It’s strange to write this down, but Tax Justice Network nearly ceased to exist a few years ago. Now we’re coming to the end of the strategy period that began from that position of frailty, and it’s a whole new world. For good – from the strengthening of Tax Justice Network itself, to a series of powerful achievements for the worldwide movement. And for ill – literally, in the case of the pandemic and figuratively, in the apparent deepening of rich countries’ opposition to a fairer global distribution of taxing rights.

Our annual conference earlier this month brought together leading global voices on tax justice and human rights, exploring powerful opportunities for national and international policy changes and narrative shifts. It also challenged us over the ways that we work with partners globally, and how we marry expertise and activism.

Our current strategy, designed in 2016-17, runs to the end of this year. It’s a good moment to catch a breath and think a little about the next phase of tax justice. Without prejudging the full review, we can look back at some of the key changes over that period, and then forwards to some of the decisions and opportunities ahead.

Looking back…

After taking up the role of Tax Justice Network’s director of research in 2015 (I had turned down the initial offer to become chief executive), it quickly became apparent that we were financially close to failure. Over a period of months, there were repeated discussions about how much of our salaries the directors could afford to suspend, in order for the whole team to be paid. And so in 2016, some five years ago now, I accepted the role of chief executive.

Lest this sound like a complaint, the first thing to say about those five years is that they have been a time of extraordinary recovery and growth. Tax Justice Network did not go bust. Instead, we flourished. It’s been an absolute privilege to work with a quite brilliant team of people, from communications and advocacy to legal and quantitative analysis, and crucially also of operations experts as we’ve moved from start-up phase into a period of rapid professionalisation.

I’d been in and around the wider tax justice movement since the turn of the millennium. Working as a junior researcher at Oxford with Prof Valpy FitzGerald (now a commissioner at ICRICT), I’d had the eminent good fortune to be involved in the background work behind a couple of the moments that seem somewhat pivotal in hindsight. We had a small hand in contributing to and reviewing the famous Oxfam report of 2000 on tax havens, in which John Christensen, Sol Picciotto and others had been centrally involved. And we were privileged to hold the pen for enough of the process to ensure that the UK government’s 2000 white paper on globalisation included what was then quite ground-breaking recognition of international tax issues:

“Taxation of the profits of transnational corporations operating in developing countries provides an important mechanism for sharing the gains from globalisation between rich and poor countries, and for reducing poverty through generating adequate revenue for investment in health and education… There is a need for greater international co-operation to avoid [a] ‘race to the bottom’.”

From the perspective of an engaged outsider, the early years of Tax Justice Network seemed to fly. By the 2007 launch of Tax Justice Network – Africa at the World Social Forum in Nairobi, the continuing progress of the movement seemed almost inevitable. The expertise and commitment of activists worldwide would surely build to global impact?

But five years later, lines were being drawn. Our co-founders John Christensen and Richard Murphy wrote a paper on ‘The Next Ten Years of Tax Justice’, proposing a division between a ‘non-campaigning’ Tax Justice Network to lead on research, and a separate global body to lead on activism. The latter spun out as the Global Alliance for Tax Justice in 2013, the umbrella body for mass mobilisation worldwide.

Two things that I’d never appreciated from outside, while working on tax justice at international NGOs and research organisations, were the organisational fragility of Tax Justice Network; and the relationship damage caused by the organisational separation. By 2015, it turned out, both were at something of a low point.

Organisational recovery and flourishing

The financial and organisational issues were the more obvious ones, from the inside – but also, as it turned out, the easier ones to address.

From that low point, we have built a diverse funding base including a range of foundations and national governments. Reflecting the growing faith of funders, we doubled our annual expenditure from 2015 to 2019 alone, and have built up committed income and reserves with a view to ensuring our future sustainability.

As important, we have professionalised fully, putting in place the set of policies necessary for a responsible employer operating in multiple countries and regions of the world. We’ve added the tech platform to make this global remote working really fly, and ways of working across timezones and cultures. And we have put in place a governance structure that maintains the cooperative ethos long held dear, with members retaining the ultimate power to determine the organisational direction, but also ensures independent accountability through non-executive directors – with the latter, for example, responsible for agreeing changes to compensation and benefits. Following team consultation, expert advice and a thorough benchmarking exercise, we moved from the previous somewhat unstructured and unfair distribution that had emerged from our ‘start-up’ phase, to establish a payscale based on transparent and explicit criteria. The ratio of the highest and lowest salaries is currently 2.7.

Introducing team retreats during the year, to allow in-person interactions among the global team, had strengthened bonds in important ways. So when the pandemic struck, we had the advantage of being fully remote already, and as good a base of personal relationships as we could hope for in a dispersed global team. It has been hard, and it continues to be hard. But we are committed to a practice of caring for each other within the team, and the conversations are always ongoing about how we can strengthen that in different ways.

