Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

In this episode, Naomi Fowler discusses degrowth, rethinking economies and value in part 2 of her conversation with economic anthropologist Jason Hickel. Part 1 is available here.

Plus: the Pandora Papers – 3 things the latest offshore leak is showing us.

Why some countries rejected the OECD’s 15% minimum global corporate tax deal

And, as COP26 begins in Scotland, it’s the ‘last chance saloon’ to take meaningful action to minimise ecological disaster. Can politicians learn from nations leading the way with good policies on energy?

Produced and presented by Naomi Fowler of the Tax Justice Network

Transcript available here. (Some is automated and may not be 100% accurate)

Rethinking economies #115

This is a global ecological crisis, and it has to do with the way the global economy works. And this requires mobilisation on the scale of the anti-colonial movement.”

~ Jason Hickel

The cutting of resources for the tax authorities and forces of law and order is a major problem and if there’s one thing above all that needs doing and that’s to start giving the tax authorities and international criminal authorities proper resources to start chasing this stuff“

~ Nick Shaxson

There are many reasons why Nigeria refused to endorse and sign the OECD deal [15% minimum corporate tax rate] Countries like Nigeria already have a company income tax rate of 30%…you have countries like Ireland, Switzerland and other countries who are already close to that 15%, so it doesn’t look like it’s going to be any significant change for them. So for countries like Nigeria, there isn’t real incentive to sign up to this deal as it doesn’t offer much for them.”

~ Mustapha Ndajiwo

The debate around how to structure the political economy for renewable energy markets hasn’t even reached its infancy. There’s very little progress towards that kind of really progressive thinking that’s needed if we’re going to make the energy markets actually work for ordinary people. Denmark, Germany and other countries are signalling how this could be done so differently.”

~ John Christensen

Further reading:

Watch the full interview with Nick Shaxson on SABC News here.

Read more from Mustapha Ndajiwo and Learnmore Nyamudzanga on why Nigeria rejected the OECD minimum global corporate tax deal here: What Does the G7 Proposal on Taxation of the Digitalised Economy Mean for African countries?

Can the Most Powerful Global Tax Organization Shed Its Racist Ways? The Organization for Economic Cooperation and Development insists it’s “inclusive,” but it’s still strong-arming countries in the Global South. Article here by Professor Steven Dean.

Here’s an interesting chart showing emissions per person of the world’s biggest countries, worth a look.

The Government of Indonesia has launched an investigation on pricing and customs reporting practices of a pulp mill owned by one of Indonesia’s wealthiest moguls. The investigation follows the launch of the Macao Money Machine report published by Indonesia’s Tax Justice Forum and other civil society groups including Tax Justice Network.

The report documents pricing practices of two pulp mills with common beneficial ownership exporting to China between 2007 and 2018. The pulp exports from Indonesia were sold at below-market prices to affiliated companies in Macao and Singapore apparently by mis-labeling the product as a lesser-grade of pulp that commands substantially lower market prices. The affiliated companies in Macao and Singapore then sold the same pulp at significantly higher prices that reflected the market values of the actual product, and thereby realizing a lot of the profit outside the grasp of Indonesia’s tax authorities.

Across a dozen years between 2007 and 2018, these pricing practices resulted in potential tax losses exceeding $150 million from an estimated $668 million in understated revenue.

The Macao Money Machine case, documented with transaction-level data and audited financial reports from publicly-held companies, is one of only a handful of specific examples that Indonesia can point to in a broader transfer pricing problem in the natural resources sector that it said is responsible for $15.6 billion in losses in 2016 alone. One of the other prominent cases involves an oil palm producer owned by the same tycoon who owns the pulp mills, and which became Indonesia’s largest case of tax evasion.

Fortunately, Indonesia’s financial governance reform efforts, led by Finance Minister Sri Mulyani, a former Deputy Director of the World Bank, have included policies that address the ‘ABC of tax transparency’: automatic, multilateral exchange of tax information with numerous countries; beneficial ownership disclosure requirements; and, critically, the requirement of country-by-country reporting by multinational companies.

Implementation challenges abound for this ambitious tax transparency reform policy. Information exchange relationships need to be operationalized. There’s been limited compliance with the beneficial ownership disclosure requirements: less than 20% of corporations (PT) have made a declaration and those that have are yet to face a credible verification mechanism. And the country-by-country reporting requirements are not made public.

But the fact that the Government of Indonesia is working through these implementation challenges sets the country on a promising trajectory. The Macao Money Machine case represents an opportunity for the Government to take action in a way that nets substantial government revenue, showing both that the tools work and that they can generate government benefits to ease a strained fiscal situation.

Indonesian civil society groups are urging the government to follow through with its investigation into one of the pulp mills, PT Toba Pulp Lestari, and to open an investigation into the larger of two pulp mills, PT Riau Andalan Pulp & Paper, for which pricing practices were documented between 2016 and 2018.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa con Marcelo Justo and Marta Nuñez:

Los Pandora Papers: la caja que contiene los secretos fiscales de los multimillonarios y los grandes poderes del mundo.

Impuesto mínimo a las multinacionales: ¿hay que aceptar o rechazar la propuesta de la OCDE y el G20?

Afganistan, la crisis de la inmobiliaria china Evengrande y quién ejerce el liderazgo hoy a nivel mundial.

El Bitcoin en El Salvador: ¿vanguardia iluminada o receta para el desastre?

José Antonio Ocampo director del ICRICT, la Comisión Independiente para la reforma de la Fiscalidad corporativa internacional.

Oscar Ugarteche Director del Observatorio Global Latinoamericano, OBELA, profesor de la Universidad Nacional Autonoma de Mexico, la UNAM y autor de Historia Critica del FMI

Los Pandora Papers, el Bitcoin en El Salvador y crisis de la inmobiliaria en China #64

The Pandora Papers is full of stories involving trusts, particularly South Dakota trusts. This short blog explains why trusts are so problematic and what we can do about it.

What is a trust?

Depending on the country, a trust may be considered an entity (similar to a company), a contract, an arrangement or just a relationship. Although lawyers and academics love to point to the nooks and crannies that set these classifications apart from each other, none of these distinctions are that important for understanding why trusts are so problematic from a transparency and justice perspective.

In essence, trusts involve a legal structure where a person (called the settlor) transfers assets to a trustee, who will hold the (trusted) assets under their name and manage them according to the settlor’s directions in favour of the beneficiaries appointed by the settlor. Why would anyone do this instead of giving the assets directly to the beneficiaries? The idea of trusts, which originated in England in the Middle Ages, is that for some reason the beneficiaries cannot or shouldn’t hold the assets yet, so it’s better for someone else, a trusted person, to manage and hold the assets on their behalf until they are ready to receive them. Based on this basic structure, trust enthusiasts commonly give the example of a responsible parent who sets up a trust to ensure that a trustee will take care of their vulnerable children after the parent (settlor) dies. This is a very noble goal, but there’s more to it.

Why are trusts problematic?

As explained in our paper “Trusts: Weapons of Mass Injustice?”, although trusts can indeed be used to protect beneficiaries who are sick and vulnerable, nothing in the law actually requires this. Instead of helping those in need, the trust beneficiary could turn out to be a person convicted of sexual abuse against a minor or a person convicted of murder. In addition, depending on the country where the trust was created, all these different parties (the settlor, the trustee and the beneficiary) do not necessarily need to be different people. Rather, they could just refer to the same person, or alternatively may be under the control of the same person.

Trusts are especially problematic for two reasons. First, their secrecy. Second, their capability to shield assets from the rest of society (tax authorities, victims of sexual abuse or murder or fraud, etc).

Secrecy

Unlike companies and other legal persons which need to incorporate and register with the commercial registry in order to exist, trusts usually require no such registration. For this reason, there’s no way of knowing how many trusts exist in the world, let alone how many assets they hold or who the people are that are behind them. While some countries require some trusts to register (eg the EU) and individuals may have reporting obligations to tax authorities if they are subject to tax, not all types of trusts are covered. Even for those which are covered, enforcement is very problematic given that no one may know that the trust exists in the first place. In many cases, the only way the public becomes aware of them is through leaks such as the Panama or Pandora Papers, or via media coverage of divorce cases of multimillionaires.

Even countries that require (some) trusts to register tend to allow trusts to enjoy more secrecy, compared to companies and other legal persons. For instance, while the EU 5th anti-money laundering directive requires public access to companies’ beneficial ownership information (the natural persons who ultimately own or control the companies), in the case of trusts access is limited only to those with a ‘legitimate interest.’

In addition to not requiring all trusts to register, countries may fail to obtain information about all the relevant people involved in a trust. While companies tend to have very simple structures encompassing just shareholders with the same voting rights, trusts involve many parties. The three parties in a classic trust setting (the settlor, trustee and beneficiary) can involve many more: a legal (nominee) settlor, an economic settlor (the real owner of the assets to be transferred), the trustee, a protector or enforcer, a beneficiary who may be determined, discretionary or anyone belonging to a defined “class”. Trusts can now just have “purposes” (eg to concentrate family wealth) instead of beneficiaries. What’s more, many of these parties may themselves be legal persons (eg a corporate trustee, a corporate protector) making it even harder to determine who is behind the trust and who is in control of it.

Trusts are therefore often used to integrate more complexity into the ownership structure of a company or asset (eg a house) in order to create more secrecy around its real owners. Institutions like the World Bank, the Financial Action Task Force (FATF) and the Egmont Group suggest that the involvement of trusts in major corruption or money laundering scandals may be underestimated because trusts are so complex that authorities don’t bother to take action against them (assuming they even know about them).

Investigators interviewed as part of this study argued that the grand corruption investigations in our database failed to capture the true extent to which trusts are used. Trusts, they said, prove such a hurdle to investigation, prosecution (or civil judgment), and asset recovery that they are seldom prioritized in corruption investigations. Investigators and prosecutors tend not to bring charges against trusts, because of the difficulty in proving their role in the crime… As a result, even if trusts holding illicit assets may well have been used in a given case, they may not actually be mentioned in formal charges and court documents, and consequently their misuse goes underreported.

The interaction of the trust with other legal persons adds an additional layer of complexity and helps frustrate efforts to discover beneficial ownership… It is also possible that the use of legal arrangements may increase the difficulty of investigating and identifying the beneficial owner, thereby explaining their relatively low prevalence in the case study sample.

Asset protection

Apart from hiding assets and owners’ identities, trusts can shield assets from everyone else even in cases where there is full transparency on the trust’s existence, the identities of their parties and the value of their assets. Unlike companies which merely grant “limited” liability, trusts may achieve full immunity thanks to what we call the “ownerless limbo”. On paper, it appears as if trust assets aren’t owned by anyone. The settlor would say: “I’m no longer the owner, I gave the assets to the trust/trustee”. The trustee would say: “I’m not the real owner, I merely hold and administer the assets in favour of the beneficiaries, but I cannot do as I want with assets nor are they a part of my personal wealth”. Finally, beneficiaries would say: “We don’t own the assets yet, they must first be distributed to us after X time”.

One of the special types of asset protection trusts are discretionary trusts, which suggest (on paper!) that the trustee has full discretion to distribute assets to beneficiaries, determining who will receive what, when, how much and even “if”. In other words, discretionary trusts allow beneficiaries to say “I’m so distant from owning the trust assets, because it’s not that I don’t own them yet, but I may never own them at all, unless the trustee uses their discretion to distribute anything to me”. This argument is used, and sometimes even endorsed by the OECD (p. 19) to justify not requiring the disclosure of “discretionary beneficiaries” – because they may end up not receiving anything at all.

Of course, reality may be very distant from what it says on paper, and all settlors and beneficiaries may be enjoying the assets (eg using the mansion, the yacht and the private jet). It’s only when someone else tries to get access to an asset that they are all able to hide behind the trust paper claiming no one actually owns it. Asset protection trusts are so effective, that they have shielded assets against the US tax administration (the IRS), and unfortunately even against victims of sexual abuse and murder.

Why South Dakota?

South Dakota has been actively promoting itself as the ideal jurisdiction of choice both for US Americans (so that they don’t go to set up trusts in some remote island) as well as for foreigners, eg actively promoting trusts to Latin American elites.

Many may prefer South Dakota over a small tropical island because it is in the US. Although the US ranks as the 2nd worst offender in the Tax Justice Network’s Financial Secrecy Index, most countries don’t consider the US to be a “tax haven”, affording a higher degree of perceived reputation to US trusts.

Although South Dakota is widely mentioned in the Pandora Papers, it would be naïve to consider that it is the only risky jurisdiction with regards to trusts. As described here, many jurisdictions such as the Cayman Islands (its STAR trust), the BVI (its Vista Trust), Belize, Cook Islands, Nevis as well as other US States (Nevada, Alaska) have been offering very abusive trust provisions. Apart from the lack of transparency (given that trusts are usually not required to be registered in most places, let alone give public access to that information), many of these jurisdictions offer legal frameworks that ensure or allow for, among others:

non-recognition of foreign laws or foreign judgements (which may invalidate the trust, eg because of violating inheritance laws)

flexibility on the duration of the trust ranging from 100 to 1,000 years or no time limit at all

the possibility for the settlor to also be a trustee and/or beneficiary or to have sufficient powers to be able to control the trustee

“spendthrift” provisions (which prevent trust distributions to indebted beneficiaries)

limited time to initiate an anti-fraud action against a trust (eg in cases where it was indeed created to shield assets from a creditor) and increasing the burden of proof, demanding the victim proves beyond reasonable doubt that the only purpose of creating the trust was to defraud them.

Finally, the strategy of these trust jurisdictions is that victims and defrauded creditors would have to file lawsuits in many of these offshore jurisdictions or to spend a lot of time obtaining sufficient details about trusts that are often changing (the trust could in many cases migrate to other jurisdictions, change trustees, etc.). This would discourage even starting investigation or legal action where a trust is involved.

What can we do about it?

Countries should:

Establish public online registries of the beneficial owners of trusts (eg. Denmark), covering any trust created according to local laws as well as any foreign trust with local assets or local parties (the settlor, trustee, etc)

Neutralise the “ownerless limbo” by considering that trust assets are always owned by the settlor, until trust assets were distributed to beneficiaries (who would then become their owners). In other words, if a settlor has creditors and claims to have no money to pay the debt, creditors should be able to get hold of the trust assets as part of the payment.

Establish lists of jurisdictions with abusive trust regimes (eg based on their secrecy and asset protection provisions) and prohibit residents from being connected to trusts from these jurisdictions, or disregard by considering invalid any of those trusts operating in the local territory or holding assets.

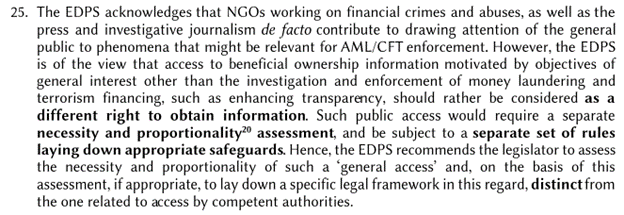

This blog post contextualises the new Pandora Papers leak. It explains the need for public beneficial ownership registries, it opposes the latest opinion by the EU Data Protection Supervisor on the matter, and it shows how to use recent US case law to get the names of enabler’s clients, regardless of professional secrecy. It ends with a proposal suggesting that, just as banks are required to report their account holders to authorities and intermediaries are required to disclose schemes to hide beneficial owners, lawyers and corporate service providers should start reporting the identities of the clients for whom they set up offshore structures to authorities on an annual basis.

