On 2 April 2020 the Tax Justice Network co-organised together with the Financial Transparency Coalition, Transparency International, Global Witness, Global Financial Integrity, Open Ownership, The B Team and the World Economic Forum’s Partnering Against Corruption Initiative (PACI), the first exploratory virtual call to form a multi-stakeholder advisory group to promote short term pilots on verifying beneficial ownership information.

Beneficial ownership

transparency has entered the mainstream and is rapidly spreading around the

globe. Within three months since the publication of the Financial Secrecy Index in January 2020, three more countries have

approved beneficial ownership registration laws, including Panama, taking the

number of jurisdictions with a beneficial ownership register to 79. However,

verification of beneficial ownership information held by registers (to make

sure registered data is updated and truthful) remains a challenge.

To promote beneficial ownership verification around the world, as a corollary of our paper on how countries can verify beneficial ownership information, we have co-developed a concept note to set up a multi-stakeholder group to share experiences and best practices among activists, investigative journalists, international organisations, governments and the private sector. The goal of the advisory group would be to promote short-term pilots to verify beneficial ownership information in at least two countries, a developed and a developing one. Lessons learnt would be used to either expand or replicate pilots in other countries.

The first exploratory call to receive feedback on the concept note had a great turnout despite Covid-19. More than 50 people joined the call (some in an “observer status”), including experts from the World Bank, the IMF, the EU Commission, Europol, the UNODC, the Inter-American Development Bank, the Inter-American Center of Tax Administrations (CIAT), the Latin American FATF (GAFILAT), EITI, Open-Government Partnership (OGP), international banks and online payment companies including Citi, HSBC, Bank of Montreal and Paypal, European and Latin American authorities, and technology companies such as Refinitiv. Here’s a summary of the first exploratory call.

Based on the interest

and feedback, we will now host three focused calls:

1) The needs of users: To discuss current

needs of beneficial ownership users such as banks, investors, law enforcement,

prosecutors, investigative journalists, activists, etc.

2) How to select countries for short-term pilots:

To discuss the criteria

to select countries and their pilots.

3) Mapping current verification strategies: To discuss current

strategies, technologies and best practices used to verify information that

could be used to verify beneficial ownership information.

Participation at the call (by invitation only) does not necessarily mean being an active member in the advisory group, which is still being developed. At the same time, while stakeholders may have different views, there is a commitment not to undermine the call for public beneficial ownership registries or the fight against illicit financial flows. If you have any questions or comments, please send an email to andres [@] taxjustice [.] net.

In the Tax Justice Network’s monthly podcast, the Taxcast: from the ashes of the coronavirus crisis how can we build a better economic and socially just system that works for all of us? The pandemic also exposes the pile-up of unaddressed crises which we must also fix. A transcript is available here due to popular request (not guaranteed to be 100% accurate)

We discuss:

tax justice (which was always key)

bailout conditions for companies now seeking government assistance

Universal Basic Services

Interviews:

Idriss Linge, finance journalist and producer and presenter of the French language Tax Justice Network monthly podcast Impôts et Justice Sociale

The voices of US Congress woman Alexandria Ocasio-Cortez, Chamath Palihapitiya of investment firm Social Capital speaking with presenter Scott Wapner on CNBC

I think it’s quite likely that we’ll see a much longer period of full depression, closer to what happened in the banking collapses in 1873. Far too many commentators have failed to grasp that we’re not facing one crisis in 2020 but we’re facing multiple crises, some of which have been building up for decades. If ever there was a moment to launch a truly radical departure from the neoliberal world order, this is that moment.”

~ John Christensent, Tax Justice Network

It’s about reclaiming the collective ideal and the idea that if we all get together and pool our resources and share risks, we will do a lot better. And it’s about putting people in control of how services are designed, to help each other, to look after each other.”

~ Anna Coote of the New Economics Foundation on Universal Basic Services

Further reading:

Tax Justice Network work and proposals on covid-19 are available here

“there’s an estimated $8-35 trillion sitting offshore that must now be tapped into”

Argentina refuses to bail out a company headquartered in Luxembourg, plus companies based in ‘non-cooperative’, low tax or no tax jurisdictions

Want to download and listen on the go? Download onto your phone or hand held device by clicking ‘save link’ or ‘download link’ here.

Want more Taxcasts? The full playlist is here and here. Or here.

Want to subscribe? Subscribe via email by contacting the Taxcast producer on naomi [at] taxjustice.net OR subscribe to the Taxcast RSS feed here OR subscribe to our youtube channel, Tax Justice TV OR find us on Acast, Spotify, iTunes or Stitcher.

Join us on facebook and get our blogs into your feed.

This is a Portuguese translation of the Tax Justice Network’s proposal of a 5-step test for coronavirus bailouts. A Spanish translation is available here (external website).

Dinamarca, Polônia, França, Argentina já anunciaram e outros países europeus estão estudando não auxiliar empresas que registradas em paraísos fiscais. Essa medida vai numa excelente direção, mas pode ser melhorada em alguns aspectos.

O teste foi desenvolvido para evitar que o dinheiro de contribuintes acabe em paraísos fiscais corporativos e para garantir a transparência tributária dos benefícios recebidos.

Se sim – e a corporação não publicar relatórios completos por país que opera até o final de 2020, de acordo com o padrão da Global Reporting Initiative para demonstrar que a presença no paraíso fiscal é para atividade comercial legítima e não com a finalidade de reduzir as obrigações fiscais em outros lugares – ela deve ser desqualificada para receber um resgate.

A Tax Justice Network convida os governos a confiar no Índice de Sigilo Financeiro e no Índice de Paraísos Fiscais Corporativos, em vez de listas de paraísos fiscais nacionais ou regionais, como a da União Europeia, já que elas provaram ser políticas e fracas demais para serem eficazes no combate ao abuso tributário. As listas da UE desde a primeira em 2017 nunca cobriram nem 10% dos serviços de sigilo financeiro do mundo.

O grupo corporativo participou de escândalos financeiros ou fiscais, como LuxLeaks, ou recebeu auxílio estatal ilegal?

Se sim, a corporação deve ser desqualificada para receber um resgate.

O grupo corporativo publicou on-line suas contas mais recentes de todas as entidades legais do grupo, incluindo relatórios completos por país, de acordo com o padrão da Global Reporting Initiative?

Se não, os governos devem estabelecer uma condição para que os beneficiários do resgate façam isso até o final de 2020. Se a condição não for atendida dentro do prazo, o dinheiro do resgate deve ser devolvido.

O grupo corporativo publicou informações sobre quem são os proprietários beneficiários e legais de todos os seus veículos legais e a estrutura corporativa completa do grupo?

Se não, os governos devem estabelecer uma condição para que os beneficiários do resgate façam isso até o final de 2020. Se a condição não for atendida dentro do prazo, o dinheiro do resgate deve ser devolvido.

O grupo corporativo comprometeu-se em proteger seus funcionários e a não distribuir dividendos para seus acionistas até que os empréstimos do resgate sejam totalmente pagos e o grupo corporativo retorne à lucratividade ou se torne insolvente?

Se não, a corporação deve ser desqualificada para receber um resgate. As empresas resgatadas, no mínimo, devem comprometer-se a não demitir funcionários que precisam ficar em quarentena ou hospitalizados e pagar a todos os funcionários significativa porcentagem de seus salários, até o reembolso total dos fundos de resgate ou a insolvência da empresa. As empresas resgatadas também não devem distribuir dividendos, recomprar seu próprio capital social e converter outras reservas de capital, como prêmios de ações, em bônus para os acionistas até que a empresa pague integralmente seus empréstimos de resgate e retorne à lucratividade.

A pressão sobre o governo para enfrentar os riscos que os paraísos fiscais das empresas representam para os esforços para combater a pandemia de Covid-19 vem crescendo. A França perdeu mais de U$ 2,7 bilhões em impostos corporativos para a Holanda. Itália e Alemanha perderam mais de U$ 1,5 bilhão cada e a Espanha perdeu quase U$ 1 bilhão para o paraíso fsical holandês.

Alex Cobham, diretor da Tax Justice Network: “A pandemia de coronavírus expôs os graves custos de um sistema tributário internacional programado para priorizar o interesse dos gigantes corporativos em relação às necessidades das pessoas. Elaboramos o teste de “fiança ou resgate” para ajudar os governos a garantir que os impostos sejam direcionados à proteção do emprego e do bem-estar das pessoas, em vez de recompensar os abusadores fiscais”.

