Jean-Claude Juncker appears to have distanced himself from making registers setting out the true owners of companies and other legal entities accessible to journalists and NGOs.

The EU Commission president’s carefully worded position is contained in a letter he sent to the Bureau of Investigative Journalism at City University in London this morning.

Juncker’s stance will spark deep unease from anti-corruption campaigners.

The president of the commission was responding to an appeal earlier this week by 45 investigative journalists from 23 countries urging him to force through the introduction of this key anti-corruption measure. Public registers of beneficial ownership will mean the disclosure of company and trust owners across all 28 member states.

In the letter to the Bureau, the EU Commission president wrote: “In the ongoing talks on the Commission proposals our negotiators support provisions of enhanced transparency and call for systems of access to beneficial ownership information including clarification on the possibility of access by third parties who demonstrate a justified legitimate interest.”

The statement will be seen as falling short of an outright endorsement that registers will be open to all.

The beneficial ownership policy forms part of a new Anti-Money Laundering Directive which is in the final stages of negotiations between the Commission, the Council of Ministers and MEPs. The Bureau understands drafts of compromise positions are already circulating.

Final agreement is expected on Tuesday. The beneficial ownership section of the directive was overwhelmingly passed by MEPs in March.

Earlier this week, senior investigative journalists from around the world called on Juncker, who is currently under intense pressure for his involvement in the “Lux Leaks” scandal, “to ensure the EU takes this critical step in the fight against corruption, which undermines the rights of people in Europe and around the world and threatens the credibility and integrity of the European market.”

But with signals suggesting the Council of Ministers are blocking the possibility that the public can access beneficial ownership registers, Tamira Gunzburg, Brussels director of the ONE Campaign said: “It is unbelievable that amidst the outbreaks of scandals resulting from financial secrecy, the Council is trying to dilute the parliament’s call for public disclosure of who is hiding behind anonymous companies and trusts. We cannot let this historic opportunity slip by settling for anything less than full public access for anyone without exception.”

Criminals and tax abusers use complex corporate structures to cover their tracks. Often shell companies are created to allow cash to move across borders so evading detection from the police and other investigators.

To combat this, it is understood that under the new Anti-Money Laundering Directive will feature a provision that will force member states to ensure that corporate and other legal entities, that include trusts, will be required to obtain and hold “adequate, accurate and current information on their beneficial ownership”.

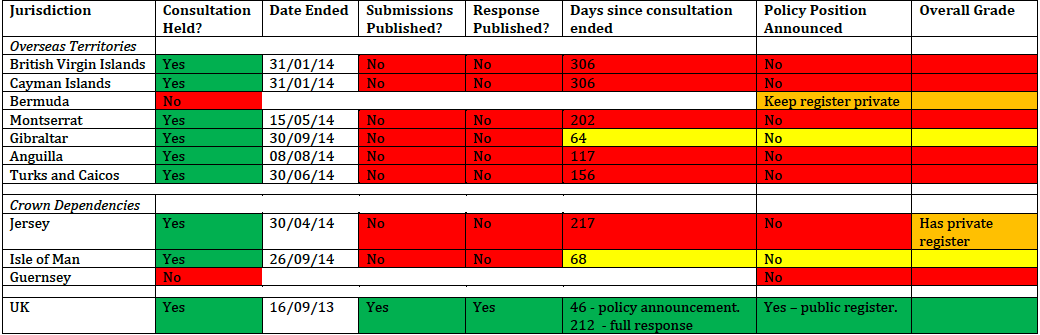

David Cameron has already committed to making this information publicly accessible. Denmark and the Ukraine have also committed to introduce public registers. But anti-corruption experts say for registers to be successful in combatting financial crime, as many countries as possible need to embrace the measure.

Letter From President Juncker to Mr Nick Mathiason

From Eurodad:

From Eurodad: