We’re pleased to share the tenth edition of the Tax Justice Network’s monthly podcast/radio show for francophone Africa by finance journalist Idriss Linge in Cameroon. The podcast is called Impôts et Justice Sociale, ‘tax and social justice.’

Nous sommes heureux de

partager avec vous cette dixième

émission radio/podcast du Réseau Tax Justice, Tax Justice Network produite

en Afrique francophone par le journaliste financier Idriss Linge basé

au Cameroun. Le podcast s’appelle Impôts

et Justice Sociale.

Dans cette neuvième

édition nous revenons sur le premier pilier des propositions de l’OCDE en vue

d’une taxation unitaire des multinationales au niveau mondial

Nous avons l’occasion

de partager des avis de deux économistes de renom, qui sont aussi des membres

de l’ICRICT,

une Commission indépendante qui mène des travaux pour la formulation d’une

taxation unitaire et équitable des entreprises multinationales dans le monde

Il s’agit notamment de:

Ricardo

Martner, un économiste indépendant avec 30 ans d’expérience dans

le secteur des Nations Unies

Thomas Piketty, Economiste lui aussi et Professeur à l’Ecole des Hautes Etudes en Sciences Sociales de Paris en France. Il est surtout reconnu pour la qualité de ses travaux sur les inégalités économiques dans le Monde

Pour écouter directement en ligne, cliquer sur notre lien Youtube, ou l’application Stitcher.

Vous pouvez aussi suivre nos activités et interagir avec nous sur nos pages Twitter, et Facebook.

As urgent reshaping of the international tax system has risen up the geopolitical agenda, the OECD’s tax reforms announced in January 2019 are proceeding at a rapid pace. The proposals set out to go “beyond the arm’s length principle”, introducing elements of unitary taxation and formulary apportionment, with the aim of redistributing taxing rights to the countries where real economic activity takes place.

To date, however, there has been little public analysis of the likely effects of these reforms and questions have been raised as to whether the current proposals are comprehensive enough to provide the drastic changes the international tax system needs to keep up with the changing landscape of multinational companies.

This one-day virtual conference hosted by the Tax Justice Network brought together international experts including speakers from the International Monetary Fund (IMF), the Intergovernmental Group of Twenty-Four (G24), the Organisation for Economic Cooperation and Development (OECD), the World Bank (WB) and the Independent Commission for the Reform of International Corporate Taxation (ICRICT) to provide technical analyses of the current proposals and consider the following questions:

How do the current reforms compare to alternative proposals tabled by other international institutions and civil society organisations?

What are the implications of the reforms for lower-income countries, particularly on tax bases, as well as those of OECD members?

How far do the suggested reforms achieve their intended goals of redistribution of taxing rights and tightening up on tax avoidance?

What are the political challenges within the OECD reform? And, looking to the future, what potential is there for involvement in the decision making process from other international bodies such as the United Nations?

Welcome and Keynote I: ‘The maldistribution of global taxing rights, and how to fix it’ and Q&A

Panel I: ‘The revenue impacts of redistributing taxing rights’ and Q&A

Keynote II: ‘The G24 proposal, and the challenges of the Inclusive Framework’ and Panel II: ‘Which way now for the reform and redistribution of global taxing rights?’ and Q&A

Shared papers and resources

Independent Commission for the Reform of International Corporate Taxation and Tax Justice Network

Welcome to our seventh monthly tax justice podcast/radio show in Portuguese. Bem vindas e bem vindos ao É da sua conta, nosso podcast em português, o podcast mensal da Tax Justice Network, Rede de Justiça Fiscal.

Penalidade máxima: a sonegação no futebol:Ouça no podcast #7:

No futebol nem tudo é jogada bonita e bola na rede. Para muitos, o aspecto financeiro e o peso do dinheiro podem manchar a beleza do esporte mais popular do mundo.

A sétima edição do É da sua contafala sobre a falta de transparência em transações milionárias, negócios suspeitos, paraísos fiscais e como funciona a indústria de sonegação de impostos no mundo do futebol.

Um intermediário da Confederação Brasileira de Futebol conta como são as transações dos jogadores de futebol entre clubes; quem ganha quanto e como se paga impostos sobre esses valores.

Veronica Grondona, da Tax Justice Network, explica o negócio do futebol nos paraísos fiscais.

O advogado do português Rui Pinto explica os motivos de sua prisão em Portugal. Também conhecido como John do Football Leaks, Rui Pinto denunciou esquema de corrupção e sonegação fiscal envolvendo clubes internacionais. A ativista e diplomata Ana Gomes questiona a vontade política das autoridades portuguesas em combater a corrupção e a sonegação fiscal.

As dívidas tributárias de mais de US$ 600 milhões dos maiores times brasileiros.

Como a sonegação fiscal virou um negócio às avessas e o que fazer para corrigir, com Marcelo Lettieri da Instituto de Justiça Fiscal

O que pensam os amantes do futebol sobre o poder do dinheiro no esporte?

Onde pagam impostos os jogadores de futebol africanos que vão pra Europa? Comentário de Nick Shaxson, da Tax Justice Network

Call to action: O mundo do futebol precisa de mais transparência fiscal. Caso queira manifestar solidariedade ao denunciante do Football Leaks, siga-o no twitter Rui Pinto

We blogged recently that the UK’s main opposition party has committed to introducing unitary taxation by the end of the next parliamentary term. As we’ve said, it represents an important further normalisation of unitary taxation, and a potentially important step to ending the great damage done by corporate tax abuse internationally. In addition to our infographic here explaining unitary taxation, we think it’s useful to share an article for Open Democracy by one of our senior advisors, emeritus professor of law at Lancaster University, Professor Sol Picciotto. He was co-author of an important report whose recommendations have been adopted by the UK Labour Party.

In this article Professor Sol Picciotto addresses two important questions: could a UK government implement unitary taxation, and what would be the benefits? As he writes in his article:

adoption by a country such as the UK of a policy of moving towards unitary taxation with formula apportionment could accelerate the growing momentum for a more effective and comprehensive international solution. Indeed, earlier this year the Indian government put forward proposals to adopt fractional apportionment unilaterally, explaining how it could be compatible with its tax treaties. Even if not all countries follow, governments bold enough to lead the way could create a new consensus for reform of the rules to make them fit for the 21st century.”

In his view, unitary taxation is

a bold, visionary plan for taxing multinationals from the Labour Party – but it is also workable and necessary.”

You can read his full article here on the Open Democracy website.

Coauthors: Andres Knobel, Markus Meinzer and Moran Harari

The

Financial Action Task Force (FATF) which evaluates countries on their

compliance with its anti-money laundering recommendations recently published a

report on best practices of beneficial

ownership for legal persons, leaving trusts aside. The report contains interesting examples of

countries doing exactly what our paper on beneficial ownership verification proposed, but misses the point on

the issue of beneficial ownership registries, let alone public ones. While the

paper proposes many measures that we agree are useful and necessary, it fails

to endorse the most critical of measures: public beneficial ownership

registries.

Recommendation 24 (not 10)

While many

FATF recommendations refer to beneficial ownership information such as

Recommendation 10 on customer due diligence by financial institutions, this new

FATF paper on best practices (as well as most of our papers on beneficial

ownership) focuses on FATF Recommendation 24. This recommendation is about making

sure authorities’ have access to accurate beneficial ownership information. If

you want to see how the measures proposed here relate to Recommendation 10,

scroll down to the bottom of the blog post.*

The multi-pronged approach

The FATF Recommendation

24 and the OECD’s Global Forum allow countries to choose at least one of the three

following approaches to ensure timely access to accurate beneficial ownership

information: the registry approach (eg a beneficial ownership register), the

company approach (the legal person collects beneficial ownership and makes it

available to authorities on request), and the existing information approach

(use any beneficial ownership information available with banks, corporate

service providers, tax authorities, land registries, etc).

