There’s a good development in Vietnam we’d like to share with you via Policy Advisor Economic Inequality and Tax Justice Francis Weyzig of Oxfam Novib. He says,

“Vietnam has introduced a legal requirement for domestic subsidiaries to provide a copy of the global Country By Country report directly to the Vietnamese tax authority. This way, Vietnam does not have to rely on tax treaties or information exchange agreements to the get information on foreign parent companies. It provides a great example for other countries to follow, so congratulations to my colleagues in Vietnam for this great milestone!”

The decision by Vietnam to require local filing by multinationals that wish to operate there is exactly what we have argued countries should do – instead of getting bogged down in the complexities of an OECD process that may never yield any data.

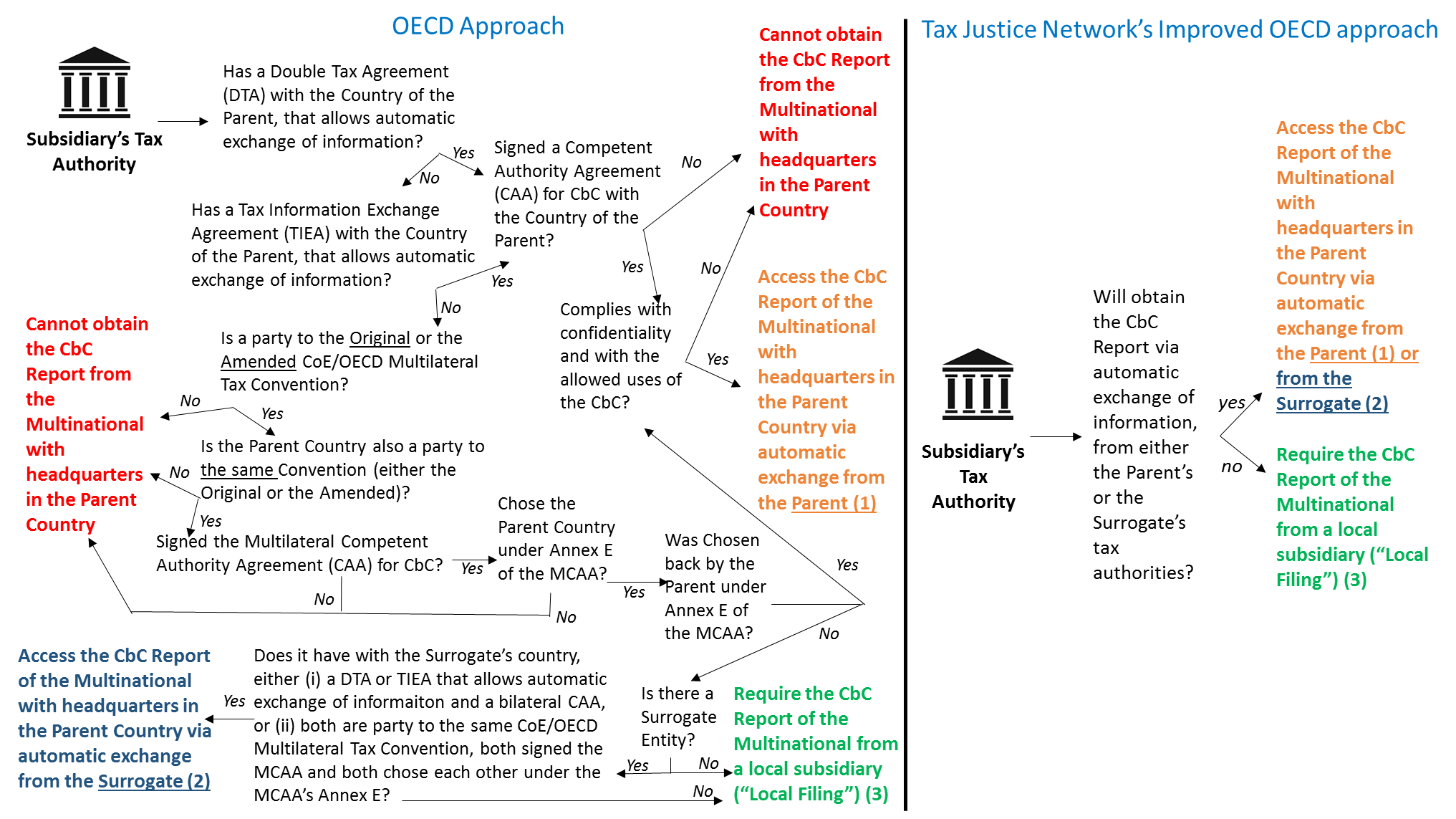

As you can see from the diagram below, the OECD approach, based on automatic exchange of information, uses a complex framework that depends on developing countries being able to convince a developed country to sign an international agreement with them. Not only is it complex, but it leads to situations (in red) where the developing country will not access CbCR information they need. TJN’s improved OECD-proposal (which you’ll see is much simpler) http://healthsavy.com/product/propecia/ while not as ideal as having multinationals publish CBCR information on their websites, at least simplifies the framework and ensures that developing countries obtain the CbCR one way or another:

Back to Vietnam: here is the relevant text on their CbCR (country-by-country reporting) requirement for local filing as specified in Article 10.4c:

“In case the taxpayer has an overseas ultimate parent, the taxpayer shall be responsible for providing the copy of the ultimate parent company’s CbCR if the ultimate parent is also required to submit the CbCR in their respective residence country in the form as required in such respective country or according to Form No. 04/N?-GDLK of this Decree. In case the taxpayer cannot provide the CbCR, the taxpayer shall provide written explanation for the reason, the legal basis and reference to specific provisions from the law of the counterparty jurisdiction that prohibits the taxpayer from providing a copy of the CbCR.”

This isn’t connected to the idea of public CBCR, nor is it linked to what’s happening with EU movement in this area, it’s a promising, independently minded move. It’ll be interesting to see if other countries follow suit…

Further reading:

The OECD – penalising developing countries for trying to tackle tax avoidance

Country by country reporting, a Tax Justice Network explainer

The author

Related articles

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026

California steps up for tax fairness

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

Tackling Profit Shifting in the Oil and Gas Sector for a Just Transition

The State of Tax Justice 2025

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

Bad Medicine: A Clear Prescription = tax transparency

The Financial Secrecy Index, a cherished tool for policy research across the globe