The IMF has just published a new Staff Discussion Note entitled “Finance and Inequality,” by Martin Čihák and Ratna Sahay. The shortest summary of its conclusions is: too much finance makes countries more unequal. And in the words of the IMF’s new Managing Director Kristalina Georgieva, introducing the study, rising inequality:

is reminiscent of the early part of the 20th century — when the twin forces of technology and integration led to the first Gilded Age, the Roaring Twenties, and, ultimately, financial disaster.

This is the latest in a now-hefty body of academic research supporting the finance curse thesis: the apparently paradoxical idea that “too much finance can make you poorer.” In other words, countries need to develop financial sectors, but only up to an optimal point, and if finance grows beyond this point it tends to harm the economy and society that hosts it. Many western economies passed this point long ago.

We’ll start with a line fairly deep in the report’s text, which is fairly explosive. In a section on policy implications, it recommends that:

regulatory policies have a role to play in reining in excessive growth of the financial sector.

That’s our emphasis, in bold. Here’s the IMF saying that countries should not allow their financial sectors to grow too big. This recommendation is related to inequality, but the IMF has not only come around to the idea that inequality hurts growth: it has published several reports demonstrating the finance curse thesis: that too much finance hurts overall economic growth (and delivers a payload of other economic and societal damage.) As we’ve said before: shrink finance, for prosperity.

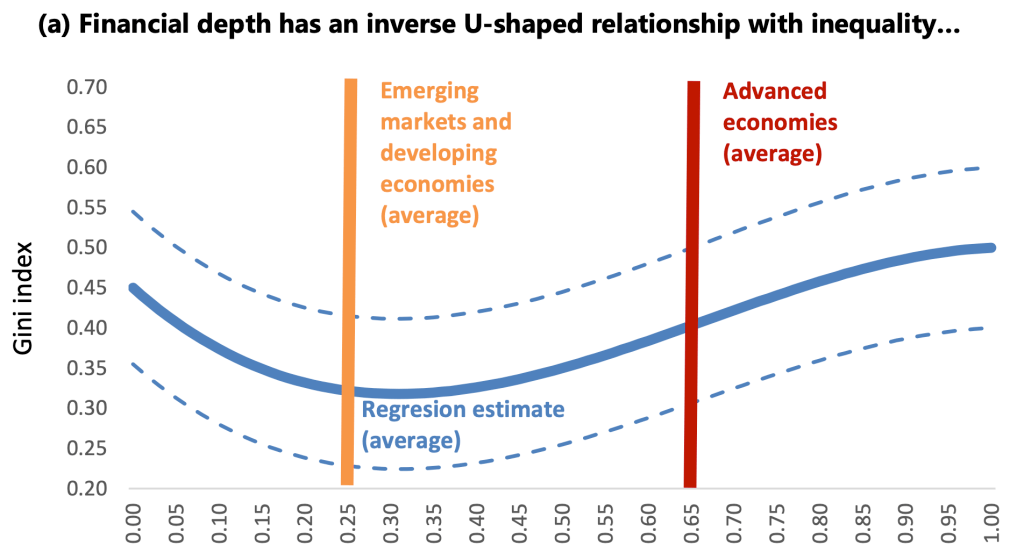

In more detail, this new paper discusses “financial depth,” which means the size of a country’s financial sector relative to the economy. Its headline graph looks like this:

This plots Gini (a measure of inequality, the lower number the better) against “financial depth” (as measured by a special IMF data set) . The report explains it succinctly:

we find that financial deepening reduces within-country income inequality up to a point, after which inequality starts rising. . . the increase in inequality beyond the turning point is not only statistically significant, but also qualitatively meaningful.

This unsurprising conclusion is exactly consistent with the idea that all countries need a financial sector, but after the sector grows beyond a certain point it starts to inflict damage on the economy that hosts it. It is also consistent with a 2018 study from the Bank for International Settlements, which finds that:

Up to a point, more finance reduces income inequality. Beyond that point, inequality rises if finance is expanded via market-based financing, while it does not when finance grows via bank lending.

This new IMF study also finds (also unsurprisingly) that

higher inequality is associated with greater financial risks.

As the IMF authors put it, rises in inequality tend to be accompanied by higher growth in credit. Growth in credit leads to crises. Crises, in turn, lead to higher default rates, making lower-income households worse off and increasing inequality after a crisis. So it’s something of a vicious circle.

The report’s third conclusion, also hardly a surprise, concerns ‘financial inclusion’ – that is “expanding the provision of financial services to low-income households and small businesses”:

greater financial inclusion is associated with reductions in inequality. . . . Both men and women benefit from financial inclusion, but inequality falls more when women have greater access.

In terms of inclusion, it’s access to payment services, not access to credit, that seems to be the inequality-reducing elixir.

Is the IMF still part of the problem?

We heartily welcome this and other research from the IMF, going against years of pro-finance orthodoxy, and we also welcome statements by new IMF Director-General Kristalina Georgieva about the importance of tackling inequality.

But we have some criticisms too. We don’t like the Gini measure of inequality much: it systematically downplays inequality where it matters (at the bottom and very top of the income distribution: we’d have been happier if the IMF had used the UNU-WIDER inequality dataset, which we think contains better quality data, and includes Palma ratios as an alternative to the Gini.

More importantly, as the U.S. inequality expert Sam Pizzigati warns:

Can we expect this new IMF to take the global lead in the charge against economic policies that keep inequality so devilishly entrenched? Unfortunately, no. We’ve seen this movie before, and it didn’t end happily.

IMF bosses have been calling for action against inequality for years, he explains, but at the operational level, IMF officials have “continued to push struggling nations to adopt keep-rich-people-smiling policies.” Or, as Oxfam put it,

“while the Fund is saying the right things on inequality, its policy advice fails to match its research and rhetoric.”

Or, as the Bretton Woods Project put it more recently:

“The more unorthodox views of some IMF staff reports, such as increasing public investments, a higher wealth tax and charging a financial transactions tax, do not seem to have made a dent on policy statements, much less actual policy.”

So: as we push the finance curse thesis, we need to keep holding these institutions’ feet to the fire.

The author

Related articles

Public finance is feminist terrain

She cleans your house but the tax system can’t see her

Joint submission: International financial architecture, debt and the right to education

20 May 2026

Taxing Ethiopian women for bleeding

Tax justice and the women who hold broken systems together

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026

The tax justice stories that defined 2025

Let’s make Elon Musk the world’s richest man this Christmas!

")