By Andres Knobel and Oliver Seabarron

The Tax Justice Network in cooperation with the CORPNET group at the University of Amsterdam (@UvACORPNET) and the Data Analytics and Society Centre for Doctoral Training at the University of Sheffield (@DataCDT) has mined and applied advanced analytics to Orbis data to identify patterns and red-flags on the ownership chains of UK companies. Findings include that 74 per cent of UK companies have very simple structures (a natural person directly owning the company or just one intermediary entity in between. Only 5 per cent of UK terminal companies have more than 5 layers, and only 0.5 per cent have more than 10 layers. However, two UK companies of our sample have 23 layers of intermediary entities up to a natural person shareholder. We checked the records of one of these 23-layered companies in Companies House and found that they have declared wrong information (entities as beneficial owners) and even contradictory information on the addresses and shareholders (when comparing information available on the accounts, annual returns and other registered data).

Context of beneficial ownership transparency

Beneficial ownership transparency (identifying the natural persons who ultimately own and control companies and trusts) is getting a lot of global momentum as one of the most relevant tools to tackle illicit financial flows related to money laundering, corruption and tax abuse. As our latest update of the state of play of beneficial ownership registration around the world shows, based on findings from the Financial Secrecy Index 2020, more than 80 jurisdictions have approved laws requiring beneficial ownership information to be registered with a government authority.

However, verification of registered beneficial ownership information continues to pose challenges in all countries. For this reason, we have set up a multi-stakeholder group to promote verification of beneficial ownership and organised a call to map current verification strategies around the world.

One of the first public cases of verification of beneficial ownership data was carried out by Global Witness. Based on the open data format of the UK’s beneficial ownership register held by Companies House, Global Witness was able to analyse UK beneficial owners and thus detect many red-flags, including 500 ways to write “British” in the field for nationality, cases of disqualified directors and so on. Unfortunately, UK data on legal owners is not available in structured data format for bulk downloads to run proper checks. The data also lacks enough identification details – only legal owner’s names are made publicly available.

The importance of legal ownership and the full ownership chain

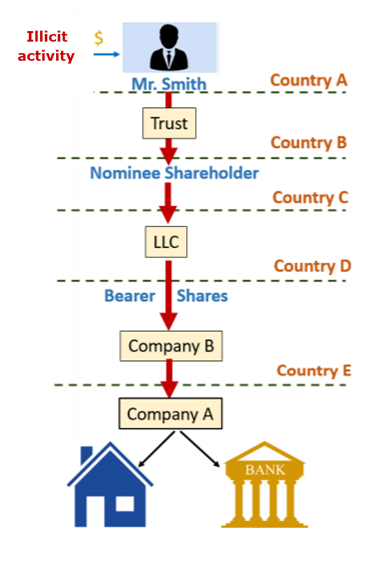

Beneficial ownership is arguably more useful than legal ownership to tackle illicit financial flows. After all, the legal owner (the shareholder) may be another company, but neither companies nor trusts can go to jail for illegal activity, only a natural person can.

This doesn’t mean that the legal owners are irrelevant. On the contrary, data on the legal owners and the full ownership chain is necessary to detect abusive practices, such as circular ownership or fragmented ownership to avoid beneficial ownership reporting requirements. At the same time, information on the full ownership chain is necessary to confirm the beneficial owner’s identity. In the figure above, Mary is both the beneficial owner of company A, and the legal owner and beneficial owner of company F. Given that the beneficial owner is in principle[1] also a legal owner of the last layer, by identifying every legal owner in the ownership chain it is possible to confirm the beneficial owner’s identity. Applying logic: if Mary -> (owns) company F -> company G -> company H -> company A, then we can confirm Mary -> company A. It’s important to note here that a beneficial owner may include an individual who controls the entity through mean other than ownership. However, here we consider that the natural person shareholder, Mary, is the beneficial owner (although she could just be a nominee, unless the information is verified).

Most countries, including the UK and Denmark only publish information on the first layer (company H) and the beneficial owner (Mary) but nothing on the intermediary entities in the ownership chain.

This lack of information on the full ownership chain is not a problem in the scenario where the ownership chain of any local company includes exclusively other local companies. Where no foreign entities at all are involved in the ownership chain of a local company, all the relevant information would be available in the same register, even if it required navigating through many different records. For instance, the register’s records on company A would hold information about company H and Mary. It would be possible to search for the register’s records on companies H, G and F to confirm that Mary is indeed the beneficial owner of company A.