The Pandora Papers are yet another leak that exemplify the urgent need for public beneficial ownership registries around the world. Public beneficial ownership registries are official registries or databases (eg a commercial register) which collect information on the natural persons who ultimately own, control, or benefit from any legal vehicle (eg company, trust, etc). Having a record of the natural person (or beneficial owner) behind every legal entity serves to prevent the kind of financial secrecy that enables illicit activity. When public access to beneficial ownership information is not available, the public (and in some cases, the authorities) rely on leaks to access this information. In fact, as we’ve argued in a previous blog post, public access to beneficial ownership information would make leaks obsolete. Everyone would have access to beneficial ownership data without needing to depend on whistleblowers and journalists.

Undermining transparency: the EU Data Protection Supervisor

In an act of apparent hostility toward beneficial ownership transparency, which started gaining public support after the Panama Papers and the Paradise Papers, the EU Data Protection Supervisor issued Opinion 12/2021 on 22 September 2021 in which they expressed opposition to the growing movement for public access to beneficial ownership information as enshrined in the EU 5th Anti-Money Laundering Directive (AMLD 5). (This non-binding opinion is about the “AML legislative package” adopted by the EU Commission on 20 July 2021, which among other items, reiterates the call for public access to beneficial ownership information as established in AMLD 5).

The EU Data Protection Supervisor (EDPS) concluded the following:

As we have described in the UN High-Level FACTI Panel background paper on beneficial ownership transparency, disclosing information on beneficial owners is critical for tackling many types of illicit financial flows. Although money laundering and terrorist financing are important issues, so are tax abuse, corruption, unjustified enrichment, bid rigging, conflicts of interest, etc. In fact, the trend now is towards using data such as automatic exchange of banking information under the OECD’s Common Reporting Standard both for tax and money laundering cases (eg Punta del Este Declaration, page 6), rather than restricting access for just one purpose.

The worst part of Opinion 12/2021, however, is that, despite acknowledging the role of civil society organisations and the media in the fight against illicit financial flows and the fact that more EU countries are establishing public online registries of beneficial ownership, the Opinion still discourages public access until another study is done to assess proportionality and other issues. Creating a commission to discuss an issue and adding as many people as possible is a commonly-known disingenuous tactic for preventing further action.

In light of this opposition to public access to beneficial ownership information, it’s worth remembering, as explained here, that no one is obliged to create companies or other structures. If individuals do not wish for their identities to be disclosed or leaked from service providers, they could operate in the economy or hold assets under their own name. Agreeing to beneficial ownership transparency should be the least of the conditions under which individuals are permitted to set up legal vehicles which operate in the economy on their behalf, own assets, etc.

This transparency requirement is especially relevant if the individuals involved will also benefit from limited liability. What’s more, most companies have very simple structures (eg 85 per cent of UK companies are directly owned by individuals or by a company which in turn is directly owned by an individual). This means that in most cases, the shareholder (legal owner) and the beneficial owner are one and the same. In addition, most countries give public access to legal ownership information (after all, many commercial registries are called “public mercantile registries”) because this was considered necessary for trade. In other words, information on the individuals who own a business was made publicly available so that investors could know who they are dealing with.

Therefore, given that for most companies the beneficial owner and the legal owner coincide, beneficial ownership information has technically been publicly available in regular mercantile registries that disclose shareholder information. Beneficial ownership registries become relevant only when individuals set up complex ownership structures, including the integration of foreign entities (mostly from secrecy jurisdictions) into the ownership structure. These complex ownership structures make it impossible to determine the beneficial owner by looking at the local commercial register alone. An attempt to restrict public access to beneficial ownership information distorts the level playing field in local economies to benefit offshore investors/vehicles.

Moreover, contrary to this opinion which undermines the case for public access, it’s worth remembering that the Panama Papers, Paradise Papers – and most likely as will the Pandora Papers — have proven time and again the same fact: it’s not that “NGOs and the investigative journalism de facto contribute to drawing attention” to money laundering, but rather that they are indispensable to addressing illicit financial flows within our current framework. Sadly, media articles are sometimes the only real sanction that wrongdoers face and the only source of information on the users of secrecy jurisdictions.

Many authorities have had access to beneficial ownership information in (confidential) registries for years. They have also had access to data held by local financial institutions. The UK even has access to the beneficial ownership registries of some of the most problematic secrecy jurisdictions including the Cayman Islands and the British Virgin Islands (both ranked among the worst offenders by the Financial Secrecy Index), because they happen to be UK dependencies. Yet, this data is rarely used proactively. Investigations by government authorities mostly happen after a leak and many times as a result of the leak. These government actions in the aftermath of leaks may be because some governments (especially in lower income countries) didn’t have access to the data prior to the leak. In other cases, however, it may be that authorities only felt pressured to take action after the leaks became public.

Access to beneficial ownership information by the media and NGOs is so important because, other than some politicians resigning, the consequences of these leaks from law enforcement do not result in bankers, lawyers, or other enabler – let alone politicians – going to jail en masse. In other words, it’s not that Civil Society Organisations (who help the media understand and contextualise data) and investigative journalists simply help law enforcement by providing the information they need to administer consequences. It’s that their work alone may be the only type of “enforcement” that takes place (reputational risk as a result of negative press). Politicians and elites may be more discouraged from using secrecy jurisdiction because of leaks than for the fear of law enforcement.

Just as the Panama Papers led to the EU 5th Anti-Money Laundering Directive, which required public access to beneficial ownership information, the Pandora Papers demonstrate the need for beneficial ownership information to be publicly accessible in all countries, starting with major secrecy jurisdictions and financial centres. This would enable these “NGOs and investigative journalists”, as well as authorities from all over the world, to conduct investigations year round rather than depending on leaks.

What is being done and what is missing

As our paper the State of Play of Beneficial Ownership describes, by April 2020 more than 80 jurisdictions had approved laws requiring beneficial ownership data to be disclosed to a government authority. Public access, albeit still limited, is now growing in Europe (not just in the EU, but also in British dependencies, Eastern Europe, and especially in the Western Balkans). To continue moving in the right direction, however, authorities need to invest more in developing verification mechanisms and closing loopholes. Beneficial ownership will not be useful if there are pathways for certain types of legal vehicles to avoid registration (eg most laws do not cover listed companies and investment funds) and if there are too many exceptions, as is the case in the US. Moreover, establishing beneficial ownership registries just for legal persons but not for trusts misses the point, given that trusts are weapons of mass injustice and have been documented again in Pandora Papers to be vehicles of choice for illicit financial activities.

Apart from major loopholes to the scope, a big impairment to data accessibility is based on limited triggers. In other words, the parameteres for when beneficial ownership data must be registered and whose data must be registered are not inclusive enough. As explained in this brief (see page 18, proposal 4), most countries require only local legal vehicles (eg companies) to register their beneficial owners, but don’t demand this from foreign entities that may be operating in their territories or whose beneficial owners may be local residents. In other words, even a super advanced beneficial ownership register like Denmark’s would have no data on what was revealed by the Pandora Papers. The Danish register would know about Danish companies, but not about offshore companies set up by Danish residents in secrecy jurisdictions.

Until public beneficial ownership registries are available all around the world, each country should require beneficial ownership registration not just from locally incorporated legal vehicles, but also from any foreign legal vehicle with operations or assets in their territory, and from any legal vehicle that has a local participant, be it a beneficial owner, shareholder, director, etc. In other words, Denmark’s beneficial ownership register should collect beneficial ownership information on any Danish legal vehicle, as it does. But it should also collect information on any foreign legal vehicle with assets or operations in Denmark and any foreign legal vehicle in which a Danish resident participates as either a shareholder, director, beneficial owner, settlor, etc. (There are some disclosure regimes, either asset returns for public officials or asset and income returns for tax authorities, which already target offshore holdings, so expanding triggers of beneficial ownership registration is not that different to what already exists).

