Published:

11 February 2016Reading time:

7 minFrom Fools’ Gold:

Recently we wrote an article entitled The Ideologists of the Competitiveness Agenda, in which we fingered the Big Four firm of accountants as among the most important vectors for the general idea that countries simply have to ‘compete’ in certain ways: namely, to shower goodies at wealthy people and multinationals, for fear that they’ll relocate elsewhere. As we’ve often argued: that attitude is not just misplaced, but generically harmful.

Recently we wrote an article entitled The Ideologists of the Competitiveness Agenda, in which we fingered the Big Four firm of accountants as among the most important vectors for the general idea that countries simply have to ‘compete’ in certain ways: namely, to shower goodies at wealthy people and multinationals, for fear that they’ll relocate elsewhere. As we’ve often argued: that attitude is not just misplaced, but generically harmful.

Now, here’s a recent example of a Big Four firm, PwC, playing the “competitiveness” game, in a lobbying document report purporting to assess the fiscal regimes for gold mining in four African countries. (Thanks to Mark Zirnsak of Tax Justice Network Australia for pointing this one out.)

This is a hugely important matter: it is a question of how billions of dollars’ worth of mining wealth is being shared out between Tanzania, Namibia, Burkina Faso and Ghana, on the one hand — and a bunch of mining multinationals from rich countries, on the other.

Our purpose here today is not to point to where the balance should lie between the two. It is to point out the economic nonsense being pushed by this extremely wealthy company.

Take a look at the image, to start with. Even in these nine words, a major illiteracy already springs out.

First, “Does the tax regime encourage new mines” is the wrong question for these countries to consider. The big question is: “Does the tax regime create the right balance between earning revenue and attracting and retaining investment?” You can of course drop the effective tax rate to zero, and encourage some new mining activity. But would that giveaway be worth it? Of course not.

Asking whether the fiscal regime is ‘competitive’ — in the sense that it encourages new mines — doesn’t answer the question of whether that country has a mining fiscal regime that is right for it.

Now let’s look at the report itself.

High up, it contains an old chestnut from the Competitiveness Agenda: the panic-inducing ‘tipping point‘ meme. Or, as PwC Australia put it:

“Ghana and Tanzania sit on a knife’s edge.”

Quick, quick! Cut taxes! Help! Panic!

Now, slow down for a minute or two. Let’s think about this. What are the most fundamental factors that drive investment decisions in mining?

Well, they are, generally, these.

First, politics. A belief that your investment isn’t going to get overrun by rebels, or subject to retrospective contract changes, and that kind of thing.

Second, the costs and difficulties of getting the stuff out of the ground and onto ships, along with the purity of what you dig up, and all that kind of stuff. Geology and geography.

Third, the agreed fiscal regime. Yes, it matters, quite a lot.

Fourth, commodity prices — and, by extension, your firm’s long term price forecast.

Now if these two countries are on a knife’s edge at the moment of this report’s being written, then a substantial change in any of these conditions will naturally take it off the knife’s edge. If prices rise a long way (and consequently, your firm’s price forecast will rise: they always do) then the investments are surely going to happen, so you needn’t give it any extra fiscal incentives. And if they fall a lot then a bit of tax-cutting is unlikely to make much difference. That’s what a knife’s edge scenario implies.

And as we all know, many commodity prices have fallen a long way, in response to falling Chinese growth prospects and other reasons, since that report was written: new commodity investments are out of fashion in the current climate, and who knows where prices will go next?

The PwC report is also littered with statements like this:

“Governments must ask themselves – is it better to take a smaller share of an economic project which will go ahead or put in place the mechanism for a greater share of a project which becomes marginal and may not generate any economic activity or employment at all.”

Which is about as loaded a question as one can get. Errr, obviously the former. But this doesn’t get us any closer to telling us whether the fiscal regime is right for that country: it is a lobbyist’s statement. And one could make a similar general accusation about a section in the PwC report called “The Multiplier effect”, which produces a bunch of figures about knock-on benefits from mining, produced by the Interntional Council on Mining and Metals, another (more overt) lobbying organisation for mining companies. Those numbers omit such minor details as the phenomenon that goes by the name of The Resource Curse.

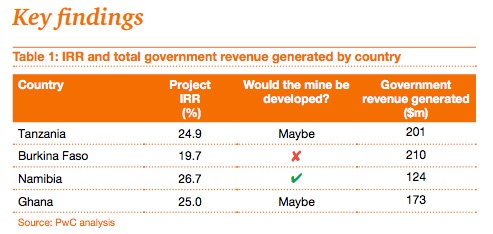

Leaving all that aside, let’s now look at some actual numbers from the PwC report, based on a project’s computed Internal Rate of Return (IRR for the company).

We can make several points.

First, they state, baldly:

“Based on analysis performed across a number of mining companies, we have assumed a minimum required Internal Rate of Return (IRR) of 25%.”

This 25 percent figure for IRR is, to use the terminology, a so-called ‘hurdle rate,’ below which the company won’t invest. How is IRR calculated? Well, here’s one short briefing. It notes:

“If all other things are equal (i.e. risk, safety), the project with the highest IRR is the one we should invest in first.”

Our emphasis added. And we can be sure that the risks of operating a mine in Burkina Faso will be very different from the risks of operating in Ghana. So why the blanket 25 percent cut-off point, applicable to all? Not only that, PWC admit that this number is hedged with all sorts of other assumptions and qualifications:

“We have modelled the economic impact of each of the four country’s systems on a gold mine, which we have standardised. We have equalised the grade, metallurgy, operating costs, production levels and construction times. We have assumed the same capital and operating costs and taken out any variability as a result of limitations in access to power and water. We have removed country specific input cost variables, such as regulated diesel fuel pricing, removed the impact of any limitations in access to skilled labour and critical infrastructure, along with the availability of parts and contractors.” (and there are further assumptions on p5, and still more in the Annex)

But let’s accept this leap of faith anway: this 25 percent figure still seems high. As Diarmid Sullivan of ActionAid points out to FG, a World Bank document looking at mining regimes says of a 20-22 percent IRR:

“most investors would find the after-tax IRR still good enough to meet profitability criteria (p181).”

That’s admittedly looking at a range of commodities, and is from 2006, but still: it’s worth bearing in mind. (And look at that IRR table on p195 too, admittedly for copper mines.)

And here’s another question for PwC. Oil and mining companies engage in a world of tax avoidance: thin capitalisation and all sorts of other tricks — bringing their effective tax rates below the headline expected rates. Has this been taken into account in their models? We can’t see any suggestion that this is so.

Another crucial thing to understand about that 25 percent number. These organisations — the Big Four accounting firms like PWC — are, among other things, paid lobbyists for big firms. (Read Prof. Atul Shah’s shocking brief analysis of KPMG, out today, just to get a flavour.) You should absolutely not trust these companies to inject the correct assumptions into their models. They have skin in the game. They have low-tax genes, acquired from years of working on behalf of tax-minimising and tax-dodging clients, and from playing a central role in helping set up the global infrastructure of offshore tax havens.

So: what should the correct fiscal regime be for these mines?

Well, we aren’t going to make any hard recommendations to countries based on any numbers. But, as usual, a few things can be said.

First, don’t believe the Big Four accountancy firms: they are structurally, historically and ideologically biased. Other bodies like the World Bank are likely to be more helpful: but even then treat them with extreme caution, given their historical track record with low-tax ideological opinions. Consult allies: other countries with mining experience, which don’t have much of a vested interest in seeing you give away the house.

Second, be patient. Your best bet for good fiscal terms is when commodity prices are high, and political conditions are good. Once you’ve signed that contract, you are usually locked in for decades. That’s why mining firms are often keen to sign deals during a civil war: that’s a recipe for contracts signed in desperation — and superlative profits for the multinationals, at the country’s expense. While waiting, learn as much as possible about the sector, and try to consult widely with people you think are trustworthy. (Here is one group you might look at, at least for the oil sector: OpenOil.net, which recently ran an article entitled Apply now for online training in financial modeling of extractives! ) Or you may (perhaps) want to engage in state-led investment as in Norway or Brazil, if foreign companies aren’t investing. It’s no panacea, but it’s another option.

And while you’re waiting patiently, remember that even if your fiscal regime were to be deterring investment in new mines, that would not necessarily be a net loss to the nation. It is more like a transfer through time: the minerals will remain safely in the ground for now, and can be harnessed for the nation’s benefit at some future date. (We’ll leave discussion of the all-important Resource Curse for another day: suffice to say that its existence reinforces this point.)

Third, a more nitty-gritty one, but still important: don’t be shy about requiring hefty royalty payments, for these are much harder to game via transfer pricing and other tricks, than other payments are.

Fourth, be transparent. There will be a lot of vested interests inside your own policy-making apparatus keen for jam today at the expense of tomorrow, or with more sinister agendas. The more visible this all is, the harder it is for them to pull the wool over the eyes of the citizenry. An important component of this would be public country-by-country reporting.

Further Reading:

Open Oil. Lots of information about oil, much of which is relevant for mining too.

Don’t listen to Big Oil’s Whining for Tax Cuts, TJN, Jan 2015

On Tax Competitiveness, Fools’ Gold, March 30, 2015

Ten reasons to defend the corporate income tax, TJN, March 2015. Although this focuses on just one component of mining fiscal regimes – the corporation tax – many of the arguments here apply, generically.

The author

Related articles

Public finance is feminist terrain

She cleans your house but the tax system can’t see her

Joint submission: International financial architecture, debt and the right to education

20 May 2026

Taxing Ethiopian women for bleeding

Tax justice and the women who hold broken systems together

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026

The tax justice stories that defined 2025

Let’s make Elon Musk the world’s richest man this Christmas!

")