This four-part podcast special series is well worth a listen. It’s called My Mother’s Murder, an investigation into the assassination of Daphne Caruana Galizia. It is narrated by one of her sons Paul Caruana Galizia. Here’s part of the description of the podcast series:

Daphne investigated corruption involving the most powerful businessmen and politicians in Malta where she lived. She paid with her life. Her son Paul goes in search of the men who ordered her murder.“

At the Tax Justice Network we have the highest respect for the courage of the incredible Daphne Caruana Galizia, whose work we followed closely, and also the bravery of her family who have continued the fight for justice in Malta.

Their perseverance, with massive support from the Daphne Project, has yielded impressive results, with regular visits and pressure from MEPs and eventually an inquiry by the European Banking Authority into the notorious Pilatus Bank, which you can read more about here and here. Members of the European Parliament expressed their concern that

in the absence of proper regulation Pilatus Bank has been free to pursue investigative journalists and whistleblowers with the full force of the law.”

This podcast is important particularly in the way it dissects how the corrupt can dismantle the State and capture it for their own ends, sliding so quickly into intimidation and violent repression of all who stand in their way.

Daphne’s work went way beyond Malta, to the very nature of corruption, its facilitators in the world’s most powerful countries, and of the finance curse, which we’ve written and warned so much about – Malta is an example of the worst that can happen when a nation has an overgrown finance sector which has total state protection. We’ve seen so much intimidation and fear of speaking out, particularly in small island nations suffering from the finance curse.

Malta is ranked number 18 in our most recent Financial Secrecy Index, with a secrecy score (62) which places it among the worst offenders in Europe . You can read our assessment here.

Here’s a trailer from Tortoise Media on the 4 part podcast series below. The podcast is available on various podcast platforms. Do have a listen.

One last thing. It’d be remiss of us not to mention our own monthly podcast the Taxcast which covers corruption, scandal and the fight for tax and economic justice around the world, which the mainstream media either ignores or covers badly. Check that out too!

Days

before the annual UN Commission on the Status of Women was scheduled to

meet in New Yorkto focus on the gender equality aims

promised in global agreements, goals and declarations, writes Liz Nelson,

will we finally look beyond traditional thinking about how these aims can (or

cannot) be funded? Are we ready to admit that progressively targeted tax is the

only effective financing solution?

We’ve all done it: promised, but not delivered. And our governments are

no different. But should we really be so forgiving of our elected

representatives when they fail to keep their promises on issues that are

fundamental to our well-being and human development?

No: for everyone’s sake, and

especially this year for women during the Beijing

+ 25 intergovernmental review of progress towards gender equality,

we should not. We must be willing to hold our governments to account when they

fail to take progressive action, or when they remain politically indifferent to

the need to take substantial measures to achieve gender equality. Even when

governments appear to be working toward those goals, how can we make sure they

are delivering on their promises? Taxation and gender impact analysis are two

of the most powerful ways we can hold our politicians to account.

Platforms, plans and priorities – and very little progress According to the Convention on the Elimination of Discrimination Against Women (CEDAW), a United Nations treaty signed in 1979 that is frequently described as an “international bill of human rights for women”, by ratifying international human rights treaties such as CEDAW, states assume obligations under international human rights law – and as “duty bearers” they have an obligation to “refrain from making laws, policies, regulations, programmes, administrative procedures and international structures that directly or indirectly result in the denial of the equal enjoyment by women of their civil, political, economic, social and cultural rights” (CEDAW/C/GC/28).

Civil society letter supporting postponement of CSW64

An official letter advocating for a postponement of UN CSW as opposed to a scaled down version and signed by 499 civil society organisations from 92 countries was sent this week to UN Secretary General António Guterres and UN Women Executive Director Phumzile Mlambo-Ngcuka.

It sets out why the Commission on the Status of Women’s (CSW) annual

meeting is such an important mechanism for accountability ‘to all women and

girls in all their diversity around the world’ and the ‘most important annual

process to review progress and challenges towards achieving women’s human

rights, gender equality and the empowerment of all women and girls.’

Launched two weeks ago, the 2020 edition of our Financial

Secrecy Index has broken every record we track on the index’s reach and media

impact. First published in 2009, the global coverage of this year’s edition of the

index reflects a growing urgency shared by people around the world to expose

and reign in rampant tax abuse by the ultra-rich and powerful.

The Financial Secrecy Index ranks each country based on how intensely the country’s legal and financial system allows wealthy individuals and criminals to hide and launder money extracted from around the world. A higher rank on the index does not necessarily mean a jurisdiction is more secretive, but rather that the jurisdiction plays a bigger role globally in enabling secretive banking, anonymous shell company ownership, anonymous real estate ownership or other forms of financial secrecy, which in turn enable money laundering, tax evasion and huge offshore concentrations of untaxed wealth. A highly secretive jurisdiction that provides little to no financial services to non-residents, like Samoa (ranked 86th), will rank below a moderately secretive jurisdiction that is a major world player, like Japan (ranked 7th). The aim is not to penalise jurisdictions with greater scale, but simply to recognise that their secrecy poses greater risks – and so it is more important that they behave responsibly.

World’s top suppliers of financial secrecy:

1 Cayman 2 US 3 Switzerland 4 Hong Kong 5 Singapore 6 Luxembourg 7 Japan 8 Netherlands 9 BVI 10 UAE

Financial secrecy keeps tax abuse feasible, drug cartels bankable. But most gov'ts are saying enough. #FSI2020https://t.co/54gVv1mmD4

— Tax Justice Network Bsky: @taxjustice.net (@TaxJusticeNet) February 18, 2020

The 2020 edition of the index saw Switzerland reduce its

ranking to the third biggest enabler of financial secrecy in the world, marking

the first time the country did not rank worst on the index since 2011. Despite

escalating its contribution to global financial secrecy since the publication

of the 2018 edition of the index, the US remained the second biggest enabler of

financial secrecy in the world after Cayman overtook both the US and

Switzerland to the top of the 2020 index. This marks the first time Cayman

ranked first on the Financial Secrecy Index.

These changes on the ranking told three major international stories that were covered widely around the world: a British territory topped the index for the first time on the same day the EU blacklisted the territory; the US continued to escalate its financial secrecy despite ambitions announced by Senator Lindsey Graham to improve the US’s ranking on the Financial Secrecy Index; Switzerland managed to lose its position as the world’s greatest enabler of financial secrecy amid a global trend of governments curbing financial secrecy. The index also told many regional and country-specific stories on which we worked with our partners and allies around the world to shine a spotlight on.

The launch of the index also saw an outpour of support and

commentary from renowned economists, organisations and tax advocates. Gabriel

Zucman, professor of economics at the University of California at Berkeley and

author of The Triumph of Injustice: How

the Rich Dodge Taxes and How to Make Them Pay, described

the index as “a valuable tool to spot where bad regulations emerge around

the world and thus be able to propose strategies for a more transparent world.”

