Welcome to the 61st edition of our Arabic podcast/radio show Taxes Simply الجباية ببساطةcontributing to tax justice public debate around the world. It’s produced and presented by Walid Ben Rhouma and is available on most podcast apps. Any radio station is welcome to broadcast it for free and websites are also welcome to share it. You can follow the programme on Facebook, on Twitter and on our website.

All our podcasts are unique productions in five different languages: English, Spanish, Arabic, French, Portuguese. They’re all available here. Here’s the latest episode:

في العدد #61 للجباية ببساطة عدنا على أهم الأحداث الإقتصادية لسنة 2022 بدءا بتبعات الصراع الروسي الأكراني وتأثيراته على أسعار الطاقة والمواد الأولية وصولا إلى أزمة الغذاء في العالم وإنعكسات كل هذا على مستويات التضخم القياسية وترفيع نسب الفائدة المرجعية في العالم.في الجزء الثاني من الحلقة، يستضيف وليد بن رحومة، المحاسب القانوني محمد مصطفى للحديث عن الفاتورة الإلكترونية التي أقرتها مصلحة الضرائب المصرية ولاقت رفضا واسعا لدى أصحاب المهن الحرة والشركات الصغرى في مصر.

الفاتورة الإلكترونية بين رفض المهنيين وإصرار مصلحة الضرائب

We’re pleased to share this blog post written by Gurminder K Bhambra and Julia McClure on the upcoming workshop on Colonial Taxation and National Welfare across European Empires, Friday 27th January, 2023, 2-4pm, University of Sussex (also livestreamed on zoom, please sign up here – a recording will also be made available after the event). UPDATE: recording now available here (it’s not great quality but it’s possible to follow most of the speakers)

Taxation tends to be seen as central to the development of the ‘imagined community’ of the nation, clarifying its limits and its boundaries. The assumed national boundaries of the modern state are called into question, however, once we recognize the forms of colonial taxation in place across European empires and the asymmetry of relations between those from whom taxes were collected and those who were the beneficiaries of its distributed returns through welfare.

How did European empires establish taxation regimes that laid the historical foundations for today´s inequalities? How were discourses of welfare used to justify colonial taxation regimes? How have tax structures cemented global inequalities into the post-colonial era? These are some of the questions addressed in the new volume, Imperial Inequalities: The Politics of Economic Governance across European Empires (Manchester University Press, 2022), co-edited by Gurminder K. Bhambra (Professor of Postcolonial and Decolonial Studies, University of Sussex) and Julia McClure (Senior Lecturer in Late Medieval and Early Modern Global History, University of Glasgow).

Imperial Inequalities is a landmark volume that is an open call to arms to focus upon the active role that taxation regimes have played, and continued to play, in creating inequalities both within and between nations. This volume comes out of critical conversations between academics and practitioners in tax justice that were facilitated by an event hosted by the Tax Justice Network in December 2020. The resulting contributions speak to the ongoing significance of deeper understanding of the connections between taxation regimes and inequality. During this event we will hear from members of the Tax Justice Network about the relevance of this volume for current tax justice campaigns and also from some of the contributors to the volume.

The volume draws together scholars from a variety of disciplinary backgrounds (including history, sociology, international relations) and with different regional specialisms (including Africa, Asia, Latin America) to offer insightful case studies of the political discourses and economic objectives that gave rise to certain taxation policies and the long-term impacts of these at both the local and global levels. It offers a critical long-durée perspective of the mechanics of imperialism, stretching from Spanish colonialism in the Americas in the sixteenth century and English colonialism in Ireland in the seventeenth century, to French, British, and Dutch colonialism in Africa, the Caribbean, India, and Indonesia, in the nineteenth and twentieth centuries. It also covers the period of decolonization, and the emergence of tax havens.

The impressive temporal and geographic range of these case studies work together to offer new understandings of the political economy of European empires. They explain the fiscal innovations in colonial and post-colonial economic policies that engineered economic policies and their racial dimensions. They shed light on the moral-political discourses that have been used both to create and to justify these inequalities. These moral-political discourses have variously incorporated themes of charity, philanthropy, justice, and citizenship, and point to the complicated relationships between nations and empires.

Attendees will have the opportunity to ask questions to any of the panelists about their specialist research and contributions to the volume and to participate in the broader conversations around how colonial and postcolonial taxation regimes have created, and continue to create, different forms of inequality, and what policies we need to address these.

Contributors at the workshop:

Gurminder K Bhambra is Professor of Postcolonial and Decolonial Studies at the University of Sussex.

Laura Channing is Assistant Professor of Economic History in the Department of History, Durham University.

Alex Cobham is chief executive of the Tax Justice Network, and a commissioner for the Scottish Government’s Poverty and Inequality Commission.

Paul Gilbert is a Senior Lecturer in International Development at the University of Sussex.

Lyla Latif lectures at the University of Nairobi School of Law and is working on her doctorate at Cardiff Law and Politics.

Andrew Mackillop is a Senior Lecturer in Scottish History at the University of Glasgow.

Julia McClure is Senior Lecturer in late medieval and early modern global history at the University of Glasgow.

Madeline Woker is University Assistant Professor in the History of France and the Francophone World, at the University of Cambridge.

We’re pleased to share this very useful look ahead to 2023 from our friends and colleagues at the Financial Transparency Coalition, originally posted here and written by FTC’s Executive Director Matti Kohonen.

Financial transparency and tax justice: Five key trends in 2023

The year 2023 is going to be crucial for financial transparency and tax justice, as countries around the world desperately seek funds amid multiple crises, whist grappling with the impact of the COVID-19 pandemic. Many global South countries face sovereign debt defaults that will lead them to apply for International Monetary Fund (IMF) loan programmes which are often linked to austerity policies.

Progressive fiscal policy shifts and further advancing financial transparency are absolutely crucial to generate enough resources to reduce the impact of the multiple crises especially among the poor who are often women and minority groups. If we do not tackle financial transparency, kleptocrats and actors engaged in natural resource crimes will not be caught, and billions of dollars in hidden funds will continue to be stolen. But progress is tremendously slow in these areas, and advances that we make are easily lost amid endless legal challenges.

So what are the five main trends to look ahead in 2023 which could help countries face the multiple current funding crises they are facing? Let us take a look:

Meanwhile COVID-19 recovery spending in the global South only reached 2.4% of GDP, a fifth of what was recommended by the UN, and much of the money did not go to those most impacted by the pandemic. As we revealed in the “Recovery at a Crossroads” report launched in September 2022 at the #EndAusterity Festival, only 4% of the funds spent in global South countries went to informal workers, who often represents the majority of the workforce and is largely made up of female workers, whilst 38% went to big corporations. Only 38% of funds went to vital social protection programmes that are key to reduce growing gender and economic inequalities.

In contrast, global North countries spent upwards of 10% of GDP in COVID recovery, and many have long-term recovery spending plans including the EU’s Recovery and Resilience Facility worth over €800bn focusing on green and digital Recovery which will continue into 2026. Meanwhile the US has its Inflation Reduction Act (IRA) spending worth $739bn going until 2032. In the global South, only Chile is likely to continue long-term support policies into 2023 and beyond with a fiscal reform package to tax large corporates and the wealthy. So the big question is whether other global South countries will follow Chile’s path. Yet, there are barriers from this taking place, such as the IMF policy advice, which is often part of loan conditions, recommending to maintain tight fiscal policies due to increasing inflation.

In 2023 we at the FTC will closely monitor initiatives to redress this imbalance especially in the global South, such as the Fiscal Pact for Latin America and the Caribbean proposed by the governments of Colombia and Chile where a key meeting is expected this year to tackle illicit financial flows, and tax abuses in Latin America, pushing also for global solutions. In the Caribbean region, the Bridgetown Initiative led by Prime Minister Mia Mottley of Barbados will seek to reform the World Bank and the IMF to provide more international financing without austerity conditionalities.

International tax deals and the UN

In November 2022, the UN took a historical step to start negotiations on the UN role on tax governance that could possibly lead to a UN Tax Commission. It builds on the ECA declaration of African finance ministers in May 2022, calling for the start of negotiations on a UN tax convention. This step is important as ongoing negotiations at the OECD have not led to significant gains for global South countries in mobilising more revenue by taxing the profits of large multinational companies. These countries including Argentina, Brazil, India, Kenya, Pakistan, Nigeria and Indonesia may even end up losing revenue if they forego existing digital taxes that have a wider scope and a clearer basis for allocating revenue to them, so a lot is at play.

In December 2022, a budget for the tax resolution was recommended to be approved, paving the way then for UN Secretary-General António Guterres to produce a report detailing the options moving ahead. Mr Guterres has already pledged his office’s support to this process, and so by the next General Assembly we can expect an evaluation of the main options and modalities for negotiations to begin.

The resolution was sponsored by the Africa Group in the UN, the wider G77 group of global South countries, and the signatories of the LAC Fiscal Pact may wish to widen its scope. Civil society will make its impact by creating widened support for this initiative, highlighting how little revenue is collected in the global South and will monitor the negotiations at each stage to defend the interests of the global South.

Public beneficial ownership registries and corporate transparency in Europe

The European Court of Justice (ECJ) ruling invalidated public access to beneficial ownership registries in December 2022 which represented a major step backwards in the fight against Illicit Financial Flows. Some EU countries have already closed public access to beneficial ownership registries, while others may keep their registries open with the support of national legislation. The European Commission recognises that journalists and civil society have legitimate interests to access this information, and are likely to propose an amendment to the 6th Anti-Money Laundering Directive (AMLD6) in January 2023.

We find this judgement misguided since it is based on a narrow understanding of the uses of public access to registries, with the rationale only covering existing money laundering and terrorist financing offences. Public access to BO registries plays a key role in the fight against environmental crimes, tax abuse, human rights abuses, and labour market abuses – but none of these were considered by the court as valid reasons for public access to BO data. It is likely that there will be on-request public access for civil society and journalists, but that requires to know already what one is looking for rather than find red flags.

Another important development to keep an eye for in 2023 is the key EU directive on corporate tax transparency, namely public country-by-country reporting (CBCR). This will move towards implementation in September 2023 as it is transposed and becomes part of national law in the 27 EU member states by June 2023, with reporting obligations to start by June 2024. EU member states will be able to make a more ambitious national transposition than what the directive sets as a minimum threshold.

Also the US Securities and Exchange Commission (SEC) accepted that public information on CBCR is a material issue for investors to demand company boards to implement, and shareholder resolutions have followed at Amazon, Microsoft, Cisco and other large multinational companies. In 2023, we will see more shareholder resolutions in the AGM season from April onwards concerning public CBCR, making the case for regulatory moves given that many investors find this information as being highly desirable especially when tax scandals are damaging to companies that work in public contracts.

We at FTC will make a renewed case for public access to BO registries and public country-by-country reporting in the EU and elsewhere based on the need to tackle environmental crimes that are not detected and reported on without the involvement of the public, journalists, and civil society as key users of BO data. Similarly, corporate secrecy of lack of tax reporting harms the enjoyment of human rights to health and education, as secretive private sector service providers in the care economy have been found to conceal their tax affairs.

Fighting environmental crimes through financial transparency

In 2023 we will seek to feed into developments towards a vessel transparency initiative, likely to be discussed both at the FAO Committee on Fisheries or the OECD Committee on Fisheries. Such a transparency initiative is necessary to implement the World Trade Organisation (WTO) agreed ban on subsidies to companies engaged in IUU fishing.

We will also look to develop proposals towards identifying IUU fishing as a natural resource crime both at FATF, as well as at UNODC which are custodians with UNCTAD of the UN SDG indicator on Illicit Financial Flows (IFFs). In Africa, we will seek recognition of IUU fishing as an Illicit Financial Flow at the African High-Level Panel on IFFs. FATF should define the scope of environmental crimes in a new report.

We already saw some progress in 2022 with the US sanctioning the beneficial owners of one of the top companies engaged in IUU fishing, Pingtan Maritime Enterprise Ltd. which we identified in our “Fishy Networks” report launched in October 2022 as one of the main companies involved in IUU fishing.. Importantly, the company was also delisted from the NASDAQ, the US based stock exchange. Yet, Europe, as mentioned above, took a step backwards with the European Court of Justice (ECJ) deeming public access to beneficial ownership registries as being invalid on the basis that privacy of ownership was more important.

Targeting oligarchs and a Global Asset Registry

The Russian invasion of Ukraine in February 2022 has led to multiple countries sanctioning assets of Russian oligarchs including real estate, private bank accounts, yachts and luxury cars. Yet very little of the over US$1 trillion in assets laundered out of Russia in the last three decades has been found so far as much of such assets are hidden under the secrecy of shell companies. The FTC and ICRICT support the idea floated by Mario Draghi to create a registry of all assets, but this Global Asset Registry should not be limited to assets of Russian oligarchs.

The KleptoCapture Task Force was set up on 2 March 2022 in the immediate aftermath of the Russian invasion in Ukraine. But thus far, and based on public knowledge, they have identified mostly yachts, aircraft, sports cars and other high-profile assets belonging to sanctioned Russian oligarchs, which represent just a small part of the shady assets held by these wealthy individuals. This is partly since it largely relies on information that public interest groups, and investigative journalists have aggregated from best available public sources of information which is limited. If the beneficial owners of all assets were public, one would not need such a task force to hunt hidden assets.

In Europe, we see proposals towards registering assets that are not currently covered by the proposed 6th Anti-Money Laundering Directive. Positively, the EU has sought to scope an EU Asset Registry but there is no proposal for to implement this yet.

In 2023, we expect Chile to implement a wealth tax for those with assets over US$4.9 million, making only the very wealthiest to pay such a tax. But all this hinges on having a global asset registry. If assets were on a public registry, it would be much easier to design effective and progressive wealth taxes that would generate much-needed revenue to tackle the impacts of the COVID-19 pandemic and to avert austerity and cuts from being made. 2023 will tell how this fight will end.

Matti Kohonen is the executive director of the Financial Transparency Coalition, a group of 11 international civil society organisations including the Tax Justice Network. Before joining the Financial Transparency Coalition, Dr Kohonen worked at Christian Aid’s Economic Justice Lead Advisor, Oxfam’s Essential Services and Development Finance Advisor and project co-ordinator at Tax Justice Network.

Welcome to our Spanish language podcast and radio programme Justicia ImPositiva with Marcelo Justo and Marta Nuñez, free to download and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónico! Escuche por su app de podcast.

En este programa con Marcelo Justo and Marta Nuñez:

La economía mundial de 2023

La justicia fiscal en el mundo: dónde estamos y adónde vamos.

El poder municipal, una vía para recuperar los servicios públicos privatizados

Quiénes pierden, cuando ganan las grandes corporaciones

Invitados:

Oscar Ugarteche, Director del Observatorio Global Latinoamericano, OBELA, profesor de la Universidad Nacional Autonoma de Mexico, la UNAM y autor de Historia Critica del FMI

As 2022 comes to an end, we would like share our reflections on the Tax Justice highlights of 2022 – a year of shifting power dynamics and increasing momentum. We’ll begin with our CEO Alex Cobham:

Organisationally, this has been a key year with the first major refresh of the board for some years. This high level, globally diverse group is now helping to steer the development of our new strategic framework, and have already contributed in significant areas of our international advocacy and partnership.

A significant milestone for our internationally dispersed team was the first in-person retreat since before the pandemic, reinvigorating relationships and energising us all. The retreat also allowed us to engage with important strategic discussions of the sort that virtual interactions, however well managed, simply cannot provide.

In our global advocacy, we have seen dramatic progress in the fruits of a long-term commitment made by the Tax Justice Network and our allies at the Global Alliance for Tax Justice. At a key strategic gathering hosted by Friedrich Ebert Stiftung in Berlin, in 2017, the two organisations committed to jointly prioritise the creation of a globally inclusive intergovernmental tax framework under UN auspices. Such an aspiration is included in foundational policy documents such as ‘Tax Us If You Can’ (2005), but had not been actively pursued to the same extent as other key elements. With multi-year core funding (from the Ford Foundation in particular), it was possible to make such a long-term commitment to what many – even sympathisers within the broader movement – had thought to be an impossible aim, because of the committed blocking of G77 attempts by OECD member countries. Impossible no more!

This year saw a major breakthrough achieved. After momentum building through a range of UN and other processes, including the High Level FACTI Panel report in 2021, the pivotal leadership came from the May 2022 declaration of African finance ministers at the Economic Commission for Africa summit. This underpinned Nigeria’s shepherding of an Africa Group resolution through the General Assembly, with the result that the Secretary-General has been mandated to produce a report on the options; intergovernmental discussions have been given the go-ahead to start next year; and the 78th General Assembly will debate the issue and consider the formal commencement of negotiations.

