The Tax Justice Network is engaged in a pioneering joint research and data analysis project to support Nigeria’s Federal Inland Revenue Service (FIRS) audit of Multinational Companies.

Like most countries, Nigeria has a plethora of international companies doing business there, and an under-resourced tax authority, so it only gets to audit a fraction of the international economic activity passing through. A tool to help prioritise audits could therefore be invaluable.

Under an agreement with the FIRS, signed in December 2019, the Tax Justice Network has developed a detailed risk assessment tool based on international data that can help Nigeria’s tax authority (and, hopefully, others in future) prioritise and target their audits of multinational companies. On January 11-13 we partnered with FIRS in a joint three day event, entitled “Workshop on effective audit of multinational corporations for domestic revenue mobilisation in Nigeria.” The workshop was attended by about 50 staff from different areas of the FIRS, including the International Tax Department in charge of transfer pricing audit, the Treaties Unit and the Exchange of Information Unit. Beyond the specific audit project, another aim of the workshop was to create and enhance synergies between these units.

Speaking at the workshop, FIRS‘ Executive Chairman Muhammad Nami said that “many rich Multinational Corporations do not pay the right taxes due from them, let alone pay their taxes voluntarily.” Nigeria is now paying greater attention to tax audits, he said, adding that “we have created more than 35 additional Tax Audit Units and deployed experienced and capable staff to take charge of these offices.”

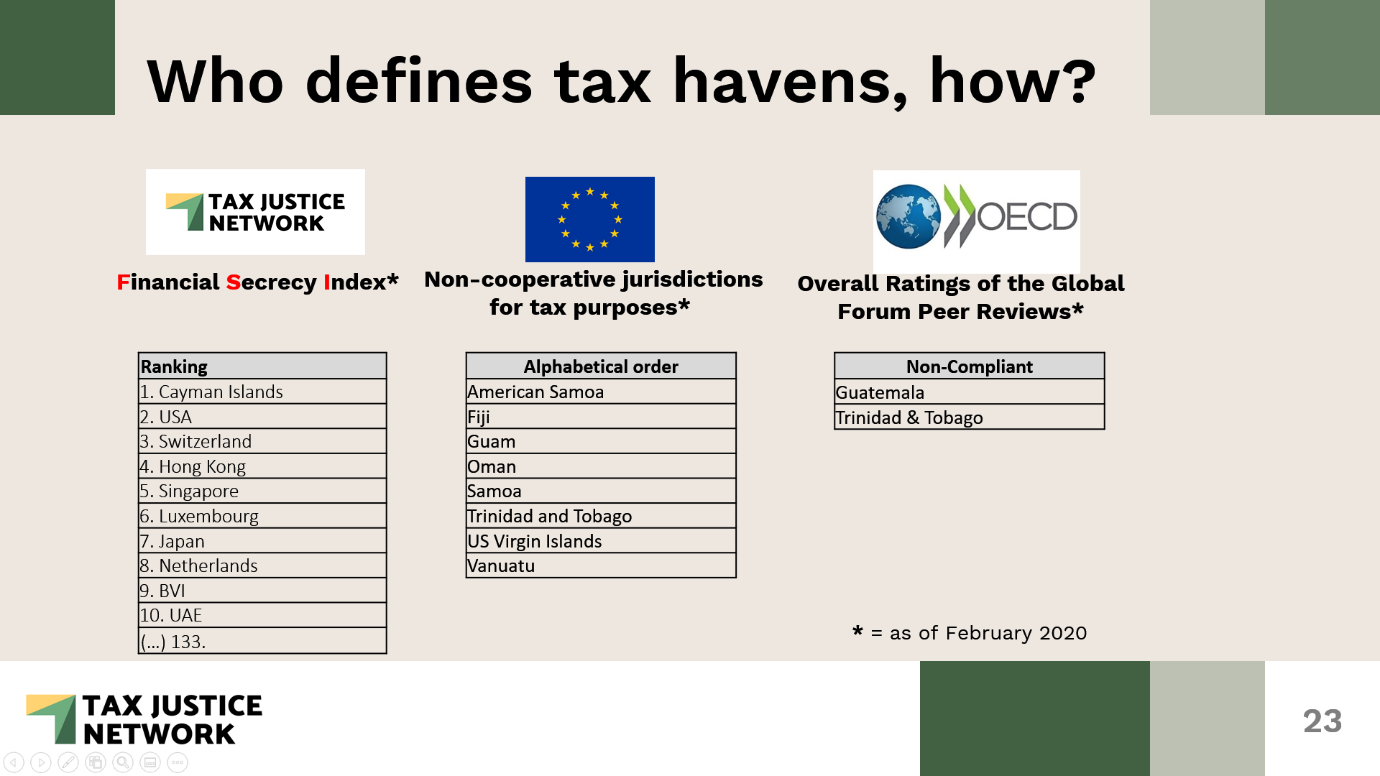

Tax havens, of course, constitute a major risk factor for the Nigerian tax authorities, and international data provided by official bodies in this area is hardly better than worthless. A slide we showed at the workshop illustrates this.

Nobody believes that American Samoa or Vanuatu, or Guatemala for that matter, are the top jurisdictions of concern for Nigeria, or for any other country. The world’s top tax havens are nearly all European or at least OECD countries, and these powerful groupings naturally exclude their own from blacklists. They are political. By contrast our rankings – the Financial Secrecy Index and the Corporate Tax Haven Index – are based on careful analysis of hard data, rather than on political considerations.

Essentially, both of our indexes involves combining two metrics for each jurisdiction: a “haven/secrecy score”, each based on 20 specific indicators, which tells us how risky the country’s legislation is in terms of enabling abuses; and a ‘scale weight’ telling us the size of financial flows through these jurisdictions. These scores are then mathematically combined to produce the final ranking.

However, our models have gone a step further, from the global, macro level analyses, to the bilateral macro level analyses: in our Illicit Financial Flows Tracker tool, we provide risk profiles of individual country’s economic cross-border activity based on their illicit financial flows risks in foreign direct investment, in their banking deposits abroad, etc. These risk profiles provide important pointers where to focus audit activity, and where to prioritise resourcing and how to target policies for information exchange better.

Yet, the next level is to take this analysis to the “micro” level. So instead of merely saying “Cayman‘s investment in my country provides risks”, the tax authority can scrutinize its taxpayers for related transactions and specific flows via Cayman, based on declarations and disclosure. Through our model, the tax authority can systematically calculate the risks for illicit activity of individual taxpayers based on each taxpayer’s entire cross-border transactions with all secrecy jurisdictions (not only with Cayman) to flag and rank those taxpayers incurring most geographic risks. The result is a ranking of taxpayers causing most of a country’s vulnerability in their cross-border economic transactions – and thus allowing the country prioritise its audits.

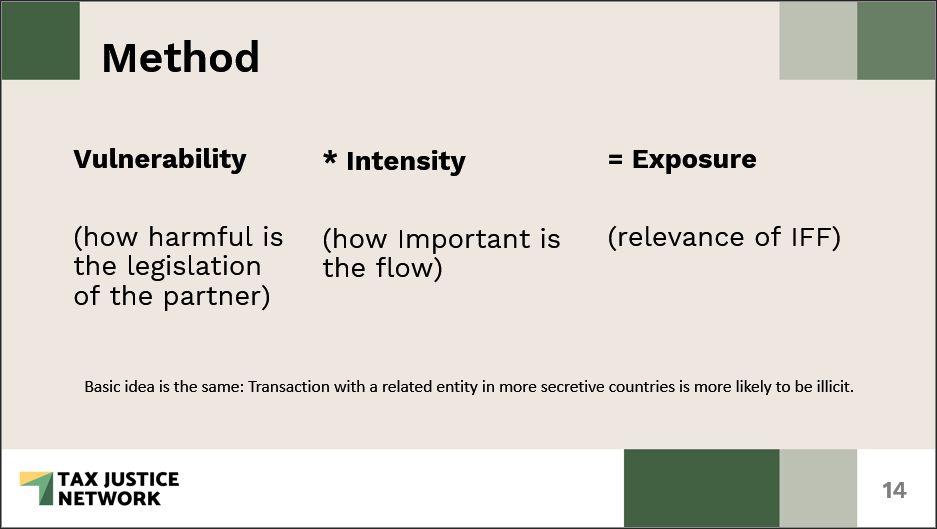

The analysis rests significantly on a core formula: Exposure = Vulnerability x Intensity. This slide illustrates the top-level view of this.

Data will be mined from certain components of transfer pricing documentation submitted as part of annual tax returns, with appropriate confidentiality and anonymisation safeguards in place. The key risk dimension driving the model is geographical risk, looking at where the connected companies and individuals (eg shareholders, intra-group trade with related companies, directors) are incorporated and/or tax resident; and at the related volume of costs or income from high secrecy jurisdictions.

In this way, tax authorities will be able to examine the risks of different corporate structures in a speedy manner and to process large volumes of corporate tax data fast, teasing out those corporate groups whose finances are most exposed to geographic risks. The model thus allows them to understand the flows better, and prioritise their audits accordingly. Similar kinds of exercises can be carried out looking at wealthy individuals, instead of corporate structures, using the data categories from our Financial Secrecy Index.

This model now needs to be subjected to the hard knocks of the real world, and refined accordingly. We will be delighted to receive feedback and are expecting that once road-tested in Nigeria, it can be useful to a range of other countries in Africa and beyond.

We’re proud to partner with Nigeria in countering illicit financial flows by sharing knowledge, capacity building and pioneering new methods and tools.