Transparency International published a comparison

of the Financial Secrecy Index and Corruption Perception Index,

illustrating how the two indices build a fuller picture. OpenOwnership discussed

the global progress on beneficial ownership revealed by the index.

Altogether, we saw eight op-eds supporting the index

published in Latin America, four in Europe, four in Africa and two in Asia. Among

these were several from Independent Commission for the Reform of International

Corporate Taxation commissioners, including Eva

Joly former member of the European Parliament and vice chair of the

Commission of Inquiry on Money Laundering, Tax Evasion and Fraud; Léonce

Ndikumana, Professor of economics and Director of the African Development

Policy Program at the Political Economy Research Institute at the University of

Massachusetts; Jayati

Ghosh, professor of economics at Jawaharlal Nehru University; Wayne

Swan, former treasurer and deputy prime minister of Australia; and Ricardo

Martner, economist and former Chief of the Fiscal Affairs Unit of the United

Nations Economic Commission for Latin America and the Caribbean.

Discussions of the Financial Secrecy Index took place beyond just screens and broadsheets. The UK’s performance on the index was raised in the House of Commons by UK Shadow Chancellor John McDonnell, and speakers from across the parliament in a debate on tax avoidance and evasion. The index was presented in the US Senate by the FACT Coalition, with speakers from Transparency International, the National District Attorneys Association, the Fraternal Order of Police, Global Financial Integrity and Jubilee USA Network.

All in all, the Financial Secrecy Index 2020 has so far reached a viewership of over 2 billion, blasting a bright, searing light through the fog of financial secrecy. Countries that peddle in financial secrecy can no longer do so in secret and the record-breaking reach of the Financial Secrecy Index shows that people around the world will no longer stomach financial secrecy.

We’re pleased to share the 13th edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa by finance journalist Idriss Linge in Cameroon covering the Financial Secrecy Index 2020 results. Nous sommes fiers de partager avec vous cette nouvelle émission de radio/podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Dans cette 13ème édition du programme Impôts et Justice Sociale:

Nous revenons sur Le Financial Secrecy Index, l’indice d’opacité financière publiée par Tax Justice Network le 18 février 2020. 17 pays africains ont été notés, et sont ceux qui impacte le moins au niveau du monde. Mais sur bien des indicateurs du classement, l’Afrique est critiquable. C’est le cas en matière de secret bancaire, ou des transactions juridiques sur les entreprises

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to the twenty-sixth edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to post it. You can also join the programme on Facebook and on Twitter.

Taxes Simply #26 – Arab countries’ performance in the Financial Secrecy Index

Welcome to the twenty-sixth edition of Taxes Simply, a special edition that covers the performance of Arab countries in the recently published Financial Secrecy Index published by the Tax Justice Network in a conversation between Walid Ben Rhouma and the researcher in the Egyptian Initiative for Personal Rights, Osama Diab.

This edition also contains a collection of the most important economic and tax news in the region and the world including:

The United Nations issues a report on companies operating in Israeli settlements

Egypt is negotiating a new agreement with the International Monetary Fund

The death of former Egyptian President Hosni Mubarak, whose era was characterised by the spread of financial corruption, which was one of the key reasons for his 2011 overthrow.

الجباية ببساطة #٢٦ –

أداء الدول العربية في مؤشر السرية المالية ٢٠٢٠

أهلا بكم في العدد

السادس والعشرين من الجباية ببساطة وهو العدد الخاص الذي يتناول أداء الدول

العربية في مؤشر السرية العالمية الصادر حديثا عن شبكة العدالة الضريبية في حوار

ما بين وليد بن رحومة والباحث في المبادرة المصرية للحقوق الشخصية أسامة دياب.

يحتوي أيضا العدد على مجموعة من أهم الأخبار الاقتصادية والضريبية في المنطقة

والعالم وتشمل: ١) إصدار الأمم المتحدة لتقرير عن الشركات العاملة بالمستوطنات

الإسرائيلية؛ ٢) مصر تتفاوض على اتفاق جديد مع صندوق النقد الدولي؛ ٣) وفاة رئيس

مصر السابق حسني مبارك والذي تميز عهده باستشراء الفساد المالي والذي كان واحدا من

أسباب الإطاحة به في عام ٢٠١١.

Just a couple of years ago, some members of a Lebanese family were suspected of committing mafia-style crimes, including blackmail, drug-dealing, the theft of a giant gold coin (100 kg!) from Berlin’s Bode Museum, and the laundering of millions of euros through real estate investments. Remember? This story reminds the whole world that Germany has so far been in no position to mock countries shaken by embezzlement scandals, such as the recent Luanda Leaks in Angola. But that is not because of foreign family clans, but because of a much more German variant of family dynasties.

A large economy, internationally networked, legally secured, with a

culture of secrecy and virtually no means of unmasking and punishing money

launderers: criminals couldn’t dream of anything better. Every year, up to €100 billion are

laundered in this country, according to an academic report written at the request

of the Finance Ministry.

When illegal funds are

laundered in the housing sector, they do not only risk financing mafias and

terrorists, but they also contribute to rising rents and purchase prices. In Berlin, real estate

transactions amounted to €11 bn in 2018, up from €3.6 billion in 2009,

with rents for ordinary tenants exploding. Some of the demand driving up the

prices is likely to consist of money of dubious origin.

That’s why we can only applaud the fact that, after years of denial,

Germany finally seems determined to get rid of its reputation of being a

“gangster’s paradise”. This is even the main piece of news coming out of the

publication of the 2020

Financial Secrecy Index. According to the 2020

Financial Secrecy Index published by the Tax Justice Network, a UK-based thinktank

of which I am a director, Europe’s

leading economy managed to dramatically reduce its contribution to global

financial secrecy, taking its ranking down from 7th on the 2018 index to

14th.

This improvement is mainly due to the adoption of the new European directive regulations into local legislation. In response to the Panama Papers revelations,the European Union (EU) tightened its directive to counter money laundering within the European financial system. One important step is to unmask criminals that hide behind anonymous companies by the introduction, in January 2020, of registers of corporate ownership, showing who ultimately controls every company incorporated across most of Europe, and in theory accessible not only to the tax administrations and law enforcement, but also to journalists and civil society.

Few countries have complied timely with the new rules. Germany’s swift action is all the more impressive as it extended the obligation to disclose the names of the beneficial owners to foreign trusts and foreign letter box companies purchasing German real estate, going even further than the EU required. This decision was made despite intense resistance, particularly from the almighty German business dynasties. Speaking in the name of tradition, these huge so-called family businesses now threaten to defend their culture of secrecy at court. .

The Deutschland dynasties believe they do not have

to reveal their profits, even though, in reality, many of them are now

multinationals. And their counterattack has already begun. Last November, in a

decision that the majority of citizens didn’t notice, Germany was, because of

their lobbying, one of the 15 European countries failing to support a new directive that would require

multinationals to reveal how much profit they make and how little tax they pay

in each country they operate in.

