Published:

18 January 2021Reading time:

5 minIn the last months of 2020, Argentina issued two new resolutions requiring the filing of relevant information to the tax administration: beneficial ownership information on trusts (General Resolution 4879) and information on tax schemes (General Resolution 4838). These resolutions help put Argentina at the vanguard of availability of information with government authorities, joining many EU countries. However, unlike EU countries, Argentina is yet to make information publicly available.

Trusts’ beneficial ownership information

As described by our papers (here and here) trusts are especially problematic legal vehicles, creating a high degree of secrecy based on the fact that, unlike companies, they need not be incorporated or registered in order to become legally valid. In addition, trusts have very complex control structures, involving many potential parties such as a (legal or nominee) settlor, an economic settlor, trustees, protectors, beneficiaries, classes of beneficiaries, purposes, etc. Moreover, even if all trust parties are disclosed, trusts have managed to keep shielding their assets against tax authorities and other legitimate creditors, including victims of murder and sexual abuse.

A few months ago, we blogged about Argentina’s beneficial ownership registration based on the tax administration (AFIP) General Resolution 4967 of April 2020. (This regulation was then amended by General Resolution 4878. An updated and consolidated version of Resolution 4697 is available here). While we commended this improvement, we noted that it covered only legal persons but failed to extend the beneficial ownership obligations to trusts. Argentina’s General Resolution 3312 from 2012 was already pretty advanced, requiring many types of trusts and their parties to be disclosed to the tax administration. However, it referred only to legal ownership information.

However, the new General Resolution 4879 of October 2020 extended the Resolution 3312’s requirements to cover also beneficial ownership information for domestic and foreign law trusts. Importantly, the full ownership chain has to be disclosed whenever the party to the trust is a foreign legal vehicle. Additionally, all beneficial owners of those legal vehicles which are parties to the trust have to be identified as beneficial owners of the trust regardless of any threshold. In other words, if trust A has company 1 as its trustee. John has 1 share and Mary has the remaining 999 shares in company 1, both John and Mary will have to be identified as the beneficial owners of company 1 and of trust A.

Positively, all beneficial ownership information will be held by a single authority, the tax administration, facilitating cross-checks. On the negative side, information will not be made public. Additionally, it’s not clear how much coordination there is with local commercial registries to ensure that all incorporated entities file their beneficial ownership information with the tax administration.

Reporting of Tax Schemes

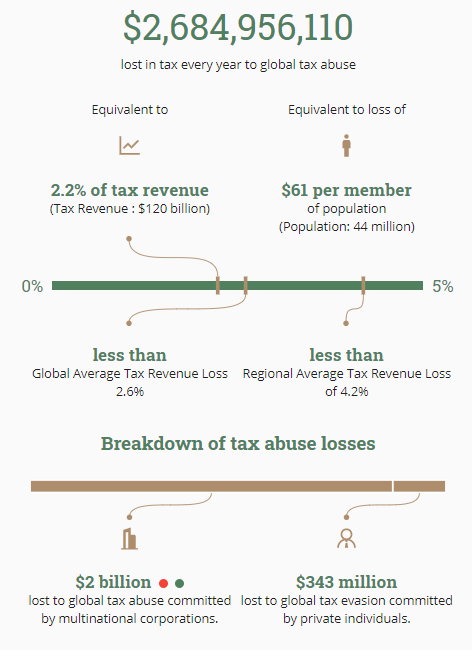

Tax abuse by multinationals and individuals continues to be a major problem, affecting state revenues and the guarantee of basic human rights. As our State of Tax Justice 2020 report described “Countries are losing a total of over $427 billion in tax each year to international corporate tax abuse and private tax evasion.”

In the case of Argentina, the Tax Justice Network’s Illicit Financial Flows Tracker (IFF Tracker) shows how much money is lost to tax abuse by multinationals and individuals:

In an attempt to tackle tax abuse, and in accordance with the OECD’s Action 12 of the Base Erosion Profit Shifting (BEPS), Argentina has issued General Resolution 4838 requiring taxpayers and tax advisers to report their tax avoidance schemes.

By doing this, Argentina joins the 27 EU Member States who are already requiring that taxpayers or tax advisers report tax schemes under the amendment to the Directive on Administrative Cooperation, known as DAC 6. As described by indicator 13 of the Financial Secrecy Index published in 2020, there were 31 jurisdictions which required tax advisers to report tax schemes. Apart from the EU, countries include Canada, Mexico, South Africa and the United States. Countries such as Canada, Israel, South Africa, the US and the UK also require taxpayers to report tax schemes. The US even requires them to report uncertain tax positions. Indicator 13 describes the reasoning that justifies the reporting of schemes:

There are several reasons to support the imposition of mandatory reporting of tax avoidance schemes. First, the reporting requirements help tax administrations to identify areas of uncertainty in the tax law that may need clarification or legislative improvements, regulatory guidance, or further research. Second, providing the tax administration with early information about tax avoidance schemes allows it to assess the risks schemes pose before the tax assessment is made and to focus audits more efficiently. This is significant mainly because, in many jurisdictions, tax administrations do not have sufficient capacity to fully audit a large number of the tax files. Thus, flagging certain files that carry a greater risk of tax avoidance is likely to increase the efficiency of tax administrations and their ability to increase tax revenues. Third, requiring mandatory reporting of tax schemes is likely to deter taxpayers from using these tax schemes because they know there are higher chances that files will be flagged, exposed and assessed accordingly. Fourth, such mandatory reporting may reduce the supply of these schemes by altering the economics of tax avoidance of their providers because a) they will be more exposed to claims of promoting aggressive tax schemes, increasing the risk of reputational damage, and b) their profits and rate of return on the promotion of these schemes is likely to be reduced because schemes are closed down more quickly. This is all the more true if contingency fees are part of contracts…

The difficulty in imposing mandatory reporting rules for tax avoidance schemes is the potential for ambiguity of whether the scheme is considered a tax avoidance scheme within the mandatory disclosure rules. In order to mitigate against this risk, the reporting obligation should not apply only to the taxpayer who uses the tax scheme or only to the promoter (tax advisers) of the scheme, but rather to both. This kind of double obligation is imposed in the United States. If both are obliged to report independently on the marketed/used tax avoidance schemes, the chances that tax administration will be able to detect hidden dubious schemes are significantly higher. Precisely because there are numerous and regular conflicts between the tax administration and taxpayers/advisers on the interpretation of tax laws, it should be expected that many tax schemes will be designed in grey areas which certain promoters might chose to interpret as not being subject to the remit of the reporting obligation. Third party reporting obligations increase the detection risk of these dubious schemes and thereby incentivises the reporting of a broader set of schemes”

Unfortunately, unlike DAC 6, Argentina’s Resolution 4838 failed to include more schemes. For instance, in relation to the automatic exchange of bank account information under the OECD’s Common Reporting Standard, countries are expected to adopt the OECD Mandatory Disclosure Rules which require the filing of schemes used to circumvent reporting under the automatic exchange of information system or to hide the beneficial owner behind opaque structures.

The other problem with Argentina’s Resolution, as with the EU’s DAC 6, is the issue of professional secrecy, where tax advisers and intermediaries may refuse to disclose information based on confidentiality rules.

We have blogged about the problem of professional secrecy, which goes beyond tax schemes and covers risks to money laundering, as described by the Financial Action Task Force. On a positive note, there are some cases of improvement as we blogged here, including a recent US case law granting the US tax administration access to a law firms’ list of clients who were potentially using the law firm’s advice to engage in tax evasion.

In conclusion, Argentina’s recent regulations keep pushing the country towards more transparency, although Argentina should not forget the importance of giving public access to information, especially on beneficial ownership. However, Argentina as well as the rest of the world will need to keep fighting against the damage of professional secrecy. Although confidentiality makes sense in some cases (eg to prevent a doctor from disclosing medical records, or the right to a fair trial), it should certainly not be used by the most powerful multinationals and high net worth individuals in order to keep engaging in abusive practices that erode state revenues, hurting the vast majority of people who are not part of the 0.1 per cent.

The author

Related articles

A heartfelt farewell to our dear Óscar

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

Fiscal hell or mirage? What Spain’s wage debate gets wrong

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas