal one, we don’t have, you know, the government pure, pristine, no! Or, for example, speaking about professional enablers, we rarely see or we rarely hear about accountants, lawyers, even architects, you know, you name it, you know, it’s a huge world the organised crime world so they do need professionals to help them, but we barely speak about them.

Naomi Fowler: Yeah I always think of it as there’s the goodies, the baddies, and the borings. And the borings are what I’m really interested in. Because nobody wants to watch a film about the boring men in suits in offices, and you know, the deals that are done in these glass buildings, and the phone calls, the accountants, papers, the transactions.

Karina Garcia-Reyes: I completely agree. How many movies and TV series we have about narcos? I don’t know, countless. How many movies do we have about professional enablers or financial crime or money laundering? What’s going on, you know, in terms of money laundering laws and how this works, it takes a lot of time to, to understand the system because it’s, it’s complicated. It’s quite technical. It’s easier to watch a movie where the villain is clear. You know, he’s a sicario, he’s a hitman, you know, that’s the bad guy. It’s easy to follow.

Naomi Fowler: Yeah, it’s a classic story structure and it’s so unhelpful. And so dangerous. It’s all part of the thinking that accelerated organised crime and violence in the first place.

Karina Garcia-Reyes: Yes. We have to look at the prohibition paradigm, the fact that drugs are illegal. First of all, we created the enemy, okay? So the drug traffickers as we know them now, didn’t exist in the 70s but, the toughest laws created the toughest criminals. The ones who initiated the war, literally the war, was the US government. In the case of Mexico is the Mexican government, and nobody is asking the governments to stop their violence. It’s, it’s, it’s nonsense. The only thing we’re doing is increasing the violence, okay? And at this point, where we are now, only the most violent will survive.

And the money doesn’t stay in Mexico. Part of the money of course it does, and I’m not trying to minimise the importance of organised crime groups in Mexico, or their leaders, I’m not saying that they’re not powerful. They are, of course, they have some sort of power, but they are not the top of the pyramid, that’s what I want to say. If anything, they’re in the middle. And who helps them to launder money? They need help from corrupt lawyers, financial advisors, there are many people benefiting from money laundering. The money that comes from organised crime and drug trafficking in particular doesn’t stay in the producing countries and that’s a myth that we really need to discuss because again, in this binary narrative, you know, we are portrayed and by we, I mean, in the case of Mexico as a producer country, these, you know super powerful drug lords, like for example, El Chapo Guzman or Pablo Escobar in Colombia. But we have seen what happens when they are either killed, like in the case of Pablo Escobar, or now in the case of Joaquin El Chapo Guzmán, he’s in jail. What happened to drug trafficking? According to the United Nations, drug trafficking continues and actually increased. What does that tell you?! After 50 years, over 50 years of an international war on drugs, after this strategy – and we haven’t had any impact. It’s increasing. So what does that mean? This is a business and let’s go back to the financial secrecy here and money laundering.

Who makes the rules? The international regime against money laundering to, you know, tackle, you know, quote unquote, tackle money laundering was designed by the US and the UK. We have to ask about political will here. What are the interests of these countries and other major players here involved? It’s not only the governments, we’re talking about banks. I think banks at the moment are as powerful as countries, especially in these two nations. This is a very lucrative business and people all over the world are getting lots of benefits from this. And that, to me, that should be the focus.

TV Presenter:A Senate investigation has found that HSBC Bank for years allowed Mexican drug cartels to launder billions of dollars through the bank’s U.S. operation. A trail of emails the investigation uncovered indicate that some officials, including the anti-money laundering director were aware of the illicit transfers:

‘There were allegations of 60 percent to 70 percent of laundered proceeds in Mexico going through, executives didn’t care about anti money laundering controls.’

David Bagley, HSBC’s head of compliance, said he will step down from the position but he’ll remain at the bank. The Justice Department is conducting a criminal investigation into HSBC’s operations. It declined to confirm that the bank is in settlement talks.

Naomi Fowler: HSBC bank ended up paying a $1.92 billion fine over their seemingly non-existent money laundering controls which facilitated two organised crime groups in Mexico and Colombia to shift $881 million in illegal drug profits, through the bank. Well, that’s what they got caught for anyway. On some days drug traffickers actually deposited hundreds of thousands of dollars at HSBC Mexico using special boxes that fitted the size of teller windows at the bank branches to speed things up. No one asked the obvious questions they should have.

Eric Gutierrez, Research Associate of International Centre of Human Rights and Drug Policy: Over time, HSBC Mexico accumulated so much cash, more than the dollars repatriated back by Latin American central banks.

Naomi Fowler: This is Eric Gutierrez of International Centre of Human Rights and Drug Policy speaking at a recent event:

Eric Gutierrez, Research Associate of International Centre of Human Rights and Drug Policy: So this is one of the reasons why the U.S. started investigating where is HSBC getting all these dollars, U.S. dollars from, bringing it back into the U.S?