Welcome to our monthly podcast in Portuguese, É da sua conta (it’s your business). All our podcasts are unique productions in five different languages – English, Spanish, Arabic, French, Portuguese. They’re all available here.

Estima-se que pelo menos 26 bilhões de dólares anuais podem ser arrecadados na América Latina com impostos sobre grandes riquezas, o que é urgente para superar as maiores crises já enfrentadas pela nossa geração. Além de contribuir com o financiamento de ações contra essas crises, o imposto sobre riqueza é essencial para auxiliar a reduzir desigualdades. O É da sua conta #21 te convida a conhecer e participar das campanhas pela tributação de grandes riquezas.

E começa mostrando que é possível: mais de cem super-ricos defendem a tributação sobre suas grandes riquezas e participam da campanha global Milionários pela Humanidade. Especialistas latinoamericanos explicam como funcionam os impostos sobre riqueza que já existem na Colômbia e na Argentina.Também contam a experiência dos países que ativaram esse tributo para enfrentar a pandemia: Bolívia, de forma permanente e Argentina, de forma extraordinária.

E você ainda ouve as iniciativas de países que seguem tentando aprovar leis de imposto sobre riqueza na região, como Chile e Brasil.

No que depender dos ouvintes do É da sua conta taxar grandes fortunas é urgente e necessário. Destacamos a opinão de alguns deles ao longo do episódio.

This blog is an expanded version of a blog published originally on CIATblog, with kind permission.

Today, the Tax Justice Network publishes its new study on “Vulnerability and exposure to illicit financial flows risk in Latin America.” It is the most comprehensive and systematic analysis of illicit financial flows risks in Latin America to date, and provides the basis for granular policy decisions. Illicit financial flows (IFFs) are transfers of money from one country to another that are forbidden by law, rules or custom. They encompass flows from both illegal origin capital (classic money laundering, arms, drugs, human trafficking, corruption) and legal origin capital (tax evasion and avoidance).

Illicit financial flows affect the economies, societies, public finances and governance of Latin American countries – as they do in all other countries. Latin American and Caribbean countries account for a significant share of trade-based illicit financial flows, and are estimated to lose US $43bn annually to global cross-border tax abuse. The urgent need to tackle illicit financial flows is clear. Despite global agreement in target 16.4 of the UN Sustainable Development Goals, however, the international architecture remains entirely insufficient to support progress – although the UN FACTI panel’s final report, due in February, will identify key gaps and make recommendations for immediate action.

At the national level, a particular challenge in countering illicit financial flows lies in prioritising among the many channels; and within each channel, identifying the economic partner jurisdictions responsible for the vulnerability. We address this research gap by elaborating on an approach pioneered in the report published by the High-Level Panel on Illicit Financial Flows from Africa (“Mbeki Panel”), which can be used to generate proxies for illicit financial flows risk by combining bilateral data on trade, investment, and banking stocks and flows, with measures of financial secrecy in partner jurisdictions. This approach rests on the observation that illicit financial flows are hidden; thus, the likelihood of an illicit component increases with the level of secrecy of any given transaction. Trade with companies in Cayman Islands will be more risky than trade with companies in Ecuador. The analysis also points to geopolitical implications, and below we explore questions of OECD responsibility for threats faced in the region.

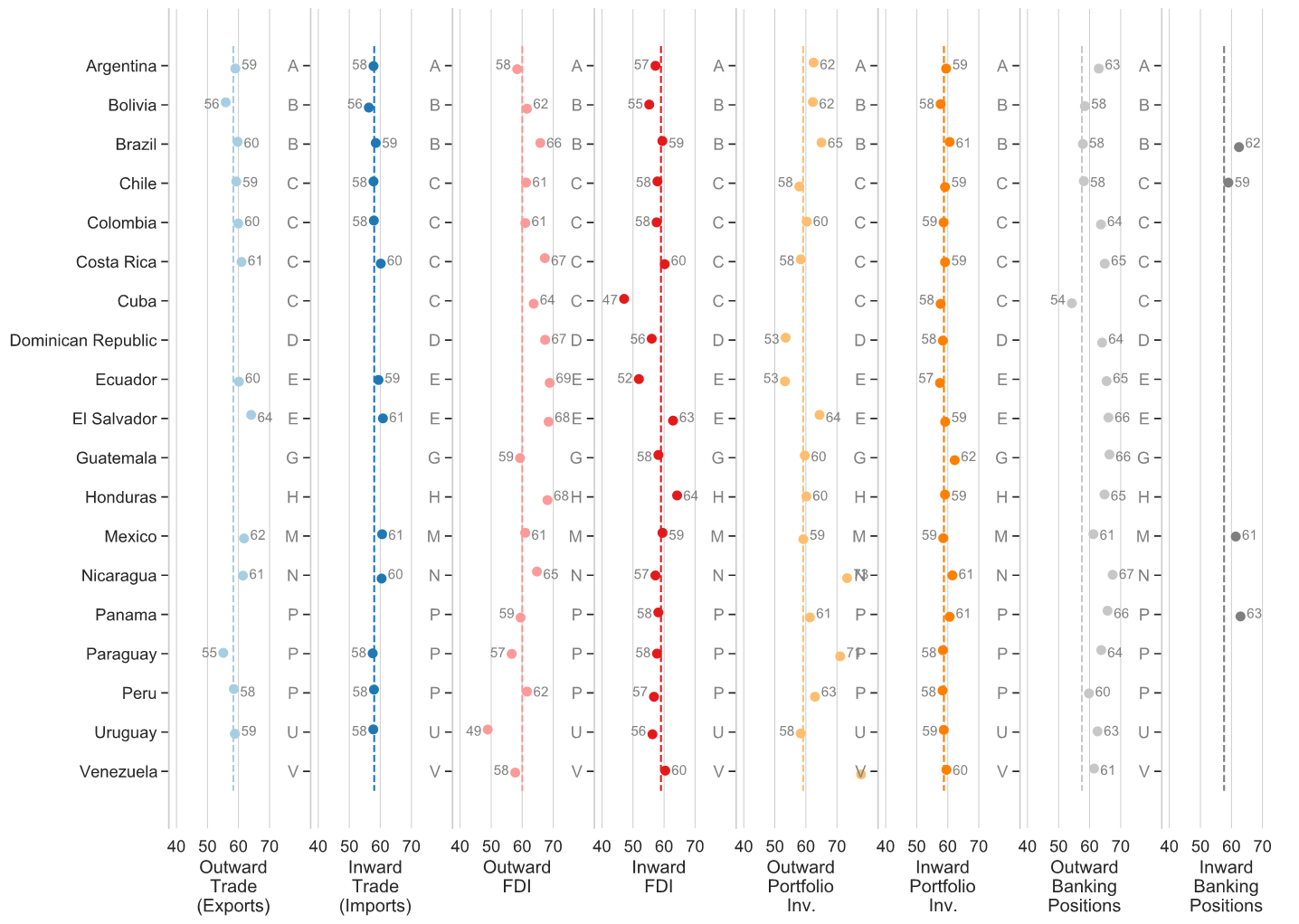

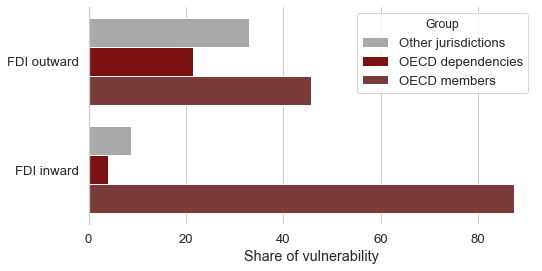

Chart 1 below illustrates the vulnerability in the eight economic channels for the 19 countries in Latin America under review, where zero represents no vulnerability or secrecy in the economic channel, and 100 implies highest vulnerability, or economic flows with an entirely secretive counterparty. The dotted lines represent the global average of vulnerability, so it can be seen that Chile, for example, faces roughly the average risk in most channels, while Mexico is more vulnerable in most.

Chart 1: Latin American jurisdictions’ vulnerability to illicit financial flows in different channels, 2018. Dotted lines represents the global average.

Risks associated with Foreign Direct Investment

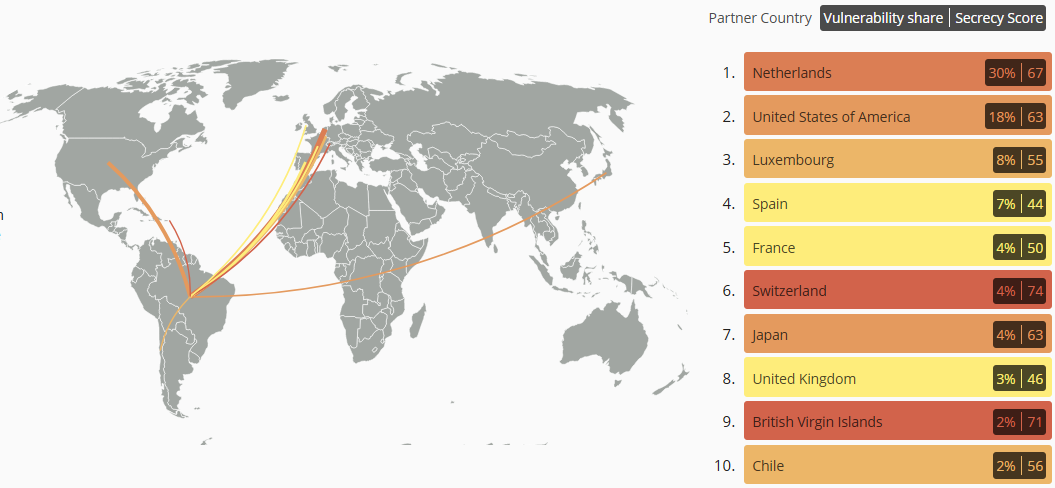

The study discusses how the data-driven vulnerability profiles for individual Latin American countries relate to, and can be used to help identify, real cases of tax avoidance, evasion, money laundering and corruption. For instance, the risks stemming from inward FDI for tax avoidance by multinational companies can be illustrated with the case of Coca-Cola in Brazil. According to a media investigation published in 2018, Coca-Cola Brazil was involved in a tax avoidance scheme. At the core of the allegations is an investment from two companies registered in the U.S. state of Delaware, a corporate tax haven and secrecy jurisdiction, into a subsidiary in Brazil. Chart 2 shows the vulnerability of Brazil’s inward foreign direct investment 2018.