The FATF

paper on best practices describes the challenges faced when implementing each

of the approaches without endorsing any specific one as the best one. To us,

this is like if a teacher gave two students the same grade on a test because they

both answered the same number of questions, regardless of whether they answered

the questions correctly.

In reality,

the three approaches were never on equal footing because the company approach

is a pre-requisite for the other two.

The company

should always be required to identify its own beneficial owners and only then it

can report this data to a registry (registry approach) or to a bank or

corporate service provider (existing information approach) – or keep it to

itself (just company approach).

To

illustrate, let’s play out a scenario where a company would not be required to

identify its own beneficial owners:

Company A

walks into a bank to open an account.

Bank teller: “Hello Company A, please tell me

who your beneficial owners are.”

Company A: “I don’t know (and I don’t need to know).”

Bank teller: “Oh, sorry to bother you.” Then, asking in every direction: “People of the world, are any of you the beneficial owners of Company A? In such case, please identify yourself.”

While this

imaginary dialogue would never take place, Germany implicitly requires this by waiving the

company’s obligation to identify its beneficial owners, when a German company

is owned by at least two layers of foreign entities.

The new FATF paper now proposes the “multi-pronged approach” to ensure beneficial ownership transparency. In other words, it suggests implementing more than one approach out of the three possible ones because this has proven to be more effective compared to choosing just one of the three. We discuss the pros and cons of each approach below. However, from our perspective choosing a combination of any two out of three approaches is not good enough. We believe the company approach and registry approach must always be implemented together as a first step. This would constitute the bare minimum requirement. The existing information approach should only ever be implemented as a second step to cross-check, complement and verify the information retrieved by the first step.

The company approach

We consider the company approach to be a pre-requisite for any of the other approaches because the company is in the best position to identify its own beneficial owners, and maybe the only actor capable of doing so. However, relying on the company itself as the only source for authorities to access accurate and timely beneficial ownership information is risky, to say the least. A company investigated for money laundering may never reveal the beneficial ownership data when requested by authorities (especially if they have no presence in the country nor local natural persons who are liable for not complying with the law). In addition, even if we assumed all companies to be honest, ensuring access to beneficial ownership information on any company would mean supervising every local company at their office and checking that they do have beneficial ownership data. This could include millions of companies. The alternatives, sample audits or harsh sanctions for non-compliance, can only get so far. While these alternatives may encourage companies to comply, authorities wouldn’t be able to know for sure that they are complying, unless they checked each and every one of them.

The existing information approach

The

existing information approach seems comprehensive, because it may cover

anything: banks, lawyers, tax authorities, real estate registries, commercial

databases – anyone who may have beneficial ownership information on a company. But,

and this is a big but, it relies on information actually existing.

Local banks

may be required to obtain beneficial ownership information from companies, but

first a company must have engaged with a bank, eg opened a bank account.

Otherwise, the bank will have no beneficial ownership information on that

company.

Tax

authorities may be required to obtain beneficial ownership information from

companies, but first a company must be considered tax resident in the country (depending

on local tax laws) and actually filing the necessary returns with tax

authorities Otherwise, tax authorities will have no beneficial ownership information.

In other

words, the existing information approach is like a country trying to identify

its citizens solely on circumstantial identities: a credit card, a driver’s

license, a library card, a student id, etc. The country would be able to

confidently identify a person who has all those documents, but what if the

person does not have a credit card or driver’s license, and is not a student at

any school? There would be no data on the person at all for the country to

identify them by.

Even if every

company did engage with either a local bank, notary, tax authority, land

registry or any entity required to collect beneficial ownership information, a

second problem remains: enforcement would still require checking hundreds to thousands

of banks, lawyers, notaries or registries that may or may not have beneficial

ownership information. Sample audits or sanctions would again create

incentives, but they would not rule out the possibility of non-compliance.

Lastly, private

actors that hold beneficial ownership information could tip off their clients

about authorities asking for their information, which could affect

investigations.

The registry approach

The

registry approach is the only way to ensure that beneficial ownership

information has been collected (and registered). The registry would hold information

on all companies that were incorporated in the country, and could simply check

whether they filed beneficial ownership information or not. For a

well-functioning beneficial ownership registry, sample tests may not be

necessary: the registry, especially if it has digital records, would be able to

look at every local company (even if there are millions of them) and check if

they have filed beneficial ownership information or not. There would be only

one place to go instead of hundreds to millions and if information is

digitalised it would take a few seconds to bulk check if any company is missing

their beneficial ownership form.

From our

perspective, the registry approach doesn’t necessarily require the commercial

registry to be the body that holds beneficial ownership information. Any

authority would do: tax authorities, central bank, etc, as long as each and

every company has to file beneficial ownership information with that registering

authority. In other words, the registry approach assumes that an authority

holds information on all companies. Instead, if filing beneficial ownership with

an authority were optional, conditional or circumstantial, we wouldn’t consider

a country to be implementing the registry approach. At best, it would be

implementing the existing information approach. What differentiates both

approaches is not only whether an authority or a private party holds the

information, but also making sure that information on all entities is available

with the authority – not just on those companies that circumstantially had to

file information. You could think of the registry approach as the ‘leave no one

behind’ approach.

Nevertheless,

if beneficial ownership information is held by the commercial registry, it is

much more likely that the information could be made publicly accessible than if

it were held by tax authorities or the central bank.

On a

separate note, verification of information is of course not ensured by just having

a registry, although once verification procedures are implemented by the

registry, it is much easier to check if they actually took place. In contrast,

if banks, companies or other data holders are required to not only collect but

also verify beneficial ownership information, authorities would still have to do

checks to ensure that both the collection and verification took place.

The ideal approach

While the

FATF paper identifies the structural problems of each approach (eg companies’

lack of incentives to identify their beneficial owners), it still allows

countries to choose any approach. In our view, the ideal solution is the

FATF establishing the three approaches as successive building blocks to ensuring

authorities’ access to beneficial ownership information.

In essence,

the most fundamental component (in bold in the figure above) is the registry

approach, with the company approach (the company identifying its beneficial

owners) as a pre-requisite. If all beneficial ownership information is

contained in one central registry, it’s possible to easily access it whenever

needed, and to verify compliance and the accuracy of registered information,

even before the information is needed (before it’s too late). This also helps

foreign authorities access and verify information, who would otherwise have to

spend time in justifying a request for information and wait until it is

received, if ever at all.

The

existing information approach definitely adds value, but it should only be the

cherry on top. Banks, corporate service providers, notaries and even other

authorities dealing directly with the company should be able to obtain

information from the beneficial ownership registry while having the

obligation to report any discrepancy (eg “John doesn’t appear as the

beneficial owner in the Registry but he is the one who manages the bank account

and withdraws money, so he should be included”).

The law

could also require engaging with a bank, notary or a corporate service provider

in order to incorporate a company (the dotted arrow in the figure above) to add

an extra layer of verification and control of beneficial ownership information.

However, a country choosing only the “company + existing information approach” as

a way to ensure authorities’ access to beneficial ownership information (without

the registry approach) would be missing out. First, it would depend on the

company actually engaging with a local bank, notary or service provider for

these to hold beneficial ownership information. Otherwise, no one in the

country would know who the beneficial owners are. Second, it makes enforcement

much more difficult and costlier: supervisors would have to check every single

notary, bank or corporate service provider to make sure that they are doing

their job right.

The

registry approach should thus be promoted as the best approach (considering the

company approach as a pre-requisite). The FATF already requires countries to

have registries providing basic company information (company name, address,

etc). Upgrading the registries to also collect beneficial ownership information

is much more cost-efficient in the long-run than having to supervise the

hundreds to thousands of banks, notaries, lawyers and corporate service

providers.

Public registries

The FATF –

in our view – fails to endorse public beneficial ownership registries as the

best strategy to ensure beneficial ownership transparency, and it even seems to

undermine them:

For example, an openly

and publicly accessible central registry does not necessarily mean that the

information is accurate and up-to-date. (page 22)

This

statement is true, but also misleading. Establishing an under-resourced

registry that is unable to run any checks or verification and rather acts as a

repository of information could end up being of little value. But the same

applies to any measure that a government could implement. If you do something

wrong, or only half-way, of course it will not be effective. The point is which

approach (or combination of approaches) is better, if done properly. For

example, we published a checklist for any country willing to

implement a beneficial ownership registry. More fundamentally perhaps, the FATF

fails to take into account the pressures arising from public scrutiny of the

data. The use (or abuse) of low level staff (natural persons) as “premium” nominee

shareholders and directors whose identities are effectively stolen or hijacked

by superiors in hierarchical law firms (as happened in case of the Panama Papers), could be detected more easily if

public scrutiny allowed questioning the veracity of a person – not least from

within the firms, but also from any business partner and journalist.

On the

bright side, the FATF acknowledge a positive trend towards public beneficial

ownership registries, which also helps foreign investigations:

The trend of openly

accessible information on beneficial ownership is on the rise among countries. (page 74),

…it is also understood

that countries have encountered difficulties in getting information on

beneficial ownership that is not publicly available. (page 70)

Highlights

The FATF

paper does have some interesting pieces of information as described below.

Switzerland applying the “every shareholder is

a beneficial owner” (no threshold approach) to domiciliary entities

The FATF

paper describes that financial intermediaries in Switzerland are required to

obtain information from all individuals without applying the 25% threshold of

capital or voting rights when dealing with domiciliary entities (companies

as entities such as legal entities, trusts or foundations, that do not have any

operational activity):

A written declaration will be required from the domiciliary concerning

its beneficial owners. (Art. 4 para. 2 of the Federal Act on Combating Money

Laundering Act and Terrorist Financing). The threshold of 25% of the capital or

voting rights in the legal entity does not apply to such type of entities. This

means that all beneficial owners must be identified, regardless of the amount

of their participation in the company (page 55)

Countries implementing automated verification,

red-flagging and appropriate sanctions

The FATF

paper mentions many strategies to verify beneficial ownership information based

on some countries’ experiences. These include automated cross-checks against

other government databases to determine the accuracy of information, and using

data mining to establish patterns and red-flag suspicious cases. These

suggestions and examples are exactly what our paper on beneficial ownership verification proposed back in early 2019 (as

well as our paper’s previous version from 2017).

In

addition, whenever inaccurate or incomplete information was detected, our paper

proposed not allowing an entity to be incorporated, or winding it up if already

existed, or at least marking it with a warning for anyone to be aware of the

risk. The FATF paper describes that some countries are doing precisely this. Below

are some extracts from countries.

Austria

Austria requires

different measures to verify beneficial ownership information, including

automated real time cross-checks against government databases, automated

sanctions in case information is missing, adding a public remark to warn users

that a company has potentially incomplete or wrong information and a system of

risk points for non-resident beneficial owners based on their country of

residence’s risk, resulting in further investigation by Austrian authorities:

Legal entities, which report beneficial owners with foreign

citizenship or place of residence, or ultimate legal entities with a registered

address in a foreign country will receive a certain number of risk points based

on the ISO Code of the foreign country. Thus, those legal entities will be more

likely be in the risk category high or very high, resulting in a greater chance

that the BO Registry Authority will request documentation on beneficial

ownership and will carry out an off-site analyses of beneficial ownership.

(…)

Through an automated alignment with other registers, it is ensured

that beneficial owners and legal entities can only be reported if their data is

also contained in other public registers. If, for example, a person with a main

residence address in Austria is entered as a beneficial owner, there is a real

time check with the Central Residence Register in the background if the entered

person has a valid main residence in Austria. (…)

By setting a

remark the legal entity will automatically be notified about the remark

(without identifying the obliged entity that set the remark) and informed that

the reported beneficial owners could not be verified and that the legal entity

therefore has to examine its report. The remark is only removed if the legal

entity then files a new report. However, the remark will still be visible in

the historical data. Consequently, a remark will be visible in all excerpts

from the BO Register. In addition, the BO Registry Authority is monitoring the

list of all remarks set in the register and may request documentation on

beneficial ownership if a remark is not resolved by a correct report.

Implementation of automated coercive penalties. If a report is not

filed within the deadline – either within the initial reporting period or within

28 days of newly established legal entities – then the competent tax office

will automatically send a reminder letter with the threat of a coercive penalty

of € 1 000 to the legal entity. (pages 41, 46, 52, 57)

Denmark

Denmark also has automated cross-checks, including validation

checks (eg to prevent dead people from being registered). If beneficial

ownership information is not checked, a company will not be able to

incorporate:

The CVR

automatically checks information that is filed (which must be done

electronically), and will cross-check this information with various

governmental registers, the CPR number – Civil registration number / CVR number

– Unique identification number for legal entities and other details such as

address (Danish Address Register – DAR) and dates. Furthermore, business rules

are set up in the system to avoid impossible situations ex. registration of a

deceased person, and as the Business Register entails information about legal

entities, certain information about the entity is prefilled in order to ease

the registration and to avoid mistakes. These automated checks are then

followed by more detailed manual checks in suspicious cases. The system is also

designed to use large datasets and with machine learning to better identify

potential risks (….)

If the BO

information is not adequate when checked, the company will not be incorporated.

If the BO information is checked in the following phase, the DBA has the legal

basis to dissolve the company compulsorily (page 48)

The Netherlands

The Netherlands has automated cross-checks against government

databases, a risk system for further investigations and creates a network maps

of relevant relationships that could be used for investigations:

The Scrutiny,

Integrity and Screening Agency performs risks analysis by automatically

scanning several closed and public sources on a daily basis, to look for any

relevant financial or criminal records of directors, and the (legal) persons in

their immediate surroundings. Data includes the Company Registry, Citizens

Registry of the municipalities and the Central Insolvency Registry, as well as

other public sources. In addition, data is obtained from the tax authorities,

the Judicial Information Service, and the National Police Services Agency. If the

computer system reveals a heightened risk, either immediately upon registration

or later on, during the life span of the legal person, this dedicated Agency

will carry out a more in-depth analysis. If the analysis confirms that there is

indeed a heightened risk, a risk alert will be sent to a group of recipients,

including law enforcement and supervisory authorities such as the Public

Prosecution Service, the Police, the Tax Intelligence and Investigation

Service, the Dutch Central Bank, the Netherlands Authority for the Financial

Markets and the Tax and Customs Administration (.…)

The

Scrutiny, Integrity and Screening Agency also provides ‘network maps’ for inter

alia law enforcement and supervisory agencies. A network map plots the relevant

relationships between a (legal) person of interest, and other persons or legal

persons, including bankrupted or disincorporated legal persons. (page 50)

Other relevant cases of beneficial ownership verification include

Belgium (page 47), Italy (page 34), Jersey (page 36), Spain (page 40) and

Sweden (page 52).

Proposals

on how to deal with foreign companies

The FATF paper also includes proposals on how to deal with beneficial

ownership from foreign companies. While the paper doesn’t mention (our paper’s)

proposals on an automated international cross-check of information using

zero-knowledge proof tests (without needing to share the actual data with a

foreign country, but only confirming information), it does present valuable

options that require no international cooperation:

b) Rating jurisdictions’ level of co-operation – Rating

jurisdictions based on the availability and extent of their co-operation. Impose

defensive measures such as restriction of certain business activities

accordingly.

c) Requiring re-registration with a local beneficial ownership.

d) Requiring

re-approval by domestic national authorities based on detailed investigation of

the relevant legal entities. (page 70)

Option b echoes our paper’s proposed quality limits (limiting the

ownership chain of a local company by allowing it to include only foreign

entities as long as they are from countries that have public legal and

beneficial ownership information). Of course, the Financial Secrecy Index could be

a basis and source of evidence to know whether a country’s entities should be

blacklisted based on the country’s level of transparency and exchange of

information.

Need to

review data protection and privacy laws that affect access to information

Importantly, the FATF paper refers to the need to revisit data

protection and privacy laws. While these are of course relevant, they should

not be abused to prevent relevant authorities and stakeholders from accessing

beneficial ownership information:

It is also

expected that countries will take action to facilitate the timely sharing of

basic and beneficial ownership information at the domestic and international

level to address barriers to information-sharing (e.g. reviewing data

protection and privacy laws). (page 72)

Our 2017 guidance paper on a checklist

for beneficial ownership registries specifies the importance of allowing

information to be searched using different fields (company name, incorporation

date, identity of owners, their residence, etc (page 5). The FATF paper also

proposed this:

Information

in the company register is generally recorded digitally and is preferably

searchable. The search function supports searches by multiple fields. (page 73)

Conclusion

In conclusion, the FATF paper proposes many measures that we agree

are useful and necessary. It also describes best cases available in several

countries that could be followed by others. However, it fails to endorse

registries of beneficial owners, let alone public ones, as the best approach.

* How does

this blog post’s proposals relate to FATF Recommendation 10?

Another

relevant FATF recommendation, which is related but not the focus of this paper,

is Recommendation 10 on customer due diligence: how banks, and other obliged

entities (eg lawyers, notaries, corporate service providers, etc) are supposed

to obtain and verify information, including beneficial ownership information,

provided by their customers. For example, when opening a bank account for a

customer, banks and other obliged entities may use information from the

commercial registry or beneficial ownership registry (green circle in the

figure below), but they cannot rely exclusively on that information for their

customer due diligence obligations. They must use other sources too, and follow

other procedures (eg obtain identity documents, in-person meetings, etc) to

comply with Recommendation 10’s procedures.

However,

this blog post doesn’t apply to Recommendation 10, and none of its observations

or proposals refer to changing Recommendation 10 in any way nor obliged

entities’ customer due diligence obligations. This blog post focuses only on

Recommendation 24 about ensuring access to beneficial ownership information by

authorities (and ideally also by the public).

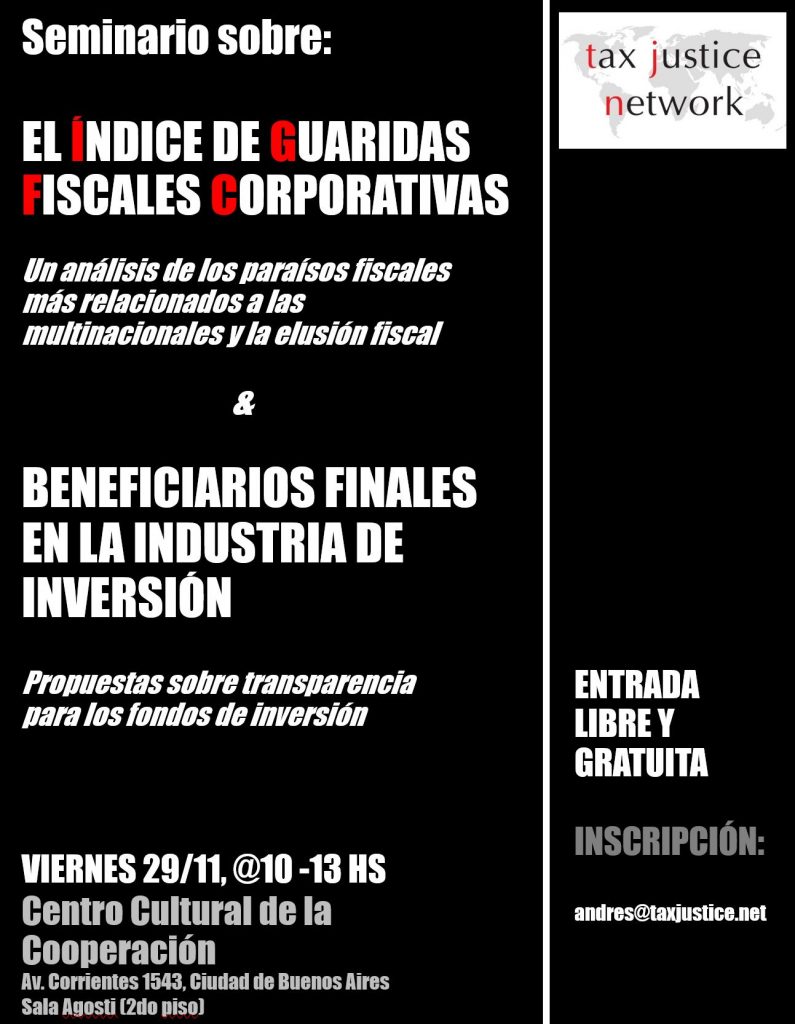

The research and advocacy seminar is organised in the context of the conference “Financialization in the Global South” (list of panels here, time table here, register here), happening from 26-28 November 2019 also in Buenos Aires. This event is free to attend. Details and location can be found below.

The seminar introduces the methodology and discusses

the research and advocacy potential of Tax Justice Network’s Corporate Tax

Haven Index (CTHI). This index combines two measures to create a ranking of the

world’s most important tax havens for multinational corporations: the Haven

Score based on 20 mostly tax-related indicators of corporate tax haven-ness,

assessing how aggressive a jurisdiction’s corporate tax haven laws, regulations

and practices are; and the Global Scale Weight showing the scale or size of

corporate investment activity as a proxy for the magnitude of the

profit-shifting potential in that jurisdiction. The jurisdictions are ranked by

how much each contributes to tax avoidance risks and the race to the bottom in

corporate income taxation. The Haven Score’s twenty indicators rely on in-depth

policy analysis in five relevant areas of corporate tax policies: the lowest

available corporate income tax rate; loopholes and gaps; transparency;

anti-avoidance measures and double tax treaty aggressiveness. Researchers and

members of social society are invited to feedback on the methodology, and to

contribute suggestions for the future geographical expansion of the index in

the Latin American region.

Another part of the seminar will introduce the present

the Tax Justice Network’s latest paper on the risks emanating from the secrecy

in the investment industry. In 2018, the total value of financial instruments

processed in the US was USD $1.85 quadrillion (USD $1,850 trillion). Still,

there is no transparency on who the beneficial owners of investment entities

and financial assets are, let alone if they are paying the corresponding taxes

or if they are part of money laundering or other financial crimes. Neither

current beneficial ownership registries nor the Common Reporting Standard for

automatic exchange of tax information solve the investment industry’s secrecy.