So first, the cocaine is smuggled to the U. S. and then it’s sold in the U. S, so dollars are earned for selling it. The wholesale and retail distributors who then resell it to their markets, and then once the sales are made, it is moved via small accounts, money transfers through banks, through postal services, through various means, no, Western Union, whatever. And then, it goes to the currency exchange firms who does the conversion and then these currency exchange firms, their preferred bank is HSBC Mexico. And then it goes typically into the accounts held by legal persons. Now, what I mean by legal persons are mostly registered companies, so once you are registered as a company, you’re able to open a bank account and transact business across borders. Now, these accounts by mostly registered companies goes to the casas de cambio, the money exchange houses, who then converts it into the local currency and then they deposit the dollars that they have accumulated to HSBC Mexico.

So, HSBC Mexico and HSBC U.S. was of course involved and they were investigated by the US Senate but their defence was that they have not broken any law because their customers are the legitimate money exchange firms. Now, if you ask the money exchange firms, they said that we accept transactions from legal persons because that is basically their business. Now, the registered companies, those with the bank accounts, the legal persons, they remain as a legal entities, even if their beneficial owners are unknown. When you go further up, it is impossible to conduct due diligence, know your customers on, you know, thousands, even, you know, hundreds of thousands of small daily transactions in moving money.

So, what this shows is that the focus of law enforcement is all on the illegal actors, but nothing is being done on the legal actors that enable this trade. And this is the main problem. And this is replicated as well in tax avoidance by many big companies. The tools of tax avoidance are the same tools that enable the illicit drug trade’s extraordinary resilience to prohibition.

The solutions to these problems are already known, but they are not being implemented. One key reform is to compel companies to declare their true beneficial owners and to make that information publicly accessible. So there have been movement in this regard in the EU, but at the moment, there are a lot of tax havens, UK overseas territories who are refusing to do so and, you know, lobbying, against the implementation of this reform.

Naomi Fowler: Let’s remember too that the US is the number one worst financial secrecy offender on our financial secrecy index. The UK would be number one if you combine all its satellite havens.

Anyway, HSBC bank didn’t lose its licence. And it’s really just the most obvious example of how the doors to the international financial system are open to people with hot cash to move. As Eric Gutierrez was just explaining, there’s a whole white collar crime feeding chain. Lawyers, middle men, company formation agents, bank staff, accountants, fixers, front people. Suits, offices. These are the borings that we mentioned earlier. I’m sure they’d see themselves as quite separate to the ‘baddies’ you see on Narcos, the TV series…

NARCOS Mexico clip

Naomi Fowler: I actually think understanding the real crime story is much more interesting than the fantasy version. But let’s rewind a bit, back to how the whole thing started.

Mary Young: The US government should have stopped trying to ban something which would only make it mushroom and grow. They did have alcohol prohibition in the 1920s as a basis, they could have looked at that as a framework for something that didn’t work.

Naomi Fowler: This is Associate Professor of International and Organised Crime at Bristol Law School, Dr Mary Young.

Mary Young: The war on drugs in 1971 targeted certain groups of people in America. That was the main issue rather than tackling drugs. So the war on drugs was ill informed, incorrect and flawed from the beginning.

We always tend to think of organised crime moving from a lesser developed country into a Western country but the U. S. government never really assesses why and how drugs get so easily into its own country, I think there’s just a demonisation of other countries.

Transnational organised crime is a US political construct. We need to know that the war on drugs has come from that. I tend to reject the word ‘cartel’ because it means a price fixing organisation if we were looking at international law, disciplines such as international competition law, and I don’t think that drug trafficking organisations tend to fix prices and monopolise in that way. It’s the user and demand, and also even to do with where the drug is being sold, in which country, tends to fluctuate the prices, leads what prices drugs will be traded at. So I will refer to drug trafficking organisations.

And rather than piling all this legislation, and one trillion dollars at the war on drugs the US should have been looking at rehabilitation, why people use drugs, and a big part of combating organised crime for the US needs to be them assessing their own borders.

Naomi Fowler: Yeah. ‘Fix your own house’! And the US at the time was absolutely paranoid about communism, their war on drugs slotted nicely into all that too. And if only they’ d used some of those huge resources they threw at all this to tackle their own banking secrecy things could have been very different, I mean without an army of intermediaries to help them move money across borders there’s a limit to how much cash you can launder and therefore how big an organised group can become.

