Among the scandals exposed by the Paradise Papers is that of residency for sale, something I covered just last month (along with passports for sale) as a special feature in our monthly podcast and radio show, the Taxcast, which you can listen to below.

The name Shakira Isabel Mebarak Ripoll showed up in leaked Paradise Papers documents. Like many other famous names exposed, the pop star Shakira appears to have used a series of structures and mechanisms to manage her wealth and assets, in her case via Malta and Luxembourg.

The Guardian newspaper also reports that although she now lives in Barcelona, Spain, she’s listed as resident of the Bahamas:

Asked about her listed residence in the Bahamas, the lawyer added that as an international artist Shakira had lived in a variety of places “throughout her professional career and, in every case, has fully met the laws of all the jurisdictions where she has resided”.”

Continue reading “#ParadisePapers: residency for sale to the rich and famous”

Our two last papers on trusts (here and here) described trusts’ involvement in grand corruption and other cases that would anger any rational person. The Paradise Papers, and recent case law, shed outrageous new light on trusts’ role in worsening inequality, shielding assets from legitimate creditors, and avoiding or evading taxes.

Why does society tolerate these kinds of trusts? When will governments take action? Do we want to live in a world where, as Oxfam put it, “8 men own the same wealth as half of the world”? Continue reading “Enough evidence on trusts – where are the State’s actions?”

In response to the latest Paradise Papers revelations, which have seen large multinational companies exposed milking profits offshore, the Tax Justice Network is calling on countries around the world to start to tax the global profits of multinational corporations.

Continue reading “Day 2 #paradisepapers revelations – Global corporations need global taxation”

As the revelations from the Paradise Papers hit the news stands many journalists are asserting as fact that nothing illegal has taken place. The BBC in the UK are the most aggressive proponents of this line, but the issue has been raised in other countries too. On several interviews I have done today I have been told by the interviewer that nothing illegal has taken place, then asked why should anyone care.

Leaving aside the moral arguments about tax avoidance often raised, I want to gently suggest to colleagues in the media that this kind of reporting is misleading, unethical, and needs to stop.

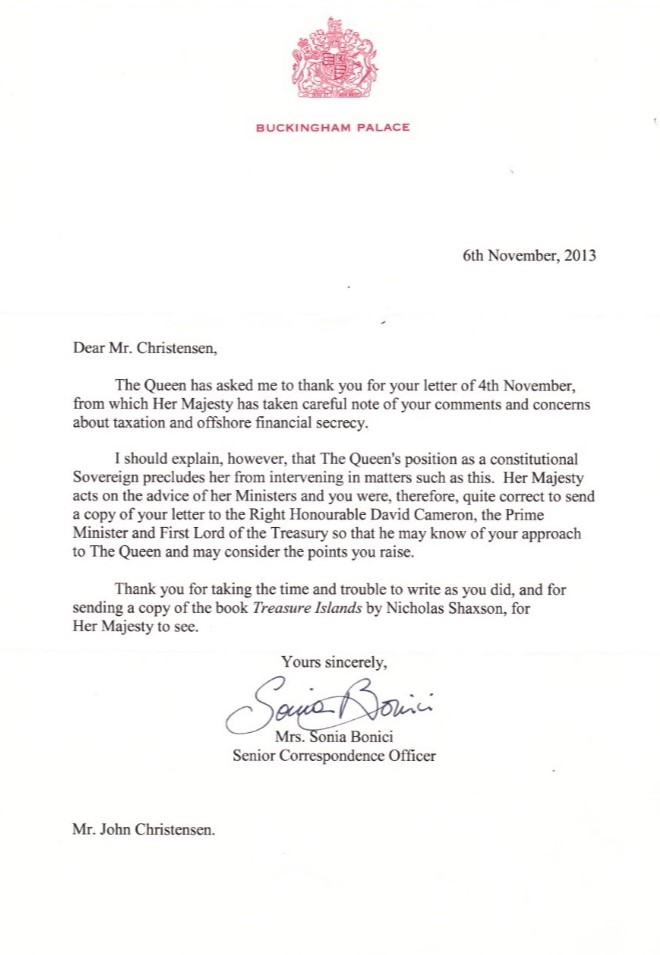

It should come as no surprise that Her Majesty the Queen uses offshore tax havens as part of her wealth management strategy. The Queen is, after all, the head of state of the British Virgin Islands, the Cayman Islands, the Channel Islands, and Bermuda where the law firm Applebys was originally based, and others, which makes her the Queen of Tax Havens. In 2013 TJN wrote a letter to the Queen requesting that she use her position as Head of State to request her Prime Minister to take steps to end offshore secrecy. Our letter pointed out that the British tax havens were deficient in transparency in key areas relating to ownership information about companies, trusts and foundations, and also publication of financial accounting information. As we said at the time:

. . none of the Overseas Territories or Crown Dependencies operate a properly transparent public register of offshore companies, trusts and foundations. None obtain and maintain information on beneficial ownership and make this information publicly available. Not one requires that all company financial accounts are made publicly available.”

In her reply, Her Majesty thanked TJN for sending a copy of Nick Shaxson’s brilliant exposé of tax havens, but answered our request by stating that her position as a constitutional monarch “precludes her from intervening in matters such as this.”

The Queen meets her Prime Minister weekly to discuss matters of state. Tax havens have been high on the global agenda since 2008 and Britain’s role as the largest global provider of offshore financial services should make this a matter of high priority to the person who is nominally Head of State of so many major secrecy jurisdictions. While we would not expect the Queen to publicly voice personal concerns, it is quite reasonable to expect Her Majesty to raise concerns about offshore secrecy with her Prime Minister and push for transparency measures to be fully implemented.

To date, however, there has been little progress. Since 2013 British secrecy jurisdictions have refused to introduce public registries of ownership and financial accounting information is still not published online (if at all). Worse, Britain continues to resist efforts to include trusts in transparency measures, which undermines attempts to strengthen international cooperation on automatic information exchange through the global Common Reporting Standard. We recently published an extensive report on the uses and abuses of offshore trusts, available here, and even more recently we published a reply to various criticisms of that paper, available here.

The Queen’s role as Head of State of so many leading secrecy jurisdictions puts her in a highly compromised position. The situation is made worse by revelations that her wealth management team have invested in an offshore portfolio which includes companies that have been accused of exploiting poor and vulnerable households. Given that Her Majesty will be meeting her Prime Minister this week, and the next, and the week after that, we humbly request that she uses the opportunity of these meetings to push for three specific measures:

Our 2013 letter to the Queen is available here. Here is a copy of the letter that Her Majesty sent to TJN in November 2013:

The International Consortium of Investigative Journalists have released their latest leak of data from the offshore world. The ‘Paradise Papers’ are a leak of over 14m documents from the offshore law firm Appleby.

So far leading politicians and even Queen Elizabeth have been revealed to be involved in the offshore world with more revelations scheduled to be published over the following days.

Our press release responding to the leak can be found below. If you need to contact the TJN, contacts are at the bottom of this post or here.

You can also see our CEO Alex Cobham’s video response here: [MEDIA PLEASE NOTE: this video is freely available for your use, no need to ask permission]

A transcript of the video can be found here.

To download a copy of this Press Release in PDF click here.

The ‘Paradise Papers’ have once again highlighted the failure of governments around the world to deal with the scourge of tax dodging and financial crime facilitated by offshore financial centres, and we commend the ICIJ on their fearless investigative journalism.

The Tax Justice Network is calling on world leaders to commit finally to ending tax abuse and financial secrecy. The United Nations should convene a summit of world leaders with the goal of agreeing a UN convention to end tax abuse and financial secrecy. World leaders need to agree binding targets to reduce all forms of illicit financial flows, with accountability mechanisms to ensure progress.

Research from the Tax Justice Network shows that the level of profit shifting by multinational companies has exploded over the last decade. The latest estimates show that world governments are losing $500bn a year in taxes due to tax avoidance by large companies. A further $200bn a year is estimated to be lost due to the undeclared offshore wealth of tax evading individuals.

The Paradise Papers is the largest leak of data to date from the world of financial secrecy. And once again, the leaks confirm that this is not a marginal activity, but a systemic, global issue. Major corporations and wealthy elites are dodging taxes – and their obligations to society – with impunity, supported by the biggest banks, accountants and lawyers.

Nor are these victimless crimes – far from it. These truly anti-social actions undermine public health and education systems, and drive inequality and corruption – leaving the poorest families and the poorest countries of the world to suffer. Tax Justice Network research confirms that lower-income countries bear a disproportionate share of the burden from global tax abuse – and this has direct costs in terms of everything from foregone economic growth to excess child mortality.

