You will shortly be redirected to the our UN tax convention live hub.

You will shortly be redirected to the our UN tax convention live hub.

Today the Tax Justice Network published two reports on real estate transparency. The first one, “Beneficial ownership of real estate around the world” summarises the findings of the Financial Secrecy Index on real estate transparency. It also it updates the report “Beneficial ownership registration around the world 2022” by assessing the state of play of beneficial ownership registration as of 2026, and checks which beneficial ownership laws trigger registration based on holding or acquiring real estate. The report identifies the frameworks and countries with the best real estate infrastructure (e.g. central, online real estate registries) and transparency (e.g. online, free and public access to information on real estate ownership). It also compares the results based on geographical region and membership to the OECD to explore the reasons that may explain why some countries are at the vanguard of real estate transparency, while others are lagging behind.

The second report “Integrating the Collection, Use and Exchange of Real Estate Ownership Information” explains the importance of beneficial ownership of real estate to tackle illicit financial flows. The report also explores all the potential sources of real estate information, considering the advantages and disadvantages of each one (e.g. the real estate registry, the tax administration, the financial intelligence unit, as well as banks, insurance companies, real estate brokers and public notaries subject to anti-money laundering requirements). On exchange of information, the report discusses the different frameworks for international exchanges (e.g. mutual legal assistance, sharing of financial intelligence and exchanges for tax purposes), illustrating how all new frameworks for automatic exchange of information (e.g. exchanges of information on immovable property, digital platforms, financial accounts and crypto-assets) could complement each other to offer information on foreign real estate held by nationals of each country. Finally, the report proposes how to integrate all this information into one platform to allow authorities as well as other stakeholders (e.g. investigative journalists, civil society organisations) to access and use this information to tackle financial crimes.

A brief summarising both reports is available here.

The tax justice movement awaits the publication of the first full draft of the UN Framework Convention on International Tax Cooperation (UNFCITC). It is expected within the coming days.

For those not intimately following the UN intergovernmental negotiations over the last two years, the Report of the High Level Panel on Illicit Financial Flows from Africa strikes at the core of why the status quo in international tax cooperation needs to change:

“The radical reduction of illicit capital outflows from [Africa], short of ending them, is precisely the outcome [Africa] and the rest of the world must achieve to produce this strategically critical new balance…

“As a Panel we are convinced that the goals of ending poverty in the world, reducing inequality within and among nations, and giving practical effect to the fundamental objective of the right of all to development remain vital pillars in the historic process to build a humane, peaceful and prosperous universal human society.”

(Chairperson Thabo Mbeki, p4 of the report)

Ahead of the fifth session of the intergovernmental negotiations to be held in New York, 3-13 August 2026, the draft text will be published in full. Many of the contentious issues are already clear from the previous sessions.

Some of the concepts under discussion are not yet clearly defined, and remain abstract yet are foundational for the successful implementation and operationalisation of the Convention’s principles and commitments. To help shed some light, in advance of the opportunity to comment upon and influence full draft text for the Convention and the two early Protocols, we wanted to support a nuanced understanding and discussion of these concepts. In a series of four webinars we brought together researchers, governmental negotiators and advocates to unpick some of the complexity and the implications.

To agree a common understanding of such issues opens up the space to create a high reaching and legitimate UN tax convention. This is surely what we need to change our world and to flourish!

You can find recordings of the first four webinars below. We plan to delve into to other topics later in the year.

Harmful Tax Practices – defining potentially unacceptable State behaviours.

Foreseeable Relevance – as a limiting criterion for the exchange of information between states.

Value Creation – as a potentially problematic basis for determining the location of companies’ real activity.

Illicit Financial Flows – an agreed component of the negotiations, with a formal UN statistical definition and potentially wide implications.

Background resources can be found here on our dedicated UN tax convention page

Debates about taxation are often shaped less by evidence than by politically convenient narratives. Across many countries, claims that taxes are the primary cause of low wages, weak growth or economic stagnation frequently gain traction despite limited empirical support. For those concerned with tax justice, the issue is not whether taxes should ever be criticised, but whether public debate is grounded in evidence rather than assumptions.

Spain offers a useful example. Arguments that employer social contributions are the main cause of stagnant wages have become increasingly prominent in political debate. Yet the available evidence suggests a more complex picture, raising broader questions about how tax policy is discussed and whether tax cuts are being presented as solutions to problems they may not actually address.

The only thing more disappointing than Spanish wages is the political debate surrounding them. According to the OECD, Spain’s real wages have grown just 5% since 1995, one of the lowest rates in the developed world. That figure deserves a serious diagnosis. Instead, like in many political arenas, opposition parties and outlets offer a comfortable narrative, statistically questionable and with solutions that would resolve nothing except the political problem of having to talk about the real economy.

The Spanish debate illustrates how discussions about taxation can become detached from the available evidence. Rather than focusing on the structural causes of wage stagnation, it increasingly seeks to blame unsatisfactory salaries on the burdens corporations must pay to fund increasingly skimpy welfare states. At least in Spain’s case, however, the data does not support that narrative, and there is little reason to believe that lower payroll taxes would deliver the wage growth their advocates promise.

Source: Own elaboration based on OECD data

In Spain, the “tax hell” discourse isn’t new, but it’s taken on a fresh form. Faced with the evidence that Spain’s personal income tax isn’t particularly high compared to its peers, its proponents have shifted the argument toward employer social contributions, in the form of payroll taxes.

They state that a Spanish employer pays approximately 30% on top of gross wages in Social Security contributions; once you add what the worker pays, you arrive at a total burden that supposedly turns Spain into a disguised tax hell. The following chart has been circulating for months, republished by outlets and commentators of a libertarian and conservative bent.

Source: Own elaboration based on OECD data

In the table, you can indeed observe that Spain has above-average payroll tax contributions on behalf of employers, which contribute to pensions and unemployment benefits and are known in Spain as social security contributions. Those parties and outlets who wish to lessen Spain’s already below-average tax-to-GDP ratio have seized on this data point.

Leader of the center-right opposition People’s Party (PP), Alberto Núñez Feijóo, summarised the argument recently: “Spain collects like a Nordic country but can’t have services like a third-world country.” Far-right Vox’s MP José María Figaredo went further, claiming that “the average worker has the state take roughly 50% of their work every year”, a figure constructed by counting employer contributions as wages stolen from the worker. Vox’s parliamentary spokesperson at the time, Iván Espinosa de los Monteros, drew a similar conclusion: the way to “raise wages” isn’t to increase the minimum wage, but to cut contributions and taxes. The cause behind low wages is supposedly well-known and easy to cure. But both the diagnosis and the cure might be mistaken.

According to Eurostat, Spain’s total tax take, taxes and contributions combined, represented 37.3% of GDP in 2023, below the EU average of 40.4%. France sits at 46.1%, Belgium at 44.8%, Austria at 43.1%, Italy at 42.4%. If Spain is a tax hell, most of Western Europe has been burning at a much higher temperature for decades.

Admittedly, social contributions represent 34.1% of Spain’s total revenue, against an OECD average of 24.8%. But Spanish companies offset that higher contribution burden with a corporate tax whose effective average rate, after deductions, depreciation, and special regimes, sits among the lowest in Western Europe. Social contributions aren’t an additional tax on businesses; they’re compensating for a corporate income tax whose effective rate, at 15.4% in 2023, sits well below the OECD average of 20.2%. Changing the label doesn’t change the bill.

You could argue that even if contributions function as an alternative business tax, cutting them would still create room to raise net wages. This trickle-down argument has permeated public discussions for decades. In Spain, that simple logic only holds up until you look at what actually happened.

In 1997, under José María Aznar’s PP government, the labour reform cut employer contributions by between 40% and 90% for permanent contracts targeting workers under 30 and over 45. Columbia University economist Ferrán Elías analysed the real effect using Social Security administrative data on more than one million workers. His conclusion was that the reduction generated a modest employment effect among workers under 30, a 2.42% increase in hirings, but wages didn’t move. For workers over 45, not even that. The tax cut translated into a transfer to companies, funded by taxpayers.

The academic research group Equalitas, studying the same reform, found that the slight wage improvement observed in that period came from the simultaneous reduction in dismissal costs, not the contribution cut. Their phrasing is direct: “with a weak link between contributions and benefits, payroll taxes are not fully passed on to employees, and employment falls.”

Additionally, the most exhaustive review of the literature for Spain, by Ángel Melguizo in Hacienda Pública Española, reaches the same wall: “results are not robust, ranging from full pass-through to zero pass-through.” The outcome depends on collective bargaining structure. In Spain, sectoral agreements set wage floors for the vast majority of private sector workers regardless of what a company contributes. Hence, the tax saving simply doesn’t reach the worker’s pocket.

Spain’s economy is overly concentrated in tourism, hospitality, and construction, sectors of low productivity and modest pay, with chronically insufficient investment in R&D and a dual labour market that weakens workers’ bargaining power. According to BBVA Research, the gap between productivity and wages, not fiscal pressure, is the central explanation for Spain’s wage stagnation. Cutting contributions doesn’t build a manufacturing industry, generate patents, or improve vocational training. It’s like trying to modernise the country by changing the ministry’s logo.

Furthermore, anti-fiscal rhetoric against left-of-centre administrations cools fast upon reaching office. In Italy, with a fiscal burden of 42.4% of GDP, Giorgia Meloni arrived promising a tax revolution. The headline achievement of her 2026 budget was an income tax cut that returned €408 per year to executives, €123 to office workers, and €23 to manual workers. Less a revolution, more finding a twenty-euro note in an old coat pocket.

The Spanish precedent is more direct. Few prime ministers have captured the gap between rhetoric and reality with such inadvertent honesty as former Spanish Prime Minister Mariano Rajoy, “I said I was going to cut taxes and I am raising them.” His government raised standard VAT from 18% to 21%, the reduced rate from 8% to 10%, and income tax rates by up to seven points, the largest tax increase in Spanish democracy according to the Ministry of Finance itself. Unfortunately, this was part of an austerity drive more concerned with maintaining the creditworthiness of Spanish bonds than with redistributing and reinvesting Spanish wealth.

Undoubtedly, the Spanish tax system is improvable, and Spanish net wages are poor relative to European neighbors. The failure to deflate income tax brackets has had a real negative effect on middle and lower earners, and there are VAT categories worth revising. There’s a serious fiscal conversation to be had. But that’s not what’s currently on air.

If PP or Vox reached government and cut employer contributions, the evidence gives no reason to expect higher wages. The most likely result is a larger public deficit and better margins for Ibex companies that just closed their best year since 1993, up 49% and at historic highs, without any of that pulling wages up with them. Low wages are the product of an economy that hasn’t modernised its productive structure in decades. That’s the debate Spaniards deserve to have.

Editor’s note: Public debates about taxation are often shaped as much by political narratives as by evidence. In this guest article, Nicolas Brennan Hernandez, an economist specialising in international trade and political economy, examines the current debate on wages and taxation in Spain, arguing that tax policy discussions should be grounded in empirical evidence rather than misleading rhetoric. The views expressed are those of the author.

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

Since 2009, the Tax Justice Network has published the Financial Secrecy Index. This is a ranking of jurisdictions around the world, based on a thorough assessment of financial transparency and relevant areas of international cooperation. By combining the overall secrecy score with a global scale weight, the ranking reflects the share of global financial secrecy risk that each jurisdiction poses.

The Financial Secrecy Index is now widely used and trusted by organisations across the world, for research, policy analysis, criminal investigations and to carry out geographic risk assessment for anti-money laundering purposes. Those who use, cite and/or recommend the index include multiple UN bodies, the International Monetary Fund, World Bank, OECD, the European Commission, the FBI and the broader ‘Five Eyes’ intelligence alliance, along with a growing number of financial institutions.

A key insight of the Financial Secrecy Index is that the analysis is not binary. It is unhelpful to try to identify a set of jurisdictions that are bad (to be labelled ‘tax havens’, perhaps, or ‘non-cooperative jurisdictions’), while all others are by default deemed to be good. Instead, according to the Tax Justice Network, there is a spectrum of financial secrecy, by which all jurisdictions have a secrecy score substantially higher than zero (which would indicate perfect transparency and cooperation). All jurisdictions can make progress, and reduce the damage they cause worldwide. But some have greater responsibility than others.

The second insight is that the main global threats are not the small islands fringed with palm trees that remain a media trope for thinking about tax havens. When jurisdictions are assessed objectively on the basis of robust, verifiable criteria, it turns out that the greatest global risks by far are attributable to some of the major financial centres.

The United States has ranked first and worst since 2022. In the latest update to the Financial Secrecy Index, that position is only confirmed. With the Trump administration having pushed back against key areas of progress initiated under its predecessor, the US continues to pose the greatest threat to the rest of the world by facilitating crossborder tax abuse and the laundering of the proceeds of corruption and other crime.

Rather than update every component of the Financial Secrecy Index in a single revision every two years, we have recently adopted rolling updates. This allows us to keep the Index relatively fresh, while focusing each update on particular variables. The 2026 update addresses the indicators of so-called ‘golden visas’, by which jurisdictions sell citizenship and/or residency programs with no requirement for a minimum physical presence in the country and exacerbate risks of financial crime; and the transparency of real estate ownership.

The ease with which high-value property can be acquired and transferred makes real estate a prime asset for those seeking to park illicit gains. As such, effective transparency of the beneficial owners is a critical measure to protect the jurisdiction where the property is located, whose markets can become heavily distorted as they are also increasingly home to corrupt funds. This transparency is also important to protect those jurisdictions from which the dirty money funding the acquisition flows.

The real estate ownership transparency assessment in the Financial Secrecy Index is constructed to reflect the general availability of ownership data for immoveable property in each jurisdiction, as well as the ability of foreign companies and other legal vehicles such as trusts to hold local property while keeping the ultimate beneficial owners anonymous. The resulting score ranges from 0 to 100.

Jurisdictions scoring zero, for perfect transparency in this area include Denmark, Slovenia and Luxembourg. The latter might seem surprising, given Luxembourg’s longstanding role in financial secrecy provision more broadly. However, the jurisdiction has shown a greater willingness to address transparency concerns when they affect its own scant area than when they arise in its wider offshore financial sector, which continues to facilitate anonymous ownership of financial assets and income streams.

Most jurisdictions have intermediate scores – from Spain (25), China (40) and Norway (45) at the lower end, to Germany (55), Qatar (70) and the UK (both 80).

The perfect failure, a score of one hundred, is obtained by a small but significant group of countries – significant because they include some of the biggest real estate markets in the world like Canada, Australia, and Mexico.