Seminario de presentación e investigación del

Índice de Guaridas Fiscales Corporativas 2019

El propósito del seminario es introducir la metodología, presentar y

discutir la investigación del Índice de Guaridas Fiscales Corporativas de Tax

Justice Network (CTHI, por sus siglas en ingles). El índice combina dos medidas

para crear un ranking de las más importantes guaridas fiscales para

corporaciones multinacionales del mundo: un ranking de guaridas basado en 20

indicadores de nivel de guaridas principalmente relacionadas con impuestos, que

evalúan que tan agresivas son las leyes, regulaciones y prácticas de una

guarida corporativa; y un ponderador de escala global que muestra la escala o

el tamaño de la inversión extranjera directa como un proxy de la magnitud del

desvío de utilidades potencial en la jurisdicción. Las jurisdicciones son

posicionadas en función de cuánto contribuyen al riesgo de elusión fiscal y a

la carrera a la baja global en el impuesto a las ganancias corporativas. Los

veinte indicadores del índice de guaridas se basan en un análisis detallado de

políticas en cinco áreas relevantes de las políticas de fiscalidad corporativa:

la menor tasa imponible disponible; los huecos para la elusión fiscal; la

transparencia; las medidas anti-elusivas y la agresividad de los tratados de

doble imposición. Académicos, miembros de la sociedad civil, y otras personas

interesadas están invitados a proveer su opinión respecto de la metodología y

contribuir con sugerencias para la futura expansión geográfica del índice en la

región latinoamericana.

This month on the Taxcast we speak to Tax Justice Network CEO Alex Cobham about his new book The Uncounted on the politics of counting. Who’s missing from the stats, from the bottom to the very top? And how can we count better?

Plus: For decades corporate tax cuts have been touted as the way to boost the economy. This month the Tax Justice Network’s John Christensen talks about a paradigm shift on corporate tax in the UK general election: and we look at the results of Trump’s corporate tax cuts in the US – what did they really deliver?

If the rich, if the elites, if the big companies are obviously not meeting their fair share, not meeting their part of the social contract, why should I? And you know, why should I be the only mug who pays tax? And it erodes all the way down. And this is how States and societies crumble.”

~ Alex Cobham

“Neo-liberalism is finished, it’s a busted flush, we’re going to see a change, if not at this election it’s certainly coming and I have the same sense from the US. And the tax justice agenda will feature prominently in whatever comes next”

~ John Christensen

Want to download and listen on the go? Download onto your phone or hand held device by clicking ‘save link’ or ‘download link’ here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher.

Join us on facebook and get our blogs into your feed.

The Labour party in the UK has today committed to introducing unitary taxation by the end of the next parliamentary term. This is significant internationally because it marks the first such manifesto commitment from a major political party, with a realistic prospect of election success, in a major OECD member country. Coupled with the leadership of the G24 group of developing countries, the Labour commitment represents an important further normalisation of unitary taxation, and a potentially important step to ending the great damage done by corporate tax abuse internationally.

But what is unitary taxation? We’ve put together an infographic below to illustrate how unitary tax works.

Under a unitary tax approach, governments treat a multinational corporation as a group made up of all its local branches, instead of treating each local branch as an individual entity separated from the global chain. The profits that the multinational corporation declares as a group are then apportioned to each country where it operates based on how much of its real economic activity took place in that country.

Simply, put a unitary approach requires multinational corporations to contribute tax based on where they employ workers and do business, not where they rent letter-boxes and hide ledgers. That means making sure corporations pay their fair share locally for the wealth created locally by people’s work.

Today sees

the crystallisation of two potentially pivotal moments in the development of

international tax rules towards the Tax Justice Network’s long-favoured

approach: unitary taxation.

In Paris, the OECD is hosting a public consultation on the biggest reform to the taxation of multinational companies in almost a century – and there is a growing demand for a comprehensive shift to unitary taxation. And in London, the UK Labour party has today become the first major political party in one of the world’s leading economies to make a manifesto commitment to introduce unitary tax.

What is unitary taxation?

Unitary taxation is the approach that treats a multinational group as the taxable unit, rather than the individual subsidiaries in different countries that make up the group. Current international tax rules are based on separate entity accounting, where transfer pricing mechanisms are used to establish the taxable profit that each entity within the multinational group would obtain, if it was operating at arm’s length (independently) from each other entity in the group. This allows gross abuses, with huge volumes of profits being shifted from where they arise, into low- or no-tax jurisdictions. Unitary tax recognises that in reality, profits are maximised at the unit of the group as a whole. ‘Formulary apportionment’ is the name for the process that allocates those global profits as tax base between the different countries where the multinational has real economic activity (employment and final customer sales, say).

The OECD Base Erosion and Profit Shifting (BEPS) process of 2013-2015 had the single, agreed goal of reducing the misalignment between where profits are declared, and where multinationals’ real economic activity takes place. BEPS failed because OECD countries could not agree to move beyond the arm’s length principle. But the new reforms, sometimes dubbed BEPS 2.0, start from an explicit acceptance of the need to move beyond arm’s length pricing. Each of the proposals under consideration include aspects of unitary taxation, of which the proposal from the G24 group of countries is the most comprehensive. The Tax Justice Network has long called for such a reform, estimating the failure to align profits with the location of real economic activity imposes global revenue losses of around $500 billion each year.

What’s at stake at the OECD?

The OECD consultation addresses ‘pillar one’ of the

organisation’s policy reforms. While pillar two focuses on the introduction of

a global minimum tax rate for all countries, pillar one is concerned with the

distribution of the tax base between countries. This is crucial to ending the

corrosive practices of profit shifting, through which multinationals, their

professional advisers and corporate tax havens such as the Netherlands have

conspired to deny taxing rights to the countries where companies’ real economic

activity takes place.

The

consultation addresses the ‘unified proposal’ put forward by the OECD

secretariat, which was put forward following bilateral agreement between the US

and France, and then received support from the G7 group of countries before

being made public. The proposal claims to combine elements of the three

proposals that are in the agreed work programme of the Inclusive Framework

group of 134 countries. All three move beyond the arm’s length principle and

the transfer pricing approaches that have dominated international tax rules

since the key decisions of the League of Nations in the 1920s and 1930s.

The

Inclusive Framework group includes many lower-income countries, not only OECD

members, and they have been promised an equal say in the changes to be made.

However, the unified proposal sets aside entirely the one approach in the work

programme that had been proposed by lower-income countries: the proposal for

unitary taxation made by the G24 group. Our analysis indicates that compared to the G24

approach, the unified proposal would be likely to redistribute a much smaller

volume of profits away from corporate tax havens, with much smaller revenue

gains for other countries – especially non-OECD members. Simulations for the French government, just published, confirm “a negligible impact on tax

revenues” is likely.

From our

partial review of the thousands of pages of submissions now made public, a number of key

points stand out. These can be grouped into areas with broad consensus, and

areas where business and other respondents are relatively sharply divided. We

identify three areas of relatively broad consensus:

Scope. There is a near-universal

rejection of the OECD secretariat’s proposed scope. While most independent

submissions criticise aspects of the attempt to reduce the scope to only the

largest, ‘consumer-facing’ businesses, with a range of other industry carve-outs,

most business submissions seek a more limited scope, higher size thresholds,

and where relevant that their own sector be excluded through an additional

carveout.

Complexity

and uncertainty.

An overwhelming share of submissions reviewed, and from all types of

participants including business and civil society, highlight the risk that the

OECD secretariat proposal would increase complexity of the rules and

uncertainty of outcomes for taxpayers and tax authorities.

Impact

assessment. Across

all types of respondents, there is a clear desire for the OECD to release data

and analysis on the projected revenue impact of the proposals. Civil society

has made this a core demand. The US Chamber of International Business said: “USCIB

members believe a completed impact assessment is critically important to enable

progress on the proposed Unified Approach framework.” The intergovernmental

South Centre said: “The South Centre supports the call for the OECD to make

public its country-by-country reporting data on MNEs headquartered in its

member states so that countries can carry out a more thorough assessment of how

the Unified Approach proposal will affect their tax base. At present the OECD

has planned to release this data only after early 2020, potentially after key

elements of the reform proposals have been pushed through.”