In response to the leaks Alex Cobham, chief executive of the Tax Justice Network said:

“These leaks confirm the systemic nature of tax abuse and corrupt practices, with global financial secrecy being marketed by major law firms, banks and accounting firms. Government efforts to combat this problem have been piecemeal at best. And that is why the Tax Justice Network is today calling for a genuinely global response.

“World leaders need to seize the moment and convene at the UN to agree a path to ending financial secrecy and tax abuse for good. And we, as citizens of the world, must demand this from our elected representatives. Otherwise we may as well just sit and wait for the next leak – because those profiting from these anti-social practices will never stop on their own.”

Liz Nelson Director of TJN’s work on tax justice and human rights said:

“Financial secrecy jurisdictions, by damaging public services and driving inequality infringe on fundamental rights including right to life, freedom from poverty, and basic sanitation

“By eating away at government revenue they deny women and other historically discriminated against groups fundamental rights to health, education, to political participation, economic empowerment and access to justice”.

John Christensen, Chair of the Tax Justice Network said:

“Law firms like Appleby specialise in providing offshore structures to their global clientele. Appleby needs to be thoroughly investigated to ensure that their partners and staff have not been knowingly facilitating criminal and corrupt practices.

“For too long lawyers have hidden behind client privilege to protect clients from investigation: the Paradise Paper revelations, and the Panama Papers stories that preceded them, show that lawyers cannot be trusted to respect the laws of sovereign states.

“Any lawyer who fails to report suspicious client activities should face strict penalties, involving custodial sentences and loss of professional status. Strong measures are needed to rebuild public confidence in the law professions.”

ENDS

Tax Justice Network spokespeople are available to respond to for media comment.Please contact [email protected] or contact the following people directly:

George Turner UK, george [@] taxjustice.net +44 (0) 7540 252 850

Alex Cobham, UK, alex [@] taxjustice.net +44 (0) 7982 236863

Markus Meinzer, Germany, markus [@] taxjustice.net +49 (0) 178 340 5673

Andres Knobel, Argentina – Spanish language, Andres [@] taxjustice.net

Henrique Alencar, Portuguese language, henriquedomenici [@] msn.com

Notes

The next in our series of articles taking a deep dive into some of the world’s tax havens ahead of the publication of our next installment of the Financial Secrecy Index. Today, we are publishing an article setting out the history and development of Jersey as a financial center.

We are reposting here an open letter sent by TJN-Germany today to Jean-Claude Juncker, President of the EU-Commission, on the forthcoming EU tax haven blacklist. It is worth noting too, that the OECD’s blacklist of June 2017 only had 1 (o-n-e!) tax haven listed: Trinidad & Tobago. All of which acts as a powerful reminder of why, at TJN, we do not hold our breath about blacklisting exercises as they have been failing for decades in delivering on their promise to curtail tax avoidance and evasion (as we have researched in some depth here and here).

You can read the full letter as a pdf here.

Dear President Juncker,

The German network of organisations aiming for tax justice (Netzwerk Steuergerechtigkeit) is very concerned that the tax haven blacklist announced by the European Union for the end of 2017 will leave out important secrecy and low-tax jurisdictions and will therefore not contribute to a solution of the problem addressed.

We became aware of the fact that jurisdictions like the Cayman Islands are lobbying heavily to not be included on the list. While every country/jurisdiction needs a fair check, it is important that the EU takes its own list seriously. The EU’s criteria must be applied thoroughly, including not accepting announcement from countries to get off the list. Instead, only real legal changes should count.

We would also welcome the EU observing a zero per cent tax rate not only as an indicator, but already as proof of a jurisdiction being non-cooperative or even harmful. The European Parliament has called for minimum tax rates in the European Union. A zero per cent tax rate should thus be a sufficient reason for being listed.

Unfortunately, however, we note that further blacklist criteria are too weak. Any result based on these criteria will only provide a misleading picture of the problems we still face.

Another major shortcoming is the fact that EU countries will by definition not be named on the blacklist, even though some have been clearly identified as harmful. The EU, at the very least, needs to strengthen its internal processes, e.g. in the Code of Conduct Group, to push for reforms in its own secrecy and low-tax jurisdictions, such as the Netherlands, Ireland, Cyprus, Malta and Luxembourg, and in all EU countries with harmful practices, such as the lack of capital income tax for non-residents.