Chart 2: Vulnerability of Brazil’s inward foreign direct investment stock in 2018. Source: IFF vulnerability tracker.

The Netherlands is responsible for 31 per cent of all Brazilian vulnerability in inward foreign direct investment (Chart 2). Brazil and the Netherlands have a tax treaty which can be exploited by multinational corporations. Due to its position as a corporate tax haven and a secretive jurisdiction, Brazilian authorities should pay special attention to Dutch inward investment and analyse the costs, risks, and benefits of the tax treaty between the two countries to consider cancellation of the treaty. Brazil also receives high inward direct investment from other corporate tax havens: are Luxembourg (#6 on Corporate Tax Haven Index 2019), Switzerland (#5), and the British Virgin Islands (#1), and the US (#25), as illustrated in the case of the Brazilian Coca-Cola subsidiary.

In outward direct investment, there is also the risk that domestic companies and individuals make false statements about the relationship, owners, and accounts of their foreign businesses or activities in tax returns. This may be done for round-tripping purposes. That is, to nominally invest abroad with the ultimate destination being the domestic economy, to exploit tax treaties or other provisions only available to foreign investors, or to pay kickbacks for securing contracts abroad. For instance, in 2019, Joaquín Guzmán Loera (a.k.a. “El Chapo”) was found guilty by a District Court in Brooklyn, United States, of drug trafficking and money laundering. According to the United States Drug Enforcement Administration (DEA), one of the methods used by El Chapo for laundering billions of U.S. dollars of drug proceeds consisted of using U.S. based insurance companies and controlling numerous shell companies. These shell companies and U.S. based insurance companies, into which El Chapo invested, would be recorded as (derived) outward FDI from Mexico.

Chile offers a striking example of highly concentrated illicit financial flows risks in derived outward foreign direct investment positions in Latin America. Panama dominates (over 17 per cent) all Chile’s vulnerability in outward FDI with over US$15bn of investment. While some of these investments may consist of genuine, tangible real investment interests of Chilean based companies, the magnitudes involved and the secrecy levels found in Panama suggest a significant risk that some of it is there for opacity’s sake. The British Virgin Islands (71) and Cayman Islands (76) are other high secrecy jurisdictions in Chile’s vulnerability in outward foreign direct investment.

Chart 3: Vulnerability of Chile’s outward direct investment (derived) stock in 2018

Rank

Jurisdiction

Secrecy score

Vulnerability score

Direct Investment Outward (derived) (billions) (USD)

Share of Direct Investment Outward (derived)

1

Panama

72

17.16%

15.1

14.62%

2

United States

63

12.47%

12.5

12.14%

3

Brazil

52

10.64%

13.0

12.61%

4

Peru

57

10.5%

11.6

11.28%

5

British Virgin Islands

71

9.93%

8.8

8.53%

6

Argentina

55

7.65%

8.8

8.52%

7

Colombia

56

5.59%

6.2

6.06%

8

Cayman Islands

76

4.74%

3.9

3.81%

9

Luxembourg

55

3.42%

3.9

3.78%

10

Uruguay

57

2.98%

3.3

3.20%

Overall vulnerability of investment outward (derived): 61

While this macro-level analysis signals red flags for the Chilean tax administration, which might consider investigating the outward foreign direct investment stock into some of the highly secretive and more notorious corporate tax havens itself, the next level would consist in applying the same analysis to micro-level outward foreign direct investment and intra-group trade transactions. By applying this vulnerability analysis to transaction level data, administrations can sift through large volumes of data and implement a high level advanced analytics risk mining of their datasets. This model could be applied for example to controlled transactions in transfer pricing returns filed by multinational companies, to customs declaration forms, to suspicious transaction reports, or to SWIFT money transfers, etc. By focusing limited audit capacity on transactions with the highest composite secrecy risks and with the greatest financial values cloaked in secrecy, both the revenue yield and the compliance impact of audits could be greatly enhanced. The Tax Justice Network currently partners with tax administrations to pioneer and evaluate the effects of this approach, and is working towards expanding this approach.

Geopolitical Implications

Another important finding of the study concerns the responsibility of OECD member states and their dependencies in the vulnerability (not only) of foreign direct investment in Latin America (see chart 4). In 2018, 91 per cent of Latin America’s vulnerability risk in direct (inward) foreign investment stemmed from OECD countries and their dependencies. The implied political economy of international tax governance points to the need for vigilance in the current “BEPS 2.0” process negotiations around reform of the taxation of multinational companies under the inclusive framework of the OECD. More ambitious proposals for comprehensive reforms, such as those made by the Intergovernmental Group of Twenty-Four (G24) and by the Independent Commission for the Reform of International Corporate Taxation (ICRICT), have been sidelined, as has become evident in the blueprints published in October 2020 by the OECD. Latin American countries should carefully evaluate their political representation at the OECD and the inclusive framework, and assess the potential for an enhanced role through a UN tax body and convention, not least through the FACTI panel.

Chart 4: Vulnerability in direct investment (inward and outward (derived)) 2018 – Top suppliers of secrecy risks faced by Latin America, by OECD membership and dependencies

Offshore tax evasion and automatic exchange of information

An even higher concentration of risks in OECD member states can be found in the outward banking deposits of Latin America. The case of Colombia – one of the Latin American countries which is most actively engaged in the automatic exchange of information system – illustrates the importance of risks stemming from banking relationships. As chart 5 illustrates (last column), the United States remains by far the biggest obstacle to a level playing field for countering banking secrecy by not participating in the Common Reporting Standard (CRS).

Chart 5: Vulnerability of Colombia’s banking claims (derived) in 2018, and AEOI: Automatic Exchange of Information (Y = indicating activated relationship under the Common Reporting Standard; N = absence thereof)

Rank

Jurisdiction

Secrecy score

Vulnerability score

Value of Banking Claims (derived) (billions) (USD

Share of Banking Claims (derived)

Activated AEOI Relationship?

1

United States

63

58.68%

9.5

59.39%

N

2

Panama

72

28.81%

4.1

25.52%

Y

3

Switzerland

74

3.22%

0.4

2.77%

Y

4

United Kingdom

46

2.76%

0.6

3.80%

Y

5

Spain

44

2.21%

0.5

3.20%

Y

6

France

50

1.35%

0.3

1.72%

Y

7

Australia

50

0.94%

0.2

1.20%

Y

8

Germany

52

0.59%

0.1

0.73%

Y

9

Luxembourg

55

0.33%

0.06

0.38%

Y

10

Austria

56

0.28%

0.05

0.32%

Y

Overall vulnerability of derived banking claims: 61

Latin American countries already participating in the exchange system (i.e. Argentina, Brazil, Chile, Colombia, Costa Rica, Mexico, Panama and Uruguay) might consider working towards a joint position for tweaking the parameters of the system to their needs. For example, requiring public statistics could be an effective means to increase compliance of reporting obligations in major OECD controlled financial centres. In addition, the artificial legal constraints the OECD places on the use of data for criminal corruption and money laundering investigations could be revisited. The Punta del Este declaration, “a call to strengthen action against tax evasion and corruption”, signed by participating ministers from Latin America in 2018, could provide a useful starting point for international political coordination towards more efficient and ambitious data usage. Furthermore, options to achieve fully reciprocal information exchanges, including with the United States, should be explored, including a continent-wide withholding tax on non-participating financial institutions.

All data underlying the report is available freely in the Tax Justice Network’s Illicit Financial Flows Vulnerability Tracker. In February 2021 the website will be updated, providing increased granularity (e.g. vulnerability through agricultural exports) and a user-friendly data explorer.

Policy recommendations

The report offers three broad policy recommendations to counter IFFs more effectively. In each of the chapters, more granular policy recommendations are provided.

1. Enhance data availability

Broadening the availability of statistical data on bilateral economic relationships is a first step for enabling both in depth and comprehensive analyses and meaningful regulation of economic actors engaged in cross-border transactions. In the process of collecting statistical data according to IMF standards, governments would need to build registration and monitoring capacity that likely helps improve overall economic governance.

2. Consider Latin American coordination on countering illicit financial flows risks

The bulk of illicit financial flows risks at the moment is imported into Latin America from outside the region. This finding could help foster joint negotiation positions among Latin American countries when engaging in multilateral negotiations around trade, investment or tax matters. Despite the lack of political organisation at the regional level, which makes coordination and joint action more difficult to achieve, Latin American countries might consider crafting alternative minimum standards for trade, investment, and financial services in order to safeguard against illicit financial flows emanating from secrecy jurisdictions and corporate tax havens controlled by European and OECD countries. Furthermore, Latin American countries should carefully evaluate their political representation at the OECD and the associated Inclusive Framework, and assess the potential for an enhanced role through a UN tax body and convention.