However, if any of the intermediary entities are foreign companies (like the example in the figure above), the UK register may have no information on the legal owners of companies H, G and F. In this case, it will be necessary to go to the registries of the country of incorporation of each intermediary entity to find the corresponding legal ownership information (in the figure’s example, it would be necessary to search the registries from the US, Luxembourg and Panama). It only takes one of these countries to fail to provide legal ownership information, to make it impossible to identify the full ownership chain. In that case, it won’t be possible to confirm the beneficial owner either.

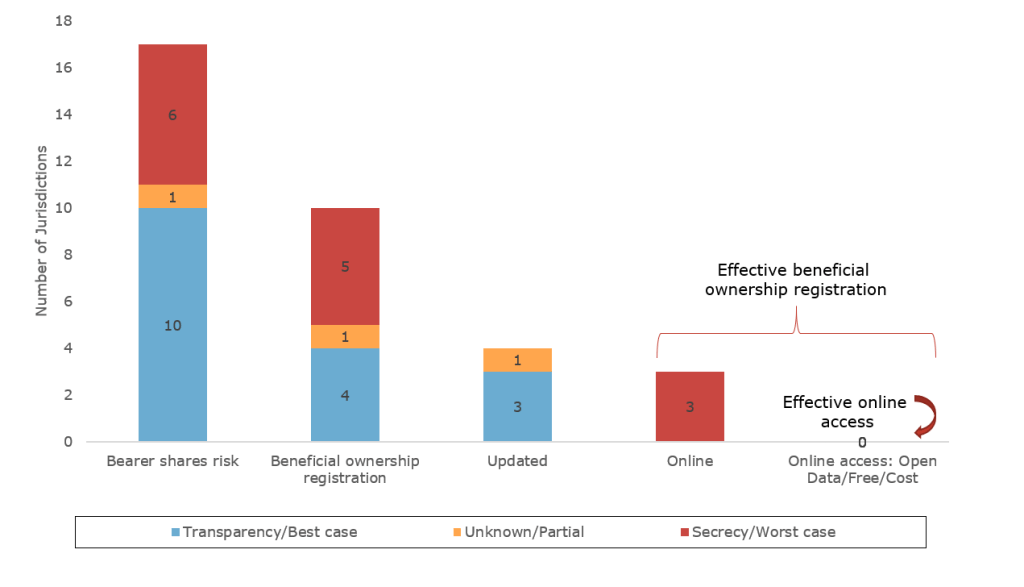

To make matters worse, the possibility of not finding legal ownership information on an intermediary entity isn’t just a potential risk but a very real one. Our latest paper on the state of play of beneficial ownership registration shows that out of the 133 jurisdictions covered by the Financial Secrecy Index, only 37 jurisdictions have proper legal ownership registration (where bearer shares don’t pose risks). Out of these 37, only 11 jurisdictions provide information online (out of which, only 1 in open data format).

Exploring the ownership structure of local companies to detect red-flags

Apart from looking at the full ownership chain of a specific company to confirm its beneficial owner, it is possible and relevant to systematically analyse ownership chains for all local companies. As described by our paper on beneficial ownership verification, that are many steps needed to verify beneficial ownership information, including authentication (eg the beneficial owner is who they say they are), authorisation (eg the lawyer incorporating a company on behalf of the beneficial owner is authorised to do so) and validation (eg write “British” properly). However, the most complex verification process is detecting red-flags and outliers (eg a director managing thousands of companies at the same time).

To detect outliers, it is necessary to know what a typical company looks like. For example, do most companies have one, two or ten shareholders? How are shareholdings allocated among shareholders, equal distribution (50-50 split, 33-33-33 split or 99-1 split)? How many layers are present in the ownership chain?

By knowing what a regular company looks like, it would be possible to identify outliers and audit them further to detect possible wrongdoing before illegal activity takes place. For example, if someone is trying to create a company with a very odd structure, authorities may want to investigate this company to understand the reason behind the extra complexity. This detection would be enhanced even further if countries knew not only the structure of a regular company, but also the typical corporate structure used in money laundering, tax evasion or corruption cases to compare it to. This way, if authorities explored and identified typical ownership structures beforehand, it would be possible to run systematic checks upon incorporation, to verify whether the new company’s structure resembles that of a regular company or that of a company involved in illegal activities. Suspicious companies could be investigated to prevent them from incorporating, opening bank accounts and engaging in illegal activities.

Exploring UK companies’ legal ownership chains

Inspired by Global Witness’ analysis on beneficial ownership data, the research on Tenders in EU: how much goes to tax havens? and Javier Garcia-Bernardo’s work on global corporate ownership networks, the Tax Justice Network produced an analysis of UK companies’ legal ownership chains. This project was the result of interdisciplinary work carried out mostly by Oliver Seabarron (DataCDT/Tax Justice Network) as part of his PhD, under training and supervision from Javier Garcia-Bernardo (UvACORPNET/Tax Justice Network), based on the legal ownership framework and analysis proposed by Andres Knobel (Tax Justice Network).

Sourcing ownership data for analysis

Based on the explanations above, Companies House’s legal ownership data was not sufficient for the purposes of our analysis . Instead, data from Orbis was used, which has the following limitations:

- It isn’t official legal ownership data.

- It doesn’t necessarily identify beneficial owners but different types of shareholders, including natural persons.

- There may be outdated, contradictory, or missing data.

It would be rather simple to analyse the ownership chain of companies, if all UK companies looked like this:

However, reality looks more like this:

To be able to analyse the data, we simplified the scope of the analysis. We took a sample that applied two conditions:

- Terminal companies: the analysis covered only companies that didn’t own other companies (or those that owned less than 50 per cent of another company). This prevents companies integrated within a long ownership chain to be considered as independent chains (in which case we would be double counting some companies).

Consider the ownership chain in the above figure: Mary -> (owns) F -> G -> H -> A. When we analyse A’s ownership chain, we see that there are three intermediary entities (F, G and H) up to the beneficial owner Mary. However, if we didn’t limit our analysis to terminal companies (eg company A), our analysis would also present “Mary -> F -> G->” as the (independent) ownership chain of company H, “Mary->F->” as the (independent) ownership chain of company G, and “Mary->” as the (independent) ownership chain of company F. In other words, we would be adding noise to the analysis by recording for one ownership chain (company (A) with three intermediary companies) as several more chains (company (H) with two intermediary companies; company (G) with one intermediary company; and company (F) with no intermediary companies).

- Shareholders with > 50 per cent ownership. To avoid circular ownership situations that would result in a never-ending loop, the sample considers only layers where the entity shareholder above owns more than 50 per cent of the capital.

Otherwise, the analysis of the figure below would result in: company E is owned by company D, which is owned by company C, which is owned by company E, which is owned by company D, which is owned by company C, which is owned by company E, which is owned by company D…

These two conditions, unavoidably, narrow the scope of our analysis to exclude more highly complicated ownership chains.

Firstly, only the chains through primary shareholders are captured, and therefore chains through any minority shareholders are not analysed.

In addition, as the following figure describes, if none of a company’s entity shareholders own more than 50 per cent (dashed arrow), it will be considered as though there are no additional layers above the company (as though the company were owned directly by natural person shareholders or beneficial owners. Another consequence is that the ownership chain may be broken into several parts:

For example, the ownership chain on the left hand side of the figure is Mary-> company F-> company G-> company H-> company I-> company L-> company M. However, given that company I owns only 20 per cent of company L, the analysis will consider that company’s M chain includes only one layer (company L). The analysis will also consider that (intermediary) company I is a terminal company (so its ownership chain, which includes companies H, G and F will be considered as independent from companies M and L).

On the other hand, the ownership chain on the right hand side of the figure, of terminal company O (Mary-> company F-> company G-> company N-> company O) will be disregarded. This is because company N only owns 20 per cent of company O, and is not a UK company, hence not considered a terminal company. Therefore, the analysis will determine that company O has zero layers (as though it were only owned by natural persons).

The narrowing of scope resulting from these conditions, however, is minor. A statistical check of our results found that less than 10 per cent of cases in the analysis had their chains simplified or “broken” by the two conditions, with the majority of these instances occurring in the first layer of ownership. To find out more about the robustness checks and results across different samples, look at the fact sheet here.

Findings – Part 1

The first sample analysed 327,587 UK terminal companies. Of these, 12 per cent had zero layers and 62 per cent had one between the company and the beneficial owner. This is consistent with the OECD’s Global Forum 2018 peer review report on the UK, which informed that “an analysis from the current PSC Register [beneficial ownership register] shows that approximately 80 per cent of companies are directly owned by natural persons or by companies whose immediate shareholders are natural persons and are managed by the same persons. The remaining 20 per cent are more complex structures” (page 45, [TJN-Note]).