However, even though a country with such comprehensive scope and trigger criteria would in theory have all the relevant information (because the law would require it), the accuracy of the registered information as well as the enforcement of its registration is a completely different issue. For this reason, countries should undertake additional measures:

Country of residence as a structured data to be searched for or exchanged

While many countries have established public online beneficial ownership registries, search mechanisms may be limited. A user may need to know the exact name of an entity, or may only do a (free) search by an entity’s name or ID. Some countries also allow users to search for information by the beneficial owner’s name or ID. What is needed, however, is the capacity to search by country(ies) of residence. This way, a countries could search for information on all their residents across every country’s public beneficial ownership registry, rather than trying to search for every individual taxpayer to see if they are mentioned as a beneficial owner. Countries without public access to information should engage in automatic or spontaneous exchanges of this information with the country of residence of the beneficial owner.

Using offshore banking data to reveal offshore strategies

As proposed by our latest blog post on the leak from a bank in the Isle of Man, offshore banking data – especially what must be exchanged under the OECD’s Common Reporting Standard for automatic exchange of financial account information – could be a game changer for authorities. Data on offshore accounts, in addition to disclosing undeclared monies, could be used to reveal offshore secrecy strategies by determining the preferred secrecy jurisdiction used (or abused) by local taxpayers. Exchanged banking information could also reveal the types of structures typically chosen (a company, a trust, an Anstalt, etc) by residents of a particular country. For instance, based on a very small sample, the blog post described that 70 per cent of British beneficial owners used discretionary trusts from Cyprus to hold their bank accounts in the Isle of Man. A systematic analysis by authorities of the information received through automatic exchanges could reveal patterns that allow authorities to focus resources on obtaining data or establishing countermeasures in the secrecy jurisdictions favoured by their taxpayers.

Obtain client information en masse directly from enablers

One of the conclusions of the Pandora Papers is that despite the many leaks, enablers such as lawyers and trust and company service providers (TCSPs) keep helping criminals and high net worth individuals hide behind secretive structures to engage in illicit financial flows including tax abuse and corruption. The Financial Action Task Force (FATF) in Recommendation 22 requires Designated Non-Financial Businesses and Professions (DNFBP) such as lawyers, notaries, and accountants to conduct customer due diligence and be subject to anti-money laundering rule. However, not all countries require this from their service providers. Even for those that try to require it, lawyers are especially prone to resistance, often invoking professional secrecy based on attorney-client privilege, which can be abused to engage in illicit financial flows in general, as well as to avoid automatic exchange of banking information.

It’s ok to ask for client information from a law firm engaging in creating offshore structures to hide the beneficial owner:

“The clients of [the Firm] are of interest to the [IRS] because of the [Firm’s] services directed at concealing its clients’ beneficial ownership of offshore assets”.

It’s also ok for the purpose of identifying unknown clients who have also obtained the services:

“The IRS is pursuing an investigation to develop information about other unknown clients of [the Firm] who may have failed to comply with the internal revenue laws by availing themselves of similar services to those that [the Firm] provided to Taxpayer-1”

This is the data that the IRS asked for:

“Documents “reflecting any U.S. clients at whose request or on whose behalf [the Firm] ha[s] acquired or formed any foreign entity, opened or maintained any foreign financial account, or assisted in the conduct of any foreign financial transaction”; “[a]ll books, papers, records, or other data . . . concerning the provision of services to U.S. clients relating to setting up offshore financial accounts”; and “[a]ll books, papers, records, or other data . . . concerning the provision of services to U.S. clients relating to the acquisition, establishment or maintenance of offshore entities or structures of entities.”

Given that the identity of the disclosed client would not necessarily incriminate them, attorney-client privilege does not apply:

“This broad request, seeking relevant information about any U.S. client who engaged in any one of a number of the Firm’s services, is not the same as the Government’s knowing whether any Does engaged in allegedly fraudulent conduct, or the content of any specific legal advice the Firm gave particular Does, and then requesting their identities.”

Based on the success of this US case, all countries should not only follow and try similar lawsuits, but they should also establish by law that, just as banks and financial institutions are required to report the identities of their accounts holders and beneficial owners, law firms and corporate service providers in general should annually report the identities of all their clients for whom they set up (or help set up) legal vehicles. These regulations should focus especially on service providers who set up offshore structures (entities incorporated in a country different from the residence of the beneficial owner). In relation to this, the OECD already called on countries to obtain more beneficial ownership information by publishing Model Mandatory Disclosure Rules on Schemes to Hide the Beneficial Owner. Based on this framework, authorities trying to catch wrongdoers should be asking not just for the scheme details but also for the identities of those clients who may have used these schemes.

Establishing such a requirement by law may also undermine any attempt to invoke professional secrecy to oppose disclosing clients. Another US case, United States v. BDO Seidman, dealt with this subject matter. This case was based on US tax regulations requiring organisers of tax shelters to register tax shelters with the tax administration. The regulations also required organisers and sellers of such shelters to keep lists of their investors. (For background information on such rules, see indicator 13 in the Corporate Tax Haven Index which monitors such disclosure rules.) In the United States v. BDO Seidman case, the US tax administration (the IRS) requested the identities of the clients because “the IRS received information suggesting that BDO [the tax advice firm] was promoting potentially abusive tax shelters without complying with the registration and listing requirements for organizers and sellers of tax shelters”.

Although the clients (the “Does”) opposed the disclosure of their identities based on professional secrecy, the US Court of Appeals concluded:

“The Does have not established that a confidential communication will be disclosed if their identities are revealed… Disclosure of the identities of the Does will disclose to the IRS that the Does participated in one of the 20 types of tax shelters… It is less than clear, however, as to what motive, or other confidential communication of tax advice, can be inferred from that information alone”

This case shows why it is important to have a regulation requiring the disclosure of at least the schemes:

“At the time that the Does communicated their interest in participating in tax shelters that BDO organized or sold, the Does should have known that BDO was obligated to disclose the identity of clients engaging in such financial transactions. Because the Does cannot credibly argue that they expected that their participation in such transactions would not be disclosed, they cannot now establish that the documents responsive to the summonses, which do not contain any tax advice, reveal confidential communication.”

Conclusion

As explained here, no one is obliged to create companies or other structures. If individuals do not wish for their identities to be disclosed or leaked from service providers, they could operate in the economy or hold assets under their own name. Beneficial ownership transparency should be the least of the conditions under which individuals are permitted to set up legal vehicles which operate in the economy on their behalf, own assets, etc. This transparency requirement is especially relevant if these individuals will also benefit from limited liability. After three major leaks, it’s high time for countries to speed up the establishment of public beneficial ownership registries. In the meantime, they must start using existing exchanges of information to obtain and verify data. These leaks, however, also prove that more is needed. Not only should schemes to hide beneficial owners be disclosed to authorities by intermediaries as proposed by the OECD and the EU, but the identities of the clients potentially using these schemes should also be part of corporate service providers’ annual reporting to authorities.

Welcome to the 46th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

ضريبة تثير جدلا لدى صانعي المحتوى الرقمي في مصر

فرض ضريبة على مداخيل الانفلونسرز وصانعي محتوى السوشيال ميديا على يوتيوب وفايسيوك وانستاغرام وتيكتوك هو موضوع الحلقة #46 من بودكاست “الجباية ببساطة” في حوار مع الباحث في مجال الحقوق الاقتصادية والاجتماعية، إلهامي مرغني، حول الجدل الواسع الذي أثارته مصلحة الضرائب المصرية والتي تقدر مداخيل سنوية لهذا النشاط تفوق 500 ألف جنيه مصري للفرد.

كيف سيطبق هذا القرار؟ بأي آليات؟ وماهي تبعاته المتوقعة؟ أسئلة تجدون الإجابة عنها في البودكاست العربي “الجباية ببساطة “.

