Published:

2 June 2015Reading time:

3 minTags:

When we look back, might today be the day that momentum swung decisively against current international tax rules?

When we look back, might today be the day that momentum swung decisively against current international tax rules?

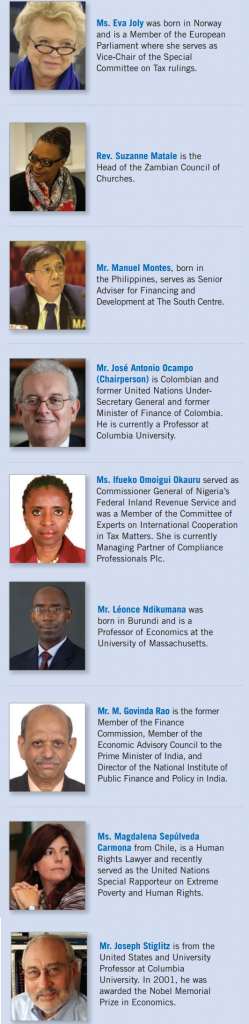

An independent commission made up of leading international economists, development thinkers and tax experts (see the graphic) has called for a radical overhaul of international corporate tax rules.

There are six main recommendations, set out below. Taken together, it’s possible that they will provide the basis for the kind of comprehensive reworking of tax rules that the G20 and G8 signally failed to deliver when they allowed the OECD mandate on BEPS (corporate tax Base Erosion and Profit-Shifting) to be watered down to a tweaking of the current system.

Here’s the start of the Commission’s press release:

“Trento, IT – Today, the Independent Commission for the Reform of International Corporate Taxation (ICRICT) launched a global declaration calling for an overhaul of the outdated international corporate tax system and demanding broad, sweeping changes in the current rules and governing institutions. The declaration will be discussed later today by a panel of ICRICT commissioners at the Trento Festival of Economics in Trento, Italy beginning at 5pm CET.

“Multinational corporations act and therefore should be taxed as single and unified firms – It is time for our leaders to be bold and recognize the legal fiction of the separate entity principle,” said Joseph Stiglitz, professor and Nobel Prize winning economist. “During the transition, leading developed nations should impose a global minimum corporate tax rate to stop the race to the bottom.”

Drawing on expert consultations held in New York in March this year, the ICRICT Declaration (pdf) contains recommendations for reform in six areas:

- Tax multinationals as single firms

- Curb tax competition

- Strengthen enforcement

- Increase transparency

- Reform tax treaties

- Build inclusivity into international tax cooperation

I can only recommend reading the full piece, but a few points stand out.

- Unitary taxation: States should ‘reject the artifice’ of current separate accounting, and tax MNEs as a single unit, apportioning profit among the jurisdictions in which they operate according to the relative scale of their economic activity in each. (We have pushed for this.)

- Public country-by-country reporting: States should make country-by-country reports (of MNEs’ economic activity, profits and tax) available to the public within 30 days of filing. (We have also pushed for this.)

- Public beneficial ownership: states should include the names of ultimate beneficial owners (the warm-blooded type) in public corporate registries. (We have also pushed for this.)

Following the IMF paper showing how developing countries appear to lose around three times as much revenue as OECD members (1.7% of GDP, or more than $200 billion), the pressure is really on the BEPS process to deliver wider progress.

And at present, despite the best efforts of OECD staff working on BEPS Action Point 11, it remains unclear if the final BEPS recommendations will include even sufficient transparency measures to allow the tracking of progress. Tom Bergin of Reuters summarises:

“[The report] said OECD proposals did not go far enough in raising transparency or taking account of developing country needs.”

This report will have influence. As the Wall Street Journal opines:

“the panel’s report could add momentum to a groundswell for major changes in taxation of global profits.”

It seems that there was a tactical political victory, before BEPS even began, for those who did not wish to see the rules opened up more widely. If world opinion continues to sway towards seeing that as an error, and the resulting process opens up the entire basis of international tax rules, that may turn out to have been a pyrrhic victory indeed.

Full disclosure: TJN is one of the organisations that helped to establish ICRICT, and Alex Cobham, TJN’s Research Director, is a member of its preparatory group. But nobody should imagine the commissioners have anything but carefully developed personal views on these issues.

The author

Related articles

")

2025: The year tax justice became part of the world’s problem-solving infrastructure

Tackling Profit Shifting in the Oil and Gas Sector for a Just Transition

The State of Tax Justice 2025

One-page policy briefs: ABC policy reforms and human rights in the UN tax convention

Bad Medicine: A Clear Prescription = tax transparency

The Financial Secrecy Index, a cherished tool for policy research across the globe

Lessons from Australia: Let the sunshine in!

Strengthening Africa’s tax governance: reflections on the Lusaka country by country reporting workshop