Published:

29 June 2026Reading time:

6 minDebates about taxation are often shaped less by evidence than by politically convenient narratives. Across many countries, claims that taxes are the primary cause of low wages, weak growth or economic stagnation frequently gain traction despite limited empirical support. For those concerned with tax justice, the issue is not whether taxes should ever be criticised, but whether public debate is grounded in evidence rather than assumptions.

Spain offers a useful example. Arguments that employer social contributions are the main cause of stagnant wages have become increasingly prominent in political debate. Yet the available evidence suggests a more complex picture, raising broader questions about how tax policy is discussed and whether tax cuts are being presented as solutions to problems they may not actually address.

The only thing more disappointing than Spanish wages is the political debate surrounding them. According to the OECD, Spain’s real wages have grown just 5% since 1995, one of the lowest rates in the developed world. That figure deserves a serious diagnosis. Instead, like in many political arenas, opposition parties and outlets offer a comfortable narrative, statistically questionable and with solutions that would resolve nothing except the political problem of having to talk about the real economy.

The Spanish debate illustrates how discussions about taxation can become detached from the available evidence. Rather than focusing on the structural causes of wage stagnation, it increasingly seeks to blame unsatisfactory salaries on the burdens corporations must pay to fund increasingly skimpy welfare states. At least in Spain’s case, however, the data does not support that narrative, and there is little reason to believe that lower payroll taxes would deliver the wage growth their advocates promise.

The Argument and Its Trap

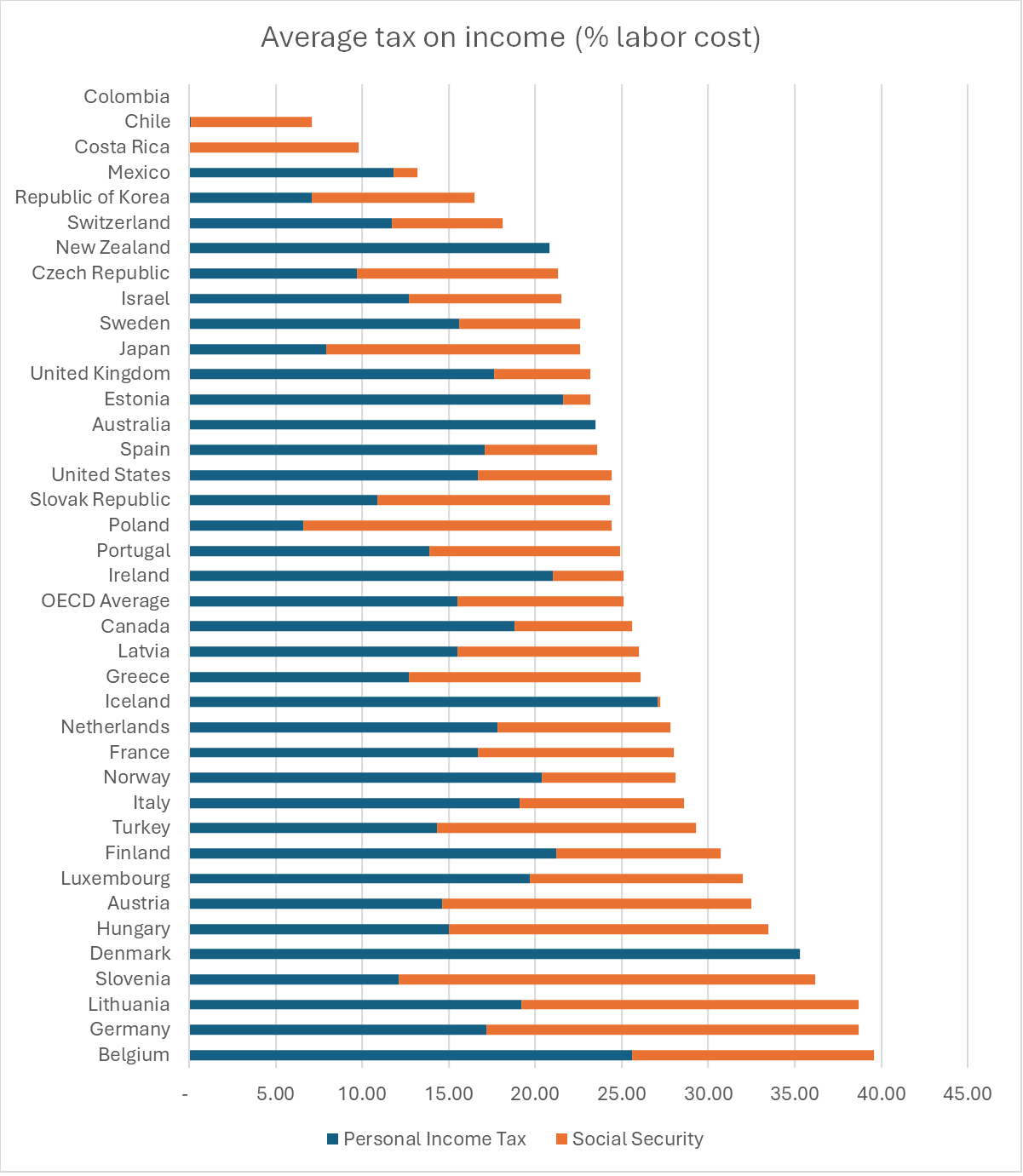

Source: Own elaboration based on OECD data

In Spain, the “tax hell” discourse isn’t new, but it’s taken on a fresh form. Faced with the evidence that Spain’s personal income tax isn’t particularly high compared to its peers, its proponents have shifted the argument toward employer social contributions, in the form of payroll taxes.

They state that a Spanish employer pays approximately 30% on top of gross wages in Social Security contributions; once you add what the worker pays, you arrive at a total burden that supposedly turns Spain into a disguised tax hell. The following chart has been circulating for months, republished by outlets and commentators of a libertarian and conservative bent.

