The single biggest change in a century to international tax rules will be discussed this weekend at an annual meeting of the G7 – a club of the world’s seven largest economies: Canada, France, Germany, Italy, Japan, the UK and the US.

The G7 will seek an agreement on implementing a global minimum corporate tax rate on multinational corporations. The proposal, which recently went from the fringes of tax justice advocacy to the top of the G7’s agenda in the span of just two months, has the potential to recover hundreds of billions in underpaid corporate tax and put an end to the “race to the bottom”↪NOTEThe idea that countries can “compete” like companies in a market is a deeply incorrect analogy that has been used to sugar-coat harmful tax cuts and deregulations, and to spur countries into a “race to the bottom”. Learn more here.

The Tax Justice Network will be publishing below responses and updates on key developments throughout the week.

🔴 – Live updates

This blog is now closed.

Tuesday 8 June 2021

11:08 am GMT Tuesday 8 June 2021 – Round up of media coverage

The G7’s deal on a global minimum tax rate has received wide coverage since Saturday. Here is a short round up of some the coverage:

- BBC: G7 tax deal doesn’t go far enough, campaigners say

- Reuters: Anti-poverty groups criticise rich countries over G7 tax deal

- Fortune: ‘Far too low’: Tax justice campaigners push back against the G7’s 15% minimum tax-rate pact

- The Times: Overseas territories to be left stranded by G7 tax reforms

- The Guardian: Global G7 deal may let Amazon off hook on tax, say experts

- France 24: Impôt “mondial” sur les sociétés : pourquoi Amazon pourrait s’en tirer à bon compte

- Il Fatto Quotidiano: Tasse sulle multinazionali, per Amazon potrebbe non cambiare nulla o quasi. Le nuove regole “graziano” il colosso di Bezos

- Der Standard: Wen die globale Mindeststeuer trifft und wie sie funktionieren soll

- ORF: Warnung vor Schlupfloch für Amazon & Co.

- RTL: G7 bereikt akkoord over minimumtarief winstbelasting multinationals

- EFSYN: «Ρηχή» η συμφωνία για φορολόγηση πολυεθνικών

- Indian Express: What the G7 corporate tax deal means for India

- The Asahi Shimbun: 最低法人税率を巡るG7合意、途上国に不利との批判も

- UOL: Novo imposto anunciado por países ricos a multinacionais não é suficiente, apontam analistas

- La Nacion: Grupos de lucha contra la pobreza critican a países ricos por acuerdo tributario del g7

- Milenio: Tras decisión del G7, paraísos fiscales enfrentan una gran amenaza

- MSN South Africa: Will G7 tax deal force big companies to pay up?

- KBC: Tax deal sets bar too low, campaigners say

- Al Eqtisadiah: حرب عالمية على جبهة الضرائب

- La Presse: Une avancée, mais encore beaucoup de travail

And some broadcast highlights:

Channel 4: Multinational giants Amazon, Facebook and Google to face G7 tax bill

ABC News: Tax Justice campaigners say G7 tax deal doesn’t go far enough

Euronews: G7 global tax deal

DW: G7 finance ministers reach deal on global taxes

Saturday 5 June 2021

13:55pm GMT Saturday 5 June 2021- G7 and OECD approach is deeply unfair

Here’s the first live response to the G7’s announcement on the global minimum corporate tax rate from Alex Cobham, chief executive at the Tax Justice Network, speaking with DW:

12:25pm GMT Saturday 5 June 2021- G7 take big step to recover tax but just for themselves

Responding to the G7’s announcement on the global minimum corporate tax rate, Alex Cobham, chief executive at the Tax Justice Network, said:

“The G7 has decided to finally move the international tax system into the 21st century but only enough to shamelessly benefit just themselves, leaving the rest of the world behind. The world’s eyes were on the G7, hoping that in the face of this global pandemic they would throw their weight behind a new tax system that would bring back home to all countries the billions in corporate tax they were robbed of and urgently need to rebuild and recover. Instead, the G7 finance ministers are proposing to follow OECD proposals that would ensure the G7 themselves take the lion’s share of any new tax revenues – which will in any case be limited by their lack of ambition.