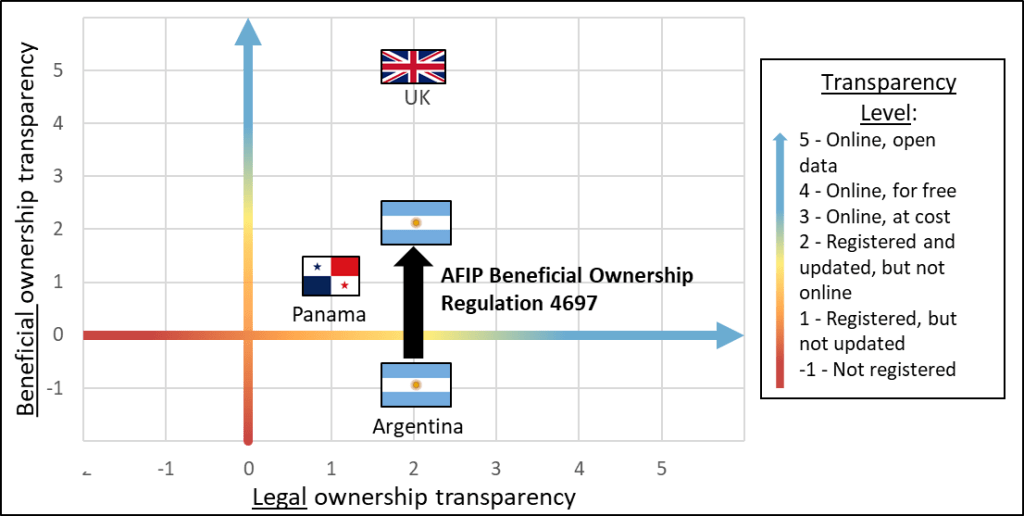

The Tax Justice

Network, together with Fundación SES, the Financial

Transparency Coalition and PROCELAC (Argentina’s anti-money laundering

prosecutor) have been co-hosting an event in Buenos

Aires for the last five years to promote public beneficial ownership registries

in Latin America. It looks like our efforts have paid off. On 15 April 2020 the

Argentine tax authorities (AFIP), who have been participating at this event from

the beginning, finally approved Regulation 4697 to require beneficial ownership registration for

a wide range of legal vehicles including companies, partnerships and investment

funds. This is a great step forward in tackling financial secrecy and tax

abuse. Unfortunately, though, the register will not be public and so falls

short of its full potential as a tool for transparency and tax justice.

By approving this new

beneficial ownership regulation, Argentina will surpass Panama’s transparency

on beneficial ownership. Panama has already approved a beneficial ownership

register, but it still has problems with bearer shares because they need not be

immobilised by a government authority and thus Panama has been unable

to obtain companies’ ownership information in a few cases. Bearer shares give

ownership of a company to whoever is physically holding the bearer share in

their hand, making it impossible to guarantee that information held by the register is up to

date. Nevertheless, Argentina is still far away from the UK which makes

information held by the register available to the public online in open data.

Beneficial ownership

transparency has entered the mainstream and is rapidly spreading around the

globe. The Financial Secrecy Index published in January 2020 found that 41 countries had beneficial ownership laws that were robust enough

to meet the index’s criteria for effective transparency. This criteria included

requiring information held by the register to be regularly updated. At least three more countries have since approved

beneficial ownership registration laws, including Colombia, Panama and now

Argentina.

In the case of

Argentina, while the Financial Secrecy Index acknowledged that beneficial ownership registration was

superficially mentioned under article 26 of its Law 27444 on “simplification and de-bureaucratization of

the State”, there was no central register of beneficial owners. Beneficial

ownership information for companies was only required in two provinces and the

city of Buenos Aires.

Regulation 4697

establishes a beneficial ownership registration to be centrally managed by the

tax authorities (AFIP). Here are some preliminary observations on the new

regulation.

Positive aspects

Wide scope: unlike other countries’ beneficial ownership laws that cover only

companies, Argentina’s new regulation covers a wide range of legal vehicles:

companies, partnerships, associations, and importantly, investment funds, which

generally present high secrecy risks as described by our paper on beneficial ownership in the

investment industry.

No threshold: many countries, especially in the EU, follow the threshold of “more

than 25 per cent of ownership” to consider an individual to be a beneficial

owner. This high threshold, considered by many countries as a fixed rule, is

actually based on what we consider to be a wrong

interpretation of the

Financial Action Task Force (FATF) Recommendations. The main problem is that it

makes it very easy to avoid transparency by creating a company with at least

four individuals with equal shareholdings (because no one would pass the “more

than 25% threshold”).

Some

countries, especially in Latin America, have established much lower thresholds,

including Uruguay and Costa Rica (15 per cent), Peru (10 per cent) and Colombia

(5 per cent). Positively, Argentina has joined Ecuador is establishing what we consider to be the ideal

threshold: any person

holding at least one share (or interest in an investment fund) should be

considered a beneficial owner.

However,

Argentina’s definition is even better than Ecuador’s because it goes beyond ownership

criterion (anyone holding at least one share), to also include anyone with

voting rights or with control through other means.

Wide trigger: from the ideal transparency perspective, beneficial ownership

registration should be triggered whenever a legal vehicle (i) is incorporated

or governed under domestic laws, and for foreign legal vehicles that (ii) have

a resident party (eg shareholder, beneficial owner, director, trustee, etc) or

that (iii) have operations in the country, including owning assets, engaging in

business transactions or having income subject to tax.

As

described by this blog, most countries including the European Union,

only require beneficial ownership registration for companies based on

incorporation (condition i) and for trusts when the trustee is resident in the

country (partial condition ii). The 5th EU Anti-Money Laundering (AMLD 5)

innovated by also requiring trusts’ beneficial ownership registration whenever

the trust acquired real estate or established a relationship with an obliged

entity in the EU (partial condition iii).

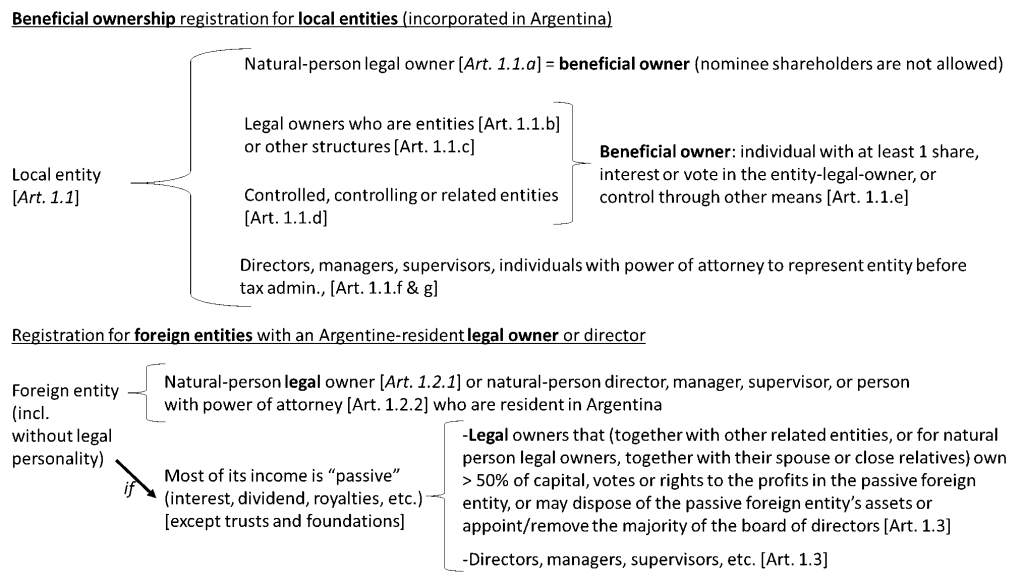

Argentina’s

new beneficial ownership applies to entities incorporated in Argentina (condition

i). However, the regulation also adds

disclosure requirements in relation to foreign entities that have Argentine

shareholders, directors, or people with a power of attorney over the foreign

entity (condition ii). First, resident individuals have to disclose any foreign

entity that they own as legal owners (but not a foreign entity that they

indirectly own as beneficial owners). The same applies if a resident individual

is a director, manager or supervisor (“fiscalizador”) in a foreign entity.

Second, there is another requirement for foreign entities that are considered

“passive” because most of their income comes from dividends, interests,

royalties, etc. Argentine taxpayers (individuals or entities) who own more than

50 per cent of the capital, voting rights or rights to profits in a “passive”

foreign entity, have to disclose this “passive” foreign entity to the tax

administration. To determine if a legal owner passes the threshold of 50 per

cent, the ownership held by other related entities (for corporate shareholders),

or by the spouse or close relatives (for natural person shareholders) must also

be considered. “Passive” foreign entities will also have to be disclosed if a

local taxpayer has the right to dispose of the “passive” foreign entity’s

assets, or appoint or remove the majority of the board of directors (regardless

of passing the 50 per cent threshold).

