Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita. En este programa con Marcelo Justo and Marta Nuñez:

La victoria de Lula en Brasil y América Latina.

El fraude fiscal de una multinacional en Argentina.

Bolivia o cómo conseguir la seguridad alimentaria en épocas de crisis y pandemia

Las Naciones Unidas buscan reformar el sistema impositivo global

The Red Sea resort of Sharm El Sheikh in Egypt is the focal point of the world’s attention this week as political leaders from all over the planet come together for COP27, the 27th United Nations climate change conference.

This latest convening comes after a series of reports giving dire warnings about the international community’s continuing failure to rise to the challenge of preventing catastrophic temperature rise. What has become viscerally clear is that climate change is no longer a distant disaster somewhere in the future. The devastating human and environmental impacts of climate change are already upon us, and the only question that now remains is just how bad it will get and how effectively humanity will be able to navigate the storm.

Given that many of the most pernicious impacts of climate change, in particular for the Global South, are now ‘baked in’, the attention of climate justice activists has shifted away from the language of mitigation and adaptation and towards the agenda of ‘loss and damage’.

The issue of loss and damage – which refers to impacts of climate change not avoided by mitigation, adaptation, or other measures – is recognised in Article 8 of the Paris Agreement, which declares that signatory countries “recognise the importance of averting, minimising and addressing loss and damage associated with the adverse effects of climate change”. Thus far, almost all developed nations – with the notable exceptions of Scotland and Denmark – have refused to make meaningful financial commitments to compensate for loss and damage, despite the fact they are precisely the ones most responsible for the historic greenhouse gas emissions that have caused the crisis.

Together with the Global Initiative on Economic, Social and Cultural Rights, the Tax Justice Network is working to develop reforms to the governance of international taxation. These must be implemented in order to deliver a just transition and ensure that poorer nations in particular have the resources necessary to navigate the years ahead. As we demonstrate in a new white paper which is being presented at the COP27 meeting, these reforms are crucial to minimise the human suffering stemming from climate change.

Proposals to create a new financial facility to address loss and damage were scuppered at the last UN climate conference in Glasgow, and there is still no formal international mechanism for addressing the harms caused by climate change to the world’s poorest populations. Yet this accelerating crisis should be considered a matter of racial, gender and post-colonial justice: it is well documented that women and girls, and people of colour in former colonial states, are disproportionately impacted by climate change. A global economic system anchored in the financial and resource extraction of these countries by the Global North has caused the climate crisis, whilst also rendering countries unable to cope with the environmental convulsions they are experiencing.

Moreover, these reforms to the governance of international taxation should be considered a human rights obligation, for wealthy and poorer nations alike. This has increasingly been recognised by the United Nations human rights system. In 2019, five human rights treaty bodies issued a declaration to remind governments that human rights obligations require that they “co-operate in good faith in the establishment of global responses addressing climate-related loss and damage suffered by the most vulnerable countries. More recently the UN Special Rapporteur on Climate Change and Human Rights, following a submission from the Tax Justice Network and the Global Initiative, called for the General Assembly to “explore legal options to close down tax havens as a means of freeing up taxation revenue for loss and damage”.

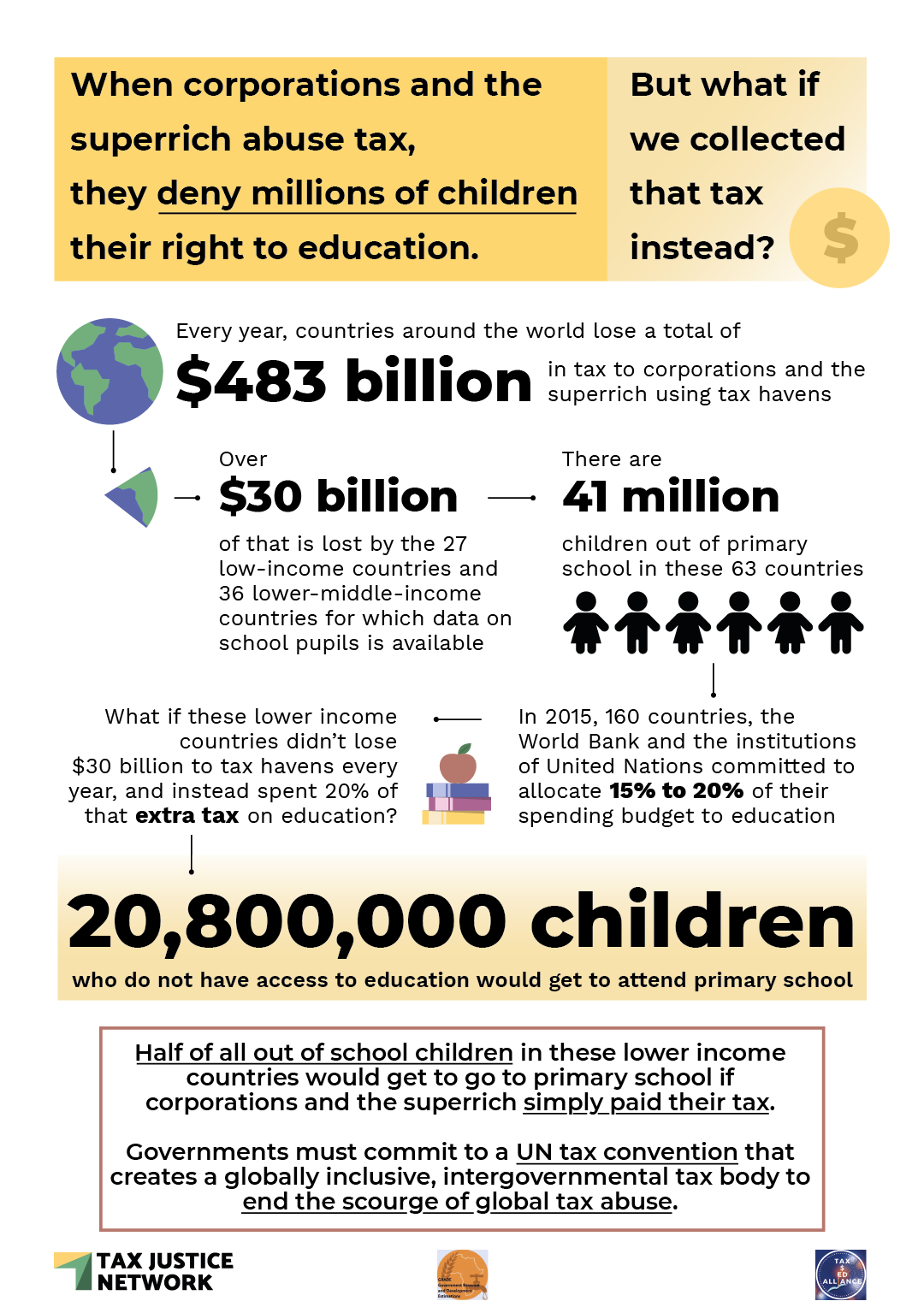

Although a radical reconstruction of the architecture of international taxation will not in itself be enough to provide the redress that is now required, it will be a crucial central pillar of any effort to deliver a just climate transition. As things currently stand, countries lost an estimated US$ 483 billion in tax each year as a result of global tax abuse committed by multinational corporations and wealthy individuals. Meanwhile, somewhere between US$ 21 trillion and US$ 32 trillion is hidden from tax authorities offshore, and the ease with which multinational corporations can shift their profits into tax havens and away from the location of actual economic activity has fed a race to the bottom on corporate taxation. Indeed, average corporate tax rates have fallen from 49% in 1985 to just 23% in 2019.

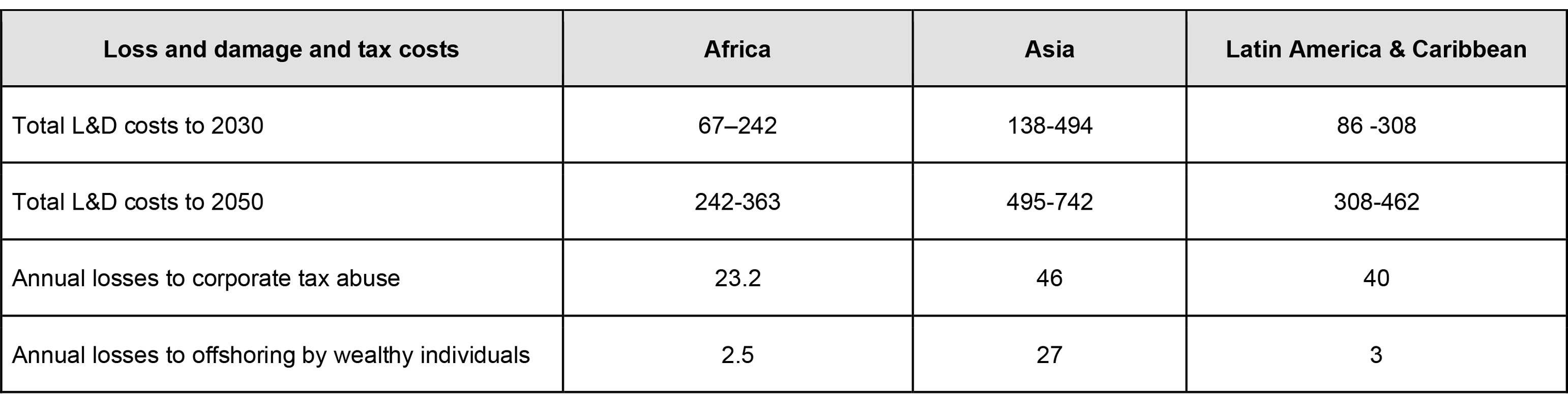

The table below, drawing on data from the Tax Justice Network’s State of Tax Justice report and the landmark 2019 study into loss and damage by Markandya and González-Eguino, illustrates the stark financial cliff the Global South is facing as the climate catastrophe gathers momentum. This grim reality gives increased urgency to the need to reform the international tax system in order to stop the pillage of government coffers everywhere.

Loss and damage and tax costs for Africa, Asia, and Latin America & Caribbean (billion USD)

Data from the State of Tax Justice report 2021 and calculations based on Markandya, A., González-Eguino, M. (2019), ‘Integrated Assessment for Identifying Climate Finance Needs for Loss and Damage: A Critical Review’, in Mechler, R., et al (eds), ‘Loss and Damage from Climate Change: Climate Risk Management, Policy and Governance’, Springer.

Among the measures needed to achieve this are a meaningful minimum tax on corporate profits, so as to halt the ‘race to the bottom’, and the creation of a United Nations tax convention to replace the century-old system of bilateral tax treaties that place weaker nations at the mercy of more powerful states. As a necessary precondition to the latter, negotiations on international tax cooperation must be moved away from the Organisation for Economic Cooperation and Development, which has not kept its promise to include the voices of developing nations, to the UN, where all countries can meet on a more equal footing.

The climate justice and tax justice movements are not separate, or even parallel, issues. They are so intimately enmeshed that our collective success or failure in addressing each of them will be integral to determining outcomes for the other. As two highly-technical spheres, both of which require deep and determined international collaboration, bridging the gap between these two areas is no easy task. It is not hyperbole to say that the future of humanity hangs in the balance.

Welcome to the 59th edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

في الحلقة #59 من بودكاست الجباية ببساطة، استضاف وليد بن رحومة، السيد محب عبود وكيل نقابة المعلمين المستقلة لنقاش وضعية المنظومة التعليمية في مصر وما تعانيه من وهن. وتطرق الحوار لسبل إصلاح وتطوير التعليم بعيدا عن التمييز الطبقي. في الحلقة نعود على توصل مصر وتونس لإتفاق مع صندوق النقد الدولي وإرتفاع الدين العام في الاردن.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Dans cette édition de votre podcast en français produit par Tax Justice Network, nous revenons sur plusieurs thématiques qui ont marqué l’actualité fiscale en rapport aux pays du sud. A l’OCDE, on intensifie les discussions pour parvenir à un document définitif de l’accord fiscal multilatéral qui a été validé en fin 2021. Selon des experts de l’ONG South Center Tax Initiative qui est basée à Genève en Suisse, de nombreux ajustements méritent encore d’être effectués pour prendre en compte les intérêts des pays en développement. Fin octobre 2021, le Ministère camerounais des finances a organisé une rencontre avec la société civile pour discuter de la réforme des finances publiques, notre ONG partenaire le CRADEC a profité de l’occasion pour élaborer un solide plaidoyer des réformes, sur la base des instruments d’analyse fournis par Tax Justice Network. Enfin, l’invité de cette édition est Seydi Demba, le Coordonnateur pour l’Afrique de l’Ouest de l’organisation internationale Publiez Ce Que Vous Payez.

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

Concentrated control of large corporations has created vast fortunes over the last four decades and fueled the drive towards market domination. Here Niko Lusiani and Emily DiVito consider how the tax system could be used to shift incentives and broaden ownership beyond a handful of latterday robber barons.

Today large incumbent firms dominate industries across the United States – from meat to medicines, from finance to tech, from retail to telecoms. This historic turn away from a dynamic multi-player business sector to a stagnant private sector stunted under the shadow of a few mega-oligopolies has real consequences for people.

Corporate concentration extracts wealth from consumers and communities and directs it to entrenched corporate shareholders and executives. Excess market power raises prices for consumers, lowers wages and worsens jobs for workers, inhibits business dynamism, compromises supply chains, reduces the supply of goods, and exacerbates racial wealth inequality both for individual households and communities as a whole. Perhaps sensing all of this, the US public has more negative sentiment towards big business than at any other point in the last five decades.

While policy thinkers and makers have rightly focused on strengthening antitrust law and competition mechanisms – as well as on building out public options to compete with dominant private firms – tax policy remains overlooked both as a driver of current levels of market concentration, and as a possible tool to remedy this problem – as this special issue of Tax and Monopoly Focus illustrates. Complementing the corporate focus of other contributions, our contribution here explores what effect a wealth tax on individual US billionaires might have on excessive market power.

A wealth tax is, as the name suggests, a tax – thus far proposed as around 1–2% – on the underlying value of the stock of the assets that make up the vast majority of multimillionaire and billionaires’ holdings, including real estate, cash, stocks and bonds, and certain business assets. Seen as fundamentally fair and highly-targeted, the idea of a wealth tax generates broad public support across the political spectrum, and its popularity has helped garner momentum for progress on various ways to tax the ultrawealthy – perhaps best evidenced by how close a 2021 proposal by Chairman of the US Senate Finance Committee for a Billionaire’s Income Tax came to legislative passage. Distinct from a 1–2% tax on the stock of wealth, this ‘mark-to-market’ (M2M) proposal taxes the income that accumulates from wealth by levying an annual tax on the change in the value of a high-net worth individual’s stock, dividends, and other tradable assets – assets that largely go untaxed in the current US system until a realisation event, like a sale, occurs.

Both a wealth tax and a M2M tax are highly-progressive and the uber-wealthy, who escape paying their fair share under the status quo, would exclusively be the subjects of these taxes. Both of these sorts of wealth taxes are largely conceived with the main aim of redistribution and raising revenue to fund broad scale public investments and programs. This revenue-forward rationale has limited discussion about how a wealth tax would shape markets – and in particular the business decisions of those wealthy individuals subject to the tax.

Only America’s top billionaires would be paying these sorts of wealth tax. So, let’s start with some stylised facts on who these individuals are. Focusing for a moment just on the top 10 wealthiest Americans, the list contains familiar names: the titans of the information age – often simultaneously the founders, CEOs and Board Chairs of some of the globe’s most profitable firms topping the stock markets. These include Amazon, Microsoft, Facebook, Berkshire Hathaway, Google, Tesla. These are (almost universally) men who sit at the top of the corporate food chain, and are compensated accordingly. Together, these 10 individuals own over $1 trillion in wealth. Importantly here, their wealth is primarily held in the stock of the companies they control. According to our estimates using the Bloomberg Billionaire Index, over 60% of the wealth of the top 10 American billionaires is held in the equity shares of the companies they control. If we zoom out to the top 50 American billionaires, over 75% of their combined $2.2 trillion in wealth is equity held in corporations that these individuals sit at the top of.