ضريبة تثير جدلا لدى صانعي المحتوى الرقمي في مصر

For this month’s episode #46 of Taxes Simply الجباية ببساطة we begin with the latest news relating to fiscal justice issues globally and in the Arab region. We then interview Elhamy Al Merghany, an Egyptian researcher and consultant on economic and social issues. Walid and Elhamy discuss the recent decision by the Egyptian government to impose taxes on social media content creators, also knows as “youtubers” or “vloggers”. Elhamy provides an analysis of the decision, the rationale behind it and how just it is when assessing fair taxation at large.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Afrique : Plus de transparence entre administrations fiscales pour lutter contre les flux financiers illicites, edition 32

Pour cette édition de votre podcast en français sur la justice fiscale et sociale produit par the Tax Justice Network, nous revenons sur les échanges qui ont porté sur la manière dont l’Echange Automatique d’Informations fiscales peut aider les administrations fiscales africaines à lutter contre les flux financiers illicites. Les discussions ont été menées dans le cadre de la Conférence Internationale sur la Transparence fiscale et les Flux Financiers Illicites en Afrique. Vous pouvez lire la déclaration finale de l’événement sous le ce lien.

Interviennent dans ce podcast :

Mustapha Ndajiwo: Founder and Executive Director, African Centre for Tax and Governance

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

The ICIJ has today revealed the biggest offshore leak since the Panama Papers in 2016. The Pandora Papers document 14 offshore professional service providers, and the way in which a mass of politicians, public officials and celebrities have utilised the offshore system to hide the true value of their wealth, and in some cases pay less tax than they owe.

These personal actions are shameful and will no doubt come under great scrutiny in the coming days, but it’s important that we don’t lose sight of one crucial fact: few of the individuals had any role in turning the global tax system into an ATM for the superrich. That honour goes to the professional enablers – banks, law firms and accountants – and the countries that facilitate them.

Every year, the world loses $427 billion in tax to tax havens – that’s a nurse’s yearly salary lost every second to the world’s wealthiest multinational corporations and individuals. It’s no coincidence that the small club of rich countries at the OECD who have held the pen on global tax rules for decades are the ones responsible for over two-thirds of the global tax abuse the world suffers every year.

A global tax system reprogrammed to prioritise the needs and wellbeing of people over the desires of the wealthiest can be our most powerful tool for tackling inequality, guaranteeing people’s human rights and protecting our democracies from the unchecked influence of the superrich. The first move towards a fairer global tax system is to take rule-setting out of the hands of a small club of rich countries and into the daylight of inclusive democracy at the UN.

Tax is about more than just money

The damage done by tax abuse goes well beyond the immediate loss of public revenues. Tax delivers the 4 Rs: revenue, redistribution, repricing and representation. When major companies and wealthy individuals cheat on their taxes, we all suffer from poorer public services. On top of that, governments are less able to redistribute and so we also suffer higher inequalities. When tax abuse defeats the repricing of public health threats such as tobacco consumption and carbon emission, we all suffer the result – and so will future generations.

But the fourth R may be the most important. The share of tax in government spending is one of very few things that is consistently associated with better governance and more effective political representation. Paying tax is a social act. When we pay tax it builds our stake in the decisions of government. That makes us more likely to hold government to account. When a government is more reliant financially on its own citizens, it functions better on our behalf. For example, when tax makes up a larger share of government spending overall, research shows that governments typically spend a higher share on public health; and that for a given level of spending on public health, the outcomes tend to be better and also more inclusive of the whole population.

So tax abuse by major companies and wealthy individuals doesn’t just leave governments with less money – it makes that money less likely to be well spent, for the benefit of all citizens. This is the real threat of tax havens from the Netherlands to Cayman and the rest of the UK spider’s web– that they rob us of effective states, and ultimately of our human rights.

Changing the way we change the rules

Ensuring that major companies and wealthy individuals pay their taxes is politically difficult – because of course these groups have disproportionate power. Major data leaks such as the Panama Papers have been crucial in raising public awareness of the scale of tax abuse, and the impunity of the perpetrators. That in turn has forced policy action, because ultimately politicians take steps not when they see the light, but when they feel the heat of public anger.

The public should not have to rely on leaks, though. We know who the major enablers of tax abuse are – from the major law firms, leading accountants and international banks who sell these services, to the OECD countries and their dependent territories that facilitate them. But we need consistent public data to ensure accountability. The High-Level FACTI Panel has adopted our proposal for a UN Centre for Monitoring Taxing Rights, which would collate, analyse and publish data on offshore financial accounts and on the country by country reporting of multinational companies. Our related proposals for indicators for the UN Sustainable Development Goals target to reduce illicit financial flows are also now being piloted by UN bodies in a range of countries around the world.

While the high-profile politicians and celebrities at the heart of Pandora Papers will be getting much of the spotlight over the coming days, it’s OECD member countries and their dependent territories that are responsible for the vast majority of the cross-border tax abuse that undermines human rights around the world.

Public outcry following the Panama Papers forced governments to adopt tax transparency measures but they stopped short of full transparency. The biggest blockers to transparency are the US, which the Pandora Papers confirms is the world’s biggest peddler of financial secrecy, and the UK, the leader of the world’s biggest tax haven network. We need full transparency so we can hold tax abusers accountable, especially when our politicians are among them.

US President Biden must match his own rhetoric on shutting down global illicit finance, and start with the biggest offender – his own country.

For far too long, the OECD itself has set the international tax rules that allow this. It’s time now to shift that role to a globally inclusive setting, and that’s why discussions about a UN Framework Convention on Tax are beginning to gather pace. That will be a key step to ensuring international tax rules and transparency that safeguard and promote human rights around the world.

O episódio #29 do É da sua conta mostra que há uma disputa no mundo hoje: recuperar a economia ou reestruturará-la e torná-la mais justa e sustentável? Um sistema tributário justo é aquele em que os que têm mais contribuem proporcionalmente com mais. Mas não é bem isso que está acontecendo: governos mundo afora encaixam as peças erradas nos lugares errados; fazem com que quem tem menos contribua proporcionalmente com mais.

Em Angola, o recém-criado Imposto sobre Valor Acrescentado (IVA) amplia as desigualdades. Em Portugal, o IVA começa a ser sentido pelas pequenas empresas. Ou seja, esse imposto sobre por exemplo, a compra de um celular, acaba pesando muito mais sobre os mais pobres. O Brasil corre o risco de seguir caminho parecido, mas pode também se espelhar na Colômbia, onde o povo saiu às ruas e não aceitou a reforma fiscal.

Ouça no É da sua conta #29:

Recuperar a economia ou reestruturar a economia?

Como fazer a economia funcionar para as pessoas e para o meio ambiente?

A posição ambígua do FMI sobre uma tributação mais justa

Experiências do Imposto de Valor Acrescentado (IVA) em Portugal e Angola

Os resultados dos protestos contra a reforma tributária que puniria as classes mais baixas na Colômbia

Temos que mudar a composição da carga para ela se torne um pouco mais progressiva.”

~ Fernando Gaiger, pesquisador do Instituto de Pesquisa em Economia Aplicada (Ipea)

Nós perdemos muita receita fiscal para países com outras regras de tributação e portanto, uma das propostas que nós temos são os acordos de dominação de dupla tributação, reabilitando os impostos de retenção, ou seja, tributar rendimentos de capital.”

~ José Gusmão, eurodeputado

Eu acho que a nossa aposta tem que estar na tributação empresarial, particularmente de multinacionais e também na tributação dos grandes multimilionários.”

~ Âurea Mouzinho, economista angolona

Penso que os frutos dos protestos serão vistos no próximo governo porque graças aos protestos, só serão aceitos a redução de benefícios tributários e aumento da tributação dos muito ricos”.

~Maria Fernanda Valdez, economista e coordenadora da Organização Não Governamental FES Colômbia.

Beneficial ownership transparency is a crucial strategy for tackling illicit financial flows. It involves identifying the individuals (natural persons) who ultimately own, control, or benefit from a legal vehicle like a company, trust or partnership. Individuals engaging in illegal or illegitimate activities, however, find it quite easy to hide themselves behind legal vehicles, which are set up in tax havens (or as we prefer to call them, secrecy jurisdictions).

