John Christensen ■ TTIP threatens ability to enforce fair taxes on corporations – report

In light of a new report showing how corporations are using secretive corporate courts to undermine national tax sovereignty, TJN has signed a letter to British Prime Minister David Cameron calling on him to call a halt to negotiations on so-called Investor-State Dispute Settlement provisions included in the framework of the Transatlantic Trade and Investment Partnership (TTIP) and a separate framework deal with Canada, known as the Comprehensive Economic and Trade Agreement (CETA).

In light of a new report showing how corporations are using secretive corporate courts to undermine national tax sovereignty, TJN has signed a letter to British Prime Minister David Cameron calling on him to call a halt to negotiations on so-called Investor-State Dispute Settlement provisions included in the framework of the Transatlantic Trade and Investment Partnership (TTIP) and a separate framework deal with Canada, known as the Comprehensive Economic and Trade Agreement (CETA).

A copy of the letter is attached at the foot of this blog.

London, 15 February 2016 – Corporations are regularly using secretive corporate courts to undermine the ability of countries to pass effective tax legislation, according to a new report, Taxes on trial: How trade deals threaten tax justice. The report warns that if the free trade deal being proposed between the EU and the USA were to come into force, it would massively increase the ability of corporations to sue member states of the EU over measures such as windfall taxes on exceptional profits, or use of taxation as a policy instrument such as a possible ‘sugar tax’.

This is just one section of the charge sheet

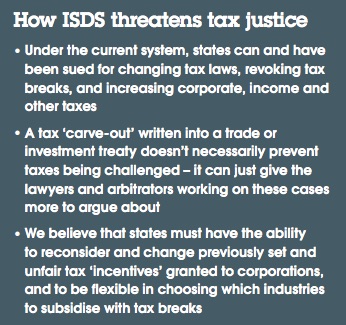

The report, published by Global Justice Now and the Transnational Institute, shows that corporations have used the ‘investor protection’ provisions of a variety of different trade deals to sue at least 24 countries from India to Romania over 40 tax-related disputes, and in some cases been able to successfully challenge and lower their tax bills. This investor protection is controversially an integral part of current free trade deals being negotiated between the EU and the USA (TTIP) and the EU and Canada (CETA) and is formally known as investor- state dispute settlement (ISDS).

Corporate tax evasion has become a growing public concern with media revelations of the tiny payments made by multinational giants such as Facebook and Google. Tax breaks cost developing countries as much as $138bn a year, money needed for healthcare and other critical public services. The report argues that under TTIP, if the UK or other member states of the EU, tried to introduce tax practices with social or environmental benefits that meant that companies had to pay more, they could be subjected to a law suit in a closed door ‘corporate court’ that could result in damages of billions of pounds being awarded to the company.

The European Commission was stunned by the strength of feeling about ISDS: a public consultation in 2014 found that 97% of thousands of responses were negative. A UN human rights expert and academic called ISDS a ‘revolution against international law.’

The report examines a number of case studies in more detail. For example:

- Vodafone, which has been involved in various tax scandals in the UK, has launched an arbitration claim against India that is still ongoing, after it was ordered to pay tax on an $11bn deal when it acquired a controlling interest in a major Indian phone company. Vodaphone had paid no capital gains tax on the deal because the transaction used a number of offshore companies.

- Food and drink corporate investors sued Romania successfully, winning a $250m award, over early termination of tax breaks, which had been specifically demanded by the European Commission for Romania to join the EU.

- US agribusiness giants Cargill and Archer Daniels Midland have successfully sued Mexico for introducing a ‘sugar tax’ on the sales of soft drinks containing high-fructose corn syrup.

The report also shows that supposed tax ‘carve-outs’, written into a trade or investment treaties, have not succeeded in stopping taxes being challenged and defeated.

The report is being released just before the next round of TTIP negotiations are due to begin in Brussels (22 – 26 February) when the negotiations on the investment chapter are officially due to resume. ISDS continues to be the most controversial aspect of the trade deal, to the point where the European Commission have been forced to propose an alternative system, which has been met with disdain from the US negotiators and business lobby. The biggest professional body of German judges recently said that there was “no need, nor legal basis” for the Commission’s proposal.

A number of civil society groups have written to prime minister David Cameron expressing similar concerns to those raised in the report and asking him to halt the TTIP negotiations (the letter can be found at the end of this press release).

That horse looks innocent enough . .

Nick Dearden, the director of Global Justice Now said:

“Despite the enormous public outcry over companies like Google and Amazon paying ridiculously small amounts of tax in the UK, the government is trying to sign us up to a trade deal that could effectively prevent us from bringing about laws that could address tax injustice. The ability to enact effective and fair tax systems to finance vital public services is one of the defining features of sovereignty. The fact that multinational companies would be able to challenge and undermine that under TTIP is testament to the terrifying extent of the corporate grab embedded in this toxic trade deal.”

Cecilia Olivet from the Transnational Institute said:

“The evidence of the dangers of these investment deals continues to mount. Not only do they affect health and the environment and cost taxpayers millions in legal fees, this report shows they also affect the ability of governments to tax corporations effectively. This is yet more money lining the pockets of corporate executives stolen from the public taxpayer. New trade deals such as TTIP and CETA have to be stopped and the public interest defended.”

Download the report.

Notes

The troubled history of ISDS

The European Commission was stunned by the strength of feeling about ISDS. A public consultation in 2014 found that 97% of the thousands of responses they received were negative.