Finally, we think that any blacklist must be accompanied by strong and immediate sanctions.

Yours sincerely,

Sarah Godar

(Coordinator, Netzwerk Steuergerechtigkeit)

***

Letter as PDF

On 23rd January 2016, the then Chancellor of the UK Exchequer (finance minister) George Osborne announced (via twitter) that he had negotiated a tax settlement with Google. On examination we decided that this deal was shockingly poor value for UK taxpayers and, worse, almost certainly contravened European Union rules on illicit state aid. On 28th January 2016 we wrote (see the full text of our letter below) to the European Commission expressing our concerns and calling for a comprehensive review not just of the Google settlement, but of ALL tax deals struck by the UK government with multinational companies. The international press are now reporting that the EU’s competition authority now plans to investigate the UK controlled foreign corporation (CFC) rules introduced by George Osborne in 2013, which will have enabled significant profits shifting to offshore based CFCs. Continue reading “Result: European Commission to investigate UK tax treatment of MNCs”

As we work towards the publication of the next Financial Secrecy Index, today we are publishing a guest post from Peter Ringstad from TJN Norway on the history of Cyprus as a tax haven.

The FSI includes with it a number of narrative reports on the history and development of a range of financial centres. If you have any comments on this report on Cyprus, or anything to add, please leave us a comment underneath. Perhaps your contribution might make it into the 2018 edition of the FSI!

Continue reading “Our paper “Trusts: Weapons of Mass Injustice?” – now available in Spanish”

We’d like to share the details of a fascinating course for those working on tax issues within the public and private spheres in Europe. It’s run by the COFFERS project team. COFFERS (Combating Fiscal Fraud and Empowering Regulators) is an EU Horizon 2020 Project. We’re sharing the details from the news section of their website here:

Continue reading “Master of Tax Course: Combating Fiscal Fraud and Empowering Regulators”

In this month’s Taxcast we look at the booming business of passports and residency for sale, and why it should worry us all. Also:

This Taxcast is dedicated to the memory of Daphne Caruana Galizia, Malta’s best-known investigative journalist who was murdered by a car bomb, a cowardly attack on all those who refuse to accept the corruption and state capture of our institutions and democracies by dirty money and financial secrecy. Our statement on the loss of this great citizen is here.

Continue reading “Passports and residency for sale in our October 2017 podcast”

I had the honour of giving a keynote address at the World Bank/International Monetary Fund annual meetings on 15th October 2017, for an event entitled ‘Technical challenges and solutions for taxing wealth in developing countries’ – which gave the impression that a new Washington consensus on tax justice may be emerging.

My slides and the video, kindly provided by the Bank, are below. Following a fascinating speech from Brooke Harrington of Copenhagen Business School on the role of wealth managers in creating anonymous, un-taxed assets, I ran through the development of the tax justice movement and the rise of the core policy platform (the ABC of tax transparency), highlighting the progress that has been made but also the extent to which lower-income countries remain excluded from the benefits – and what is necessary to enable effective wealth taxation.

The event, and the discussions with a variety of experts and senior figures from the two Bretton Woods institutions (BWIs), made clear just how far both the Bank and the Fund have moved towards tax justice – and also highlighted some key areas where they need to make progress now.

Continue reading “Tax justice, the new Washington consensus?”

As reported by Reuters, Daphne Caruana Galizia, Malta’s best-known investigative journalist was killed today by a powerful bomb which blew up her car. Only fifteen days earlier she had reported threats against her to the police. Her absolutely fearless blog Running Commentary continually broke revelations about the corruption of Maltese politics (on all sides), and her work went way beyond Malta.

She was reporting from Europe’s smallest member state. which is ranked 27th in the Tax Justice Network’s 2015 Financial Secrecy Index (FSI). It will be re-assessed soon – the 2018 Financial Secrecy Index data will be released in January. It is described as ‘a pirate base for tax avoidance inside the EU’ by the European Investigative Collaborations Network behind the Malta Files investigations, which also exposed the jurisdiction numerous times as ‘a target for firms linked to the Italian mafia, Russian loan sharks and the highest echelons of the Turkish elite.’ You can read about some shocking examples here, here and here. Much of the work she did over the last couple of years was focused on the Panama Papers leak of more than 11 million documents from law firm Mossack Fonseca.