“The G7 made it clear that they know the race to the bottom has been damaging economies and people’s lives for decades. By settling for anything less than a 25% tax rate, the G7 is telling their citizens and the world that they’re willing to keep the race to the to bottom alive and kicking. Rarely does the opportunity to better the lives of billions of people in a single stroke come by but when history came knocking today, the leaders of the richest countries in the world turned their back on it.

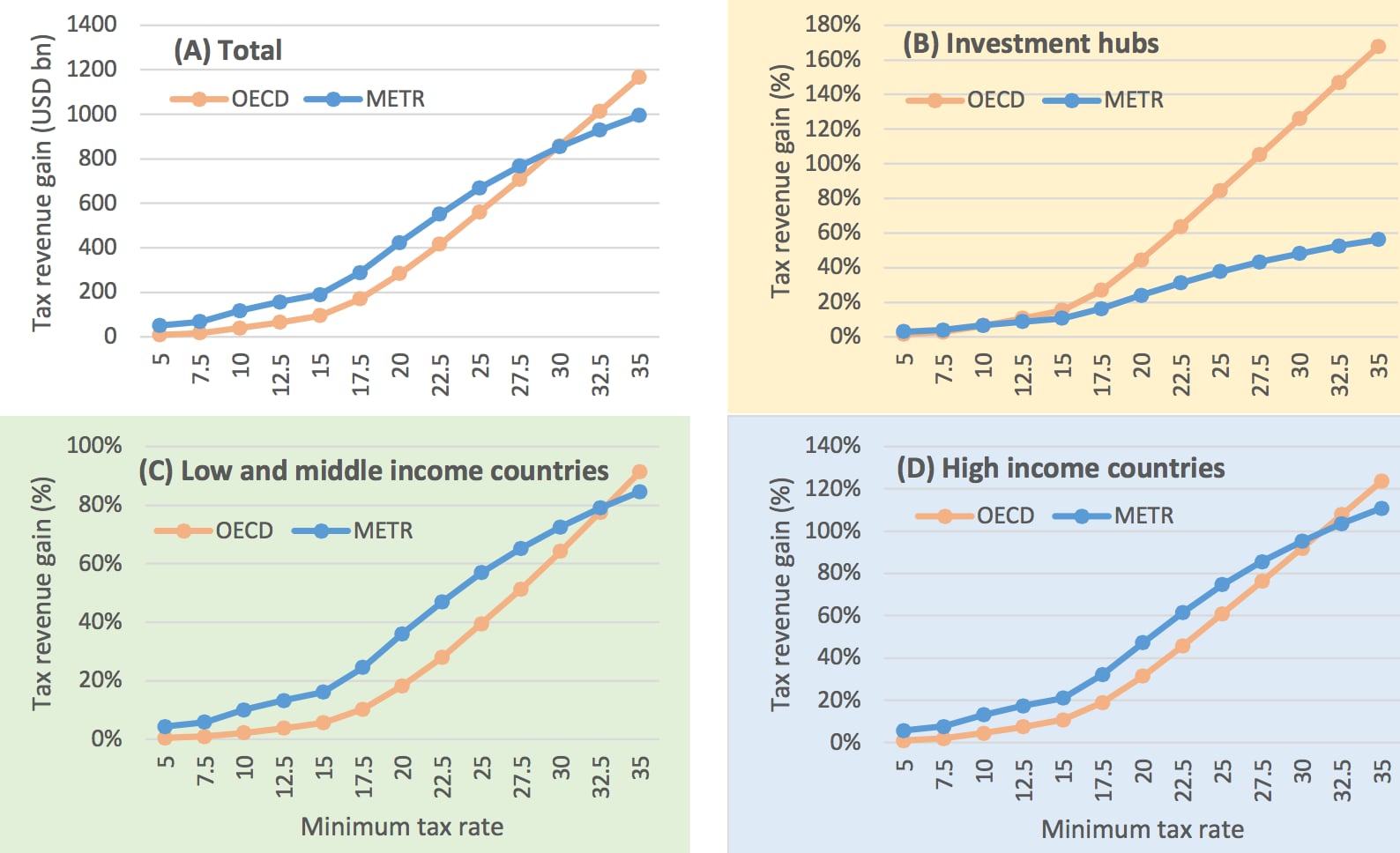

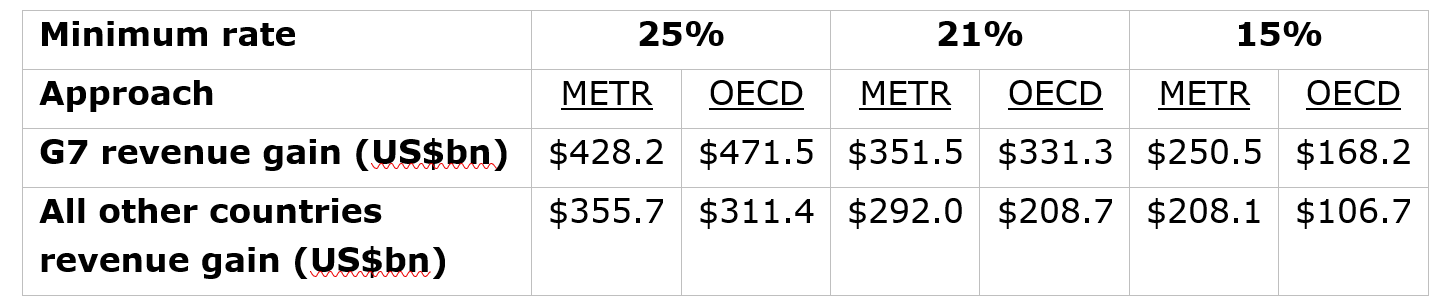

“Our modelling1 shows that a 25% minimum effective tax rate could raise $780bn in additional revenues worldwide – and still leave multinationals with three quarters of their gross profits. Countries outside the G7 could receive $355 billion under the fairer approach we’ve proposed. If the G7 pushes ahead with a 15% minimum rate under the deeply unequal OECD approach, they will leave barely more than $100 billion for other countries – while taking $170 billion just for themselves.

“This cannot stand. The rest of the world must object absolutely. The G20 group, and the Inclusive Framework, may rightly feel entirely disenfranchised but they can take back the power by challenging this openly, pushing for a higher rate and insisting on a balanced distribution of recovered tax, like that offered by the METR2 proposal.

“Even the G7 and OECD recognise that the international tax rules are unfit for purpose. The disproportionate power exercised by these rich countries’ clubs today shows that the way international tax rules are determined, too, is unfit for purpose. It is now well past time for international tax rules to be set democratically at the UN, starting with a UN tax convention.”

-ENDS-

Contact the press team: media [@] taxjustice [.] net

Notes to editor

- Our analysis of how much each country can recover in underpaid corporate tax under a global minimum corporate tax applied under the OECD and METR proposals. You can view the country figures in this table here. Provided below is a table presenting these country figures grouped into two categories: G7 countries and non-G7 countries.