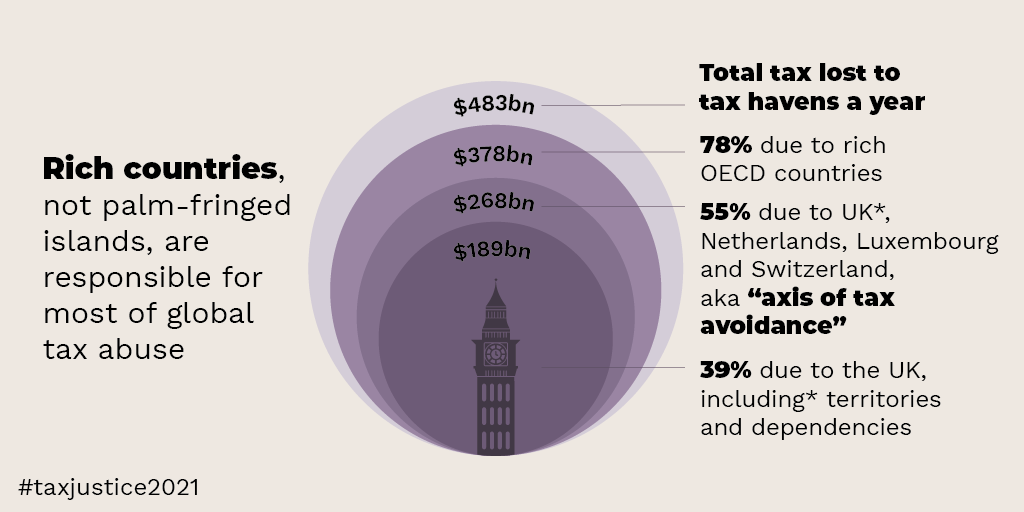

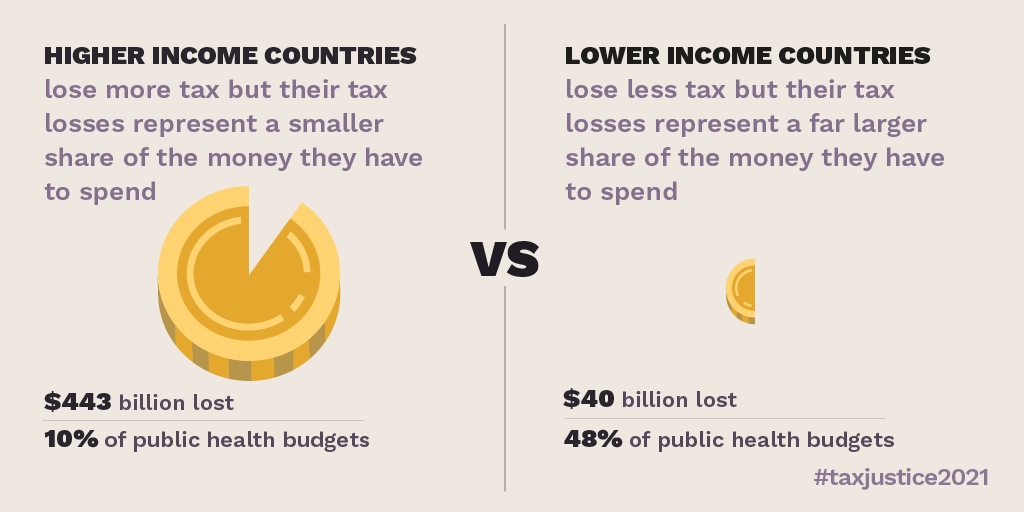

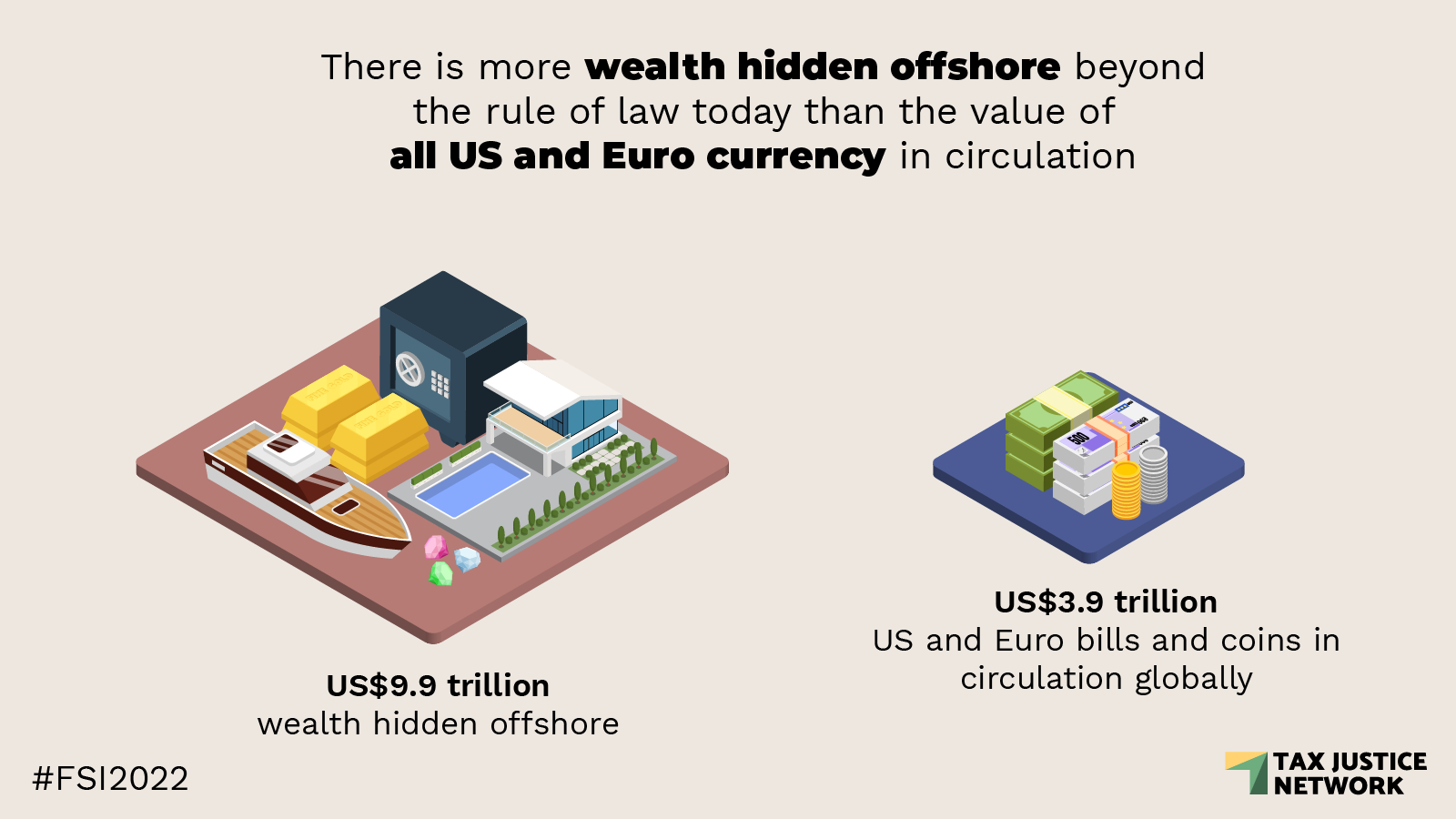

International tax abuse costs the world – in our conservative estimates – US$483 billion, the best part of half a trillion dollars in lost revenues each year. While OECD countries lose the majority of that sum, it is lower-income countries that lose the greatest share of their tax revenues – and for whom that translates most directly into foregone public services upon which people crucially depend. But the OECD has failed to deliver tax reforms that are effective even for its members; and failed to allow meaningful representation for non-members. And as we wrote in an open letter to the G20, the OECD has also failed in its stewardship of a key global public good, in the form of data that is critical for countries to understand and combat tax abuse.

It is no surprise, in this context, that the Africa Group resolution was adopted by unanimous consensus. Some OECD members have signalled they may still be obstructive in the discussions to come, but everyone – including their own citizens – knows full well that the answer lies in a genuinely global process, under UN auspices. You can read more about the resolution here and listen to our podcast here, which breaks down and analyses the power plays in that historic meeting.

In 2023, we will work with allies around the world to support governments in preparing national and regional positions for the intergovernmental discussions, and in holding governments to account to ensure that they take progressive, open perspectives with a focus on curbing tax abuse – not protecting the anachronistic power structure of the OECD.

Tax Justice and HumanRights – Liz Nelson

Austerity has followed quickly on the heels of the pandemic and the related dual crises of inequalities and climate have sharpened our work on human rights. Across all our work human rights resonate. Whether in forging partnerships in advocacy, developing policy solutions, building upon jurisprudence or collaborating on research, overlapping inequalities and human rights failures are our concern. The links to tax justice provide the critical narrative that have guided our successes over the last twelve months and will continue in our new work.

In March 2022 we made a joint submission to the United Nations Human Rights Council Universal Periodic Review (Fourth Cycle). Our focus was the United Kingdom of Great Britain & Northern Ireland (UK & NI) and the issues raised centred on the UK & NI’s poor record on implementation on financial transparency, including in its crown dependencies and oversea territories. Working in collaboration with the Government Revenue and Development Estimation tool (GRADE) at St. Andrews University and our data on tax abuse (2021) we were able to highlight the human rights impact of cross border tax abuse illustrating that the additional revenue lost to tax abuse “would be associated with 36 million people accessing their right to basic sanitation, 18 million accessing their rights to basic drinking water, and almost 7 million children attending school for an extra year. Additionally, this increased access to rights would be associated with over 600,000 children and nearly 80,000 mothers surviving over ten years.”