An important underpinning of this whole organisational strengthening was a five-year commitment from the Ford Foundation. Two elements were crucial. First, the engagement of Rakesh Rajani, leading the Foundation into an understanding of tax justice and a decision to support it – and encouraging us to lay out a strategy for systemic change (‘build it and they will come!’), rather than look to address funders’ immediate interests. And second, the Foundation’s BUILD program designed specifically to support ‘organisational resilience’ – everything from the provision of expert consultants with understanding of issues like founder’s syndrome, through to a positive encouragement to commit their funds to building our reserves.

It’s a great sadness that Ford switched focus within a couple of years, but to their credit that they maintained this support anyway. We would not be the organisation we are today without it, and much of what has been achieved would instead have been lost. Coupled with the consistent policy-led engagement of key funders like Norad, this support has been transformative.

Thematic priorities

In terms of activities, each of the four workstreams in the strategy we laid out has delivered substantial progress. Perhaps the deepest work has been that of the workstream on tax justice and human rights, led by Liz Nelson (who is also a Senior Atlantic Fellow for Social and Economic Equity). This has developed with a range of partners including the Global Alliance for Tax Justice and the Centre for Economic and Social Rights, and valuable funding from the Wallace Global Fund, a powerful analysis that is increasingly recognised in both the human rights discourse and across the tax justice movement. Tax justice perspectives are increasingly reflected in country assessments under a range of UN human rights instruments; and human rights arguments are increasingly central to advocacy for tax justice in national policy debates.

Our annual conference earlier this month focused on this workstream and saw the launch of a major new report, Tax Justice and human rights: The 4 Rs and the realisation of rights. A stellar global cast was testimony to the platform that Tax Justice Network has built, and the strength of partnerships in this area in particular. Speakers and discussants included Andres Arauz, Ecuadorian presidential candidate; Attiya Waris, Associate Professor of Fiscal Law and Policy at University of Nairobi, and the newly appointed UN Independent Expert on the effects of foreign debt and other related international financial obligations of States on the full enjoyment of human rights; Dorothy Brown, Professor of Law at Emory University and author of The Whiteness of Wealth: How the Tax System Impoverishes Black Americans- and How We Can Fix It; Irene Ovonji-Odida, women’s rights activist and member of both the UN FACTI Panel and ICRICT; Logan Wort, Executive Secretary at the African Tax Administration Forum (ATAF); Paul Caruana Galizia, on behalf of the family and foundation of Daphne Caruana Galizia; and Philip Alston, Professor of Law at NYU and recently UN Special Rapporteur on extreme poverty and human rights.

The workstream on financial secrecy led by Dr Markus Meinzer has consistently delivered our flagship Financial Secrecy Index, and has successfully introduced the complementary Corporate Tax Haven Index. Together, these have been recognised in policy spheres and in research as unique and technically excellent contributions. At a campaigning level, they have supported a powerful shift in public narratives towards the understanding that financial secrecy and corporate tax abuse are largely driven by rich countries, promoting illicit financial flows and corruption around the world.

The index teams have also been consistently innovative. Where the human rights workstream has contributed to establish tax justice within a much wider discourse and international political canvas than could have been imagined ten years ago, the secrecy workstream has gone far beyond the initial ambitions of challenging weak ‘blacklists’, and overturning the narrative of corruption as a problem of lower-income countries, and has developed a whole series of analyses and tools that are increasingly being used by national authorities to strengthen their responses to tax abuse, of which the Illicit Financial Flows Vulnerability Tracker has been especially important. In addition, detailed policy work on aspects of the ABC (automatic exchange of information; beneficial ownership transparency and country by country reporting) has taken each far beyond the original ideas set down by the Tax Justice Network in the early years.