Based

on the above explanation, there may be an overlap for individual taxpayers:

they would have to disclose a foreign entity over which they own at least one

share or vote, as well as any “passive” foreign entity over which they own more

than 50 per cent. This redundancy may be explained because for “passive”

foreign entities, disclosure requirements include also reporting the gross

income of the “passive” foreign entity.

The

following figure summarises the beneficial ownership requirements for local entities

and the legal ownership requirements for foreign entities (including “passive”

foreign entities):

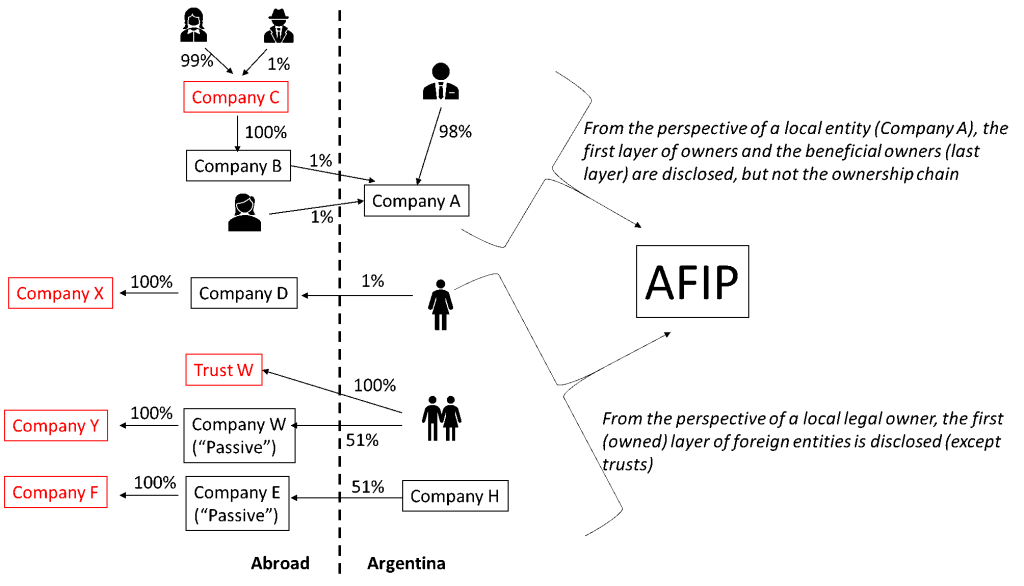

The

following figure gives examples of who gets to be reported (in black) and who

avoids being reported (in red):

Comprehensive details must be registered: not only must beneficial owners be registered

(and updated) with enough identity details (eg name, tax identification number,

number of shares or ways in which control is exercised), but also directors,

and other officers, including those with a power of attorney to represent the

entity before the Argentine tax administration. It would have been better to

include those with any power of attorney, eg to manage the entity or the

entity’s bank account.

On the other hand, shareholders and beneficial owners must report the

number of shares or votes they own, and their value. As described by our paper

on “beneficial ownership verification”, by reporting the value of the acquired

shares, authorities could also check whether the person could have afforded

those shares in the first place, based on their declared income, to detect

cases of illegal nominees or money laundering.

Negative aspects

No public access: the 2019 Financial Action Task Force (FATF)

paper on “Best practices on beneficial

ownership for legal persons” recognises that “the trend of openly accessible

information on beneficial ownership is on the rise among countries”. All EU

countries now must establish public beneficial ownership registries based on

the 5th anti-money laundering directive. Even the UK has required its

dependencies to open the beneficial ownership register and Cayman has already

promised to make it public by 2023.

In Latin

America, Ecuador

is already making beneficial ownership publicly available online and Paraguay

is considering giving public access to the name of beneficial owners. Other

countries, like Uruguay at least give access to law enforcement authorities,

including the financial intelligence unit in charge of anti-money laundering.

In Argentina’s case there is no mention of access, suggesting that information

will be confidential and only accessible to tax authorities.

This is a big

problem. Many stakeholders have an interest and need for beneficial ownership

information. In the UK, the public online beneficial ownership register was

accessed 6,500

million times only in 2018. Publicly accessible registries allow

verification of the information by journalists and activists, as exemplified by

Global

Witness’ analysis of the UK beneficial ownership data. This public verification

was also recognised by the Financial

Action Task Force paper on best practices on beneficial

ownership.

By ensuring

access to obliged entities such as banks, the EU is also able to require them

to report any discrepancy to the beneficial ownership register based on the

information that they obtain from their clients, eg when opening a bank

account. Argentina will be missing out on this verification system.

Lastly,

beneficial ownership is relevant not only for tackling tax evasion and abuse,

but also money laundering and corruption. In 2018, Argentina signed the Global

Forum Punta del Este declaration committing to use information to tackle

tax and corruption. At the very least, Argentina’s tax authorities should sign

memoranda of understanding to give access to information to the financial

intelligence unit and the anti-corruption office.

Regulation text is unclear

and confusing. Beneficial ownership regulations are

supposed to be clear to be understood by everyone. AFIP’s Resolutions

(generally, not only about beneficial ownership) could do a much better job in

writing clearly and stating explicitly who will be covered (rather than

referring to article 53 of the Income Tax Law, which in turns refers to article

73, which in turns refers back to article 53). Additional guidance would be

most welcome.

Trusts aren’t covered by this regulation. Annex I of the new AFIP resolution excludes trusts from its scope. It

could be argued that, as described by the Financial Secrecy Index on Argentina,

trusts are already required to register all their parties by AFIP Resolution

3312 from 2012. However, that Resolution doesn’t require the parties to the

trust, say a settlor or trustee, that are an entity (eg a corporate trustee) to

identify their beneficial owners.

The Ownership chain must be kept but need not be registered. Whenever a beneficial owner owns or controls an entity indirectly,

information on the full ownership chain must be kept by the company but it need

not be registered with the tax administration. The ownership chain is extremely

relevant for verifying the beneficial owner because it shows all the

intermediate layers up to the beneficial owner. This information should be

filed with authorities at least as a free text or image.

Potential for improvements

While the beneficial ownership resolution

is rather brief, given that it will be managed by the tax administration, there

are several synergies that may be exploited:

Verification of beneficial ownership information. While registering information with a government authority is of

utmost importance to guarantee availability of beneficial ownership information,

verification of information is indispensable to confirm the accuracy and

veracity of registered information.

We have written a paper on

how

countries could verify beneficial ownership information. It’s not only about

establishing validation mechanisms (eg to prevent a company from registering

another entity rather than an individual as a beneficial owner), but also to

cross-check information with other databases and to do big data or data mining

analysis to detect suspicious patterns and red flags. AFIP will be a in great

position to verify the newly registered beneficial ownership information given

their sophistication in the access and use of data. They already have an intelligence

unit to detect patterns of tax abuse and other red

flags. They also obtain

wealth and income information on all taxpayers from the private sector and

other state agencies to determine their risk profile. AFIP’s data includes information

on real estate and automobile ownership, bank accounts, credit card

consumption, private school fees, private health insurance fees, insurance contracts,

etc. This data can be used to cross-check information submitted to the

beneficial ownership register and vice versa.

Cross-check data with beneficial ownership data reported by

financial institutions. Based on the OECD Common

Reporting Standard (CRS) for automatic exchange of information, the Argentine

tax administration is already receiving a trove of data from local financial

institutions, including beneficial ownership data. The Common Reporting

Standard requires banks and other financial institutions to report the account

holder and, when the account holder is an entity considered “passive” (because

most of its income is related to dividends, interest or royalties), to also

report the beneficial owner of these passive entities.

Commendably, as recognised

by the Financial Secrecy Index, Argentina

is implementing the “widest approach”. This means that Argentine tax

authorities receive information on all account holders (regardless of their

country of residence). Therefore, AFIP should be able to compare the beneficial

ownership information reported by local financial institutions (based on their

own customer due diligence) as part of automatic exchange of bank account

information, with the information reported by entities directly to AFIP, based

on the new beneficial ownership regulation. For example, if an Argentine entity

reported to AFIP that John is its beneficial owner, but the same entity – when

opening a bank account- told its Argentine bank that Mary is the beneficial

owner, then Argentina’s tax authorities will be able to detect this

discrepancy.

In addition, authorities

should be able to compare information reported by resident legal owners about

their foreign legal vehicles, with the banking ownership information

automatically received from abroad based on the Common Reporting Standard.

In other words, AFIP

should cross-check:

information on beneficial

owners of local entities, by comparing the information reported directly by

local entities with the information reported by local banks; and

information on legal owners of

foreign legal vehicles, by comparing the information reported directly by local

legal owners, with the information automatically received by AFIP from foreign

banks pursuant to automatic exchange of information

Recommendations

Based on the above analysis, we would

propose that Argentina should take the following measures:

Publish guidance and organise

trainings for the private sector (companies, lawyers, accountants, etc) to

provide clarity and explanations on the new beneficial ownership regulation.