Mary Young: Yeah, so offshore financial centres, financial secrecy havens, tax havens, all phrases that we tend to use interchangeably and synonymously, but we’re all usually referring to the same thing, a jurisdiction or a country or a territory which enables somebody to bank basically anonymously. And financial secrecy havens will say that they don’t have laws which exist which guarantee anonymity, that there’s always the chance that information can be released if an investigation is started, but the US weren’t going to put all their money into combating organised and drug trafficking crime. Neither were the UK. Because when Britain’s financial services industries really started to kick off in the 1980s, along with the U. S., when they really started recognising the value of these small island states, especially in the Caribbean, as places where they could put money very easily, they were not going to undermine their ability to use their financial havens for their own dealings, if you like.

It’s not that the US, it’s not that the UK, it’s not that Western countries were ever going to put the trillions used on the war on drugs into combating financial secrecy havens because it was never about the destruction of drug money laundering. It was never about ending criminal financial enablers with hot money. It was always about the U.S. and the UK in particular, protecting and leveraging their own national trading interests on both sides of the Atlantic.

Naomi Fowler: Yeah and you and another researcher Michael Woodiwiss analysed six months of previously unseen, classified personal correspondence and documents exchanged between various actors in the UK and US government in 1987 which absolutely bears that out.

Mary Young: Yes. For me, it’s really frustrating to read through hundreds of pages of correspondence and see how anti money laundering control was actually being constructed so that they didn’t tackle money laundering. We looked through 600 pages of exchanges between the US and the UK, between bankers, between politicians, which showed that these vested interests were being talked about, which showed that the point of the financial secrecy havens, point of financial services industries embracing financial secrecy was to really leverage the US and the UK’s own trading interests. And you know, the US Bank Secrecy Act was constructed in 1983. Has it worked? No. Is there still financial secrecy? Yes. Are U. S. territories embedded with financial secrecy? Yes. And the economic interests, we only need to look at some of the world’s biggest banks, some of the biggest Western banks which reside in these financial secrecy centres to know that they are used by the U.S., they are used by the U.K., they are used by the big, huge Western companies who need them, who need the financial secrecy centres to keep their economies ticking.

Naomi Fowler: I’m going to put a link to that research in the show notes because it really is fascinating and I know you’re looking through more exchanges at the moment which will be really interesting too.

Mary Young: Yeah. We’re still doing it now. The US and the UK may tend to advertise how they want to stop money laundering, how they want to stop money laundering in their offshore territories, how they want to combat money laundering at the wider global level because it’s destructive to the international financial architecture. But actually, they’re very important. Offshore financial centres are very important for Western countries. And we know this because the US and the UK policymakers who started to set the agenda for regulating the financial services industry, the financial secrecy jurisdictions. And we know by the fact that nothing has been done, that still nothing is being done by the UK government, for example, that there is no incentive to do so because they still remain a large part of our trading and economic interests. It will never work. It can’t work. It never gets a fair chance from the beginning.

Naomi Fowler: The Tax Justice Network’s been arguing for so many years now that if governments are really serious then yes, they would make proper laws and they would enforce them. There’s a whole army of what we call ‘professional enablers’ delivering financial secrecy and wielding huge influence in high places. They never get the attention they deserve.

In Part 2 of the drugs war myth in the next Taxcast, we’re going to focus on the invisibles in this story, the money managers and how we fix the systems that facilitate all these hot money flows creating such misery and destruction in so many nations. We’ll explore how to have real impact without firing a shot.

Countries at the UN General Assembly are likely to vote this year-end on the UN Secretary General’s proposals for a UN tax convention, which would deliver the biggest shake-up in history to the global tax system.

The adoption of a UN tax convention has been heralded as countries’ best chance to avert losing nearly $5 trillion to tax havens over the next decade. The Secretary General’s proposals would have global tax rules be decided at the UN instead of the OECD, a small club of rich countries which has overseen global tax rules for the past 60 years.

We’ll be sharing rolling updates here over the coming months on the run-up to the UN vote.

⚫ – Live updates closed

This blog is now closed.

Thurs 23 November 2023

3:57pm GMT – South Centre statement welcoming the adoption of the resolution

The South Centre has published a statement welcoming the adoption of Africa Group’s resolution. The statement says:

“Such a Convention can bring a badly needed stability, coherence and equity to the international tax system by solving the governance deficits in the existing system, largely designed by the OECD through opaque and non-inclusive procedures which have produced over-complex rules of the lowest common denominator that primarily serve to benefit large multinational companies that exploit the gaps and complexity of the rules, rather than the people in developed or developing countries.

“Such a Convention can ensure that international tax rules are formulated by an intergovernmental body with participation of all UN members on a genuinely equal footing; a body that has a multilateral statutory basis, functions on the basis of clear and transparent rules of procedure, incorporates the principle of democratic decision-making and is accountable to all countries (and not just a few). The Convention can produce equitable international tax rules that provide all countries with additional resources and contribute to the achievement of the Sustainable Development Goals.”

An OECD ‘Statement by the Secretary General on International Tax Cooperation’ was issued shortly after the vote yesterday. The statement failed to recognise or engage with any of the grievances or desires for change expressed by countries at yesterday’s vote. The statement did not mention the resolution adopted at the UN nor acknowledge that the historic vote had even taken place, which was largely seen as a vote of no confidence in the OECD’s leadership on global tax policy.

In a press release we published earlier today, our CEO Alex Cobham said on the OECD’s statement:

“The OECD has shown no humility about the fact that so many countries, including some of its own members, resisted its intense lobbying and instead rejected its continuing monopoly over international tax rules. More than a hundred countries – the governments of 4 out of every 5 people on the planet – united at the UN to say they’re fed up of not being heard at the OECD. And the OECD responded by refusing to even acknowledge the vote took place! If the OECD hopes to support its members in the UN process that will now get underway, it’s hardly an auspicious start.”

3:38pm GMT – “No” voters on UN tax reform enable 75% of global tax abuse

Countries who voted against UN tax reform yesterday enable 75% of global tax abuse, our latest analysis finds. These countries represent just 15% of the global population. Countries that voted in favour of reform represent 80% of the global population.

“These numbers cut to the heart of what happened at the UN vote yesterday. The world united to fight global tax abuse together, and the small circle of countries fuelling that tax abuse tried and failed to stop them,” says our CEO Alex Cobham.

10:20am GMT – Round up of media coverage on UN vote

ICIJ: UN votes to create ‘historic’ global tax convention despite EU, UK moves to ‘kill’ proposal ↗

FT: Developing countries secure bigger international tax role for UN ↗

Bloomberg: UN Votes for Framework Tax Convention Amid Work on OECD Deal ↗

El País: La ONU aprueba negociar un nuevo marco fiscal global con el rechazo de EE UU y la UE ↗

La Jornada: Se abstiene México en votación sobre reglas tributarias globales ↗

Il Fatto Quotidiano: All’Onu passa (con il no di Ue e Usa) la risoluzione dei Paesi africani per riscrivere le regole fiscali globali e combattere i paradisi ↗

Euractiv: UN tax body to go ahead after EU, US and UK fail to defeat it ↗

Wed 22 November 2023

5:20pm GMT – Tax Justice Network statement on UN vote

“This is a historic victory delivered by the countries of the global South, for the benefit of people all around the world. Tax havens and corporate lobbyists have had too much influence on global tax policy at the OECD for too long. Today, we start to take back power over the global tax rules that affect all of us.

“The great majority of countries have declared today that they are ready to move on from the OECD, and will start negotiating global tax rules at the UN instead. We invite all countries to join in these negotiations and begin a new chapter of economic prosperity for people everywhere.”

Happy to learn that the vote on the convention has PASSED! The rich country governments voting against this motion have shown that they are on the wrong side of history–and on the side of the rich and big corporations rather than their own people. https://t.co/IfEeU7ghfT

— African Union Mission to the UN (@AfricanUnionUN) November 22, 2023

Voting results on the #UNTaxConvention! 🎉🎉🎉Thank you for being on the right side of history! Voting for a truly inclusive and democratic intergovernmental mechanism under the @UN, where every nation stands on equal footing! pic.twitter.com/oD4B2pLXbz

— Civil Society Financing for Development Mechanism (@cs_ffd) November 22, 2023

The #UNTaxConvention vote has passed at the @UN 2nd committee with 125 votes in favour, we look forwards to negotiations starting and for all countries participating on an equal, inclusive, transparent way for better global tax governance to end #taxabuses and #IFFs. pic.twitter.com/HjTjnHtApu

History in the making: the Global South has just won over the Global North at the @UN: A framework convention for tax is reality! Thanks so much to everybody who made that happen! #UNTaxConvention@GA4TJpic.twitter.com/ILUxoruQgy

The Africa Group’s resolution has been adopted – with no amendments – by a landslide majority: 125 countries for; 48 against; 9 abstained.

The UK’s amendment seeking to defang the resolution was by nearly 2 to 1.

3.45pm GMT – Discussions on Africa Group’s resolution happening now

The Second Committee is now discussing today’s tax resolution. Countries will make statements, followed by votes on any possible amendments to the resolution, and then a vote on the resolution.

3.10pm GMT – UN session begins; resolution third time on the schedule

The session of the Second Committee of the UN General Assembly is now beginning and be watched live here. Today’s tax resolution is the third item on the schedule.

3.05pm GMT – Media advisory: Analysis and links on today’s UN tax vote

Our head of communication Mark Bou Mansour writes:

Countries are voting today on a UN resolution that could deliver the biggest shakeup to the global tax system in history.

The resolution, tabled by the Africa Group, seeks to begin the process of establishing a UN framework convention on tax, first by creating an inclusive, intergovernmental committee to set the terms of reference for negotiations by August 2024, which would then be carried forward into the final stage of establishing the convention. A UN tax convention will ultimately move decision-making on global tax rules from the OECD, a small club of rich countries where these have sat for the past 60 years, to the UN.

The UK has tabled a last-minute amendment ahead of the vote that removes all mentions of a convention from the resolution. More amendments may be proposed ahead of today’s vote, and each must be voted before the final vote on the (possibly amended) resolution.

We have published an analysis here on how today’s vote may go, what the implications for the future are and what the UK’s amendment may mean.

2.50pm GMT –How might today’s vote on the UN tax resolution go?

Our CEO Alex Cobham writes about three reasons to expect progress to follow from a majority vote today:

Today sees the vote by countries of the world on a resolution to move ahead towards a UN tax convention. Amongst the global media coverage, one article stood out. More or less all coverage reflects on the continuing opposition of some major OECD countries including the EU, UK and US, and focuses on the potential for a majority vote if the resolution is broadly supported by G77 members. The Guardian article instead claims that the resolution “is expected to fall at the last hurdle in a vote in New York on Wednesday”, because, it says, it “would need widespread agreement, including by the US and rich nations in Europe.”

This is not factually the case. A majority vote for the resolution could be delivered from G77 members alone, regardless of the stance of OECD members. However, it is true that OECD members have been successful in past cases (eg on debt negotiations) in preventing any movement simply by boycotting a process agreed by majority rather than by consensus. And it is notable that last year’s resolution on “Promotion of Inclusive and Effective Tax Cooperation at the United Nations” (A/RES/77/244) passed by consensus, with all countries agreeing not to require a vote.

9.30am GMT – ICRICT open letter in El País (France) “EE UU y la UE deben respaldar un convenio fiscal de la ONU”

Esta semana seremos testigos de lo que puede ser un avance histórico hacia una economía mundial más equitativa… o quizás de un terrible fracaso. En el marco de las Naciones Unidas el conjunto de países votará para decidir el futuro de la gobernanza fiscal internacional.

9.20am GMT – The Guardian article “Push to give UN more say on global tax rules likely to stumble at vote”

Phillip Inman writes: A long-running campaign for the United Nations to have greater influence over international tax rules is expected to fall at the last hurdle in a vote in New York on Wednesday with the US, Brussels and the UK blocking the move.

9.10am GMT – El Espectador (Colombia) “La reunión de la ONU que será clave para el futuro de la tributación en el mundo”

Esta semana en la Asamblea General de las Naciones Unidas se llevará a cabo una discusión crucial. Sobre la mesa está un proyecto de resolución que, de ser aprobado, promovería una cooperación fiscal internacional más inclusiva. Le contamos de qué se trata y cuál parece ser la posición de Colombia.

6:35pm GMT – Press conference will be held after UN vote by the Global Alliance for Tax Justice

The Global Alliance for Tax Justice will be holding an online press conference tomorrow after the UN vote at 12:00pm ET (New York time) / 5:00pm GMT/ 6:00pm.

Tomorrow’s vote is now listed on UN Web TV. The UN session will start at 10am ET (New York time). The Africa Group’s resolution is the third item of the session. The session will be livestreamed here.

12.08pm GMT – ICRICT open letter “The US and the EU should back a UN tax convention”

In an open letter, the Independent Commission for the Reform of International Corporate Taxation (ICRICT) stresses the pivotal importance of this week’s United Nations vote on global taxation. Calling on the US and EU to reconsider their stance, and back the Africa Group’s resolution.

11.07am GMT – Speaking at the Cartagena Fiscal Summit earlier this year, Dereje Alemayehu, Executive Coordinator of the Global Alliance for Tax Justice, explains why only the United Nations can provide the legitimate and inclusive forum that is a precondition to fair negotiations on tax cooperation.

11.06am GMT – Alicia Nicholls of the Shridath Ramphal Centre for International Trade Law, Policy and Services at the University of the West Indies, Barbados, reflects on the role of OECD countries in facilitating cross-border tax abuse, and their problematic role in leading global tax negotiations.

10.50am GMT – Fundar call on Mexico and Latin America to support resolution.

Fundar, a Mexican civil society organisation, explains why Mexico and Latin American countries should support the African Group’s draft resolution with their vote. “To vote in favour of the resolution is to vote in favour of tax justice and human rights,” they argue.

9.50am GMT – Endorsement from the African Commission on Human and Peoples’ Rights

The African Commission on Human and People’s Rights have published a joint Statement on support for an international treaty on tax cooperation and resources for financing social and public services.

9.30am GMT – The Nation (Barbados) “Government backing UN move”

Prompted by Marla Dukharan’s recent special report urging Caribbean nations to support the upcoming UN vote for a tax framework convention, Shawn Cumberbatch writes:

Barbados is supporting a push for the United Nations to help bring more “transparency and fairness” in international taxation.

Kerrie Symmond, Minister of Foreign Affairs and Foreign Trade: “We believe that there is a necessity to have this ongoing matter of international tax regulation transparently and fairly discussed, in a setting that accommodates and takes into account the voices and circumstances of all, including the most vulnerable and the smallest of states. Barbados welcomes the possibility of the involvement of the United Nations in this process.”

1.18pm GMT – Manila Bulletin article “Civil society groups urge support for UN Tax Convention”

Ma. Joselie C. Garcia writes:

Civil Society Organization (CSO) leaders from various countries have expressed support for a United Nations (UN) Convention on inclusive tax cooperation to combat profit shifting and illicit financial flows in extractive industries.

This was resounded in an international conference on tax justice held last Nov. 9 to 11 in Quezon City while the convention on inclusive tax cooperation is being deliberated at the UN.

1.10pm – Law 360 article “African Nations Rally For UN Tax Treaty After Facing Pushback“

Kevin Pinner writes: African diplomats are rallying support for a global tax convention at the United Nations, they said Thursday, after a group of mostly wealthy countries blocked their resolution from being adopted, likely forcing a vote next week.

11.10am GMT – War on Want article “Why we need to fix global tax rules!”

Amazon paid £0 in UK corporation tax last year. How do rich multinational corporations get away with paying little-to-no tax on their vast profits – and who is paying for the black hole this lost tax revenue leaves in public finances?

9:00am GMT – CBGA interview with Alex Cobham, Chief Executive at Tax Justice Network, offering insights into the background of the UN tax convention vote and underscoring the limitations of the OECD.

Fri 17 November 2023

1:40pm GMT – Malala Fund calls on global leaders to support Africa Group’s resolution

Malala Fund has published a statement urging countries to support the Africa Group’s resolution. The statement says:

“Positive outcomes for African governments are more likely to emerge at the U.N., where each member state has one vote on proposals, also known as U.N. resolutions. Global leaders have an important opportunity on November 22 to increase investment in education by adopting a proposal on global tax cooperation at the U.N. General Assembly.

“Malala Fund joins tax and debt justice organisations to support African countries’ draft resolution for a U.N. tax convention — a legally binding agreement between countries — to make global tax rules more inclusive, help tackle tax abuse and free up public funds for girls’ education.

“…Malala Fund urges all member states to challenge the status quo on global tax systems and clear the way for a U.N. tax convention by 2025 — a decision that would only be good news for girls.”