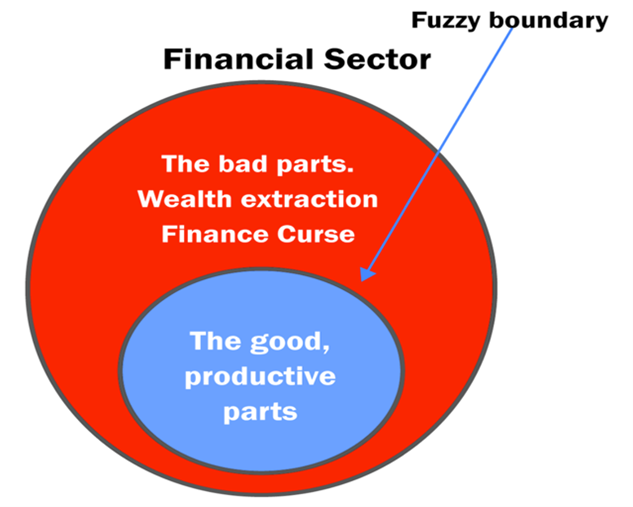

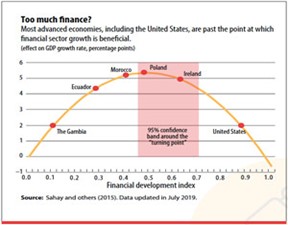

The workstream on the race to the bottom has also contributed to progress in shifting narratives, building the view that tax (and regulatory) competition damages the ‘winners’ and the losers alike. Major outputs include the Balanced Economy Project, which has been incubated and fledged as an independent organisation to lead analysis and campaigning on the threats of monopoly power; the continued strengthening of the ‘finance curse’ argument (that too much finance is damaging for economies and societies), including through Nicholas Shaxson’s book of the same title; and John Christensen’s forthcoming film that will address these issues.

The workstream on the scale of tax injustice has focused on strengthening the evidence of the damage of tax abuse and its profile, and on embedding that analysis – including of the disproportionate losses suffered by lower-income countries – in public narratives and policy processes alike. Outputs include a range of peer-reviewed journal articles, and two books – a more academic volume published by Oxford University Press, and a lighter piece, The Uncounted. These outputs have provided the basis for Tax Justice Network to play a leading role in a range of policy processes, including work on defining the indicators of illicit financial flows for the UN Sustainable Development Goals target, in driving an agenda for global architectural reform, and both technical and political engagement in the OECD tax reform process that is still ongoing.

The work has culminated in our new annual flagship report, the State of Tax Justice, which provides for the first time a country-level estimate of revenue losses due to cross-border tax abuse by multinational companies and by individuals. Published in conjunction with the Global Alliance for Tax Justice (the umbrella body for mass mobilisation organisations worldwide), Public Services International (the tax lead of the seven global union federations) and the German foundation FES, the State of Tax Justice offers a platform for national and regional tax justice activists to raise the profile of their demands each year.

Impact and communications

The much greater depth of expertise in the team has been coupled with an expansion of the longstanding strength in communications. The Taxcast series of podcasts, led by Naomi Fowler, has been expanded from the original English to include monthly Spanish, Portuguese, French and Arabic language versions also, focusing variously on Latin America, Francophone Africa and the Middle East.

Alongside social media improvements, the Tax Justice Network doubled the volume of traffic to its website from 281,379 total sessions in 2015 (an average of 23,448 sessions per month) to a record total of 588,205 sessions in 2020 (an average of 49,017 sessions per month).

In external media, Tax Justice Network doubled the volume of coverage gained on a monthly basis from the period 2009-2015 to the strategy period 2016-2021. We gained an average of 223 media hits per month in 2009-2015 and an average of 467 media hits per month in 2016-2021. This increase in media coverage was matched by a proportional increase in coverage from high profile media sources. We gained an average of 14 media hits per month from high profile media sources like the Financial Times and the Washington Post in 2009-2015, and an average of 28 media hits per month from high profile media sources in 2016-2021.

A core part of this growth in media coverage has been the continuing strengthening of the indices, and the introduction of the State of Tax Justice report. In recent years we have built up the global media reach of the Financial Secrecy Index and the Corporate Tax Haven Index, so that their launch weeks obtained media coverage with a combined circulation reach of 0.4 billion (Financial Secrecy Index 2018) and 0.73 billion (Corporate Tax Haven Index 2019); then 2 billion (Financial Secrecy Index 2020) and more recently 4 billion (Corporate Tax Haven Index 2021).

The State of Tax Justice eclipsed even this, with a launch week reach of 8 billion, and has continued to be widely cited in policy documents, including in various United Nations outputs – not least, the FACTI Panel report. EU MEPs adopted a resolution to improve the EU blacklist of ‘non-cooperative jurisdictions’ just a few weeks after the launch of the State of Tax Justice, directly quoting our analysis that the blacklist covers “less than 2% of tax abuse”. The State of Tax Justice has also provided key reference figures for the scale of tax injustice in less politically ‘natural’ publications such as the report of the advisory group of the G7 countries prepared for their UK summit, and a report of the World Economic Forum’s Global Futures Council.

Importantly, this is not profile for its own sake. As the Tax Justice Network has become increasingly established as a credible and legitimate voice on international tax issues, so too have we been able to achieve normalisation of a range of tax justice proposals once considered too radical to mention.

Our framing of the G7 agreement on the G20/OECD global tax deal was widely adopted in media and press. The Tax Justice Network was referenced in 4% of all articles published around the world on Monday 7 June 2021 about the G7 tax deal agreed over the preceding weekend. These articles accounted for 11.5% of all global media reach gained by all the articles published on the G7 tax deal on Monday 7 June 2021. In other words, over 1 in 10 articles read on Monday 7 June 2021 around the world about the G7 tax deal quoted the Tax Justice Network.

