The ICIJ’s MauritiusLeaks has produced a series of revelations about the behaviour of international investors using the law firm Conyers

Dill & Pearman in Mauritius, typically to hold their assets in other countries across Africa. But why Mauritius? Here we set out the key features of this small island in the Indian Ocean.

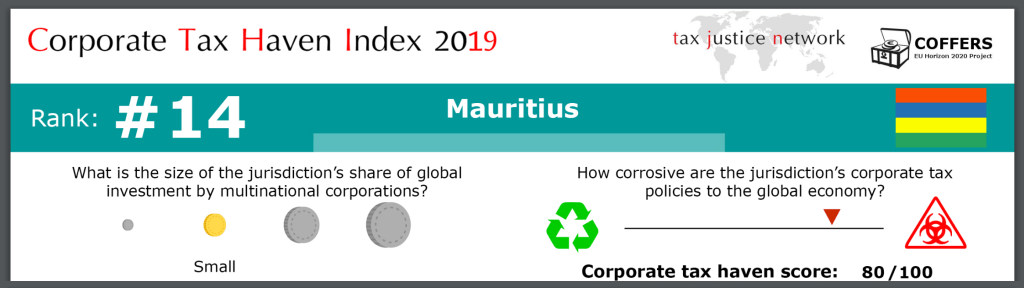

1. Mauritius is a leading corporate tax haven

The Republic of Mauritius lies around 2,000 kilometres to the east of Africa. A former British colony, Mauritius on its independence in 1968 relied on sugar production. But by the late 1980s, it had followed in the path of many UK dependencies and became increasingly captured by the lobbyists of offshore financial services, who bent its law and regulation to their own ends.

Mauritius ranks 14th on our recently released Corporate Tax Haven Index, because despite being a small player globally, its policies are very aggressively focused on undermining corporate taxation in other countries by attracting profit shifting.

Researchers at the International Monetary Fund estimate that the global revenue losses due to profit shifting amount to around $600 billion each year. We estimate a slightly more conservative $500 billion a year. The key drivers are the “conduit jurisdictions” such as Mauritius, that make themselves attractive for investors and multinational companies to shift profits out of the places where they actually make money.