2. An explanation of the METR (Minimum Effective Tax Rate) proposal by Sol Picciotto, Coordinator of the BEPS Monitoring Group, emeritus professor of law at the University of Lancaster in the UK and Tax Justice Network senior adviser, is available here.

Friday 4 June 2021

1pm GMT Friday 4 June 2021 – Our CEO speaks with CNBC International

Here’s the clip of our CEO Alex Cobham speaking with CNBC International earlier this morning about today’s G7 discussions on a global minimum corporate tax rate.

6:30am GMT Friday 4 June 2021 – Is today a turning point against corporate tax abuse?

With the G7 meeting today in London due to start, we’ve published an extended version of our chief executive Alex Cobham’s op-ed in the Guardian.

Thursday 3 June 2021

2:28pm GMT Thursday 3 June 2021 – Tax Justice Network CEO op-ed in the Guardian on global minimum corporate tax rate

Our CEO Alex Cobham has written an op-ed for the Guardian making the case that a corporate tax reset by the G7 will only work if it delivers for poorer nations too.

“After decades of evidence that the international tax rules are unfit for purpose, the Biden administration has finally injected genuine ambition into efforts to prevent the super-profits of the world’s largest multinationals disappearing into tax havens. It’s a deal could deliver hundreds of billions of dollars in tax revenues to boost the pandemic response and recovery. But there is also a downside: the current OECD proposals would distribute those revenues in a manifestly unfair way. That would surely eradicate any remaining legitimacy the richest nations could claim for their privileged position of setting rules for the rest of the world.”

In addition to the op-ed, the Guardian’s Richard Partington has written a helpful explainer on the global minimum corporate tax rate and the key issues in G7 negotiations.

