We recently published a special edition of Tax Justice Focus on national security, guest edited by Jack Blum, Charles Davidson and Ben Judah. You can read their editorial here. In the following article, Yakov Feygin from the Berggruen Institute, argues that the United States could and should use its central position in the global monetary system to tackle the related phenomena of tax avoidance and corruption.

The Financial Infrastructure of Corruption

Yakov Feygin

National security practitioners have become increasingly aware of the threat of ‘Kleptocratic regimes’ and ‘strategic corruption’ to the internal politics of liberal-democratic polities. In the classical version of this narrative, authoritarian regimes exploit global financial and business networks to penetrate the internal politics of democratic societies and secure their domestic rule by exploiting the self-interest of particular business groups.[1] Some have even suggested that foreign ‘dark money’ might enter the democratic process by supporting particular candidates.[2] The common thread that unites these views is that dark money is seen as a foreign policy problem and thus related to either extra-systemic actors or foreign competitors that exploit legitimate systems.

Viewing this issue as only the result of ‘corruption’ or as an aspect of power politics alone is flawed. The dangers highlighted above are not the result of aberrations in an otherwise functioning system that can be patched by some legal reforms. Rather they are a feature of how the international financial system has evolved to serve the world’s most powerful, whether they are kleptocrats in the developing world or reputable fortune 500 companies. The global financial infrastructure, as it has evolved in the post-war period, requires vast pools of offshore dollar accounts, so-called Eurodollars. This credit money, ‘issued at the book maker’s pen’ forms the basis for global payments and currency exchange.[3] Within these money pools, often held in tax havens with opaque ownership law, it is impossible to distinguish kleptocratic activity ‘threats’ from ‘legitimate tax optimization’ by multinational corporations and high net worth individuals. Moreover, without these wholesale money market ‘deposits,’ the global monetary system would find itself short of liquidity as even formal bank institutions are deeply intertwined with offshore finance.[4]

Instead of viewing these activities as national security threats created by the exploitation of a legitimate financing system by illegitimate actors, any attempt to curtail these activities must be done in the context of a radical reform of the global monetary order. This is not simply an academic distinction. If one sees kleptocracy as simply a form of corruption, the solutions presented are traditional anti-corruption measures focused on transparency and the strengthening of civil society. However, if we accept a systemic perspective that incorporates the centrality of offshore cash pools to the ‘dollar system,’ then we must take a broader perspective that calls for wholesale monetary reform and the mobilization of U.S. monetary power, specifically to move toward a ‘systemic’ reform of global capitalism itself.

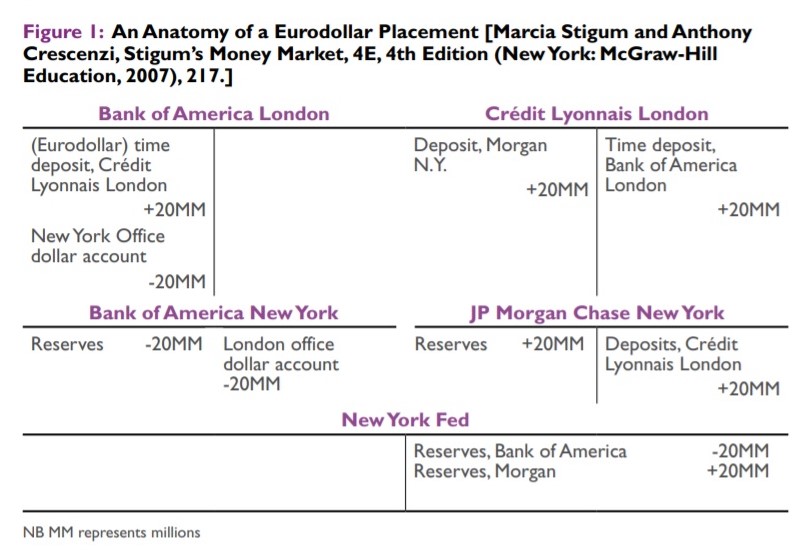

The formal definition of a ‘Eurodollar’ is a dollar deposit in a non-American domiciled banking institution. As such, Eurodollars are pure credit instruments. They have no formal backing at the United States Federal Reserve. That means that unlike onshore credit money, Eurodollars have no explicit guarantee for their par value. As such, Eurodollars are secured via a set of inter-bank funding agreements benchmarked by the London Interbank Overnight Rate (LIBOR). Eurodollar deposits emerge when non-American domiciled firms book a dollar inflow in non-American domiciled banks. These banks then ultimately lend these deposits to other financial institutions that require immediate dollar funding and expect a dollar-denominated inflow at some future period. The creation of a Eurodollar deposit is represented in Figure 1 through a set of stylized balance sheets.

Figure 1: An Anatomy of a Eurodollar Placement [Marcia Stigum and Anthony Crescenzi, Stigum’s Money Market, 4E, 4th Edition (New York: McGraw-Hill Education, 2007), 217.]