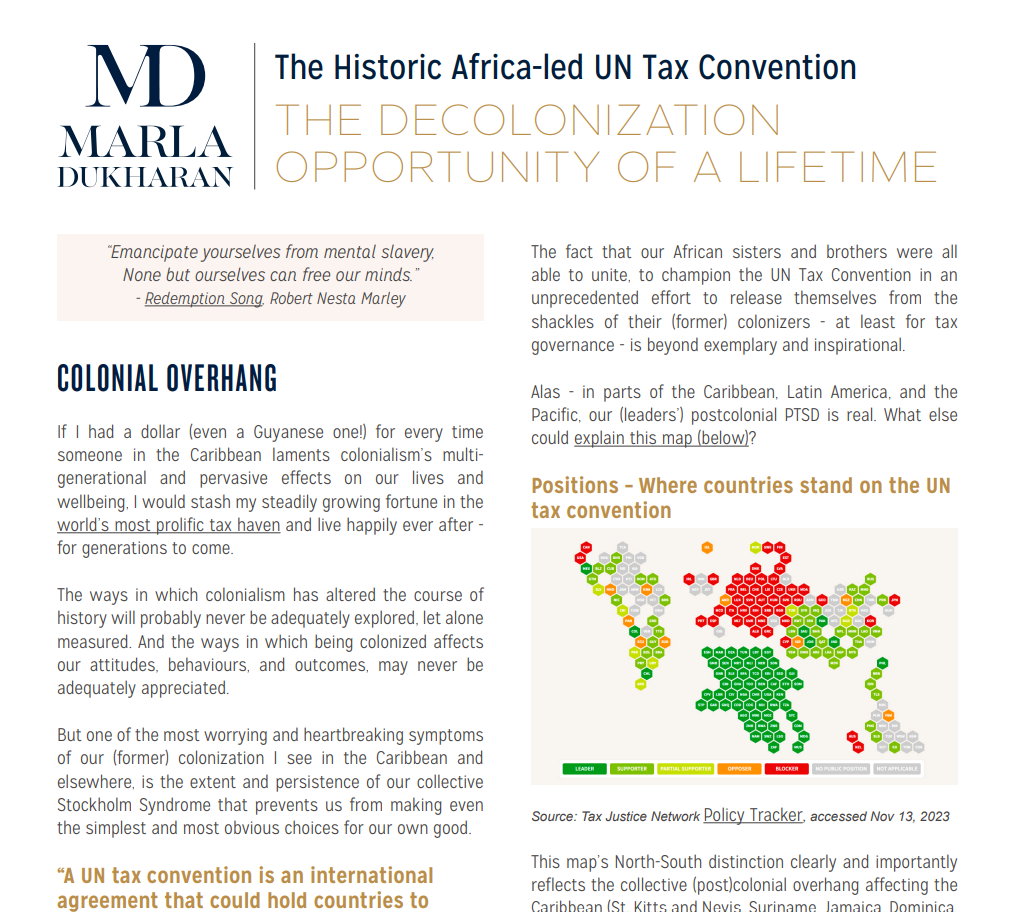

11:54am GMT – Leading Caribbean economist Marla Dukharan calls on Caribbean nations to support UN framework convention on tax

Leading Caribbean economist Marla Dukharan has published a detailed special report on the upcoming UN vote for a framework convention on tax in which she calls on Caribbean nations to support the convention.

Dukharan writes:

“To support the OECD, is to implicitly support the EU and its indefensible, racist and hypocritical blacklisting of nonwhite former colonies, especially in the Caribbean and Pacific Islands. Again, is that what we really meant to do?

“…I call on the Governments of St. Kitts and Nevis and Suriname who have for whatever reason opposed the UN Tax Convention, to please reconsider their rather regressive position. I also call on the Governments of Dominica, St. Vincent and the Grenadines, St. Lucia, Jamaica and Haiti to indicate their support for the UN Tax Convention. Show the world that you can stand up to injustice, further your decolonization journey, and break free of the OECD. It’s now or never.”

8:45pm GMT – World to vote next week on strongest option for historic global tax shakeup

“Thanks to the leadership of African countries, the world is now potentially days away from ushering in a global democratic revolution in tax that can finally put people before tax havens.”

Read our full statement on the Africa Group’s announcement here.

7:00pm GMT – Full transcript of the press statement by the Chair of the Africa Group

Here’s the full transcript of the chair’s statement today:

Statement on behalf of the African Group by the H.E. Dr. Chola Milambo, Permanent Representative of the Republic of Zambia during the Press briefing on Resolution “Promotion of Inclusive and Effective International Tax Cooperation at the United Nations”

16 November 2023

Excellencies,

Ladies and Gentlemen,

As the current Chair of the African Group, I have the honor to address this gathering on behalf of the Group:

Today marks a significant moment in our collective journey towards a more equitable and inclusive global tax system. The African Group has taken a significant step forward with the proposal of a Framework Convention on International Tax Cooperation, a landmark initiative reflective of our collective commitment to fairness and inclusivity in the global tax system.

This Framework Convention is not merely a policy document; it is a beacon of hope for developing countries that have long sought a voice in the shaping of international tax norms. It addresses the critical shortcomings of the current system, which often sidelines the unique challenges and perspectives of developing nations.

Our proposal acknowledges the contributions of existing bodies like the OECD and the UN Tax Committee, while also recognizing their limitations in fully representing the interests of all nations, particularly those in the developing world.

The Convention’s primary goal is to ensure that all countries, regardless of their size or economic power, have an equal seat at the table in setting the agenda for international tax cooperation. This is a step towards rectifying the historical imbalance in global tax governance, offering a more equitable platform for dialogue and decision-making.

By establishing a more equitable tax system, we unlock greater potential for spending in critical sectors like healthcare and education, pivotal for Africa and the Global South. The increased revenue generated will enable us to allocate resources where they are most needed, supporting sustainable growth and development. This approach is encompassed under the umbrella of ‘sustainable development’, ensuring that our initiative directly contributes to the Sustainable Development Goals (SDGs), reflecting our shared commitment to a future where holistic progress and well-being are accessible to all.

The human aspect of this Convention cannot be overstated. By reforming the international financial systems and ensuring fair taxation, we can significantly reduce the strain on international aid. More revenue for the Global South translates to less dependence on Overseas Development Assistance (ODA), fostering a more self-reliant and resilient world economy.

To our partners in the OECD, the EU, the US and the UK, I appeal to your understanding of our shared humanity. This Convention is not just a fiscal tool; it is a lifeline to millions who aspire for better healthcare, education and a life of dignity. Your support is crucial in turning this vision into a reality.

Looking ahead to the 2025 Financing for Development (FFD) conference, this Convention sets the stage for a more inclusive approach to global economic challenges. It is a step towards a future where sustainable development, encompassing economic growth and environmental stewardship, goes hand in hand.

In essence, this Convention is about humanizing our approach to global economics. It’s about creating a system that serves not just economies but the people at their core. It represents a commitment to a future where every nation, regardless of its economic stature, can thrive.

In conclusion, on behalf of the African Group, I appeal for collaborative effort and consensus in realizing this Convention. Together, we can forge a global tax system that is truly representative, fair and effective, benefiting every nation and every citizen.

