At the heart of tax justice is the idea that everyone, everywhere, should pay their fair share of taxes. When they don’t, it results in an increased tax burden on the compliant few, in a decreased availability of funding for fundamentals like access to schooling, healthcare and social safety nets, and in an increase in the reliance on third-party funding, which reduces a country’s sovereignty.

By contrast, if one were to craft a poster child for tax “injustice” it would probably look a bit like this: a corporate bully making products that kill half its clients, costing our governments more in healthcare than they make from tax revenues. Its business model would be built on illicit, untaxed supply lines, and shifting what profit it doesdeclare to tax havens. All the while illegally spying on its competitors, polluting our beaches and stripping our forests, and hopping in bed with North Korea. And it gets away with it because it has captured the very same governments that are meant to regulate them.

They exist, and are collectively referred to as “Big Tobacco.”

Their business model comes at the expense of other taxpayers. Healthcare costs exceed tax revenues from tobacco companies. There is no accountability for cleaning up the pollution they leave behind (with the financial burden instead falling on society). Their abusive profit shifting leaves them paying obscenely low effective tax rates. Their opaque supply chains let them freely pump cigarettes into illicit markets, no taxes or duties paid. And they use illicit financial flows to launder ill-gotten income.

Unwavering profitability

The tobacco industry is unwaveringly profitable. British American Tobacco, for instance, has been the best performer on the UK stock market over the past 35 years. In global terms, while the volume of cigarettes sold may have decreased, its value has increased. There is a simple reason for its continued success: the multinational tobacco companies are masterful at keeping both their supply chains and finances almost entirely opaque, emboldened by the criminality that is hardwired into its very DNA.

Tobacco is the most widely smuggled legal substance in the world, with profit margins on a smuggled (that is, tax free) container of up to 2,400 per cent – making it more profitable than heroin, cocaine or arms, but with far less risk of imprisonment.

Most criticisms of the tobacco industry arguably focus on their marketing of addictive, killer products, but there is so much more about them that is “unjust,” starting, perhaps, with the fact that their tax contributions don’t cover the healthcare costs that arise from smoking.

1. Taxpayers spend more on the healthcare costs of smoking than big tobacco contributes in tax

Excise duties are different from other taxes, in that their primary purpose is to drive specific behaviours, by taxing public “bads,” and to help to compensate for negative impact they have on our societies. So it makes sense that excise duties are levied on tobacco products.

Unfortunately, they don’t nearly cover the healthcare costs of smoking.

Instead, smoking is a net negative for most nations, costing the world more than US$ 1.8 trillion annually in healthcare expenditure and lost productivity. Smoking costs us – as taxpayers – the equivalent of 1.8 percent of global GDP, every year.

A research paper on the health and economic burden of smoking in 12 Latin American countries exposes how health-care costs attributable to smoking represent 6.9 per cent of the overall health budgets of these countries – tax revenues from cigarette sales cover only 36 per cent of these expenditures.

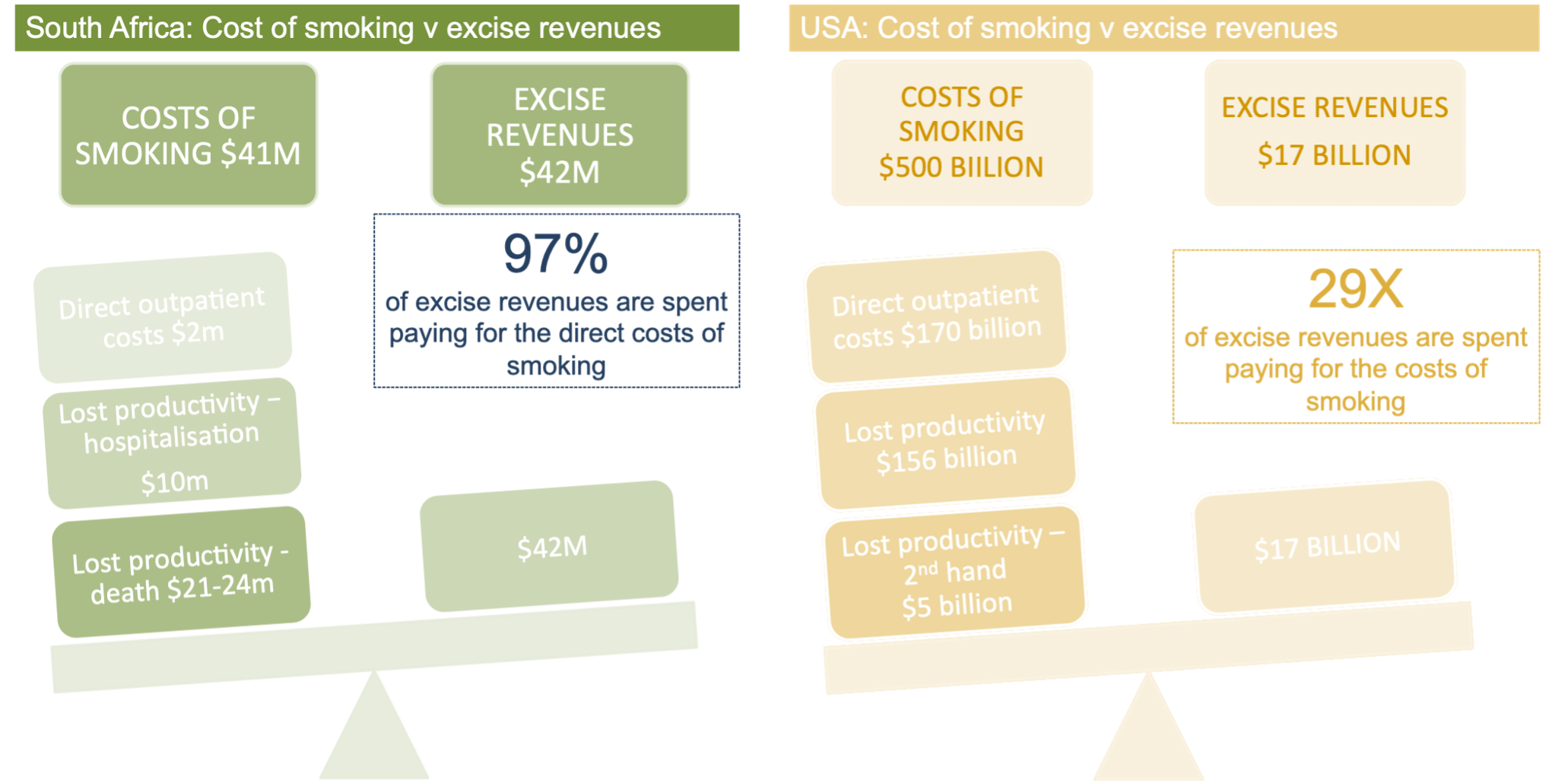

It is an easy enough analysis to replicate on a country by country basis, by comparing the cost of smoking to the excise revenues collected. In South Africa, for instance, 97 per cent of excise revenues are spent paying for the direct costs of smoking alone (in other words, not accounting for any of the indirect costs like loss of productivity or second-hand smoke). In the USA, more than 29 times the amount collected through excise duties is spent on healthcare for smoking-related diseases.

But of course, tobacco companies don’t only pollute our lungs, they pollute our beaches too.

2. The tobacco industry’s pollution costs millions to clean up

As Tobacctactics reports, the tobacco industry’s emissions are larger than those for entire countries, including Denmark and Croatia – comparable to emissions from the oil, fast fashion and meat industries; and the tobacco product life cycle releases 80 million tonnes of carbon dioxide equivalent every year. If cigarette production ceased tomorrow, it would be equivalent to removing 16 million cars from the roads each year.

This not being devastating enough already, more than 600 million trees [AC3] are cut down every year to cure tobacco leaves, and another 9 million trees to make matches. British American Tobacco, for instance, stands accused of being responsible for 30 per cent [AC4] of the total annual deforestation in Bangladesh, cutting down 200,000 hectares a year. The industry’s reforestation programs are having little discernible impact on deforestation, planting non-indigenous, thirsty eucalyptus trees which are not intended to replenish the destroyed forests but for use in tobacco curing.

“Polluter pays” is a principle in international environmental law aimed at making polluters pay for the cost of their environmental harms, which can be further broadened to make the producers of polluting products accountable for ensuring the product can be responsibly disposed of (as is the case, for example, with paint in the US).

Oluwafemi Akinbode of Corporate Accountability and Public Participation Africa has suggested that litigation against oil company Shell in the Niger Delta could provide a template for introducing a more just approach in the tobacco industry.

That should reasonably include commitments to:

Introduce climate justice perspectives in debates around tobacco regulation

Implement the “polluter pays” principle in the tobacco industry, and hold the industry to account for clean-up cost reimbursements

Introduce extended producer responsibility to make tobacco multinationals accountable for ensuring their product can be responsibly disposed of.

3. Big Tobacco underpays its taxes ever year

At the British American Tobacco annual general meeting in 2014 an activist asked, “Mr. Chairman, I note that BAT reports on the amount of corporation tax paid in the UK (which appears to be zero) and the amount of corporation tax paid overseas, without providing a breakdown of the countries comprised within the overseas heading. The Sustainability Summary states that ‘Transparency is important to us’. With the importance of transparency in mind could you let us know in what countries the company does pay corporation tax, and can you confirm whether the company would be open to providing a country-by-country breakdown of taxes paid in annual reports in the future?” BAT’s CEO responded simply that there was “no need to report globally.”