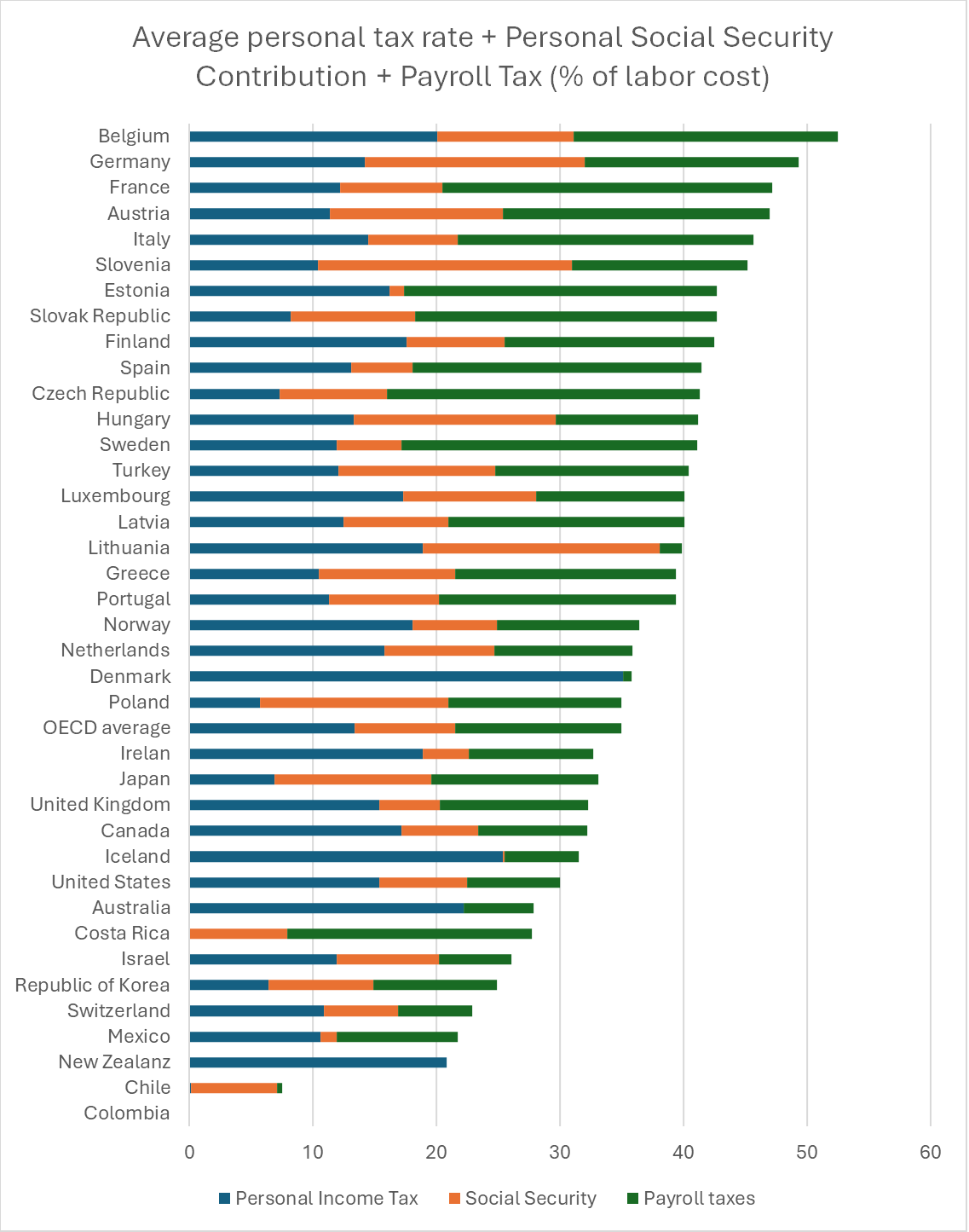

Source: Own elaboration based on OECD data

In the table, you can indeed observe that Spain has above-average payroll tax contributions on behalf of employers, which contribute to pensions and unemployment benefits and are known in Spain as social security contributions. Those parties and outlets who wish to lessen Spain’s already below-average tax-to-GDP ratio have seized on this data point.

Leader of the center-right opposition People’s Party (PP), Alberto Núñez Feijóo, summarised the argument recently: “Spain collects like a Nordic country but can’t have services like a third-world country.” Far-right Vox’s MP José María Figaredo went further, claiming that “the average worker has the state take roughly 50% of their work every year”, a figure constructed by counting employer contributions as wages stolen from the worker. Vox’s parliamentary spokesperson at the time, Iván Espinosa de los Monteros, drew a similar conclusion: the way to “raise wages” isn’t to increase the minimum wage, but to cut contributions and taxes. The cause behind low wages is supposedly well-known and easy to cure. But both the diagnosis and the cure might be mistaken.

Spanish Fiscal Pressure in Context

According to Eurostat, Spain’s total tax take, taxes and contributions combined, represented 37.3% of GDP in 2023, below the EU average of 40.4%. France sits at 46.1%, Belgium at 44.8%, Austria at 43.1%, Italy at 42.4%. If Spain is a tax hell, most of Western Europe has been burning at a much higher temperature for decades.

Admittedly, social contributions represent 34.1% of Spain’s total revenue, against an OECD average of 24.8%. But Spanish companies offset that higher contribution burden with a corporate tax whose effective average rate, after deductions, depreciation, and special regimes, sits among the lowest in Western Europe. Social contributions aren’t an additional tax on businesses; they’re compensating for a corporate income tax whose effective rate, at 15.4% in 2023, sits well below the OECD average of 20.2%. Changing the label doesn’t change the bill.

Would It Reach Wages?

You could argue that even if contributions function as an alternative business tax, cutting them would still create room to raise net wages. This trickle-down argument has permeated public discussions for decades. In Spain, that simple logic only holds up until you look at what actually happened.