Establish beneficial ownership

registration requirements for trusts. Add beneficial ownership definitions for complex

structures that combine legal persons and trusts (eg when a trust owns a

company, all parties to the trust should be considered the beneficial owners of

the company).

Sign memoranda of understanding

to allow at least other local authorities to access beneficial ownership

information, and to cross-check with data available in other agencies,

including the commercial register, the securities regulator, the real estate

registry, etc.

Publish at least basic

beneficial ownership information through Argentina’s “National Register of

Companies” (Registro Nacional de Sociedades) which is the recent federal online

public register that publishes

basic company information. AFIP is already providing data to the National

Register of Companies, which is also fed with data from the local (provincial) commercial

registries.

Verify beneficial ownership

information obtained pursuant to the new regulation, with information already

available to AFIP based on wealth and income information reported by the

private sector and local government agencies as well as bank account

information related to the automatic exchange of information.

Welcome to this month’s latest podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! (Ahora también estamos en iTunes.)

En este programa especial sobre el Coronavirus:

La crisis económica mundial y la intervención del estado. ¿Hay que rescatar a grandes compañías que usan paraísos fiscales para la evasión?

Las distintas respuestas sanitarias y económicas de los países en América Latina

En el medio de la crisis, ¿cómo financiar al estado en la lucha contra el Coronavirus? La respuesta de un panel especial de Naciones Unidas.

Y ¿qué nos dice el presupuesto económico de un país? Examinamos la inversión en justicia y fuerzas armadas en medio de la crítica situación política y económica de Honduras

Invitados:

Desde Ciudad de Mexico Oscar Ugarteche del Instituto de Investigaciones Económicas de la UNAM (Universidad Nacional Autónoma de México)

Desde Buenos Aires, Juan Valerdi, profesor de la Universid de la Plata y ex aseseor del Banco central de Argentina. Publicaciones https://unlp.academia.edu/JuanValerdi

Desde Bogota, el economista y ex ministro colombiano, José Antonio Ocampo, hoy director del ICRICT, la Comisión Independiente para la Reforma del Impuesto Corporativo Internacional

We’re sharing this personal story from an anonymous writer who has been made redundant in the past month. The consequences of a world where we tolerated the excesses of so-called ‘wealth creators’ are becoming starkly clear as their lack of responsibility or loyalty to employees and to the society that has enriched them is hitting us hard. The wealth they extracted has flowed almost entirely one way – into their pockets via tax havens and through bending and breaking rules with impunity, leaving societies thoroughly weakened and less able to cope with the pandemic than they would otherwise have been. Now read on. [Photo by Anders Nord on Unsplash]

If you’re not careful, you’ll be next: How offshore finance has managed to make the coronavirus crisis even more unpleasant

You love your job. You’re doing good work, providing a vital service that’s making the world a better place. You work in a beautiful office, with free fitness classes, healthy snacks, social events, all the resources you need to do your job. You even get monthly emails from HR telling you how much of a valued team member you are. It’s a far cry from the drab and depressing places you worked at for years, gaining valuable experience but horrifically underpaid and making do with only just enough resources. There’s just one thing not quite right. You report to a head office based in a tax haven, and the finance department have some very specific rules around contracting and invoicing, as if they really do want to keep the operations in the ‘high-tax’ location very separate from those in the ‘low-tax’ location.

Until recently, this was my life, and I’ll admit that I thought it was brilliant. I turned a blind eye to the tax avoidance and the company’s conspicuous wealth. We were being provided for, so who minds if the family that owns the business has a couple of private jets and a bunch of multi-million pound mansions? There’s enough money to go around for everyone.

Then coronavirus happened. Demand took a huge downturn and the company’s revenue dropped close to zero. Within weeks entire departments were being cut. Years of work and experience was being lost, and people were being made unemployed just in time for the biggest recession in a generation. The founder, who before the crisis had always made a point of developing a cult of personality around himself suddenly disappeared from sight. Redundancies were handled by managers, who would in many cases soon be laid-off themselves. Not a word of apology or even acknowledgement from the owners that people were being let go. We were even told to tell suppliers that we weren’t going to pay them the money they were owed for work done. A global company, owned by billionaires, deliberately pushes small business owners and their families into destitution, simply because the cost of enforcing the contract would be too high for a small trader.

But how has offshore finance made this worse? Put simply, for years I worked to help funnel money offshore, into a place that’s only accessible to a chosen few. I skirted the very edges of the law because I had no choice, but when the going suddenly got tough, we were told that there’s no money in the business and that we have to be let go. That may be true, but since the company is privately held offshore, there’s no way at all of knowing.

We were offered the bare minimum in terms of redundancy, but as far as I know, the owner still has his private jets. The company even offered to furlough staff on the understanding that they’ll be laid off once the furlough period ends. We’ll make a few hundred pounds more but the company is going to save hundreds of thousands by reducing redundancy payouts, letting the state make up the difference through furlough payments. This company, which spent years (legally?) cheating the taxpayer out of the funds it needs, now dips into the public pocket when things turn bad, just so it can protect the offshore wealth of a family of billionaires. They’re ripping off the state, which is currently engaged in its biggest and most deadly battle since the Second World War to keep the rich in the lifestyle that they’re accustomed to. All while National Health Service workers struggle to get the equipment they need.

The coronavirus doesn’t discriminate based on how rich you are, and I hope this realisation sinks in with the people remaining at the company, especially those protecting the offshore assets. When your grandchildren ask you what you did during this crisis, do you really want to tell them that you helped swindle the same public sector that kept you and your family alive? If now isn’t the time to finally recognise that for a healthy world, we need properly funded government, then that time will never come. To all those who are working for companies that abuse the tax system, I say this: The offshore world has no loyalty to anyone. Blow the whistle, expose the fraud, let’s build a better system. Do it now, before it’s too late. Last month, I lost everything after years of defending this system. It could be you next.

Costa Rica has been at the vanguard of

beneficial ownership registration in Latin America and the world. The country approved

its beneficial

ownership registration law 9416 in December 2016 and continued to

strengthen the robustness of its beneficial ownership registration requirements

since then, as recognised by the 2018

and 2020

editions of the Financial Secrecy Index. A new bill making its way now through

Costa Rica’s legislative assembly threatens to render the country’s beneficial

ownership register useless by delaying the requirement to update information

held by the register from once a year to once every five years on shareholders

below a certain threshold.

While Costa Rica still has room to improve

its beneficial ownership transparency even further by making its register

publicly accessible, following the example of Ecuador and most countries in

Europe, Costa Rica has been a leader in beneficial ownership registration for

trusts since 2018. The country has also set a leading example on the

implementation of automated verification of beneficial ownership information,

as described in our report

here (see pages 42-43).

However, a new bill is threatening to throw

away Costa Rica’s progress on transparency by rendering the country’s beneficial

ownership register obsolete and of little use. The new bill delays the

requirement to update information held by the register from yearly to once

every five years. While the bill still requires information to be updated

whenever someone acquires more than 15 per cent of ownership, it no longer

requires updating information on lower shareholdings on a yearly basis, which may still be relevant

if an individual controls the entity through other means. For example, if the

beneficial owner controls the entity not by holding many shares, but by having

voting rights or significant influence over the entity’s decisions. No matter

how comprehensively a beneficial ownership register is staffed, resourced and verified,

it will be of little use if it’s not updated on all beneficial owners.

For the Financial Secrecy Index to consider

a country’s beneficial ownership register to be effective, based on global norms

set by the Financial Action Task Force and the OECD’s Global Forum, it requires

countries to update legal and beneficial ownership information at least

annually or whenever a change occurs (whatever happens first). Costa Rica’s

current law requires this as well. However, this will no longer be the case if

the new bill proposing to postpone the update of legal and beneficial ownership

information from each year to every five years passes. To put this into

perspective, imagine using a five year old used car listing to contact the

owner of the car about buying it!

The most puzzling part of the bill however

is the argument underlying the proposal. It doesn’t question the importance of safeguarding

against money laundering and tax evasion, but it considers the process of updating

information every year to be too costly for companies. This is a false economy.

If there has been no change in ownership or control, then updating the

information should cost little to nothing. A company is able to get the last

filed data from the register (in case they forgot to keep a copy), so they

could simply copy-paste the information when it’s time to file beneficial

ownership information again. On the other hand, if there has been a change, say

there is a new shareholder, the company should already have the information on

record, not for the sake of reporting it to authorities but for the company’s

own operations. Otherwise, how would the company know who is allowed to vote or

to receive dividends?

We all know that there is a big stretch

between approving a law and properly implementing its enforcement. However, if

the beneficial ownership law of 2016 is weakened by making the information it

gathers obsolete, there won’t be enough improvements to enforcement that could

make up for its weakness.

We hope that Costa Rica will keep up its

transparency leadership and take it forwards (towards publicity) instead of

backwards (towards outdated data).

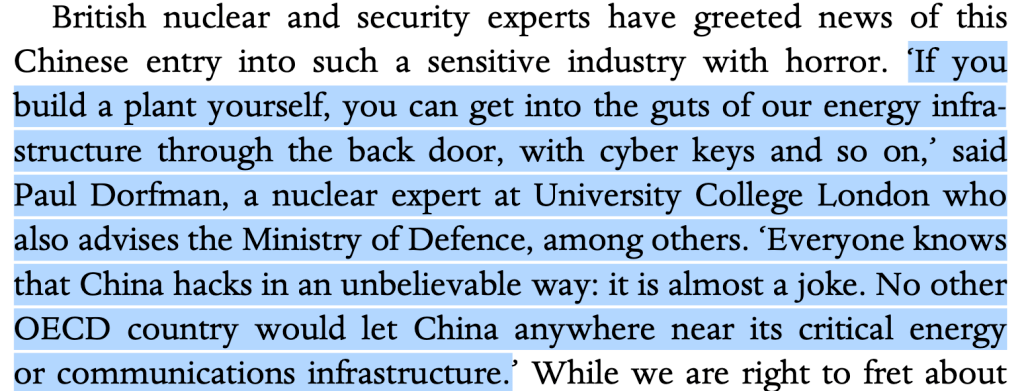

The Bank of England’s pressure on HSBC to cancel its dividend for the first time in 74 years has reignited a debate at the top of the bank over whether it should redomicile to Hong Kong.

This is shocking, on several levels.

First, that’s a direct threat by HSBC against UK policymakers – in the middle of a pandemic and a global economic shock. Classy timing.

Next, the Bank of England’s gentlemanly discouragement of dividend payments to help tackle the Coronavirus crisis is far too timid: we (and many others) have recently encouraged permanent bans on share buybacks (which used to be illegal) and temporary bans on dividends – especially banks which should now be ploughing money into shoring up their capital safety cushions in the current environment.

Furthermore, we have seen exactly this intimidation before, from exactly the same global bank, deploying the very same kinds of anonymous whispers, to favoured journalists who the bankers judge will put the “right” spin on the story.

This is, once again, the Competitiveness Agenda. Threaten to relocate elsewhere if you don’t get what you want — knowing all along that you’re not going to carry through on this threat. Talk, after all, is cheap. (HSBC is going to throw itself decisively into the arms of the Chinese Communist Party? Really?)

The same FT story cites an anonymous HSBC director accusing the Bank of England of “put[ting] a gun to the head of the board of directors . . . the calls for redomiciling will increase”.

No, it’s the other way around: HSBC is trying to put a gun to Britain’s head. Here’s how this game tends to pan out: Large multinational threatens to relocate, knowing secretly it has no plans do so. Yet an obsequious British state gratefully hands over goodies, extracted from current and future taxpayers and other sections of society. The bank then piously decides, after “careful consideration”, not to relocate. We described it thus, after the last big round of empty threats in 2016:

The bank’s been conducting a ‘review’ of its operations, and constantly drip-leaking panic-inducing details about these supposed internal deliberations, as a way of maximising pressure on British politicians to relax regulations and minimise pesky things like criminal probes, capital requirements, bank levies, and plenty more. And boy, have some concessions been made . . .

Those concessions alone have since cost the UK an estimated billion pounds a year, equivalent to the cost of educating 200,000 schoolchildren. HSBC didn’t, of course, relocate. (This kind of game happens all the time: it’s the same basic ploy as Amazon’s widely-reported efforts to engineer a “Hunger Games environment” to create ‘competition’ between US states to host its second headquarters, in which it sought to squeeze maximum subsidies and tax breaks out of the states. As one analyst put it, “Amazon already knows where it wants to be” – and in the end, his prediction proved exactly right.

To be fair, this time the FT journalists didn’t let the bank have it all its own way, pointing out that HSBC originally relocated from Hong Kong to London after Britain handed its colony Hong Kong to China in 1997: as an investor put it:

“it’s the price to pay if you’re going to domicile in the UK with all the protection that gives you.”

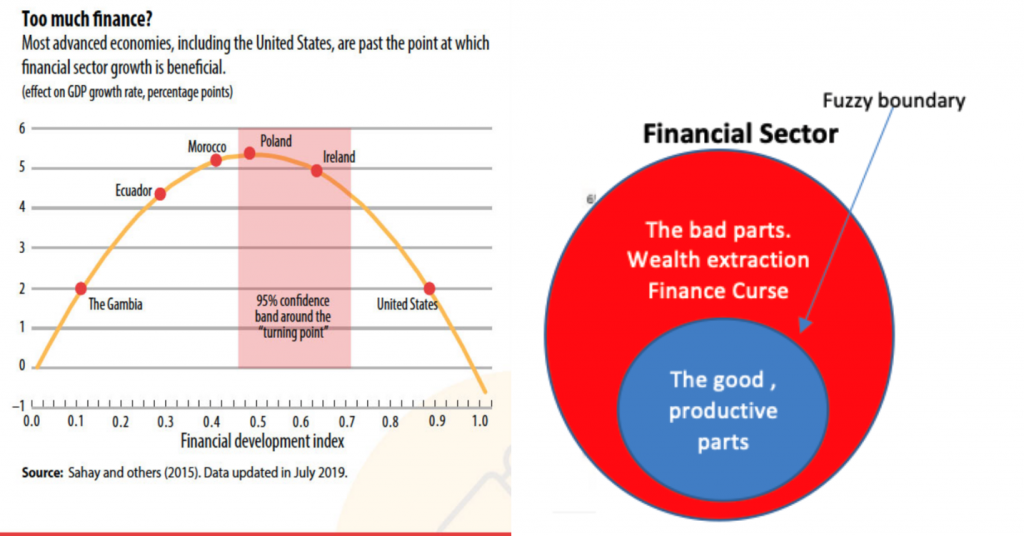

But here’s an even more important thing. The British financial sector is too big – much too big. There’s an ocean of research out there now, showing that countries with oversized financial sectors tend to become less prosperous as a result. Shrink the financial sector, for prosperity. Two images, the first from the IMF, and the second from us, show the basic issue, which is the Finance Curse.

The right hand graph is pretty much unarguable. Shrink the red, and keep the blue, seems to be a sensible approach. The left hand graph – an upturned banana shape (repeated in study after study) shows that we all need a functioning financial sector, and countries with underdeveloped financial sectors need to expand them to support prosperity. But there is an optimal point — the UK and the UK probably passed it some time in the 1980s – when the sector is providing the services an economy needs. Further growth of a financial sector beyond that optimal point starts to damage economic growth.

Why? For a number of reasons, most important of which is that once a financial sector has (to put it crudely) set up the useful services an economy needs, it finds that there are further profits to be mined by penetrating into other parts of the real economy – from agriculture to healthcare to the film industry to tourism – and finding ways to extract wealth from those parts. Frequently, it’s done by financial sector players buying up perfectly good companies then financially engineering them – running their financial affairs through tax havens, say, or by increasing their debt, or sitting astride and milking some sort of monopolistic choke point — to extract more wealth from them, and in aggregate this leaves behind a more fragile corporate landscape. This is in essence what private equity and a lot of merger and acquisitions do – or it could happen in a related guise, public-private partnerships (see the Private Equity and the March of the Takers chapters here).

These pigeons will soon come home to roost: after which we might get a better idea of the costs. It’s impossible to estimate the scale of the damage from oversized finance with any degree of accuracy, but the best estimates suggest it is very large indeed. Much is not measurable: such as the fact that in 2013 and 2015 when Britain signed a series of deals with the Chinese Communist Party to give the City of London financial sector access to lucrative financing, the quid pro quo was that Britain would have to allow the China General Nuclear Power Corporation (CGN) to take a large stake in Britain’s mega-nuclear power station, Hinkley C. Here is one reaction to that:

What the UK should be doing is taxing and regulating this rather lawless global bank, and taking a very hard line — so that it either shrinks its operations to the useful core of services it provides, or the bank relocates to Hong Kong, taking its political, economic and democratic damage with it.

In recent days a number of sudden and dramatic changes have happened in the labour market in already fragile economies, as the Business and Human Rights Resource Centre has shown. Many workers who are poorly paid and in precarious relationships [read zero or no contracts] with ‘absent’ employers – are losing their incomes. Many of these workers are women and girls.