Although many countries are approving laws to establish beneficial ownership registries (our report on the State of play of play of beneficial ownership registration counted more than 80 countries by April 2020), many challenges remain. Those challenges include difficulty in the verification of registered ownership information as well as the enforcement of registration requirements. Additionally, however, most beneficial ownership registration laws are flawed from the onset by requiring transparency just for local entities. This means that countries have no guaranteed access to beneficial ownership information on foreign entities operating in their territories nor on the foreign entities operating abroad but controlled or owned by local individuals.

Given that banks must also collect beneficial ownership information as part of their due diligence process whenever a customer opens an account, they can help verify beneficial ownership information contained in central registries. If a country has failed to establish a beneficial ownership registry, banks may be the only source of beneficial ownership data. However, authorities are usually able to ask for this information from local banks only, not foreign ones.

The sharing of information held by foreign banks would be crucial, not just for uncovering the location of money held offshore, but also for identifying the offshore strategies used by local individuals to hold this money. Authorities could then determine whether individuals are holding their foreign assets in their own name or through offshore entities. By identifying the most commonly used secrecy jurisdictions and the preferred types of legal vehicles (eg company limited by shares, discretionary trust, etc), authorities would have a better understanding of where to focus their resources in order to find secret assets and income held offshore.

Unfortunately, the current system for the automatic exchange of bank account information, based on the OECD’s Common Reporting Standard (CRS), provides limited data. We know, however, that this data is already collected by banks. It could be disclosed for analysis, as we have been calling for since 2017, in a template such as this.

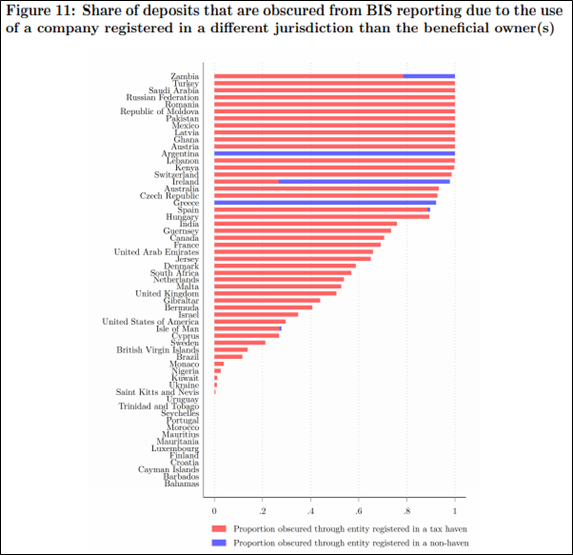

Our template offers a theoretical explanation of how to analyse and utilise shared international banking data, but at the time of publication in 2017, we didn’t have any examples to demonstrate with. That all changed when economist Matt Collin at the Brookings Institution published a brilliant paper this year titled “What lies beneath: Evidence from leaked account data on how elites use offshore banking”. Collin uses a leak from a private bank on the Isle of Man to analyse several interesting patterns regarding offshore financial behaviour. One of these patterns that caught our attention in relation to beneficial ownership transparency is illustrated below in Figure 11, as it is labelled in the paper.

This table shows that the Bank for International Settlements’ (BIS) statistics on foreign deposits by country of origin may be misleading due to data being reported at the account holder level instead of the beneficial ownership level. In other words, if Joanne from France set up a shell company in the Cayman Islands (with no operations, no office, no employees or equipment), and holds a bank account in Luxembourg through this shell company, the Bank for International Settlements’ statistics will report the Luxembourg account as belonging to a party in the Cayman Islands, even though it really belongs to Joanne in France. (The Bank for International Settlements’ statistics for many countries don’t even differentiate between accounts held by individuals or entities– all are reported together).

While the issue of misleading statistics is very relevant, our interest was to know more about the entities used to hold the bank accounts: where they were incorporated (in which secrecy jurisdiction) and their type (a company, trust, partnership, etc).

It was extremely helpful of Matt Collin to share statistical data from the leak with us. No names or account numbers were shared, only the number of accounts based on the residence of the beneficial owner and other details.

Results

Before we go into the findings, some caveats must be mentioned. First, this is a leaked database from a small private bank, which doesn’t include all the details the bank may have on each customer, and which may involve errors (eg if the bank recorded the information incorrectly or if the customer declared wrong information). The data contained in the leak is obviously not representative of the whole world. Our point, however, is not to draw conclusions about global offshore strategies, but to show what could be done – and how – if this analysis were conducted across the whole of the banking data that is being exchanged under the OECD’s automatic exchange system.

Second, our focus is on how the Isle of Man is used by beneficial owners from elsewhere in the world in their offshore strategies, so first we excluded all beneficial owners from the Isle of Man. In addition, we excluded all accounts with a beneficial owner using an entity from their country of residence to hold a bank account in the Isle of Man. In other words if Joanne from the France held her bank account in the Isle of Man through a French company, this was excluded because both Jane and the company are from the same country: France (in this case, Joanne didn’t go offshore to set up a company). Instead, if she held the bank account in the Isle of Man through a company in Luxembourg, this was considered. In essence, we removed from the sample cases where the beneficial owner and the company are from the same country.

Third, given the potential bias for having a local entity in the same place where you hold your offshore bank account (this may be a package offered whenever you set up an offshore company), we excluded entities from the Isle of Man, which represented 67 per cent of all the offshore cases. If Joanne from France held the bank account in the Isle of Man through an Isle of Man entity, this was excluded. The strong assumption here is that if the bank account was not in the Isle of Man, then we would expect a much lower percentage of Isle of Man entities. We may be wrong, however. It may be case that the Isle of Man is indeed the preferred secrecy jurisdiction of the world to set up an offshore entity, regardless of where the money will be held, either in the island or anywhere else. In essence, we removed from the sample cases where an entity from the Isle of Man was used to hold the account in the Isle of Man.

Finally, we disregarded cases where the entity was “unknown” or had an invalid value. To sum up, this is what we removed from the sample on “offshore strategies”:

Beneficial owners from the Isle of Man, because the bank account was in the Isle of Man so it’s not an offshore strategy

Beneficial owners who use an entity from their country of residence (a French beneficial owner using a French company) to hold the bank account in the Isle of Man, because again this is not an offshore entity

Beneficial owners (from any country) using an Isle of Man entity to hold the Isle of Man bank account (here we assume there is a bias in favour of using an entity from the same country as the bank account, so this would overstate the relevance of the Isle of Man as the preferred tax haven to set up entities)

Unknown or invalid values

This is what we found:

The sample involved 249 bank accounts indirectly held by beneficial owners from 36 countries. These owners held their accounts not through their own names, but through offshore entities. It’s possible that the number of countries where the beneficial owners are apparently resident may be inaccurate due to several of these countries themselves being secrecy jurisdictions: Belize, Cayman Islands, Cyprus, Gibraltar, Guernsey, Hong Kong, Jersey, Seychelles, Singapore, Switzerland and the UAE. On the one hand, it could be the case that rich individuals from these secrecy jurisdictions (eg the Cayman Islands) are holding their accounts in the Isle of Man, in which case there are no inaccuracies and the 36 countries of residence identified among the beneficial owners are genuine. On the other hand, the more likely case is that the account holder lied on their documents and (wrongly) declared a nominee from the Cayman Islands as the beneficial owner. In this case, we have no clue as to the real residence of the beneficial owner. A third alternative explanation is that this is just a mistake by the bank when recording the data.

The beneficial owners from these 36 countries used entities from 17 offshore jurisdictions: 45 per cent from Cyprus, 18 per cent from the British Virgin Islands, 9 per cent from the UK, 7 per cent from St. Kitts and Nevis, 4 per cent from Seychelles, and another 4 per cent from Switzerland.

