We’re delighted to bring you a guest blog by Lukas Hakelberg, a researcher from the University of Bamberg – one of our partners in the EC-funded COFFERS project. The blog outlines the motivation and key findings of a study by Lukas and a colleague, Max Schaub.

We’re delighted to bring you a guest blog by Lukas Hakelberg, a researcher from the University of Bamberg – one of our partners in the EC-funded COFFERS project. The blog outlines the motivation and key findings of a study by Lukas and a colleague, Max Schaub.

We’ve been raising the alarm about the global impact of ‘Tax Haven USA’ as the world’s biggest financial centre, increasingly an outlier, resisting broader trends towards tax transparency. The study by Hakelberg and Schaub uses the Tax Justice Network’s Financial Secrecy Index in addressing the question of whether this behaviour has effectively redistributed financial activity in favour of the US, and at the expense of other secrecy jurisdictions.

The Redistributive Impact of Hypocrisy in International Taxation

The Obama administration’s Foreign Account Tax Compliance Act (FATCA) has been widely characterized as a watershed in the fight for increased financial transparency. The Act, which was adopted by Congress in March 2010, requires foreign banks to automatically report the account data of their US clients to the Internal Revenue Service (IRS), while imposing a 30% withholding tax on US-source payments going to incompliant financial institutions.

Owing to this sanctions threat, all countries hosting internationally active banks entered into bilateral FATCA agreements, committing themselves to remove legal barriers to the requested automatic reporting of account information. For traditional secrecy jurisdictions, this meant the removal of banking secrecy provisions that had previously prevented such transfers of data. Accordingly, they could also no longer turn down requests from third countries for additional information simply by referring to the domestic legal situation. By weakening the bargaining position of traditional secrecy jurisdictions, FATCA thus enabled the emergence of the multilateral automatic exchange of information (AEI) regime sponsored by the Organisation for Economic Cooperation and Development (OECD).

There is, however, an important caveat to this success story. The US government itself has neither signed the multilateral AEI agreement nor reciprocates automatic information reporting under its bilateral FATCA treaties.

As a result, secretive US states like Delaware or South Dakota enjoy a competitive advantage vis-à-vis other secrecy jurisdictions in the attraction of hidden capital.

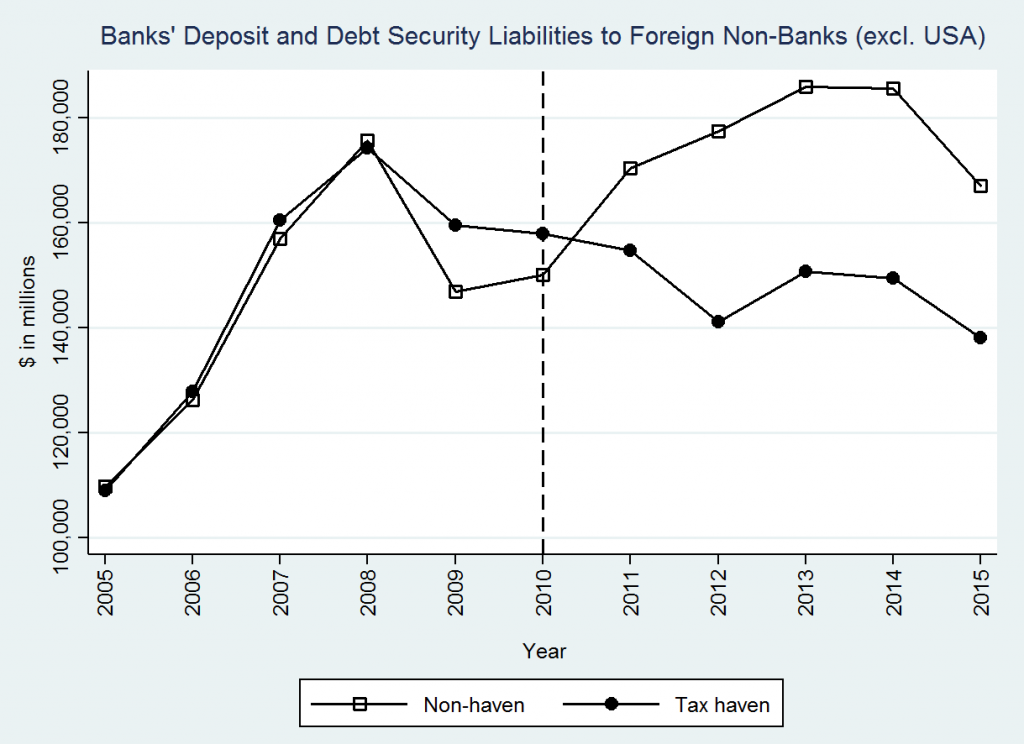

Against this background, my co-author Max Schaub and I wanted to find out to what extent this competitive advantage leads to an actual redistribution of financial wealth from traditional secrecy jurisdictions to the US. For an article just published with Regulation & Governance we therefore performed a difference-in-differences analysis comparing banks’ deposit and debt security liabilities to foreign non-banks in tax havens and non-havens before and after the adoption of FATCA in 2010.

Our results show that tax havens on average lost more portfolio investment to the introduction of the AEI, than to the 2008 financial crisis. In contrast, portfolio investment in non-havens grew rapidly between 2010 and 2014. This divergence in trends becomes even stronger when including the US in the non-haven group, which suggests that the government’s decision not to reciprocate the AEI has recently afforded the country an above average influx of foreign capital.

From a theoretical perspective, this confirms the US’s ability to redistribute financial wealth internationally through the enforcement of organized hypocrisy.

The entire study, including the full statistical analysis, is available on the Regulation & Governance website.

The author

Related articles

Public finance is feminist terrain

New Tax Justice Network reports on real estate transparency

Beneficial Ownership of Real Estate Around the World

7 July 2026

Integrating the Collection, Use and Exchange of Real Estate Ownership Information

7 July 2026

Introducing the Real Estate Secrecy Index

Indicator deep dive: Golden Visas

Finally, the European Court of Justice cracks down on trusts

Financial secrecy has entered the EU AML rulebook. What comes next?

Malta: the EU’s secret tax sieve