Published:

23 June 2026Reading time:

7 minIn a world where we push people crossing seas in small boats back into dangerous open water and build ever higher walls to keep out people who seek a better life, the commodification of citizenship and residency and the selling of golden visas to the richest raises serious moral concerns. The Golden Visas indicator of the Financial Secrecy Index shows that the practice of investment immigration also raises serious financial secrecy concerns.

The ‘Golden Visas’ indicator assesses the financial secrecy risk posed by investment immigration by scoring countries on two separate components: how strict or lax their rules on citizenship and residency are (based on whether they offer golden visa programmes), and the comprehensiveness of their personal income tax regime. Given that the interaction of the two components can trigger additional secrecy risks, countries are also scored on the combination of scores they get on the two components.

So, if a country scores badly on the first component and badly on the second component, it gets additionally penalised in its total score for the indicator. That’s because the risk of an individual pretending to be resident in another country just to underpay personal income tax someplace increases if said country has both weak citizenship and residency rules and weak personal income tax rules.

Golden visa programmes can create significant financial secrecy risks by providing opportunities for money laundering, tax evasion and the circumvention of transparency measures.

Below, we provide more details on the indicator’s components and on the results of our most recent assessment of the 141 jurisdictions covered by the Financial Secrecy Index.

Strict or lax citizenship/residence rules

One of the aspects assessed under the Golden Visas indicator is whether countries have strict or lax citizenship or residency rules based on any available citizenship by investment (CBI) or residency by investment (RBI) programmes. These programmes grant citizenship or residency if the applicant makes a passive investment in the country (eg in purchasing local real estate, shares in local companies, or bank deposits or donations). We consider these rules to be lax and pose risks if they do not require sufficient physical presence.

Citizenship or residence by investment programmes without the requirement of sufficient physical presence are known to provide a range of opportunities to hide assets, mask suspicious high-value transactions or enable the movement of significant sums of illicit funds across the borders. These risks are well documented, including by the OECD and the FATF in their recent publication on ‘Misuse of Citizenship and Residency by Investment’.

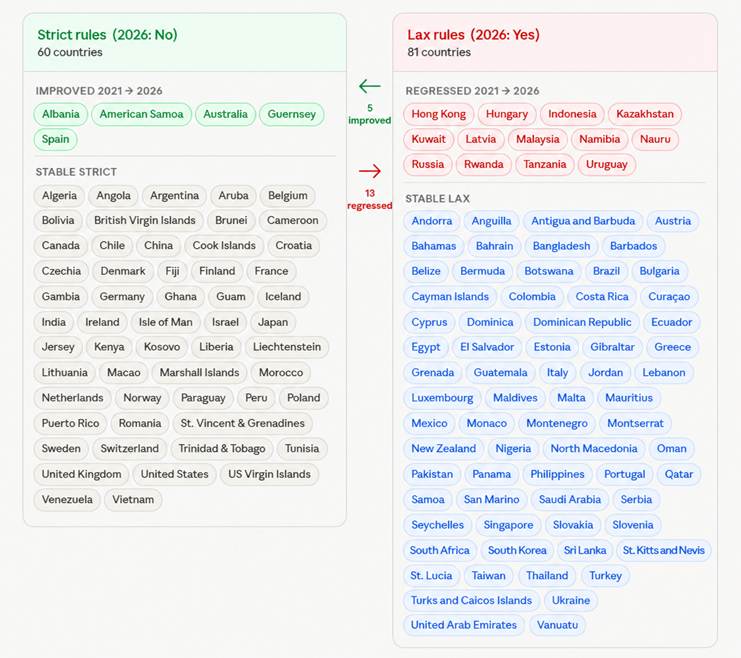

Our findings show that the number of jurisdictions assessed as having lax citizenship or residency rules increased from 73 out of 141 jurisdictions in 2021 to 81 jurisdictions in 2026.

Worryingly, among those countries having regressed into the adoption of lax citizenship/residency rules are a significant number of Global South countries. Countries like Namibia, Nauru and Rwanda have historically stayed clear of polices that score negatively on the Financial Secrecy Index, consistently landing them in the bottom half of the index’s ranking. The regression on citizenship/residency rules is out of character for the countries financial secrecy risk profiles.

Countries often adopted lax citizenship/residency rules under the impression that doing so has the potential to boost domestic resource mobilization through investment migration. It is not disputed that there is money to be made by countries in the sale of golden visas. Citizenship by investment passport sales in Dominica, for example, are reported to have accounted for up to one third of the country’s gross domestic product in recent years. However, as noted by the IMF in a recent study, countries should be wary about expecting similar revenue windfalls based on anecdotal evidence. The authors conclude that for most countries, the likely effects of golden visa programmes may not be beneficial and might be outright harmful. A recent study by the United Nations details how criminal groups in Southeast Asia are increasingly targeting citizenship by investment schemes in the region to circumvent law enforcement.

Comprehensive personal income tax (and the lack thereof)

For a personal income tax to be comprehensive in its scope, it needs to apply the same tax base rules – a rate above zero per cent – equally to all natural persons considered tax residents, including all income from any sources across the world. Any opt-out from the general tax regime in a certain jurisdiction (eg lump sum taxation, tax exemption on foreign-sourced income, territorial tax base or taxes on a remittance basis) results in the jurisdiction being considered by the indicator to not have a comprehensive personal income tax. It can also be the case that the country does not even levy a personal income tax.

The number of jurisdictions without a personal income tax is 17, 15 of which offer golden visa programmes. This combination of components presents a significant problem to automatic exchange of information, as will be explained below.

Avoiding the Common Reporting Standard (CRS) and Crypto Asset Reporting Standard (CARF)

Since the inception of the Common Reporting Standard (CRS) in 2014, the Tax Justice Network has consistently warned that the combination of citizenship and residency by investment regimes and low or no personal income tax in a country creates a specific risk for abusive behaviour, namely Common Reporting Standard avoidance. With the Crypto Asset Reporting Standard (CARF) coming into for this year, this risk of avoidance now also extends to the new standard.

Avoidance of reporting under either standard can take place if the owner of a financial account or crypto wallet in Country A obtains a golden visa in Country B and uses their new passport to record Country B as their country of residence for reporting purposes under the standards. Country B will receive the automatically exchanged information on taxable income and assets. If Country B does not levy income tax on the offshore income and assets, the information is exchanged but not used. At the same time, Country A, the genuine residence country, will be left in the dark regarding its resident’s foreign finances.

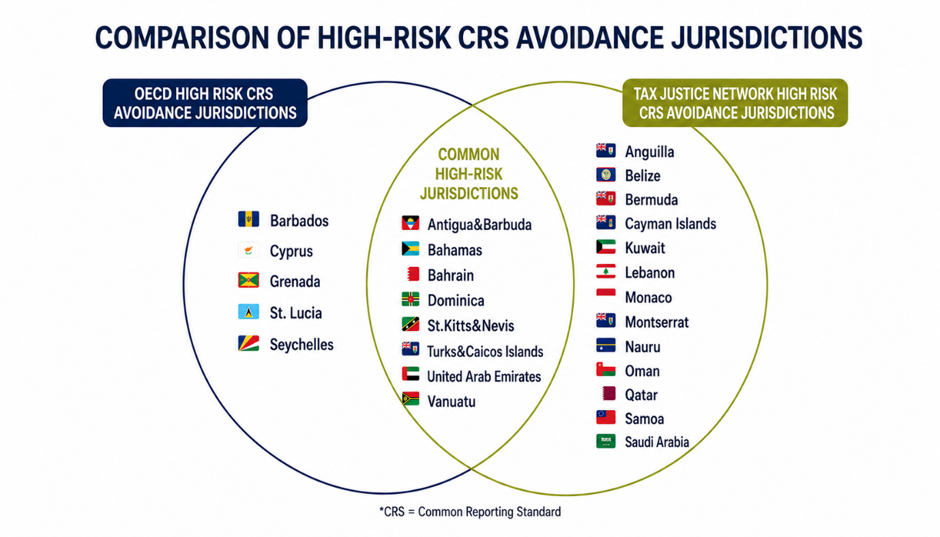

The OECD, aware of the abovementioned risk, keeps as of 2018 an updated list with jurisdictions that operated citizenship and residence by investment schemes that can potentially be abused for to avoid reporting under the Common Reporting Standard. Jurisdictions are listed if they give a taxpayer access to a low personal income tax rate of less than 10% on offshore financial assets and do not require significant physical presence of at least 90 days in the jurisdiction offering the citizenship and residence by investment scheme (see OECD FAQ). Based on this methodology, 13 jurisdictions are currently listed.