Alongside the 2026 update of the Financial Secrecy Index, we have constructed a separate Real Estate Secrecy Index, which follows the methodology of the overall Financial Secrecy Index. This combines the secrecy score with a measure of global scale, in a cubic/cubed root formula to balance the components. Here we use the specific secrecy score of the real estate ownership indicator, and combine it with a measure of the market size for commercial real estate in each jurisdiction.

| Country | Commercial real estate market, $bn | Real estate secrecy score (SI06) | RESI value | RESI rank |

| United States | 12440.77 | 100 | 678,425 | 1 |

| Canada | 985.4 | 100 | 291,356 | 2 |

| Australia | 788.2 | 100 | 270,457 | 3 |

| India | 687.75 | 100 | 258,442 | 4 |

| Mexico | 558.86 | 100 | 241,168 | 5 |

| Indonesia | 312.98 | 100 | 198,789 | 6 |

| United Arab Emirates | 235.01 | 100 | 180,682 | 7 |

| United Kingdom | 1533.91 | 80 | 172,884 | 8 |

| Italy | 1025.83 | 80 | 151,187 | 9 |

| Malaysia | 128.86 | 100 | 147,885 | 10 |

| Switzerland | 400.9 | 80 | 110,535 | 11 |

| Saudi Arabia | 536.73 | 70 | 81,614 | 12 |

| Sri Lanka | 19.57 | 100 | 78,901 | 13 |

| Turkiye | 394.72 | 70 | 73,668 | 14 |

| Chile | 112.01 | 80 | 72,262 | 15 |

As the table of the top 15 jurisdictions shows, the worst actor in terms of the global risks posed through real estate secrecy is the same as for overall financial secrecy: the United States.

The other worst-ranked jurisdictions include some with large markets but somewhat better transparency (eg the UK and Italy), and a number with much smaller markets but perfect failure scores for secrecy, such as the United Arab Emirates (UAE). Not shown are the many jurisdictions with much larger markets than the UAE, but much stronger transparency that rank far down the index, including China, France, Germany, Japan and South Korea.

The UK has rescheduled its Illicit Financial Flows summit for December 2026. One component of the summit is intended to address the transparency of real estate ownership, and it is understood that discussions continue with invited jurisdictions. Meanwhile the UK government’s Anti-Corruption Champion (and long-time opponent of financial secrecy), Baroness Margaret Hodge, is working on a broad analysis of ownership transparency that is expected to make key recommendations in the coming months.

The opportunity is clear, to set a new standard and lead a global shift away from secrecy in some of the world’s largest real estate markets. With political commitment, the UK can advance into its summit with policies in place to reach the gold standard of transparency, and credibly encourage a range of participants to do likewise.

Many countries in the global South outperform major OECD countries. The OECD’s 2025 standard on exchange of immoveable property information will commence its first exchange in 2029 but so far has fewer than 30 members. With no loss of time, an obvious alternative would be to support a globally inclusive instrument to be developed as part of the ongoing negotiations on the UN Framework Convention on International Tax Cooperation.

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

In a world where we push people crossing seas in small boats back into dangerous open water and build ever higher walls to keep out people who seek a better life, the commodification of citizenship and residency and the selling of golden visas to the richest raises serious moral concerns. The Golden Visas indicator of the Financial Secrecy Index shows that the practice of investment immigration also raises serious financial secrecy concerns.

The ‘Golden Visas’ indicator assesses the financial secrecy risk posed by investment immigration by scoring countries on two separate components: how strict or lax their rules on citizenship and residency are (based on whether they offer golden visa programmes), and the comprehensiveness of their personal income tax regime. Given that the interaction of the two components can trigger additional secrecy risks, countries are also scored on the combination of scores they get on the two components.

So, if a country scores badly on the first component and badly on the second component, it gets additionally penalised in its total score for the indicator. That’s because the risk of an individual pretending to be resident in another country just to underpay personal income tax someplace increases if said country has both weak citizenship and residency rules and weak personal income tax rules.

Golden visa programmes can create significant financial secrecy risks by providing opportunities for money laundering, tax evasion and the circumvention of transparency measures.

Below, we provide more details on the indicator’s components and on the results of our most recent assessment of the 141 jurisdictions covered by the Financial Secrecy Index.

Strict or lax citizenship/residence rules

One of the aspects assessed under the Golden Visas indicator is whether countries have strict or lax citizenship or residency rules based on any available citizenship by investment (CBI) or residency by investment (RBI) programmes. These programmes grant citizenship or residency if the applicant makes a passive investment in the country (eg in purchasing local real estate, shares in local companies, or bank deposits or donations). We consider these rules to be lax and pose risks if they do not require sufficient physical presence.

Citizenship or residence by investment programmes without the requirement of sufficient physical presence are known to provide a range of opportunities to hide assets, mask suspicious high-value transactions or enable the movement of significant sums of illicit funds across the borders. These risks are well documented, including by the OECD and the FATF in their recent publication on ‘Misuse of Citizenship and Residency by Investment’.

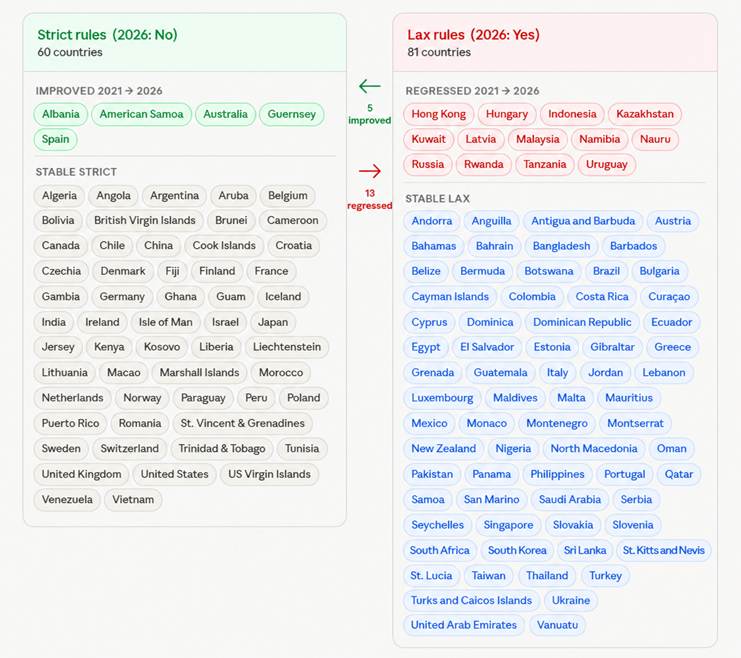

Our findings show that the number of jurisdictions assessed as having lax citizenship or residency rules increased from 73 out of 141 jurisdictions in 2021 to 81 jurisdictions in 2026.

Worryingly, among those countries having regressed into the adoption of lax citizenship/residency rules are a significant number of Global South countries. Countries like Namibia, Nauru and Rwanda have historically stayed clear of polices that score negatively on the Financial Secrecy Index, consistently landing them in the bottom half of the index’s ranking. The regression on citizenship/residency rules is out of character for the countries financial secrecy risk profiles.

Countries often adopted lax citizenship/residency rules under the impression that doing so has the potential to boost domestic resource mobilization through investment migration. It is not disputed that there is money to be made by countries in the sale of golden visas. Citizenship by investment passport sales in Dominica, for example, are reported to have accounted for up to one third of the country’s gross domestic product in recent years. However, as noted by the IMF in a recent study, countries should be wary about expecting similar revenue windfalls based on anecdotal evidence. The authors conclude that for most countries, the likely effects of golden visa programmes may not be beneficial and might be outright harmful. A recent study by the United Nations details how criminal groups in Southeast Asia are increasingly targeting citizenship by investment schemes in the region to circumvent law enforcement.

Comprehensive personal income tax (and the lack thereof)

For a personal income tax to be comprehensive in its scope, it needs to apply the same tax base rules – a rate above zero per cent – equally to all natural persons considered tax residents, including all income from any sources across the world. Any opt-out from the general tax regime in a certain jurisdiction (eg lump sum taxation, tax exemption on foreign-sourced income, territorial tax base or taxes on a remittance basis) results in the jurisdiction being considered by the indicator to not have a comprehensive personal income tax. It can also be the case that the country does not even levy a personal income tax.

The number of jurisdictions without a personal income tax is 17, 15 of which offer golden visa programmes. This combination of components presents a significant problem to automatic exchange of information, as will be explained below.

Avoiding the Common Reporting Standard (CRS) and Crypto Asset Reporting Standard (CARF)

Since the inception of the Common Reporting Standard (CRS) in 2014, the Tax Justice Network has consistently warned that the combination of citizenship and residency by investment regimes and low or no personal income tax in a country creates a specific risk for abusive behaviour, namely Common Reporting Standard avoidance. With the Crypto Asset Reporting Standard (CARF) coming into for this year, this risk of avoidance now also extends to the new standard.

Avoidance of reporting under either standard can take place if the owner of a financial account or crypto wallet in Country A obtains a golden visa in Country B and uses their new passport to record Country B as their country of residence for reporting purposes under the standards. Country B will receive the automatically exchanged information on taxable income and assets. If Country B does not levy income tax on the offshore income and assets, the information is exchanged but not used. At the same time, Country A, the genuine residence country, will be left in the dark regarding its resident’s foreign finances.

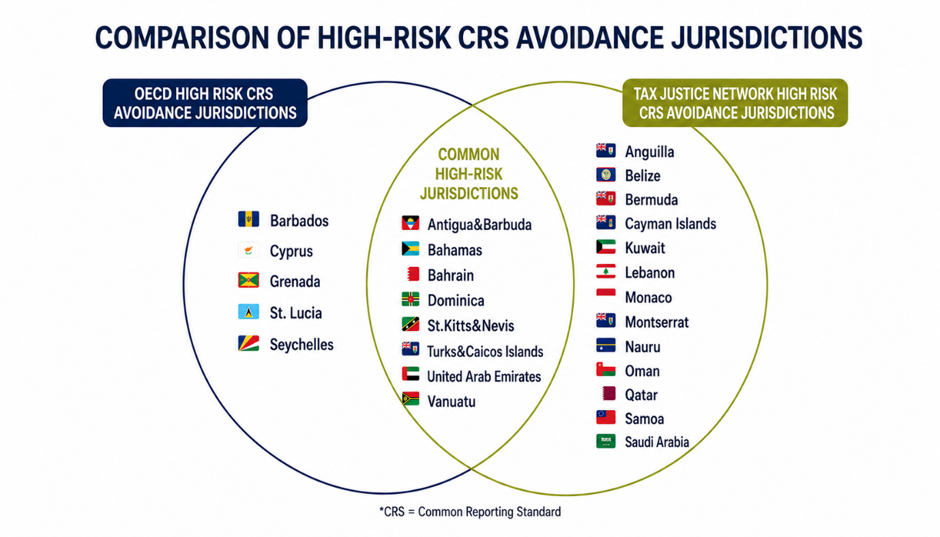

The OECD, aware of the abovementioned risk, keeps as of 2018 an updated list with jurisdictions that operated citizenship and residence by investment schemes that can potentially be abused for to avoid reporting under the Common Reporting Standard. Jurisdictions are listed if they give a taxpayer access to a low personal income tax rate of less than 10% on offshore financial assets and do not require significant physical presence of at least 90 days in the jurisdiction offering the citizenship and residence by investment scheme (see OECD FAQ). Based on this methodology, 13 jurisdictions are currently listed.

The Golden Visa indicator casts a different and wider approach to identify jurisdictions that pose a high-risk of Common Reporting Standard avoidance. Under the indicator, high-risk jurisdictions are those that have a citizenship and residence by investment scheme that does not require 183-day physical presence, and have either a complete absence of personal income tax or active choose ‘voluntary secrecy’ under the Common Reporting Standard. As explained in detail in the indicator on automatic exchange of information, voluntary secrecy jurisdictions participate in the Common Reporting Standard but have actively opted out of receiving information from other jurisdictions on their residents’ offshore accounts.

As a result, the indicator identifies a larger and different group of jurisdictions that potentially pose a high risk to the integrity of the Common Reporting Standard than the group of jurisdictions listed by the OECD. This larger group of high-risk jurisdictions consists of the jurisdictions that score a maximum secrecy score on the indicator.

It also means that certain jurisdictions listed by the OECD as high-risk are not considered to be high-risk (or highest-risk) by the Financial Secrecy Index and vice versa. Monaco, for example, is considered a high-risk jurisdiction under our indicator because it has no personal income tax and a golden visa regime that requires only 90 days of presence. These 90 days are sufficient for the OECD to consider Monaco non-risky. The opposite is true for Cyprus. Cyprus has a problematic golden visa regime earning it a high-risk grading by the OECD, but because it has a personal income tax (albeit with important exemptions), the indicator qualifies it as less risky.

In total, we have identified 21 jurisdictions that pose a high-risk for avoiding the Common Reporting Standard. New additions on the list of high-risk citizenship and residence by investment regimes are Kuwait and Nauru. Both countries are exercising voluntary secrecy under the Common Reporting Standard, and have recently jumped on the citizenship by investment (Nauru) and residency by investment (Kuwait) bandwagons.

Conclusion

Investment migration and especially the role played therein by golden visas is a controversial topic, as their issuance does not equate physical relocation of individuals. It usually means applicants obtain a secondary place of residency or citizenship, with the associated risk that the golden visa will be abused for nefarious purposes, like money laundering and tax evasion.

The new data under the indicator reveals two things. First, the number of jurisdictions with ‘lax’ citizenship/residency rules remains high. A number of countries have abolished their questionable citizenship and residence by investment regimes, whereas a slightly bigger number have introduced new ones. Another worrying trend is that these newcomers include Global South countries not generally known to be financial secrecy hotspots. Domestic resource mobilization through citizenship and residence by investment is not a good idea, however.

Meanwhile, countries have also not been addressed gaps in their personal income tax systems over the past five years. There is no significant change in the number of countries whose personal income tax systems are not comprehensive or who do no tax income altogether.

Second, the total of countries with lax citizenship/residency rules combined with the absence of personal income tax or the choice for voluntary secrecy under the Common Reporting Standard also remains high at 21 jurisdictions. The indicator shows that the financial secrecy risk caused by citizenship and residence by investment is of a wider scale than that estimated by the OECD and remains as problematic as ever. For money launderers and tax evaders, the buying of a golden visa remains one of the main ways to obtain financial secrecy.

We therefore advise: visa-selling countries beware (and reconsider)!

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

There is weaponisation of privacy, and then there are cases that take it a step further. One thing is to close “public” access to information, as the infamous ruling of the European Court of Justice did to beneficial ownership information in 2022. But restricting routine access to information by tax authorities is another matter entirely. The European Court of Justice also did this in 2024, when it prevented Luxembourg tax authorities from accessing information held by a law firm to respond to a request from Spain. In that case at least, legal professional privilege (a sharp double-edged sword against privacy) was also at play. Now, the European Court of Human Rights (ECHR) has taken a similar approach. In the ruling Ferrieri and Bonassisa v. Italy of May 2026, it prevented Italian tax authorities from accessing local banking data on Italian taxpayers because it breached the right to privacy.

Again, the tax authority didn’t want to access medical records, WhatsApp messages or personal photos. Italian tax authorities only sought information from banks including bank account details, transaction histories, and details of other financial operations.

Importantly, the ECHR ruling also notes that, based on domestic regulations, these access powers are not a blank check, but based on objective criteria, mainly upon any indication of tax evasion or high-risk transactions:

“the Tax Authority established criteria for selecting taxpayers and investigation methods in relation to checks on income tax and value-added tax. In respect of the criteria for carrying out tax audits of banking data, the relevant part of the circular read as follows:

‘Tax audits of banking data will, in particular, be carried out in respect of

- total or near-total tax evaders;

- persons with no accounting records or with accounting records that are obviously unreliable;

- persons carrying out import-export transactions;

- persons who have issued and/or used invoices for non-existent transactions; [and]

- persons whose financial capacity is clearly in stark contrast to the[ir] declared income.”