In areas

with a divide between business respondents and others, we identify four main

areas:

Curbing

profit-shifting. There

is little engagement from business respondents or their professional services

providers with the question of whether the reforms would reduce the scale of

tax abuse. The major lobby group Business at the OECD (BIAC) goes so far as to

ask that the label ‘BEPS 2.0’ not be used for the process: “that language is

quite unhelpful and, indeed, misleading.

Pillar 1 is – should be – about constructing a new tax system for new

business models and a new economy. That

needs to be a tax system which takes account of the way business is working

(and even more importantly, will come to work); a system that allows

governments to raise money based on new value-creating forms of activity; but

also a system that fosters and enhances cross-border trade and investment and

creates inclusive growth. To impose an anti-avoidance narrative on Pillar 1

could frustrate that.” Non-business respondents, meanwhile, consistently

criticise the proposals for the likely failure to address the scale of profit

shifting.

Fair

distribution of taxing rights.

Here again, there is little engagement from business respondents and their

professional services providers, but a clear consensus among civil society

respondents and those from non-OECD countries that the secretariat proposal will

not redress the stark inequalities in taxing rights that characterise the current

system.

‘Equal

say’. A position

common to many of the civil society responses and those from non-OECD

countries, is to highlight the extent to which the OECD secretariat proposal

has disregarded the key tenets G24 approach, casting doubt on the commitment to

give non-OECD countries an equal say.

Dispute

resolution. Here

is perhaps the sharpest divide. While many business respondents call for rapid,

binding arbitration, often conditioning acceptance of any other changes on

this, it is anathema to respondents from non-OECD countries and to civil

society – often appearing to be a red line, even if other elements of the

proposal were to be accepted.

Where next?

Three main

outcomes can be envisaged. First, and perhaps most likely given the recent

history of the BEPS project (2013-2015), is that the OECD delivers a limited

reform meeting the constraints of major members including the US, which neither

curbs profit shifting to a significant degree nor provides substantial benefits

to Inclusive Framework members.

In this

scenario, trust in the OECD to act as the forum for international tax

rule-setting would be damaged perhaps to the point of being beyond repair. The

power of major OECD members, however, might be enough to prevent any shift of

forum to the UN. That would leave countries with the option of pursuing

unilateral measures, from the digital services taxes that are already

proliferating, to more comprehensive unitary tax approaches. The resulting

pressure from business for an international solution would likely see a quick

return to negotiations – but would they be at the OECD?

A second

scenario sees the current process collapse, due to the lack of trust. Here, a

move to the UN becomes conceivable, if major OECD members were to accept that a

more genuinely inclusive process was necessary since unilateral proliferation

would not represent a stable equilibrium. Again, a return to the OECD process,

or the start of a new one, would seem more immediately likely than a shift to

the UN; but the quid pro quo to achieve this might be a much more serious

commitment to the ‘equal say’ for non-OECD members.

The third

scenario is that the current OECD process is reset. Recognising the depth of

opposition to the secretariat proposal, key actors might decide that the aim of

completing the process during 2020 is incompatible with a full assessment of

the options and obtaining broad agreement. That would in turn open the door to

more serious consideration of the Inclusive Framework’s three approaches,

including the G24 proposal.

The

starting place is the recognition in the current process that the old transfer

pricing rules are not fit for purpose in an age of complex globalisation. In

each of three scenarios, the medium-term prospects are increasingly positive

for a complete shift to a unitary approach – whether led by the OECD or UN, or

simply as the result of cumulative, unilateral actions.

Unitary

taxation has moved from a radical civil society demand in the early 2000s, to

being a core element of the international policy debate today. It offers the

potential to reprogramme international tax, making profit shifting abuses of

multinational companies a marginal problem rather than the major cause of

revenue losses that they are today.

What’s the Labour manifesto commitment?

In the UK, the Labour party has today committed to introducing unitary taxation by the end of the next parliamentary term. This is significant internationally because it marks the first such manifesto commitment from a major political party, with a realistic prospect of election success, in a major OECD member country. Coupled with the leadership of the G24 group of developing countries, the Labour commitment represents an important further normalisation of unitary taxation, and a potentially important step to ending the great damage done by corporate tax abuse internationally.

FAQ

How much revenue would the Labour policy bring in for the UK?

The Labour

party estimates that in the fifth year of the next parliament, the tax would

bring in £6.3bn. This comes from the work of Prof Sol Piccciotto, who is

perhaps the leading international expert on unitary taxation and a Tax

Justice Network senior adviser, and Daniel Bertossa.

Picciotto

and Bertossa lay out a full proposal, and refer to our

analysis (with

Prof Valpy FitzGerald of the University of Oxford, and Tommaso Faccio of the

University of Nottingham) of data on US multinationals for the revenue impact.

We found a revenue impact of nearly $4bn for the UK, from an international

shift to unitary taxation with full formulary apportionment. Scaling up to

include non-US multinationals, and depending on the approach taken, this

implies a total revenue gain of between £6bn and £14bn.

The Labour

party have taken the lower extreme of this range (i.e. the most conservative

estimate). They then reduce it by 30% to allow for possible behavioural changes

(multinationals moving away, or finding other ways to dodge tax). This seems on

the high side for a behavioural response, so this again looks a conservative

assumption. Finally, they roll forward five years, allowing for inflation. That

gives an estimate of revenue at the end of the next parliament of some £6.3bn.

Can the UK do this unilaterally?

Yes. Countries including OECD members have quite different approaches to international tax, whether in terms of defining the tax base or setting the rates, so there is no reason the UK couldn’t go ahead and do this. As above, however, there is an increasing chance that this would be in line with an emerging international consensus to adopt unitary taxation, so the UK could be well positioned to play a leading role in that process.

Wouldn’t the UK have to renegotiate all its double tax treaties?

Many believe that current tax treaties would not pose an obstacle, just as they already allow the application of related ‘profit split’ approaches. However, a renegotiation is not out of the question. The OECD secretariat has confirmed that its current, more complex proposal, for example, would require revisions to the whole global tax treaty network. As George Turner of TaxWatch has written, instead of renegotiating it is also possible for the UK parliament to “legislate to unilaterally disapply the provisions of tax treaties. This last happened in the UK in 2008, when the government legislated to unilaterally override all of their tax treaties to close down a disguised remuneration scheme (FA 2008 ss 58 and 59, which amended ICTA 1988). The action by the UK government was subsequently upheld by the European Court of Human Rights, which noted that double tax treaties should do no more than seek to relieve double taxation, and should not be permitted to become an instrument of avoidance.”

Wouldn’t multinationals leave the UK rather than pay this tax?

Multinationals

operate in the UK because they make money in the UK. A distribution of some

percentage of that profit towards the UK exchequer, just as any domestic

business makes, doesn’t stop it being profitable to operate in the country.

While there would no doubt continue to be a lot of work from professional

service firms including accountants and lawyers trying to game the system,

unitary tax offers a much simpler way to determine taxable profit than the

current rules and so is likely to be much less open to abuse. As noted, the

Labour party’s revenue estimate assumes a 30% reduction due to behaviour

change, which may well be on the high side.

Is the information available to make unitary tax work?

Yes. Following the G20 decision in 2013, the OECD has developed a version of the Tax Justice Network’s proposed standard for country-by-country reporting. This, together with corporate tax returns, provides all the information needed to apply unitary taxation. It would be advisable to ensure that the data to be relied upon is fully audited, and to sharpen the definitions in places to reduce scope for chicanery, but the instruments are in place.

As global capitalism continues to lurch from one crisis to the next, massive levels of tax abuse and avoidance are robbing governments of the resources they need to provide basic social services while also contributing to economic instability, fuelling gender inequalities and undermining human rights.

Nowhere is this systemic malaise more

manifest than in the extractives industry, which pillages the resources of

developing countries while offering them a pittance in return. Last year the 40

largest mining companies raked in US $683 billion, mostly from the Global

South, through the extraction of oil, gas and minerals. But rather than paying

their fair share of taxation to the countries where they operate, most

extractive companies channel their revenue through a complex network of

corporate tax havens and financial secrecy jurisdictions to avoid contributing.

Meanwhile, local elites in host countries collude in providing tax incentives

and low corporate tax rates to ensure these companies pay the absolute minimum

to local economies.

On 19 November hundreds of civil society organisations around the world will join forces to demand an end to this plunder. The Global Day of Action will see public protests, educational events and vigorous social media campaigning all over the planet as people who care about justice and equality unite their voices to say enough is enough. Organized by our sister organisation the Global Alliance for Tax Justice, this co-ordinated international effort represents a crucial opportunity for ordinary people everywhere to push back against the injustice of a global economy that has been programmed to rip them off.

This mass mobilisation comes in a context

of multiple enmeshed abuses being perpetrated by the extractives industry. The

sector is notorious for its role in human rights abuses, such as forced

displacement, the destruction of livelihoods and even, in some instances,

murder, not to mention fuelling climate change and widespread environmental

destruction. By confronting the abusive tax practices of the extractives

industry, the Global Day of Action will also aim to build solidarity with and

strengthen these ongoing battles for economic, social and environmental

justice.

The organisers have made an array of resources, including infographics, social media assets and press materials, available on their website to support all those who wish to take part. Here at the Tax Justice Network, we’ll be adding our voice to this important international call to action. While the Tax Justice Network relies on high-level technical analysis and advocacy to shine a light into the opaque structures that rig the global economy, we also recognize that this alone is not enough to transform the unjust international tax system. That’s why the campaigning work of the Global Alliance for Tax Justice, which spun off from Tax Justice Network in 2013, is so fundamentally important. We hope you will join us on 19 November to demand the global Goliaths of the extractives industry pay their fair share.

Welcome to this month’s latest podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónica!

Some troubling news you may not have heard about: recently United Nations staff were informed that the United Nations will run out of money due to a 30% underpayment by member states, most notably the United States: if that nation paid what it owed, that would make up at least 60% of the total unpaid contributions for 2019. Here’s a tweet thread which purports to show the text of an email sent out to staff by the UN Secretary-General, António Guterres:

In news of other diplomatic woes, UN staff were informed by email last night the organisation will run out of money by the end of October. @antonioguterres informed them that as a result of a 30% underpayment by member states (esp Trump administration) they are nearly insolvent.

The Tax Justice Network has long argued that the United Nations is a far more suitable and democratic forum for resolving international tax rules than the OECD, which we often refer to as a ‘rich countries club.’ The Tax Justice Network CEO Alex Cobham puts these failures to pay into an interesting context:

UN currently needs $230 million to keep functioning.

To put that another way, it's less than 0.05% of the $500bn in revenues lost to corporate tax abuse each year. (An issue the UN is not allowed to work seriously on, because OECD members would rather keep it in their power.) https://t.co/ReowhYmNm4

— Alex Cobham @alexcobham.bsky.social (@alexcobham) October 8, 2019

The United Nations Special Rapporteur on extreme poverty and human rights Professor Philip Alston raised the alarm on extreme inequality levels in the United States and in the UK. His evidence-based research was immediately rubbished by both the US administration and the UK government. Since President Trump was elected in the US, there has been a deliberate attempt to weaken an institution which has told some inconvenient truths to power.

We’re not saying that the UN is perfect. But we think it might interest citizens around the world to know whether or not their country has paid its 2019 contribution:

I interviewed Alex Cobham for the Tax Justice Network’s monthly podcast the Taxcast about his new book out this month, The Uncounted. That full interview will be released shortly in the November 2019 Taxcast, but we discussed this threat to the United Nations, and how a more stable future might be achieved. Here’s an audio clip here, followed by a transcript:

I don’t think very many people are actually seized of the urgency of this, I think because the UN seems very far away for most of us, but you know, there are two things at the moment that are really deeply concerning.

So on the one hand, you know, yes because of particularly the role of the US but actually quite a lot of other countries also not doing their bit, the UN is seriously underfunded and looking at having to make quite serious cuts. But actually because it’s only, only I say, missing a couple of hundred million dollars, right? Pretty small in terms of the national budget of lots of high income countries but big in terms of absolute amounts of money and you can see how that will impact very quickly on lots of people’s employment for example, but also on the organisation’s ability to do stuff.

But look, at the same time that the US in particular is effectively imposing deep cuts on the UN, the US is also blocking, in practical terms, all sorts of measures for progress and pushing through some quite regressive positions on things like women’s rights. How this country, or rather this country’s current administration, is being allowed both to starve the organisation of funds and to continue to exert a completely disproportionate amount of power is slightly mind-boggling.

And this doesn’t feel like a position that can continue. Surely it can do one or the other but not both. But ultimately what it points to in some ways is that we need to accelerate something that should have been happening anyway, which is thinking about how the UN becomes self sustaining.

It cannot survive, because good organisations do not survive on voluntary donations, because donations bring with them influence. And that’s as true for an organisation like the Tax Justice Network as it is for a government.

We know that governments that are more dependent on tax respond more to their own populations. Governments that have large natural resource wealth or aid flows become increasingly unresponsive to their people.

For the UN we need to think about countries making payments on a tax-like basis and with a social contract, countries having benefits that stem from their participation and therefore, you know, having some incentives to take part in that.

But, if the UN continues as I’m afraid it is currently, to look at private sector financing solutions for development and indeed, partnerships for itself, rather than seeing the literally hundreds of billions in revenues lost to avoidance and evasion as an obvious place for it to find the relatively small global budget that it needs, it’s kind of condemning itself to going further down this road.

I think that the people working on illicit financial flows need to start making the case very strongly within the UN that there are revenue streams here that would allow the organisation to have a basis of reserves, at least for a kind of independence that would stop it getting back into the situation that it’s got into now through the extreme behaviour of the Trump administration. Maybe there can be a silver lining if this kicks off some structural changes that make this impossible in future.

But right now everyone should be sounding the alert and asking their governments, their own governments, first of all, if they’ve made their contribution, because so many governments haven’t yet done their bit.”

We asked our newsletter subscribers to complete a short survey to help us make sure the Tax Justice Network is delivering the research, stories and opportunities that matter to them, in the ways that help them best engage in tax justice.

We’ve put together an infographic summarising what people said about our work and why tax justice matters to them. You can view the infographic below.

Based on people’s feedback, we’ve created a new supporter scheme for individuals who want to make a one-off or regular donation to the Tax Justice Network. Our supporters will help us to undertake our research and campaigns to expose corruption, fight vested interests and build a fairer global economy by providing us with predictable, unrestricted funding.

Fighting for tax justice

Corporations and wealthy elites have made historic levels of inequality possible by taking over the tax systems of countries around the world, turning tax policy into a tool that prioritises the interests of the wealthy instead of treating the needs of all members of society as equally important. The Tax Justice Network believes a fair world, where everyone has the opportunities to lead a meaningful and fulfilling life, can only be built when we each pitch in our fair share for the society we all want.

Every day, we equip people and governments everywhere with the information and tools they need to reprogramme their tax systems to prioritise the needs of all members of society, over the desires of corporate elites. We need your support, now more than ever, to continue the fight for tax justice. With your help, we need to raise £300,000 to continue our research, advocacy and communications work in 2020, as part of our four-year strategy.