3. Embed illicit financial flows risk analyses across administrative departments

A holistic approach to countering illicit financial flows requires capacity to identify and target the areas of the highest risks for illicit financial flows. Illicit financial flows risk profiles can assist governments to prioritise the allocation of resources across administration departments and arms of government, including tax authorities and customs, the central bank, audit institutions, financial supervisors, anti-corruption offices, financial intelligence units and the judiciary. Within these departments, the illicit financial flows risk profiles would support the targeting of audits and investigations at an operational level as well as the negotiation of bilateral and multilateral treaties on information exchange at a policymaking level. Whether on tax, data, trade or corruption related matters, capacity building strategies at a continental level should include illicit financial flows risk analysis.

New year, new logo: our monthly podcast the Taxcast is entering its tenth year on the air and to celebrate we’ve got a new logo!

In this episode of the Tax Justice Network’s monthly podcast, the Taxcast:

This month Naomi Fowler speaks to activist and writer Ben Phillips about how past struggles for justice were won and how we can win them again. We discuss valuable lessons he learned from living and working around the world which he writes about in his book How To Fight Inequality and why that fight needs you.

Plus: Why is the Chinese economy so successful? Naomi discusses with John Christensen the rise of China and, unless they chuck shareholder capitalism, the continuing demise of the US and the UK.

Transcript is available here (some has been transcribed using automation so may have small inaccuracies)

Hosted and produced by Naomi Fowler of the Tax Justice Network.

Download this link to listen on your mobile device

If we on our side have every fact and every policy and the other side has all of the stories, the passion, the emotion, the excitement, then we’ll lose”

From where I’m sitting, this is the end of the line for Thatcherism and for shareholder capitalism, it’s made a tiny number of people, bankers and private equity people and mergers and acquisition specialists spectacularly rich in the past 40 years, but overall the development strategy has failed the vast majority of people in the United States and in Britain and in other countries that went down this route.”

~ John Christensen, Tax Justice Network

Want more Taxcasts? The full playlist is here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher etc. Please leave us feedback and encourage others to listen!

Join us on facebook and get our blogs into your feed.

In January 2021 the US finally joined the more than 80 jurisdictions that, as of April 2020, had a law requiring beneficial ownership information to be registered with a government authority. As described in our recent blog, this is a major victory for US activists, with particular recognition to the leading role the Fact Coalition has played, which has been working tirelessly for beneficial ownership transparency in the US.

While the new legislation is an incredible achievement that sets the world’s largest economy on the right track, it does not yet go far enough to reduce the US’s ranking of second place on the Financial Secrecy Index if it were to be reassessed today. (Currently jurisdictions are assessed every two years). Due to the limited scope of the Corporate Transparency Act and numerous exceptions in its application, we cannot yet conclude that the US is practicing effective beneficial ownership registration. Nevertheless, the law does mark a seismic shift for this super-sized economy towards tax transparency and for the imminent global reforms of the highly influential global anti-money laundering (AML) standards of the Financial Action Task Force (FATF) towards acknowledging the essential importance of the principle of central registration of ownership data at government agencies – the potential of which could be monumental further down the line.

Ironically, the US has been the cause for many countries in the world to become more transparent, either because of US domestic laws (eg the Foreign Account Tax Compliance Act, FATCA) which resulted in many countries having to change their laws in order to start exchanging bank account information automatically both with the US and with each other, or through international organisations such as the OECD or the Financial Action Task Force (FATF) where the US exerts a high degree of influence. However, when it comes to achieving change within the US, the situation is entirely different.

The US is ranked as the world’s second greatest enabler of global financial secrecy on our Financial Secrecy Index in 2020, overtaking Switzerland and coming in just after the Cayman Islands. While countries in the index on average reduced their contribution to global financial secrecy by 7 per cent, the US bucked the trend by increasing its supply of financial secrecy to the world by 15 per cent.

Given the progress other countries have been making on beneficial ownership registration, we would have expected the US to make up for lost time. For example, the EU 5th anti-money laundering directive (AMLD 5) already requires EU countries to provide public access to beneficial ownership information, and some countries like the UK have been offering free access to beneficial ownership information in open data for years. Instead, the new US law considers beneficial ownership information to be confidential. The information will have to be filed with the notoriously under-resourced financial intelligence unit (FinCen).

At the Tax Justice Network, our preference is for countries to use commercial registers for holding beneficial ownership information for three reasons. First, given that commercial registries usually hold legal ownership information, if they also register beneficial ownership, all information would be in one place, facilitating easier checks and preventing contradictory information. Second, it improves enforcement; a commercial register usually confers the status of a legal person upon fulfilling certain criteria, so entities have an incentive to comply and those not compliant with beneficial ownership requirements would be flagged directly as such on the commercial register, avoiding delays or friction between one body alerting the other and making sure non-compliant entities can be prevented from operating, holding assets or incorporating other legal vehicles. Third, it is more likely that a commercial register will give public access to information, compared to other authorities such as the tax administration, the central bank or the financial intelligence unit which are usually subject to different confidentiality and secrecy laws.

While it may have been too much to ask for the US to provide public access to its beneficial ownership register like EU countries are already required to do, we did not expect the new beneficial ownership registration law to have so many loopholes.

The Corporate Transparency Act only requires “reporting companies” to disclose the identities of their beneficial owners. The law defines “reporting companies” as follows:

‘‘(A) means a corporation, limited liability company, or other similar entity that is—‘‘(i) created by the filing of a document with a secretary of state or a similar office under the law of a State or Indian Tribe; or ‘‘(ii) formed under the law of a foreign country and registered to do business in the United States by the filing of a document with a secretary of state or a similar office under the laws of a State or Indian Tribe”

While the definition of “reporting companies” covers a “corporation, limited liability company, or other similar entity that is created by the filing of a document with a secretary of state or a similar office”, it is not clear if “other similar entities” would include other types of legal vehicles available in the US: trusts, private foundations and partnerships with limited liability.

On top of this, some reporting companies can still get out of disclosing information. While the above extract of “Paragraph A” in the bill describes what is within the scope of beneficial ownership registration in only four and a half lines, the next paragraph, “Paragraph B”, spanning across almost three pages, describes the 24 scenarios where companies are not required to file beneficial ownership information.

Any legislation with these many exceptions should be a cause for concern. It certainly makes enforcement harder and the design of circumvention strategies easier. In many cases, the reasoning for the exclusion may be that these types of companies already file information or are supervised by another authority. However, this means that for these companies, filing beneficial ownership information should not be that big of a deal, and it would ensure that all beneficial ownership information is centralised in one place.

The 24 exceptions do not refer only to companies listed on the stock exchange and investment funds, which are unfortunately often excluded from many countries’ beneficial ownership frameworks (for more information on why companies listed on the stock exchange and investment funds should not be exempted from beneficial ownership registration, see our recent brief). The exceptions extend to banks, brokers, public utility companies, public accounting firms, and even companies above a certain number of employees and sales:

‘‘(xxi) any entity that— ‘‘(I) employs more than 20 employees on a full-time basis in the United States; ‘‘(II) filed in the previous year Federal income tax returns in the United States demonstrating more than $5,000,000 in gross receipts or sales in the aggregate, including the receipts or sales of— ‘‘(aa) other entities owned by the entity; and H. R. 6395—1223 ‘‘(bb) other entities through which the entity operates; and ‘‘(III) has an operating presence at a physical office within the United States.“

Even dormant companies, instead of being de-registered to prevent them from operating in any country, benefit from an exemption from registering.

Leaving the exclusions from the scope aside, the other problem with the new US legislation has to do with the way beneficial ownership is defined. According to the new law:

“The term ‘beneficial owner’— ‘‘(A) means, with respect to an entity, an individual who, directly or indirectly, through any contract, arrangement, understanding, relationship, or otherwise— ‘‘(i) exercises substantial control over the entity; or ‘‘(ii) owns or controls not less than 25 percent of the ownership interests of the entity.“

While many countries adopt the (too high) threshold of 25 per cent, the US could have opted for lower thresholds. For example, the US could have followed the examples of Argentina, Botswana, Ecuador or Saudi Arabia which impose no threshold at all. In other words, no matter how minimal the ownership, beneficial owners will be identified. The US could also have added control scenarios, such as a percentage of voting rights (or at least one vote), the right to appoint or remove the board of directors, and so on. The high US threshold means that even companies that do not qualify for exemption and are required to disclose may still evade identifying their beneficial owners if these individuals own less than 25 per cent of a company’s shares (and are not considered to exercise “substantial control” either).

Lastly, the beneficial ownership definition does not specify in cases where a reporting company is owned by a trust, which party from that trust should be identified as a beneficial owner. The US could follow the lead of the Financial Action Task Force and the EU’s 5th Anti Money Laundering Directive in such cases, which would require every party to the trust – the settlor, trustee, protector, beneficiaries and any other individual with control over the trust – to be registered as a beneficial owner.

Given the new US administration under Biden, we are optimistic that through regulation some of these issues may be resolved. In any case, kudos to our US friends who have achieved what was long considered impossible. We should now all feel strengthened to achieve even more ambitious progress together.

In the last months of 2020, Argentina issued two new resolutions requiring the filing of relevant information to the tax administration: beneficial ownership information on trusts (General Resolution 4879) and information on tax schemes (General Resolution 4838). These resolutions help put Argentina at the vanguard of availability of information with government authorities, joining many EU countries. However, unlike EU countries, Argentina is yet to make information publicly available.

Trusts’ beneficial ownership information

As described by our papers (here and here) trusts are especially problematic legal vehicles, creating a high degree of secrecy based on the fact that, unlike companies, they need not be incorporated or registered in order to become legally valid. In addition, trusts have very complex control structures, involving many potential parties such as a (legal or nominee) settlor, an economic settlor, trustees, protectors, beneficiaries, classes of beneficiaries, purposes, etc. Moreover, even if all trust parties are disclosed, trusts have managed to keep shielding their assets against tax authorities and other legitimate creditors, including victims of murder and sexual abuse.

A few months ago, we blogged about Argentina’s beneficial ownership registration based on the tax administration (AFIP) General Resolution 4967 of April 2020. (This regulation was then amended by General Resolution 4878. An updated and consolidated version of Resolution 4697 is available here). While we commended this improvement, we noted that it covered only legal persons but failed to extend the beneficial ownership obligations to trusts. Argentina’s General Resolution 3312 from 2012 was already pretty advanced, requiring many types of trusts and their parties to be disclosed to the tax administration. However, it referred only to legal ownership information.

However, the new General Resolution 4879 of October 2020 extended the Resolution 3312’s requirements to cover also beneficial ownership information for domestic and foreign law trusts. Importantly, the full ownership chain has to be disclosed whenever the party to the trust is a foreign legal vehicle. Additionally, all beneficial owners of those legal vehicles which are parties to the trust have to be identified as beneficial owners of the trust regardless of any threshold. In other words, if trust A has company 1 as its trustee. John has 1 share and Mary has the remaining 999 shares in company 1, both John and Mary will have to be identified as the beneficial owners of company 1 and of trust A.

Positively, all beneficial ownership information will be held by a single authority, the tax administration, facilitating cross-checks. On the negative side, information will not be made public. Additionally, it’s not clear how much coordination there is with local commercial registries to ensure that all incorporated entities file their beneficial ownership information with the tax administration.

Reporting of Tax Schemes

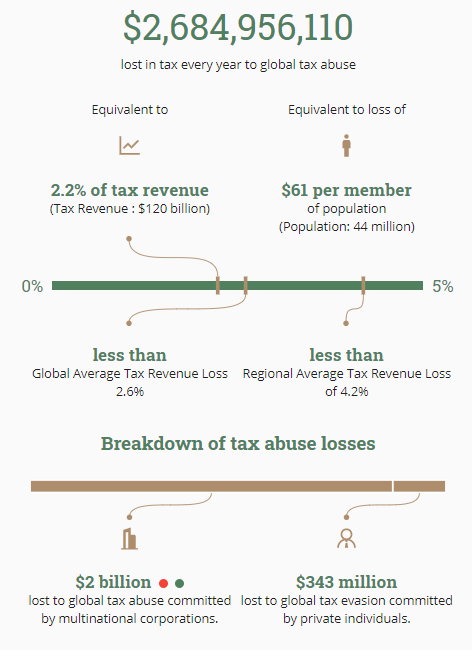

Tax abuse by multinationals and individuals continues to be a major problem, affecting state revenues and the guarantee of basic human rights. As our State of Tax Justice 2020 report described “Countries are losing a total of over $427 billion in tax each year to international corporate tax abuse and private tax evasion.”

In the case of Argentina, the Tax Justice Network’s Illicit Financial Flows Tracker (IFF Tracker) shows how much money is lost to tax abuse by multinationals and individuals:

In an attempt to tackle tax abuse, and in accordance with the OECD’s Action 12 of the Base Erosion Profit Shifting (BEPS), Argentina has issued General Resolution 4838 requiring taxpayers and tax advisers to report their tax avoidance schemes.

By doing this, Argentina joins the 27 EU Member States who are already requiring that taxpayers or tax advisers report tax schemes under the amendment to the Directive on Administrative Cooperation, known as DAC 6. As described by indicator 13 of the Financial Secrecy Index published in 2020, there were 31 jurisdictions which required tax advisers to report tax schemes. Apart from the EU, countries include Canada, Mexico, South Africa and the United States. Countries such as Canada, Israel, South Africa, the US and the UK also require taxpayers to report tax schemes. The US even requires them to report uncertain tax positions. Indicator 13 describes the reasoning that justifies the reporting of schemes:

There are several reasons to support the imposition of mandatory reporting of tax avoidance schemes. First, the reporting requirements help tax administrations to identify areas of uncertainty in the tax law that may need clarification or legislative improvements, regulatory guidance, or further research. Second, providing the tax administration with early information about tax avoidance schemes allows it to assess the risks schemes pose before the tax assessment is made and to focus audits more efficiently. This is significant mainly because, in many jurisdictions, tax administrations do not have sufficient capacity to fully audit a large number of the tax files. Thus, flagging certain files that carry a greater risk of tax avoidance is likely to increase the efficiency of tax administrations and their ability to increase tax revenues. Third, requiring mandatory reporting of tax schemes is likely to deter taxpayers from using these tax schemes because they know there are higher chances that files will be flagged, exposed and assessed accordingly. Fourth, such mandatory reporting may reduce the supply of these schemes by altering the economics of tax avoidance of their providers because a) they will be more exposed to claims of promoting aggressive tax schemes, increasing the risk of reputational damage, and b) their profits and rate of return on the promotion of these schemes is likely to be reduced because schemes are closed down more quickly. This is all the more true if contingency fees are part of contracts…

The difficulty in imposing mandatory reporting rules for tax avoidance schemes is the potential for ambiguity of whether the scheme is considered a tax avoidance scheme within the mandatory disclosure rules. In order to mitigate against this risk, the reporting obligation should not apply only to the taxpayer who uses the tax scheme or only to the promoter (tax advisers) of the scheme, but rather to both. This kind of double obligation is imposed in the United States. If both are obliged to report independently on the marketed/used tax avoidance schemes, the chances that tax administration will be able to detect hidden dubious schemes are significantly higher. Precisely because there are numerous and regular conflicts between the tax administration and taxpayers/advisers on the interpretation of tax laws, it should be expected that many tax schemes will be designed in grey areas which certain promoters might chose to interpret as not being subject to the remit of the reporting obligation. Third party reporting obligations increase the detection risk of these dubious schemes and thereby incentivises the reporting of a broader set of schemes”

Unfortunately, unlike DAC 6, Argentina’s Resolution 4838 failed to include more schemes. For instance, in relation to the automatic exchange of bank account information under the OECD’s Common Reporting Standard, countries are expected to adopt the OECD Mandatory Disclosure Rules which require the filing of schemes used to circumvent reporting under the automatic exchange of information system or to hide the beneficial owner behind opaque structures.

The other problem with Argentina’s Resolution, as with the EU’s DAC 6, is the issue of professional secrecy, where tax advisers and intermediaries may refuse to disclose information based on confidentiality rules.

We have blogged about the problem of professional secrecy, which goes beyond tax schemes and covers risks to money laundering, as described by the Financial Action Task Force. On a positive note, there are some cases of improvement as we blogged here, including a recent US case law granting the US tax administration access to a law firms’ list of clients who were potentially using the law firm’s advice to engage in tax evasion.

In conclusion, Argentina’s recent regulations keep pushing the country towards more transparency, although Argentina should not forget the importance of giving public access to information, especially on beneficial ownership. However, Argentina as well as the rest of the world will need to keep fighting against the damage of professional secrecy. Although confidentiality makes sense in some cases (eg to prevent a doctor from disclosing medical records, or the right to a fair trial), it should certainly not be used by the most powerful multinationals and high net worth individuals in order to keep engaging in abusive practices that erode state revenues, hurting the vast majority of people who are not part of the 0.1 per cent.

Welcome to our Spanish language podcast and radio programme with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. New year – new logo! We hope you like it! ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita. ¡Nuevo año, nuevo logo! Esperamos que les guste a todos.

En este programa:

La economía mundial del 2021 ¿Qué pasará con la pandemia y con América Latina?

La necesidad de un sistema tributario internacional equitativo para el desarrollo económico y la justicia social

Y el hashtag impuesto a la riqueza ya la nueva campaña en América Latina para que los ricos paguen más impuestos.

Invitados:

Oscar Ugarteche, profesor de la Universidad Nacional Autonoma de Mexico, la UNAM y autor de Historia Critica del FMI

Daniel Titleman, director de planificación económica de la CEPAL

Swiss bankers, and many other tax haven operatives, have always complained that they are unfairly victimised by international anger over their financial secrecy practices. “What about Delaware,” they routinely asked, “how come they can get away with it?”

And, at least in this respect, they had a point, even though it was merely a cheap exercise in what-aboutism. But, as of January 1, no longer:

“An historic anti-corruption measure ending anonymous companies in the United States became law on Friday, capping a more than decade-long campaign by transparency advocates, after both Chambers of Congress voted to override the president’s veto of the annual defense bill.”

This is a major victory. As we have long pointed out, the United States has long been one of the world’s biggest, if not the biggest, tax havens: our latest Financial Secrecy Index ranks them as Number 2 worst offender.