In November we presented, to the UN CEDAW Committee (Convention on the Elimination of All Forms of Discrimination against Women) a follow up report to our collaboration in 2016 on the impact of financial secrecy and cross border tax abuse facilitated by Switzerland. The Committee recognised the continued failure to address the financial secrecy that keeps Switzerland ranked number 2 at the top of our Financial Secrecy Index.

Our advocacy and research strengthened a valuable collaboration with the Tax Ed Alliance. The Alliance which has a three target country focus and multiple national, regional and international partners, analyses the impact of tax abuse on the right to education. Our research has supported advocacy and provided graphic illustrations, including for the Heads of State Transforming Education Summit, on the how the financing of free public education is negatively impacted by tax abuse.

Our Future is Public (#OFiP22) Conference in November gathered social movements and civil society organisations from all over the world in Santiago, Chile for a 4-day Conference. We contributed to discussions across many sectoral sessions and plenaries aimed at developing strategies and narratives to strengthen public services for the realisation of economic, social and cultural rights and tackle the effects of climate change.(see link here to read the Santiago Declaration).

In September we began our work as a contributing partner to the Demo Trans Research Consortium. Over the next three years will be working with researchers from the universities of Leuven, Charles (Prague), Bergen and Utrecht. The research will explore the interactions between governments and corporations and their impact accountability and on human rights. Demo Trans is funded by the European Commission in its Horizon Europe Framework.

In 2022 we have been successful in attracting funding to bolster our human rights evidence building, and have secured additional funding to explore how tax justice can provide policy solutions for the dual crisises of inequalities and climate justice through an international perspective.

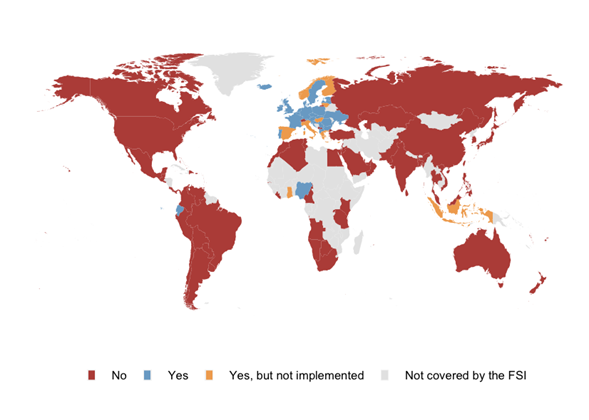

Beneficial Ownership – Andres Knobel

The State of Play of Beneficial Ownership Registration report, based on the Financial Secrecy Index edition published in 2022 shows that almost 100 jurisdictions already have laws establishing beneficial ownership registration, where companies, trusts or other types of legal vehicles must file information to a government authority on their beneficial owners (the natural persons who ultimately own or control them). Mainstream implementation of beneficial ownership registries will also be promoted by the 2022 Reform of the Financial Action Task Force (FATF) Recommendation 24 on beneficial ownership of legal persons in relation to the fight against money laundering and the financing of terrorism.

While beneficial ownership registration has been improved and expanded, the Reform of Recommendation 24 fell short of requiring public access to beneficial ownership information.

An even harsher blow to public access was struck on 22 November 2022 by the EU Court of Justice which invalidated public access to beneficial ownership information in a ruling that caused outrage in the financial transparency movement. While the Court clarified that the media and civil society organisations involved in the fight against money laundering have a legitimate interest to access beneficial ownership information, implementing this type of access has already created many challenges and some EU countries have already closed access, affecting calls and improvements for public access in non-EU countries, including many British Overseas territories. On the bright side, the ruling has woken up civil society actors and regroupings and strategising have already begun to counter the ruling’s effects.

Secrecy – Moran Harari

Financial Secrecy Index: Global financial secrecy has shrunk:

In May, we published the 2022 edition of the Financial Secrecy Index. The results show that the supply of financial secrecy services, like those utilised by Russian oligarchs, tax evaders and corrupt politicians, has continued to decrease globally due to various transparency reforms. However, five G7 countries alone – the US, UK, Japan, Germany and Italy – were responsible for cutting global progress against financial secrecy by more than half. When excluding the increases in financial secrecy from these five countries, the Financial Secrecy Index 2022 finds that global financial secrecy was reduced by 5 per cent.

Public Country by Country reporting:

In October 2022, Australian government showed global leadership in its announcement on a new requirement for multinational corporations to publicly disclose their country by country reporting, a type of reporting method designed to expose and deter multinational corporations from shifting their profits to tax havens. The new requirement was part of Australia’s federal budget for 2022-2023 and the legislation is expected to be implemented by 1st July 2023. The Australian initiative appears to be far broader than the recent EU directive on public country by country reporting -which requires multinationals to publicly report on on activities that multinationals have in Member States as well as in jurisdictions included in the EU list of non-cooperative jurisdictions.

Automatic Information Exchange:

In light of the rapid growth of the Crypto-Asset market, and following a public consultation meeting on 23 May 2022, in which our Andres Knobel participated, the OECD published in October 2022, the Crypto-Asset Reporting Framework (CARF), which constitutes a further improvement to the automatic exchange of information set out by the Common Reporting Standard (CRS). The Crypto-Asset Reporting Framework will require jurisdictions to report on tax information on transactions in Crypto-Assets, with a view to automatically exchanging such information with the jurisdictions of residence of taxpayers on an annual basis. In light of the Crypto-Asset Reporting Framework, the OECD has also made changes to the Common Reporting Standard for it to cover also indirect investments in Crypto-Assets through derivatives and investment vehicles.

Data – Miroslav Palansky

During 2022, the Tax Justice Network made a lot of progress in the area of data collection and infrastructure. The first half of 2022 was dominated by work on the Financial Secrecy Index 2022, which was released in May. The index provides a treasure trove of detailed information on financial secrecy offered by 141 jurisdictions around the world, which is unprecedented in terms of both scope and coverage. All the underlying data is available on the revamped website of the Financial Secrecy Index.

Throughout the year, we have been working on developing a new data portal, which will allow researchers, journalists, or anyone else interested in tax justice to explore, download, and use data collected by us, as well as other relevant variables from various sources. With the data portal, we aim to provide a one-stop-shop for anyone interested in working with indicators of tax havens and financial secrecy. We expect to launch the data portal for public use in early 2023.

Another significant area of data-intensive work was on estimating the scale of illicit financial flows (IFFs) and on identifying the actors responsible for these. We have been developing a bilateral gravity model of financial flows in which we are able to disentangle licit and illicit financial flows by including indicators of financial secrecy and tax havenry. This new approach allows to estimate the scale of IFFs across several different channels and across most countries of the world.

Lastly, we have been busy working with government authorities around the world on analysing microeconomic data (at the firm- or transaction-level) to identify Illicit Financial Flows in order to effectively design policies that mitigate these flows. For example, in Nigeria, we worked with the tax authority to identify companies that most likely engage in profit shifting, and we estimated the semi-elasticity of profits reported by multinationals in Nigeria. We are at various stages of work in several other countries, such as Ecuador, Uganda, and Ghana. We aim to strengthen this area of work further to bring the most possible impact of our work on actual reductions in the scale of IFFs and the resulting tax revenue losses.

The Tax Justice Network reaching people, Communications and media

The Tax Justice Network continued to bring tax justice issues to more people through our media and online work in 2022. Our research and commentary was featured in over 4,600 media and press articles in over 140 countries. Over 344,000 sessions occurred on the Tax Justice Network website in 2022 and our social media posts on Twitter, Facebook and Linkedin had a combined reach of over 1,024,298.

Our podcasts continue to go from strength to strength, each of them unique productions in five different languages, released each month and available for any radio station to broadcast in English, Spanish, Arabic, French and Portuguese. They’re all available here {where you can also subscribe} and you can find them on most podcast apps. We hope to be adding an exciting new regional podcast to our output in 2023…

In 2022 the podcasts have covered many of the developments and tax justice advances mentioned above, along with their significance in each region. We leave you with our English language podcast the Taxcast’s take on the day global power shifted, which gives you a fly on the wall look at the historic UN meeting and vote marking the beginning of the end of the OECD’s sixty-year reign as the world’s leading rule maker on global tax, an encouraging way to end 2022 and look ahead to 2023:

Para promover políticas públicas que garantem direitos à toda população, é preciso investir na administração tributária, que é o órgão que arrecada os recursos para financiar a realização de políticas.

O episódio #44 do É da Sua Conta analisa a destruição das administrações tributárias no Brasil, Europa e Estados Unidos, ressalta a importância de investir nesse órgão fundamental para a realização de políticas, bem como na necessidade de contratação e valorização de herois e heroínas invisíveis e que, neste momento, estão em extinção: auditores fiscais.

No É da sua conta #44:

O desmantelamento da Receita Federal no Brasil, com falta de investimento em tecnologias, cinco mil auditores fiscais a menos, se comparado com 2009, e portanto sobrecarga para os servidores que seguem neste órgão.

Falta de fiscalização e menos serviços à população como consequência direta do desmonte da Receita Federal.

A desigualdade social como consequência do desmantelamento das administrações tributárias: classe média e pobres contribuem com mais impostos e grandes empresas e super ricos escapam da tributação.

A ideologia por trás do desmonte das administrações tributárias: neoliberalismo e austeridade fiscal.

A importância de auditores fiscais e administrações tributárias fortalecidas para uma sociedade mais justa e para uma economia forte que inclua todas as pessoas.

“O que é mais urgente na receita federal é tampar certos ralos de dinheiro público; a receita federal precisa se equipar de pessoas, auditores fiscais motivados com o trabalho.” ~ Isac Falcão, Sindifisco Nacional

“Devemos comemorar os cobradores de impostos. Muitos deles são heróis. Em alguns países, eles são mortos por tentarem cobrar impostos de pessoas poderosas.” ~ Nick Shaxson, Tax Justice Network

“A quantidade de operações que visam elidir as pessoas do pagamento de tributos se torna sempre cada vez mais sofisticada, com cada vez mais estruturas que dão suporte às empresas pra fugirem da tributação. Nesse cenário em que a gente vê investimentos em bancas de profissionais assessorando grandes grupos internacionais favorecendo o planejamento tributário, a Receita Federal do Brasil, vem sendo sucateada.” ~ Patricia Gomes, auditora fiscal

“Administradores tributários servem para corrigir injustiças sociais profundas, para conseguir recolher o dinheiro de grandes bilionários, grandes empresas, grandes criminosos que escondem dinheiro. ” ~ Gabriel Casnati, Internacional do Serviço Público

“A falta de investimento na receita federal é lastimável, principalmente porque afeta a questão da fiscalização. O sistema tem que estar atualizado pra cada vez mais atender a população. Na medida em que há sucateamento da tecnologia integrada, que os sistemas não são atualizados e que não tem investimento isso tudo vai repercutir na vida e no cotidiano das pessoas.” ~ Telma Dantas, Fenadados

Patrícia Gomes, auditora fiscal, presidenta do Sindifisco Ceará (2019-2021)

Telma Dantas, dirigente sindical da Federação Nacional dos Empregados em Empresas e Órgãos Públicos e Privados de Processamento de Dados, Serviços de Informática e Similares (Fenadados)

É da sua conta é o podcast mensal em português da Tax Justice Network. Coordenação: Naomi Fowler. Produção e apresentação: Daniela Stefano e Grazielle David. Agradecimentos: BandTV e Jack Mochila. Download gratuito. Reprodução livre para rádios.

Welcome to our monthly podcast in French, Impôts et Justice Sociale with Idriss Linge of the Tax Justice Network. All our podcasts are unique productions in five different languages every month in English, Spanish, Arabic, French, Portuguese. They’re all available here and on most podcast apps. Here’s our latest episode:

Pour cette nouvelle édition de votre podcast en français sur la justice fiscale et la justice sociale dans le monde, nous revenons sur la rencontre virtuelle d’experts organisée conjointement par Tax Justice Network et Tax Justice Network Africa pour échanger sur la connexion entre la Justice Fiscale et la Justice climatique. Les participants ont répondu aux questions de savoir pourquoi la justice fiscale et la justice climatique devraient être rapprochées et surtout comment financer les deux ambitions.

L’autre thématique du jour parle de l’accès au public des bénéficiaires effectifs en Europe. La Cour de Justice Européenne a estimé que cette possibilité qui existait jusque là pouvait violer d’autres et rendu l’accès à ces registres à condition de montrer un intérêt légitime. Pour de nombreux pays africains, c’est l’opportunité d’une meilleure transparence qui s’efface et cela l’est davantage pour la République Démocratique du Congo, riche pays d’Afrique, mais dont plus de la moitié des 90 millions d’habitants vivent en dessous du seuil de pauvreté. Nous avons posé la question à quelques citoyens de ce pays sur le point de savoir s’ils connaissaient les propriétaires effectifs de leurs mines

Et pour ceux qui ont l’application Stitcher et iTunes ect

Si vous souhaitez recevoir cette production ou être média partenaires ou simplement contribuer, vous pouvez nous écrire à l’adresse Impô[email protected]

With the European Court of Justice (ECJ) ruling ringing in our ears – invalidating public access to beneficial ownership registries – it now seems timely to elevate the recent concerns expressed by the CEDAW Committee (Commission on the Elimination of All Forms of Discrimination Against Women) in their Concluding Observations on Switzerland’s financial secrecy laws. The Financial Transparency Coalition documents how the ECJ ruling: “reversed much of the progress [we] have made in a decade in the fight against corruption, economic and natural resource crimes, tax abuses and other forms of illicit financial flows across the world.”

The perverseness of the ruling illustrates the dangerous environment in which the tax justice movement operates. Moreover, it perhaps illustrates the enormous chasm in understanding of the linkages between financial transparency and economic, social and cultural rights. The ruling places an emphasis on the right to private life, while it fails to consider the importance of public access to company ownership data for purposes of fighting corruption and tax abuses.

The ruling suggests deliberate indifference to the cross-border consequences of financial secrecy on the human rights, such as the foreign ownership of companies and trusts to hide vast amounts of wealth in tax havens like Switzerland. Even if this ruling by the ECJ doesn’t apply to Switzerland, it will make it less likely that the upcoming centralised beneficial ownership registry, which includes also foreign ownership of companies and trusts, are made publicly accessible by Switzerland.

The ruling represents a travesty and a pernicious retrogression. It reminds us that private wealth can, when it chooses, turn legal channels into a weapon to surmount the rights and interests of citizens.

Meanwhile and in parallel, seemingly ‘softer’ law, such as CEDAW, reiterated its concern in the lack of progress that Switzerland has made since 2016 and in addressing previous concluding observations (CEDAW/C/CH/CO/4-5, para. 41 (a)) on Switzerland and the systemic financial secrecy and the threat to rights. The CEDAW Committee comes to this conclusion using evidence from our joint submission with Alliance-Sud and CESR. The Financial Secrecy Index 2022 also corroborates this view in ranking Switzerland number 2 at the top of the Index.

Last month CEDAW published its draft Concluding Observations on their October 2022 review of Switzerland including the recommendation:

“that the State party undertake independent, participatory and periodic impact assessments of the extraterritorial effects of its financial secrecy and corporate tax policies on women’s rights and substantive equality, ensuring that such assessments are conducted impartially, with public disclosure of the methodology and findings.” (CEDAW/C/CHE/CO/6., 2022. Para.22)

Financial secrecy has a profound impact on economic and social rights, and not only on the rights for women and girls. Financial secrecy corrupts democracies, and thus reduces the enjoyment of civil and political rights in a meaningful democratic dialogue. Also, the clandestine influence of wealth and the illicit flow of finance at the bidding of financial crime and wealthy elites, denies opportunities for citizens to determine progressive economic and social policies that work to address inequalities and provide public services for all such as free public education, health and decent housing.

The ECJ ruling resting “on a narrow interpretation of beneficial ownership” and CEDAW’s emphasising of Switzerland’s notoriety as proponents of financial secrecy, underline the retrogression of public scrutiny and government accountability. The ruling should also steel the tax justice, climate justice, human rights movements for an intense and unwavering drive for the establishment of a United Nations intergovernmental framework on tax with the now accepted remit to provide both the design and governance for international taxing rules, transparency and accountability. Such a convention should also address the question of how tax and financial transparency advance the enjoyment of human rights in a broader sense, recognising the impact on economic, social and cultural rights.

We should hold dear ‘soft’ deliberations and recommendations of the UN Treaty Bodies such as CEDAW. They can and arguably should make bold linkages to the nascent UN framework on tax rules in their purpose to provide accountability for economic and social rights, and equality. The basis of well-used and well-regarded ‘softer’ UN instruments is a perfect platform to move towards a ‘hard’ framework that would require commitments to transparency and the genuinely inclusive negotiation of international tax rules.

Co-authored by Liz Nelson, Director, Tax Justice & Human Rights, Tax Justice Network and Dr Matti Kohonen, Executive Director, Financial Transparency Coalition.

Welcome to the latest episode of the Tax Justice Network’s monthly podcast, the Taxcast. You can subscribe either by emailing naomi [at] taxjustice.net or find us on your podcast app.