A UN human rights expert and academic called ISDS a ‘revolution against international law’

The controversy and strength of feeling against it has been continuous– at one pointFrance was saying they wouldn’t sign TTIP if it was in.

The Commission was under so much pressure that in September 2015 they made a proposal for an alternative system that they’ve called ICS. Civil society thinks it has all the problems of ISDS – that it was essentially a rebrand with all the same problems.

US negotiators and business lobby are not keen at all on ICS proposal – they want the original ISDS in TTIP.

And in Germany (which has huge anti-TTIP sentiment – 250,000 people marched in Berlin against TTIP at the end of last year) the biggest professional association of judges has said there is no need, or legal basis for the ICS proposal.

Text of the letter to David Cameron, UK Prime Minister

Dear Prime Minister

We write to express our concern at the way bilateral and multilateral investment agreements are obstructing the ability of countries to decide their own tax law.

Through mechanisms known as Investor State Dispute Settlement (ISDS), countries are being successfully challenged by transnational corporations for making decisions about tax incentives and tax rates. Some of these challenges are being brought by shell companies registered in British territory.

We are particularly concerned that the negotiations on the Transatlantic Trade & Investment Partnership (TTIP) and the Comprehensive Economic & Trade Agreement (CETA) propose incorporating ISDS systems which will vastly expand access to such arbitration. We predict a real impact on tax sovereignty in the EU and North America as a consequence, regardless of whether conventional ISDS clauses are used or an Investment Court System is set up.

It is true that many bilateral investment treaties contain exemptions for tax matters. These exemptions are of varying effectiveness, but they have not stopped such cases being brought, or attaining a successful outcome. Timothy Lyons QC, a barrister and arbitrator with 39 Essex Chambers in London, commented recently in the Global Arbitration Review: “States often want to take the view that tax carve-out clauses protect them whenever a dispute arises in the context of tax. A number of arbitral awards show that is not the case.”

Our recent analysis of data and documents on hundreds of ISDS cases filed so far reveals foreign investors have already sued at least 24 countries from India to Romania over tax-related disputes. The true figures are likely to be even higher. This includes several cases where companies have used this system to successfully challenge, and lower, their tax bills.

Included in these cases are challenges: to undercut tax avoidance in India, to issue a windfall tax on energy profits in Ecuador, to remove tax incentives to comply with EU law in Romania and to introduce a sugar tax in Mexico. They all involve decisions where sovereignty should lie with the state. Unless a state can exercise such power, a government’s ability to improve the lives of people in their country will be impaired.

Most ISDS claims so far have been filed against developing countries. But richer states are increasingly being sued too.

We have discovered that at least 20 of the UK’s bilateral investment agreements, signed with countries from Belize to Turkmenistan, expressly extend “by diplomatic notes” cover to investors from Jersey and Guernsey and the Isle of Man, giving companies registered in these dependencies access to ISDS through Britain’s treaties. Several of the UK’s treaties have also been extended to cover investors from Hong Kong, the Cayman Islands, or the Turks and Caicos.

In one ongoing case, the Canadian mining company Gabriel Resources is using its subsidiary in the tax haven of Jersey to claim protection under a treaty signed between the UK and Romania. The company is suing Romania for halting the controversial Rosia Montana gold mine in Transylvania that has been the subject of mass opposition from local communities fearful of its environmental impacts.

Many ISDS cases also involve investments made in developing countries through tax havens. A case brought by the UK company Rurelec against Bolivia, for example, which ended in a multi-million dollar award against the country, centred on investments made by Rurelec in the Bolivian energy sector via intermediaries registered in the British Virgin Islands.

In light of this deeply worrying evidence, we call on the British government to:

- Halt the negotiations on all deals which include ISDS, most urgently TTIP and CETA

- Reject the new Investment Court System proposed by the EU Trade Commissioner, which would simply embed these concepts more firmly in international law

- Intervene in current ISDS cases which use shell companies in British territories, by advising arbitrators that you do not regard these companies as ‘British’. The case between a company called Gabriel Resources and Romania is particularity urgent

- Conduct an investigation into the impact of all current bilateral investment treaties to examine the impact of ISDS on tax sovereignty

- Renegotiate all bilateral investment treaties as they come due, to remove ISDS. These systems have proved ineffective in protecting tax sovereignty.

Tax justice requires binding international standards on transnational corporations. We finally urge you to support the initiatives at the United Nations to create international rules to hold transnational corporations to account for their human rights violations.

We would very much like to discuss the matter with you further.

Yours faithfully,

Nick Dearden, Global Justice Now

Cecilia Olivet, Transnational Institute

Prof Richard Murphy, City University

John Christensen, Tax Justice Network

Craig Bennett, Friends of the Earth

Emma Hughes, Platform

Blanche Shackleton, 38degrees

The author

Related articles

Vulnerabilities to illicit financial flows: complementing national risk assessments

A tax justice lens on Palestine

New article explores why the fight for beneficial ownership transparency isn’t over

UN Submission: A Roadmap for Eradicating Poverty Beyond Growth

A human rights economy: what it is and why we need it

Strengthening Africa’s tax governance: reflections on the Lusaka country by country reporting workshop

Do it like a tax haven: deny 24,000 children an education to send 2 to school

Urgent call to action: UN Member States must step up with financial contributions to advance the UN Framework Convention on International Tax Cooperation

Incorporate Gender-Transformative Provisions into the UN Tax Convention

Asset beneficial ownership – Enforcing wealth tax & other positive spillover effects

4 March 2025