The International Consortium of Investigative Journalists (ICIJ), has issued a statement, noting;

Caruana Galizia has been at the forefront of important investigations in the public interest and has exposed offshore dealings of prominent political figures in Malta.”

Welcome to this month’s latest podcast and radio programme in Spanish with Marcelo Justo and Marta Nuñez, downloaded and broadcast on radio networks across Latin America and Spain. ¡Bienvenidos y bienvenidas a nuestro podcast y programa radiofónica! (abajo en castellano). In the October 2017 programme:

Our CEO Alex Cobham recently addressed the 5th Pan Africa Conference on Illicit Financial Flows and Tax, organised by Tax Justice Network Africa and the UN Economic Commission for Africa in Nairobi, Kenya. Alex’s presentation focuses on the debate emerging over the inclusion of the goal to reduce illicit financial flows within the UN’s Sustainable Development Goals (SDGs).

Below you can hear him discuss the meaning of the word ‘illicit’, which he says is a cover for people who want to remove tax avoidance by multinationals from the Sustainable Development Goals. The battle to come is over the inclusion of a meaningful target in the SDGs for the reduction of multinational tax avoidance. In this presentation Alex explains why it is so important that the reduction of multinational tax avoidance is included as a target for the SDGs and puts forward a suggested indicator as to how that target could be monitored. Continue reading “The campaign to subvert the UN Sustainable Development Goals – TJN presentation from the Pan Africa Conference on Illicit Financial Flows and Tax”

According to the Institute for Public Policy Research’s Commission on Economic Justice report called Time for Change: A New Vision for the British Economy, we need a “fundamental reform of the British economy on a scale comparable with the Atlee reforms of the 1940s and the Thatcher revolution of the 1980s.” Like many so-called developed economies around the world, the British economy’s no longer delivering rising earnings for most of the population, and young people today are set to be poorer than their parents. In this Taxcast Extra I speak with Grace Blakeley of the Institute for Public Policy Research on the findings of their report.

we’ve had this massive explosion in inequality…and wealth inequality is actually even starker than income inequality…really very dramatically high, it’s almost as high as the level you see in Russia…over the last 30 years and that relates to a number of underlying broad structural trends in the UK economy, not least what the Tax Justice Network talks about quite a lot, which is the explosion of financial services and the financialisation of the UK’s economy…we find that whilst we have one of the world’s largest financial sectors, that is not financing investment in the wider economy, we actually have one of the lowest levels of investment of any major economy.”

Continue reading “Podcast: A New Vision for the British Economy, a Taxcast Extra”

The new Dutch government is to announce that it will cut its corporate tax rate according to leaked details of the current round of coalition talks. This move is the equivalent to the country jumping into the race to the bottom pool with both feet.

We’ve always highlighted the false narrative behind the race to the bottom tax ‘competition’ on which such policies are based. The winners are a tiny business elite (and we should give a dis-honourable mention to many politicians who seem to pass far too quickly through revolving doors from public to private servant – here’s one such example right here). The losers are, well, everybody else. Continue reading “The Dutch government cuts its corporate tax rate…”

If you were working on tax as a development issue in the early 2000s, not only were you a lonely figure but you were also faced with some of the most pathetic cross-country data imaginable. For a 2005 paper (which introduced the 4 Rs of tax, inter alia), I tried to put together a comprehensive picture of tax revenues – only to find that both the International Monetary Fund and World Bank data contained such basic errors as tax/GDP ratios in excess of 100%.

The need for a concerted effort to improve data collation methods was clear; but it wasn’t until 2008-9 when the British Government’s Department for International Development (DFID) decided to fund a research centre on tax that the funding came into view. When the Norwegian Agency for Development Cooperation (Norad) joined forces to match the money available, the International Centre for Tax and Development was born and so began the process to create what is now the ICTD-WIDER Government Revenue Dataset (GRD). Through the blood sweat and tears of altogether too many researchers, a dataset emerged. Along the way, more issues came into view – including some series that still included tax/GDP over 100%, and areas of irresolvable uncertainty – but the resulting dataset is unequalled in consistency and comparability. The original working paper with Wilson Prichard and Andrew Goodall sets out the process and the issues encountered.

There’s now a new release of the GRD (Government Revenue Dataset) fully updated and offering all kinds of new insights. With their kind permission, we cross-post from United Nations University WIDER Kyle McNabb’s great post on this new release. Continue reading “New release of global tax data”

New rules to prevent corporations using debt and interest payments to lower their taxbills have been one of the outcomes of the OECD BEPS programme. However, how effective are these rules? And is the new debt cap proposed by the OECD likely to have any impact at all?

Corporation tax is a tax on profits. Interest payments are counted as a business expense in corporate accounts and so any interest paid by a company is deducted from profits before tax is paid. The more interest a company pays, the lower the profits, the lower the tax bill. This is sometimes called the debt shield.

Using debt has been a well known and widely practiced form of tax avoidance. Multinationals can set up finance companies in tax havens to loan money to their operating companies around the world. The debt shield also encourages companies to take on debt as it makes debt a cheaper form of financing.

The OECD, under the BEPS programme, has proposed that countries limit the amount of debt that can be deducted from profits before corporation tax is paid. The OECD have suggested a cap on interest of between 10% to 30% of Earnings before Interest Taxation, Depreciation and Amortisation (EBITDA), sometimes referred to as operating profit. The cap takes into account all loans, whether intra-company loans or commercial loans from an external source.

These rules have been carried forward into the EU’s Anti Tax Avoidance Directive, which mandate the lowest cap of 30%.

I decided to run some numbers to understand what that cap means in practice. Take a notional company Dodgyco. Dodgyco has an income of $300,000,000. It makes a profit on its operations of 30%, which leaves it with $100,000,000 before interest and tax.

| Dodgyco | |

|---|---|

| Revenue | $300,000,000 |

| EBITDA | $100,000,000 |

| Debt | $600,000,000 |

| interest @ 5% | $30,000,000 |

| Interest to EBITDA | 30% |

Under the OECD rules the company is allowed to deduct $30,000,000 in interest payments a year from its taxable profit.

If we assume that dodgyco can borrow at an interest rate of 5% then an interest payment of $30,000,000 implies a debt of $600,000,000.

Lets say that dodgyco is valued at ten times its earnings – $1,000,000,000. This implies that the company will have a financial leverage of 60% before the cap bites.

In today’s low interest world a 5% interest rate is generous. Currently $ denominated investment grade corporate bonds are yielding 3.5% on average. European bonds see even lower yields.

Once the interest rate hits 3%, then a $30,000,000 interest payment represents a debt of $1,000,000,000.

These ratios are very high. Currently the average debt to equity ratio of the Standard and Poor’s 500 is 50%, which has led to fears that US companies are over-leveraged. The historic average is just 14%, suggesting that when interest rates start to increase, leverage will decrease too.

It seems then that most companies will have little to worry about from the new rules from the OECD.

But one area where companies have much higher levels of leverage is infrastructure, particularly in cases where a company has been subject to a leveraged buyout. Infrastructure projects generally have very stable and sometimes government backed revenue streams. This allows companies to sustain very high levels of debt, as there is greater certainty that the money will be there to make the interest payments.

Heathrow, the UK’s largest airport, is just one example. In recent years the company has sustained a ratio of over 90%. In 2016, interest payments accounted for 91% of EBITDA, well over the OECD’s proposed upper limit of 30%.

But even in these cases, it appears that companies could have a get out. The EU’s Anti Avoidance Directive allows a get out from the interest cap for loans used to invest in “infrastructure” for the public benefit. How this will be interpreted will be an important issue for many companies, and is likely to have a serious impact on tax revenues too.

Clearly the OECD guidance, of a 30% cap on interest payments, is far too high, and the infrastructure exemption in the EU directive leaves a giant loophole for the most highly leveraged companies. So what would a more effective solution look like?

A hard cap on interest deductions that takes into account commercial loans is desirable because it discourages companies from over-leveraging. Within the OECD proposals countries are free to implement a cap of 10% EBITDA and should be encouraged to do so.

But why not disallow all tax deductions on loans that originate from related companies? By removing the tax incentive for firms to borrow from their parent companies or shareholders, we remove a major source of profit shifting.

From the point of view of the firm, a loan which comes from a related party can’t be considered to carry the same risk that a commercial loan carries. Why then, should they expect to be treated equally?