Global Justice Now press release:

Download the report

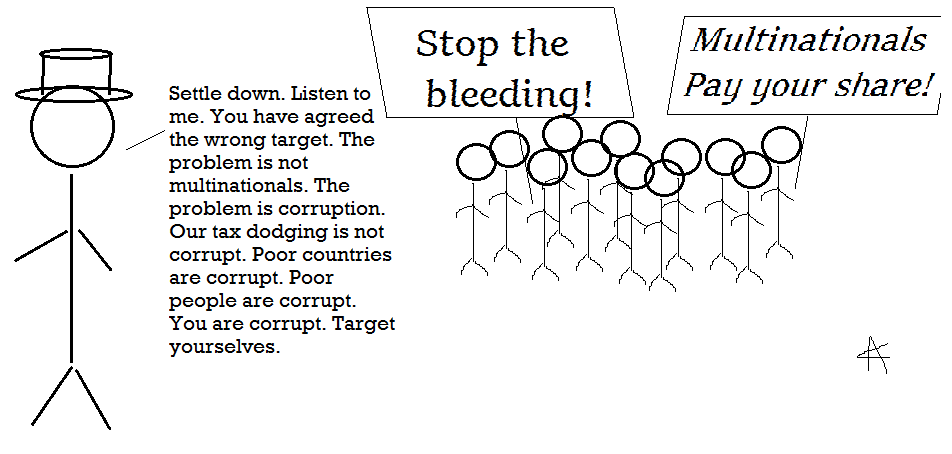

Much more wealth is leaving the world’s most impoverished continent than is entering it, according to new research into total financial flows into and out of Africa. The study finds that African countries receive $161.6 billion in resources such as loans, remittances and aid each year, but lose $203 billion through factors including tax avoidance, debt payments and resource extraction, creating an annual net financial deficit of over $40 billion.

The research shows that according to the most recent figures available in 2015:

- African countries received around $19 billion in aid but over three times that much ($68 billion) was taken out in capital flight, mainly by multinational companies deliberately misreporting the value of their imports or exports to recuse tax.

- African governments received $32.8 billion in loans but paid $18 billion in debt interest and principal payments, with the overall level of debt rising rapidly.

- An estimated $29 billion a year was stolen from Africa in illegal logging, fishing and the trade in wildlife and plants.

Tim Jones, economist from the Jubilee Debt Campaign, said:

“The African continent is rich, but the rest of the world profits from its wealth through unjust debt payments, multinational company profits and hiding proceeds from tax avoidance and corruption.”

Aisha Dodwell, a campaigner with Global Justice Now said:

“There’s such a powerful narrative in Western societies that Africa is poor and that it needs our help. This research shows that what African countries really need is for the rest of the world to stop systematically looting them. While the form of colonial plunder may have changed over time, its basic nature remains unchanged.”

Martin Drewry, director of Health Poverty Action said:

“To end poverty we need to focus our efforts on preventing the policies and practices that are causing it. That means we need to stop our tax havens facilitating the theft of billions, clamp down on illegal activities and compensate African countries for the impact of climate change that they did not cause. “

Bernard Adaba, policy analyst with ISODEC in Ghana said:

“’Development’ is a lost cause in Africa while we are haemorrhaging billions every year to extractive industries, western tax havens and illegal logging and fishing. Some serious structural changes need to be made to promote economic policies that enable African countries to best serve the needs of their people rather than simply being cash cows for Western corporations and governments. The bleeding of Africa must stop!”

The report Honest Accounts 2017: How the world profits from Africa’s wealth, published by a coalition of UK and African organisations, including Global Justice Now, Health Poverty Action and Jubilee Debt Campaign, makes a series of recommendations as to how the system extracting wealth from Africa could be dismantled. These recommendations include promoting economic policies that lead to equitable development, preventing companies with subsidiaries based in tax havens from operating in African countries, and transforming aid into a process that genuinely benefits Africa.

Notes

The research covers the 47 countries classified as ‘sub-Saharan Africa’ by the World Bank.

The research was published by Global Justice Now, Health Poverty Action, Jubilee Debt Campaign, Uganda Debt Network, Budget Advocacy Network, Afrika and Friends Networking Open Forum, Integrated Social Development Centre, Zimbabwe Coalition on Debt and Development, Groundwork and People’s Health Movement.

For more information please contact Kevin Smith:

T (+44) (0)20 7820 4913 or (+44) (0)7711 875 345.

[email protected]

The dirty world of tax evasion and avoidance involves all sorts of unpleasant and anti-social characters, none more so than the professional enablers who devise avoidance schemes, market these schemes to their clients, lobby governments for special treatments and permissive laws, and generally play the role for tax dodgers that Tom Hagen played for The Godfather. Continue reading “How Global Audit Firms Are Using Their Lobbying Clout to Dilute Sarbanes-Oxley Reforms”

The dirty world of tax evasion and avoidance involves all sorts of unpleasant and anti-social characters, none more so than the professional enablers who devise avoidance schemes, market these schemes to their clients, lobby governments for special treatments and permissive laws, and generally play the role for tax dodgers that Tom Hagen played for The Godfather. Continue reading “How Global Audit Firms Are Using Their Lobbying Clout to Dilute Sarbanes-Oxley Reforms”