There’s been a shift in global power, a tax justice milestone, and the most powerful nations couldn’t stop it…

In this episode, Taxcast host Naomi Fowler gives you a fly-on-the-wall take on what happened at the United Nations on November 24th 2022. We look at the power plays around a fundamental global power shift – the beginning of the end of the OECD’s 60 year reign as the world’s leading rule-maker on global tax. Featuring:

The UN Chairperson, UN Secretary and UN representatives of Nigeria, South Africa, the United States, the United Kingdom, Singapore, Liechtenstein, Republic of Korea, and Eritrea.

Produced and hosted by the Tax Justice Network’s Naomi Fowler.

A transcript is available here (some is automated)

~ The Day Global Power Shifted

“It was absolutely incredible to watch the proceedings at the UN to see what was like a boxing match where Nigeria, alongside all other countries that have really been cut out of international tax discussions, stood up and said, ‘this is the time to change the rules of the game’.” ~ Rachel Etter-Phoya

“The resolution really is a kind of watershed moment. The OECD has lobbied its absolute hardest to try to get this blocked. And yet the resolution in the end went through unanimously by consensus.” ~ Alex Cobham

“We look forward to taking further steps as urgently as possible. We have only eight years to realise our ambitious 2030 agenda. We will not achieve it unless we step up the pace of our efforts to reshape multilateralism for the 21st century.” ~ UN Representative for Nigeria

In this month’s Taxcast – it may not sound like it, but this is history being made at the United Nations:

UN Chair: “The committee will now take action on draft resolution L11 rev 1. May I take it that the committee wishes to adopt draft resolution L11 rev 1? I hear no objection. Draft resolution L 11 REV 1 is adopted.” [Bangs gavel]

Naomi: “We’re going to give you our fly-on-the-wall take on what happened at the UN on November 24th 2022. We’re going to look at the power plays around what really is the beginning of the end of the OECD’s 60 year reign as the world’s leading rule-maker on global tax:”

UN Chair: “I call to order the 25th plenary meeting of the second committee at the 77th session of the general assembly.”

Naomi: “OK so usually a meeting with a title like that would make my eyes glaze over. And a vote on a resolution called ‘L11 Rev 1’ wouldn’t exactly set me on fire either BUT, honestly, it’s a fascinating meeting. It’s all the more interesting because of the power dynamics. Because in many ways, we’re witnessing a shift in power. I’ll put a link to the video in the show notes, it kicks off at about 20 minutes in, it’s worth a look. But let’s start by understanding what this resolution is and what nations have just voted for. Here’s Alex Cobham of the Tax Justice Network:”

Alex: “Look, this is a great resolution, and yet it is much less than it could have been, much less than the original proposal from the Africa Group. I think we should say, first of all, what a just fantastic job the Nigerian delegation have done to get this through. I think without Nigeria’s leadership, it’s not clear who else would’ve stood up, and that’s been vital in, in getting this, this really unprecedented success. So even in the state that it went through, the resolution really is a kind of watershed moment. There’s three main elements to it. So first of all, um, most concretely, it calls for the Secretary General Antonio Gutierrez to produce a report on the options for a framework at the UN for intergovernmental discussions and decisions on tax rules. Um, so looking at the options and over the next six months or so, delivering a, a report to the UN.

Secondly, it calls for the beginning of intergovernmental discussions, not negotiations – that got watered down to discussions – but this is still significant. Um, and that we’ll see countries and regions, uh, coming together and starting to formulate their positions on these questions: to what extent do they want to see, uh, a full intergovernmental body on tax under UN auspices? What do they want it to cover? What issues, what aspects from, uh, transparency measures through to rule setting and so on? And what form do they think that should take? So it will effectively begin informally the process of negotiations.

And then thirdly, the resolution calls for and establishes a session in the next general assembly, so from September, 2023 to discuss the Secretary General’s report and to consider decisions, and that’s where you’d expect to see a resolution of the form that this one originally took. That basically fires the starting pistol on formal negotiations, sets out a timetable for those meetings and a budget to support that negotiation process. So that’s been delayed in a sense to next year, but what we’ve already got in place is very significant.”

Naomi: “And the Nigerian representative makes it really clear at this UN meeting about the interference and attempts to water all this down, let’s listen here:”

Nigeria rep: “Nigeria is happy to be taking this historic first step, but we are also troubled that this resolution could not be more ambitious. Most countries find it difficult to accept the legitimacy of international norms of forums that they have no effective voice in shaping. We also have not had a single globally inclusive forum on international tax cooperation. Unfortunately, the enormous pressure put on sovereign countries by the secretariat of another less inclusive international organisation is regrettable, but something we hope we can all move past as we forge ahead together.”

Naomi: “She’s talking here about the OECD, when she’s mentioning pressure put on countries by ‘another less inclusive international organisation’! The OECD does seem to have seen this vote as a paradigm shift that threatens their dominance in the area of international tax, or they wouldn’t have tried so hard to stop, or weaken this resolution, right?”

Alex: “Yeah, it’s funny to hear the Nigerian statements referring to the very significant extent to which, although they don’t name it, the OECD has lobbied its absolute hardest to try to get this blocked. And yet the resolution in the end went through unanimously by consensus. That’s quite a condemnation of the OECD. Uh, in fact, their lobbying was thought by some to be so extreme that it actually put people off voting against this resolution who might otherwise have been more sympathetic.”

Naomi: “So it backfired! Even though the resolution did get passed, afterwards a load of countries, (largely OECD members) then complained about how they weren’t happy about it after all!”

Alex: “Yes I think, you know, from the OECD’s point of view, they’d be pretty disappointed that although these countries are so unhappy, none of them was willing to actually go the whole way and object.”

Naomi: “Ha, no, interestingly they weren’t willing! Joining us to analyse the vote on this historic UN resolution is the Tax Justice Network’s Rachel Etter-Phoya in Malawi. Rachel, what did you make of this UN meeting?”

Rachel: “Naomi, it was absolutely incredible to watch the proceedings at the UN to see what was like a boxing match where the underdog Nigeria, representing the Africa group at the UN, alongside all other countries that have really been cut out of the international tax discussions to stand up and say, ‘this is the time to change the rules of the game, to start negotiations on international tax’. It was so incredible because it is so different from how we’ve seen international tax negotiations over the last few years. The OECD, so the club of the richest nations, former imperial powers, they’ve been setting the rules for the last 60 years. They’ve had their banquet and they’ve been eating at it. They did in the last couple of years try to bring in a few more, but it wasn’t to the banquet table, it was really around it, catching the scraps. And in this so-called inclusive framework, countries were pressured to sign up to things that they maybe wouldn’t have signed up to otherwise. And the African Tax Administration Forum called out political pressure and coercion of members in these negotiations.”

Naomi: “Yes. What’s really striking to me straight away, just visually when you watch this UN meeting is that nations are all there, seated in alphabetical order, so you get Cameroon sitting next to Canada, Nepal sitting next to the Netherlands and New Zealand. Because if you compare that to the OECD, that’s not the case at all for, let’s say, Malawi is it?”

Rachel: “Malawi doesn’t have a seat at this banquet table. It’s not even in the room getting scraps. And there are other countries like this, so you cannot talk about inclusivity if you are not talking about the entire world. And you have to look at the power dynamics in the room and who actually is calling the shots. And even though there are challenges with the UN system, at least every country is sitting side by side.”

Naomi: “Yes! And the African Group of nations have really led the way throughout the process, all the way to the successful passing of this resolution:”

Rachel: “Sorting out the international tax system is really important for everyone and it’s really important for Africa. Africa is a net creditor to the world because of illicit financial flows, flows of money that flow out of the continent illicitly. You might assume that the greatest flows are from criminal and corrupt activity, but actually the high level panel report from a few years back that assessed the scale of illicit financial flows by the African Union saw that 60% of the illicit flows out of the continent are actually through trade. And unless we sort out the international tax system, this is not going to change. Countries have already committed to curbing illicit financial flows, which requires a change in the international tax rules in signing up to the 2030 agenda for development, known as the sustainable development goals. And part of the Addis Ababa action really explicitly states that we need to curb illicit financial flows if we’re gonna be able to finance the development that we need across the world. And this is also really explicit in Africa’s own continental blueprint for development, the Africa we want, which is the Africa Union 2063 agenda. And delegates mention this as a reason for the resolution – that we need to change the tax system to tackle illicit flows. So that’s why it’s so important to hear South Africa reminding all the other UN members in the room that they have an obligation to implement the Addis Ababa action agenda on financing the development goals. And part of that is tackling illicit financial flows, which requires a shake up to the international tax rules because multinational companies are at the moment able to exploit the rules so that they can shift the profits out of the countries where they’re actually doing business, where they’re employing people, where they have the most customers, where they’re extracting resources.”