The U.S. has provided secrecy on two main levels. First, at a federal level, where the US doesn’t share too much financial information with foreign governments whose residents or taxpayers stash assets in the U.S. Second, at a state level, where individual U.S. states have made it easy to set up impenetrable shell companies where it’s impossible for the forces of law, order and taxation to find out who owns a company’s assets. It has famously been easier to set up a secret shell company in the U.S. than it has been to obtain a library card. Some U.S. states, most famously Delaware, South Dakota, and Wyoming, have specialised in setting up cheap, sleazy company formation businesses which have stooped to catering to and abetting human traffickers, mafia organisations, North Korean despots and peddlers of nuclear materials.

Most positive of all, perhaps, is the amazing coalition that grew up in the US to oppose shell company secrecy, and the power that came with joining forces. This was a classic “fusion coalition“, led by the indefatigable Financial Accountability and Corporate Transparency (FACT) Coalition, which was originally set up under the leadership of Nicole Tichon, who was also Executive Director of our affiliate Tax Justice Network USA. FACT brought together a range of unlikely bedfellows, as they outline:

hundreds of national security experts, police and prosecutors, banks and credit unions, CEOs, the real estate sector, large businesses, small business owners, faith groups, anti-human trafficking groups, human rights organizations, global development NGOs, anti-corruption advocates, labor unions, and conservative and liberal think tanks.

The victory, and the long list of supporters that helped deliver it, highlights how “our” issues with tax havens can find support from across the political spectrum, and in this respect it mirrors our successes elsewhere in pushing for global reforms. For a look at the history of this movement, this is a good place to start.

This is an incomplete victory, of course. For one thing, the Corporate Transparency Act requires corporations and limited liability companies (LLCs) to tell law enforcement and others with legally mandated anti-money laundering responsibilities (such as financial institutions) information on the real, natural person (or “beneficial owner”) who owns and controls an entity at the point of formation, and update this information when there is a change — but this information is not required to be made publicly available (as is now partly required, for example, by the European Union). In addition, the U.S. is still a laggard when it comes to sharing information with other jurisdictions. We have argued that in many cases authorities should move beyond forcing legal entities and arrangements to disclose information to the relevant authorities, and to make certain information public.

But this is not to take away the significance of this hard-fought and well-earned victory.

Britain’s Times Newspaper is carrying a story entitled Errors in The Crown may prompt tighter rules for streaming services. The issue at hand, apparently, is that the Netflix series The Crown isn’t sticking closely enough to historical facts, and showing the Royal Family in a poor light.

Quelle horreur!

But what’s of interest to us here at the Tax Justice Network is that this is the latest sign of a race to the bottom among jurisdictions when it comes to investigation and enforcement of abuses. As the article states:

“Streaming platforms such as Netflix and Amazon Prime Video are covered by a weaker EU-wide regime, known as the audio visual media services directive. Netflix is registered with the Commissariaat voor de Media, a little-known Dutch regulator, which as of last year had not investigated a single complaint from a British viewer about the streaming service.”

We don’t care much whether or not The Crown,a drama, sticks to historical facts. But we do care that complaints get taken seriously.

The Netherlands is at No. 4 in our Corporate Tax Haven Index — meaning, in effect, that it is the world’s fourth most damaging tax haven. And as we shall see, it is no coincidence that a damaging tax haven should also be super-lax on regulating audio-visual services like Netflix. A privacy expert told TJN, via an email on this subject:

“Being a tax or data haven is wanting to profit from allowing others to behave questionably and promising to turn a blind eye.”

Internet services are another case in point. Giant monopolising platforms like Facebook or Google fall under Europe’s General Data Protection Regulation (GDPR). Lax regulation of data sharing has contributed to all manner of abuses, from climate crimes to fake news to genocide.

The specific problem here involves what is called, in EU jargon, the “Lead Supervisory Authority” for the internet giants, which is the jurisdiction where the Facebooks of this world decide to put their European HQs for tax and regulatory purposes — this will be the country that co-ordinates investigations into abuses across Europe. Obviously — obviously — this approach of letting large global platforms go jurisdiction-shopping to find the friendliest data supervisor and enforcer is likely to lead to a race to the bottom, as jurisdictions try to outdo each other in laxity, to capture the giants’ business.

A report from Access Now, a group that protects people’s digital rights, provides new evidence on lax supervision of online content — and highlights jurisdictions whose identities will surprise nobody who is familiar with corporate tax havens.

“Ireland and Luxembourg, which are the main authorities dealing with the cases involving Amazon, Facebook, WhatsApp, Twitter, PayPal, Instagram, Microsoft, Google, and others, have issued zero fines against the tech giants to date. In the meantime, in 2018 and 2019, the Irish authoritiy received a total of 11,328 complaints.”

In fact, Ireland has now just imposed a fine (against Twitter) for failing to notify regulators after a data breach. This may sound like progress — but it isn’t. Under the GDPR Ireland could have fined Twitter two percent of its $3.5bn global annual revenue, or around US$70 million (nearly €60m) according to our calculations. In the event, the Irish regulator took two years to levy the fine and came up with . . . $450,000. Ian Brown, an authority on internet regulation, described the fine as “an embarrassment… the Irish data protection commissioner is notoriously lax.” And, as one article on the fine put it:

“The Irish regulator originally wanted to fine Twitter even less than this, but through the dispute-resolution process, it was told to increase the amount.”

Brown told TJN that the Irish data regulator:

“just do not remotely have the resources they need to employ enough staff — including highly expert staff who understand the technology — or the political will to really make use of their enforcement powers.”

Ireland is, alongside its data haven role, another of the world’s largest — and sleaziest — corporate income tax havens, bowing down to rootless global capital by offering tax loopholes such as those that allowed Apple to set up companies that existed, in effect, nowhere. This game has undercut other countries’s tax systems and has not even benefited the broad population of Ireland. Luxembourg, at number 6 on the CTHI, also engages heavily in the data haven game, particularly through its hosting of Amazon.

Access Now summarises the problem:

Large tech companies have nearly endless financial resources in comparison to the restrictive budget allocated to Data Protection Authorities. In the case of Ireland, the revenue of some of these companies is even higher than the Gross Domestic Product of the country.

There is more bad news — alongside some potentially good news.

On the worrying side, Britain, which hitherto hassuccessfully levied some meaningful fines against large companies for GDPR abuses, now faces Brexit, its departure from the European Union. A recent article by Carissa Veliz in The Guardian quotes the UK’s digital secretary as saying that:

“Data and data use are seen as opportunities to be embraced, rather than threats against which to be guarded.”

That is indeed worrying. And the article continues:

“The UK could develop into a data haven, in the way some countries are tax havens. A data haven would be a country involved in “data washing”, being willing to host data acquired in unlawful ways (eg without proper consent or safeguards) that is then recycled into apparently respectable products.

(Data washing) would involve the UK allowing companies and governments the world over to do their dirty data work under its protection in exchange for money. [This] could turn into a privacy catastrophe.”

This is a realistic fear: there are powerful interests in the UK pushing for the UK, once out of the EU, to engage in tax-cutting and deregulation to attract capital, and data havenry. (That’s another can of worms.)

But now, for some potentially very good news.

There is a straightforward solution to this, at least to the race-to-the-bottom element of it. And that is to do away with the “lead supervisory authority” system that allows giant companies to shop for the friendliest supervisor. Instead, supervision and enforcement should be centralised at a European level.

The European Commission has just published its proposals for a Digital Markets Act (and Digital Services Act,) a broad, sweeping set of proposed legislation to deal with the digital economy in there. And we find, in the DMA proposals, this:

The Commission examined different policy options . . . All options envisaged implementation, supervision and enforcement at the EU level by the Commission as the competent regulatory body. Given the pan-European reach of the targeted companies, a decentralised enforcement model does not seem to be a conceivable alternative, including in light of the risk of regulatory fragmentation . . . the functioning of the internal market will be improved through clear behavioural rules that give all stakeholders legal clarity and through an EU-wide intervention framework allowing to address effectively harmful practices in a timely and effective manner. [our emphasis]

This, potentially, is huge — and worthy of support: these are still just proposals, which need to pass through the EU sausage machine before they harden into law, perhaps a year or two hence.

The tax justice movement must now join forces with digital rights groups and others, to protect this crucial aspect of regulation in the digital age. This is the kind of cross-silo movement-building of “fusion coalitions” which, history suggests, can be the most effective of all.

We recently covered the global Cigarette Tax Scorecard, published by Tobacconomics, which assesses the extent to which countries’ tax policies are up to the job of curbing the public health costs of tobacco. Now we look at a new report on the tax behaviour of the tobacco companies. The University of Bath’s Tobacco Control Research Group, which tweets at @BathTR, is a world leader in critical analysis of the harms done by tobacco. We’re delighted to post this blog by the group’s Dr J Robert Branston and Andy Rowell, on a major new study conducted with The Investigative Desk, into the international tax abuse practices of the big tobacco companies. The full report is available to download, as is the Tax Justice Network’s earlier study on this subject, Ashes to Ashes.

Guest blog by Dr J Robert Branston and Andy Rowell

There are often stories in the media about large tech companies not paying much corporation tax despite their business generating massive earnings. Companies such as Facebook and Google are often cited as examples of companies who use clever corporate structures to avoid paying tax at the levels their revenues might imply. It is therefore very welcome that HM Revenue & Customs, the UK tax and customs authority, has recently moved to crackdown on such schemes. As part of this push to hold companies account, they would do well to start by looking at the tobacco industry.

It is widely known that tobacco companies are immensely profitable, but a lot less is known about how the industry structures their commercial activities to pay far less tax than they should on these profits. The Investigative Desk, working with the University of Bath, have been starting to figure out what they are doing.