But even that average belies the degree to which most of these people functionally control their businesses, and the wealth that these businesses create. Warren Buffet – Board Chair, CEO and the largest shareholder in Berkshire Hathaway – holds 99% of his wealth in his company’s stock. Mark Zuckerberg – who reigns over Meta – holds 95% of his wealth in company stock. And Jeff Bezos – no longer CEO but still Board Chair at Amazon – holds 83% of his wealth in Amazon equity, and a very powerful 10% controlling interest in the company as a whole. (An individual owning over 5% of shares in a firm is generally considered a ‘blockholder,’ with unique effective power over corporate decisionmaking.) Even Bill Gates – whose wealth is relatively more diversified and holds much less effective control over Microsoft – became one of the top wealthiest people in the US through his shares in the company while he was at its apex.

This is all to say that the central source of wealth for America’s top billionaires is the growth in the value of their corporate equity – which, not coincidentally, is in monopolistic firms facing intense antitrust scrutiny. In the US today, so it seems, control and beneficial ownership of the most dominant firms have once again fused in the form of manager-blockholders who are simultaneously CEO, Board Chair and largest shareholder.

It’s also perhaps not a coincidence that the managerial power of these corporate leaders (and the economic power and wealth that such managerial positions have produced) is correlated with the growth in the market power of the firms they control. While a number of factors contribute to stock appreciation, the most fundamental driver is real and expected earnings: that is, profitability projections. Companies with more market power have more opportunity to increase profitability into the future, and thus are valued higher by financial analysts and stock pickers. It should be little surprise then that the wealthiest billionaires derive their fortunes from their control over precisely the companies able to charge monopoly rents and whose business models rely on building ‘moats’ against competition by killing or swallowing potential challengers.

All else being equal, the larger the ownership stake of an individual Billionaire in their own company, the greater incentive they would have to increase firm value by capturing market share. Personal financial motives then align with the means of controlling the firm to present the opportunity to consolidate market power. That is, the personal financial motivations of America’s top billionaires come together with their means as central corporate decision-makers (as both ‘agent’ and ‘principal’ in many cases with little effective Board accountability) to use their leverage to extract economic rents through capturing market share and dominating competitors. It may just be precisely the ability of billionaires’ companies to capture rents (and thus hikeprofitability, thus share prices, and thus their personal wealth) which drive the decisionmaking of these corporate leaders.

In this context, then what effect, if any, would the introduction of a new tax on the wealth of these individuals have on the broader problem of concentrated market power in the US today? The effective taxation of the firms themselves would not change whatsoever, and all else being equal, the after-tax profits would not either – posing no direct effect on the rents derived from market concentration. It is only the tax liabilities of those individuals in control of the dominant firms that would change. But they would change – and substantially.

First, given how concentrated these billionaires’ wealth is in their companies, both a 2% wealth tax and a mark-to-market annual accrual tax would have a sizable effect on their tax liability, primarily through decreasing the amount of capital gains they would actually see from the appreciation of the stock they own. The higher the effective tax rate, then, the less incentive these individuals would have to make decisions that would ensure the companies they control – and have very concentrated financial stakes in – extract supernormal profits by exerting more and more market power.

This logic connects to recent research on top end income tax, which confirms that high top tax rates in the US previously were, in fact, useful in placing a brake on rent extraction among top earners, as the net benefit for highly-paid executives to continue to seek larger pay was blunted if not eradicated. It wasn’t until top rates dropped that these executives started bargaining more aggressively to hike their pay. Today’s top billionaires’ wealth does not amass from wage income but from the appreciation of their stock, hence their bargaining power over compensation plays out in their ability to manipulate or otherwise affect the stock price by, most especially, capturing excessive market share. A wealth or billionaire income tax then could be seen to decrease the net benefit of this form of rent-seeking, while the absence of said tax leaves the wealthiest with a very strong incentive to seek more returns through their control over their dominant firms.

In fact, those individuals who play simultaneous roles of CEO/Board Chair/ controlling shareholder – in particular in firms with high rents – have many more opportunities to set their own pay than traditional corporate management. This is because they have arguably more control over the levers of stock appreciation – levers which don’t pose a cost to the firm, other shareholders nor workers in the same way labor income does.

Second, a wealth tax may pose liquidity challenges for some of these US billionaires as their wealth is so concentrated in the stock of their own companies. They might be forced to sell some of their stock to come up with the cash to cover their tax liability. That could be thought of as a feature not a bug. Doing so would necessarily decrease their ownership stake and thus their relative control of these companies – thereby diversifying the equity ownership of those firms and making the stakes less concentrated in one individual. More diffuse ownership in dominant firms would not automatically reduce the incentives to capture market power, which is latent in large US businesses no matter the number of shareholders. Wrap-around antitrust rules and competing public options are still very much needed to reduce entrenched market power. That being said, more diffuse ownership would weaken the concentrated decision-making power of these manager-shareholders in key areas such as mergers and acquisitions strategy and executive compensation.

In sum, a wealth tax – given the specific characteristics of the ultra-wealthy in the US – would arguably work to disincentivise the hoarding of market power by decreasing the intensely concentrated personal returns of the individuals controlling the business strategies of some of the country’s most dominant firms. Importantly, in the US context in particular, more assertive antitrust enforcement is needed to break down the hoarding of market power by today’s dominant firms, diminish the economic power of today’s billionaires, and prevent further concentrated wealth accumulation into the future. While the market power effect of taxing the ultrawealthy in the US is necessarily tied up in the specific design choices brought to bear, the time has come to dig deeper into how a wealth tax could dent the personal financial incentives top Billionaires have to capture the rents that emerge from corporate consolidation.

This essay is derived from a forthcoming Roosevelt Institute Issue Brief. Many thanks to Ivan Cazarin for research assistance. Comments encouraged.

As Director of Corporate Power at the Roosevelt Institute, Niko Lusiani leads the think tank’s program to dissect and dismantle the ways in which extractive corporate behavior jeopardises workers, consumers, our natural environment, and our shared economic system.

Emily DiVito is Senior Program Manager for the Corporate Power program at the Roosevelt Institute. She supports the think tank’s work identifying, explaining, and advancing solutions for the problem of unchecked corporate power in today’s economy

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

As some companies reap outsize profits while consumers struggle to keep pace with inflation following the pandemic and Russia’s aggression against Ukraine, lawmakers around the world have been considering whether and how to respond.

In recent months, the UK approved a ‘windfall’ tax on oil and gas producers, US lawmakers proposed a tax on ‘super-normal’ profits under the rubric of a ‘Taxing Big Oil Profiteers Act’, and UN Secretary-General Guterres called for governments around the world to tax ‘excessive’ oil and gas profits. Meanwhile, global talks surrounding the tax affairs of large multinationals look to redistribute the ‘abnormal’, ‘non-routine’, and ‘residual’ profits among countries in furtherance of fairness goals.

In describing profits, are abnormal, excess, non-routine, super-normal, residual, and windfall just synonyms used to describe the same phenomenon? If so, what is that phenomenon? These terms are often used interchangeably, and they generally point to someone (usually a company) receiving an unexpected cash flow of some kind. In truth, there is no scientific way to distinguish precisely between normal or routine profits, on the one hand, and everything else, on the other. But the various terms for ‘everything else’ have distinct enough technical and social meanings that a terminology choice can influence the feasibility of a policy proposal. So it is worth understanding what people mean when they choose one of these terms to advance tax reform.

‘Normal’ and ‘Routine’

To understand what non-routine, excess, windfall (and so on) profit might be, it helps to start with the categories of income that distinguish them, namely, ‘normal’ or ‘routine’ profit. Are these the same thing? In an informal sense, they are. Both might be used to describe the return a competitive market would be expected to produce for an investment of labour or capital (or both).

A risk-averse investor might, for example, seek a relatively slow and steady gain of or 6% per year – a ‘normal’ return. When the market unexpectedly improves, the higher return appears other than normal (it may be short-lived or averaged out over time). For a company, a normal return might be described as the amount required to justify keeping the business going; in other words, to pay for requisite assets and employees.

A ‘routine’ profit might refer to the same phenomenon, but in a tax context it can refer particularly to the return on a specific activity performed in the context of a multinational enterprise. For example, an expert might explain that a routine prof it is what an independent (‘arm’s length’) service provider expects to earn by undertaking functions for another business, without taking on the other business’s broader risk.

