We’ve said this before, and we may have felt radical saying it at the time – but now it’s The Economist saying it. It has an article entitled and subtitled A senseless subsidy: Most Western economies sweeten the cost of borrowing. That is a bad idea.

We’ve said this before, and we may have felt radical saying it at the time – but now it’s The Economist saying it. It has an article entitled and subtitled A senseless subsidy: Most Western economies sweeten the cost of borrowing. That is a bad idea.

Quite so. And the potential rewards it outlines from doing so are incredible.

There are the tax revenues, for one thing: it estimates that the subsidy cost the equivalent of 2-5% of GDP in tax revenues in rich countries by the time the global financial crisis struck. But here is another massive reward for countries suffering from financial ‘capture’:

“Around the world banks would shrink.”

That, in itself, would be a massive benefit.

What is more, this subsidy (often via housing markets) contributed in a big way towards the build-up of private sector debt that helped bring on the global financial crisis and its ongoing aftermath.

In short, you borrow money (to buy a house or finance a business investment), then pay interest on that borrowing. The subsidy happens when your government (all too often) allows you then to deduct that interest payment against taxes, as a cost. As a result of this perk you’re more likely to borrow money, in contrast to other ways of financing these things, which aren’t tax-deductible.

The conventional response to this distortion is based on the half-baked ideas that this fosters ‘investment’ and that it is quite reasonable to ignore the costs associated with the lost tax revenue and the build-up in debt and an engorged, rent-seeking financial sector. If you think tax revenues don’t matter one jot, then you will (like the IMF and many others) push for cutting taxes on equity returns, and leaving the debt feeding trough subsidy in place too.

So it’s refreshing that The Economist sails in the other direction: the right direction. End this gigantic and senseless subsidy, it says, in no uncertain terms.

The historical anachronism that debt should enjoy tax perks “emerged as much by accident as design,” it notes, and says that tax breaks for debt are embedded in all economies and “viewed as the natural order of things.”

And it adds:

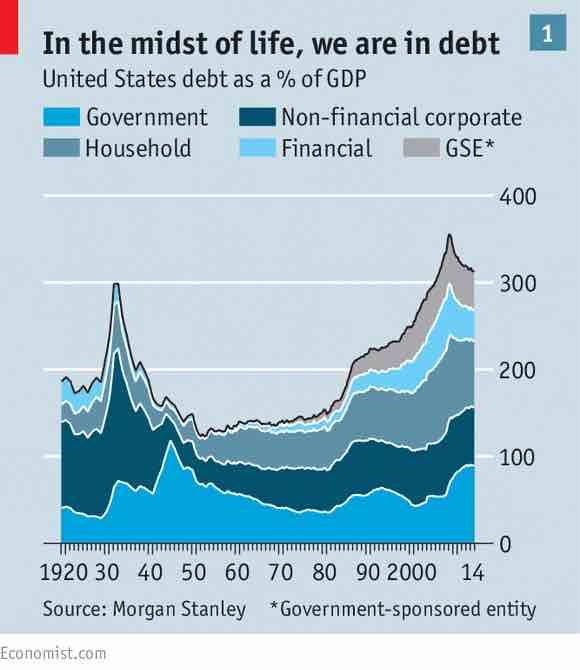

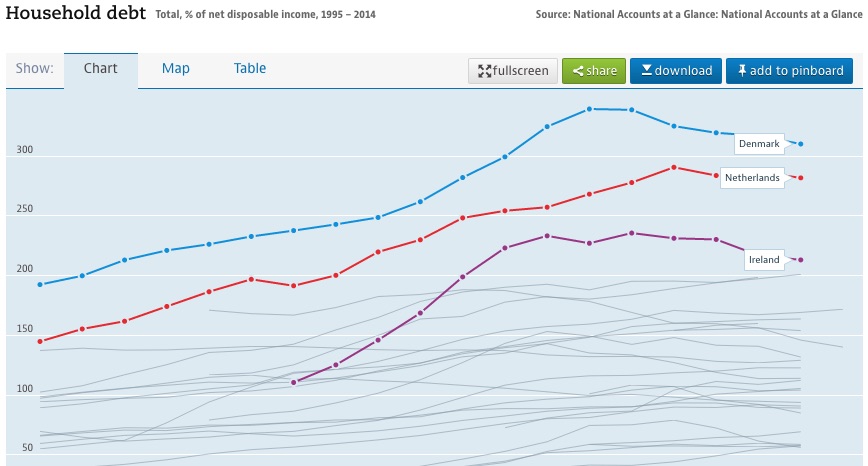

“Beyond a certain point, though, debt seems to be bad for the economy. The Bank for International Settlements (BIS), a club of the world’s central banks, reckons the threshold is 85% of GDP for household debt, and 90% of GDP for non-financial corporate debt.”

Where do rich countries stand? Well, far above these levels, in most cases:

Source: OECD national accounts

And why is too much debt harmful? It identifies two big problems. First, it is hugely wasteful, and crowd out good jobs and genuine productive activity.

“In the rich world most new debts do not finance new productive assets like factories or machines; they just reshuffle claims on existing assets. But these debts still need a big financial industry to administer them, says Stephen Cecchetti, now of Brandeis International Business School and before of the BIS. That sucks resources from the rest of the economy.”

Second, it creates greater financial fragility, as should be obvious. But there’s an interesting twist: with greater fragility comes (again) a more fragile financial sector, which means greater reliance on the public ‘too big to fail’ subsidy that ends all too often in public sector bailouts of the banks.

There is lots more in this excellent article. We’d just make one final comment here. They say, in light of how making debt tax-deductible distorts corporate behaviour:

“The purest option is to abolish corporate tax entirely—and instead have one layer of tax levied on the income individuals receive from investments in firms. That would remove a vast amount of complexity from the system and limit the incentive for tax-dodging and lobbying by firms. But cutting corporate taxes would be politically toxic at a time of stagnant wages for many workers around the world.”

They are quite right to reject abolishing the corporate tax. But they have massively undersold that reason. Inequality is just one of ten huge reasons to defend the corporate income tax.

If you haven’t already seen it, read all about that crucial subject here.

The author

Related articles

The Financial Secrecy Index, a cherished tool for policy research across the globe

New Tax Justice Network podcast website launched!

Como impostos podem promover reparação: the Tax Justice Network Portuguese podcast #54

Convenção na ONU pode conter $480 bi de abusos fiscais #52: the Tax Justice Network Portuguese podcast

As armadilhas das criptomoedas #50: the Tax Justice Network Portuguese podcast

The finance curse and the ‘Panama’ Papers

Monopolies and market power: the Tax Justice Network podcast, the Taxcast

Tax Justice Network Arabic podcast #65: كيف إستحوذ الصندوق السيادي السعودي على مجموعة مستشفيات كليوباترا

Remunicipalización: el poder municipal: January 2023 Spanish language tax justice podcast, Justicia ImPositiva