The following figure shows the distribution of the number of layers (intermediary entities between a company and its beneficial owner), for those companies with one or more layers:

Interestingly, only 5 per cent of UK terminal companies have more than 5 layers, and only 0.5 per cent have more than 10 layers. This suggests the proposal mentioned in our paper on beneficial ownership verification to limit the length of the ownership chain to up to two or three layers (to make it easier to verify beneficial ownership information) wouldn’t affect the vast majority of UK companies because most of them already use very few layers. Coincidentally, the World Bank’s well-known The Puppet Masters’ report on grand corruption cases proposed a three-layer test for sniffing out inappropriate complexity (this may likely apply to small companies but not to listed multinationals): “One compliance officer suggested an informal ‘three-layer complexity test’ as a quick-and-dirty rule of thumb. Whenever more than three layers of legal entities or arrangements separate the end-user natural persons (substantive beneficial owners) from the immediate ownership or control of a bank account, this test should trigger a particularly steep burden of proof on the part of the potential client to show the legitimacy and necessity of such a complex organization before the bank will consider beginning a relationship.” (page 56).

As regards the outliers, there are two companies that have 23 layers up to a natural person (or where there is no more data)

Cross-checking Orbis and Companies House data

According to Orbis, one of the terminal companies with 23 layers had 15 layers of UK entities and 8 layers of entities from the Cayman Islands. We decided to check the information from that terminal that was available at Companies House.

The first observation is that it is very difficult to obtain information on legal owners from Companies House. The first and best option is to look at annual returns which are available as an image, ie non-machine-readable pdfs. However, many of the layers didn’t have updated annual returns. Second, it is possible to look at the company’s full accounts, read the notes and hope that there is some information on legal owners. Many of the layers’ accounts referred to the immediate layer above, and the controlling group, a private equity company from Canada listed on the Toronto’s stock exchange.

However, these are some of the issues we found:

- Almost all the 13 layers of legal owners that we checked failed to identify a beneficial owner. They reported their immediate legal owner (another company) as the beneficial owner, even though a beneficial must always refer to a natural person. Only the last UK layer reported the founder of the Canada private equity group as the beneficial owner.

- Most layers shared one of three addresses: one in Scotland, one in London and one in Birkenhead. They also shared some directors.

- The address of the shareholder (the layer above) reported by the controlled company (the layer below) sometimes didn’t match the address reported by the controlling company (the layer above). For instance, if company Bowns company A, company A would report that the address of its shareholder (B) was in London, while the records of company B showed an address in Scotland.

- The legal owner reported by a company on its full annual accounts didn’t match the legal owner reported by that same company (under the beneficial ownership field). For example, company X’s annual accounts described that its shareholder (immediate layer above) was company Holdings 1 from the UK, while company X’s reported beneficial owner was Holdings 1 from the Cayman Islands (not only was the contradiction problematic, but a beneficial owner must always be a natural person).

- While Cayman Islands’ register appears to have information on the companies, it costs more than USD $36.59 to do a company search. So, if Orbis data is correct and there are eight layers in Cayman, it would take almost USD $300 to find out the legal owners of those layers.

Conclusion

A first analysis of Orbis data shows that corporate ownership is very complex and messy. Company registries that offer information online, for free and in open data format can help obtain necessary information to verify the beneficial owners. However, the lack of verification and enforcement on beneficial ownership data, allows companies to declare an entity, instead of a natural person, as a beneficial owner (as Global Witness had already warned). On top of this, the UK’s lack of open data format for companies’ legal ownership information, makes it very hard to track the ownership chain of companies. This problem is exacerbated by the lack of verification on legal owners, where either annual returns are not filed on time, or where the information reported by the full annual accounts contradicts the shareholder information reported by the same company. In any case, the trove of useful free online data in the UK makes it possible to obtain some information, which is much better than Cayman’s case, where each search costs USD $36, and it’s not clear what information will be obtained.

However, this problem is exacerbated when the ownership chain is long and it includes different types of legal vehicles from different countries. The terminal company that we analysed was “easy” because it included many companies from the UK. Had it included trusts or limited partnerships from the UK, or entities from many other countries, our findings would have been even more limited.

One way to reduce the risks of legal and beneficial ownership inaccuracies is to set limits on the length of the ownership chain, so that it includes few layers (ideally not more than one or two, unless the need is justified). The other complementary limit would be qualitative: to only allow intermediary entities, as long as they are incorporated in countries offering free online data on their legal and beneficial owners. In the case of the UK, both our findings and the OECD’s Global Forum peer review report demonstrate that the vast majority of UK companies (between 75 and 80 per cent) already have very simple structures, so none of them would be affected by the proposed length and quality limits.

The next part of this project will include an analysis of the country of incorporation of most layers of UK terminal companies.