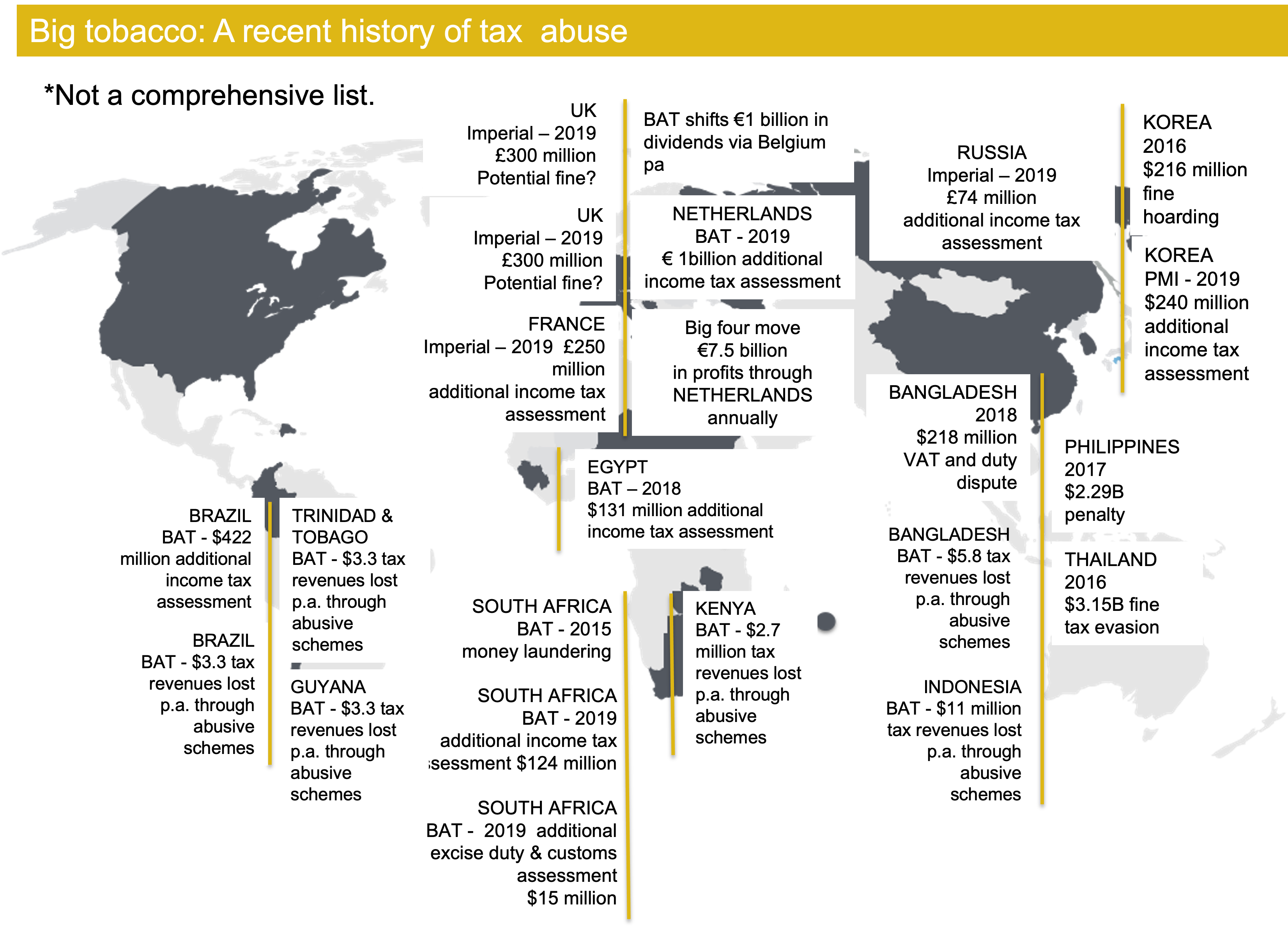

In our 2019 report, Ashes to Ashes, the Tax Justice Network estimated that in Bangladesh British American Tobacco managed to shift $21 million in profits through royalties and IT charges, costing the country $5.8million in lost taxes. In Indonesia, they shifted $73 million through loans and royalties, costing the country $13.7 million in lost taxes. By booking Brazil’s profits in Madeira, they managed to shift $110 million out of the country, costing Brazil $33 million in tax revenues a year. In Kenya, by shifting dividend payments to the tune of $26 million, they avoided payment of $2.7 million in local taxes annually. Over the course of a decade these practices could have cost countries around the world $700 million in lost tax revenues.

Companies pay themselves royalties, management fees and IT charges. They lend themselves money. They send profits back home, away from where the commercial activity takes place. There may often be no commercial substance to these payments, instead existing solely or mainly to reduce the groups’ tax liability. And while the schemes involved are similar to those used in criminal activities, they get away with it all because multinational companies can back up what they do with opinions from tax advisers that make it difficult to establish the intent necessary for a criminal offence.

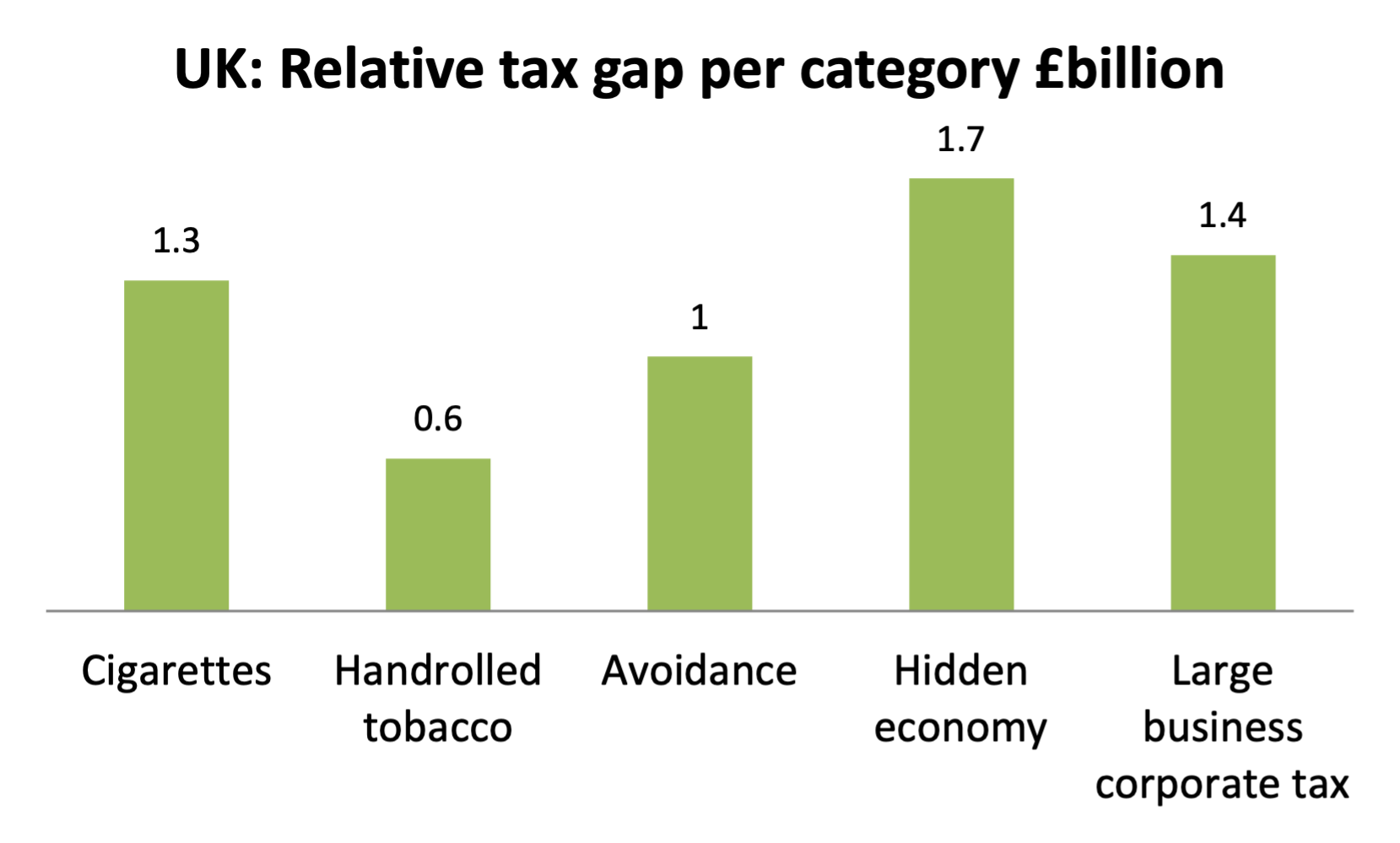

Grossly abused rules on taxpayer secrecy provide a veritable invisibility cloak to multinationals, making it extremely difficult to assess with any certainty the extent to which multinational companies are taken to task by tax administrations. While many of the investigations into their practices are opaque, there are some clues: estimates, like the ones in our report Ashes to ashes, and the comprehensive tax gap analysis done by HMRC in the UK; occasional disclosures by whistle blowers; and – historically – disclosures made by the companies themselves in their annual reports.

British American Tobacco unfortunately does not publish details of its contingent liabilities in its annual reports anymore, but when it used to, no fewer than 15 pages of their annual report were dedicated to listing tax abuse lawsuits it was defending across the globe. In the last report where these “contingent liabilities” were disclosed, they were facing an additional tax assessment of $124 million for aggressive tax planning using debt financing structures in South Africa, a $422 million income tax assessment in Brazil, a VAT and duty dispute to the tune of $218 million in Bangladesh, and a $131million tax assessment in Egypt. Altogether, the potential liabilities – should they fail to successfully challenge the assessments – total some $2.1 billion. That’s just for one year.

(The other Big Tobacco companies unfortunately don’t publish similar information. We back the tax standard of the leading international sustainability standards setter, the Global Reporting Initiative, under which companies’ uncertain tax positions should be reported, by country.)

In the following year British American Tobacco was sued by the Dutch government for €1billion for tax evasion (it had paid £1.6 million in tax on income of £1.6 billion – a tax burden of 0.1 per cent). British American Tobacco also shifts €1 billion in dividends via Belgium each year, again paying less than 1 per cent tax.

By underpaying tax at a colossal scale, Big Tobacco companies shift the tax burden even further on to the shoulders of ordinary taxpayers. This is tax burden made a lot heavier by the healthcare costs and environmental costs of smoking.

The Tax Justice Network’s recommendations in this area address both tax and transparency. We call for international tax rules to eliminate profit shifting by taxing multinationals according to the location of their real economic activity, and with an effective minimum rate. On transparency, necessary steps including public country by country reporting on the GRI standard, with full disclosure of uncertain and contested tax positions, and greater transparency about anti-abuse investigations of tax authorities.

4. Big tobacco knowingly supplies the black market

As much as 98 per cent of illicit trade in tobacco comes from legal manufacturing operations, many of which are owned, operated by or contracted by the four big tobacco companies, which continue to control more than 80 per cent of the world’s tobacco market. The math is obvious: if there is a significant illicit trade problem, it cannot exist without the involvement of the big four tobacco companies.

Indeed, evidence shows that the multinational tobacco companies are not only peripherally involved in supplying illicit markets, it is an explicit part of their business model.

This US settlement speaks only to the fact that British American Tobacco consciously and knowingly set out to circumvent sanctions. It doesn’t even begin to speak to the tax consequences of the “joint venture” in question.

There is nothing particularly shocking about this revelation, with questions about their involvement in North Korea and their dealings through Singapore having been raised for some time.

It’s a textbook example of the impunity with which multinational tobacco companies act: selling killer products in a prohibited market, then laundering the profits, all while paying little to no domestic duties on the cigarettes sold, or income tax on the downstream profits.

There is incontrovertible evidence of multinational tobacco companies benefiting from the smuggling of their own packs: in some instances, through “indiscriminate sales” where they choose not to track how the packs end up in illicit supply chains, but more often through structured, planned, organised schemes selling what they colloquially may refer to as “duty not paid” cigarettes, through corporate structures aimed at making their supply chains as opaque as possible.

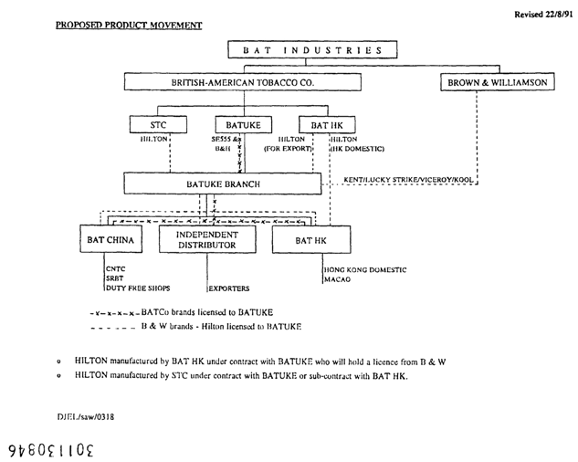

Schemes like the one British American Tobacco ran in North Korea. Or their well-documented structure in the 1990s which explains how they did something similar through Hong Kong.

It’s a pattern of behaviour that is consistent, if nothing else.

“I believe you are the least credible witnesses that I have ever seen come before the committee of public accounts. You have lied unashamedly. If you did not know all I can say is that you must have been totally incompetent. If I were one of your shareholders I would say, ‘these guys are incompetent.’”

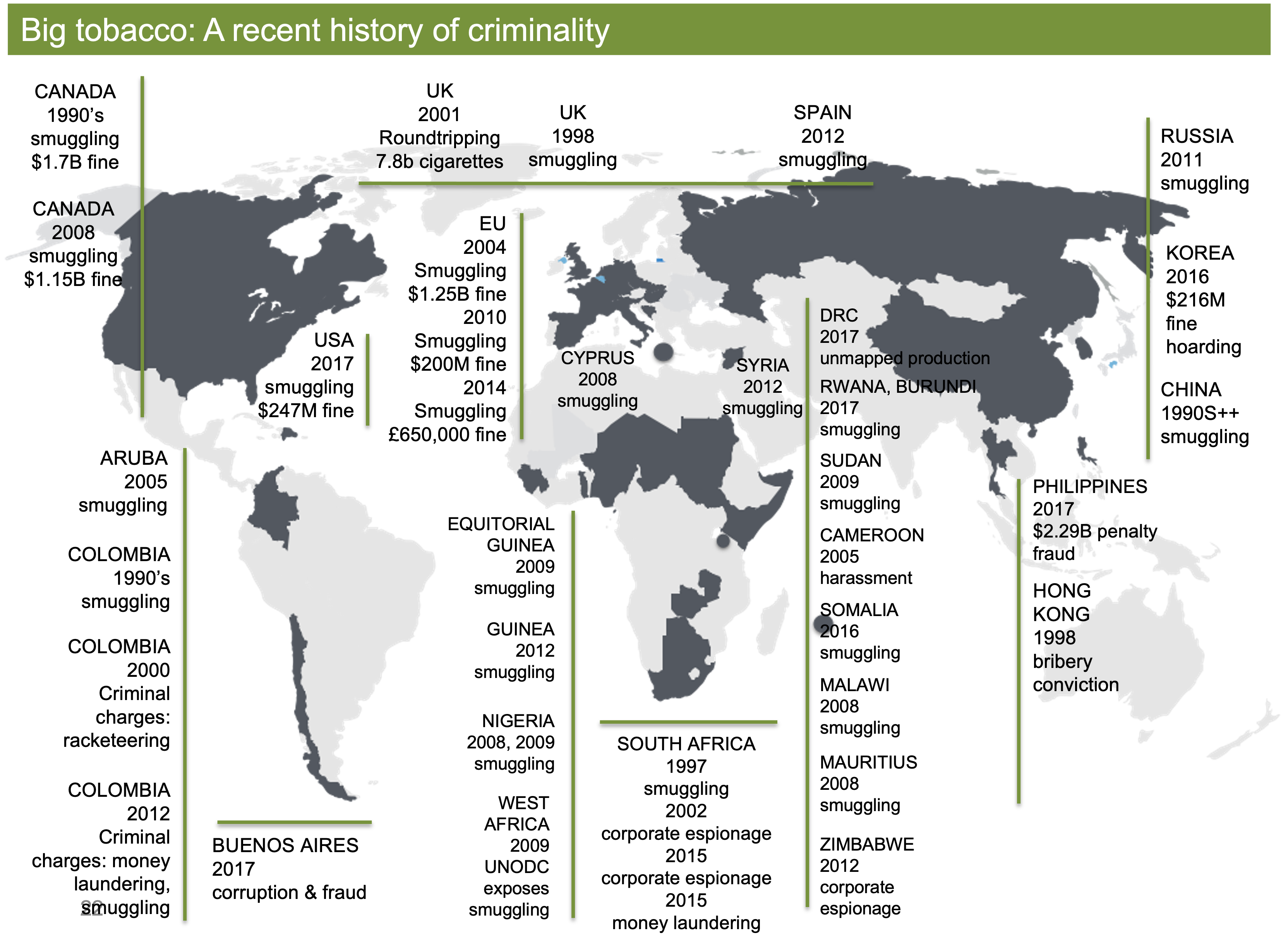

The four big multinationals have faced credible smuggling charges in at least Canada, Aruba, Colombia, the US, Buenos Aires, Equatorial Guinea, Guinea, Nigeria, the DRC, Cyprus, Syria, South Africa, Rwanda, Burundi, Sudan, Cameroon, Somalia, Malawi, Mauritius, Zimbabwe, Philippines, Hong Kong and Russia.

“Management of BAT was aware duty-not-paid cigarettes would ultimately be smuggled in China and other countries. There could be no other explanation for this enormous quantity of duty-not-paid cigarettes worth billions and billions of dollars. BAT’s irresponsible behaviour amounted to assisting criminals in transnational crime.”

British American Tobacco’s own documents suggest that the company may historically have been involved in smuggling in around 30 countries. BAT’s own managers note how smuggled cigarettes accounted for nearly 30 per cent of BAT’s sales in Canada, and accounts suggest that at one point as much as 25 per cent of BAT’s global profits may have come from selling contraband in China. Multiple sources document their strategies in China, including memorandums that explicitly explain eg, “…alternative routes of distribution of unofficial imports need to be examined.” That is just code for “smuggling.”

5. Big tobacco’s illicit financial flows allow dirty money to seep into the global financial system

As the UN notes, once illegal money has been laundered through the global financial markets – as some 70 per cent of illicit income in fact is – it is much harder to trace its origins.

In the simplest terms, it is virtually impossible to generate illicit income – in this case, from sales on the black market – and not create some kind of illicit financial flow. That income has to be accounted for somewhere, to ensure that the company’s shares remain popular.

“Defendants created a circuitous and clandestine distribution chain for the sale of cigarettes in order to facilitate smuggling. The decision to establish and maintain this distribution chain was made at the highest executive level of PMI. Defendants have collaborated with smugglers, encouraged smugglers, and sold cigarettes to smugglers, either directly or through intermediaries, while at the same time supporting the smugglers’ sales through the establishment and maintenance of so-called ‘umbrella [cover] operations’ in the target jurisdictions.”

In 2015 British American Tobacco was accused of money laundering in South Africa.It paid a network of undercover agents using Travelex cards registered overseas – but in other people’s names, so that the payments could not be traced. One agent, for instance, received at least £30,500, either in cash or loaded on to Travelex cards registered in the name of a BAT employee in the UK. An information request from HMRC in the UK confirms that the agency identified at least eight South Africans who had a “peculiar relationship with BAT” and received payments from BAT through “concealed transactions.” UK tax authorities described these as an “al-Qaeda-style” method of payment. Correspondence between the agent and BAT shows she became worried about BAT’s surreptitious payment methods. A senior BAT employee assured her that the same method of payment is used by BAT UK around the globe for payment of its other undercover agents.

These illicit financial flows come at a cost – they reduce transparency, making it impossible for our tax administrations to properly assess the taxes due by behemoths like British American Tobacco. But they do more than that: they allow listed companies to engage in purely criminal behaviours.

Conclusion

Big Tobacco’s behaviour is the very definition of “unjust.”

Multinational tobacco companies pose an enormously complex risk – one that includes elements of illicit trade, but one that goes far beyond just that. There is ample evidence of multinational tobacco companies being involved in smuggling their own product. But what lies beneath that is a series of smoke and mirrors that covers how they illegally spy on their competitors, how their structures allow them to pay virtually no corporate income tax, how they inflate sales volumes through fictitious revenue schemes, how they abuse their relationship with tax agencies to secure even more preferential treatment, and how their tax abuse is hardly distinguishable from the criminality perpetrated by organised crime syndicates.

Ultimately, the end result from both their more sophisticated schemes and their dalliances with illicit trade are the same – monies lost to the state, and us as taxpayers having to bear more of the tax burden.

There is something fundamentally unjust about the way in which multinational tobacco companies engage with our tax systems. Complex structures allow them to shift profits and underpay corporate income tax, while opaque supply chains allow them to move billions of cigarettes untaxed. Policies meant to curb tax abuses are diluted and rendered ineffective through relentless lobbying and corruption. Enforcement agencies are coaxed to look the other way with donations of vehicles or are plied with evidence on their smaller competitors, illegally obtained through their corporate espionage programs.

This year on World No Tobacco Day, we say no to multinational tobacco companies shifting obscene amounts of profits. We say no to opaque lobbying and engagements by multinational tobacco companies. We say no to tobacco companies capturing our enforcement agencies. And we say no to opaque supply chains and opaque global financial systems that provide them with an invisibility cloak.

Image credit: Tuxedo Tobacco, Public domain, via Wikimedia Commons

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app. All our podcasts are unique productions in five languages: English, Spanish, Arabic, French, Portuguese. They’re all available here. In this edition of the Taxcast:

When dominant multinationals get to run the world, it’s not a happy place. Or a very secure one. For a long time governments have failed to take the threat from monopolies and the corporate concentration of power seriously, and deal with it. But recent crises have demonstrated how the neoliberal era is crumbling around us and governments must take action. In this episode we look at the challenges and how to tackle this in the public interest.

And, in the US, Minnesota nearly took a historic step for tax justice this month that could have changed everything by bringing corporate profit shifting to heel. The lobbyists said it was the end of the world as we know it – and sadly, they won – for now. What was the big deal? And what are the possibilities for other states and other countries?

Naomi: “Hello and welcome to the Taxcast, the Tax Justice Network podcast. We’re all about fixing our economies so they work for all of us. I’m your host, Naomi Fowler. You can find us on most podcast apps. Our website is www.thetaxcast.com You can subscribe to the Taxcast there, or you can email me on [email protected] and I’ll put you on the subscriber’s list. Let me know what you think of the show! Coming up later on the Taxcast – the state of Minnesota nearly took a historic step for tax justice this month. But the lobbyists won – for now:”

Alex Cobham: “If you’re a big four accounting firm or one of the major law firms that support multinational companies in their tax abuse, this is guaranteed to freak you out. What you want is to make sure that nobody ever tries it, that they feel the threat, the pressure before they get to that decision point, and they don’t go ahead. You tell them everything will go wrong for you, you tell them anything!”

Naomi: “Aaaah it was so close! We’re going to talk about that later. But first, the threats from monopoly power. A world where dominant multinationals get to run the world isn’t a happy place. Or a very secure one, as it turns out. For such a long time governments have been absent from taking the threat seriously and dealing with it. In the United States what they call the ‘anti-trust’ movement has a long history – the Biden administration has actually been much more active in protecting people and the economy, more than any administration in decades actually, there’s a VERY long way to go, obviously. But everywhere really, the threats posed to us all from monopolies just aren’t that well understood, some of the effects on our lives aren’t that obvious. And really, it’s more accurate to call it ‘concentrated market power’, ‘cos we’re talking about saturation by only a handful of companies in each sector. So what does that look like? Well, according to one estimate we’ve got a problem when only four companies are getting 40% of sales. That’s a market that’s distorted and it’s lost its competitive character.”

Nick Dearden: “The increasing build-up of corporate power, the increasing concentration of corporate power over lots of different bits of our economy over many years is actually the central feature of our economic system.”

Naomi: “This is Nick Dearden of Global Justice Now:”

Nick Dearden: “If four corporations have cornered the entire global market in grain, they effectively decide what gets grown and how, they decide what food we buy and at what price. They decide what we eat. And indeed who doesn’t eat. And you can apply that logic across the whole economy.”

Naomi: “It sounds a bit simplistic to say this but it seems like we only have one value – and that’s the sacred right to make a profit, no matter who gets hurt or killed. The climate crisis and lack of proper action is an obvious example.”

Nick Dearden: “Yes, and it’s endangering our very existence on this planet. And if we’re honest, you know, big business does not operate in any kind of a free market whatsoever.”

Naomi: “It’s often hard to see the era you’re living through when you’re in it, but we’ve been living through a neoliberal era for a very long time. But now it’s beginning to crumble. Here’s journalist Nick Shaxson, formerly of the Tax Justice Network and now with the excellent Balanced Economy Project. He’s speaking here at Yale University and describes here the kind of waking up with a hangover from the big party the night before…”

Nick Shaxson: “The new idea was that we should stop worrying about democracy, we should stop worrying about power, we should stop worrying really about the structure of markets and we should boil everything down narrow everything down to consumer prices and as long as consumers are happy everything’s great, and we should also focus on the internal efficiency of corporations, if corporations are efficient then they’re going to spread their wealth around and everything will be fine, so don’t worry about these other issues. This story, that was one of the components of what many people call neoliberalism, spread rapidly, it was obviously very well funded and it became the dominant narrative and it effectively allowed for the massive consolidation that we’ve seen since then. Private equity firms were among the drivers of this consolidation, buying up firms all over the place and bolting them all together, but many other drivers of consolidation. There was effectively a falling away of the state, the state decided to stand back and this was both under Republicans and Democrats, all the way up to the Trump administration. And so you had this story that once you start picking at it’s so obviously incoherent, it’s obviously wrong but power was with it and it carried, it survived and flourished across the world, spread across the world, spread to Europe, spread to other countries to Australia to Asia, to lower income countries and so we have the giants of today and there’s pretty much no government anywhere has been effectively cracking down until very recently. So the new movement came along with this new story saying ‘we need to start thinking about power again, we need to start thinking about democracy, we need to start thinking about the structure of markets and we need to start taking down these giants and regulating with confidence again in the interests of people.'”

Naomi: “Yes! Obviously the most recognised monopolies are easy to see because they clearly wield too much power – like Facebook, Amazon and Google. And not all monopolies are a bad thing – I mean, a well-run state healthcare monopoly that has the buying power to keep medical costs down and tackle pharmaceutical giants seems like an undeniably good thing. The National Health Service here in Britain is humanity at its very best, I’ve seen that for myself. And we used to have public-owned railways, public-owned water – sadly we lost those. But we can’t say all state-owned monopolies are run in the public interest in the ways they should be – we’ve got creeping private sector involvement, and sometimes the same extractive processes as any other dominant company. So our solutions must be about enshrining rights to essential things we all need, keeping them firmly in the non-profit sector. It’s gotta be also about democratising ownership and control, as well as – of course – breaking up corporate power where we need to.

And it’s bad. Very bad. In the States, despite the Biden administration being the most active for decades in tackling these big mergers – the top 1% of corporations make 81% of all sales and they own 97% of all assets. You can check out stats like that on www.businessconcentration.com – it’s pretty interesting. The biggest market players dominate our every waking hour – what we eat every day, how we travel, how we get our news and information, who we bank with, they influence what decisions our governments make, how much we pay for stuff, how much we fall short in tax revenues and the consequences of that. But if it seems like we’re taking on the impossible here, we’re not. As any good freedom fighter will tell you. Here’s Nick Shaxson again:”

Nick Shaxson: “I worked with the Tax Justice Network for many years. I started not quite at the very beginning but near the beginning, and it was just a tiny group of us and we had some demands and policy proposals that you know the powers, you know everybody said ‘oh that’s utopian nonsense, nobody’s ever going to do that’ and all of those proposals are now to one degree or another, with many gaps obviously, but have been accepted as mainstream policy by governments around the world. I’ve seen from the inside of a movement having you know some significant success and, you know, we made a lot of progress. Not as far as as much we want but the whole international tax justice movement, we did achieve a lot.”

Naomi: “That’s Nick Shaxson there, speaking at a recent event held by Global Justice Now called ‘the threat of monopoly capitalism.’ And you can’t really separate monopoly power and market concentration from tax havenry and corporate secrecy – all of them have happened because we’ve allowed huge imbalances of power across our economies. And just like tax havens and the companies who use them, it’s the same, it’s all about ‘escape’ – escaping things they don’t like – whether it’s taxes other small businesses pay, regulations, laws, accountability when things go wrong, transparency about how they operate or which politicians they’re funding. Here’s Nick Shaxson again:”

Nick Shaxson: “One of the things that I think is very important is that monopoly is – it’s like privatisation, it’s a form of privatisation, in a way privatisation of regulation because if you get a bunch of companies together and they form a cartel, their bosses collude to um rig prices or rig wages or whatever that is subject to public regulation, there’s anti-cartel laws and rules around the world and they can be stopped, they can be fined, they can be punished for that with public state regulation. But the alternative – and that’s what all the companies have been doing instead is just merging, they just join together and once they’re merged together it’s like a reinforced legalised version of a cartel and the public regulation has been pushed out, so we are seeing monopolisation as a kind of privatisation of regulation.”

Naomi: “Underlying the neoliberal era and globalisation was always the philosophy that markets will answer our needs and solve our problems. The pursuit of what’s the cheapest, with no other consideration – the State’s job is to get out of the way. But we’re finding out why that philosophy is so dangerous – and why markets left to their own devices can do the opposite of solving our problems. Here’s Nick Dearden again:”

Nick Dearden: “You can take a number of different sectors and look at it and, and see the problems. But what was really interesting to me about the pharmaceutical example was the more I started looking into it, these pharmaceutical corporations like to say, ‘we need these monopolies because otherwise we’d have no incentives to provide the medicines that society desperately needs.’ And it’s a complete and utter lie. Actually, the more power they have accumulated, the less creative, the less inventive they have become. It isn’t simply a matter of, they make some really important medicines and then they squeeze as much profit out of it as they can. That was may be the case in the 1960s and 1970s. Today, it’s not like that at all.”

Naomi: “Yes, we’ve seen how big companies put their efforts into financialising every aspect of what they do, and that includes minimising their taxes. Pharmaceutical companies – just like in pretty much every sector – have merged to the point where in the US between 1995 and 2015, 60 pharmaceutical companies merged into just ten. The number of companies producing vaccines fell from 26 in 1955, to 18 in 1980, to only four in 2020. Do you remember that urgent chasing of covid vaccines by different nations? This stuff left the world at a huge disadvantage dealing with Covid, especially poorer nations.”

Nick Dearden: “Pharmaceutical corporations are more like hedge funds. They don’t do, they don’t invent any of the medicines, you know, or very few of the medicines on their books, they buy out other companies that have done that research, they then sit on literal monopolies, I mean, you know, through the intellectual property, basically only that that company can make this medicine for at least 20 years. And there’s all sorts of ways that they try to extend that, and they squeeze as much out of it as they possibly can, because they’re making so much on every single sale, if you can only sell it to a few rich countries’ health systems, well, that’s okay, you know, and actually the very value of these companies comes not really from how much they sell, but from the value of the intellectual property they hold and how much investors assume that’s gonna be worth in the years to come. So it’s extraordinary really, because this system is supposed to be all about, you know, rewarding innovation. But what it’s actually done is completely hollowed out these enormous corporations. And I mean, I’ve just looked at the amount that these corporations return to their investors through dividends and share buybacks, it way exceeds their research and development budget, indeed for most, for most years, it exceeds their profit. It exceeds their net income. Because we live in a political system, in an economic model that assumes that the market will provide, it assumes that these corporations have all the answers, we’ve eroded all the institutions that would have allowed us to provide a counterbalance to all this. And so when the pandemic struck, even though basically all of the research into those medicines had already been done by the public sector or small biotechs, at the end of the day, we couldn’t actually produce them because we’re still dependent on these tiny pipelines. And so we had to turn to Pfizer and Moderna and AstraZeneca and say, ‘take all the money you want,’ um, handed it over. Now AstraZeneca behaved a bit differently, of course, but Pfizer and Moderna, I mean, sold hardly anything to the vast majority of the world, they just weren’t interested. Absolutely shocking! And that’s not just, it’s not just morally wrong, it’s stupid because as long as there were huge parts of the world unvaccinated, we were all at risk of a new, more virile and more deadly strain of the virus coming out and undermining the vaccines that we had had. But that seemed to be as of nothing to the pharmaceutical companies because well, if the, if the pandemic goes on longer, you know, there’s simply more money to be made. So there’s no interest, it’s not only that there’s no interest in equitably selling the medicines the world needs and researching the me the medicines that that, that, that all people urgently need. There’s not really any interest in researching anything other than, you know, drugs that have marginal differences on chronic diseases because those are the most lucrative drugs.”

Naomi: “And even if politicians in the wealthiest countries in the world don’t care about equitable access to drugs at prices that aren’t taking advantage of market dominance, they should care about this:”

Nick Dearden: “We are faced with antimicrobial resistance. Yes, we’ve overused antibiotics massively, but the pharmaceutical industry hasn’t researched any more of these things because there’s no profit in it, essentially because they would be second, third generation antibiotics that wouldn’t be used very much for the next 15, 20 years anyway. They’re not gonna make anything of them. Look, you just need to nationalise parts of this industry. It is simply not fit for purpose.”

Naomi: “When you look at the logic of governments letting the biggest companies decide on supply chains based only on the bottom line – without any thought about global security, the world we’ve allowed corporations to build gets riskier and riskier for all of us. This is MEP and competition lawyer Stéphanie Yon-Courtin speaking in Europe at an event called ‘How Monopoly Threatens Democracy and Security:'”

Stéphanie Yon-Courtin: “The pandemic has highlighted the EU’s long-existing structural problems related to the supply of medicines and the higher dependency on third country import for certain essential and highly critical goods and materials. In the wake of the pandemic it is as if we finally found out that we were 100% dependent on third countries such as China or India. One of the key lessons of the crisis is that there is a need to get a better grip an understanding of where Europe’s current and possible future strategic dependencies lie. The notion of resilience of supply chains was already much discussed before the pandemic in the context of ensuring availability of resources necessary for the twin transitions – green and digital – of the economy and society in Europe. It became as pertinent as ever with the crisis. Now facing this situation it seems clear that our competition policy plays an essential role – it’s one of the tools, a key one to increase our strategic autonomy and our industrial policy that could secure supply chains. I think we are slowly moving from a naive Europe to a pragmatic and realistic one – no choice. Now, with the Russian invasion to Ukraine we have no choice, no choice to face our dependency to Russian gas.”

Naomi: “In the case of Russian gas, markets – and the German government didn’t come out of this well either – allowed storage and pipelines to be monopolised, ignoring the obvious security threats. It ended up enhancing the dominant power of Gazprom, majority-owned by Russia, an expensive lesson. Here’s Christopher Gopal of the Global Supply Chain Center, at the University of Southern California, he’s speaking at the same event:”

Christopher Gopal: “The Russia issue is huge and will cause a great deal of grief to a lot of people, but this is nothing compared to the type of impact that something over in China and Taiwan can have on us. Russia has probably four to six major leverage points by which it can disrupt supply chains and some of them are not global. China has hundreds. Just to give you one example and when I say people are not ready for this, when we talk about the chip industry and the chip problem, what we felt in covid was a hiccup. If the chips from China and Taiwan are blocked from coming in for any reason, those two together own about 20 to 30% of the world’s production and the high-end chips. More to the point, the impact is not just on the chip industry, 100 billion dollars of plus. Those are the primary industries, the impact goes under the secondary industries, defence and aerospace, automobiles, heavy trucks, industrial equipment, infrastructure, all of these things and then cascades to things like tourism, food production, traffic lights, shipping, everything else. Something like that would have enormous impact, it could bring countries to their knees. I mean to say even worse – there could be even worse than semiconductors is pharmaceuticals – China produces, you know, the numbers vary from place to place but 90% of the antibiotics. A lot of the pharmaceutical chemicals, the APIs used in the production of pharmaceuticals, cortisone, all of these things, ascorbic acid – if that gets cut off we have no pharmaceuticals, we have no antibiotics, you know enough with the, the place comes down because lack of semiconductors, the place comes down because we have no medications. Our PPEs and so on are built in those areas, a cut off in those areas would be calamitous.”

Naomi: “Here’s MEP Stéphanie Yon-Courtin again on better competition policy Europe needs:”

Stéphanie Yon-Courtin: “If the political will is there, that’s another question. Let me name a few, four main milestones. First I think a paradigm shift in the objective of competition policy – the objective of competition policy I think has moved from a single perspective of maximising the interest of consumers to a more balanced objective, particularly with regard to taking into account Europe’s industrial interest. Second is the resilience – the resilience is now mentioned clearly as an objective of competition policy, and from now on competition policy instruments will also have to take into account resilience issue for all supply chains, that’s quite new. Third point is the announcement of a new competition framework, you know, including stated for semiconductors. I think this is a major step forward and a kind of an implicit recognition that the current framework is not adequate to address the urgency of the crisis and the importance of this dependency issue. We need to multiply this approach I think without waiting to be paralysed by drug, semiconductor shortage and think about now, right now for Europe. And the vaccine crisis has shown us that being excellent in research is not enough to meet our needs, we need to know how to produce, we need the right scale and vision necessary to overcome persistent industrial weaknesses.”

Naomi: “Big challenges – much of them caused by markets and market domination by a few companies. But that sounds to me like many European governments are recognising that States can no longer just stand aside. And at the heart of all of this has been misconceptions about ‘competition.’ You hear that word all the time, but in the neoliberalist era it moved from meaning businesses competing with each other on innovation and efficiency, to competiton between nations – so, governments climbing over each other to cut labour rights, cut taxes, cut regulation; a race to the bottom. In the long run that reduces real competition when it comes to creativity and diversity – small and medium companies get crowded out and governments don’t seem to know how to encourage anything else. And something as valuable as ‘collaboration’ doesn’t get a look in. But, going back to the pandemic for a moment – despite all those troubles in – for example – sourcing PPE during the pandemic across the world – do you remember that? What’s happened since then? Well, most countries have defaulted to relying blindly on markets again. Christopher Gopal again:”

Christopher Gopal: “From all my discussions with people in Europe and they’ve been mainly companies I have to have add, nobody, not Europe, has governmental policy. We are going back to the old normal, you know the financialisation of the supply chain where we hit just-in-time inventory, lowest cost, assets going out and for instance one of the biggest companies in the US, in the world rather, has just announced that they’re going back to China for cheap chips. Not having learned any of the lessons.”

Nick Shaxson: “This is about the corruption of markets really and this is about markets not working as they should.”

Naomi: “Nick Shaxson again:”

Nick Shaxson : “I think the United States has been so lax for so many years that anything that Europe does look good. Having said that, the record in Europe is appalling. Just for example I was looking the other day at the merger statistics. I think they get about 15,000 mergers a year in Europe and of those maybe I think three or four hundred get notified you know ‘here’s the merger it’s potentially gonna cause competition concerns, you guys are gonna have to look at it.’ If you look at the record of the mergers that are notified, which are mergers of potential concern since 1990, 0.4% of those have been prohibited – almost nothing – they just don’t block mergers, so that’s a sign that there’s serious trouble. Anybody who looks around in Europe will know that we have a problem with big pharma, with big agriculture, with big retail, with big tech, with the big four accounting firms, with big banks – we’ve got the same problems. We have social democracy here in Europe that takes off some of the hardest edges of these things but I think that whereas social democracy in Europe has been quite effective in certain areas such as tax policy, in terms of excessive concentrations of power, I think Europe has basically drunk the kool-aid. The fines that you see – several billion dollars on the the tech giants look big – you know once you have the number of billion in there it makes a great newspaper headline but again it’s almost a rounding error in the actual size of the profits that these companies are making, so Europe is especially weak in this area. It’s a very nuanced picture, of course there are positive things you can say about Europe, but Europe is not in a position at the moment to spread a beneficial Brussels effect around the world in this area. We’re working with hope to spread this new story and over time this is something that takes years to do to shift things in Europe so that Europeans wake up and I think Europeans are quite capable of waking up and doing things differently, I think there’s a lot of questioning going on.”

Naomi: “Nick Dearden again:”

Nick Dearden: “To prevent the increasing concentration of capital is really important. The problem is, I think competition regulators over the last 40 years have almost forgotten how to do that job. Although I am heartened by the fact that an antitrust activist was appointed, to the head of the US central regulation body, Lina Khan, and I’m even more heartened that she seems to be taking that job really seriously, I mean, only this week really interesting that they’re challenging a big pharma merger. And so, you know it is not the only answer, but it is part of the answer. We’re in this economy, which is supposed to be all about, you know, promoting small businesses. And we hear this from government all the time, and it’s just the opposite of the truth. In the sector I know best, the pharmaceutical sector, your only option, your best business model is ‘how can I get bought out by Pfizer?’ That’s it! I mean, what kind of a balanced economy is that creating? None, obviously.”

Naomi: “Yeah, quite! So what are the key things would you say to tackle market concentration, monopoly power?”

Nick Dearden: “I would argue three things. First of all, what Biden has already started to do, which is industrial strategy, which is using the power of the state procurement and so on to begin shaping the economy. The thing I want to make sure is that doesn’t just become a form of corporate welfare, that doesn’t just become about de-risking the kind of investment that you want. There’s got to be a very clear public return. If we are putting this in, what do we expect back? And that’s gotta be about reshaping the way that the private sector operates. I think the second thing obviously is, is more use of alternative forms of economic unit, whether that be public sector but also, you know, cooperatives, I mean, let’s give some real competition to these behemoths and create that more balanced economy. And that’s not just gonna happen, you know, that needs a framework and a plan by government. And I think third, and I know this is gonna be welcome on your show, it’s financial regulation – because the deregulation of finance is absolutely crucial to how all of this happened. I mean, two or three massive investment funds now own a significant proportion of virtually all corporations traded in London and New York, and they are driving these kind of incentives ever more towards profit maximisation, and that is helping this corporate concentration, there’s only the big monopolies that can thrive in this kind of world. Because of financial deregulation, of course, as well, these behemoths can shift their wealth around the world and avoid taxes because we have such a financialised economy – as we’ve already talked about, you know, big pharma doesn’t particularly make medicines that we need anymore, what its job is, is to maximise shareholder wealth. So financialisation is the other side of the monopoly capitalism equation, and I think we cannot properly bring this kind of economy to heel and make it work in the public interest without controlling that, and without regulating how capital can be used.”

Naomi: “Yes, yes. And tax is such a strong tool for shaping markets and encouraging things that we want to see and discouraging things that we don’t want to see. This comes down to the fundamentals of the purposes of tax, I mean there’s five Rs of tax – everyone knows the Revenue ‘R’ – but the Repricing one is crucial here – pricing damaging behaviour out, and incentivising activity that’s beneficial to the majority of us. I’ll put a link to the five Rs in the show notes, but tax fixes, just off the top of my head – there’s excess profit taxes, financial transaction taxes are an obvious one, wealth taxes, windfall taxes, taxes to address the climate crisis – the list goes on, and governments just aren’t using the taxes that are available to them in the public interest. OK, thank you Nick Dearden for joining me on the Taxcast. He’s got a book coming out all about the pharmacuetical industry later this year – Pharmanomics: How Big Pharma Destroys Global Health – I’ll link to that in the show notes.

So, let’s head to Minnesota now in the United States. There were many eyes on Minnesota this month – we had great hopes, but there was huge scare-mongering by lobbyists, all because it looked like Minnesota might take a historic step in making big companies active there do worldwide combined reporting. It could have raised an estimated $600 million in extra corporate tax revenue over the next two years. Very sadly, the enabler professions and their arguments won the day and the proposal was dropped from the bill. But why do they hate it so much? Here’s Alex Cobham of the Tax Justice Network:”

Alex: “The idea of worldwide combined reporting sounds kind of technical and boring, but it’s really powerful. What we’re talking about is when US states decide the basis on which they’re going to apply a formula to work out how much profit they should be allowed to tax from a given multinational. Instead of looking at their share of the multinationals’ declared activity in the United States as a whole, they would look at their share of the multinationals activity globally. Now what that means is at a stroke, you put a pen through any profit shifting that the multinational is doing anywhere. And you’re just looking at, you know, if 1% of your global sales and employment, let’s say, is in Minnesota, if that’s the formula that you’re using, then 1% of the global profits will be taken as tax base by Minnesota. So you more or less switch to a complete unitary basis, you assess the profits at the unit of the multinational itself and you give up on the arm’s length principle that the OECD and before that the League of Nations have been defending for a hundred years, even though it’s become increasingly clear to everyone that it just doesn’t work, and that profit shifting is the only result of trying to do corporate taxation on that basis.

But here’s the thing, because this is such a good idea, because it is simple and powerful and pretty difficult to, to cheat, there’s enormous interest for the lobbyists in making sure it doesn’t happen anywhere. Because if it happens in one place, whether that’s one US state or one country, as soon as it becomes clear that it works, which, you know, I think there’s a general confidence that it absolutely will, and that it raises significantly more revenue, um, than trying to make arms length pricing or anything else work, then the demonstration effect to everyone else is going to be enormous. Why wouldn’t everyone just do the same thing? And of course, if everyone does the same thing, the effect is that there is no possibility of double taxation. If everyone says ‘we’re gonna take our share of the global profit,’ then if that’s done right, all global profit will be taxed precisely, once and once only. No double taxation, but also no double non-taxation. So if you are a big four accounting firm or one of the major law firms that support multinational companies in their tax abuse, this is guaranteed to freak you out. What you want is to make sure that nobody ever tries it, that they feel the threat, the pressure before they get to that decision point. And they don’t go ahead. You tell them you’re gonna lose all of your investment if you do this, everything will go wrong for you. We will hang you out to dry. We will make an example of you as people who don’t understand how to do corporate taxation. You tell them anything, you tell them, you’ll give them money for their political campaigns if they don’t do it, whatever it is. Not that I’m accusing anyone here of corruption, I’m sure, but the point is, you are desperate to stop that first state, that first country trying this. And, you know, that’s kind of what appears to have happened in Minnesota. We don’t know the basis on which the lead Democrat who brought this all the way forward flipped at the last moment and just took it out completely. But we do know there was an enormous amount of lobbying and we do know that that’s what happened. So we don’t know the basis of that decision, but you can be sure similar things will happen in each other case.”

Naomi: “I bet! If Minnesota had passed this proposal to implement combined worldwide reporting it could have shone the light not just for other US states to follow, but for other countries too – they could implement this couldn’t they?”

Alex: “The G24 group of lower income countries brought forward a proposal, you know, not dissimilar to do that globally, within the OECD inclusive framework process. And that was what pretty much demonstrated that the inclusive framework was not inclusive because the framework group of countries agreed that that would be the work plan for the secretariat, they would evaluate it and a couple of other options and then come back. And the secretariat at the OECD never did that. They didn’t do it because before they got there, the United States and France did a bi-lateral deal on a completely different approach, and then the secretariat came back to the inclusive framework and said, ‘hey, this is, um, this is the way we’re gonna go instead.’ So it became immediately clear, this is back in 2019, that the inclusive framework was a sham. There was no inclusivity for, for non-OECD members and that that type of option, even though the OECD had promised to the world to go beyond the arm’s length principle in that process, they didn’t mean going that far beyond, just a tiny tiny tiny little bit as they’re now trying in Pillar One. And that’s why the OECD process, of course, isn’t gonna really change the world because they gave up on the original ambition. And again, we’ll never quite be sure if that was the result of really intense lobbying but we know there was an enormous amount of lobbying and we know they were pushing very hard to limit the extent to which the OECD did actually go beyond the arms length principle. So here we are.”

Naomi: “Here we are, yeah! So, lower income countries already tried to propose something like this combined worldwide reporting in the OECD, the not-so-inclusive OECD – which is after all, a rich countries club? Would it be easier, or harder for countries, rather than a US state like Minnesota to implement this?”

Alex: “You know, it’ll be interesting to see which is the next US state to consider this, given how much revenue it’s likely to to generate. For countries though, there is a limitation, which is that most countries have a significant number of double tax treaties that probably makes it impossible to go straight to a unitary approach of this sort and simply tax your share of the global profit. Now, that doesn’t mean that no one should do it. What it means is you probably want to do it in a group of like-minded countries and agree together that you will set aside these treaties. The European Union is still taking forward its BEFIT proposal, which would effectively do this within the EU. And there’s a question there about whether that can be extended, as in the Minnesota proposal to a worldwide combined reporting basis.”

Naomi: “BEFIT – that’s the EU’s “Business in Europe: Framework for Income Taxation” – it’s supposed to be a ‘single corporate tax rulebook for the EU, providing for fairer allocation of taxing rights between Member States.’ So where do the G24 group of lower income countries go? I mean we all know the OECD isn’t the place to get what they want, so how about the United Nations?”

Alex: “There’s also the process now around the, the proposal for a UN framework on international tax corporation. We know that both the African and the Latin American and Caribbean regional discussions have included the possibility of pushing for unitary taxation, which could be done at the regional or the UN, the full global level. So in a sense, if things get blocked by some OECD member countries, for example, within the UN process we could see regional moves to jointly, unilaterally move towards unitary taxation and their sort. So there’s a lot to play for. That’s a huge amount of revenue involved, in effect the 312 billion, that’s our last estimate for the annual tax revenue losses due to corporate tax abuse by multi-nationals. That would more or less be available to be reclaimed if countries switched to a unitary taxation basis. Bigger amounts of money in high income countries, but a bigger share of current tax revenues in lower income countries. So really a pretty strong incentive for everyone to make that shift. And it’s only the lobbying that continues to hold that very sensible step back. This year might be the year that we see that dam start to crack, and particularly within the UN process and the related discussions. Whether or not this proposal starts to become more concretely possible Minnesota might just be an early sign that this could be on the way.”

On 16 May 2023, the Council of the European Union reached agreement on the adoption of the latest proposal for amendment of the EU Directive on Administrative Cooperation (‘DAC’). The proposal for amendment – known as DAC8 – was launched by the EU Commission in December 2022 and serves the general purpose of ensuring that the EU’s automatic exchange of information regime stays in line with the evolving economy. More specifically, the DAC8 proposal intends to extend the regime to also include crypto assets and e-money. The amendment is being adopted under the ‘consultation procedure – general approach’ which means that a subsequent vote in the EU Parliament is necessary, but the outcome of the vote is not binding. The text of the DAC8 amendment agreed by the EU Council differs little from the original proposal by the EU Commission, and this despite the Commission receiving a plethora of feedback from the public during a public consultation round which ran from December 2022 to March 2023.

Automatic exchange of information↪NOTEAutomatic exchange of information is a data sharing practice that prevents corporations and individuals from abusing bank accounts they hold abroad to hide the true value of their wealth and pay less tax than they should at home. Learn more here. is one of the core policy measures advocated for by the Tax Justice Network since its inception in 2003. Together with beneficial ownership transparency and country by country reporting, the automatic exchange of information is a crucial part of what the Tax Justice Network calls the ‘ABC’s of tax transparency’, a set of crucial policy tools for the fight against tax abuse and illicit finance. Given that the DAC8 amendment aims to create a more comprehensive framework for automatic exchange of information that also includes information on crypto assets, the Tax Justice network welcomes the initiative.

However, the amendment does not fully seize the opportunity to improve the general efficiency of the EU’s automatic exchange of information regime. Furthermore, the new rules that will apply in relation to crypto asset transactions retain some of the current biases in the DAC, like the strict adherence to information sharing reciprocity in relation to third countries, and especially lower income countries. In addition, it is also far from certain whether the proposed rules catch all relevant crypto asset transactions.

To highlight and suggest solutions to these and other issues, we summarise some of the Tax Justice Network’s recommendations made to the EU Commission during the DAC8 public consultation round.

1. No country left behind.

As mentioned by the EU Commission in its proposal, the newly proposed rules on automatic exchange of crypto asset information have to be seen in the light of the parallel work of the OECD on its so-called Crypto-Asset Reporting Framework (CARF). The OECD first developed the CARF in March 2022, which was then approved by the G20 in November 2022. As of yet, the OECD has not delivered on developing the CARF implementation package. Such a package would consist of model legislation and a model multilateral competent authority agreement.

With its DAC8 amendment being all but final, the EU gives a clear signal that EU countries will no longer wait for the implementation of CARF. Information provided by foreign crypto asset service providers on resident taxpayer’s crypto asset ownership is a crucial tool to compel tax compliance by crypto asset owners. Such compliance is needed, both for the purpose of raising revenues and avoiding crypto assets putting pressure on countries’ tax gaps, as well as for taxpayer fairness. It simply cannot be that one type of asset is left to slip through the cracks of the tax reporting system.

The DAC8 amendment attempts to fill this crypto shaped crack. Under the new rules, EU Crypto Asset Service Providers (CASPs) – such as crypto exchanges, custodial wallet providers and brokers – will report information on the crypto assets held by taxpayers resident in EU countries. Providers that are not based in the EU will only obtain access to the EU market if they register in an EU country and comply with the reporting rules in this country. This extra-territorial scope of the directive squares the circle: no crypto-asset service provider will be able to offer crypto services to EU taxpayers without being subject to reporting obligations. The EU can afford this approach of leveraging market access to obtain tax information because the region is the world’s biggest crypto asset market. Foreign CASPs cannot afford to lose out on selling services to EU customers.

Obviously, EU countries are not the only ones in dire need of information on their residents’ crypto assets. Especially in lower income countries, where the grassroots adoption of crypto asset amongst the population is reported to be skyrocketing and crypto-induced tax gaps are widening, governments could do with the information on their resident taxpayers’ crypto assets. Many lower income countries cannot leverage market access to obtain tax information from foreign CASPs. The alternative solution of addressing crypto tax compliance issues by instating a ban on crypto assets has proven difficult to enforce. In Egypt, for instance, the government issued an absolute ban on crypto ownership and service provision as of 2019. In 2022, Egypt is reported to be the fastest growing crypto asset market in the Middle East/North Africa Region. Arguably, due to the local ban most locals rely on foreign crypto-service providers to own and transact crypto assets. Without international cooperation, this information is out of reach for the local tax authorities.

From this perspective, the forging ahead of the EU on this topic comes as a bittersweet development. Obviously, any effort to reinstate fairness of the tax system is to be welcomed. The EU should use its market leverage for ensuring global crypto transparency, eg by the speedy adoption of a single global standard, rather than push ahead for a regional standard with regional benefits only. Speeding up development of the CARF implementation package will not be aided by the fact that the biggest crypto market in the world now has its own plan to solve the issue, a plan that due to its extraterritorial reach does not require approval from any third country.

2. Beyond third-country reciprocity: the wider-wider approach in crypto asset reporting

The framework of international exchange of information in tax matters is built on the principle of reciprocity. Under the Common Reporting Standard (CRS), for example, countries exchange financial account information of non-resident taxpayers with only those countries that do the same in the inverse scenario. The idea of tit for tat has some merit in the case of similarly situated countries. But the world is a place of rampant cross-border inequality. Lower income countries simply do not have the administrative resources in place to meet the administrative standards to be eligible to send information, and thus they are not allowed to receive it, preventing them from finding out in which foreign countries local taxpayers have financial accounts. This lack of reciprocity affecting lower income countries makes little sense as well-off citizens of lower income countries tend to rely on financial institutions in high income countries to keep their wealth. The opposite is highly unlikely.

The Tax Justice Network has since long argued that the strict insistence on reciprocity in exchange of information works not only to the detriment of lower income countries but also risks being abused by the host countries of information holders to effectively prevent international administrative in tax matters from reaching its full potential. Allowing intermediaries to distinguish between ‘reportable clients’ (clients residing in participating jurisdictions) and ‘non-reportable clients’ (clients that need not to be vetted because they reside in a non-participating jurisdiction) opens the scope for all kinds of arbitrage and abuse.

For this reason, the Tax Justice Network’s Financial Secrecy Index assesses countries’ implementation of the so-called ‘wider-wider approach’. Under the OECD’s optional ‘wider-approach’, countries are encouraged to implement rules under the Common Reporting Standard which force intermediaries to employ the same ‘onboarding’ due diligence to all clients, both those residing in participating and non-participating countries. The ‘wider-wider approach’ goes one step further by forcing intermediaries to remit information on clients in non-participating countries to their local government. Although the country will not be able (or willing) to automatically exchange the information with the non-participating jurisdiction, it would at least be possible to draw up statistics on non-resident taxpayer activity and assets. The publishing of aggregated statistics on crypto asset information should not be controversial. It’s been shown in recent years that statistics on automatic exchange of information are a necessary tool to hold governments and intermediaries accountable and to reveal reporting irregularities, like penguins owning bank accounts.

The implementation of a wider-wider approach is especially relevant in the case of crypto assets. As noted by the EU Commission in its own DAC8 proposal, the characteristics of crypto assets make the traceability and detection of taxable events by tax administrations very difficult. If the EU wants to assume market leadership in the Web 3.0 era by providing EU CASPs with a solid regulatory framework, it cannot close its eyes to the fact that these EU CASPs might be instrumental to tax evasion in third countries, and especially, lower income countries. As such, it is highly regrettable that the EU has not seized the opportunity to implement the ‘wider-wider approach’ in DAC8 to oblige EU CASPs to provide information on the totals of crypto assets owned by residents in lower income countries. This information is key for those countries to assess the need for the development of solid domestic crypto tax rules and participation in the international exchange of a crypto asset information framework.

3. Call of duty to spontaneously exchange

The implementation of the ‘wider-wider approach’ might not make up for the fact that without legal ground in place (like the yet to be developed a CARF competent authority agreement), EU countries cannot automatically exchange crypto asset information with third countries.

The EU Commission should however have taken the opportunity in the preamble of DAC8 to remind EU Member States that besides the exchange of information rules in the DAC, all of the 27 EU Member States are also party to the Multilateral Convention on Mutual Administrative Assistance in Tax Matters. This convention is signed by over 120 countries, among which are a large number of lower income countries. Under Article 7 of the Convention, a country shall spontaneously exchange information that it has grounds for supposing may relate to a risk of tax loss in another country.

Spontaneous exchanges of information typically take place on a case-by-case basis, are not compulsory, and not comprehensive. As such, they cannot replace the automatic exchange of information. But even ad hoc exchanges of information gathered by European CASPs can help lower income countries to foster general tax compliance amongst crypto asset users, be it to serve as the basis of ‘nudge letters’ inviting taxpayers to correct their tax returns in view of newly received information, or as the start of full-blown tax investigation procedures of recalcitrant taxpayers.

Both the European Commission and the EU Member States should be reminded on this point that under article 208 of the Treaty on the Functioning of the European Union, the EU has accepted, as part of its development cooperation policy, to comply with the commitments approved in the context of the United Nations, like the UN’s Sustainable Development Goals. Arguably, the development of a crypto asset tax reporting system which serves the EU Member States own interests but that does not live up to its potential to contribute to domestic resource mobilisation in lower income countries, fails this obligation.

4. Silent elephants in the room: self-hosted wallets and decentralised exchanges

A final issue in the DAC8 amendment that deserves attention is the fact that the proposed reporting rules stay silent on the concept of self-hosted crypto wallets and decentralised crypto exchanges. Self-hosted crypto wallets allow individuals to set up accounts to own and transact crypto assets over the internet without the involvement of a CASP. Decentralised crypto exchanges are smart contracts embedded in the blockchain which provide for the ability to exchange crypto assets online and in a decentralised way, ie without the involvement of an intermediary. The DAC8 rules are however conceived on the mould of the DAC2/CRS rules and, as such, based on the assumption that crypto users rely on intermediaries to own and transact crypto assets. Just like in the case of the Common Reporting Standard, obliging these intermediaries to report on crypto users’ assets and income is presented as the silver bullet to tax compliance.

It is worth nothing that the crypto ecosystem is, however, fundamentally based on the premise of disintermediation. Unlike in traditional finance, intermediaries – the CASPs – are not indispensable for users to own crypto assets or undertake exchange transactions. Self-hosted wallet users can easily trade crypto assets by relying on peer-to-peer trades or by relying on fully decentralised applications. Given the lack of service provider involvement, this ‘dark side’ of the crypto ecosystem is fully out of the reach of tax authorities.

Under the new rules, CASPs should report transfers of crypto assets to or from self-hosted wallets, ie crypto wallets owned by users without involvement of a custodial entity. The EU commission admits this reporting is needed to help “track the wealth of a particular taxpayer”. The Tax Justice Network commends any measure that serves the purpose of registering wealth. It is highly doubtful however whether this measure alone – which echoes the extension of the ‘travel rule’ to crypto transactions under the EU Transfer of Funds Regulation as part of the 6th anti-money laundering package – is sufficient to deal with the phenomenon of self-hosted wallets. This doubt seems to be shared by the G7 Finance Ministers, who in their meeting communiqué of 13 May 2023 are calling for solutions to address the risks associated with peer-to-peer crypto-transactions beyond the implementation of the travel rule. As acknowledged by the European Commission itself, there is a clear need to track the wealth of crypto users, both for tax purposes and for anti-money laundering purposes. The global ownership of bitcoin, for example is both highly concentrated in the hands of a few owners who mostly rely on self-hosted wallets. Compulsory declaration of self-hosted wallet ownership by EU taxpayers and a European asset registry for crypto asset ownership above a certain monetary threshold are the only effective ways to track crypto wealth in the EU and to deal with the crypto ecosystem’s decentralisation and anonymisation in a technology neutral way.

The problem of self-hosted wallets is further exacerbated by the gain in popularity of decentralised exchange services. Decentralised exchange services are blockchain based applications that effectuate crypto asset trades between users entirely through automated algorithms and smart contracts. Like self-hosted wallets, fully decentralised exchanges allow exchanging crypto assets without involvement of a standard ‘centralised’ intermediary. Decentralised applications without identifiable persons with control or sufficient influence does not give rise to CASP status under the proposed DAC8 regime. As such, they allow crypto asset users (and especially those using self-hosted wallets) to exchange crypto assets without incurring any reporting of the transaction for tax information exchange purposes. Here too, the EU Commission is well-advised to devise rules on the registration or reporting of decentralised application use.

Without rules that fix the loopholes created by self-hosted wallets and decentralised applications, the DAC8 main purpose, which is to restore fairness in the tax system by ensuring tax compliance on crypto asset income just like any other income, will not be attainable.

5. Additional recommendations to maximise the DAC’s potential.

Finally, in the public consultation document, the Tax Justice Network makes a number of general recommendations to improve the DAC framework as a whole. These improvements are not included in the DAC8 amendment, but they should be if this latest amendment of the DAC is to live up to the DAC’s purpose as explained in one of DAC8’s recitals.

Recital 35a of DAC8 provides that:

“It is essential that the information communicated under Directive 2011/16/EU is used by the competent authority of each Member State which receives this information. Therefore, it is appropriate to require the competent authority of each Member State to put in place an effective mechanism to ensure the use of information acquired through the reporting or the exchange of information under Directive 2011/16/EU.’

Recital 35a was not included in the original proposal by the EU Commission. Its addition by the EU Council hopefully signals a willingness to make work of measures focusing of effective use of exchanged tax information, be it for compliance programmes, risk assessments or general audits.

The Tax Justice Network has since long advocated for measures that make the most of exchanged tax information, also for the purpose of wider policy development in the field of tax and anti-money laundering. As mentioned above, an important first step in this regard is the introduction of rules on the compulsory publication by EU Member States of aggregated statistics on information exchanged per-country on financial accounts and – in the near future – crypto assets. The EU should in this regard follow the example of countries like Argentina, Australia and Germany which recently have started publishing statistics on financial accounts held by non-residents. Additionally, the EU should adopt strategies for Member States to be able use the exchanged data in a pro-active way to map hidden offshore wealth planning.

The EU should also consider the introduction of measures that combine beneficial ownership transparency with exchanges of tax information, be it on request, spontaneous or automatic exchanges. Such measures are needed to tackle the loopholes in the exchange of information framework in the case of individuals holding bank accounts through foreign companies. This loophole was already pointed out by the Tax Justice Network at the time of inception of the Common Reporting Standard in 2014 but continues to persist until today.

A final recommendation concerns the specialty principle and the need to remove this principle from the DAC. Under the specialty principle, information exchanged under the DAC can only be used for tax assessment and tax fraud investigation purposes. However, the exchanged information is often instrumental for the investigation of closely related crimes, like corruption or money laundering. Just like many Latin American countries do under the Punta del Este Declaration, the European Union should also allow natural synergies to take place between administrative cooperation on tax matters and the fight against money laundering and corruption.

Conclusion

The EU is right to press ahead with addressing the secrecy and tax abuse risks posed by crypto assets. The OECD’s delay in putting out a timeline for the implementation of the CARF has meant the harms of crypto asset evasion continue to rack up. However, for third countries and especially lower-income countries, the adoption of DAC8 does not solve this problem.

DAC8 furthermore perpetuates some of the existing flaws in the DAC and in the OECD’s Common Reporting Standard, like the requirement of strict reciprocity for information exchange. Given the market leverage it wields in the crypto industry, the EU had a real opportunity to design a system that would secure transparency for all countries. DAC8 also perpetuates certain flaws present in the OECD’s CARF proposal, like the lack of a solution to deal with peer-to-peer crypto transactions.

Finally, the DAC8 amendment also squanders a good opportunity to revise the DAC regime as to the effective use of the exchanged tax information. Various measures can be taken and have been suggested, but besides recognising the problem in the preamble, DAC8 does not deliver.

Some reflections on how a small band of people sparked a global movement.

Tax Justice Network announced today that tax justice pioneer Nicholas Shaxson is leaving the Tax Justice Network to co-lead the newly-established Balanced Economy Project. We thank Nick for his outstanding contributions to the development of the tax justice movement, and wish him all the best.

One afternoon in Amsterdam in 2006 I took a phone call from John Christensen, who I’d come across before as a private investigator of interesting trends in troubled countries. As a journalist, I’d been living in and writing about west African petro-states since serving as a Reuters and Financial Times correspondent in Luanda in the early 1990s during the Angolan civil war. Until I took John’s call, I assumed that would continue to be my career.