As we can see, Eurodollars are initially funded through an interbank transaction with a U.S. domiciled bank and its foreign branch. From the point of view of the onshore money system, no actual dollars have left the United States. However, credit has now been issued that can ultimately be multiplied many times over to create a system of dollar funding.

Moreover, the term Eurodollar is often used not only to describe the specific type of money market instrument described above, but also the larger global market for wholesale dollar funding. This market and its instruments—Money Market Fund Shares, Repurchase Agreements (Repos), and asset-backed commercial paper—form the backbone of the global ‘shadow banking system.’ One can think of shadow banking as the expansion of the category of banking beyond registered bank holding companies. There is a robust academic debate as to what counts for deposits within this system, but a general consensus is that the key to the shadow banking system’s operation are large institutional cash pools, often held in offshore banking jurisdictions.[5] These pools of Eurodollar deposits – essentially credit entries – require cash inflows to validate holdings. As such, an army of money managers has arisen to attempt to find returns for these large, global pools of cash.[6]

The Eurodollar system is thus ‘hybrid,’ insofar as dollar denomination depends on a state action—the U.S.-issued dollar—but is intermediated by and created through private credit. This is not an accidental arrangement but a set of political choices.[7] A popular legend holds that the offshore dollar market was created when the USSR, fearful of seizure, wanted to hold its dollar deposits outside of American banks. More realistically, the Eurodollar market seems to have arisen through intercorporate ‘swaps’ of currency liabilities designed to get around Bretton Woods-era capital controls. These swaps evolved into markets and eventually became the source of funding for offshore issued ‘Eurobonds.’[8] In the 1970s, as the Bretton Woods system began to collapse, regulators began to give up on efforts to coordinate to control this system and financial globalization was born.[9] More importantly, a whole industry of consultants, often with the encouragement of major governments, sprang up to offer newly decolonized states—often with common law systems—roadmaps to becoming offshore financial centers.[10]

The existence of shadow banking and wholesale Eurodollar financing makes it increasingly difficult to draw specific borders between national, and global financial systems and between legitimate transactions and kleptocratic activities and ‘strategic corruption.’ Disclosures of offshore structures such as the Panama Papers reveal a mix of both obviously political corruption and ‘normal’ corporate tax optimization. An anatomy of several transactions demonstrates just how similar and indistinguishable both activities are.

Take the ‘double Irish’ tax structure favored by pharmaceutical and technology companies. Company A in California develops a piece of software. It sells the patent for this software to a wholly-owned subsidiary in the Cayman Islands for one dollar. That subsidiary then revalues the patent to 100 dollars and pays no taxes on that re-evaluation. Next, the Cayman company ‘sells’ right to the patent to an Irish subsidiary of Company A, which markets and sells the software in Europe. The Irish company thus pays low taxes on European sales and renumerates its American parent through licensing fees, paid in dollars, to the Caymans subsidiary. Note that at this point, the Irish subsidiary has entered the Eurodollar market to transform its Euro receipts into dollar deposits and has then transferred those deposits to a bank in the Cayman Islands. This bank can now engage in Eurodollar funding with its dollar deposit. Meanwhile, the Cayman company can lend to the parent firm at a zero-interest rate to bring profits home or can purchase the parent firm’s assets. Taxes have been minimized with no violation of the law.[11]

Now, let us examine a ‘kleptocratic transaction’ that uses a similar set of channels. A politically exposed person (PEP) in Country A wishes to benefit from a privatization scheme of a state-owned company. To do this, the PEP sets up a company in Cyprus which has a tax treaty with Country A. The individual then swaps shares in the worthless Cyprus company owned by him and the valuable firm in Country A. Thus, the Country A firm’s profits are now captured, and it is effectively privatized. The firm in Cyprus then sells its shares, in dollars, to another firm owned by the PEP in the Cayman Islands, thereby eliminating any tax liability and creating a dollar deposit in the Cayman Islands. Again, these chains of firms have entered Eurodollar markets to both convert cash flows from Country A to dollars, and to then deposit these receipts. The PEP can now use his dollar deposit to purchase property in London or to make investments in an American PR campaign. Again, a dollar deposit is now created within the Caymans and, with the likely exception of laws in Country A being broken, nothing illegal has happened.

The parallels between ‘tax optimization’ and ‘corruption’ are so strong that the illegality of the latter is only present because in the United States, we have made tax optimization legal and acceptable de jure. Moreover, both of these schemes have created Eurodollar deposits that can then be lent and borrowed in the global dollar system to fund trade, investments, and capital goods that are completely unrelated to these transactions. The incentives for not tampering with this existing system are thus quite high.

The offshore financial system was created in the wake of the collapse of the Bretton Woods System as a means to avoid high-cost political decisions while allowing an increasingly globalized financial system to serve the needs of a global elite. While this elite was largely in line with the interest of the United States, the national security establishment has paid little attention to the misery that the offshore world has caused due to lost tax revenue, illegal privatization of public assets, and financial instability. Now, however, that these structures are not only used by multinational corporations but also by state-related actors that might threaten American sovereignty, the national security and foreign policy establishment has woken up.

The tools it has offered us to combat these problems are a mix of relatively effective measures to boost transparency and some half measures that at best will try to restrict access to the offshore world to legitimate actors. Indeed, beneficial ownership legislation, now being championed by many in Washington, will not only help American officials push foreign counterparts to adapt their own transparency legislation but give us better ideas about the American side of many transactions. However, there is an open question about whether this legislation alone will allow the United States to effectively deal with the holes of global sovereignty caused by the offshore world. Efforts to empower civil society in corrupt states are noble but will not address the root causes of what makes kleptocracy so simple: the easy movement of capital through offshore networks.

Most importantly, these policies do not take into account the fact that such transactions are critical to global dollar funding. If the United States is really serious about fighting offshore finance and kleptocracy, it has to put in some deep thought into what the outlines of a global financial system that replaces it would look like. At the original Bretton Woods Conference, John Maynard Keynes proposed a global clearinghouse system denominated in an international currency called Bancor. States would not actually use Bancor but would settle accounts in it.[12] States with persistent surpluses of Bancor would be charged a negative interest rate to encourage them to lend to states that needed funding. Capital controls would help contain private international finances.

It would be exceptionally hard for a New Bretton Woods to happen. However, we can simulate some of its features unilaterally and eliminate incentives for other countries to serve as nodes in the offshore system. A major reason that a country like the United Kingdom might want to be a tax shelter is to attract foreign exchange to its country and thus have sources of financing for development, as well as to sustain the value of its own currency relative to a global funding currency like the dollar. The United States has a tool to sustain the purchasing power of the UK’s currency: the central bank swap line. Swap lines came into public consciousness during the 2008 financial crisis, when the Fed allowed major central banks to exchange their local currencies for dollars to backstop Eurodollar deposits. During the COVID-19 crisis, larger swap interventions prevented a general, global economic collapse. The United States should consider giving countries with strong macroprudential policies, open trade practices, and, most importantly for this piece, transparent financial systems pre-approved access to Federal Reserve swap lines.

This would, of course, mean crowding out opportunities for private finance to intermediate global monetary transactions. However, if the United States is really serious about fighting global corruption, and treating it as a national security threat, the problem has to be cut out at its root. The centrality of private offshore banking and Eurodollar creation to global funding must be eliminated to counter global corruption, not only abroad but at home.

The United States, as the issuer of the world’s dominant currency, has a responsibility to sustain this ‘global public good’ in a manner that limits the ability of rentiers and oligarchs to exploit this public good. Without recapturing the role of global intermediation from private actors, we will never solve the problem of kleptocracy. A national security strategy that addresses these new threats must realize that the enemy is not a set of particular corrupt individuals, but the structure of global capitalism itself.

Yakov Feygin is Associate Director of the Future of Capitalism Program at the Berggruen Institute. This piece was first published in The American Interest on September 21, 2020.

[1] Ben Freeman, ‘America’s laws have always left it vulnerable to foreign influence’, Washington Post, October 19, 2019.

[2] Joseph Biden and Michael Carpenter, ‘Foreign dark money is threatening American democracy’, Politico, November 27, 2018

[3] Milton Friedman, ‘The Euro-Dollar Market: Some First Principles’, Federal Reserve Bank of St. Louis, September, 1971

[4] Iňaki Aldasoro, Wenqian and Esti Kemp, ‘Cross-border links between banks and non-bank financial institutions, BIS Quaterly Review, September 2020; Marco Cipriani and Julia Gouny, ‘The Eurodollar Market in the United States’, Liberty Street Economics, Federal Reserve Bank of New York, May 27, 2015

[5] Steffen Murau and Tobia Pforr, ‘Private Debt as Shadow Money: Conceptual Criteria, Empirical Evaluation and Implication for Financial Stability’, Private Debt Project, May, 2020

[6] Zoltan Poszar, ‘Shadow Banking: The Money View’, Office of Financial Research Working Paper, July 2, 2014; Daniela Gabor, ‘Critical macro-finance: A theoretical lens’, Finance and Society, 2020

[7] Daniela Gabor, op. cit.

[8] Perry Mehrling, The New Lombard Street, Princeton University Press, 2010

[9] Benjamin Braun, Arie Krampf, Steffen Murau, ‘Financial globalization as positive integration: monetary technocrats and the Eurodollar market in the 1970s’, Review of International Political Economy, March 22, 2020

[10] Vanessa Ogle, ‘Archipelago Capitalism: Tax Havens, Offshore Money, and the State’, The American Historical Review, December 2017

[11] Edward Helmore, ‘Google says it will no longer use “Double Irish, Dutch sandwich” tax loophole’, Guardian, January 1, 2020

[12] Luca Fantacci, ‘Why not bancor? Keynes’s currency as a solution to global imbalances’, unpublished draft, January 19, 2012

The author

Related articles

A heartfelt farewell to our dear Óscar

Public finance is feminist terrain

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

Fiscal hell or mirage? What Spain’s wage debate gets wrong

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

What we learned from three years of conversations on poverty beyond growth

Finally, the European Court of Justice cracks down on trusts

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026