Policymakers reflect these intuitions about what is normal or routine when they craft tax policy, including in the OECD’s two-part initiative to redistribute taxing rights in respect of highly digitalised companies (‘Pillar 1’), and to reduce tax competition for large multinationals with a global minimum tax regime (‘Pillar 2’). The language chosen conveys a sense that there is no political appetite for upsetting status quo rules around how countries tax (or not) normal profits. Only the proliferation of profits ‘beyond normal’ appear to justify tax reform.

The word ‘normal’ is also a core feature of excess profits surtaxes proposed in the wake of macroeconomically destabilizing events (such as pandemics and wars). In this context, normal profits can be determined in different ways. For instance, the ‘average earning’ approach considers the taxpayer’s average profit over a few years before the destabilizing events; the pre-existing tax rate applies to current profits up to that average, while the surtax applies to the excess. In contrast, the ‘invested capital’ approach designates a specified rate as ‘normal’ such that everything earned above that rate is treated as excess and subjected to the surtax.

The latter idea is seen in the OECD’s Pillar 2 framework, which (currently) effectively defines an 8% return on tangible assets and a 10% return on payroll costs as normal profits. Following this classification decision, national tax incentives that reduce or eliminate the tax on those profits are left alone, while the global minimum tax would apply only to returns in excess of the specified percentage.

Whether applied in the context of tax avoidance, tax competition, or a specific calamitous event, the animating idea here is that there is normal profit, and there is something beyond normal profit – and the tax system ought to respond differently to each category.

Beyond Normal

Beyond normal is a vast category. Within it, the terms excess, abnormal, windfall, supernormal, etc are often chosen to convey some underlying social or economic malaise.

But in a general sense, all the terms describe the same thing (even if different types of excess may have distinct economic origins): the recipient is benefiting from some form of market distortion. In the extreme, acompany that generates significant beyondnormal profits might have done so by gaining a monopolistic position; if so, regulators may have to step in more forcefully. Policymakers have to decide whether and how to react to various market distortions all the time, typically with insufficient information. In describing beyond-normal profits, the term ‘excess’ is the most ubiquitous, serving as a catch-all for abnormal, windfall, nonroutine, etc. Context matters: one term may be used to describe a common market imperfection – for example, residual profits often arise from intellectual property rights. Others are used to connote a bounty reaped from chance events (super-normal and windfall are typically deployed in this manner).

A non-windfall excess profit might be called ‘pure’ economic profit or ‘rent’. In brief, the owner (for example, a monopolist with significant and durable market power) has simply earned more than business viability requires. In theory, a perfectly competitive market will remove rent from the equation until everyone only receives normal returns. In reality, this never happens, and some economic rent is always available. But a windfall is distinct: all market participants reap advantages or disadvantages from sudden disruption, due to simple luck at the relevant time.

The question for policymakers is how to determine whether and when to respond to excess profits with a surtax. If a policymaker aims at excess profit and hits normal profit instead, they will worry about harming or chasing away productive economic activity. But if they aim correctly, a tax on pure windfalls can approach 100% without affecting investors’ future behavior.

A key challenge for policymakers is figuring out what the surtax will hit. Since an imperfectly designed surtax might induce investors to shift their profits around, and a perfectly targeted surtax might be easier for some countries to design than others, a global excess profits tax would likely be the most effective.

Summary

Abnormal, non-routine, super-normal, windfall, excess, and residual profits might all mean the same thing intuitively: profits that exceed what would be expected in perfectly competitive market conditions. There are different reasons why these ‘beyond normal’ profits arise, and there may be more and less politicised ways to measure what constitutes ‘normal’ and what constitutes ‘beyond’. The distinctions might matter because economic theory predicts different impacts on future investments. While experts will always seek precision, tax law is always as much about social and political maneuvering as scientific inquiry. As the world continues to navigate through crises of one kind and another, the niceties of precise rhetorical usage will likely matter less than overall public demand for reform.

Allison Christians is the H. Heward Stikeman Chair in Tax Law at McGill University in Montreal, where she writes and teaches national and international tax law and policy. Her latest book, with Laurens van Apeldoorn, is Tax Cooperation in an Unjust World (OUP 2021).

A longstanding issue in tax policymaking is the tendency to treat questions as technical ones to be solved by tax professionals, leaving any social justice concerns to be dealt with ‘politically’ elsewhere. In practice, this claimed political neutrality has yielded consistently regressive policies and left structural inequalities intact.

Carbon tax policymaking could easily repeat these failures. We need to provide truly transformative solutions which set out positions and policy coherence that halt more of the loss and damage that the most marginalised people live through.

Our world is faced with the existential threat of extinction. Right now hundreds of millions of people are broken by generational poverty, systemic and structural inequalities, their human rights denied, and their well being ignored. Tax justice has a powerful contribution to make and to change how this story ends.

Tax has a determinative impact on both the wellbeing of citizens and societies broadly through support of human development. It raises revenue and acts as a redistributive tool. In so doing, it has an important means to curb the severest effects of inequality and of realising human rights, and opens a means of reparation for the colonial legacies curtailing economic and social inequalities. It also enables a robust process of representation within society so that political inequalities can be overcome (for example, to ensure that wealthy elites are subject to effective, progressive taxation).

We are recruiting two posts to strengthen our work on climate justice and to further build human rights evidence to bring about a radical change through our research and international advocacy. These posts will contribute to a body of work across the social justice movement which attempts to shut the door on regressive solutions and on continued extraction. We want to investigate and propose a path forward where the pivotal role of tax tilts towards greater equality and rights, and mitigates against environmental loss and damage.

The focus of one post is to deliver peer reviewed research in in order to establish the technical feasibility of measures that address the dual crises jointly of climate and inequalities. The post also must advocate to ensure detailed consideration and understanding of the economic and social impact of carbon pricing proposals on inequalities, both within and between countries.

The focus of the second post is threefold: to serve as a continuation of work to build evidence and jurisprudence within United Nations legal framework treaty bodies; to support the work undertaken by Independent Experts and Special Rapporteurs; and to establish the central human rights and tax justice arguments for urgent tax policy reform. Both posts will use differing approaches to build a powerful narrative and build policy maker awareness of the political costs of failing to act.

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

For too long policymakers have failed to distinguish between productive profits and rents derived from market concentration and the control of scarce resources. A revived anti-monopoly movement must make full use of this difference to ensure that taxes encourage investment while eliminating rent-extraction as a business model.

Open and competitive markets are good for the economy, for business, and for consumers. To compete, companies must invest, innovate, be productive, and offer lower-cost, better quality products to customers. Fear that a competitor will bring out a newer or cheaper product keeps companies on their toes.

The most successful companies enjoy modest profits because the rest are competed away. Or so says the orthodoxy.

The problem

This idealised world does not exist outside economics textbooks, however. To the extent that real markets resemble the ideal, they do so as a result of state intervention. Left to themselves, market forces will often tend towards monopoly and the capture of value through the extraction of what economists call ‘rents’ – or unearned profits. The task of policymakers is to protect the level playing field while confronting corporate power when it seeks to escape from competitive forces. Economist Adam Smith recognised this very problem, observing that a truly free market would require an active government to guard against anti-competitive behaviour. Firms can earn productive profits (e.g., due to past investment, risk-taking or innovation,) and they can also receive rents, the fruits of uncompetitive behaviour. Distinguishing these two is critical.

All markets suffer concentration or monopolisation, to a lesser or greater degree. In some areas, called natural monopolies, competition is all but impossible. Take, for example, a railway between two cities: it makes no sense for a competitor to build a duplicate railway next to it, before they can compete. But monopolisation happens in less obvious areas: for example, the ‘network effects ’enjoyed by tech giants like Google; control over scarce resources like oil; or where companies lobby to create high ‘barriers to entry’ to competitors. The negative effects of such market power can include higher prices, sluggish innovation, and as economists such as Jan Eeckhout have shown, economy-wide lowering of wages. The critical distinction, when looking at corporations, is therefore between profits that are generated by firms in exchange for the goods they sell and the services they provide (‘productive profits’), and the profits they generate simply because of their size or their market power. Economists tend to call the latter ‘rents’.

One of the best ways to understand market concentration is to look at rates of profit. In an open and competitive market, profits should tend towards zero as firms undercut each other. As sectors move away from perfect competition, firms can use their market power to charge higher prices, and profits (or ‘mark-ups’) tend to rise. There are some exceptions to this, for example what may appear as unearned profits may in fact be the return on past investment, competition, risk-taking or innovation – so called Schumpeterian rents.

Brett Christophers argues that rent-seeking is particularly stark in 21st century Britain: ‘the leading corporations are largely rentiers, and the biggest sectors of the economy are largely characterised by rentier dynamics’. Today, for instance, six energy companies hare 83% of the retail gas market, four broadband companies supply over 85% of broadband customers, and four banks have 64% of retail bank accounts. The UK Competition and Markets Authority (CMA) also observe ‘a marked increase in concentration [and profitability] in the years after the 2008 financial crisis’. This may help explain the UK’s chronic underinvestment in capital compared to other OECD countries. The pandemic has made matters worse: just six US tech firms added over $4 trillion to their market value since the pandemic began. For UK-listed firms since the pandemic, profits were up 34% at the end of 2021, with 90% of this increase accounted for by only 25 companies that largely operate in concentrated sectors.

Solutions

So, what can we do? And what is the specific role of taxation?

There are no magic bullets: to confront monopoly or market power needs policymakers and regulators to act in coordination and use a range of tools, as the Biden administration recognised last year with a new cross-government antitrust agenda.

The most powerful tool to re-shape the economy, potentially, is re-invigorated competition policy (or, to use the US term, antitrust). But the tax system can be exceptionally powerful tool both as a shaper of the economy – by applying different tax rates to extractive versus productive activities to re-balance economic activity – and as a redistributor of unearned rents. It’s on this that we focus in what follows.

Corporate tax

The past decade has seen a race to the bottom on headline corporate tax rates, across developed economies and beyond. In the UK, the headline rate has fallen from 30% to 19% today. Politicians have claimed that this boosts investment – a laudable aim, but tax cuts have not achieved it. Slashing rates by over a third has not remedied the UK’s low investment problem. We argue that other factors are driving the UK’s low investment — potentially including widespread rentierism. Many economists argue that the optimal rate of corporate tax is likely to be much higher than the current average global rate. Corporation tax rate is not the only, or even the principal, factor in firms’ decisions about where to locate, even where they are relatively mobile. Rather, firms invest when they can see future growth and profit opportunities. This is better addressed through broad industrial policy. IPPR has previously called for UK corporation tax rates to rise to 25–30%.

Recent agreements at the G7 and OECD on a global minimum corporation tax rate at 15%, and tools to recoup tax revenues internationally if tax havens cut their headline rates below this level, will potentially end this race to the bottom. Far better than a race to the bottom is ‘upwards competition’ on broader policies that make the UK an attractive investment destination: to create sound infrastructure, a well-trained and skilled workforce, thriving research and development, and rising productivity.

Headline corporation tax is levied on all profits, so does not distinguish between ‘productive profits’ and rents from market power. It is possible, however, to alter the effective rate that different firms pay, via a system of allowances or tax exemptions that benefit productive firms over rentiers.

The design of tax reliefs or exemptions matters as deductions that are set too high, or are too complex, will erode the tax base without countervailing positive economic effects. Badly designed tax reliefs can be less effective – and less transparent – than public spending of equivalent cost. Yet there can be good economic arguments for well designed reliefs and exemptions as part of an economy-shaping tax system to steer corporate behaviour towards desirable outcomes. Investment allowances, for example, are widely supported to encourage companies to invest their profits. The UK recently created a temporary investment deduction at a generous 130%.

Windfall taxes and beyond: excess profits tax

Separate from the headline rates of corporation tax levied on all profits, a country can also directly tax windfall profits (which we define as profits reaped from sudden, extreme price changes in products or commodities outside firms’ control). For example, global gas prices have spiked following the Russian invasion of Ukraine, massively increasing the profits of fossil-fuel firms. These firms have distributed these enormous windfalls to their share holders via record-breaking dividends and share buybacks. The UK, Italy and other countries have responded by levying a windfall tax on energy producers/fossil-fuel extractors, and redistributing these to support struggling consumers. This is legitimate redistribution, and it also curbs these profits by firms with market power that can monopolise windfall returns. It is no coincidence that, more broadly, windfall returns tend to be made in highly concentrated sectors: oil and gas extraction, tobacco, and mining and mineral extraction

Yet, as discussed above, returns to firms with significant market power are not just in monopolising windfalls. Without competition, firms can reap excess profits on an ongoing basis. These profits are clearly unearned, at the expense of the wider economy and consumers, so excess profits that are not just windfall profits should be taxed, to disincentivise rentier activity and redistribute its unearned gains.

To make this happen, policymakers must first establish a toolkit to determine which firms operate in environments of significant market power, and to quantify the magnitude of the returns on that power. An emerging community of economists on both sides of the Atlantic is now studying this problem and developing novel solutions.

The final way of taxing economic rents is to focus on the ways in which they return to, and further enrich, (already wealthy) shareholders, widening economic inequality. Share buy-backs, for instance, are anathema to a productive and competitive market: they are symptomatic of firms that can identify no further investment opportunities beyond artificially boosting their own stock market price. Companies like BP and Shell, for example, have paid out record sums to shareholders at the expense of under-investing in clean, renewable energy technologies. The Biden administration’s landmark Inflation Reduction Act includes provisions to tax share buy-backs at 1%, an initiative that should be replicated internationally, and – in time – at an increased rate.

Other economists have proposed novel methods of taxing firms’ market capitalisation as an easily-implemented proxy for wealth taxation which should be considered by policymakers.15 These approaches are attempting to achieve the same objectives as an excess profits tax but levied on a different tax base, and so to some extent are substitutes for each other.

Corporate Power and Competition Policy

Taxes alone can never fully resolve market concentration and monopoly. It is simply not enough to bemoan low investment and innovation across modern economies – we must recognise that there are firms and sectors that benefit and profit from stagnation. Their power must be confronted directly. There will always be a role for pro-active competition or antitrust policy, which will need to change over time as new technologies open markets that may be particularly prone to market concentration. This is particularly important during periods of high inflation when monopolistic firms may take advantage of broad price rises to increase their markups.

We have proposed that the UK’s CMA should launch pre-emptive investigations into the potential for excess profits in the most concentrated sectors of the economy. In Germany, the government has already suggested ways to tighten competition enforcement in sectors perceived to be unfairly profiting from the current situation.

In the US, the Biden administration is embarking on an ambitious programme of anti-trust policy that combines a broader conception of competition with more rigorous enforcement. Similarly, the UK’s CMA should broaden its conception of market power which is currently focussed too narrowly on prices. IPPR has previously called for the CMA to consider the interests of consumers, suppliers, entrepreneurs, taxpayers, workers and the broader value of innovation in order to promote and protect the public interest.17 A review of the CMA’s powers and decision-making principles could determine whether market share thresholds for regulatory action should be set, whether regulatory tools to address vertical integration and price discrimination should be strengthened, and whether competition policy should have an a priori objective to limit market power by limiting market concentration.

If we truly want to shape our economies for the better, it is high time that we concentrate on the division in our economy between productive profits and rent extraction that costs us all. This has been neglected for too long, but the effects of the pandemic and the current global inflationary crisis highlight this. Taxation is both a way to confront rent extraction and an important tool to redistribute rents.

George Dibb is head of the Centre for Economic Justice at the Institute for Public Policy Research (IPPR), the UK’s leading progressive thinktank. George leads IPPR’s work on economic policy and is based in Westminster. With a background in science and innovation, George’s interests include economy-shaping industrial strategy, research and development, sustainability, and climate change.

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

Corporate income tax in the United States was originally introduced as an antitrust measure. A steeply progressive version of the same tax would reduce the economic and political power of monopolists and reintroduce competition in an economy increasingly burdened by rent extraction.

When the United States enacted its first corporate income tax in 1909, the main purpose was to regulate corporate power, especially that of the major monopolies such as J.P. Morgan’s US Steel and John D. Rockefeller’s standard Oil. The corporate tax was part of the same antitrust campaign that culminated in 1911 with the Supreme Court ordering the breakup of Standard Oil. Because the purpose of the tax was to regulate rather than to raise revenue or redistribute income, the initial corporate tax rate was a flat 1%. The point was to force corporations to disclose their business activity and therefore make them easier to regulate through antitrust enforcement. In addition, corporate tax returns were to be public, to expose their immense profitability to the voters.