The ruling also described that Italian regulations require requests to be substantiated before tax directors can authorise them, and that these directors must check that those conditions are met:

“Circular no. 131/1994 further stated that tax offices asking for authorisation to carry out tax audits of banking data “[had to] sufficiently substantiate requests for authorisation to the regional directorates, in order to provide them with useful elements of evaluation”. In particular, a request had to indicate the following elements:

“- the data aimed at identifying the taxpayer;

- the reasons for undertaking the inquiry;

- the elements aimed at assessing the fiscal situation of the taxpayer;

- the reasons for considering that a tax audit of banking data would be useful in respect of the tax inquiry;

- the time period in respect of which the tax audit of banking data should be carried out;

- the banks … to which the request should be submitted …;”

Circular no. 131/1994 clarified that, on the basis of that information, the regional directorates had to check the formal and substantial legality (controllo sia di legittimità che di merito) of the request before issuing the requested authorisation.

The ruling’s description of Italian circulars also suggests that Italian tax authorities do not seem too eager to access banking data, because doing so involves more time and resources to finish the audit. For that reason, directors should only authorise such requests where the likely benefits justify the costs:

As regards a decision to carry out a tax audit of banking data, the circular further stated that the domestic authorities had to undertake a cost‑benefit analysis:

“It must be stressed that tax audits of banking data should be initiated in cases [where] the fruitfulness of the tax audit [in question] has been assessed. So, on the basis of common experience, the ‘costs’ of the tax audit (represented by the inevitable extension of the inquiry in terms of time and the complexity of the analysis of the accounts) must be weighed against the relative ‘benefits’ of an evidential nature, relating to the presumed size of the recoverable taxable amounts. The principle of economy of action (in terms of cost-benefit) must, moreover, strongly guide all the tax audit activity of the offices.”

And again:

“With specific regard to … financial investigations, it is reiterated that [they] must be used only after carefully assessing the risk of significant discrepancies in [a] tax declaration (significative anomalie dichiarative), and ideally only when the tax office has already instituted a tax inquiry.”

Taken together, these provisions suggest that Italian tax authorities are not particularly inclined to obtain banking information unless it offers substantive benefits compared to the costs involved.

However, the ruling focused on another issue. The ECHR ruling cited an Italian court decision suggesting that the final authorisation (likely from a director of a tax office) to request information from a bank did not need to be reasoned. In the court’s view, this gave the authorities unfettered discretion and made the measure incompatible with the right to privacy:

27. In judgment no. 8849 of 30 April 2015, the Court of Cassation observed that authorisation did not have to contain reasons, as no such requirement had been imposed under the applicable domestic provisions. The court held that such authorisation was merely an internal administrative act which could not be challenged by the bank that had been asked to provide the information, and the taxpayer concerned did not have to be notified of it. Since the authorisation could not be challenged, in the Court of Cassation’s view, it did not need to include any kind of reasoning.

…

81. The Court is prepared to accept that the clear and detailed criteria laid down in the circulars adopted and published by the Tax Authority [mentioned in the quotes above] might be sufficient to complement the applicable domestic provisions and delimit the scope of discretion conferred on the domestic authorities, provided that they are binding on the authorities.

However, this does not appear to be the case. In particular, the Court cannot but note that in the light of the Court of Cassation’s case‑law, authorisation does not have to contain reasoning (see paragraph 27 above). It follows that the authorities are not required to justify the exercise of their powers by giving reasons for their decisions and thereby showing that they are following the criteria laid down in the relevant domestic provisions, including the administrative circulars, resulting in them exercising unfettered discretion (see Bernh Larsen Holding AS and Others, cited above, § 130).

82. In the light of the above, the Court considers that the legal basis for the contested measures was incapable of sufficiently delimiting the scope of discretion conferred on the domestic authorities, and accordingly did not meet the “quality-of-law” requirement under Article 8 of the Convention.” (emphasis added).

Let’s recap. Tax authorities in all cases struggle to detect tax evasion. Tax evasion is not a binary issue. It’s not like mining for gold and you either find something yellow and shiny or you don’t. Tax evasion is determined after looking at what the taxpayer declared, the risk of transactions, and many other factors. Even then, it can only be confirmed after getting access to additional documentation (e.g. banking data) to verify the taxpayer’s declarations.

Even then, Italian tax authorities do not seem too eager about banking data. In addition to taxpayer rights’ concerns, Italian tax authorities’ circulars suggest that accessing banking information is mostly discouraged in the tax administrations’ own interest. It should not be done on a routine basis but only after a cost-benefit analysis because of the extra resources and time it will demand. For this reason, the tax auditor should provide reasons why access to banking data is necessary before the tax office director will authorise it. Once the director authorises it, however, the authorisation does not add to or explain the reasoning behind the request when asking the bank to provide the information (luckily, as the bank then tells its clients, as in this ruling). So, because this final authorisation does not require reasoning or justification, the ECHR found it to be discretionary and thus lacking a sufficient legal basis to justify interference with the right to privacy enshrined in Article 8 of the Convention for the Protection of Human Rights and Fundamental Freedoms.

We could be more sympathetic to the case if the tax authorities seemed to be exceeding their need for data, or going after political opponents or vulnerable populations. However, based on the limited information available in this case (the ruling also anonymises the full names of the taxpayers), it appears that they are ordinary taxpayers and that the tax authority only sought routine banking information.

While Italian law could perhaps be drafted more effectively, supranational courts need to understand the crippling effect of their rulings, especially at a time when inequality is soaring, tax authorities are being diminished (including in Italy), and tax transparency is being challenged on privacy, data protection and taxpayers’ rights grounds. After the European Court of Justice ruling of 2022, many European countries closed their beneficial ownership registries, including secrecy jurisdictions where the ruling was not even binding. The weaponisation of privacy, whether through court rulings or concerns about the EU’s General Data Protection Regulation (GDPR), can also result in self-censorship. A report by Transparency International described the challenges of investigating grand corruption when it comes to privacy:

“Privacy concerns compound the problem. Across EU member states, enforcement authorities have pointed to data protection rules, particularly the General Data Protection Regulation, as a major obstacle. Unclear or overly strict interpretations have fostered a climate of caution among data providers, who fear heavy fines for non-compliance. This has created a legal paradox: investigators need access to ownership and financial data to substantiate suspicion but cannot access that data until suspicion already exists.” (emphasis added)

In other words, this ruling is a new bump in the road in the fight against tax evasion and illicit financial flows, especially considering that the road is already in poor shape. Although this case dealt with access to information for domestic tax purposes, there have also been lawsuits seeking to stop the exchange of information for tax purposes.

If this weaponisation of privacy or abuse of taxpayers’ rights continues, it may not be long before new lawsuits or rulings begin requiring suspicion of tax evasion or the existence of a tax audit in order to narrow the scope of automatic exchange of information. Currently, automatic exchanges such as the OECD’s Common Reporting Standard and the Crypto-Asset Reporting Framework are useful precisely because they apply to all taxpayers. One could also imagine attempts to narrow access by tax authorities to domestic data based on conditions that apply to exchange of information on request, such as the “foreseeable relevance” requirement.

To address these secrecy risks, a UN Tax Convention may help strengthen tax transparency, particularly on access to and exchange of information, and counter the weaponisation of privacy. Countries in the Global South may also offer useful alternatives to current European approaches to privacy, data protection and tax transparency. For instance, in Argentina the tax authority routinely has access to bank account and credit card information on taxpayers above a relatively low threshold. Better examples need to be identified to counter the weaponisation of privacy in Europe.

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

We’re pleased to share this blog from the Tax Justice Network chair Lyla Latif (Pan-African lawyer, academic, and policy strategist) on how domestic work platforms are replicating colonial labour exclusions in digital form. As Lyla writes: “This is not simply an administrative inefficiency. It is a form of structural injustice with fiscal mechanisms.” You can read the original blog here in The Elephant which provides African analysis, opinion and investigation. The image is Lucy Nyangasi, domestic worker, Kenya by Solidarity Center, licensed under CC BY 2.0.

There is a woman who crosses Johannesburg before dawn. She takes two taxis, changes in Bree Street, and arrives at a house in Sandton by seven. She will spend eight hours cleaning floors, scrubbing bathrooms, washing laundry, and caring for children who are not her own. She booked this job through an app on her phone, a platform that promises convenience to homeowners and flexibility to workers. By six that evening, she will be on her way home, exhausted, with R250 deposited into her bank account and nothing else to show for her labour. No Unemployment Insurance Fund contribution. No Compensation for Occupational Injuries and Diseases coverage. No formal tax record that would make her visible to the state as a worker deserving of protection. She is economically active, socially essential, and fiscally invisible.

This is the situation of hundreds of thousands of women working through domestic service platforms across Africa. SweepSouth, the largest such platform in South Africa, has over 1.2 million domestic cleaners registered on its app. The company’s own annual reports document that 92 per cent of these workers are women, the vast majority are Black, and 83 per cent are the sole financial providers for their families, and they are supporting an average of four dependents each. They are, in the language of economics, essential workers. In the language of the fiscal system, they do not exist.

To understand why this matters, one must go further back than the app, further back even than the post-apartheid constitutional settlement. The exclusion of domestic workers from labour and fiscal protection in South Africa was never accidental, it was a design feature of a colonial labour economy that needed Black women’s reproductive and care labour to be cheap, abundant, and invisible. The Natives (Urban Areas) Act of 1923, the Women’s Enfranchisement Act of 1930, and successive pass laws constructed a legal architecture in which Black women moved through cities as necessary to service white domestic life but were denied the civic status that would have made that service legally cognizable as work. They could not vote. They could not own urban property. They were excluded from the Unemployment Insurance Act of 1946 and from the Workmen’s Compensation Act of the same year on precisely the grounds that domestic service was not “real” employment within the meaning of those statutes. These were not neutral administrative decisions. They were the fiscal expression of a racial political economy that required the extraction of labour without the obligations of reciprocity.

The post-apartheid settlement has progressively extended formal protections to domestic workers through the Basic Conditions of Employment Act in 1997, the extension of Unemployment Insurance Fund coverage in 2002, the landmark Constitutional Court ruling in Mahlangu v Minister of Labour in 2021, which finally extended Compensation for Occupational Injuries and Diseases Act coverage to the domestic sector after a decades-long legal battle. Each of these victories was hard won and significant. Yet each has also been partial, operating at the margins of a fiscal and labour architecture that was built around the formal male waged worker as its normative subject. The platform model did not create this problem. It inherited it, systematized it, and gave it a new interface.

The promise of platform work was supposed to be different. The app would bring work to your fingertips. No more walking from house to house looking for “piece jobs”. No more uncertainty about whether you would earn anything today. The algorithm would match you with clients, the platform would handle payment, and everything would be documented, transparent, modern. Yet what has actually happened is something more troubling: the formalization of informality, the digitization of invisibility. The problem is not that these women are unregistered with the tax authority. Many of them are. The problem is that the entire fiscal architecture of the South African state was built around a model of the formal employee, someone who has an employer who deducts taxes at source, contributes to the Unemployment Insurance Fund, registers the worker with the Compensation Fund, and generates the documentary record of economic participation that makes a person legible to state institutions. The platform model deliberately avoids triggering any of these obligations by classifying workers as “independent contractors” rather than employees.

This classification is a legal fiction that merits examination under any honest application of the common law tests of employment. SweepSouth sets the prices. SweepSouth allocates the bookings. SweepSouth rates the workers and removes those whose ratings fall below the threshold. The platform controls every meaningful dimension of the working relationship, that is, the terms on which labour is offered, the discipline mechanism by which workers are sanctioned, the data through which their performance is assessed. But by calling these workers contractors, the company transforms what would be employer obligations into worker burdens. The woman cleaning the house in Sandton is now responsible for registering herself as a provisional taxpayer, filing biannual returns, and navigating a system designed for accountants and professionals. The results are predictable in that, according to SweepSouth’s own data, 77 per cent of domestic workers surveyed are not registered for Unemployment Insurance Fund. Only 12 per cent fully understand their rights under the Compensation for Occupational Injuries and Diseases Act. When a platform worker is injured cleaning a client’s home, she falls through a gap in the law: she is not an employee of the homeowner, and the platform denies that she is its employee either. The 2021 Mahlangu ruling, which extended the Compensation for Occupational Injuries and Diseases Act coverage to domestic workers, has not reached her.

The discipline of fiscal sociology, which traces the relationship between taxation, state formation, and social legitimacy, has long argued that a tax system encodes the political priorities of the state that designs it. Rudolf Goldscheid, writing in 1917, described the state budget as “the skeleton of the state stripped of all misleading ideologies”. More recently, scholars working in the tradition of feminist political economy, such as Kathleen Lahey and Miranda Stewart, have documented how tax systems systematically undervalue care work and reproduce gender hierarchies through apparently neutral rules. The South African fiscal system is an example of this dynamic in unusually sharp relief: a state that formally committed itself to gender equality and substantive transformation through its constitution continues to operate a tax and social insurance architecture that cannot see the economic contribution of the majority of women who work within its borders, precisely because those women do not work in the forms the system was built to recognize. Platform companies have understood this architecture better than the legislators who are supposed to regulate them, and they have designed their business models accordingly.

What makes this particularly urgent is that the model is replicating across the continent. Kenya has Lynk which operates with the same basic architecture of contractor classification and algorithmic management in the domestic and skilled trades sectors. Nigeria has Eden Life. Egypt has FilKhedma. Each of these platforms interacts with national fiscal systems that were not designed to see informal workers in the first place. These are systems inherited from or shaped by colonial administrations that likewise excluded domestic and care workers from formal fiscal recognition. The colonial and apartheid-era exclusions were constructed through explicit statutory text. The platform-era exclusions are constructed through contractual design and data architecture. The technical form has changed. The structural outcome has not. In each case, the state loses the fiscal data it would need to extend social protection, the worker loses the social protection to which she would otherwise be entitled, and the platform company captures the economic value of the labour without assuming the legal responsibilities of the employer.

The European Union has recognized this structural problem and moved to address it. The EU Platform Work Directive, which came into force in October 2024, establishes a rebuttable presumption of employment for platform workers across member states. This means that platforms like SweepSouth, were they operating in Europe, would be required to demonstrate that their workers are genuinely self-employed rather than placing the burden on exhausted, low-income women to prove that they have employment relationships they often do not fully understand. The Directive is imperfect; it took years of lobbying by platform companies to weaken its enforcement mechanisms, and transposition into member states’ national law will be contested. But it represents a legislative acknowledgement that the contractor classification model is a legal fiction incompatible with social protection obligations, and it places the burden of proof where the informational and legal power actually lies, that is, with the company. African states have no equivalent protection, and it is not sufficient to argue that African economies are “different” or that informality is somehow culturally embedded. Informality in Africa is structurally produced – by colonial labour law, by structural adjustment programmes that dismantled social protection systems in the 1980s and 1990s, and now by platform architectures that exploit the regulatory gaps those earlier transformations created.

Why does this matter beyond the individual hardship it produces? Because taxation is not merely about revenue collection. It is about the social contract between state and citizen, the mechanism through which economic contribution is recognized and social protection is earned. When a woman works for years through a platform, paying for transport, wearing out her body cleaning other people’s homes, and generating nothing that the fiscal state can see, something has fractured in the relationship between economic contribution and social protection. She is sustaining households. She is enabling the productivity of formal-sector workers who would otherwise have to provide their own childcare and domestic labour. She is performing work that the society she lives in cannot function without, and the systems that are supposed to recognize and reward economic contribution have no category for her existence. This is not simply an administrative inefficiency. It is a form of structural injustice with fiscal mechanisms.