The Golden Visa indicator casts a different and wider approach to identify jurisdictions that pose a high-risk of Common Reporting Standard avoidance. Under the indicator, high-risk jurisdictions are those that have a citizenship and residence by investment scheme that does not require 183-day physical presence, and have either a complete absence of personal income tax or active choose ‘voluntary secrecy’ under the Common Reporting Standard. As explained in detail in the indicator on automatic exchange of information, voluntary secrecy jurisdictions participate in the Common Reporting Standard but have actively opted out of receiving information from other jurisdictions on their residents’ offshore accounts.

As a result, the indicator identifies a larger and different group of jurisdictions that potentially pose a high risk to the integrity of the Common Reporting Standard than the group of jurisdictions listed by the OECD. This larger group of high-risk jurisdictions consists of the jurisdictions that score a maximum secrecy score on the indicator.

It also means that certain jurisdictions listed by the OECD as high-risk are not considered to be high-risk (or highest-risk) by the Financial Secrecy Index and vice versa. Monaco, for example, is considered a high-risk jurisdiction under our indicator because it has no personal income tax and a golden visa regime that requires only 90 days of presence. These 90 days are sufficient for the OECD to consider Monaco non-risky. The opposite is true for Cyprus. Cyprus has a problematic golden visa regime earning it a high-risk grading by the OECD, but because it has a personal income tax (albeit with important exemptions), the indicator qualifies it as less risky.

In total, we have identified 21 jurisdictions that pose a high-risk for avoiding the Common Reporting Standard. New additions on the list of high-risk citizenship and residence by investment regimes are Kuwait and Nauru. Both countries are exercising voluntary secrecy under the Common Reporting Standard, and have recently jumped on the citizenship by investment (Nauru) and residency by investment (Kuwait) bandwagons.

Conclusion

Investment migration and especially the role played therein by golden visas is a controversial topic, as their issuance does not equate physical relocation of individuals. It usually means applicants obtain a secondary place of residency or citizenship, with the associated risk that the golden visa will be abused for nefarious purposes, like money laundering and tax evasion.

The new data under the indicator reveals two things. First, the number of jurisdictions with ‘lax’ citizenship/residency rules remains high. A number of countries have abolished their questionable citizenship and residence by investment regimes, whereas a slightly bigger number have introduced new ones. Another worrying trend is that these newcomers include Global South countries not generally known to be financial secrecy hotspots. Domestic resource mobilization through citizenship and residence by investment is not a good idea, however.

Meanwhile, countries have also not been addressed gaps in their personal income tax systems over the past five years. There is no significant change in the number of countries whose personal income tax systems are not comprehensive or who do no tax income altogether.

Second, the total of countries with lax citizenship/residency rules combined with the absence of personal income tax or the choice for voluntary secrecy under the Common Reporting Standard also remains high at 21 jurisdictions. The indicator shows that the financial secrecy risk caused by citizenship and residence by investment is of a wider scale than that estimated by the OECD and remains as problematic as ever. For money launderers and tax evaders, the buying of a golden visa remains one of the main ways to obtain financial secrecy.

We therefore advise: visa-selling countries beware (and reconsider)!

Donate to Tax Justice Network

We rely on donations from people like you who value our research and campaigning to keep our work going. Help us do more work like the work above with a donation.

The author

Related articles

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

Finally, the European Court of Justice cracks down on trusts

Financial secrecy has entered the EU AML rulebook. What comes next?

Malta: the EU’s secret tax sieve