Corporate lobbying soon eliminated the publicity of corporate tax returns, but the corporate tax itself proved more resilient. During World War I, income tax rates were raised dramatically to finance the war effort, and this included the corporate tax rate, which was raised to 12%. In addition, from 1917 onward a series of excess profits and war profits taxes were imposed on corporations that profited from the war. The war profits tax was levied on corporate profits above a three-year pre-war average, and its top rate could be as high as 80%. Similar excess profit or windfall profit taxes were enacted in other belligerent countries like the United Kingdom, France, and Germany. The same type of excess profits tax was used by the US during World War II with rates as high as 95% (but the overall combined regular corporate tax and excess profits tax could not be higher than 80%), and this tax was retained until the Korean War in the 1950s.

During the 1930s, the Roosevelt administration decided to use the corporate tax to curb the power of corporations permanently. In addition to other reforms (e.g., breaking up ‘pyramid’ structures that enabled the ultra-rich to control public corporations like utilities) the administration proposed a permanent ‘surtax’ on retained earnings and a reduced tax on dividends (to encourage distributions that would reduce the power of corporate management). This proposal was defeated, but Congress eventually adopted a progressive corporate tax up to 53%, and corporate tax rates were progressive from 1936 until 2017. The tax brackets and rates for 1942-1945, for example, were 25% for the first $5,000, 27% for the next $15,000, 29% for the next $5,000, 53% for the next $25,000, and 40% for income above $50,000. These relatively high rates were only reduced gradually in the following decades. Before 1986, the top corporate rate was 46%. After the tax reform of 1986, the highest corporate rate was cut to 35%, and the brackets from 1993 to 2017 were 15% for the first $50,000, 25% up to $75,000, 34% up to $100,000, and a flat 35% for income above $100,000.

The corporate rate structure remained progressive in the US until 2017. However, the brackets were not adjusted for inflation, so that by 1993 the top rate of 35% was reached at $100,000- a large sum in the 1930s, but a pittance for corporations in the 1990s, so effectively it was pretty much all taxed at the top rate, and its progressive nature was rather hidden. Moreover, the major difference between the post 1986 rate structure and earlier rate structures was that from 1987 on the corporate tax was imposed almost entirely on large, publicly traded corporations, so that almost all taxable corporations were subject to the flat 35% rate. In the 2017 tax reform, progressive rates were formally abandoned, and the corporate tax became a flat 21%, where it remains today.

There is, however, a strong case to be made for reviving progressive corporate taxation, with more meaningful tax brackets. If the main reason to have a corporate tax is to tax rents and limit monopolies, then the effective tax rate on normal corporate profits should be zero. But on monopolistic returns, the tax should be progressive, with a very high tax rate (e.g., 80%) for profits above a very high threshold (e.g., $10 billion).

Normal Returns

There is no reason to tax corporations on normal returns. Normal returns are the risk-free return from investing in assets like US Treasuries. In recent years, these returns have been quite low, but they have historically been higher. However, from the point of view of only applying the corporate tax to monopoly rents, these returns should be exempt. In addition, there is the uncertainty about the incidence of the corporate tax (i.e. who bears the economic burden of the tax), which suggests that a tax on normal returns is less likely to contribute to the progressivity of the system. Finally, any inefficiency from the corporate tax arises from the tax on normal returns since a tax on pure rents does not generate ‘deadweight loss.’ Deadweight loss is a term economists use for the difference between the revenue a tax raises and the decline in the taxpayer’s welfare caused by a change in taxpayer behavior due to the tax. A tax on rents does not change taxpayer behavior since taxpayers not subject to any competition would derive net profit from rents even if 99% of them were taxed away.

Since from a political perspective a zerotax rate on normal returns is unlikely to pass, and since it is hard to determine what normal returns are, I would suggest that we allow for permanent expensing (i.e., immediate deduction) of corporate capital expenditures (such as building a new factory). Such expensing is equivalent to an exemption for the normal return to capital.

Super-normal Returns (Rents)

Economists are almost unanimous in supporting a tax on rents since (a) it does not influence corporate behavior and is therefore efficient, and (b) it falls on capital and is therefore progressive. Above the exemption resulting from expensing, the corporate tax should be sharply progressive. The reason to have a progressive tax on rents is that in addition to targeting rents, we also want to discourage bigness, which is equivalent to monopoly or quasi-monopoly status. The less competition a business firm faces, the more profitable it is likely to be, because competition generally drives down prices. That is why the most monopolistic firms are also the most profitable, and why they engage in behaviors like ‘killer acquisitions’ designed to eliminate competition.

At the top, the corporate tax rate should be 80% for income above $10 billion, like the excess profit taxes of the two world wars. In 2019, this rate would have applied to the Big Tech: Amazon ($10.1 billion), Apple ($59.5 billion), Facebook ($22.1 billion), Google ($30.7 billion), and Microsoft ($16.6 billion). Other corporations that had profits over $10 billion in 2019 include other major tech companies (Intel, Micron), Big Banks (Chase, Bank of America, Wells Fargo, Citi, Goldman Sachs, Visa), Big Pharma (Pfizer), Big Oil (Exxon, Chevron), Big Telecoms (AT&T, Verizon, Broadcom), United Health, Boeing, and some major consumer brands (Johnson & Johnson, Home Depot, Disney, Pepsi). All of those enjoy some degree of monopolistic or quasi-monopolistic status.

Such a high tax rate may persuade the corporations subject to it to split up. Splitting up corporations to reduce their profits and therefore escape the 80% tax rate is a feature of the proposal and not a bug: as FTC commissioner Lina Khan and others have proposed, we should ideally want to induce Big Tech to divest their anticompetitive acquisitions (e.g., Facebook’s acquisitions of Instagram and WhatsApp). And if the tax structure also motivates an actual break-up of the core business (e.g., along geographic or business segment lines), any loss in efficiency would be more than compensated by the removal of the threat to democracy posed by Big Tech.

Reuven Avi-Yonah is the Irwin I. Cohn Professor of Law at the University of Michigan, where he teaches individual, corporate, and international taxation. He has published over 300 books and articles on various areas of tax law including several recent publications on the relationship between the US corporate tax and antitrust.

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

For decades the United States’ tax system has favoured large corporates over locally embedded and competitive firms. The resulting social and economic costs of monopoly are artefacts of the political process and can be reversed by government action.

When Jeff Bezos launched Amazon in 1995, he made securing government favours a core part of his strategy. Chief among these were lucrative tax advantages largely unavailable to his competitors, especially small independent businesses. This disparate tax treatment gave Amazon a pivotal early edge over rivals in the online market. And it’s continued to finance Amazon’s dominance ever since, supplying billions of dollars in free cash flow that the tech giant has used to fund predatory pricing (systematically selling key goods and services below cost, to monopolise markets) and acquisitions designed to thwart competition.

The opening salvo for Bezos’s tax strategy was locating Amazon’s first headquarters in Washington, instead of California, to avoid sales tax in a populous state. As Bezos explained in 1996, ‘It had to be in a small state. In he mail-order business, you must charge sales tax to customers who live in any state where you have a business presence…We thought about the Bay Area, which is the single best source for technical talent. But it didn’t pass the mall-state test.’

No matter how hard brick-and-mortar retailers competed with Amazon they were hamstrung by the sales taxes they had to collect from their customers. This tax disparity was due to a 1992 US Supreme Court ruling that blocked states from imposing sales tax collection on retailers that lacked ‘nexus’, or a physical presence, in the state. Independent booksellers, later joined by the big chains, campaigned vigorously for Congress to level the playing field, but time and again, Amazon’s lobbyists defeated their efforts.

How much did this tax rule bolster Amazon? A 2014 study of credit card transactions found that, when a state extended sales tax to Amazon (because it had opened an in-state office or warehouse), households significantly reduced their spending with the tech giant, particularly for high-priced items.

More telling evidence can be found in the extraordinary lengths Amazon took to preserve this tax advantage. Amazon had employees carry fake business cards to ensure their presence in a state would not trigger nexus. In Texas, Amazon concealed that it was operating a warehouse from state tax officials. When the state sued for $269 million in back taxes, Amazon threatened to shut down the facility. The state cancelled the tax bill. In South Carolina, Amazon made a deal with the governor to remain sales tax free despite building warehouses in the state. When the state legislature protested, Amazon halted construction until lawmakers backed down.

From sales tax-dodging to development subsidies and beyond

As Amazon’s logistics growth accelerated, it began building more warehouses in more places, which made it harder to sidestep sales tax.

In 2012, Amazon pivoted to a new strategy for getting the public to finance the company’s growth: development subsidies. As of July 2022, Amazon has been awarded at least $4.8 billion in local subsidies to help it undercut its competitors and fund its expansion.

Amazon has also skirted corporate income taxes in both the US and Europe by establishing a labyrinth of shell companies, which transfer profits to subsidiaries based in Luxembourg, a lucrative tax haven. In 2021, Amazon’s European operations generated 51 billion Euros in sales, but paid no income taxes. The European Commission has challenged Luxembourg’s tax arrangements with Amazon as a form of “illegal state aid” that violates competition policy by favouring one company over others.

However, the Commission has yet to make an effective case to the courts. Meanwhile, in the US, Amazon paid just 6% in federal corporate income tax on $35 billion in reported profits, meaning it avoided paying over $5 billion into federal coffers, according to the Institute on Taxation and Economic Policy.

Through their inaction policymakers have gifted Amazon billions of dollars, giving it a major advantage over smaller competitors that must shoulder fuller tax obligations. They’ve also provided a crucial source of funding for Amazon’s predatory pricing schemes, enabling it to sell below cost to capsize competitors and lock-in online shoppers.

More recently, Amazon has used its prodigious subsidy-enhanced cash flow to acquire other companies, taking over pivotal technologies to cement its dominance of cloud computing, while buying its way into new industries with a string of acquisitions in groceries, health care, entertainment, and more.

A Tax Code to Consolidate Corporate Power

Amazon’s strategy offers a road map of how to harness the tax system to build a monopoly. But most of the giant corporations that now dominate their industries owe their market power in part to government handouts and tax favours. For decades, local and federal US policymakers have systematically structured the tax system to fuel the concentration of corporate power, at the expense of small businesses, workers, communities, and the economy as a whole.

At every level the tax system works to concentrate economic power and disadvantage small businesses. Take tax shelters, for example. We know US based multinationals – not just Amazon – deploy elaborate schemes to hide their federal and state tax obligations in places like Luxembourg and the Cayman Islands. But they also do this on US soil. Companies operating in multiple US states shield much of their income from state taxes by transferring in-state revenue as a payment (for rent or use of trademark, for example) to subsidiaries in states that don’t tax corporate income, like Delaware or South Dakota. This maneuvering is not an option for most small, independent businesses, who don’t have a fleet of tax attorneys on their payroll to set up out-of-state subsidiaries.

Local development incentives are another example. Corporations get almost all of the $65 billion to $90 billion a year that cities and states spend on tax breaks, economic development incentives, and other subsidies. In a 2015 study of 4,200 economic development incentive awards in 14 states, Good Jobs First found that large companies collected between 80 and 96% of the dollar value of the funds they analysed. Research indicates that these incentives generally don’t pay off, often failing to increase overall employment while saddling communities with new infrastructure costs. Many of these deals do not provide a boost to the local economy, but rather undermine the small, independent businesses that are excluded from these tax breaks and incentives and left to finance their own expansion.

Many states have also allowed big corporations to systematically contest their property tax bills. Walmart and other large retailers have paid lawyers to implement a dubious ‘dark store’ theory of value, challenging the valuations of thousands of their stores in multiple states on the basis that their properties would be nearly worthless if they were empty. This strategy – used against communities across the US – involves upfront legal costs that large corporations, because of their scale, can easily absorb and are far outweighed by the payout. They have managed to sharply cut their tax bills, which has led directly to funding cuts for local schools, libraries, and other services.

Small is beautiful

Research shows that small, independent businesses often outperform in key ways. Small banks are better at making productive community-based lending and were much more effective at distributing federal relief loans during the pandemic to independent businesses, for example. Small companies produce 13 times more patents per employee than large companies, and those patents tend to generate better industry impact and growth. The tax code and system of big-corporate handouts are sapping innovation, quality, and local resilience.

When we lose small businesses, we don’t just lose the innovations. A spate of new economic research shows that the high corporate consolidation we’re seeing across different industries is a main driver of declining real wages and job losses. A Harvard Law Review study calculates that a 2018 median US annual wage of $30,500 would be about a third higher – $41,000 – if it weren’t for monopsony concentration. Corporate dominance over our supply chains has also helped make them brittle, and opportunistic price gouging by megacorporations is a primary driver of the recent surge in inflation. Small businesses are integral to healthy communities and our democracy. As locally owned businesses disappear, communities of all kinds lose their sense of social connectedness and collective agency. Industrial agriculture, for example, has devastated rural communities in the US and is linked to higher rates of crime and declining social cohesion. When retail chains like Walmart dominate the local economy, they undermine civic participation and social capital. Monopolies of all kinds disproportionately harm Black and Brown communities. Fossil fuel conglomerates and the big electric utilities have hindered our ability to address climate change. Amazon and Comcast exert so much power over our political system that efforts to help our society are continually crushed by powerful lobbying efforts. On the other hand, small businesses disaggregate economic power, create a more equitable distribution of income and wealth, and nurture democracy by fostering community self-determination.

An Antimonopoly Tax Agenda: Politics and Policy

If pro-monopoly tax policy is bad economics, it’s even worse politics for progressives. Although long forgotten today, the Democratic Party once counted small business as a key constituency alongside workers, and steadfastly fought for their rights and welfare. This helped win New Deal programs that secured, in the words of FDR, “economic freedom for the wage earner and the farmer and the smallbusiness man.”

But in the 1970s and 1980s, an ascendent faction of Democrats abandoned their party’s concern about concentrated economic power, and many liberals began distancing themselves from both labor and small business. This created a vacuum for the US Chamber of Commerce, which used small businesses’ frustration and lack of a political home to drive a right-wing agenda.

If US progressives advance an antimonopoly tax agenda, they can recover a populist politics, which would help them compete in rural areas and swing states, drawing in voters who are yearning for a fairer, more equitable economy. Stronger tax and spending policies, at every level of government, is an essential spoke on the wheel of strong antimonopoly reform. When our tax system is built to foster fairness and justice in addition to vitality and economic growth, it can help to restructure economic power and more broadly distribute and boost prosperity.

Small business should be at the centre of an antimonopoly tax agenda. Yet it’s rarely brought under the tent of rebuilding our tax system to be fairer, despite that it is inherently good for small business – and small business is so good for a robust, resilient, vital economy. That means designing policies that close monopoly tax loopholes – in part, to eliminate global and state tax shelters – and redistribute tax obligations to level the playing field for small business and curtail corporate concentration. It also means helping small business rebuild from the damage done by providing targeted support for smaller competitors.

Combatting monopoly power is not only a matter of reinvigorating antitrust policy. We must also address the many ways in which neoliberal policymaking has favoured corporate consolidation at the expense of local economies. Using tax policy to foster fair competition and decentralise economic power should be high on this list.

Antimonopoly Tax Reform: Policy examples

Implement a Progressive Corporate Tax Rate

One potent antimonopoly tax reform measure would be a progressive corporate tax rate. As Reuven S. Avi-Yonah argues in this issue of Tax and Monopoly Focus, the primary reason we need a corporate tax is to limit the ‘power and regulate the behavior of our largest corporations,’ which is the same reason the US first adopted the corporate tax in Instead of a flat tax, he proposes that the tax should be 0 for normal returns that reflect fair markets and increase sharply to target the high profits indicative of monopoly rents.

Raise Taxes on Shareholder Payouts

We need to more fairly tax where the bulk of profits of megacorporations go — shareholders. Shareholder payouts in the form of stock dividends and share repurchases are taxed at a lower rate than workers’ income tax. The tax preference for capital should be eliminated and these different forms of income treated as equivalent by the tax code. It is also important to unlock these tax revenues on a more timely basis, as the current system fails to impose a tax until the stock is realised. A mark-to-market capital gains system could release this revenue annually. (As a side note: The Inflation Reduction Act, enacted into law in August 2022, imposes a 1% excise tax on some repurchases of corporate stock by publicly traded companies. While the tax provides a clear legislative signal that stock buybacks are problematic, progressive analysts generally agree it is not enough. In fact, economists William Lazonick and Lenore Palladino argue stock buybacks should be banned altogether.)