The solution is not to extend the reach of existing systems without reconsidering their design premises. Fiscal systems built around the formal male waged worker cannot be made to see care work by simply adding a new registration category. They need to be redesigned on the premise that care work is economically valuable, that informal economic activity is legitimate economic activity, and that fiscal citizenship should not depend on participation in formal employment structures that were never designed to include the majority of those who work. This requires statutory reform in at least three directions: first, a rebuttable presumption of employment for platform workers that mirrors the EU approach but is adapted to African institutional contexts; second, care-adjusted social insurance contribution frameworks that account for the interrupted, part-time, and multi-employer nature of domestic and platform work; and third, algorithmic impact assessments for fiscal and labour systems, so that states can identify and remedy the discriminatory outcomes that digital management systems produce without anyone having consciously intended them. None of this is technically complicated. It is politically contested, because it would require platforms to assume costs they have successfully externalized onto workers and the public purse, and because it would require states to acknowledge that their fiscal architectures have reproduced, in digital form, the exclusions they formally committed themselves to dismantle.

This research forms part of Project TERRA (Technology, Equality, Regulatory Risk Assessment), a programme investigating how algorithmic systems interact with fiscal architectures to produce exclusion across Africa. The project is supported by Luminate and has enabled sustained research into the mechanisms through which digital transformation is reshaping how gender bias and fiscal policy interact across Africa. The woman crossing Johannesburg before dawn is not a marginal case. She represents the majority of those who labour in African economies, and her fiscal invisibility is not an oversight but an outcome, produced by specific legal choices that specific states have made or failed to make. The app did not create her invisibility. But it has perfected it, and the tax system is being asked to see her in a language it was never designed to speak.

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

I was often told that ending poverty required economic growth.

Grow the economy. Create more wealth. Raise incomes. And poverty will eventually disappear.

Yet after decades of growth-centred policymaking, poverty remains widespread, inequality continues to rise, and governments around the world struggle to fund the public services people depend on.

What if poverty is not just the result of economies growing too slowly? What if it is also shaped by political choices about who benefits from economic activity, who accumulates wealth, and who is expected to pay for the systems that keep societies functioning?

These are some of the questions explored in the Roadmap for Eradicating Poverty Beyond Growth, launched in April following a three-year collaborative process led by Olivier De Schutter’s team and involving hundreds of participants from civil society organisations, trade unions, research institutions, UN agencies and governments around the world.

The roadmap challenges the idea that economic growth alone can deliver social progress. Instead, it asks what would be needed to build economies centred on human wellbeing, social justice and ecological sustainability.

For the Tax Justice Network, the launch of the roadmap marks the culmination of a process we have been part of since 2024.

Our involvement began when the UN Special Rapporteur on Extreme Poverty and Human Rights launched a call for inputs on eradicating poverty in a post-growth context.

In our 2024 submission, we argued that discussions about poverty cannot be separated from questions of tax abuse, wealth concentration and governments’ ability to raise revenue.

In 2025, we contributed again through a second call for inputs. This time, we focused on what tax justice looks like in a post-growth economy, including the role of corporate taxation and the unequal distribution of taxing rights between countries. We joined hundreds of organisations, researchers and advocates in contributing to the roadmap’s development from different areas of work and expertise.

Over the following year, the roadmap evolved through consultations, exchanges and discussions involving organisations working across a wide range of issues, from labour rights and social protection to climate justice and human rights.

In April, many of those contributors gathered in Geneva for the roadmap’s launch conference to reflect on the process and discuss the next steps.

One thing that stood out throughout the consultation process was how often discussions about poverty led to questions about public revenue.

Participants approached the conversation from very different perspectives – social protection, labour rights, public services, care work, climate action and human rights. Yet many of these discussions returned to a common challenge: how can governments reduce poverty and inequality if they lack the resources needed to invest in people?

For the Tax Justice Network, that question inevitably leads to tax.

Every year, governments lose an estimated US$492 billion to tax abuse by multinational corporations and wealthy individuals. These are resources that could otherwise be invested in healthcare, education, social protection and other measures aimed at reducing poverty and inequality.

Governments are currently negotiating a UN Framework Convention on International Tax Cooperation (UFCITC), which could reshape the global rules that determine where profits are taxed and who gets to tax them.

While the roadmap focuses on poverty eradication and the convention focuses on international tax cooperation, both processes raise related questions about economic governance, inequality and governments’ capacity to act. How can countries secure the revenues needed to fund public services? How can they curb cross-border tax abuse? And how can international rules better reflect the needs and priorities of all countries, particularly those that have historically had less influence over global tax rule-making?

The roadmap will be presented to the Human Rights Council on June 25, 2026. In addition, a series of policy briefs will now explore different aspects of the roadmap in greater depth. One of these, written by the Tax Justice Network and due to be published later this month, focuses on corporate taxation and the role it can play in supporting poverty reduction and more equitable economies.

Together, these briefs will deepen the evidence base underpinning the roadmap by exploring how different policy domains can contribute to a post-growth transition. By linking broad principles with concrete policy measures, they aim to support informed debate and help identify pathways towards more equitable and sustainable economies.

As this work move forward, we also welcome the appointment of Ms Elena Carolina Díaz Galán, as the new Special Rapporteur on Extreme Poverty and Human Rights. We look forward to continuing to support this agenda and helping hold governments and institutions accountable for the delivering the commitments needed to tackle poverty and inequality.

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

Picture the scene. It’s August in New York and international negotiators are meeting to continue moves to ensure that multinational companies are finally required to pay taxes according to where their real economic activity takes place.

Only one country is missing from around the table – the United States. Despite physically hosting the discussion, the Trump administration refuses to participate in the talks that will define the UN Framework Convention on International Tax Cooperation.

This is part of a pattern. After coming to power in 2025, the administration upended everything that had been negotiated at the OECD since 2019. First they vetoed ‘pillar one’ of the agreement, and then they demanded an exemption from most of ‘pillar two’ – which was largely designed by the US to begin with. Now the negotiations have moved to the UN, and the US is being left behind.

When combined with the deeply damaging Tax Cuts and Jobs Act passed by the first Trump administration, the result is that US multinationals are now shifting twice as much profit out of the countries where they do business.

But don’t imagine that the US is benefiting. On the contrary, those multinationals are paying even less tax to the US than they did before. Don’t think that foreign multinationals are lining up to pay tax either – when in Rome, after all. Nor has the US gained any jobs from giving away the farm – so pretty much everyone is a loser.

That includes US states, who typically base their state-level corporate income tax on whatever the US administration accepts at federal level, adjusted for the state’s share of the multinational’s real (US) economic activity. So as the second Trump administration again lets multinationals, US and foreign, walk all over their tax obligations, that laxness deprives the states of revenue too.

And this is where California is stepping up.

The US states, just like the provinces of Canada and the cantons of Switzerland, among others, use a taxing method known as formulary apportionment to determine their corporate taxes. A multinational’s total profits are added together and then distributed to states according to the share of its economic activity taking place there. Each state is then allowed to tax the share of profits that fits its share of the multinational’s employees, assets, or sales. For instance, if half of the employees and half of the sales are happening in California, California would be allowed to tax half of the profits.

The key point is to make sure that companies pay where they play – rather than making their profits in one place, but declaring them somewhere else for tax purposes.

The reason to rely on this formulary apportionment method is that the basis of international corporate tax rules – the arm’s length principle – is unfit for purpose. This approach allows multinational groups to set ‘transfer prices’ for the exchange of goods and services between sister companies, as if they were operating independently (at arm’s length from one another). Inevitably, multinationals succumb to the temptation to manipulate these transfer prices in order to shift the group’s profit into entities in other jurisdictions where they will pay little or no tax. This allows companies to pay where they say the profits are, instead of where they actually arise.

The growing importance of intangible assets such as corporate brands and intellectual property, and the more recent phenomenon of digitalisation, has made it increasingly difficult for tax authorities to challenge abusive transfer prices. The result is that the scale of profit ‘misalignment’ – the share of multinationals’ profits that are declared where they say, instead of where they play – has rocketed. Back in the early 1990s, around only 5% of the global profits of US multinationals were misaligned in this way. That doubled within the decade and continued to rise ever since, reaching 20% by the 2010s and an average of 24% for 2016-2021 – supercharged by the Tax Cuts and (No) Jobs Act.

The current Trump administration’s recent changes, and undermining of even the limited OECD reforms, have further exacerbated the problem. Major US tech companies now pay tax at effective rates that are barely into double digits. Pharma companies and others channel vast profits through Switzerland, Ireland, Puerto Rico and Singapore.

That’s why the countries of the world, with the exception of the refusenik Trump administration, are now negotiating on a UN tax convention that would commit to allow all states to exert taxing rights over economic activity in their jurisdiction. This lays the base for the subsequent Conferences of the Parties to agree a formulary apportionment approach – an approach that may already be embedded in the protocol for taxing crossborder services which is being negotiated alongside the convention.

The state of California is now pioneering the approach in the US. At present, and like a number of US states, California offers companies an election: for the apportionment of tax base that underpins their state tax liability, they can either be assessed on their declared US profit, or they can elect to be assessed on the appropriate share of their global profit. To the extent that the US share of profits has historically been less than its share of economic activity, it has almost always been cheaper for multinationals to pay state tax on the basis of their US profits – and so they elect for ‘water’s edge’ option, where the assessment stops at the US border.

California’s proposed legislation, AB 1790, would end this election and require companies to be assessed on the unitary basis – according, that is, to the global profits of the whole group, rather than the claimed US profits only. This would mandate ‘Worldwide Combined Reporting’ (WWCR). That is, companies would have to report the global activity and profits of their group.

If the legislation passes, California will cut through the abuses of the arm’s length principle and simply tax multinationals according to California’s fair share of each group’s global economic activity. This will not only point the way for other US states to follow, but also aligns with the direction of travel for negotiators at the UN: away from the obsolete arm’s length principle, and towards a system of taxing rights based on the location of real economic activity.

As this new future of corporate taxation comes ever more closely into view, California’s policymakers are weighing up their opportunity to end the loophole of the water’s edge election and mount a powerful defence of their tax base.

Thinking of the questions that policymakers might have, we’ve put together a Q&A based on close engagement with expert allies. The full text is below, or you can download a pdf.

Q1. How do multinational companies use profit shifting to avoid US state taxes?

In US states, a corporation’s income tax base essentially begins with its federal tax base. That means that the offshore profit shifting that drains the federal tax base drains the state tax base as well. Profit shifting schemes take different forms, many incredibly complex and intentionally opaque. Often, they are engineered by creating paper transactions among artificially manipulated legal entities, typically in the types of jurisdictions that top our Corporate Tax Haven Index – while the real economic activity that produced those profits never moves at all.

Q2. Do traditional anti-abuse rules eliminate state tax avoidance?

No. Traditional anti-abuse rules still rest on the legal fiction that the prices for internal transactions in a multinational group, including of subsidiaries transacting with their controlling parent, can be set as if they were independent equals operating at ‘arm’s length’ from each other in a free market. This absurdity allows multinationals great leeway in practice to manipulate these transfer prices in order to make sure the profit from economic activity in one place, is declared in a much lower-tax jurisdiction elsewhere.

Q3. How does WWCR end multinational state tax avoidance?

Worldwide Combined Reporting (WWCR) ends multinationals’ state tax avoidance by taxing them based on economic reality instead of on embarrassing fictions. When a commonly controlled group of affiliates are functionally integrated and mutually interdependent, as virtually all multinationals are, then WWCR treats them all as a single taxpayer. It requires complete reporting of the entire group’s profits, everywhere. Then, to determine what portion of those profits the state may fairly tax, it uses a standard “apportionment formula” (for example, the group’s in-state share of its worldwide sales and employment).

Under WWCR, the entire group’s worldwide profits are in the tax base, so shifting profits around the group achieves nothing. And corporate state-tax avoidance disappears.

Q4. Does WWCR have any impact on corporate location decisions?

Under WWCR, corporate relocation threats are hollow. The cost and disruption of relocating significant operations out of state can be enormous. Such decisions are based not on marginal increases in tax costs but on access to infrastructure, resources, trained workers, and customers. And, in the majority of states that apportion taxable profits by sales alone, relocation would not avoid a single dollar of tax.

Furthermore, no executive could credibly justify, to shareholders, the decision to abandon a profitable market over the end of an unfair tax advantage. If anything, WWCR improves the business climate: it levels the playing field for local small and medium-sized businesses that do not have shell companies in offshore tax havens. And this is crucial: by ending the unfair tax advantage that multinationals have over the smaller, local businesses that typically provide the bulk of employment and economic dynamism, WWCR is a fundamentally pro-business measure.

Q5. Why will corporate owners, not customers, be impacted by WWCR?

WWCR’s economic incidence falls on those who actually pocket the profits — shareholders and senior executives — not consumers. The multinationals that will pay more under WWCR are not businesses competing on thin margins; they are the giants whose profits flow from market dominance, valuable intangibles, pricing power… and tax avoidance. Economic research consistently finds that this windfall — what economists call “supernormal profits” or “excess rents” — accrues to corporate owners, not customers. In fact, some research shows that where multinationals have engineered lower effective tax rates, even shareholders do not gain – they appear to receive no higher return, but they do end up taking on greater risk because the shares of aggressive tax-avoiders become more volatile. Customers never share the upside when these corporations book outsized profits. They will not bear the downside when WWCR captures part of those profits as state tax.

Q6. What ensures that WWCR taxes only those profits attributable to each state?

Two long-established principles ensure that each state taxes only its fair share. The “unitary business principle” treats an integrated and interdependent multinational corporate group as the single enterprise that it is in the eyes of management and financial regulators. “Formulary apportionment” then calculates the state’s fair share by an objective formula — for example, its share of the group’s worldwide sales, employment, etc. Picture the group’s worldwide profits as a pie: if 2 per cent of the group’s worldwide sales are to in-state customers, and 2 per cent of the group’s employees work there, the state’s slice is 2 per cent of the pie. That slice reflects in-state economic activity, not foreign profits. There is no double taxation.

The US Supreme Court has confirmed that WWCR, operating this way, does not tax “extraterritorial values.” And that makes sense, because if every state and every country took this same approach, the tax base would be precisely defined and apportioned among the different jurisdictions. No profits would be taxed in two different places; and no profits would be left entirely untaxed.

Q7. Is the legality of WWCR firmly settled?

Yes — and twice over. The US Supreme Court has upheld WWCR in Container Corp. v. Franchise Tax Board (1983), as applied to a US-based multinational, and again a decade later in Barclays Bank PLC v. Franchise Tax Board (1994), as applied to foreign-parent multinationals. Both decisions rest on principles of state taxing power and federalism that have remained stable across changes in the Court’s composition.

Q8. Is WWCR consistent with current global aims to stop tax avoidance?

Fully consistent. Article 5 of the draft United Nations Framework Convention on International Tax Cooperation being negotiated today shares the goals of WWCR, indicating that each countries’ taxing rights should be tied to the economic activity that they host. Also, for more than a decade, foreign governments have worked with the OECD on the Base Erosion and Profit Shifting (BEPS) initiative and its successor framework, Pillar One and Pillar Two. Both efforts expressly recognize the serious harm aggressive corporate profit shifting causes to public revenues worldwide.