10:25am GMT – Final text for UN vote expected today as opposition shrinks

The Tax Justice Network understands that the Africa Group will announce at a live press conference today the final text of the resolution it plans to take to a UN vote next week. The resolution, we understand, will seek to begin negotiations on a framework convention on tax – despite EU countries remaining the main obstacle to global consensus.

The Africa Group’s press conference will take place at 11am ET and can be watched live on UN Web TV here.

5.15 pm GMT – Thabo Mbeki: Use the UN to tackle the scourge of global tax abuse

Former President of South Africa Thabo Mbeki has published an op-ed in the FT urging countries to support moving global tax rules from the OECD to the UN. “I appeal to the UK government and its counterparts in the EU to join the majority of UN member states, which represent the bulk of the world’s poor, and vote to sit at the same table as the representatives of developing countries.”

11.30 am GMT – Financial Times article:Developing countries and Europe in dispute over global tax role for UN

Emma Agyeman writes:

Diplomats from the European Union and UK have been accused of trying to “kill” proposals that seek to give more voice to developing countries in international tax negotiations. Countries are in talks at the United Nations over plans to give the UN more of a role in global tax discussions — a measure being pushed for by low and middle income countries.

The OECD has convened countries over international tax matters for decades, but it has attracted criticism from officials in some developing economies who believe it does not reflect their interests.

8:15am GMT – Names of companies behind $870bn tax abuses kept from public by global tax body; 60% of countries in favour of UN tax convention

Our new analysis shows records collected from multinational corporations by governments confess to nearly $1 trillion in corporate tax abuses – names of abusive corporations remain intentionally withheld from public.

And our newly launch Tax Justice Policy Tracker reveals that 60% of countries are in favour of establishing a UN tax convention. Those for a UN tax convention outnumber those against by 2 to 1.

However, a minority of “blocker” countries, primarily the US, UK and EU countries, are attempting to block this month’s planned UN vote on beginning formal negotiations on a UN tax convention.

“It’s unconscionable that these blocker countries would rather go against the interests of their own citizens, and have us all keep losing billions to tax havens every year instead of bringing global tax rules into the daylight of democracy at the UN,” says Amelia Evans, the Tax Justice Network’s advocacy consultant in New York.

9:17am GMT+1 – Draft resolution published, brings world one step closer to UN tax convention

A long-awaited draft UN resolution to formally begin negotiations on establishing a legally-binding UN tax convention has now been published, marking the latest milestone in a UN process that could potentially deliver the biggest shakeup in history to the global tax system. The motion triggers the final stage of deliberations, which start today, among countries to determine the process that will be used to negotiate the intricacies of a UN tax convention – negotiations that will begin early next year if the draft resolution is adopted at an upcoming vote at the UN General Assembly this November.

The draft resolution, which was tabled by Nigeria on behalf of the African Group on Wednesday last week but only made public on the UN website late yesterday evening, signals a direction in favour of the strongest of the three options proposed by the UN Secretary General.

The draft resolution:

“Emphasizes that a United Nations comprehensive convention on international tax cooperation is needed in order to strengthen international tax cooperation and make it fully inclusive and more effective; (OP1)

“Recognizes that this will also help in accelerating the implementation of the Addis Ababa Action Agenda on Financing for Development and the 2030 Agenda for Sustainable Development;” (OP2)

The draft resolution, if adopted, would establish an intergovernmental committee tasked with the job of drafting the UN tax convention by June 2025.

The draft resolutions specifies that any possible UN tax convention ought to consider the impact of international tax rules on inequality, gender and the environment.

The draft resolution is available on the UN website here.

Wed 4 October 2023

2:15pm GMT+1 – Draft resolution expected next week

A draft resolution will first be tabled at the Economic and Financial Committee (the ‘Second Committee’ of the UN General Assembly). The item on ‘Promotion of inclusive and effective international tax cooperation at the United Nations’ is considered under macroeconomic policy questions, and marked 16(h) on the committee’s agenda. Per the committee calendar, this item will be discussed on Thursday 5 October – but it’s not uncommon for the calendar to change. At present, draft resolutions are required to be submitted for this item by Wednesday 11 October, after which they will be published and the committee will continue its negotiations.

10:40am GMT+1 – EU rift on UN tax convention talks emerges as finance ministers defy EU Parliament with spoiling stance

Just a week after countries of the world met in New York to confirm their support for UN global talks on international tax cooperation, finance ministers of the European Union have signalled their intention to oppose any substantive progress. Rather than support negotiations on a UN tax convention to claw back countries’ astronomic losses to tax havens, the EU finance ministers have recommended that “the EU and its Member States could consider option 3 [from the UN Secretary-General’s recent report], i.e. working at the UN on a non-binding multilateral agenda.”