Adopt Worldwide Combined Reporting to Close State and Federal Tax Loopholes

A simple way for states to address tax dodging is to implement a ‘Worldwide Combined Reporting’ system, which requires companies to report their total global profits and pay a tax on the portion of those profits produced in a given state. For example, if 5% of a company’s global business occurs in Montana, then Montana’s corporate tax rate would apply to 5% of the company’s taxable profit. Only a few states – Idaho, Montana, and North Dakota – currently utilize worldwide combined reporting, which ensures transparency on large companies, levels the competitive playing field for independent businesses, and can help generate public revenue. Meanwhile, twenty-eight states and Washington, D.C. have adopted ‘water’s-edge’ combined reporting only, which applies the same principles but excludes affiliates of the conglomerate that are incorporated outside of the United States or that conduct most of their business outside the US implementing worldwide combined reporting – at the state and federal level – would buttress the current reporting system by building and synthesising transparency on the full extent of multinational corporations’ tax liabilities.

Close the Dark Store Tax Loophole

States should adopt legislation clarifying how tax assessors determine the property value of big-box stores. The dark store tactic has not only deprived local governments of billions in revenue, but it has also forced local businesses and residents to pay higher taxes to maintain services. States can address this with a simple clarification that modern retail buildings must be valued based on their current operations and not on a theoretical future in which they are decrepit.

Stop Subsidising Corporations and Invest in Small Business

Instead of giving subsidy deals to corporations that are channeling their profits to Wall Street, local municipalities and states can use those funds to circulate dollars locally and drive long-term growth For example, local governments can invest in real estate for commercial use and public goods like high-speed fiber networks, and provide carefully targeted loans to Black and Brown entrepreneurs to close the racial entrepreneurship gap.

Stacy Mitchell is co-director of the Institute for Local Self-Reliance and directs its Independent Business Initiative, which produces research and analysis, and partners with a broad range of allies to design and implement policies to reverse corporate concentration and strengthen local economies.

Susan Holmberg is a political economist and the Senior Editor and researcher of the Independent Business Initiative at the Institute for Local Self-Reliance. She writes on corporate power and inequality.

The following article is from the “Tax and Monopoly” October 2022 issue of the Tax Justice Focus, an online magazine that explores boundary-pushing ideas in tax justice and revolutionary solutions to the most pressing challenges of our time. Each edition features articles from prominent experts and academics from around the world. The “Tax and monopoly” issue is co-published with the Balanced Economy Project and Roosevelt Institute.

Monopolists and rentseekers have been running rings round the democratic fiscal state for decades. It is obvious to everyone that the game is rigged. But we still have a few more rolls of the dice. Let’s use them wisely.

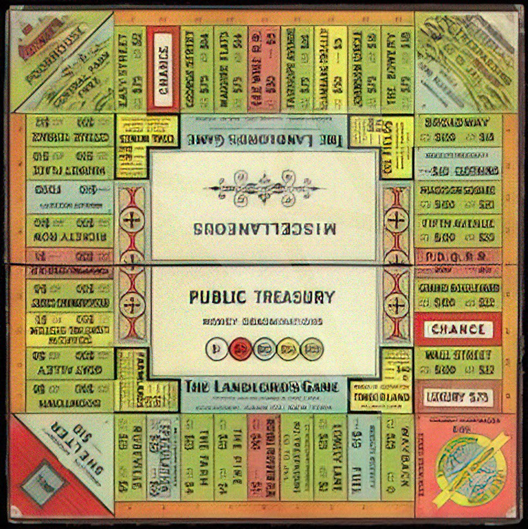

The earliest known version of Monopoly, called The Landlord’s Game, was designed by an American women’s rights and anti- monopoly advocate, Elizabeth Magie, in 1902. She invented the game to illustrate the economic consequences of rent-seeking and the value of wealth taxation to discourage large agglomerations of economic power.

The instructions included a graduated tax table, with increasing marginal rates depending on property/wealth, and the funds went back to pay for basic necessities of all the players. In this first version of the Monopoly game, everyone won when the poorest player doubled their original stake. Compare that to today’s rules of the Monopoly game, where the goal of the game is financial domination. Paying income taxes is purely bad luck, and when you are forced to contribute, the proceeds just go back to the bank – helping no one.

Elizabeth Magie’s The Landlord’s Game (1902).

Different eras, different rules of the game, very different conceptions of the role and the value of taxing entities with excessive market power.We begin this issue of Tax and Monopoly Focus with this bit of folk wisdom to show not just how far back the relationship between tax policy and anti- monopoly goes in the public conscience, but also to illustrate that the current tax rules – which exacerbate corporate consolidation – are not natural or necessary. They are in fact long due for a rethink and a re-write.

Before jumping into this rethinking, we might well start with some of the ways in which current tax rules incentivise and otherwise actively subsidise the growth of corporate oligopolies.

First, current international tax rules and the presence of tax havens work to boost after- tax profits for globally-integrated large firms. Smaller domestic competitors who cannot engage in the same sort of regulatory arbitrage are at a structural disadvantage.

The mere size and complexity of large, global corporate structures with many subsidiaries worldwide allow these entities to befuddle tax auditors and essentially prevent equal enforcement of tax laws. This is frustrating enough for richer countries: just think how much harder it is for revenue authorities in lower-income countries. Simply put, the more complicated the corporate structure, the less enforceable the tax code is. The bigger you get, the less likely you’ll have to pay tax.

Second, and relatedly, the tax code and its enforcement are particularly vulnerable to lobbying by concentrated special interests, such as incumbent corporate oligopolies. Again, this is troubling enough in wealthy nations; lower-income countries are even more susceptible. Indeed, the more profitable and more incumbent a corporation becomes, the more is at stake in the formation and enforcement of tax policy. Lobbying for lower taxes may indeed be inefficient economically, as Professor Philippon has argued,2 but changing tax laws and how they are enforced becomes a premium when a corporation becomes a highly-profitable incumbent.

Third, the flat corporate income tax rate – as it exists today in the US – is facially neutral between small and large firms. But given the exorbitant tax privileges large, incumbent firms have in practice, a statutorily flat rate in reality means a much lower effective rate for larger, global firms compared to smaller, domestic ones. Given all the other tax advantages of bigness, this de jure equal treatment creates defacto advantages for large, incumbent firms. Further, by taxing the first dollar of firm profit the same as excessive profits gained from rent-seeking, a flat rate effectively incentivises super-normal rent-seeking by dominant firms.

Fourth, unlimited corporate interest deductions (until recently in the US, and this is still being battled in the EU) allow for highly-leveraged buyouts that wouldn’t be done without such tax deductions.

Finally, the US Federal tax code for over a century has subsidised many merger and acquisition (M&A) deals via what’s called a tax-free reorganisation, which allows sellers to defer (sometimes indefinitely) the gain from their sale to avoid tax liabilities.3 This implicit subsidy incentivises corporate consolidation, with little if any redeeming economic or societal value.

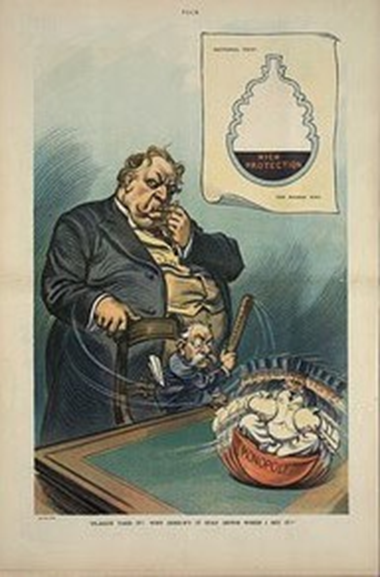

In Udo Kepler’s 1911 cartoon William Taft wonders why his Attorney General George Wickersham can’t keep the monopolists from springing back every time he hits them with the Sherman Act.

Just as today’s tax system contributes to corporate consolidation, so then too can our tax policies help restructure the economy to disrupt concentrated economic power and drive a more dynamic, multi- player economy. This special edition collects five timely contributions which help to diagnose the role our tax code can have to deconstruct and deter excessive market power as a complement to a more assertive anti-monopoly agenda.

Susan Holmberg and Stacy Mitchell brilliantly chronicle Amazon’s tax break-financed rise to retail dominance, a vivid illustration of how a broken tax system has helped spawn a 21st century monopoly.