The most common types of legal vehicle used to hold the 249 accounts in the data sample included private companies limited by shares (45 per cent) and discretionary trusts (35 per cent). Most of the private companies limited by shares were from the British Virgin Islands, followed by Cyprus and the UK. Most discretionary trusts were from Cyprus followed by St. Kitts and Nevis. As described in our paper Trusts: Weapons of Mass Injustice?, Nevis offers one of the most abusive types of offshore trusts.)

If we had had a large enough sample, these could have been valid global conclusions. For example, it would be possible to conclude that Cyprus and the British Virgin Islands are the preferred secrecy jurisdictions in which to hold bank accounts. In turn ,country authorities would know to be especially wary of private companies from the British Virgin Islands, Cyprus and the UK, as well as discretionary trusts from Cyprus and St. Kitts and Nevis. Country authorities could also learn which secrecy jurisdictions and types of entities are most often utilised by their local taxpayers to hide their wealth.

This all goes to show the leap in tax transparency that can be achieved, and the better equipped country authorities can be to tackle global tax abuses, if the data collected under automatic exchange of bank account information was publicly disclosed and properly analysed using our template.

Here are some of the more detailed findings we obtained by applying our analysis template to the small data sample (the number in parenthesis refers to the number of beneficial owners in the database):

In Africa, beneficial owners from Ghana (4), Nigeria (1) and Zimbabwe (1) used offshore companies from the British Virgin Islands, Seychelles and the UK respectively.

In Latin America, beneficial owners from Argentina (1), Brazil (1), Costa Rica (2), Mexico (1) and Paraguay (1) mostly used offshore companies from other countries in their region with a history of being tax havens: Uruguay, the British Virgin Islands, Panama and Belize respectively.

In Southeast Asia, beneficial owners from India (4) and the Philippines (3) used offshore companies from the British Virgin Islands, Malta and Jersey respectively.

In the EU, the choice of tax havens and types of entities is more diverse. Beneficial owners from Czechia (6), France (1), Greece (1), Hungary (1), Latvia (1), Spain (6) and Sweden (6), mostly used offshore companies from the UK, the British Virgin Islands, Cyprus, Belize and Seychelles. However, beneficial owners from Latvia (1) and Sweden (1) also used discretionary trusts from St. Kitts and Nevis. Seventy per cent of beneficial owners from the UK used offshore trusts to hold their accounts, mostly via Cyprus, St Kitts and Nevis and the Cayman Islands. Oddly enough, the leaked data shows some UK beneficial owners using trusts from Switzerland to hold their bank accounts despite it not being possible to create a trust under Swiss law. It may be that in all these cases, the data refers to the location of the trustee, rather than the governing law of the trust.

To stress the relevance of this data one last time, consider the following. If Indian authorities had access to this data regarding all of their residents’ offshore holdings (not just for the 4 Indians mentioned in the leaked database), they would know which secrecy jurisdictions to prioritise safeguarding against, either by signing agreements to exchange information, making requests for information, or including those jurisdictions in their secrecy jurisdiction list.

Conclusion

In conclusion, banking data can provide very useful insights, if properly analysed, to reveal offshore strategies. This in turn would indicate where authorities should focus their efforts towards financial transparency and curbing tax abuse. Based on the example of the Isle of Man banking leak, the OECD’s automatic exchange of information system could become a great source, provided it broadens the scope of information exchanged. For more background information on beneficial ownership and automatic exchange of information, and an explanation on how both systems can be improved to reveal offshore strategies, please see our brief via the button below.

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

In this episode, Naomi Fowler explores degrowth and how we liberate ourselves from ‘growthism’ with economic anthropologist Jason Hickel. (You can listen to Part 2 of that conversation here.)

Plus: there can be no liberation without tackling monopoly power, or the role of finance sectors and States, investing in death and destruction across the world.

The transcript is available here (some is automated and may not be 100% accurate)

Hosted and produced by the Tax Justice Network’s Naomi Fowler.

Degrowth: liberation from ‘growthism’ #114

“We should seek to organise the economy around meeting human needs rather than around servicing elite consumption and capital accumulation. And that requires a pretty dramatic shift from sort of the status quo of our economic system.”

~ Jason Hickel

There’s no way we can build local resilience and sustainable economies when faced with monopoly players who can dominate markets and use their financial power to over-ride democracy through their lobbying.”

Taxation is really easy to understand, right? Well, no, not really. In fact it can all seem a bit complicated. The way governments design and implement tax policies has a huge impact on how fair and equal our societies are, though, and just taxation can make the difference between success and failure when it comes to a whole range of issues, including climate crisis, sustainable development and tackling gender and racial inequalities. That’s why it’s so very important for everyone who cares about our world – and the people in it – to learn about tax justice.

Over the next few weeks the Tax Justice Network will be rolling out a new series of ‘Tax Justice 101’ videos, in which we’ll explain the ways fair taxation is linked to many of the most pressing issues of our time. The first of these – The 4 ‘R’s of Taxation – has just gone live, and sets out the four fundamental functions that make just taxation crucial to building a just society.

What’s tax for? The 4 ‘R’s of tax

Every Monday for the next ten weeks we’ll be sharing a new video, with each one taking on a key theme on the tax justice agenda and explaining it in an easily understandable way. Next week we’ll be looking at the ‘ABCs of Tax Transparency’, and after that we’ll get to grips with a host of other issues such as why taxation is crucial to human rights, the ‘race to the bottom’ in corporate taxation, and why tax is better than international aid or debt for developing countries. We’ll also be asking some thorny questions about who calls the shots in international taxation issues and whether ‘tax avoidance’ is actually legal (as so many tax avoiders claim!).

Join us! Every Monday you’ll be able to find a new video on our Facebook, Twitter and Youtube channels, and also on our website’s video page. You’ll be a tax justice guru in no time!

La COVID-19 survenue en 2020 a plus que jamais rappelé l’impérieuse nécessité qu’il y a pour les pays, de garantir un accès à des systèmes de santé publique dotés de ressources suffisantes, et accessible de manière équitable pour tous. Aussi, elle a compromis la capacité des pays à poursuivre leurs efforts visant à assurer un accès pour tous à une éducation de qualité, sur un pied d’égalité, surtout pour ceux qui ont le moins de ressources financières. Toutefois, cette pandémie n’a fait qu’aggraver une situation qui nécessitait déjà des améliorations. On retrouve ainsi des structures économiques héritées de la colonisation, et qui profitent toujours aux anciennes métropoles, et surtout une pratique d’abus et d’évasions fiscales par des multinationales qui cherchent à maximiser leurs profits.

En Afrique subsaharienne où on compte 27 pays, la moyenne des dépenses publiques en éducation avant la pandémie était de 4,3% du Produit Intérieur Brut selon les statistiques disponibles sur le site internet de la Banque Mondiale. On pourrait penser que c’est presqu’autant dans l’Union Européenne, où les pays ont collectivement dépensé 4,7% de leurs Produit Intérieur Brut pour l’éducation. Mais en valeur absolue, les dépenses de l’UE pour le secteur éducatif représentaient jusqu’à 654 milliards €, contre seulement 62,3 milliards € pour les gouvernements de la région. Dans son édition 2020 des perspectives économiques pour l’Afrique la Banque Africaine de Développement revient sur ce qu’elle appelle l’inefficience de financement de l’éducation sur le continent. Dans certains des pays (Soudan, Ouganda, Libéria ou encore Sierra Leone), le nombre de personnes vivant avec peu de ressources financières est élevé. Pourtant, les ménages selon des récentes informations, y contribuent encore à plus de 60% des dépenses d’éducation. Or parfois, il faut entre 10 et 12 ans, pour qu’un enfant de 6 ans achève une formation de primaire et de secondaire, ce qui revient cher pour les familles.

