Published:

28 October 2016Reading time:

4 minThis week saw the re-launch of the European Union’s Common Corporate Consolidated Tax Base (CCCTB). The purpose of the CCCTB is to harmonise the rules around how multinational corporations are taxed across the European Union, and to switch from OECD tax rules to a unitary approach with formulary apportionment (more on that below).

The CCCTB was originally launched in 2011, after many years of discussion, but in the EU’s own words the proposals proved ‘too ambitious’ for member states. The immediate proposal now is but a baby step towards the bigger goal and we welcome the intention; but there is a long way to go before this will significantly impact on multinational profit-shifting, and there are important weaknesses that must be addressed even in the existing proposal.

What is the CCCTB?

The most ambitious part of the CCCTB is an attempt to create a single, harmonised tax base for multinational companies with operations in Europe. This means that large companies will report their profits across the whole European Union. Those profits will then be apportioned among countries, based on the real economic activity taking place in that country (e.g. people and sales), so that countries can then choose how much to tax those apportioned profits (i.e. there will be no harmonisation of rates).

This system is intended to lower compliance costs for multinationals operating across multiple EU jurisdictions, but also to prevent multinationals from apportioning their profits to low or no tax jurisdictions where they have few or any staff, starving countries where they are really operating, of tax revenues.

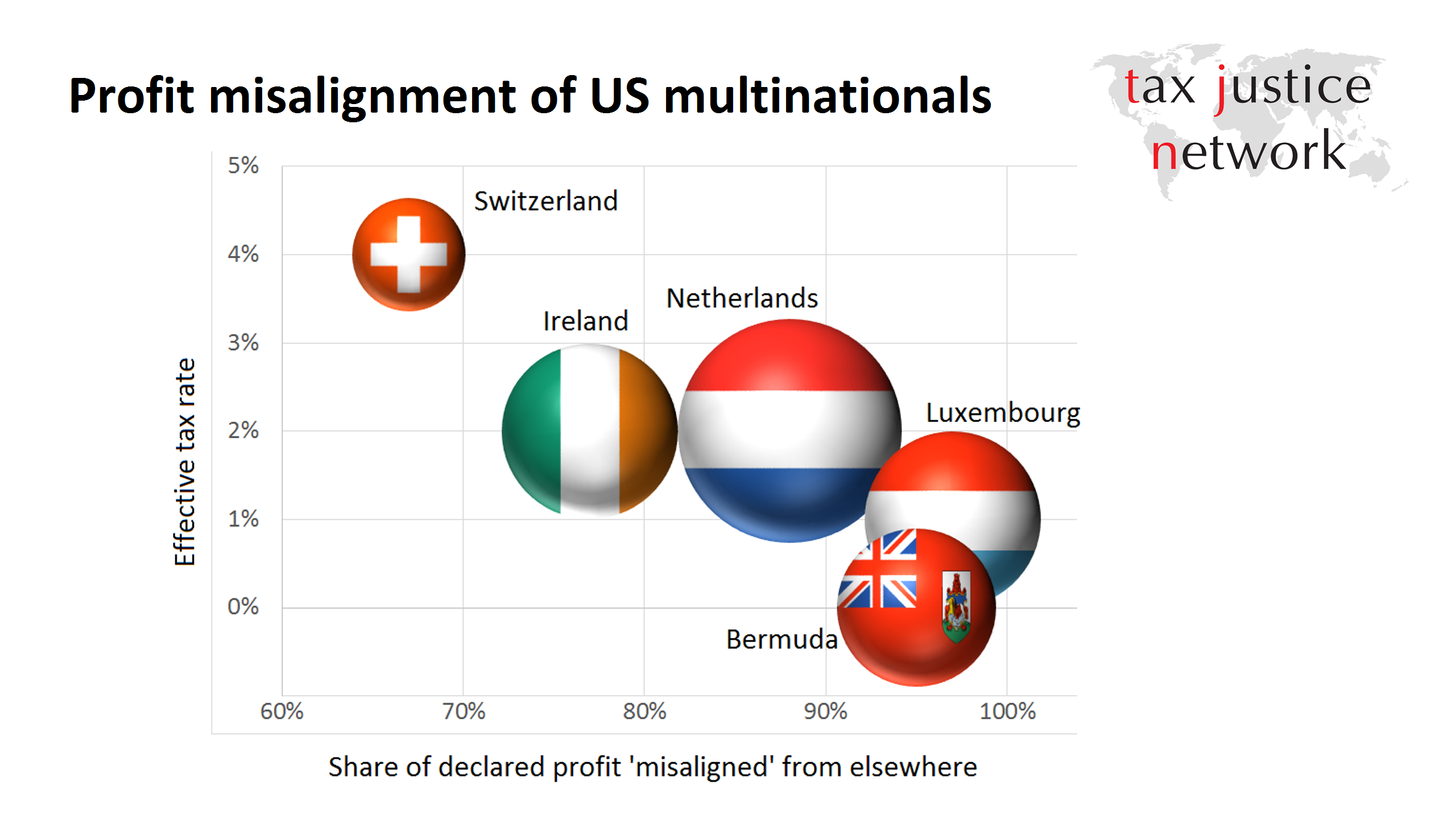

As our research into US multinationals has shown, there are a number of EU jurisdictions which offer near-zero effective tax rates in order to poach the taxable profit from their neighbours. The CCCTB would go a very long way towards addressing this anti-social behaviour, and many of the high-profile avoidance cases such as Google and Facebook.

All of this has the potential to make a huge difference to the fight against tax avoidance and evasion. Tax avoidance is facilitated by mismatches between legislation between different countries, and by companies shifting profits from high tax to low tax countries.

As Tove Maria Ryding, from our partners Tax Justice-Europe said:

“We all stand to benefit from this proposal. When multinational corporations are not paying their fair share of taxes it means that we have to pay more taxes and that there is less money in the public sector for hospitals and schools. This is a big step forward.”

Why now?

The CCCTB has been in the works for a very long time. The European Parliament reported on the issue in 2005. The European Commission launched the proposals the first time in 2011. At that time the proposals were killed off by vocal opposition from member states, and as measures such as this require the agreement of all member states, the proposals were dead in the water.

Back in 2011 the most vocal opponent of the CCCTB was the United Kingdom, who saw it as a threat to their goal to create a “competitive” system of corporate taxation (aka a tax haven). With the UK now choosing to leave the EU, this proposal may now have more legs. Although in theory the UK could still block it, interfering with the rules of a club that they are seeking to leave would do very little to improve their negotiating position in the Brexit negotiations. However, it must be said, that the UK were not the only opponents at the time.

It is also clear that we are moving on from the world of the mid-2000s when these proposals were first made when too many people thought that tax avoidance by multinationals simply wasn’t an issue. It is clear that the EU is responding to the demand for more action following the many high profile stories of tax abuse, including most lately, the Panama Papers.

Will it work?

Of course the devil will be in the detail, and there is still long road to travel before the measures are implemented. The most ambitious parts of the CCCTB, the consolidation of the tax base and apportionment of profits between nations is still being negotiated and so could never happen.

But even without the ‘third C’, two CCs are an important step forward, particularly for developing countries which have often been the victim of companies using Europe as a tax haven. The proposals also contain a number of other measures for dealing with mismatches between tax rules in different countries. As Francis Weyzig of Oxfam Novib told us:

“This [the anti-avoidance package without consolidation] is the core of the package that really matters to developing countries. If agreed, it will be a big improvement. It will do away with all patent boxes in EU member states, eliminate the double Irish, eliminate Dutch hybrid structures (multi-billion dollar overseas cash boxes) widely used by US-based multinationals, and replace the harmful Belgian notional interest regime with something less harmful.”

Others have highlighted that the elimination of patent boxes is ‘compensated’ by the introduction of massive tax deductions for R&D. In combination with other elements, this risks the overall package seeing the EU take a further step down the foolish road of tax ‘competition’ – a race to the bottom which no state, nor its citizens, can win. This has the potential also to make the EU more of a problem for lower-income countries, as they seek to exert their own taxing rights.

Finally, Richard Murphy raises a fundamental problem with the current hopes for a CCCTB: that the data generated under International Financial Reporting Standards is simply not fit for tax purposes. Can accounting standard-setters finally rise to the challenge, or is there a need to develop separate tax reporting standards?

Unitary tax: the direction of travel?

How far the EU will manage to go with the CCCTB is an open question. There will be many, including the TJN, keeping a close eye on how these proposals advance. But we are heartened by the Commission’s appetite to move to a unitary basis for taxing multinationals. Other economic blocs around the world are likely to give increasingly serious consideration to such an idea – especially as the OECD’s BEPS reforms are increasingly seen to have failed to reduce the gross misalignment of taxable profits with real economic activity.

The author

Related articles

When measurement is political: Accounting for natural resources and the true location of sales under unitary taxation

A 500-billion-dollar decision for the world: the revenue impacts of global unitary taxation

2 August 2026

Detecting Profit Shifting in Administrative Data: A South African Perspective

28 July 2026

Four definitions to change the world: Struggles over meaning in the UN tax convention negotiations

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026

California steps up for tax fairness

The bitter taste of tax dodging: Starbucks’ ‘Swiss swindle’

The tax justice stories that defined 2025

Admin Data for Tax Justice: A New Global Initiative Advancing the Use of Administrative Data for Tax Research

")