A core element of our narrative – that the global minimum tax rate is potentially a great step forward, but that the specific deal in prospect disproportionately favours the G7 and other high-income countries, while exacerbating the global inequalities in taxing rights facing lower-income countries – has been carried far and wide. This has allowed us to raise up voices of lower-income countries in a way that has no precedent in any previous OECD process. (Not unrelatedly, we have been targeted repeatedly by the OECD secretariat to negotiators, ambassadors, at the UN, and to media – but sadly for them, this has served only to strengthen our profile.)

Or consider another example with genuinely transformative potential for the global tax architecture: with our partners in the State of Tax Justice 2020 report, we have put the proposal for a UN tax convention on the map. In the seven months before the launch of the State of Tax Justice 2020, the term “UN tax convention” had an average monthly media reach of 348,000. In the launch month of November 2020, the term gained a reach of 1.7 billion. 83 per cent of stories published with the term “UN tax convention” in November 2020 reference the Tax Justice Network, almost all of which were about the State of Tax Justice 2020. From April 2020 to date, half of all media reach for the term “UN tax convention” included reference to the Tax Justice Network.

Our ability to drive previously unthinkable narrative shifts and policy consideration stems from the combination of our deeper research capacity and the technical strength of our outputs; with the growing power of our communications work, based on the comprehensive professionalisation of the organisation.

Relationship building

In contrast to the success of that transformation, the harder issue – of relationships within the tax justice movement – is one where I have to hold my hands up to having failed to identify the extent of the issue at the outset, and having failed to act with the necessary speed.

In this year’s annual tax justice lecture, we invited Dr Dereje Alemayehu, the executive coordinator of the Global Alliance for Tax Justice, to reflect on the challenges of the movement. He pulled no punches. Laying out a history of paternalistic and dismissive behaviour from ‘experts’ in the global North to their ‘activist’ counterparts in the South, he set out a key challenge: to bring expert and activist approaches together, in mutual respect and solidarity.

This is crucial, if tax justice is to move forward together with the impact that we wish to have, and in the spirit of care for one another and an understanding of the inequalities and discrimination embedded in our world by the unfair economic practices we seek to challenge – and without which, ‘tax justice’ seems little more than a slogan.

Looking forwards…

As our existing strategy comes to a close and we review while developing the new one, there will be time and opportunity to consider each element in more detail.

Many of the central pieces of our approach are already clear though, among them: global campaigning, in partnership; global communications and media reach; technical excellence; high-level advocacy; built upon financial resilience and robust governance.

Thematically, we will continue to build upon the outline of issues that John Christensen and colleagues began expertly to develop in the early 2000s, and of which we have since solidified key elements and increasingly taken them further.

On the corporate tax side, we now have a clear position towards unitary taxation with formulary apportionment, backed by a fair global minimum effective tax rate. The tax transparency umbrella is formed by what we have coined as the ABC: automatic exchange of tax information, beneficial ownership transparency, and public country by country reporting. The global architectural requirements include a UN tax convention, setting the basis for intergovernmental negotiations under UN auspices, and a UN centre for monitoring taxing rights; and the continuing development, with our partners at ICRICT, of the arguments and technical basis for a global asset register, in turn supporting the case for wealth taxes.

We will continue to extend the analysis of tax justice in a range of areas. We’re likely to pay greater attention to the pressing threat of the climate crisis, to the extent that we can make clear contributions without duplicating the efforts of others. We may put more emphasis on the role of tax collection, recognising the political threats to tax authorities and the regressive impact of cuts; and on the continuing scale, opacity and ineffectiveness of tax expenditures. And we’re likely to address some important questions of race and reparations, from a tax perspective.

Perhaps more important than individual areas is the overarching aim – which will be to approach tax justice as a feminist issue. Adding specificity to this, to ensure it too is more than a slogan, will be key. We are now clear that we must take a rights-based approach in all our work, and one that challenges intersectional inequalities head-on. That includes reflecting on the many processes of racialisation and minoritisation embedded in the legacies of imperial capitalism on which so much of our current inequalities rest – and without an understanding of which, any tax ‘justice’ can be superficial at best.

This understanding must continue to lead our own behaviours and operations, not only to inform our analyses – from Tax Justice Network’s engagements in the wider movement, to our internal processes and interaction.

Feminist leadership isn’t built on rigid hierarchies, or dictating plans. Caring for others, dismantling bias and the sharing of power are among the central principles that Tax Justice Network will strive to meet. And tax justice itself? Well, that definitely isn’t mine, or even ours – it’s yours.

Together, we can change the weather. We must. Let’s do it.