Gangster's Paradise Germany: What criminal clans and German family businesses have in common. My op-ed today in @handelsblatt

When multinationals and the super-rich manage

not to pay their fair share of taxes, governments cannot invest in access to

education, health care, and decent pensions, or take measures to mitigate and

adapt to the climate crisis. Arguing that their coffers are empty, those

governments opt for austerity measures, becoming more and more discredited in

the eyes of the population, and fostering the kind of populist

backlash that allows authoritarianism to flourish.

This dynamic also exacerbates gender inequality,

because, in Europe just as in the rest of the world, women are overrepresented

among the poor and among the demographic group with informal or low-paid jobs.

In addition, they tend to take on a larger share of unpaid care work when

social services are cut.

Germany must now prove that it is really willing to enforce its stricter

laws. It will have the opportunity to do so in the coming months when faced

with the experts from the Financial Action Task Force (FATF), the most

important international body for the prevention of money laundering. Based in

Paris, this organization examines every ten years whether states comply with

international standards, and Germany’s audit will begin in April.

In 2010, the experts were unforgiving. Germany failed 20 out of the

49 criteria and according to observers barely escaped the body’s

blacklist. To make them forget their last evaluation, Berlin should take bold

steps: give its public prosecutors, police and supervisory agencies real

resources to investigate, as well as annul old bearer shares that allow their

holders completely anonymous ownership of companies despite all transparency

registers.

With Brexit a reality, the risk now is that the UK may transform itself

into a so-called “Singapore-on- Thames”, ie an even more harmful facilitator of

financial secrecy, putting European countries’ efforts in jeopardy. But it is

also an amazing opportunity. Outside the EU, the United Kingdom will no longer

be able to block anti-tax haven measures from being adopted in Brussels, and to

defend its satellite secrecy jurisdictions. Europe, and especially Germany, no

longer has an excuse for not going further with transparency. German family

dynasties finally have to let go of some of their cherished secrecy because it

is this very secrecy that keeps criminals in business.

In this special extended Taxcast, Naomi Fowler takes you on a whistle-stop guided tour on an express train around the world with some of the Tax Justice Network team, looking at the worst offenders selling secrecy services according to the latest Financial Secrecy Index results What can nations can do to protect themselves and their populations from financial and legal secrecy?

The financial secrecy index was first published in 2009. So we now have over 10 years of data to draw on…and it shows that civil society can really make a difference.

Non-OECD countries should recognise that OECD member States are only interested in protecting their own interests and cannot even begin to pretend that they are representing the interests of the rest of the world. So if the non OECD member States, in other words, the rest of the world, want to become rule makers, not rule takers, then they need to reject the pretensions of the OECD member States to be the rule makers. We need a global, legitimate rule maker. And ideally it should be the United Nations that takes on the role of making the rules for the whole of the world.”

~ John Christensen

Find out more:

There’s more information on the Financial Secrecy Index here.

The full podcasts on each region are available here.

Webinars on the index, including tutorials are available here.

Want to download and listen on the go? Download onto your phone or hand held device by clicking ‘save link’ or ‘download link’ here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher.

Join us on facebook and get our blogs into your feed.

An article in the U.S. magazine The Nation, written by today’s blogger (pictured above), highlights how the finance curse strikes U.S. agriculture.

It starts by focusing on the political divides that seem to have opened up between the so-called “coastal elites” which tend to vote for Democrats, and more rural constituencies, which voted more heavily for Donald Trump in the last elections. Voting patterns are obviously more complex than that, but the article highlights that there is great resentment among many people in urban centres about “whining and begging” rural farmers taking handouts.

Once the finance curse analysis comes into the picture, however, the picture changes completely. As the article notes:

both the narrative that subsidies flow from “coastal elites” to farmers and the fatalism about rural economic decline indicate a profound misunderstanding of what’s actually going on.

That’s because of the role of financial players, institutions, mechanisms and techniques, often on behalf of distant shareholders. Several decades ago, much of the wealth that was created from the soils, sun and rains tended to circulate back to local communities, as farmers bought inputs and services from local seeds suppliers, grocery stores, parts suppliers, doctors, restaurants, banks, insurance firms, and so on. Since the 1980s in particular, “financialisation” has happened: the penetration of financial players, techniques, institutions and mechanisms into every step of the agricultural process.

Large firms often based in distant money centres have gobbled up the local players, taken these formerly local services in-house, cut out the local suppliers, and sent the dividends off to shareholders and owners in New York, Chicago, Houston, and overseas and offshore. Those local circulatory systems for wealth have been unrolled and turned into a one-way conveyor belt shipping wealth outwards.

We have already pointed to the same essential geographical story in Britain, as private equity firms and other predatory players based substantially in London extract wealth from other parts of the country, not just redistributing wealth upwards, but harming overall national prosperity too.

This giant extraction machine generates tremendous anger, of course. But the article goes on to say that this extraction isn’t just happening in agriculture: it’s happening all across the economy.

It turns out that rural U.S. farmers and those “coastal elites” are on the same side of the real economic divide, which is between the beneficiaries of the financial extraction, and those being extracted from. In this analysis, of course, lies the seeds of some potentially interesting political alliances.

Join Tax Justice Network and the FACT Coalition for a discussion of the 2020 Financial Secrecy Index and relevant US legislation.

As Congress considers measures to combat financial secrecy and end the formation of anonymous companies in the United States, the Tax Justice Network and the Financial Accountability and Corporate Transparency (FACT) Coalition ask you to join them on Capitol Hill for the US launch of the 2020 Financial Secrecy Index on Wednesday, February 19, 2020, from 9:30 am – 10:30 am. The event will take place in SD-106 (Dirksen Senate Office Building).

Since 2009, the Tax Justice Network has produced the Financial Secrecy Index biennially, analysing the level of secrecy in the world’s financial centres. It is the only comprehensive ranking that seeks to apply a methodical approach to defining secrecy jurisdictions. The previous iteration of the Financial Secrecy Index, released in January 2018, rated the United States as the 2nd largest secrecy jurisdiction in the world, behind only Switzerland.

The 2020 Financial Secrecy Index Launch Event will feature a presentation by Tax Justice Network on the 2020 Financial Secrecy Index results, including where the US falls in the new rankings and why. A panel of experts will then discuss the national security, law enforcement, human rights, and economic implications of financial secrecy in the United States as well as bipartisan legislation (such as the ILLICIT CASH Act and the Corporate Transparency Act) currently pending in Congress to tackle financial secrecy.

Coffee, Tea, and Light Pastries Will Be Provided

9:30 AM – Welcome Remarks — Clark Gascoigne, The FACT Coalition 9:35 AM — Presentation of the Financial Secrecy Index 2020 – Jack Blum, Tax Justice Network 9:50 AM – Panel Discussion featuring:

Caren Benjamin, Polaris

Jack Blum, Tax Justice Network

Annabel Lee Hogg, The B Team (TBC)

Tim Richardson, Fraternal Order of Police

Jodi Vittori, Transparency International Defense & Security

The Cayman Islands will join Oman, Fiji, and Vanuatu on an EU blacklist of foreign tax havens, making it the first UK overseas territory to be named and shamed by Brussels

We have lambasted Europe’s blacklists for years, which are based above all on political considerations. In particular, the EU does not seem to want to blacklist EU member states, or powerful countries or . . . any tax haven that really matters. At the time of writing, the list consists of these giants of global finance:

American Samoa

Fiji

Guam

Oman

Samoa

Trinidad and Tobago

US Virgin Islands

Vanuatu

The EU even has official excuses for this nonsense. For a more serious list, based on objectively verifiable criteria, see our 2018 Financial Secrecy Index (FSI) – Cayman is at number three, below Switzerland and the United States. The all new Financial Secrecy Index 2020 will be published next week – where will these three jurisdictions be? We can already reveal that there will be significant changes, up and down the index! (And some good news.)

In the tax haven world, Cayman isn’t a minnow. So this latest move by the EU, which needs to be confirmed by EU Finance Ministers next week, is significant.

We also expect, based on conversations we’ve been having, that the forthcoming blacklist will include the current eight, plus Palau, Botswana, Panama and Cayman. Turkey is a question mark. This is an improvement: in 2018, we reckoned that the EU’s blacklist targeted just 1 percent of financial secrecy services threatening EU economies: if our sources are correct, the new list would represent 7.3 percent. Or about one fourteenth of the total problem…

It’s notable, of course, that this comes just a few weeks after Britain’s formal exit as a full member of the European Union, and as it enters a transitional negotiation stage for final exit. Cayman and the British Virgin Islands, another British overseas territory, was already under review and on an EU grey list, (a classification that gives jurisdictions time to shape up). While it could be argued that Cayman had simply failed to address the specific technical criteria laid down by the criteria, there is no doubt that it represents, as the Guardian puts it:

a clear indication of [Britain’s] loss of influence on the EU’s decision-making

Britain has for years fought hard to protect the interests of the offshore financial industry in its Crown Dependencies and Overseas Territories like Cayman, and Brexit certainly weakens their positions. While TJN has not taken a position to support Brexit (far from it), we recognise that the EU’s new freedom to sanction recalcitrant British offshore jurisdictions, without British lobbying, is a positive thing.

The EU has made clear, repeatedly, that the UK will not be allowed to undercut it on financial and other regulations, and keep full access to the single market. While UK politicians may insist on their post-Brexit right to race to the bottom, and profess surprise at the unreasonableness of the EU position, the choice is stark. If Britain is determined to hold onto its grubby role as the master of ceremonies for the financial recalcitrants of its secrecy network, the UK and the City of London financial centre which derives so much wealth from these places will face some uncomfortable truths. Many Europeans don’t have much appetite for compromise, and even see Brexit as an opportunity.

In the words of Sven Giegold, a leading member of the European Parliament (and also, as it happens, a founder of TJN):

The time for special treatment of the UK is over. The British government’s attempt to give its London financial centre permanent and comprehensive access to the European financial system for decades is audacious. The EU will not let the decision as to which British financial market rules are compatible with European rules be taken out of its hands.

We’d fully support that. Interesting times lie ahead.

Welcome to this month’s latest podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! (Ahora también estamos en iTunes.)

En este programa:

El Fondo Monetario Internacional y América Latina

Las batallas impositivas en todo el mundo desde Europa a América Latina

Los multimillonarios en Estados Unidos que quieren pagar más impuestos y aumentar el salario mínimo

¿Qué compañías latinoamericanas operan en Londres y para qué lo hacen?

We’re pleased to share the twelfth edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa by finance journalist Idriss Linge in Cameroon. Nous sommes fiers de partager avec vous cette nouvelle émission de radio / podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Dans cette 12ème édition du programme Impôts et Justice Sociale:

Nous revenons sur les

grands sujets qui ont marqué l’actualité de la justice fiscale et sociale avec

une incidence sur l’Afrique. Il s’agit notamment des Luanda Leaks, de la justice fiscale

dans le secteur de la santé en Afrique et de la position des sociétés civiles

africaines sur les négociations en cours pour une fiscalité internationale.

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Welcome to the twenty-fifth edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to post it. You can also join the programme on Facebook and on Twitter.

Taxes Simply #25 – Oxfam’s shocking data on increasing inequality and wealth concentration

Welcome to this latest edition of Taxes Simply. We begin with an interview with Nabil Abdo, the Regional Policy Adviser for Oxfam in the Middle East, on that organisation’s recent report, which contains new shocking figures on the increasing disparity in wealth between the world’s rich and the rest of humanity.

In the second part of the programme, we present a summary of the most important tax and economic news in January 2020, including:

new leaks from Luanda, Angola

confidence in capitalism collapses globally

the arrest by the administration of the head of the Egyptian Tax Authority, charging him with bribery

Jeff Bezos earns $15 million a second

Jordan signs a new agreement with the IMF

الجباية ببساطة ٢٥# – بيانات أوكسفام الصادمة حول تزايد اللامساواة وتركز الثروة

أهلا بكم في في العدد الخامس والعشرين من الجباية ببساطة.

نبدأ العدد بحوار مع نبيل عبدو، مستشار السياسات الإقليمية لمنظمة أوكسفام في الشرق الأوسط، بخصوص التقرير الصادر مؤخرًا عن المنظمة والذي يحتوي على أرقام صادمة جديدة عن التفاوت الرهيب والمتزايد في الثروة بين أغنياء العالم وباقي البشرية. في الجزء الثاني من البرنامج

نقدم ملخص لأهم أخبار الضرائب والاقتصاد في شهر يناير/كانون الثاني، ويحتوي ملخصنا للأخبار على: ١) تسريبات جديدة من لواندا، أنجولا؛ ٢) الثقة تنهار في النظام الرأسمالي عالميًا؛ ٣) الرقابة الإدارية تضبط رئيس مصلحة الضرائب المصرية متلبسًا بتلقي رشوة؛ ٤) جيف بيزوس

يربح ١٥ مليون دولار في الثانية؛ ٥) الأردن توقع اتفاقًا جديدًا مع صندوق النقد.

The OECD secretariat has announced that it obtained agreement from the Inclusive Framework to press ahead with its own proposals, following US-French agreement of sorts – but at what price for the organisation’s legitimacy, and the future of international tax rules? I’ll discuss three scenarios, the implications of the announcement and the broader context. If you just want to read about the scenarios, skip to the bottom of this blog.

While the outcome is disappointing, it is of course not entirely surprising. The ‘Inclusive Framework’ is built on the OECD’s pledge that members would have an equal say – but even membership is premised on non-OECD countries that had no say in the first Base Erosion and Profit Shifting (BEPS) process, in 2013-2015, having been forced to accept and implement the BEPS outcomes. It cannot be shocking, then, to see the OECD secretariat’s ‘unified proposal’ now confirmed in place of the work programme agreed by the Inclusive Framework last year. But a range of implications flow from this, and they are largely not positive for the OECD – although they may, eventually, set the stage for more positive global tax outcomes.

Immediate implications for the OECD process

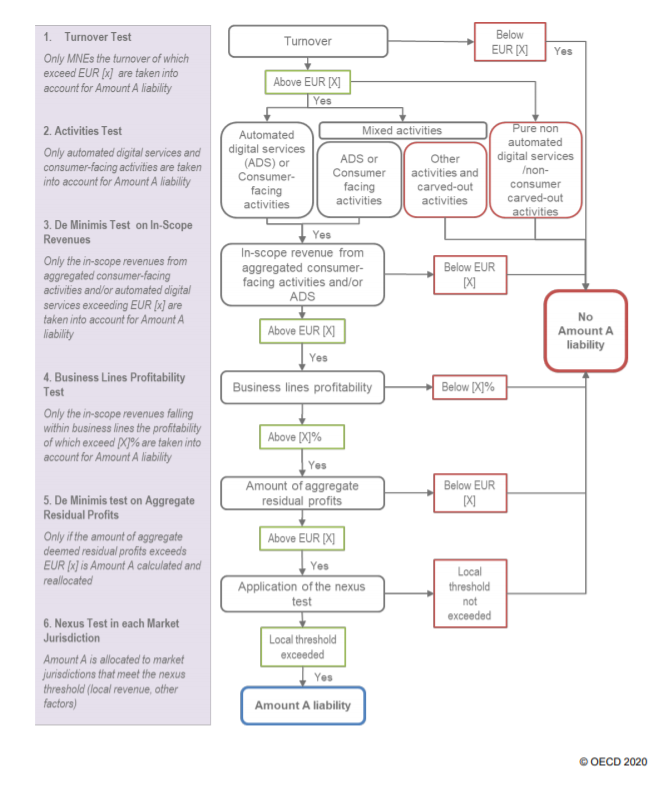

In terms of the OECD process, there is an insistence that things stay on schedule – that is, that everything must be wrapped up by end-2020. But there are so many, quite large things still open in Pillar One, from the scope of industries to be covered to the range of financial thresholds.

The 11 elements of work remaining on pillar one demonstrate how much is still open, even after the Inclusive Framework has been forced to drop its own work programme.

Even now, the work plan remains extremely ambitious. Taking into account that the public consultation saw strong and widespread objections on everything from the scope of Pillar One, to thresholds, to concept of dispute resolution mechanisms, only further brute force will obtain a 2020 conclusion.

One implication of these interacting pressures seems likely to be a tendency towards the lowest common denominator: that is, the need for quick agreement across a whole range of issues will set a tendency towards narrower scope, higher thresholds and less substantial redistribution.

And this is without mentioning that the US proposal for ‘safe harbours’ (or opt-outs for multinationals, if you prefer) is still noted in the OECD document. Unless the agreement was to note it and then never mention it again, that might well threaten the process down the track. There has been no suggestion that the US is ready to drop the idea, despite widespread opposition from other OECD members.

On Pillar Two, things remain very wide open – there’s not much new detail in the document, just an indication that work continues. One very welcome element: “Working Party 11 has set up a special subgroup on financial accounts.” An important technical issue that has come up in the process is the weakness of international accounting standards, or more specifically their failure to provide a common basis for any kind of unitary tax approach. It is fundamental for progress and any hope of certainty for tax authorities and taxpayers, that the negotiations can reach a common position on the data that will be relied upon.

Broader context

Stepping back, the broader implications of the politics seem larger than the technical challenges that remain. A quick look at the timeline:

2018: Comprehensive recognition, including from the OECD and with US support, that global reforms are needed and – crucially – that they must ‘go beyond the arm’s length principle’. This is a truly momentous shift, finally agreeing to unpick the League of Nations decisions of 1920s and 1930s that imposed the separate entity approach and with it the path to increasingly unsustainable transfer pricing approaches as multinational companies became increasingly global, complex and structured to avoid. The framing, in a commitment to a fairer distribution of global taxing rights, is equally significant.

January 2019: The Inclusive Framework agrees a work programme with three proposals on Pillar One, including the G24 proposal for a relatively full unitary approach with formulary apportionment. All three proposals include a unitary approach; the big question is what element of transfer pricing may remain in place, if any.

Summer 2019: A deal between the US and France, subsequently backed by the G7 group of countries, becomes the basis on which OECD secretariat brings forward its own ‘unified proposal’. This eliminates the G24 approach and the rest of the Inclusive Framework’s agreed work programme, and replaces it with much more complex and uncertain arrangements, per the US-French position. The main attraction appears to be that the various issues of scope and amounts A, B and C offer the possibility of introducing a unitary element but without any significant shift in taxing rights – either away from the main corporate tax havens, nor towards the lower-income countries that lose the greatest share of revenues to avoidance, but still increasing revenues for OECD members.

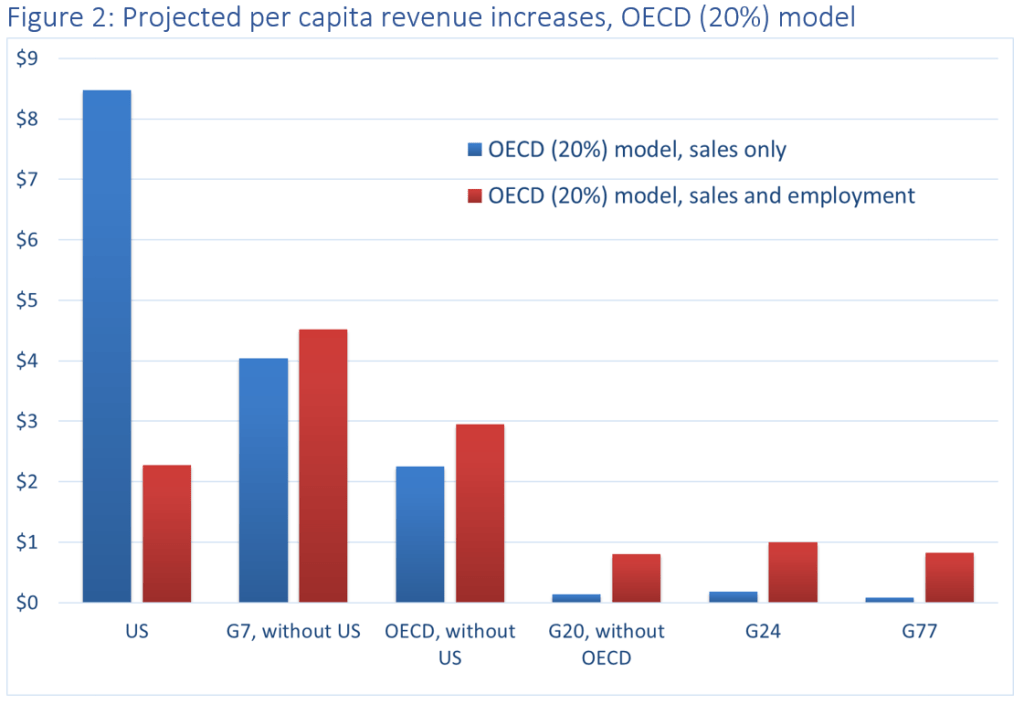

Autumn 2019: The subsequent public consultation and private responses, not least from G24 members, show widespread discontent with both the secretariat proposal itself, and the undermining of the agreed process. The failure ever to evaluate the Inclusive Framework work programme’s three proposals is a particular issue. For that reason, there is great interest and concern about our analysis, commissioned by ICRICT, that uses the only public data (on US multinationals) to show the potential implications of the new proposal. In our figure 2, we model a heavily simplified version of the OECD proposal (the blue bars) – and the implications are clear, with global inequalities in taxing rights actually exacerbated rather than ameliorated as once promised.

Finally, as we have seen, the US went back on the deal with France, and December 2019 and January 2020 have been spent in their public and private dispute and renegotiation, concluding only as the Inclusive Framework meeting begins.

Political implications

And now the Inclusive Framework has ‘agreed’ to go ahead with the secretariat’s ‘unified proposal’, tweaked for the US-French position which remains without full agreement, but with the continuing commitment to urgent finalisation within 2020. What does this mean for the current reform process, and the longer-term dynamics? There are two main aspects.

First, for the current reforms, there is a real risk. Most of the ambition, in terms of redistributing revenues away from tax havens, has already been sacrificed in the unified proposal – which brings complexity without benefits, especially for lower-income countries. But that weak and complex outcome may still come with a high cost – because the spectre remains of mandatory binding dispute resolution, which would tie the hands of lower-income countries in particular in the face of multinationals’ aggression.

At the same time, any promised benefits of Pillar Two remain at best uncertain – and quite possibly entirely ephemeral, if a global blending approach were to be demanded by the US and others.

Second, however, it is the broader political ramifications that may prove to be the most important. The questionable credibility of the ‘Inclusive Framework’ is in tatters. As the Indian delegate said last year, ‘just because you call something ‘Inclusive’, does not make it inclusive’.

The Inclusive Framework’s agreed work programme has been thrown out, in favour of a secretariat proposal designed purely to meet the demands of two big OECD countries, the US and France (the biggest member and the OECD’s host country). The OECD’s claims that Inclusive Framework members have an ‘equal say’ have been shown to be completely hollow. The complete elimination of the G24 proposal in particular, and the Inclusive Framework’s forced acceptance of the unified proposal this week, has confirmed lower-income countries’ irrelevance at the OECD.

It’s hard to see how any future OECD process can make any credible claim to be inclusive. A good many OECD members may feel excluded; while the remaining Inclusive Framework members probably feel that their presence has done nothing but allow the OECD to bolster its claims to legitimacy.

Listening in the morning’s press conference to Pascal Saint-Amans talk about the importance of this agreement to avoid a (US-France, or global) trade war, you can only feel sympathetic. Within the problems facing the secretariat was a tradeoff between being vaguely inclusive, or addressing this threat. But that dynamic will always exist at the OECD, and so claims of inclusivity of non-members will never ring true. The comprehensive demonstration this week that the Inclusive Framework can simply be bent to OECD members’ perceived priorities has surely removed any last doubts.

Where next? Scenarios and opportunities

A major question now is where the next global tax talks after 2020 will take place. Such talks will certainly be needed, even if the timetable for BEPS 2.0 can be kept, and the OECD seems unlikely to be able to claim ‘inclusivity’. In the absence of new talks, and perhaps also in their presence, an explosion of unilateral measures seems the most likely outcome.

Those countries pursuing DSTs (digital services taxes) seem at least to have obtained some of the Trump administration’s attention, and so far no punitive response – confirming the value at one level of unilateral actions.

At the same time, the continuing resistance of OECD members to any meaningful UN process on international tax rules seems unlikely to dissipate any time soon. As the high-level participants at our virtual conference in December concluded, things will not be fixed by this OECD process – but ‘the genie is out of the bottle‘ as far as unitary taxation is concerned.

We had earlier identified three scenarios for the OECD process:

Limited reform. In this scenario, intended to meet US demands, the secretariat would deliver a reform that would redistribute little profit from tax havens, with some revenue benefit for major OECD countries and little for anyone else.

Process collapses due to lack of trust. In this scenario, the refusal to allow G24 countries or others the ‘equal say’ promised to the Inclusive Framework would be met by a rejection of the secretariat, and ultimately a collapse of the process.

Reset. Here, the threat of collapse would see the secretariat forced to make concessions to the Inclusive Framework. This would necessarily include a longer timeline, recognising that 2020 is simply too short for such a major overhaul of the rules, and an agreement to evaluate fully the three proposals that the Inclusive Framework had agreed to consider, including that of the G24.

As things stand, the secretariat has avoided scenarios 2 and 3 for now. The Inclusive Framework has been forced to accept the path to limited reforms on the basis of US-French dominance. Scenario 1, an agreement of sorts by end-2020 is now more likely; but it is also certain not to be the last word.

The Inclusive Framework has, perhaps, one last chance to bring concerted pressure to bear by June 2020. It’s conceivable that the G24 could demand a reopening of the issues and also the timeline, so that there could actually be an evaluation of the revenue implications of different proposals. A public demonstration of discontent might be worthwhile, despite the likely rebuff.

The chances are, in either case, that there will be no reset, and therefore no prospect in this process of considering the more full unitary approaches that would deliver meaningful redistribution of taxing rights, as was the initial promise of the negotiations. But that does not make this a success for those who favour minimal change from the status quo: the more complex and limited the outcomes of the OECD process, and the greater the insistence of the multinationals on binding dispute resolution, the greater the chance that this proves to be, for the OECD and its main members, a truly Pyrrhic victory: a deal that creates great uncertainty itself, and is followed immediately by multiple unilateral measures.

The OECD should be congratulated for holding things together this week; but the longer-term implications seem likely to be substantially damaging for international tax coordination, and for the organisation’s credibility as a broker of reforms.

Meanwhile, a number of G24 countries and others will currently be discussing their next moves – and it seems inevitable that much of their analysis will focus on options outside of the OECD and the Inclusive Framework. The Tax Justice Network, and the broader tax justice movement, will be active in supporting technical and political discussions alike. The upcoming Bangkok conference of the Financial Transparency Coalition can provide an important moment for broader evaluation.

Over the next year, the recently announced UN high-level panel on financial accountability, transparency and integrity (FACTI) will work to identify key priorities to address gaps in the international architecture that impede progress against illicit financial flows – including the major component which stems from the tax abuses of multinational companies. With power dynamics at the OECD laid bare this week, FACTI has a clear opportunity to propose a UN tax convention that would lead to a new, and globally representative forum for future policy negotiations.

No início de cada ano no Brasil, as prefeituras começam a cobrar o Imposto sobre a Propriedade Predial e Territorial Urbana (IPTU). Mas quanto se arrecada e para onde vai o dinheiro arrecadado? É sobre isso que vamos falar no episódio 9 do podcast É da sua conta.

O IPTU é um tributo que poderia ser muito mais importante para as cidades brasileiras, já que 45% de sua arrecadação é usada para financiar educação e saúde públicas. Mesmo assim, os municípios têm alíquotas baixas e quase não arrecadam IPTU. Esse imposto também sofre muita sonegação, o que acaba comprometendo serviços públicos, investimentos em infraestrutura urbana e a política de moradia. O que algumas prefeituras fazem para reverter esse quadro? E o que poderia ser feito para melhorar a arrecadação?

Uma das alternativas é a progressividade na cobrança do IPTU. Internacionalmente, apresentamos a proposta de tributação sobre o valor da terra de forma complementar no sistema tributário com o nosso colunista Nick Shaxson.

No É da sua conta #9 você ouve:

Como funciona a tributação do IPTU e para onde vai sua arrecadação.

Receita de IPTU no Brasil atinge 0,65% do PIB, enquanto em países da OCDE chega a 2% do PIB.

Dívida e sonegação: os desafios para a implementação do IPTU progressivo.

O IPTU, a função social da propriedade e o direito à moradia

Índice de qualidade de arrecadação do IPTU e atualização de seus valores.

Questão habitacional: a situação do centro de São Paulo.

Exemplo internacional: o imposto sobre o valor da terra.

Tema da próxima edição: Índice de Sigilo Fiscal 2020 da Tax Justice Network.

Please find our research and resources below. Some research and resources will be added in the coming weeks ahead of the launch of the index. All content, resources and information provided and linked to on this page are strictly embargoed for 18:00 CET Tuesday 18 February 2020.

These documents are password protected and require the same password used to access this webpage.

After three and a half years of acrimony, Brexit will become a reality in just a few days time. January 31st will be a historic moment, for both Europe and the United Kingdom, marked by jubilant celebrations in some circles and profound misgivings in others. One very small but extremely powerful grouping within British society is likely to be delighted that the independence they have long desired has finally been achieved; alongside a variety of fringe ethno-nationalist organisations that long to stop migrants from coming to Britain, the UK’s bloated, regulation-light finance sector and freemarketeers around the world are excitedly looking forward to Capital being able to move in and out without any limitations or oversight imposed by pesky EU regulations. It remains to be seen whether the EU will use its power to try to scupper their plans although all around the world, those who work for greater social justice and human rights fear that the City of London, with the active support of its allies in the UK government, will move hastily to transform itself into an even more pernicious facilitator of abusive international tax practices, thereby accelerating the race to the bottom among nations on tax, secrecy and regulations.

As the world’s economic elite met in Davos recently to discuss the future of the global economy, a gaggle of international journalists was touring the City of London to find out what Brexit might mean for ordinary people. The Brexit Tax Haven Tour was organised by the Tax Justice Network and the Global Alliance for Tax Justice together with Tax Justice UK, Women’s Budget Group and Womankind Worldwide, taking international press on a walking tour of key sites in the City of London where they heard about the real and imminent threat posed to poorer/plundered and industrialised countries alike by the UK government’s ‘Singapore on the Thames’ strategy.

Speaking at the Bank of England, the Tax Justice Network’s John Christensen explained the peculiar history of this curious institution, which acts as both a central bank and also as a banking regulator, but has done little to counter London’s role as a global money-laundering centre, resolutely ignoring the global risks posed by Britain’s global tax haven network. When considered as a whole, Britain’s network of tax havens and financial secrecy jurisdictions represents the largest and most deleterious tax haven in the world, denying poorer/plundered countries billions of dollars in revenue every year and siphoning away resources urgently needed in all nations for climate change adaptation, economic and social progress and the fulfillment of basic human rights. Look out for the Tax Justice Network’s Financial Secrecy Index 2020 results out soon to see how the UK ranks this time as a global corruption offender.

Following the Bank of England, the walking tour took journalists to the Maternité statue, Aimé-Jules’ 1878 depiction of a French peasant woman breastfeeding, which is nestled discreetly, and without any deliberate irony, behind the rather more imposing Bank and the Royal Exchange. At this stop, Womankind Worldwide’s Roosje Saalbrink explained the disproportionate burden of unpaid care work imposed on women by unjust tax policies, and the danger of this trend being further exacerbated by increased regulatory ‘competition’ among states.

Feminist economist Susan Himmelweit of the Women’s Budget Group then elucidated the role the City of London plays in pillaging resources from poorer countries, and thereby preventing them from providing the basic social services that are fundamental to confronting inequality for women and girls. As she explained, countries that are unable to raise enough revenue from businesses through corporate income taxes often have to resort to implementing higher taxes on working people through more regressive forms of taxation such as VAT, or through myriad fees and special charges paid only by local residents. Women living in poverty, who generally have lower incomes than men, are doubly disadvantaged by such revenue generation measures.

The final stop of the Brexit Tax Haven Tour took us to Guildhall Square, site of the City of London Corporation building, which is the administrative hub of this “city within a city”. At this stop Dereje Alemayehu, Executive Coordinator of the Global Alliance for Tax Justice, explained the machinery of international tax abuse that is managed from the site and the serious threat that the City of London poses, in pursuing its ‘Singapore on the Thames’ ambitions, to become “the capital of financial secrecy”.

As things already stand, countries in the Global South lose one trillion dollars every year because of capital flight and tax dodging. In Africa alone, between US$ 30 and 60 billion per year is transferred illicitly which is equivalent to 40 years of the development funding the continent currently receives every year. These figures are likely to rise post-Brexit.

As the afternoon’s activities drew to a close, and the mega-rich continued their conversations 700 miles away in Davos, a protest illumination bearing the words ‘Tax Haven Britain: A threat to us all,’ appeared first on the City of London Corporation building and then on the Bank of England. It remains to be seen whether the world’s elite will see fit to hear this crucial message. Davos organisers notably opted not to invite economist Rutger Bregman back to this year’s event after he argued, at the previous 2019 meeting, that tax justice was the only way to confront the multiple crises now afflicting the world. Here’s a reminder of his comments which resonated strongly across the world:

You can watch Al Jazeera’s coverage on Bregman’s comments and on the politics of how the media report tax here:

Change always comes from the bottom, never from the top, and citizens must continue to add to the pressure on governments to serve the public interest.

If the situation collapses in Europe then I don’t think the tax havens, secrecy havens and the US will be in any rush to try and repair the situation.”

We are in the longest struggle, social conflict in France. Imagine it’s something that is longer than what happened in 1968. What we are afraid of is that it’s a strategy to weaken our system. In France, the social security, all the money in the system of social security is more important than the state budget of France – imagine what some people of the financial place would like to do with that money.”