The analysis of group annual reports and accounts for the period 2010-2019, including of a number of crucial subsidiaries, shows that all of ‘Tobacco’s Big Four’ transnational companies – British American Tobacco, Imperial Brands, Japan Tobacco, and Philip Morris International – have ‘aggressive tax planning’ strategies, in spite of their own codes of conduct suggesting otherwise.

It is clear that all four make extensive use of the entire range of common corporate tax abuse methods. This includes shifting dividends through low tax countries, utilising notional interest payments on inter-subsidiary loans, making royalty payments to other subsidiaries, and offsetting profits in one subsidiary against losses elsewhere, all of which reduce profits on paper and hence their tax bills.

Six European countries play a key role in the elaborate corporate tax abuse strategies of Tobacco’s Big Four because of the tax rules in each of the countries: Belgium, Ireland, Luxemburg, the Netherlands, the UK, and Switzerland. For instance, on average, Tobacco’s Big Four shift around €7.5 billion of worldwide profits through the Netherlands annually. While in the UK, the local subsidiaries of Imperial Brands (IB) and British American Tobacco (BAT) – groups based and headquartered in the UK – were able to lower their UK corporate tax burden by £2.5 billion between 2010 and 2019. As a result, BAT paid close to zero corporation tax over this period. IB’s annual reports are so untransparent that their actual UK tax burden is virtually impossible to determine.

One telling illustration of the lengths the industry goes to avoid paying tax on their profits is from BAT’s operations in South Korea. All BAT cigarettes produced by local subsidiary BAT Korea Manufacturing Ltd (South Korea) are sold – on paper – to Rothmans Far East BV, a BAT subsidiary in the Netherlands. They are then immediately re-sold to a different BAT subsidiary back in Korea, BAT Korea Ltd, at a much higher price. This way, on average each year, €98 million in Korean profits are shifted to the Netherlands where the tax regime is more favourable.

All countries, most especially the six mentioned above, need to crack down on these corporate tax abuse measures. A number of countries are already trying to do just that, with the industry engaged in tax disputes in at least 11 countries over the last ten years, with claims ranging from €45 million to €1.2 billion. So far, in the majority of cases, the courts’ decisions have been in favour of the companies. This shows that changes to tax laws are desperately needed so that tobacco companies can’t circumvent their tax obligations with the use of complex loopholes.

Since the tobacco industry profits enormously from a product that kills at least half of its long-term users, tobacco companies need to pay their fair share in line with the spirit, as well as the letter, of the law. With many governments facing huge COVID-19 related expenses, the time has never been better to hold the industry to account in this way.

—

The TCRG is supported by Bloomberg Philanthropies, which had no influence on the research for the report, or blog.

In this episode of the Tax Justice Network’s monthly podcast, the Taxcast:

This month we take a look at the transformative power of financial transactions taxes. There’s a chance that New York, home to two of the world’s largest stock exchanges, could be about to set an important precedent. We go to Kenya to look at its experience with a financial transactions tax. And we see how much further the tax could go.

Plus: we discuss three major waves of change in 2020: the black lives matter protests, Trump’s departure from the Whitehouse and the end of the Brexiteers dream. (Subscribe to the Taxcast via email by contacting the Taxcast producer on naomi [at] taxjustice.net)

Transcript available here (some is automated and may not be 100% accurate)

Produced and presented by the Tax Justice Network’s Naomi Fowler

Want to download and listen on the go? Download onto your phone or hand held device by clicking here.

“It’s interesting that you know, now the gospel is spreading from Africa to the more developed world that have been overtaken by the likes of Kenya and Tanzania and South Africa in implementing a robin hood tax.”

A Financial Transactions Tax is “a brilliant, easily collected tax. It doesn’t cause any pain to investors. I mean there are damn few alternatives. Do you want us to really just fire all the state workers shutting down schools and laying off teachers, you know, how do you get Wall Street to pay its fair share here?!”

~ Economist, lawyer and senior Tax Justice Network advisor Jim Henry

The value of global capital flowing through financial markets is actually 28 trillion pounds per day. if we just charge a 0.05% tax rate, we’re looking at 14 billion pounds per day to fund reparations and systems change.”

The Brexiteer project was to break the European Union’s resolve, to break the whole project of trying to create an international rules-based trading order, in other words, to create a kind of globalisation where there were no rules, no frameworks for cooperation. And that project has failed.“

You can read Keval Bharadia’s paper “Recalibrating financial transaction tax policy narratives” here. You can look at his slides on Recalibrating financial transactions tax policy narratives for reparations here.

You can read about the efforts towards a financial transactions tax in New York here.

The Tax Justice Network’s Financial secrecy Index is available here

Africa’s battle against financial secrecy is here.

You can listen to the Tax Justice Network’s Rachel Etter-Phoya speaking on Africa and the Financial Secrecy Index here:

Want more Taxcasts? The full playlist is here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher etc. Please leave us feedback and encourage others to listen!

Join us on facebook and get our blogs into your feed.

Towards the end of a challenging, yet also dramatically impactful year, we are excited to announce the recruitment of two researcher roles in the Financial Secrecy and Governance workstream. In the past years, at the Tax Justice Network we have made substantial progress in demonstrating how tax avoidance and evasion globally are sufficiently large and certain to constitute a first-order economic distortion, especially in lower-income countries. In line with this, we have been widening our perspectives on and in the planet, by shifting our attention and centre of gravity beyond the UK and other OECD countries. With the current recruitment of two researchers focused on Latin America and francophone Africa we are very pleased to further support this shift in the next years.

The researchers are going to work in the technical engine rooms of our two leading indices that underpin and monitor the global progress towards a more equal and just world. By researching in the laborious cycles of both the Financial Secrecy Index and the Corporate Tax Haven Index, the researchers will be able to develop an in-depth and cutting edge understanding of leading policies for countering cross-border illicit financial flows, ranging from money laundering by organised crime to tax avoidance by multinational corporations. Yet the pauses in between the nitty-gritty research will offer the researchers to partner with others in- and outside the Tax Justice Network to transform empirical data into studies, reports and peer reviewed academic articles for publication and presentation.

We look forward to recruiting these new roles and invite you, dear reader, to consider applying or distributing this link to any suitable candidates.

Please click on the links below to view for further information on each of the roles and details on how to apply.

Welcome to our monthly podcast in Portuguese, É da sua conta (it’s your business). All our podcasts (unique productions in five different languages – English, Spanish, Arabic, French, Portuguese) are available here.

#20 Mundo perde US$ 427 bi com abuso fiscal internacional em 2020

O mundo perde pelo menos US$ 427 bilhões por conta de abusos fiscais cometidos por corporações multinacionais e super-ricos em 2020.

Esse dinheiro, que poderia combater as crises social e econômica da pandemia de covid-19 ou ainda a crise climática, é desviado da justa contribuição com impostos e enviado a paraísos fiscais.

Tobacconomics Scorecard Shines a Light on the Untapped Potential of Cigarette Taxes.

We are delighted to publish this guest blog by Erika D Siu, Project Deputy Director, Visiting Senior Research Specialist, Institute for Health Research and Policy, The University of Illinois. It illustrates the justice of, and the need for, re-pricing to limit public “bads” such as tobacco consumption and carbon emissions.

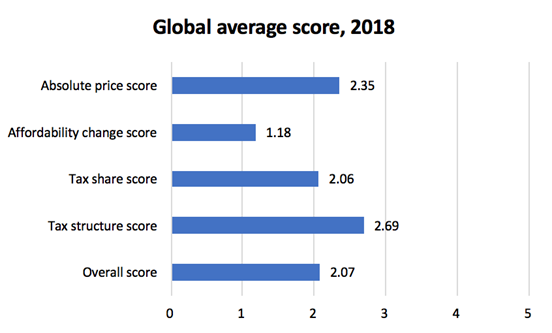

Tobacconomics — a group of researchers at the University of Illinois Chicago recently released the first edition of the international Cigarette Tax Scorecard assessing the performance of cigarette tax policies in over 170 countries. Using data from the World Health Organisation, the Scorecard assessment is based on four key components: cigarette price (using purchasing power parity dollars to compare price across countries), changes in the affordability of cigarettes over time, the share of taxes in retail cigarette prices, and the structure of cigarette taxes. Each of the four components is scored using a five-point index, with the total score reflecting an average of the four component scores.

The results show that globally, the overall performance of cigarette tax policies is quite low—especially given the magnitude of the economic and health losses related to tobacco use. Out of a maximum of five points, the global average score is only 2.07.

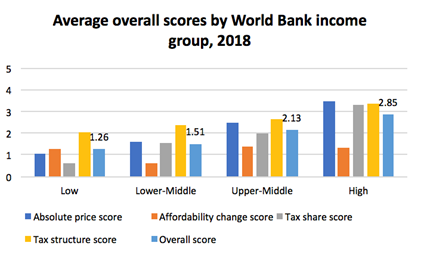

The Scorecard also reveals that low-income countries in particular stand to reap the most health and economic benefits by raising their tobacco taxes as they have very low tax shares of retail price. The higher the tax share, the more the government gains in revenue vis-a-vis the tobacco industry, which in most countries is dominated by transnational tobacco companies.

Evidence from around the world shows that higher taxes lead to higher prices and that these higher prices decrease overall tobacco use, lead current users to quit, prevent young people from initiating tobacco use, and reduce the negative health and economic consequences of tobacco use.

Tobacco tax increases have the greatest impact in reducing tobacco use among vulnerable populations, including young people and low-income populations. Tobacco use among young people is more sensitive to price increases than tobacco use among adults, which is particularly important given that nearly all tobacco users start during adolescence or as young adults.

Similarly, low-income tobacco users are more responsive to tax and price increases than higher income groups in addition to being more susceptible to the damaging health impacts of tobacco use because they often lack access to health care and services and/or are more likely to have other serious health problems. Faced with higher taxes and prices, these users are more likely to quit or reduce their tobacco use.

At the same time, increasing tobacco taxes generates new government revenues. Despite the reductions in tobacco use that follow tax increases, country experiences across the globe show that significant tobacco tax increases lead to increases in tobacco tax revenues. This happens because the reductions in tobacco use are less than the increase in price, given the addictive nature of the nicotine in tobacco products. The increases in government revenue can be used to fund public health and other sustainable development priorities. The WHO estimates, for example, that a cigarette tax increase of US$ 1 per pack would have raised between US$ 178-219 billion in 2018.

The simultaneous global health and economic crises caused by the COVID-19 pandemic have had devasting impacts on government budgets. Increasing tobacco taxes provides a logical first step for governments to raise revenue for economic recovery while promoting public health. Tobacco use—a slow-moving pandemic in itself—results in more than 8 million deaths and costs economies around US$ 1.4 trillion each year, with the burden falling heaviest on low- and middle-income countries. The Scorecard results show considerable untapped potential for cigarette tax increases to curb these costs and raise much needed revenue.

See also Tax Justice Network’s earlier report Ashes to Ashes.

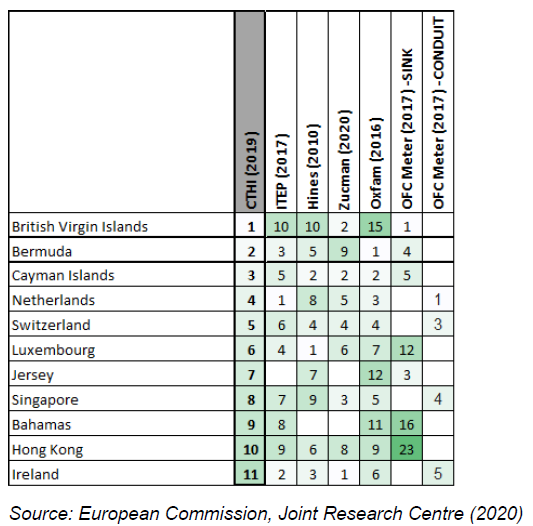

The statistical side of the tax equation: The Joint Research Centre Audit of the Corporate Tax Haven Index

By Szilárd Erhart, European Commission’s Joint Research Centre

Indexes are getting increasingly important for policy design, implementation and assessment in today’s information age. Multifaceted issues like tax evasion are difficult, if not impossible at all, to measure by a sole indicator. Information aggregated in an index can, however, effectively synthesise complex and large dataset and distil messages into user-friendly and easy-to-understand measures.

Still, we have to admit that the index development process is challenging at every stage from the conceptualisation to the measurement and communication. To support index developers in improving the reliability and transparency of their indices, the European Commission’s Competence Centre on Composite Indicators and Scoreboards (COIN) at the Joint Research Centre (JRC) in Italy, carries out statistical audits of indexes upon request of international organisations and other European Commission services. To date, over 100 indexes, in a variety of policy domains, have received tailored recommendations from our research team at the JRC.

In 2019, the Tax Justice Network reached out to JRC colleagues and requested the statistical assessment and audit of the Corporate Tax Haven Index, similar to a 2018 JRC audit of the Financial Secrecy Index. The Tax Justice Network team wanted to cross-check the methodology, the background calculations and conceptualisation of the Corporate Tax Haven Index. The JRC’s statistical assessment of the Corporate Tax Haven Index was undertaken between Dec 2019 and June 2020.

After mutually beneficial discussions in 2020, with suggestions for improvements in terms of data characteristics, structure and methods used, the JRC published the statistical audit of the Corporate Tax Haven Index. The audit focused on the statistical coherence of the structure of indicators and the impact of key modelling assumptions on the Corporate Tax Haven Index.

The Corporate Tax Haven Index methodology was found by the JRC to be coherent and thoroughly considered by experts of tax evasion. The audit showed some of the differences in scoring of Corporate Tax Haven Index indicators, their correlation with other indicators and discussed how all these can influence the final Corporate Tax Haven Index scores and rankings. The JRC suggested to weigh up the possibility of using a geometric average for the aggregation of indicators, as it may better reflect the non-compensatory nature of tax avoidance. In general, the Corporate Tax Haven Index was found to be robust, top ten ranked countries of the Corporate Tax Haven Index are in the top of other lists of tax havens in recent studies, applying different empirical methods for the identification. As recommended by the JRC team in its Financial Secrecy Index audit, it would be worthwhile to publish confidence intervals alongside the ranking.

Table 1: Top-ranked countries in corporate tax haven rankings

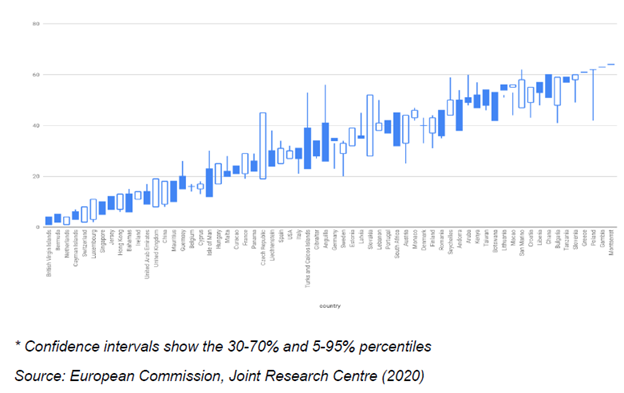

The development of the Corporate Tax Haven Index, like the construction of any composite indicator, involves assumptions and subjective decisions. The JRC tested the impact of varying some of these assumptions within a range of plausible alternatives in an uncertainty analysis. Here, the objective was to attempt to quantify the uncertainty in the ranks of the Corporate Tax Haven Index, which can demonstrate the extent to which countries can be differentiated by their scores. Although many assumptions made in the development of the Corporate Tax Haven Index could be examined, three particular assumptions were examined in this uncertainty analysis

1. Corporate Tax Haven IndexIndicator set [Full set] vs. [Reduced set]

2. Aggregation method [Arithmetic mean] vs. [Geometric mean]

3. Weights [Randomly varied +/-25% from equal weights]

These were chosen as plausible alternative pathways in the construction of the Corporate Tax Haven Index, which can be relatively easily investigated.

The uncertainty in the Corporate Tax Haven Index rankings, given the assumptions tested, was found mostly quite modest. Country ranks could be stated to within around 13 places of precision (Figure 1), although some countries are especially sensitive to the assumptions made. This information should be also used to guide the kind of conclusions that can be drawn from the index. For example, differences of two or three places between countries cannot be taken as “significant”, whereas differences of 10 places upwards can show a meaningful difference. One can also observe that the confidence intervals are generally wider for mid-ranking countries, and narrower for top and bottom-ranking countries.

Figure 1: Simulated rankings (median values and confidence intervals)*

We expect the Corporate Tax Haven Index and its background dataset to energise tax evasion experts, to provide them with a useful benchmark and to help re-colour the black economy with colours from white to green.

About JRC: The Joint Research Centre (JRC) is the European Commission’s science and knowledge service. The JRC provides European Union and national authorities with solid facts and independent support to help tackle the big challenges facing our societies today. The JRC creates, manages and makes sense of knowledge, delivering the best scientific evidence and innovative tools for the policies that matter to citizens, businesses and governments. Twitter: @EU_ScienceHub

Welcome to this month’s latest podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast favorita. [The image “i bleed america latina” by leonelponce is licensed under CC BY 2.0]

“Shell and other oil majors are avoiding hundreds of millions of dollars in taxes in countries where they drill by shifting profits to thinly staffed insurance and finance affiliates based in tax havens, according to a Reuters review of corporate filings and rating agency reports. Shell, BP Plc, Chevron and Total use subsidiaries in the Bahamas, Switzerland, Bermuda, the UK Channel Islands and Ireland.”

Companies claim they do not “engage in artificial tax arrangements.”

One of the most interesting aspects of this report concerns “captive insurance”, which are subsidiaries of the fossil fuel companies, parked in tax havens: their core role seems to be more about escaping tax, than about insuring things. The Reuters story contains an excellent short explainer about how captive insurance works.

Normally, an insurance company hopes to take in more in insurance premiums (which are income) than it has to pay out in insurance claims (which are costs), and if income is greater than cost then it makes a profit.

Captive insurance throws a well-aimed tax haven spanner into this, as the story notes:

“The big oil firms’ captive insurers are far more profitable than a typical insurance company. That’s because the amount they pay in claims accounts for a far lower proportion of the money collected in premiums – all from other affiliates of the oil giants – than is the case at other insurers, Industry data shows. That means the captive insurance units absorb part of the revenue made by the oil majors’ subsidiaries elsewhere – often in high-tax countries where they extract oil and gas – and shift it to operations located in low-tax or no-tax jurisdictions.”

For tax justice connoisseurs, it’s another form of transfer pricing to shift profits into tax havens. But what is astonishing is how brazen this all is. Here’s an example from BP:

“In 2014, Jupiter had an operating ratio – which includes pay-outs and other costs as a share of premiums – of just 1.3%. That compares to more than 90% for most U.S. insurers.”