Des injustices sont aussi perceptibles en matière de santé, tant sur le plan de l’accès aux soins de santé, que de la disponibilité d’un cadre adéquat pour une bonne qualité de vie, comme l’accès l’eau potable, une bonne hygiène ou encore une nutrition saine et de bonne qualité. Avec la Covid-19, on a vu émerger le risque que représentent les pandémies mondiales pour les pays faibles, tant sur le plan économique, que social. Selon le Global Health Security Index, plusieurs pays africains se retrouvent dans la catégorie de ceux qui sont les moins préparés à faire face à d’éventuelles pandémies. Les données sur l’éducation et la santé, ne prennent pas en compte les disparités entre les zones urbaines et les zones rurales enclavées et reculées. Aussi, ces données ne reflètent pas suffisamment la plus grande vulnérabilité qui existe chez les femmes. Ces dernières sont les plus susceptibles de solliciter des soins de santé en raison de la maternité. Elles ont le plus besoin d’eau potable pour les enfants dont elles prennent soin, et sont aussi les moins privilégiées lorsqu’il faut choisir entre le financement des études du garçon ou de la fille.

Dans les discussions multilatérales, les gouvernements africains évoquent l’absence de moyens financiers pour faire face à leurs engagements en matière des droits de l’homme. Les capacités d’intervention des gouvernements demeurent assez modestes en Afrique subsaharienne et les attentes des populations sont grandes. En plus de la précarité, l’Afrique subsaharienne doit faire face à des défis de sécurité et de plus en plus des catastrophes naturelles comme des sécheresses, des inondations, ou des feux de brousses. Mais de nombreuses recherches ont aussi démontré que le continent laisse échapper des opportunités pour adresser ces défis, faute de résoudre le problème des pertes de ressources budgétaires. Dans une étude publiée en 2017, le Curtis Research a estimé sur la base de sa méthodologie, que les pertes de revenus pour les administrations africaines s’élevaient à 182 milliards $. A cette période-là, cela représentait 400% de l’aide international au développement et autant que les dépenses combinées de la région dans les secteurs de la santé publique et de l’éducation. Dans une autre étude disponible depuis en 2018, les chercheurs Léonce Ndikumana et James K. Boyce ont démontré, que 30 pays d’Afrique subsaharienne ont perdu un total de 1 400 milliards $ sur 45 ans, en raison de la fuite des capitaux. Ce montant permettrait de tripler les dépenses d’éducation sur une période de 10 ans.

Dans son premier rapport sur l’Etat de la justice fiscale dans le monde publié en octobre 2020, Tax Justice Network a estimé que l’Afrique dans son ensemble perdait l’équivalent de 23,24 milliards $ de revenus fiscaux par an du fait de l’évasion fiscale des entreprises, majoritairement des multinationales installées sur le continent. A cela s’ajoutent 2,5 milliards $ perdus du fait de la fraude fiscale par les personnes fortunées, pour un total de 25,7 milliards $US de pertes fiscales estimées dans la région. L’étude a évalué que cette somme représenterait le 52% des budgets consacrés à la santé publique par les pays de la Région. Cela aurait pu permettre de créer 10,13 millions de postes supplémentaires d’infirmières. Alternativement, ces sommes représentent jusqu’à 29% des budgets d’éducation des gouvernements africains.

« Le COVID-19 a dévoilé les terribles conséquences d’un système fiscal international programmé pour faire primer les intérêts des sociétés et individus les plus fortunés sur les besoins de l’ensemble de la société. Il a mis au grand jour les multiples inégalités qui entachent nos sociétés et dans quelle mesure la destinée des personnes les plus marginalisées continue de dépendre de structures inéquitables, qui conservent un élitisme politique et l’héritage du passé colonial », on lire dans le document.

Aussi, l’inefficience dans la collecte des ressources financières par les administrations fiscales en Afrique, renchéri le coût de la vie pour des personnes qui ont déjà des moyens financiers limités. Comme on l’a évoqué plus haut, la part des dépenses des ménages pour des questions de santé publique et d’éducation est plus élevé sur le continent que dans d’autres régions du monde, selon des indicateurs de la Banque Mondiale. Sur le faible revenu qui reste pour la consommation, les gouvernements de la région qui ne parviennent pas à collecter efficacement les impôts sur les profits des entreprises et riches individus, prélèvent encore des taxes sur la valeur ajoutée qui dans certains pays atteignent 20%. Enfin, les inégalités d’accès au travail rémunéré rendent les choses encore plus difficiles pour les femmes. Mais plus que la santé publique et l’éducation, ce sont des avancées en matière de justice sociale au sens large qui pourraient apporter le plus de changements en Afrique. Des recherches menées en 2013 sur 31 pays africains par les professeurs Arne Bigsten et Thushaynthan Baskaran concluait déjà qu’il existait une corrélation entre la capacité des gouvernements africains à mobiliser des ressources fiscales et l’atteinte des objectifs de réduction de la corruption et d’amélioration du fonctionnement du système démocratique. Mais il y a aussi une responsabilité des pays dits développés. Dans le cadre du processus de décolonisation, ces pays ont mis en place un cadre économique extractif, qui leur permettait de tirer profits des pays nouvellement devenus indépendants. Aujourd’hui, Ils abritent l’essentiel des juridictions opaques, qui permettent aux multinationales d’y dissimuler des revenus imposables, dont ceux en provenance d’Afrique. En même temps, ces pays compromettent les chances d’une véritable fiscalité internationale qui soit équitable et juste pour tout le monde, en assurant le contrôle des organisations les plus influentes en matière de politique économique et fiscale, comme le G20 ou l’OCDE

Les critiques à la justice fiscale ne manquent pas de dire que mobiliser des ressources ne suffit pas à faire reculer l’injustice sociale. Liz Nelson, experte sur les questions de justice fiscale et droits de l’homme chez Tax Justice Network et auteur d’un important rapport sur la justice fiscale et les droits de l’homme, a une réponse appropriée à cette manière de voir. « L’utilisation des ressources est une chose très importante et non-négligeable. Sans vouloir donner de leçons à qui que ce soit, nous pensons, qu’aucun gouvernement dans le monde qu’il soit d’un pays riche ou d’un pays pauvre, ne doit manquer l’opportunité de se donner les moyens de répondre aux attentes sociales de ses populations, et le Covid est venu montrer que personne n’est à l’abri. Aussi il y a de la part des gouvernements du monde un engagement presque catégorique et obligatoire, pour honorer aux promesses des objectifs de développement durable et il faut pouvoir financer leurs atteintes, pour toutes les catégories de citoyen », a-t-elle fait savoir. Il est urgent d’intervenir aujourd’hui. Aux défis historiques en matière de droits de l’homme, se superposent de nouveaux enjeux qui prennent la forme des changements climatiques et d’épuisement des ressources essentielles à la survie.

Plus que jamais, les trois piliers d’une meilleure justice fiscale internationale défendues par Tax Justice Network s’imposent, pour réduire l’opacité générale qui favorise les inégalités et l’iniquité des opportunités dans le monde. Il s’agit de l’échange automatique d’informations, des registres des bénéficiaires effectifs et de la déclaration publique des comptes financiers pays par pays pour les multinationales. Bien au-delà de l’Afrique, les inégalités sociales dont la fraude, l’évasion et l’évitement des impôts constituent des causes majeures entre autres, continuent de gagner du terrain. Cela justifie de se mobiliser toujours d’avantage au niveau international, pour une plus grande justice fiscale, mais aussi pour un meilleur accès à l’éducation pour de millions de personnes, et pour une protection sanitaire plus efficace.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita.

En este programa:

¿Habrá nuevas reglas impositivas para las grandes multinacionales?

Las cortes internacionales que deciden los litigios entre multinacionales y los estados

La banca británica, Estados Unidos y el tráfico de drogas

y América Latina tiene más del 80% del litio mundial, pero ¿puede dar el salto a la producción con valor agregado?

Welcome to the 45th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

الجباية ببساطة #45 – لبنان ما بعد الإفلاس