15 years ago the Tax Justice Network proposed that multinational companies be required to report publicly on their operations, profits and taxes paid in each country where they operate. Our aim was to bring the transparency of the world’s biggest economic actors more in line with that of individual companies operating in a single country. Tax expert Richard Murphy wrote a draft international accounting standard, and then we took it to the world.

In 2013, the G20 and G8 groups of countries recognised the importance of this data in the fight against tax avoidance, and mandated the OECD to introduce just such a standard. But as yet, the data remain private to tax authorities. The UK passed legislation two years ago that would allow it to make the data public – but for unknown reasons, the government has not used this power.

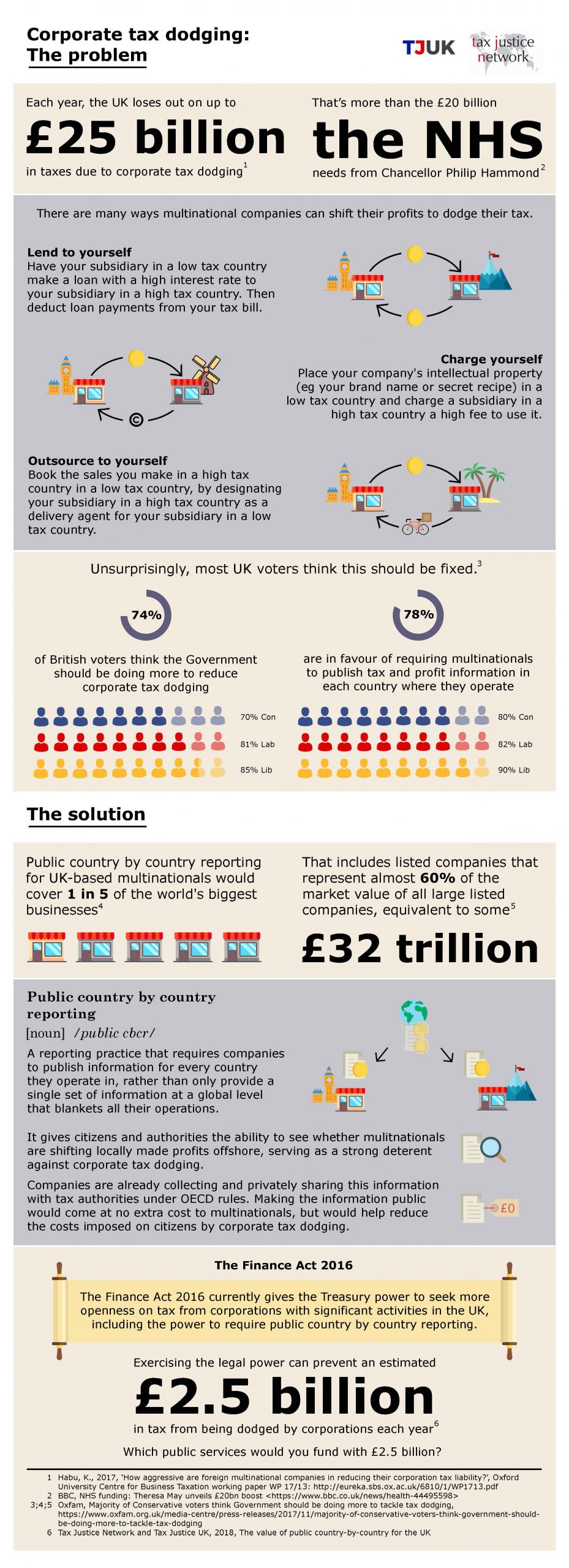

Now, in joint work with our independent sister organisation Tax Justice UK, we present new evidence showing that public country by country reporting could raise revenues of £2.5 billion a year. The Chancellor Philip Hammond should simply say the word in his budget speech next week.

We draw on two key pieces of research to generate this estimate. First, work done by Dr Katarzyna Habu, an international research fellow at the Oxford University Centre for Business Taxation (which was founded by leading multinationals). With unique first access to a UK dataset of corporate tax returns, Dr Habu finds that the UK subsidiaries of foreign multinationals declare taxable profits at the rate that is just half that of equivalent UK companies of similar scale and in the same industries. If that difference could be eliminated, those multinationals would pay an additional £25 billion pounds a year in UK tax (Habu, 2017).

This estimate relates to the period before changes to the international tax system made after the financial crisis, in the OECD Base Erosion and Profit Shifting initiative (BEPS). But BEPS involved piecemeal changes only, rather than confronting the need for a comprehensive alternative. Unsurprisingly perhaps, there is as yet no evidence that BEPS has reduced the scale of the problem. But BEPS did bring in the private country by country reporting standard…

Meanwhile, the European Union had introduced its own, much weaker and less consistent but public country by country reporting standard for banks. New research by Dr Michael Overesch and Dr Hubert Wolff shows that the average effect of publication was to increase tax paid by multinational banks by around 10% – and significantly more for those that had ‘tax haven’ structures within the group.

If the UK Chancellor Philip Hammond announced on 29 October that he will use the existing legislative power to require public country by country reporting, the compliance costs for multinationals would be near zero since they collect the data already. And the impact would be global, since around one in five of the world’s biggest multinationals are in the UK.

The revenue benefit, on the basis of the new research, can be conservatively estimated at £2.5 billion a year. That’s a little more than the Chancellor could expect from reversing a percentage point cut to the corporate income tax rate. But while that would affect all businesses, this transparency measure would raise revenue purely from those companies that are currently not paying their fair share.

Once upon a time, politicians asked us why they should create a new reporting standard. Now the standard exists. The only question is why politicians wouldn’t immediately make the data available to the public. It wouldn’t just be a win for accountability – the revenue benefits would be substantial too.

The author

Related articles

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026

California steps up for tax fairness

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

Tackling Profit Shifting in the Oil and Gas Sector for a Just Transition

The State of Tax Justice 2025

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

Bad Medicine: A Clear Prescription = tax transparency

The Financial Secrecy Index, a cherished tool for policy research across the globe