12:50pm GMT Thursday 3 June 2021 – Microsoft subsidiary paid no corporate tax on $315bn in profit last year

The revelations just published today ahead of this weekend’s G7 meeting are extraordinary “even for tax justice experts”.

Extraordinary, @FairTaxMark. Even for jaded #taxjustice types.

— Alex Cobham (@alexcobham) June 3, 2021

Irish subsidiary of Microsoft made $315bn profit last year, c.3/4 Ireland’s GDP.

Zero employees and zero corporation tax as is “resident” in Bermuda.

“Microsoft Round Island One” indeed.

https://t.co/feXHlD1KYt

10:50am GMT Thursday 3 June 2021 – Eight tech companies in the UK avoided an estimated £1.5bn in 2019

A new report by Tax Watch reveals that Amazon, eBay, Adobe, Google, Cisco, Facebook, Microsoft, and Apple made an estimated £9.6bn in profit from sales to UK customers in 2019, a new analysis by TaxWatch shows. But by moving money out of the UK, these companies ended up declaring a fraction of these profits in the accounts of their UK subsidiaries, radically reducing their tax liabilities.

The eight large tech companies faced UK corporation tax liabilities of £297 million in 2019. That puts the total amount of tax avoided by the companies in the UK at an estimated £1.5bn in 2019, the latest year where figures exist.

Commenting on the report, Alex Cobham, chief executive said:

“These corporate tax abuses makes it clear how self-sabotaging the UK’s position is on putting a digital tax on some multinationals before a a global minimum tax on all multinationals. The UK’s current digital tax would raise less than half a billion pounds a year, while TaxWatch show this handful of tech companies have short-changed British taxpayers out of three times that amount in tax in 2019 alone. A global corporate tax rate on the other hand can add £14.5 billion in annual tax revenues.”

The report is available here.

Wednesday 2 June 2021

5:31pm GMT Wednesday 2 June 2021 – WEF latest to join tax justice consensus; points to OECD alternative for global tax rate

The World Economic Forum (WEF) has published a white paper identifying the global minimum corporate tax rate and a UN tax convention as key policy pathways for ambitious economic recoveries post-pandemic. Reacting to the white paper, which references the Tax Justice Network’s research, Alex Cobham, chief executive at the Tax Justice Network said:

“We’re delighted to see WEF join the growing consensus around the recommendations of the high-level UN FACTI panel on how to replace failing global tax rules set by the OECD. The WEF hasn’t just identified a global minimum tax rate as a crucial tool for economies’ recovery post-pandemic, but has specifically drawn attention to the importance of implementing a global tax rate under the more balanced METR proposal instead of the OECD proposal.

“The METR (Minimum Effective Tax Rate)1 proposal recovers more underpaid tax from multinational corporations and spreads it more fairly among countries. Economically, morally, logistically, the METR proposal is the superior way to implement a global minimum corporate tax rate.2 The fact that the less effective, more complicated and grossly unfair proposal put forward by the OECD is even being considered in face of a far better alternative only goes to show how inappropriate it is for our global tax rules to be set by the club of rich countries and tax havens at the OECD.

“WEF is right to support the call for a UN tax convention to inclusively and meaningfully bring an end to the race to the bottom. Under the OECD proposal, the G7 countries – which account for 10% of the world’s population – would capture more than 60% of the additional revenues. The G7 meeting this weekend could set the course for an ambitious minimum tax rate with a fair share of revenues for all – or they could confirm that they are only looking out for their own narrow interests, even during a worldwide pandemic. That would underscore how right the World Economic Forum is to join the calls for a globally inclusive process at the UN, to ensure that global corporate tax rules are genuinely democratic and principled on our human rights.”

Tuesday 1 June 2021

8:22 GMT Tuesday 1 June 2021 – EU shot at tax transparency rattles multinationals’ woodwork but fails to score

An EU trialogue agreement was reached today on country by country reporting after months of negotiations. Responding to the agreement, Alex Cobham chief executive at the Tax Justice Network said:

“The EU trialogue’s shot at tax transparency has rattled multinationals’ woodwork but failed to score the goal the world urgently needs right now. It’s a step forward because the EU has formalised its commitment to make at least some of the largest multinational corporations publish at least some of their country by country reporting data. While this may not go far enough to finally lift the lid off of hundreds of billions in global corporate tax abuse, the EU has broken the taboo over requiring any publication of this data. The EU just showed everyone even a corporate giant can disclose.”

Read the full statement from the Tax Justice Network here.

6:18pm GMT Tuesday 1 June 2021 – New report reveals US Company ViacomCBS underpaid at least $4bn in corporate tax in the US

The Centre for Research on Multinational Corporations (SOMO) has just published a report showing that for almost two decades, ViacomCBS has been using the Netherlands to avoid paying at least US$4 billion in corporate income tax in the United States. From 2002 onwards, the media conglomerate has been sublicensing its television rights to third parties and consumers outside the North American market via the Netherlands. In total, at least US$32.5 billion in revenues have been collected by the company’s Dutch subsidiaries during the period 2002-2019.

The report is extensively covered in a New York Times article titled “SpongeBob and ‘Transformers’ Cost U.S. Taxpayers $4 Billion, Study Says“, which draws attention to how US President Biden’s proposed tax overhaul could prevent ViacomCBS and other large corporations from abusing tax.

5:30pm GMT Tuesday 1 June 2021 – Renowned economist Joseph Stiglitz pens FT piece calling on European economies to support the global rate

Ahead of the G7 meeting this weekend, Joseph Stiglitz, a recipient of the Nobel Memorial Prize in Economics and commissioner on the Independent Commission for Reform of Corporate Taxation, has calling in an article for the FT on European economies to step up and support a global minimum corporate tax rate.

Stiglitz writes: “The leaders of the G7 can either be a force for change or they can reinforce the status quo. The US has made the right move. Now it is Europe’s turn to take its responsibilities seriously and ensure the winners from globalisation contribute to the wellbeing of future generations.”

5:15pm GMT Tuesday 1 June 2021 – WEF summit session on global minimum tax held today

The global minimum corporate tax rate is the subject of a session at the World Economic Form’s The Jobs Reset Summit today, where Tax Justice Network CEO Alex Cobham is speaking, along with Alicia Bárcena Ibarra, Executive Secretary, United Nations Economic Commission for Latin America and the Caribbean (ECLAC), and Stephen Carroll, Senior Business Editor at France 24.

Echoing the growing consensus in support of a global minimum corporate tax rate, the session summary reads:

After decades of a ‘race to the bottom’, major economies are now backing a global minimum tax estimated to bring in $100 billion in new revenue annually. How can international tax reform contribute to a more sustainable, equitable economic recovery?

Here’s a clip from the session featuring Alex Cobham:

.@alexcobham at @taxjusticenet says “15% will be… the biggest change in 100 years of international tax rules… When you’re thinking about what’s needed for COVAX, this is game-changing.” #JobsReset21 pic.twitter.com/KYN31yJ4tC

— World Economic Forum (@wef) June 1, 2021

The session is running now from 6pm to 6:30pm CEST can be watched live here.

2:30pm Tuesday 1 June 2021 – Draft G7 agreement shown to Reuters

A draft G7 communique shared with Reuters shows the intention to delay meaningful decisions on the global minimum corporate tax rate to July this year, when the G20 will meet.

Alex Cobham, chief executive at the Tax Justice Network, said:

“The draft G7 statement tabled by the UK would kick all the details of the global minimum corporate tax rate to a G20 meeting in July. It’s unclear at this stage whether other G7 members will support this, or insist the UK stop holding up urgently needed global progress.”

10:00am GMT Tuesday 1 June 2021 – Background information

Ahead of this weekends G7 meeting, here are a few points on why this weekend’s G7 meeting is so significant:

- Regardless where G7 members land on the rate for the global minimum tax, this marks an important steps towards cementing a global consensus in support of tax justice policy platform. A global minimum tax rate is the latest in a series of tax justice policies that were initially dismissed when first proposed by tax justice campaigners only to become international norm in recent years. This includes automatic exchange of information, beneficial ownership registration and country by country reporting.

- US President Biden’s push for a global minimum corporate tax rate, and the support it has so far received from most G7 members, has effectively called time on the sacred narrative of “tax competition” – a deeply incorrect analogy that has been used for decades to sugar-coat harmful tax cuts and deregulations, and to spur countries into a “race to the bottom”.