2. Mauritius is among the most aggressive corporate tax havens towards African countries

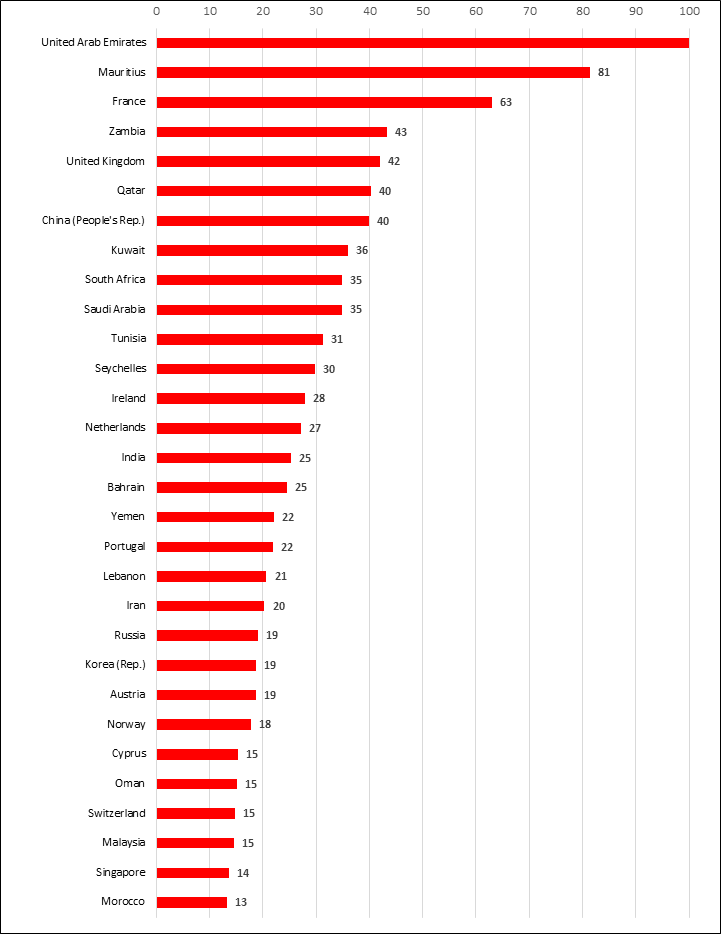

An important element in corporate tax havenry is the establishment of a network of bilateral tax treaties with other countries, which can reduce their ability to levy corporate tax before the profits are shifted away. The lower are the agreed rates of withholding tax, the less revenue a treaty partner can expect to hold onto.

Our research shows that the France and the UK have the most aggressive tax treaty networks worldwide, pushing treaty partners to accept worse terms. But in Africa, it is the United Arab Emirates and Mauritius which have the most aggressive treaty networks, and hence Mauritius is responsible for large revenue losses across the continent, as foreign investors channel their holdings in African countries through the island.

Normalised scores of most aggressive double tax treaty partners towards African countries

Following the publication of the Corporate Tax Haven Index in May 2019, the Senegalese government cancelled its tax treaty with Mauritius in June 2019.

3. Mauritius is one of the most financially secretive jurisdictions in the world

The provision of financial secrecy is central to “tax haven” success. This is the secrecy that allows the ownership of companies, trusts and foundations to be anonymous. That means, the holders of foreign bank accounts need not worry about information being provided to their home tax authorities, or that company accounts are hidden. The Financial Secrecy Index measures these policy failings and more, and Mauritius obtains an overall secrecy score of 72 out of 100 – one of the highest.

But Mauritius only ranks 49th on the Financial Secrecy Index, globally, because the volume of financial services that it provides to non-residents is relatively small in the grand scheme of things.

4. Globally, Mauritius is a small player and should not be singled out. Global solutions are needed.

In terms of corporate tax havens, the dominant players are UK overseas territories the British Virgin Islands, Bermuda and the Cayman Islands, followed by the leading European jurisdictions the Netherlands, Switzerland and Luxembourg. Among financial secrecy jurisdictions, Switzerland, the United States and the Cayman Islands dominate.

And so putting Mauritius up against a wall will not deliver the progress needed. Instead, raising global standards is key. We propose a UN tax convention which would require all jurisdictions to deliver, at a minimum, the ABC of tax transparency:

- Automatic exchange of tax information between jurisdictions, to end the scourge of bank secrecy – and fully multilateral, as opposed to the OECD Common Reporting Standard which systematically excludes most lower-income countries.

- Beneficial ownership transparency – public registers of the real owners, as standard for companies, trusts and foundations.

- Country by country reporting, publicly, by multinational companies to reveal misalignments between the location of their real economic activity, and where they declare their profits for tax purposes.

In addition, the current reform process for international tax rules must ensure, finally, that profits are apportioned between countries according to the location of real activity – that is, where companies have their employment and where their sales take place. At a stroke, this would eliminate much of the current incentives for profit shifting that Mauritius and other conduit jurisdictions exploit.

As immediate steps, African governments should consider revoking abusive tax treaties with Mauritius, the UAE, and other jurisdictions that consistently undermine their corporate tax base.

Mauritius should take the leaks as a last, clear signal: if it wants to be seen as a responsible neighbour in the world, rather than damaging all around it, the island must act now.

Image credit: © Ashok Prabhakaran

The author

Related articles

🔴UN tax convention hub – updates & resources

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

A 500-billion-dollar decision for the world: the revenue impacts of global unitary taxation

2 August 2026

Detecting Profit Shifting in Administrative Data: A South African Perspective

28 July 2026

A heartfelt farewell to our dear Óscar

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

I study the tax system of different countries of the world. Also interested in the creation of offshore companies around the world. Thank you for sharing information and your research!

Comments are closed.