Naomi: “Yes, and for particularly the smaller, less economically powerful nations, plundered nations, the OECD really hasn’t delivered. Just one example is with the minimum global corporate tax rate of 15% – a while back we saw countries like Nigeria rejecting that for many reasons – not least that it actually undercut their corporate income tax rate of 30%! Here’s the South African representative making a statement strongly supporting Nigeria’s tabling of this UN resolution:”

South Africa rep: “South Africa supports the resolution tabled by Nigeria on behalf of the African Group entitled ‘Promotion of Inclusive and Effective International Tax Cooperation at the UN.’ It is now seven years since the world adopted the first ever target to reduce illicit financial flows including corporate tax abuse following the report of the high level panel on illicit financial flows out of Africa, chaired by South Africa’s former President Thabo Mbeki. This remains of critical importance for global efforts in support of sustainable development goals. Developing countries have for many years been calling for a global intergovernmental process to deal effectively with tax matters. Paragraph 29 of the Addis Ababa action agenda emphasises that member states will increase the engagement on tax matters with a view of enhancing intergovernmental consideration of tax issues. We therefore believe that the time is now to realise one of the important aspect of the Addis Ababa action agenda with a huge potential for scaling up domestic public resources. By supporting the adoption of the resolution before us, member states are indicating their support for an equitable and just world and expressing support for the right to development for all states. A UN tax convention will set global standards and create the mechanism for transparency and accountability to address illicit financial flows and corporate tax abuse amongst others. The UN is the most appropriate venue for this discussion due to its universal membership and all-inclusive character. We therefore call on all member states to support this resolution, thereby recommitting to strengthened international development cooperation. I thank you.”

Naomi: “That’s the South African representative there. In this UN meeting we’re hearing so many representatives saying what a great process the OECD has for achieving better global tax rules for all nations, and how inclusive it’s been!”

Alex: “Yeah, in the debate we are, we are hearing a lot from the core OECD member countries about how the OECD process is perfect and we don’t need anything else, but they’re arguing from a very weak position. You know, clearly the OECD process is not inclusive. The OECD is, you know, in its own articles of association, is required to prioritise the economic interests of its own members, but also the inclusive framework process itself has been widely criticised by pretty much all of the non-OECD member countries in it, because it doesn’t give them a vote, it doesn’t give them an effective voice, they’re really almost just there to, to sign on the dotted line and that’s become increasingly clear. But it isn’t just that the OECD process hasn’t been inclusive, it also hasn’t been effective, so it hasn’t delivered on its own timetable. So, even for the OECD members, I think they themselves know it’s quite a stretch to say that the OECD process has done anything other than really slowly fail and take up lots of people’s time and resources.”

Naomi: “And even though this resolution gets passed unanimously in the end, look what happens here – I mean, the United States makes a last ditch attempt to water it down even further by putting forward an amendment to the resolution for a vote. Here’s the UN chair:”

UN Chair: “An amendment to operative paragraph two of draft resolution L 11 rev one was submitted by the United States of America and circulated in document A/C2/77CRP2. In accordance with rule 130 of the rules of procedure of the general assembly, the committee will take first a decision on the proposed amendment.”

Naomi: “Check this out…”

UN Chair: “I now give the floor to the representative of the United States to introduce the draft amendment.”

Naomi: “And now we get the vaguest explanation of this amendment from the US representative, I think they know it’s going to fail and they’re wasting their time:”

US rep: “Thank you Madame Chair and thank you to the facilitator of this resolution and fellow delegates. I will be brief. Hopefully all have had the opportunity to review the amendment we’ve put forward. Operative paragraph two calls for intergovernmental discussions at the United Nations in the spirit of undertaking a truly inclusive process to strengthen international tax cooperation. For this reason, the United States strongly feels that it is not in the spirit of beginning an inclusive process to prejudge the outcomes of these discussions – in this paragraph, our edit does not preclude any option from the discussions. It simply does not limit the conversation. We hope you’ll consider our amendment. Thank you.”

Naomi: “Erm, Alex, what’s the US trying to do here?”

Alex: “This amendment was really very weak. What it tried to do was to water down the content of the intergovernmental discussions that will follow to make them so vague as to be almost meaningless, so it was sort of a pure wrecking amendment. Word on the grapevine, and, you know, you hear lots of things, so perhaps shouldn’t put too much weight on this, but the word on the grapevine in New York was that the US had been very heavily lobbied by corporate lobbyists. And so they put this amendment down, you know, because they thought they, they should but then didn’t push other countries as hard as the US sometimes does, but I think it’s also there is an absolute clarity a very large majority of UN member states that want this to go ahead.”

Naomi: “So they’re going through the motions without conviction, that is what it sounded like! Er, let’s listen to this – so all the country representatives are now voting on whether or not to accept this US amendment to Nigeria’s resolution:”

UN Chair: “The committee will now commence the process of voting on the amendment on draft resolution L11 rev 1 contained in CRP2. Those in favour of the proposed amendments to draft resolution L11 rev 1 please signify. Can we have the voting screen up? Yep. Perfect. So those in favour please signify, those against, and abstentions.”

UN Secretary: “The committee is now voting on the proposed amendment draft resolution L 11 rev 1 entitled ‘Promotion of Inclusive and Effective International Tax Cooperation at the United Nations contained in document CRP2. Will all delegations confirm that their votes are correctly reflected on the screen? The voting has been completed. Please lock the machine.”

UN Chair: “I thank the secretary. The result of the vote is as follows: in favour 55, against 97, abstentions 13. The proposed amendment to operative paragraph two of draft resolution L11 rev 1 is rejected.”

Naomi: “Ha ha ha, now THAT is something the US is probably not used to – they got voted down!”

Alex: “Yes, I’m sure the US is, is really not used to not getting its own way, including at the UN! It’s also a quite significant sign, just how few countries were willing to back that.”

Naomi: “Hmm. And now that’s out of the way, before Nigeria’s resolution gets voted on, a number of nations are wanting to make statements. Here’s Singapore having its say:”

Singapore rep: “In the current climate, when the UN is expected to address ever more complex and evolving challenges, it is imperative especially for delegations from small states that we avoid duplication of efforts as far as possible and maximise the limited resources available to us. We are also mindful of the important work on this topic already being done at other forum such as the OECD G20 inclusive framework on base erosion and profit shifting and its two pillar solution. It is in this spirit that Singapore engaged in the negotiations in good faith and worked with like-minded delegations to put forward compromise proposals that reflect a delicate balance and diversity of views on this matter.”

Naomi: “Alex, Singapore isn’t an OECD member, why do they seem so against a more inclusive UN forum for deciding global tax rules?”

Alex: “Singapore is a funny one. I mean, it’s kind of long been known that within the G77 group, which is 134, I think, countries of mainly with lower per capita incomes, former colonies and so on, Singapore has very often been the one that stood out on tax issues in particular, and tried to block unanimity. And the G77 operates by unanimity. What we’ve heard, although this hasn’t been publicly confirmed, is that in this case, the OECD actively sought out high level policy makers in Singapore and asked them to prevent a G77 position in favour of the resolution. Now, with Singapore being by far the biggest corporate tax haven even within the G77, perhaps that’s canny politics by the OECD, but it seems pretty destructive and, and really kind of puts the lie to any claim that they’re fighting this because they care about ending tax abuse. You know, you choose your friends and your allies in this game, and they seem to have done that here.”

Naomi: “Interesting! And now the UK’s wanting to speak ahead of the vote on the final resolution. Let’s listen:”

UK rep: “In recent years, we’ve collectively made significant progress at the OECD.”

Naomi: “Er who’s ‘we’?!”

UK rep: “The global forum on tax transparency, the inclusive framework on base erosion and profit sharing and the OECD’s two pillar solution are all significant steps in building a fairer international tax system for all, including developing countries. These initiatives are open to all. Non-OECD members, participate in them on an equal footing.”

Naomi: “Er…I don’t think so! And now the UK representative’s making it clear they voted in support of the US’s amendment, that’s the one that just got voted down:”

UK rep: “On the present resolution, we voted in favour of the amendment because the original language prejudges new initiatives at the United Nations which could duplicate and potentially undermine existing OECD work.”

Naomi: “A lot of nations use this word ‘duplicate’ over and over throughout the session, which is quite interesting. Time for the vote now, the actual vote on the actual resolution…”

UN Chair: “The committee will now take action on draft resolution L11 rev 1. May I take it that the committee wishes to adopt draft resolution L11 rev 1? I hear no objection. Draft resolution L 11 REV 1 is adopted.” [Bangs gavel]

Naomi: “Now, you’d think that would be that right? This historic resolution is passed, it’s passed by consensus, so it’s unanimous. But then there are quite a lot of sulky, antagonistic statements from some countries which, after all, have just agreed to pass the resolution, right Rachel?”

Rachel: “So what I found fascinating at the proceedings was that after the US’s blow didn’t really land and didn’t wipe out the strong resolution, and then all the nations by consensus passed the resolution that is going to pave the way for tax negotiations to happen at the UN, there was a series of speeches given like additional blows, as if the match hadn’t ended. It was quite incredible, countries were laying their cards on the table. So we saw OECD member states talk a lot about duplication of efforts because they say that through their programme BEPS, which is base erosion and profit shifting, that they’ve been working on this and that the UN shouldn’t duplicate the efforts, but as we know, these, these efforts at the OECD have not been inclusive. So you have countries that enable the most financial secrecy according to the Financial Secrecy Index, I mean the notorious tax havens like Singapore, the US, Luxembourg, coming out after the resolution has passed to sort of throw punches in the air and say, ‘we don’t like this because it might duplicate efforts’ or ‘it’s gonna cost a lot of money’ and still trying to defend their banquet table as inclusive, as effective. And you have to imagine the other delegates in the room who are not at that banquet table or maybe just around the edge of that table in the inclusive framework who are shaking their heads inside.”

Naomi: “Yeah, we saw one nation after the other, overwhelmingly OECD member states, using this UN forum to kind of parrot very similarly worded objections about a resolution they all just reluctantly passed, it was like they were all reading from the same page!”

Alex: “This point we are hearing about, you know, the potential duplication of the OECD process, about the scarcity of resources. I mean, this is really, it’s not a question for UN member states, it’s a question for the G20 to consider. It gave this mandate to the OECD to set these rules in 2019, even after the OECD had effectively failed in the first attempt from 2013 to 2015. The G20 countries have given the OECD an enormous amount of resources to do this, while at the same time, the core members of the OECD have repeatedly starved the UN system, including the UN tax committee of any resources to do its job. Oh, and let’s not forget the inclusive framework member countries have been required to pay the OECD for their membership at a table where they don’t have an effective voice or vote. Um, you know, so we should be thinking about their scarce resources, and we should very much be encouraging them to allocate those scarce resources to a process where they do have the chance of an effective voice and effective vote. And that’s only gonna happen, uh, at the UN. So this isn’t an argument that that really holds any water at all.”

Naomi: “No. And after the resolution is passed, the US representative gives a pretty strong and disappointed statement, listen to this:”

US rep: “The United States joins consensus, but wishes to clarify its position on critical issues related to this resolution. We disagree with the notion implied by this resolution that there is not presently a highly inclusive forum working to strengthen international cooperation on tax. A United Nations intergovernmental process proposes a process that will tear down much of the progress that has been made in international tax cooperation since the 2008 to 2009 financial crisis and will undermine the inclusive framework at the OECD through which so much progress is being made. For that reason, the United States must dissociate itself.”

Naomi: “Ouch! Sore losers! Remember that part of the resolution calls for the UN Secretary General to make a report on the next steps to enhance tax rule setting leadership at the UN, something the Secretary General has supported. The US doesn’t like that:”

US rep: “We feel calls for a new report by the Secretary General at this time are inappropriate. Establishing a UN-headquartered open-ended ad hoc intergovernmental committee to recommend new actions will undermine efforts both to stabilise the international tax system and help it become fit for purpose for the 21st century. Thank you.”

Naomi: “Hmmm. And as for what the Liechtenstein representative says, I really can’t take this seriously:”

Liechtenstein rep: “Madame Chair, the strengthening of international corporation on taxation matters has been a longstanding priority for Lichtenstein. As a member of the global forum on transparency and exchange of information for tax purposes as well as the OECD G20 inclusive framework on base erosion and profit shifting, Lichtenstein is committed to international collaboration to tackle tax avoidance, ensure a more transparent tax environment and strengthen the rule of law.”

Alex: [Laughs] “Yeah, Liechtenstein, I mean, Liechtenstein has for a long time at the UN, been very much at the forefront of European jurisdictions fighting any kind of tax or transparency progress. To hear them say, you know, ‘we are against this because we are really strongly with the OECD’s efforts against tax abuse,’ you know, really confirms just how far jurisdictions like that, that are so heavily involved in facilitating tax abuse see the OECD process as being on their side, you know, the rest of us can draw our own conclusions!”

Naomi: “And Rachel, your personal favourite – or I should really say unfavourite statement after the resolution was passed is from South Korea?”

Rachel: “I found it quite astonishing to hear South Korea in quite a patronising manner, say that the Africa group had not followed the correct process in drafting the resolution. They even explicitly stated, this delegate from South Korea, that they do not agree that an inclusive discussion can take place only at the UN. I mean that’s convenient to say when you’re sitting at the OECD’s banquet table, isn’t it?!”

Naomi: “Ha, exactly! Let’s hear what the representative of the Republic of Korea has to say on the drafting of the resolution:”

Korea rep: “It was deeply unfortunate to see in the first place a draft simply tabled to establish a new legally binding mechanism without any preparatory work to accommodate different views and identify common ground. The draft, which was supposed to serve as a basis of the negotiations only referred to unrealistic promises to create a new mechanism and ignored all relevant achievements, efforts and progress accumulated over a very long time. This year’s process should not constitute the precedent for our future process and must not ever be repeated again. The Republic of Korea agrees on the need for ensuring more inclusiveness and effectiveness in international tax cooperation. My country, however, does not agree that an inclusive discussion can take place only at the UN. The discussion should be guided by a pragmatic and effective approach instead of a political and simplistic one. We may have to ask ourselves if such a rush to launch of the UN consultations could promote and advance the relevance of the UN and ensure genuine inclusiveness. It might be convenient and easy to rely only on binary views like developed and developing when we see the world, but especially for tax matters, with such an approach we are certain that we’ll not be able to reach any meaningful outcome.”

Naomi: “Wow, she’s being quite rude there in saying the African Group of nations brought this process forward in a rush, and in a simplistic way, they’ve been working on this for years!”

Rachel: “And some explicitly say that ‘actually what you’re saying isn’t correct.’ I mean, the Eritrean representative speaking on behalf of the Africa Group says that we need a space that has equal footing for tax negotiations, clearly meaning that the OECD’s process and inclusive framework is not that.”

Naomi: “Right, here’s the Eritrean representative:”

Eritrea rep: “Tax-related illicit financial flows inclusive including tax evasion and avoidance are global problems and require global solutions and global cooperation, and no other multilateral fora is better than the United Nations to address such challenges and provide inclusive solutions. Effective international tax cooperation remains neglected in the global economic governance and needs concerted joint efforts to bridge that gap through a comprehensive United Nations framework on tax. Developing and developed countries need to join forces in pursuit of just, global UN-led solutions. The African group stresses the need to promote tax cooperation and the establishment of a governance structure where all member states can participate on an equal footing, contrary to the structures that we have today. The group stress the need to reinforce the global fight against illicit financial flows, including tax avoidance and evasion by increasing transparency and cooperation between governments and by creating more coherent and less complex global tax rules, standards and structures that fully take into consideration the interests, concerns and needs of developing countries. This resolution is a milestone toward ensuring a high standard of transparency. The resolution aims to ensure cooperation among all member states to establish one coherent global system designed to work for all countries, and not just a few.”

Rachel: “And I guess at the end of it all, after all is said and done, Nigeria’s representative speaks so powerfully about how historic the resolution is and what it means to the sovereignty of African nations and other nations who finally have a place at an inclusive table.”

Nigeria rep: “Madam Chair, Nigeria’s presidency of the 74th General Assembly had jointly convened with Norway as President of Economic and Social Council, the high level panel on financial accountability, transparency and integrity for achieving the 2030 agenda. One of the recommendations made over a year ago was a need for a fully inclusive and effective international tax cooperation at the United Nations. Madam Chair, African ministers publicly have stated their desire for a United Nations tax convention six months ago. We look forward to taking further steps as urgently as possible. We have only eight years to realise our ambitious 2030 agenda. We will not achieve it unless we step up the pace of our efforts to reshape multilateralism for the 21st century. I thank you.”

Naomi: “That’s the Nigerian representative. Alex, will this resolution really help African and other nations do that? I mean we can hear in this session from the US and many others, that although this resolution was unanimously passed by consensus, things seem far from consensus, some of the world’s most powerful countries don’t like this at all – what are the battles ahead now, hopes and challenges?”

Alex: “This is such an important question. Again, I want to reiterate what a great job Nigeria has done with the full backing of the Africa group. And they’re really right to say there’s only eight years left, almost, you know, eight going on seven. The sustainable development goals were inaugurated in 2015 and included the first ever commitment to curb illicit financial flows, including from the panel chaired by Thabo Mbeki, the high level panel on illicit financial flows out of Africa, they’re dominated by corporate tax abuse. So it’s really crucial that we get policy progress in that area. We also have within the sustainable development goals, tax identified as the primary means of implementation. So, everything that the world has committed to in terms of the 2030 agenda really depends on effective progress against the international tax abuse that drains the world of perhaps half a trillion dollars in revenues every year and forces inequalities systematically higher.