Even under normal circumstances women and girls don’t get a great deal. Only half of women in developing regions receive the recommended amount of health care they need, and while 17,000 fewer children die each day than in 1990, still more than 6 million children die before they are five years old for a lack of adequate health care and well-being, according to UN Women. Women and girls face many gender based inequalities, generated from exclusive policy and provisions, violence, discrimination and poverty. All of these will be exacerbated as women and girls continue to care, and experience more extreme conditions for their health, security and safety. ‘Social distance’ is a health luxury that most women and girls in developing regions will be unable to achieve.

In a COVID-19 environment public health workers and cleaners are on the COVID front line.

But it is not just the frontline health and social care workers, 70% of whom globally are women. Other professions employ a disproportionate number of women on fragile contracts. In India alone 45 million people work in the garment industry – 60% of them women . At the same time women most often are the ones who are providing care for children, the sick or at-risk family and community members.

In many of the countries where the garment industry operates, for instance, workers create economic profits for the multinationals that employ them but often create little taxable profit, so little of the value these workers create is yielded as government revenue or translates into social protections and targeted services for those on the lowest incomes.

With no or little savings, and no prospect of redeployment or re-employment, governments need urgent and reactive solutions – but they also need sustainable and progressive tax regimes to help meet adequate social care, health and well being needs.

Country by country reporting (CBCR) – the transparency mechanism where multinationals are required to produce information on economic activity in each country where they operate, offers a protective measure to help governments find the information they need to tax companies appropriately – and fulfil their human rights obligation to promote women’s health and well being.

This would be a unique moment in corporate history to record a step change in leadership for CEOs, Boards and shareholders. As UN Women’s Executive Director stated last week, this is a ‘time of reckoning for our national and personal values and a recognition of the strength of solidarity for public services and society as a whole’. Financial transparency and paying a fair share is fundamental to this notion of solidarity.

Women are at the sharp end of any health crisis, but the impact of this pandemic will have first order and secondary impacts that will devastate the lives of, and kill, many women. Country by country reporting is one significant progressive step which all multinational corporations need to establish as part of their responsibilities to their workers and the communities from which they extract wealth. It won’t help women with this health pandemic, but it could have profound implications when the next one breaks.

The EU Commission has called for feedback from the public on its new roadmap for tackling tax fraud evasion. Recognising that “every year in the EU, billions of euros are lost to tax evasion”, the Commission has outlined an initial action plan, presenting key initiatives to:

tackle tax fraud

make compliance easier

take advantage of the latest developments in technology and digitalisation

The Tax Justice Network submitted feedback which can be found here and which has been reproduced below.

Tax Justice Network feedback to EU Commission’s “Action Plan on fight against tax fraud ” initiative

With the Corona pandemic exacerbating inequalities and

ushering in extreme stress on the budgets of EU member states, the Action Plan

of the European Commission is planned during the most severe crisis of the

European and global institutional architecture in 70 years, exposing hundreds

of millions of citizens inside and outside the European Union to extreme economic

vulnerability. In this context, the role of corporate tax havens and secrecy

jurisdictions within and outside the EU in undermining solidarity cannot be

tolerated any longer and calls for decisive action in order to safeguard the

European Union’s cohesion and help preventing the further spread of populist

and extremist movements.

The scope of the EU Action Plan should be broadened to

include personal and corporate income tax matters, including tax avoidance in a

legal grey zone. Options for an EU supported wealth tax and options for an

excess profits tax on firms profiteering from Corona should urgently be

explored and included in the Action Plan, jointly with reviving plans for a

broad and comprehensive tax on financial transactions.

The EU would benefit from the European Commission hosting or acting as a European Tax Intelligence Centre (EUTIC), transmitting innovative data and policy analyses for improved tax compliance and fairer taxation. Among others by applying a novel geographic risk assessment tool, EUTIC would assess vulnerabilities to illicit financial flows in Europe including from tax evasion, tax fraud and tax avoidance. A more detailed proposal for scope and data implications of an EUTIC are enclosed in the draft summary recommendations of the Horizon 2020 research project “COFFERS” (Combating Fiscal Fraud and Empowering Regulators). This project has concluded end of January 2020 and offers a wide range of relevant research findings and innovative policy recommendations (full details accessible under http://coffers.eu).

While the European Union has taken many bold legislative

steps in the past years, some policy gaps remain that need addressing. In the

realm of automatic information exchange of financial account information and

personal income and wealth taxation, the effectiveness of the entire system is

jeopardised by recalcitrant jurisdictions that refuse to engage in fully

reciprocal information exchanges. To ensure a level playing field, the EU

should consider implementing a withholding tax policy against non-participating

banks that fail to provide financial account data on a fully reciprocal basis,

using its market access as a leverage to ensure compliance.

Furthermore, the validity of passports issued under golden

passport schemes by some members states should be constrained in order to

prevent tax evaders and criminals to open foreign bank accounts with purchased

citizenship to circumvent reporting to tax authorities at their place of

primary residence. The efforts to counter tax evasion and money laundering

through beneficial ownership disclosure need to be complemented by disclosure

of legal ownership in all cases, by expanding the disclosure to EU real estate

and the registration to freeport users, and by abolishing bearer shares or

immobilising them with a government authority.

In order to rein in corporate tax havens, various conditions for participating in the Single Market should be enacted, ensuring a level playing field and robust tax revenues: group-wide public country by country reporting, full publication of unilateral cross border tax rulings including the name of the companies and minimum corporate tax rates. Other policies to consider are discussed in the current special issue of “Intertax”: Leyla Ates, Moran Harari and Markus Meinzer, ‘Positive Spillovers in International Corporate Taxation and the European Union’, Intertax, 48/4 (2020), 389–401). Full details of reform options are detailed in the 20 indicators of the Corporate Tax Haven Index.

Recommendation 1: Establish tax intelligence centres in member states and at the EU commission

The cross border integrated tax planning departments of investment

banks, accounting and legal firms require a response by the state that transcends regulatory silos. A

robust response that will safeguard the interests of ordinary citizens by

countering the multi-billion tax avoidance and money laundering industries must

include not only operational capacity to detect the latest complex cases, but

equally capacity for strategic orientation. This needs to be innovative and

responsive to changing dynamics. At the

moment, this capacity is fragmented at the national level and absent at the EU

level. As a result, there is increased risk of disconnects and time lags

between policy making and regulatory implementation, with the EU public COFFERS

suffering from billions in lost tax revenues and uncounted costs in terms of

crime and money laundering.

An EU-level Tax Intelligence

Centre (EU-TIC) would meet both of these challenges, monitoring macro-economic

trends for risks of illicit financial flows and the spillover effects of domestic

tax policies, and building advanced data mining and analytical capacity to

support targeted tax audit and policy formulation. An EU-TIC would facilitate

the prioritization of the negotiation of international agreements, shape

policies and programmes for tax compliance, and support local tax administration in operational decision

making (staffing, auditing). At the

request of member states, the EU-TIC would provide support in policy and

operational analyses, as well as tactical and strategic advice.

Dedicated tasks of the EU-TIC would include the identification of

abusive tax avoidance structures in EU financial systems and the internal

market, and the design of suitable responses. The identification of structures

would rely inter alia on the new directives

on mandatory reporting of aggressive tax planning schemes (Council Directive

2018/822/EU) and on the protection of whistleblowers (Council Directive

2019/1937/EU). Furthermore, the role of the EU-TIC would encompass the

identification of tax evasion and money laundering risks across the entire EU,

and individual EU member states, by providing data-driven country profiles of

vulnerability and exposure to illicit financial flows. This would rely in part on

bilateral financial secrecy index analyses. The EU-TIC would also provide and

review tax gap estimates.

The EU-TIC would set an example in transparency, by publishing periodic reviews, documenting in detail its activities and impact.

Recommendation 2: Addressing data gaps

Without reliable data, tax evasion and avoidance and money

laundering cannot be countered successfully and sustainably. Public data for

researchers and the wider public and the integrity of confidential

administrative data require improvement. This will foster trust in

institutions, contribute to a level playing field and fortify the rule of law.

Interoperability of available registry data is a pressing concern

that requires a response both within, and beyond the European Union. With some

economic groups in the financial sector controlling up to 25,000 separate

entities, a need for the unambiguous identification of ownership structures is

evident. The potential of the Legal Entity Identifier to allow

interconnectivity, or even to replace EU-wide separate numbering systems of

domestic legal entities, should be explored. Incentives to keep the data valid

and updated have to be implemented consistently. Measures to ensure integrity

and timely information include ensuring public access to financial statements,

ownership data, and statistics on regulatory and enforcement actions taken by the registries in cases of non-compliance.

The current lack of data on country by country information should be

remedied to construct a level playing field between SMEs and large

multinationals. SMEs often operate in one country and are unable to shield

relevant accounting data from public scrutiny. Large multinational companies do

so by consolidating accounts and structuring corporate networks strategically.

To ensure the continued success of the automatic exchange of tax

information on financial accounts, commitment by participating jurisdictions and

data quality should be monitored. Comprehensive statistics on the data

exchanged by country of account holder, controlling person and bank location

should be published. Public statistics on golden visas and similar programmes

should be made mandatory to protect against the undermining of the effectiveness

of automatic information exchange of financial account information.

Standard statutory tax rate datasets should be complemented with measures of the lowest available corporate income tax rates (LACIT) legally available in jurisdictions, to improve the validity of academic research and policy analyses. Such data on LACIT is provided by COFFERS’ in the Corporate Tax Haven Index.

Recommendation 3: Addressing policy gaps and loopholes

While the European Union has taken many bold legislative steps in

the past years, policy gaps remain that urgently need addressing. In the realm

of automatic information exchange of financial account information, the

effectiveness of the entire system is jeopardised by recalcitrant jurisdictions

and banks that refuse to engage in fully reciprocal information exchanges. To

ensure a level playing field, the EU should consider implementing a withholding

tax policy against non-participating banks that fail to provide full financial account

data on a reciprocal basis, using market access as leverage to ensure

compliance.

Furthermore, the validity of passports issued under golden passport schemes by some members states should be constrained, at a minimum by requiring this status to be declared on the passports and through information exchange protocols. Without this measure, tax evaders and criminals are able to open foreign bank accounts with purchased citizenship to circumvent reporting to tax authorities in their place of primary residence. In order to improve pan-European cooperation in prosecuting cross border tax evasion and money laundering, legislative efforts should be directed towards creating harmonised and clear definitions of both crimes. A pan-European prosecutorial agency for these matters should be instituted. Efforts to counter money laundering through beneficial ownership disclosure need to be complemented by disclosure of legal ownership in all cases. Disclosure requirements should be expanded to incorporate EU real estate and freeport users. Bearer shares should be abolished or immobilised with government authority.

A return to a truly progressive tax system can help prevent the further spread of populist and

extremist movements. Effective cooperation on business taxation supports this. To date no breakthrough in the area of

business taxation comparable to automatic information exchange has been

achieved. A first step t is the speedy enactment of public country by country

reporting rules for large corporate groups. This is as is proposed in a

directive under negotiation amending Directive 2013/34/EU in regard to the

disclosure of income tax information by certain undertakings and branches.

Minimum taxes should complement the

adoption of the Common Consolidated Corporate Tax

Base (CCCTB).

Fundamental corporate tax reforms (towards unitary taxation/CCCTB)

will take some time. They should be

complemented by intermediate policy steps that can be implemented unilaterally

and immediately. Examples of such intermediate steps include the abolition of

patent boxes and notional interest

deductions, the inclusion of capital gains in the corporate income tax base,

constraining loss utilization over time, and the introduction of robust

deduction limitations on intra-group royalty and service payments.

These new EU policy-making efforts should be implemented in a way

that contributes to stronger democracy in the EU. This can be achieved by

establishing channels for the greater participation of independent academics

and civil society organisations in the reform process. Reform should no longer

be dominated by private interests and a closed and technocratic network.

Welcome to the twenty-seventh edition of our monthly Arabic podcast/radio show Taxes Simply الجباية ببساطة contributing to tax justice public debate around the world. Taxes Simply الجباية ببساطة is produced and presented by Walid Ben Rhouma and Osama Diab of the Egyptian Initiative for Personal Rights, also an investigative journalist. The programme is available for listeners to download and it’s also available for free to any radio stations who’d like to broadcast it or websites who’d like to post it. You can also join the programme on Facebook and on Twitter.

Taxes Simply #27 – The Coronavirus and taxjustice

This month Walid Ben Rhouma and Osama Diab discuss the economic consequences of the coronavirus crisis that the world is currently experiencing. They also present the most important tax and economic news from the MENA region and the world, including:

the oil price war emerging between Russia and Saudi Arabia

the European Central Bank is offering 1 trillion euros this year to alleviate the impact of the coronavirus

the MENA region economy may shrink by an estimated 1.7% and the Eurozone by 12.5%

Lebanon defaults on debt repayment

الجباية ببساطة #٢٧ –

فيروس الكورونا والضرائب

أهلا بكم في العدد الجديد من الجباية ببساطة، ونتمنى أن تكونوا بأفضل حال في هذه الفترة الاستثنائية. في الجزء الأول من العدد يتحاور وليد بن رحومة وأسامة دياب حول التبعات الاقتصادية لأزمة فيروس كورونا التي تعيشها العالم حاليا. أما في الجزء الثاني من العدد، نعرض أهم أخبار الضرائب والاقتصاد من المنطقة العربية في العالم في شهر مارس/آذار، وتشمل أخبارنا: ١) حرب أسعار النفط تشتعل بين روسيا والسعودية؛ ٢) البنك المركزي الأوروبي يطرح 1 تريليون يورو هذا العام للتخفيف من وطأة فيروس الكورونا؛ ٣) اقتصاد المنطقة العربية قد ينكمش بمعدل ١.٧% ومنطقة اليورو بمعدل ١٢.٥%؛ ٤) لبنان يتخلف عن سداد الديون.

Here’s the 14th edition of Tax Justice Network’s monthly podcast/radio show for francophone Africa by finance journalist Idriss Linge in Cameroon. Nous sommes fiers de partager avec vous cette nouvelle émission de radio/podcast du Réseau pour la Justice Fiscale, Tax Justice Network produite en Afrique francophone par le journaliste financier Idriss Linge au Cameroun.

Impôts et Justice Sociale, Edition 14 : Malgré ses cadeaux fiscaux, L’Afrique

abandonnée face au Coronavirus

Dans cette quatorzième édition de votre podcast « Impôts et Justice Sociale » nous revenons sur le Coronavirus, et le risque qu’il représente pour les économies africaines. Nous explorons surtout le fait, que la région qui a accordé de nombreux avantages fiscaux aux multinationales qui exploitent ses ressources, et à des pays riches dans le cadre des accords fiscaux avantageux, obtenus de manière agressive, tarde à recevoir un soutien, alors que partout on annonce des milliers de milliards $ de subventions.

Pour en parler

Jean-Bertin Kemajou, il est le président de l’ONG Camerounaise Freedom Service

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

Guest blog by Professor Colin Haslam, Queen Mary University of London

In our working paper Safeguarding financial resilience for sustainability’ we argue that large companies listed on the European and the US stock exchanges have become financialised, leaving many with weak, financially exposed balance sheets and higher risk of insolvency. As the Covid-19 crisis hits, we are on the verge of a perfect financial storm as the European and US financialised corporate sectors have sacrificed financial resilience for shareholder value.

In response to the COVID-19 crisis governments are stepping up to underwrite company liquidity through wage and salary subventions. France, Spain and the UK, for instance, have unveiled emergency packages including direct pay-outs to employees as well as loans and guarantees for companies to mitigate the economic blow from the coronavirus. These economic interventions are about securing the financial stability of companies.

In accounting and auditing practice, company viability is tested by looking at both liquidity and balance sheet solvency. Companies need cash for liquidity to cover everyday business expenses. But to maintain balance sheet solvency, a company also needs a surplus of assets over liabilities, in the form of shareholder equity reserves. These reserves provide a critically important loss-absorbing buffer.

For example, when a company suffers a deterioration in income because of a downturn in product markets, any negative earnings need to be absorbed by shareholder equity reserves if that company is to remain a going concern.

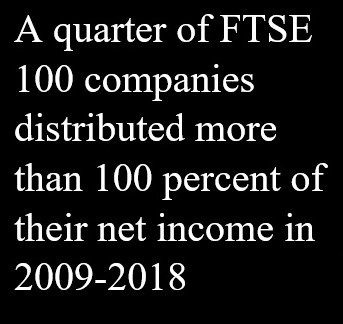

In a financialised company, the primary modus operandi is asset value extraction for shareholders, through paying dividends and buying back its own shares. Aggressive distributions to shareholders can reduce retained earnings accumulated in shareholder equity, undermining the loss-absorbing buffer.

During the period 2009 to 2018 we estimate that net income earned by all FTSE 100 companies was £898bn, while dividends amounted to £571bn and share buy-backs £167bn. So in total, roughly four fifths of total net income was distributed. Nearly half of FTSE 100 companies distributed more than three quarters of their net income, while 25 distributed more than 100 percent of their net income!

This high distribution of earnings is a pattern that resonates across all the major European and US large company quoted stocks. To modify this behaviour, dividends could be added back to earnings for the purposes of calculating corporation tax. Where a company increases debt to fund distributions to shareholders the interest payments on this debt would be treated as being non-tax deductible. Stricter restrictions could include: stronger criteria for what constitutes realised earnings available for distribution to shareholders and changes to the UK companies act, that is, prohibiting company repurchases of their own share capital.

Table: Net income distributed to shareholders as dividends and share buy-backs[1]

Dividends

Share buy-backs

Total

%

%

%

EuroStoxx 600

65

7

72

S&P 500

36

51

87

FTSE 100

64

19

83

Source: Thomson Eikon datasets

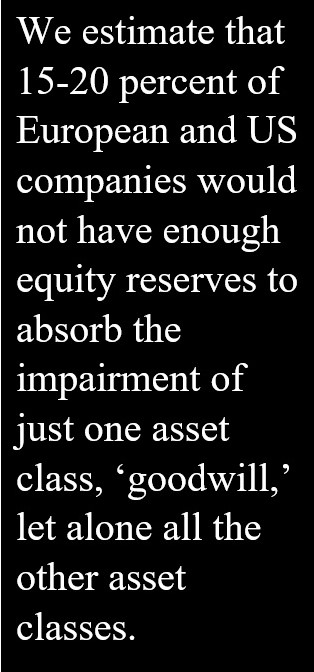

Financialised companies that have

hollowed out their equity reserves are vulnerable not only to losses made in

the normal course of business: they are also vulnerable to impairments of speculative

asset values reported on their balance sheets.

The COVID-19 crisis will undermine company revenues and profits from selling goods and services as we now all lock down. But when company cash flows dry up there will also be a compounding negative impact on asset valuations that have been speculatively “marked to market” as part of fair value accounting (FVA) practices. The current market value of many assets recorded on a company’s balance sheet are speculative valuations. This is because these valuations are based on estimates about future cash flows that may or may not be realised by these assets.

Assets adjusted to speculative

market value include not just goodwill but also property, financial

instruments, hedging products, pension funds, biological assets, brands, patent

and licenses. These speculative asset valuations will also become compromised.

Our working paper reveals that 15-20 percent of European and US companies would

not have enough equity reserves to absorb just one asset class ‘goodwill’ being

impaired – let alone all the other asset classes marked up to speculative market

value.

So what’s to be done? A new social settlement.

The COVID-19 crisis has

resulted in unprecedented state subvention of wages and grants to sustain our

corporate sectors. When this crisis is over it will be necessary to demand corporate

obligations, not just entitlements, attached to the granting of the social

license of limited liability. A new

social settlement will be required, as it will no longer be possible for

corporate governance to operate solely for shareholders.

A starting point would be to

restore prudential resource management, conservative accounting practices, and

the preservation of capital and solvency for a going concern.

Policy interventions should

now:

● Promote a default to historic cost

accounting to limit speculative asset value impairment, and in the short run put

in firebreaks to prevent asset value impairment and its transmission into the

company equity funds.

● Restrict distributable dividends out of

shareholder equity to accumulated realised earnings rather than realised and

unrealised earnings that arise when asset values are inflated.

● Modify company tax law on dividends and

tax deductible interest charges attached to debt finance used to fund

distributions of all kinds to shareholders: adding these expenses back to

compute corporation tax.

● Restrict the capacity of a company to

convert other shareholder equity reserves, such as share premiums, into bonus

issues for shareholders and other manipulations.

● Reform our company’s acts to stop

companies from buying back their own share capital. We need to revert to the

previous common law position prohibiting companies from buying their own

shares.

In this time of crisis it is essential to ensure that, in

the immediate short-run, companies do not liquidate assets because this will

very quickly threaten company balance sheet solvency: a systemic Carillion

effect.

In return for subvention, and beyond this current crisis,

we should now all demand that companies fulfil broader obligations to society

(not just shareholders).

This will require companies prudently safeguarding capital

for a going concern in return for the social license granted by limited

liability.

As economies crumble under coronavirus pandemic, powerful interests are hoping to get rich from huge government bailouts. A well-informed Washington D.C. insider described the latest U.S. bailout package, for instance, as a “corporate coup” to reshape the U.S. economy:

“it’s really really bad, and much of the bad stuff is not being included in the sleazy marketing materials . . [it is] a Christmas wish-list of corporate lobbyists. . . The bill establishes a series of boring-sounding slush funds [with] alphabet-soup names . . that’s where the real money is.”

Economist Gabriel Zucman has described it as literally a $170 billion tax cut for real estate tycoons.

With President Trump declaring that “I’ll be the oversight” for the bailout, and potentially receiving a personal bonanza from it, this looks bad. And the pandemic is giving other authoritarians elsewhere opportunities to erode political freedoms further.

But on the positive side, governments are having to throw out broken old orthodoxies and bring in progressive policies — such as versions of universal basic income, or nationalisations — that would have been unthinkable just a few weeks ago. Everyone is scrambling for money.

In this context, “Michael” in Ireland raised a pertinent question:

“Do you think that it is possible (technically) for governments to tap into the trillions which are hidden offshore?”

To which the answer is: yes, plenty of it. There’s some $8-35 trillion or so sitting offshore, depending on how broadly this is measured, which can certainly be tapped with stronger political will. And we must never forget that while all countries are victims of offshore chicanery, lower-income countries are the worst hit, as dictators and oligarchs loot national treasuries and sew up their economies into private fiefdoms, then transfer their ill-gotten gains overseas and stash it offshore.

Now, in the COVID-19 era, old orthodoxies are crumbling fast, and popular demands for new, radical measures will grow explosively. Already food security for millions of people is threatened, and the worst is yet to come. There will be riots, and worse. We can now, with luck, achieve a lot.

We just wrote about how national tax systems should be adjusted to cope with the Covid-19 pandemic: a large fiscal stimulus, with spending running far ahead of tax revenues — but no blank cheque. The poor and vulnerable should pay less and receive more, while rich people and strong, highly profitable corporations should pay more — a lot more.

So far, according to this OECD list of Covid-19 measures, countries have been radical on the spending side, but not on tapping the wealthy or large profitable corporations. Corporate tax rates on “excess” profits of 50-75 percent? It’s the monopolists, hedge funds and financial engineers that are making excess profits — this proposal wouldn’t hurt fragile companies or ones with low profit margins.

This proposal is nowhere now — but let’s start the ball rolling. And we need a lot more than this.

But first, we must walk through a minefield or two.

The great dilemma

Imagine a large multinational has been aggressively shoveling profits offshore for years, lobbying for and getting tax cuts and state subsidies, buying back its own stock, paying its employees peanuts while delivering its bosses exorbitant compensation. If a company has spent the better part of the past decade enriching its owners and executives, should it get a bailout?

The scale of what’s been happening is shocking. The largest 500 U.S. multinationals, for instance, spent over $1.5 trillion in 2018 and 2019 just buying back their own stock, to boost their share prices and their executive stock rewards. On top of that, they paid out nearly a trillion more in dividends. This has sucked colossal productive investment out of the real economy, and mostly into the pockets of the wealthiest 10 percent of Americans. They monopolised, extracting wealth from consumers, workers, and many others. Then, after gorging on a gigantic job-killing corporate tax cut in 2017 (“I don’t think we’re ever going to lose money again,” an airline boss gushed that year), US corporations alone continued to shift $300 billion in profits offshore each year to dodge tax (and other rules of civilised society.) Luxury cruise lines have been registering offshore to escape taxes and regulations, then sailing on amid pandemic on their own ships. They took huge risks with borrowed money, juicing profits and bosses’ bonuses, and the risks now fall on society’s shoulders. And on, and on.

Do we bail these people out? Do we “foam the runway” for crime-soaked banks if they face collapse? Justice says ‘no.’ But if the consequences of letting these firms collapse is worse still, how do we proceed?

On balance, a company whose collapse will cause social catastrophe should likely be saved. But no blank cheque. Instead, there must be powerful conditions. Here are a few: some of which must continue long after this shock has passed.

A HARD crackdown on tax havens, and more resources for tax authorities. More on this below.

Implement huge – maybe 50-75 percent annual — “excess profit taxes” as our last blog on this argued, targeting only highly profitable firms, and sparing fragile firms. The tax haven crackdown will help stem leaks.

Tax wealth. Hefty wealth taxes, land value taxes, capital gains taxes, and more, with only modest reliefs where appropriate and truly needed. This was in the air before Coronavirus: time to make good.

Don’t bail out investors or large corporations. Bail out people. (These economists explain how and why.)

Nationalise failing firms, or take large stakes in them, where necessary. Buy their stock cheaply now, take control, clean house, and when market conditions normalise, sell many (but not all) of them back, at a profit. This happened after the global financial crisis. Here’s more.

Put unemployed people back to work in a climate-friendly Green New Deal.