- Anywhere between $200bn to $400bn of additional tax revenues is on the table. While a global minimum corporate tax rate set at 21% implemented under the METR proposal↪NOTEThe METR proposal is a simplified and balanced implementation of the global minimum tax rate proposed by a group of leading tax experts. The proposal can more fairly distribute recovered tax among countries than the OECD proposal for a global rate can, while recovering an extra $103 billion in comparison to the OECD proposal at a rate of 21%. The METR proposal offers a rare win-win situation where both lower income countries and almost all higher income can recover more tax by simplifying and balancing the global minimum tax rate. up to $640bn in underpaid corporate tax from multinational corporations, compromise among the G7 members is expected to reduce the potential benefit of the global rate. Nonetheless, a total of $200bn to $400bn in additional revenue per year for countries can dramatically change the lives of billions of people.

However, there are some areas of concern the Tax Justice Network will be monitoring.

- The US has already signalled a willingness to consider the low rate of 15% for the global tax instead of the 21% the US initially proposed. The low rate not only leaves hundreds of billions of unpaid corporate tax on the table but risks leaving the race to the bottom alive and kicking.

- If the G7 go ahead with a global rate on the basis of the OECD blueprint, they will take a disproportionate amount (more than 60%) of the revenues for themselves – despite the fact that it is lower income countries that lose out most heavily in terms of the share of tax revenues lost to corporate tax abuse.

- The METR proposal delivers a much fairer distribution of recovered tax, providing lower income countries with double the amount of tax revenue they would recover under the OECD blueprint. Implementing the METR proposal for the global minimum rate would recover the equivalent to 36 per cent of the combined public health budgets of lower income countries.

- There are concerns about other more specific limitations and exceptions, like patent boxes, expected to be discussed at the G7 meeting that could unfairly limit lower income countries’ industrial strategies while failing to deter tax abuse mechanisms.

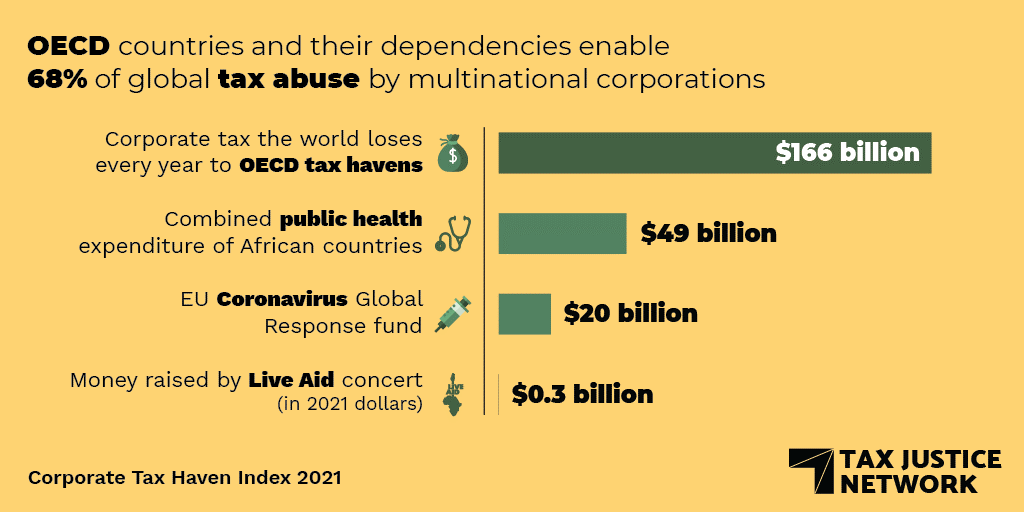

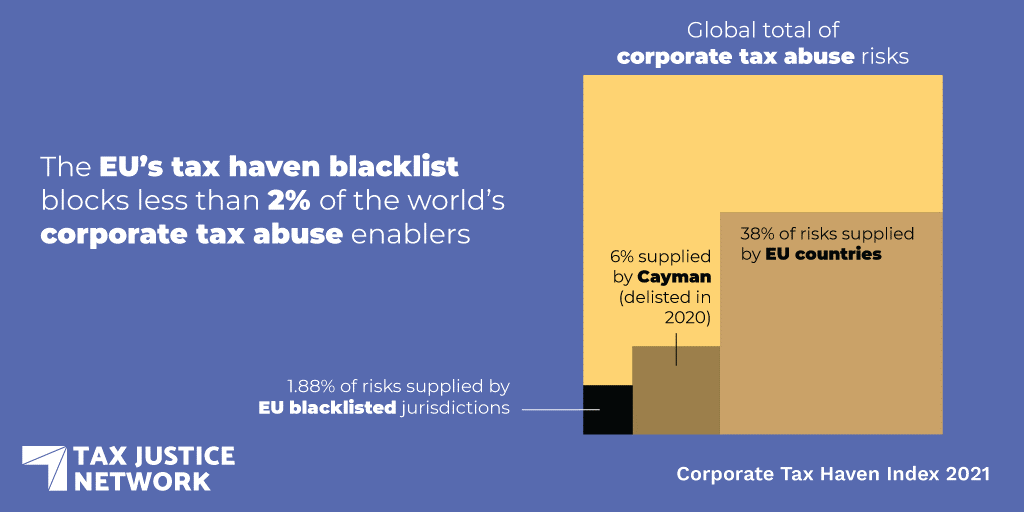

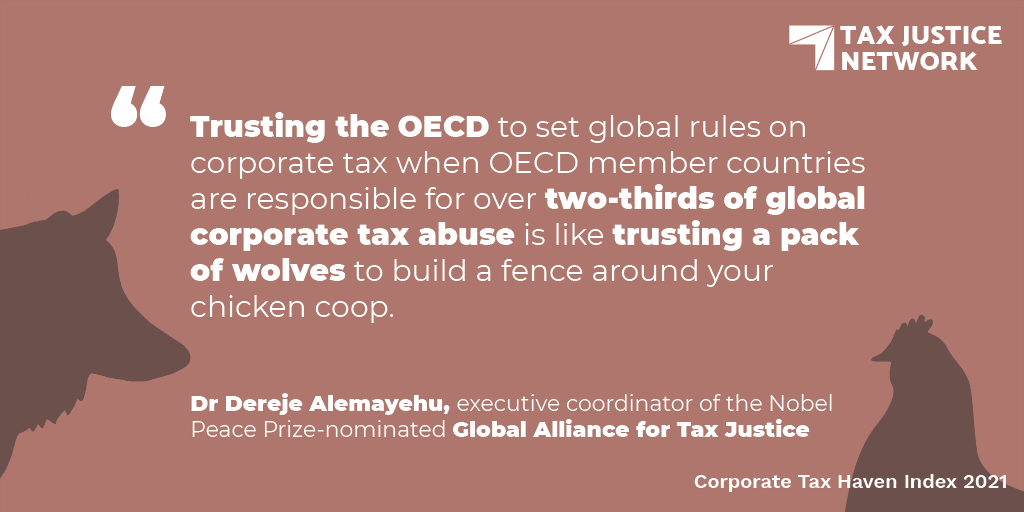

- All these above concerns only compound to confirm that having international tax rules set by a small club of rich country is entirely inappropriate and unjust. OECD countries are responsible for over two-thirds of global corporate tax abuses documented by the Corporate Tax Haven Index 2021. At the same time, the OECD blueprint from the global minimum corporate tax will see OECD countries collect a disproportionally larger share of recovered corporate taxes – which they enable multinational corporations to underpay. It’s not a shocker to see a club of rich, tax abuse enabling countries put forward a plan to end the race to the bottom that excessively rewards themselves, the worst perpetrators of the race to the bottom. Tax sovereignty requires globally inclusive setting of tax rules, through an intergovernmental tax body under UN auspices.

Here’s is some helpful reading material to get up to speed.

- Our analysis of how much each country can recover in underpaid corporate tax under a global minimum corporate tax applied under the OECD and METR proposals. You can view the country figures in this table here.

- The IMF joined growing consensus for tax justice last week in a report in published calling for both the global minimum corporate tax rate and public country by country reporting to be implemented hand in hand. Our Director of Human Rights and Tax Justice Liz Nelson, who was invited to speak on the report at an event hosted by the European Parliament Subcommittee on Tax Matters issued a statement here.

- An explanation of the METR (Minimum Effective Tax Rate) proposal by Sol Picciotto, Coordinator of the BEPS Monitoring Group, emeritus professor of law at the University of Lancaster in the UK and Tax Justice Network senior adviser, is available here.