In 1997, under José María Aznar’s PP government, the labour reform cut employer contributions by between 40% and 90% for permanent contracts targeting workers under 30 and over 45. Columbia University economist Ferrán Elías analysed the real effect using Social Security administrative data on more than one million workers. His conclusion was that the reduction generated a modest employment effect among workers under 30, a 2.42% increase in hirings, but wages didn’t move. For workers over 45, not even that. The tax cut translated into a transfer to companies, funded by taxpayers.

The academic research group Equalitas, studying the same reform, found that the slight wage improvement observed in that period came from the simultaneous reduction in dismissal costs, not the contribution cut. Their phrasing is direct: “with a weak link between contributions and benefits, payroll taxes are not fully passed on to employees, and employment falls.”

Additionally, the most exhaustive review of the literature for Spain, by Ángel Melguizo in Hacienda Pública Española, reaches the same wall: “results are not robust, ranging from full pass-through to zero pass-through.” The outcome depends on collective bargaining structure. In Spain, sectoral agreements set wage floors for the vast majority of private sector workers regardless of what a company contributes. Hence, the tax saving simply doesn’t reach the worker’s pocket.

The Real Problem

Spain’s economy is overly concentrated in tourism, hospitality, and construction, sectors of low productivity and modest pay, with chronically insufficient investment in R&D and a dual labour market that weakens workers’ bargaining power. According to BBVA Research, the gap between productivity and wages, not fiscal pressure, is the central explanation for Spain’s wage stagnation. Cutting contributions doesn’t build a manufacturing industry, generate patents, or improve vocational training. It’s like trying to modernise the country by changing the ministry’s logo.

What Happens in Government

Furthermore, anti-fiscal rhetoric against left-of-centre administrations cools fast upon reaching office. In Italy, with a fiscal burden of 42.4% of GDP, Giorgia Meloni arrived promising a tax revolution. The headline achievement of her 2026 budget was an income tax cut that returned €408 per year to executives, €123 to office workers, and €23 to manual workers. Less a revolution, more finding a twenty-euro note in an old coat pocket.

The Spanish precedent is more direct. Few prime ministers have captured the gap between rhetoric and reality with such inadvertent honesty as former Spanish Prime Minister Mariano Rajoy, “I said I was going to cut taxes and I am raising them.” His government raised standard VAT from 18% to 21%, the reduced rate from 8% to 10%, and income tax rates by up to seven points, the largest tax increase in Spanish democracy according to the Ministry of Finance itself. Unfortunately, this was part of an austerity drive more concerned with maintaining the creditworthiness of Spanish bonds than with redistributing and reinvesting Spanish wealth.

Poor Debate, Poor Economy

Undoubtedly, the Spanish tax system is improvable, and Spanish net wages are poor relative to European neighbors. The failure to deflate income tax brackets has had a real negative effect on middle and lower earners, and there are VAT categories worth revising. There’s a serious fiscal conversation to be had. But that’s not what’s currently on air.

If PP or Vox reached government and cut employer contributions, the evidence gives no reason to expect higher wages. The most likely result is a larger public deficit and better margins for Ibex companies that just closed their best year since 1993, up 49% and at historic highs, without any of that pulling wages up with them. Low wages are the product of an economy that hasn’t modernised its productive structure in decades. That’s the debate Spaniards deserve to have.

Editor’s note: Public debates about taxation are often shaped as much by political narratives as by evidence. In this guest article, Nicolas Brennan Hernandez, an economist specialising in international trade and political economy, examines the current debate on wages and taxation in Spain, arguing that tax policy discussions should be grounded in empirical evidence rather than misleading rhetoric. The views expressed are those of the author.

The author

Related articles

The European Court of Human Rights has upheld the weaponisation of privacy to restrict tax authorities’ access to banking data

What we learned from three years of conversations on poverty beyond growth

Q&A on California’s proposed legislation on Worldwide Combined Reporting (WWCR)

27 May 2026

California steps up for tax fairness

Finally, the European Court of Justice cracks down on trusts

Joint submission: International financial architecture, debt and the right to education

20 May 2026

Taxing Ethiopian women for bleeding

Tax justice and the women who hold broken systems together

")

What Kwame Nkrumah knew about profit shifting

The last chance

2 February 2026