The German government is currently blocking a measure to publish country-specific balance sheet data, known as country by country reporting, in Brussels. Citizens and European politicians could use this data to free themselves from the headlock of the world’s most powerful lobbyists and tax avoiders. So far, however, the German government has failed to recognise both the inherent opportunity for a renewal of the European project and the EU’s great weight as a standard-setter in the global economy.

Since the global financial crisis of 2008, journalists have used leaks and painstaking research to show the industrial scale of tax trickery by the world’s largest economic players. Whether Google, Apple, Facebook, Amazon, Ferrero, Starbucks, BASF, Ikea, Vorwerk or SAP: their stories all too often give rise to a picture of brazen bilks who are flouting the public on top of causing the injury of unpaid taxes when they reel off their mantra of paying taxes everywhere in accordance with the law.

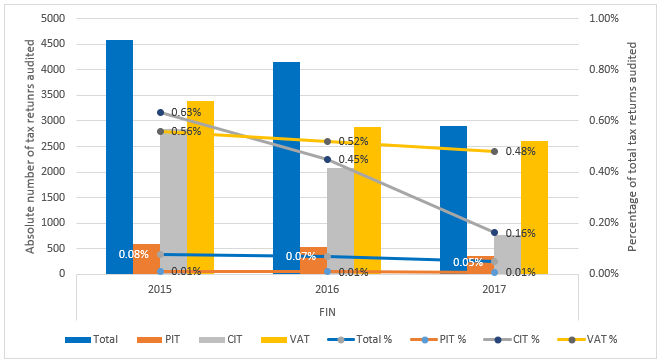

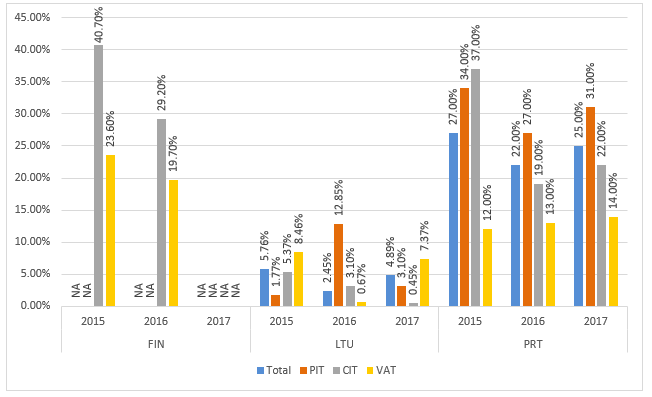

This assertion is only partially correct, as is shown by the billions in additional taxes assessed to be due during corporate tax audits. In 2016, for example, the tax authorities in Germany collected over €10 billion in taxes that large companies had failed to include in their tax returns. Data by the OECD shows that in 28 countries that reported data for 2015, on average additional 10.7 per cent of total corporate tax revenues are assessed through corporate income tax audits. In these 28 countries, on average fifty percent of all corporate income tax audits resulted in additional taxes assessed. To claim that corporates always pay tax everywhere in accordance with the law is thus simple corporate spin.

But the corporate mantra is badly misleading for another reason, too. It contains the subtle pretense that these companies are completely detached and uninvolved in the legislative process. In reality, global corporations afford a highly efficient lobbying machine and professional helpers. These are privileged professional groups such as tax advisors, lawyers and accountants who devise highly complex legal constructs for tax avoidance on the assembly line. To do this, they resort to artistically woven networks that reach from the economy to the highest political circles in order to guarantee impunity and tax loopholes.

These insider relationships function as long as they can work in secret. Essential for this opaque, criminogenic environment is that the extent of industrial tax avoidance is not exposed to public scrutiny. In this respect, Paradise Papers, LuxLeaks & Co. are serious system errors, anomalies in the matrix that have allowed a rare look behind the scenes. Individual errors, however, cannot paralyze a system.

The worst case scenario, the system breakdown for industrial tax avoidance, on the other hand, would be the regular measurement of tax dodging by public country by country reporting. These reporting obligations would reveal important indicators of economic activity, profits and tax payments for all countries in which corporations operate. Similar obligations already exist in the EU banking sector. A few months ago, German economists at the University of Cologne showed that these disclosure requirements have led to significantly higher tax ratios, especially for banks with tax haven operations.

Public country by country reporting generates more tax revenue due to incalculable reputational risks. If a company has to assume that the “fruits” of the elaborate tax acrobatics will be easily visible to the public at the end of the day, then suddenly other goals than aggressive avoidance play a more important role: management must act for the good of the company and therefore avoid possible calls for boycotts and negative headlines. When in doubt, corporate leaders are more afraid of reputational damage and shareholder pressure than tax authorities. The same applies to the tax authorities: their political leadership is more likely to shy away from unlawful or questionable deals if they threaten to entice enquiries.

The EU Commission and the EU Parliament have therefore proposed introducing such reporting obligations for the largest corporations in all sectors. Annual, complete financial transparency for the largest corporations could trigger incalculable reactions from voters, small and medium-sized domestic companies and consumers. Equipped with such corporate data, they could make better informed decisions at the ballot box, in the chamber of commerce and at the supermarket shelf on how they want to use their vote, their influence and their household budget.

Those who suffer most from corporate tax dodging are average and low-income earners, because they can hardly evade taxation via value-added tax and payroll tax and thus step into the breach for missing tax revenues. In line with the trend of recent decades, these groups shoulder a growing share of the tax revenue. Generally, these are the same social strata that also suffer most from a lack of quality public services due to a lack of taxes – be it a shortage of teachers at public schools, under-equipped public universities or under-funded social services for single parents.

The same applies to small and medium-sized companies, which are losing out against big companies. Double standards are also applied when it comes transparency. Insofar as they are only active domestically, the annual financial statements of small and medium-sized enterprises usually contain the balance sheet data, the publication of which the global monopolistic giants have so far successfully resisted.

No wonder, then, that the EU Commission’s request rouses powerful, ancient forces to resist. In 1978, such a system breakdown was looming on the horizon when the United Nations was on the brink of obligating multinationals to publish annual accounts for every single subsidiary in their global corporate web – including in all tax havens. With the help of the USA, Japan and other OECD countries, economic lobbyists succeeded in stopping this push at the last minute. Instead of the United Nations, private accounting firms have since been enthroned by the OECD as standard setters.

In a classic manner, the fox was appointed guardian of the hen-house: to this day, it is above all the Big Four accounting firms that set the influential accounting standards for corporations. The European Union and many other countries in the world have so far nodded off these as supposedly non-political, purely technical standards.

This could change if the Federal Government finally gave up its opposition to the proposal for public country by country reporting. In the European Council of Ministers, Germany is playing the key role – and has so far rejected public country by country reporting alongside Luxembourg, Ireland, Cyprus, Malta, Hungary, Sweden and Austria. With the exception of Sweden, all other countries are more or less notorious corporate tax havens, and thus hardly surprising opponents of the reform.

In short: it is one of the regulations where the SPD-led ministry would be well advised to take an example from the CSU Minister of Agriculture and his Glyphosat decision and “do the Schmidt” – simply to give its approval in Brussels on its own. There are more unworthy plans to jeopardize coalition peace. Instead, every argument, however far-fetched, against this proposal is being made by the business community – and unfortunately many of them have so far been taken up by the government coalition and the SPD finance minister.

As long as Germany hides behind narrow-minded legal arguments, irrational fears of the decline of Germany as a business location or the retracting of half-baked intermediate steps already achieved, Europe cannot prosper. It is time for Germany to find its way from being Europe’s taskmaster to a new role. Germany should no longer deny Europe’s weight as a standard-setter for the world economy and help give globalisation a more human face. Europe needs to expand its efforts on this ethical mammoth project to the extent that its great transatlantic ally is failing.

For this very reason, however, Europe and Germany still have an important lesson to learn from the USA: to finally use our market access as a lever to enforce (transparency) standards. The window for the adoption of the proposal ready for signature in Brussels is closing rapidly – there are only a few weeks left to get it through before the EU elections. What are we waiting for?