It’s really a question that arises now in France how all those governments and presidents that we have are not chasing tax avoiders, the big multinationals. The big multinationals, people know them and when they find out that those multinationals pay virtually no taxes in France they think it’s appalling. Whether its public schools, public health, public infrastructures, the justice system, and pensions, Macron could fund them with a proper tax justice policy.”

I’m afraid with the massive victory they got on Brexit, they are emboldened to be the capital of international secrecy. And I’m afraid they will make things worse for the rest of the world without benefiting the UK economy.”

There’s ample evidence that inequality harms the economy…inequality is now actually threatening to topple the whole thing and turn the whole thing over.”

~ John Christensen of the Tax Justice Network on the head of the IMF’s warnings on another Great Depression

Want to download and listen on the go? Download onto your phone or hand held device by clicking ‘save link’ or ‘download link’ here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher.

Join us on facebook and get our blogs into your feed.

The International Consortium of Investigative Journalists (ICIJ) has today published a set of reports based on 715,000 leaked documents about Angola, and particularly Isabel dos Santos, the daughter of former President José Eduardo dos Santos.

In summary, dos Santos enjoyed tremendous Angolan state largesse to amass a large fortune overseas, using more than 400 shell companies and other structures — 94 in recognised tax havens — to park or hide assets. The story once again highlights a menagerie of ‘enablers’ such as the Big Four accounting firm PwC, and Boston Consulting Group, to help her. Dos Santos has denied looting the country.

Newspapers around the world have picked up the story, and we

won’t add to the details at this stage. However, we will provide two

important bits of context, which will almost certainly have been missed.

First, here’s an excerpt from an IMF report in 1997 (not long after your humble TJN correspondent had served as Reuters‘ and the Financial Times‘ resident reporter in war-ravaged Angola.)

Source: IMF

In other words, minerals accounted for 99.4 percent of Angolan exports! One might be tempted to excuse that shocking, astonishing figure, given that Angola had been in the throes of a large-scale civil war since independence in 1975.

One also might have expected this to have improved

significantly today. The war ended decisively with the killing of rebel

leader Jonas Savimbi in 2002, and Angola has undergone a massive

oil-fueled (and Chinese-enhanced) reconstruction effort.

Has this helped Angola diversify its economy?

That is, of a (nominal) $487 billion in estimated exports

from 2010-2019, just $2.7 billion did not come from petroleum or

diamonds. In other words, 99.4 percent of Angola’s exports come from its

minerals.

The end of the war and reconstruction does not seem to have dented Angola’s capacity to build a diverse economy. Angola provides a stark illustration of the infamous Resource Curse, a.k.a. the paradox of poverty amidst plenty.

This failure has many causes, but there can be no doubt that kleptocracy – and by extension the enabling role of western (and

other) banks, law and accounting firms, real estate agents, tax havens and many others – carry a large share of the blame.

Two more things.

First, it has become increasingly clear – from this set of stories, and from

others – that we need to turn our attentions increasingly to Dubai

as a paradise for the world’s ne’er do wells. Our imminent Financial

Secrecy Index will provide more details.

Second, if western countries are going to crack down on these activities, given the scale and power of the vested interests that enable this stuff, it will never be possible to crack down effectively based on altruistic ideas about helping poor people in countries like Angola. A far more powerful approach comes through understanding the Finance Curse. For more on that, read this recent Guardian article, or this longer piece for the IMF, both by today’s TJN blogger. And there’s more on the “blowback” into western democracies receiving this dirty money, in this TV debate.

The United Nations Commission on the Status

of Women (UN CSW) 64 is coming round soon. This annual event, held in New York

at the UN HQ from 9 to 20 March 2020, has special significance this year.

2020 marks the twenty fifth anniversary year of the Beijing Declaration and

Platform for Action (1995).

The Beijing Declaration and Platform for Action (1995) provides a blue print for our work on tax justice and gender justice. Its agenda is pivotal in directing the demands we must make on others – private sector, foundations, governments, international financial institutions and fellow actors in civil society for the advancement of women and gender justice.

As part of the preparation for the 2020 Beijing+25 review process undertaken with the cooperation of all signatory countries we have collaborated in the preparation of a brief Fact Sheet on Tax Justice and Gender Equality. Please share widely.

Remembering…

Paragraphs

from the Declaration which resonate with our work on tax and gender justice:

21

The implementation of the Platform for Action requires commitment from

Governments and the international community. By making national and

international commitments for action, including those made at the Conference,

Governments and the international community recognize the need to take priority

action for the empowerment and advancement of women.

26

Promote women’s economic independence, including employment, and

eradicate the persistent and increasing burden of poverty on women by

addressing the structural causes of poverty through changes in economic

structures, ensuring equal access for all women, including those in rural

areas, as vital development agents, to productive resources, opportunities and

public services

36

Ensure the success of the Platform for Action, which will require a

strong commitment on the part of Governments, international organizations and

institutions at all levels. We are deeply convinced that economic development,

social development and environmental protection are interdependent and mutually

reinforcing components of sustainable development, which is the framework for

our efforts to achieve a higher quality of life for all people. Equitable

social development that recognizes empowering the poor, particularly women

living in poverty, to utilize environmental resources sustainably is a

necessary foundation for sustainable development. We also recognize that

broad-based and sustained economic growth in the context of sustainable

development is necessary to sustain social development and social justice. The

success of the Platform for Action will also require adequate mobilization of

resources at the national and international levels as well as new and

additional resources to the developing countries from all available funding

mechanisms, including multilateral, bilateral and private sources for the

advancement of women; financial resources to strengthen the capacity of

national, subregional, regional and international institutions; a commitment to

equal rights, equal responsibilities and equal opportunities and to the equal

participation of women and men in all national, regional and international

bodies and policy-making processes; and the establishment or strengthening of

mechanisms at all levels for accountability to the world’s women

37 Ensure also the success of the Platform for Action in countries with economies in transition, which will require continued international cooperation and assistance;

The Declaration’s preamble is rich in guidance on gender equality and empowering women. Tax justice is part of the Declaration too. Since 1995 the development and engagement with the tax justice agenda (the four R’s: revenue, redistribution, repricing and representation) has come a long way.

No tax justice without gender justice; no gender justice

without progressive tax and financial transparency.

2020 is a pivotal year.

Registration

DEADLINE FOR UNCSW 64 IS APPROACHING – 27 January

2020!

If you are

interested in contributing to the preparation for UNCSW 64 and Beijing + 25

contact Global Alliance for Tax Justice: Tax and Gender Working Group contact Caroline

Othim

The IMF has just published a new Staff Discussion Note entitled “Finance and Inequality,” by Martin Čihák and Ratna Sahay. The shortest summary of its conclusions is: too much finance makes countries more unequal. And in the words of the IMF’s new Managing Director Kristalina Georgieva, introducing the study, rising inequality:

is reminiscent of the early part of the 20th century — when the twin forces of technology and integration led to the first Gilded Age, the Roaring Twenties, and, ultimately, financial disaster.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.