Your donation will make a big impact. We estimate that every $1 invested in the Tax Justice Network may have yielded $1,000 in additional revenues for national governments to spend on reducing inequalities and building strong public services.

Welcome to the twenty-second edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. (In Arabic below) Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to post it. You can also join the programme on Facebook and on Twitter.

Taxes Simply #22: how socioeconomic demands are overcoming sectarianism in Lebanon and Iraq

In October 2019, large demonstrations broke out in Lebanon and Iraq, countries that are both governed by sectarian politics. But, this time economic demands have transcended sectarian rhetoric.

In this episode, Lebanese economic researcher Nabil Abdou explains what protestors mean by the “down with the rule of the bank” slogan, and how the tax system in Lebanon encourages rent-seeking at the expense of all other productive sectors. Abdou also explains how demonstrations in Lebanon are organically linked to demonstrations in other Arab and Latin American countries.

In the second part of the programme, we speak with one of the participants of the Iraqi uprising; journalist Karim al-Nur, about the economic motives driving his participation in the demonstrations.

الجباية ببساطة ٢٢ – تجاوز الطائفية بالمطالب الاقتصادية في لبنان والعراق

أهلا بكم في العدد الثاني والعشرين من

الجباية ببساطة. في شهر أكتوبر/تشرين اندلعت تظاهرات واسعة في كلا من لبنان

والعراق، وكلاهما بلاد تحكمهم وتتحكم بهم السياسات الطائفية، لكن هذه المرة جاءت

الكثير من المطالب اقتصادية الطابع متجاوزة الخطاب الطائفي. في هذا العدد نلتقي

بالباحث الاقتصادي اللبناني نبيل عبدو ليشرح لنا تحديدا فحوى شعار “يسقط حكم

المصرف” و كيف أن النظام الضريبي في لبنان قائم على تشجيع الريع على حساب أي

قطاعات منتجة أخرى، فضلا عن ارتباط التظاهرات في لبنان عضويا بتظاهرات في بلدان

أخرى من العالم العربي وأمريكا اللاتينية. في القسم الثاني نلتقي بأحد المشاركين

في الانتفاضة العراقية، الصحفي كريم النور، متحدثا عن الدوافع الاقتصادية لمشاركته

في التظاهرات.

Europe Needs a “Tax Justice Network for monopolies.”

Introduction

The BBC recently carried a short article which began:

“Luxembourg’s data privacy watchdog says it is in discussions with Amazon about voice recordings made of customers who have used the firm’s Alexa smart assistant. The regulator is the “Lead Supervisory Authority” (LSA) for the company in the EU, meaning that it co-ordinates investigations into the business on behalf of the other member states.”

You may have heard stories about Alexa listening in on users’ sex lives, its occasional bursts of creepy laughter, the peculiar jokes, the story of the customer who was reportedly told to “Kill your Foster Parents,” and more. So it’s heartening to think there’s a watchdog out there, keeping tabs.

But Luxembourg? Anyone familiar with tax havens knows immediately that this monster corporate tax haven is about the last place you’d want to host a watchdog to curb abusive behaviour by large multinationals.

For those unfamiliar with Luxembourg’s role as a criminalised corporate tax haven at the heart of Europe, it’s worth reading up about the “Luxleaks” scandal (revealing the world’s biggest multinationals using Luxembourg as giant corporate tax-cheat factory;) or pondering Luxembourg’s sixth-place ranking in both the recent Corporate Tax Haven Index (CTHI) and its sister ranking of shame, the Financial Secrecy Index. Luxembourg’s stance goes back decades: consider, for instance, its central role in Bernie Cornfeld’s crime-infested Investors Overseas Services, or in the scandal of the Bank of Credit and Commerce International (BCCI,) arguably the rottenest bank in world history; its key role in the Elf Affair, Europe’s largest corruption investigation since the Second World War, in the Clearstream Affair; in Bernie Madoff’s still-unresolved Ponzi-scheme frauds; or in the Icelandic Kaupthing saga. To name just a few. As a searing Financial Times analysis summarised in 2017:

Luxembourg sometimes resembles a criminal enterprise with a country attached.”

Luxembourg’s national development strategies revolve around ‘competing’ to attract footloose global capital and the operations of multinationals, essentially by offering them an easy ride on taxes, disclosure, financial regulations, and criminal enforcement. These strategies, which have been called the ‘Competitiveness Agenda,’ are always harmful: in Luxembourg they have created a state whose political and regulatory machinery is captured by banks and large multinationals it hosts. This ‘competitive’ approach applies to data protection, as companies “forum-shop” for the jurisdiction most favourable to data firms. An adviser to multinationals explains:

Sophisticated organizations are structuring their decision-making functions concerning data in a manner which reflects a preferred enforcement forum strategy. . . . EU attorneys are seeing data planning exercises, somewhat similar to tax planning structures, emerging.”

Alert: loose language! The word “monopoly” refers to a market where there’s just one seller. There’s also oligopoly (only a few sellers), monopsony (only one buyer,) and so on. “Market power” covers these terms – and perhaps “coercive market power” is clearer. Sometimes ‘monopolies’ will be used as a loose general term, even if not strictly accurate.

Anyone familiar with ‘tax competition’ – a central issue for the tax justice movement – will recognise this language. It’s offshore business: this time not for tax, but for big data.

The location of these European Lead Supervisory Authorities (LSAs) shows a familiar pattern. Where is the LSA for Google? Ireland, another gigantic corporate tax haven. Facebook? Ireland again. Uber? The Netherlands, ranked fourth in the Corporate Tax Haven Index. Airbnb? LinkedIn? Microsoft? Ireland. And if you move beyond these privacy and data issues, to (say) cryptocurrencies, you find that the jurisdictions seeking to get ahead are places like Malta, an especially unsavory tax haven where dissidents against the offshore establishment get blown up with car bombs.

The overall result of this ‘data protection competition’? Well, in Alexa’s case, back to the BBC

It has not launched a formal privacy probe. [A spokesman for the Luxembourg watchdog said] “we cannot comment further about this case as we are bound by the obligation of professional secrecy.

Quelle (as the French say) surprise!

But now. What has all this got to do with monopolies? Well, we will get to that. The sections that follow necessarily starts by covering some widespread misconceptions about monopolies: that antitrust is just about ‘breaking things up;’ that it’s all about consumer prices; and that Europe doesn’t have much of a monopoly problem, or that its competition authorities are doing a good job.

Sections 2, 3 and 4 then lay out the scale of the issue, using both data and analysis, and Sections 5 and 6 cover some history, showing how we got here, and explores possible historical links between monopolies and fascism. It then, in Sections 7 and 8 we look at the several links between monopolies and tax havens, and the bridges between antimonopoly and tax justice, then follow this with

1. Myths and misconceptions

Monopolies are widely misunderstood, in several ways.

Many people mistakenly think that monopolies are all about consumer welfare and prices. As in, a dominant player jacks up prices with impunity, and everyone pays more. No! Prices matter, but just think: Facebook’s and Google’s services are free! Amazon’s the cheapest! Consumer paradise! Yet if you think that their awesome dominance of the markets they are in — between them Facebook and Google have a stranglehold over two thirds of the $110 billion US internet advertising market — isn’t a problem, then you haven’t been paying attention. Price is the wrong metric here. Yet under the influence of Chicago Law & Economics, especially since the 1970s, this obsession with consumers and with prices has increasingly been the central guiding principle of antitrust law and enforcement, in the United States, in Europe, and elsewhere. The central problem isn’t prices, but private power.