Dan Neidle, a tax lawyer who recently retired from the multinational law firm Clifford Chance, and Richard Murphy, a professor of accounting practice at Sheffield University who resigned as a member of the Tax Justice Network in 2007 and as Tax Justice Network company secretary in 2009, have republished their criticisms of the Tax Justice Network’s State of Tax Justice 2023. While we have previously provided a point by point explanation of the errors on which these criticisms rest, we are always keen to engage with other views. Below we summarise the criticisms and again provide responses, but first we deal with the main concern raised.

The State of Tax Justice reports how much tax countries lose to two types of cross-border tax abuse: offshore tax evasion by individuals and corporate tax abuse by multinational corporations. The primary claim against the State of Tax Justice is that the report overestimates the scale of hidden wealth held offshore by individuals in its calculations.

This is also the primary error in the criticisms, because the State of Tax Justice report does not calculate the scale of hidden offshore wealth. The estimate on the scale of hidden offshore wealth used in the report, as set out in the methodology, is sourced from a separate study commissioned by the European Commission and carried out by ECORYS, a respected research institute. The estimates from ECORYS are widely regarded as the best available estimates on the scale of hidden offshore wealth.

The ECORYS study uses an established methodology initially developed by the economist Gabriel Zucman, in his 2013 paper published in the leading Quarterly Journal of Economics.

What the State of Tax Justice report does calculate is the distribution of hidden offshore wealth, rather than the scale. That is, the report evaluates where the wealth hidden offshore should be declared for tax purposes, not how much wealth is hidden offshore. This is the report’s original contribution to the field. The report applies its evaluation of distribution to ECORYS’s calculation of scale to determine how much tax each country loses to offshore tax evasion.

In its other component, the State of Tax Justice does calculate the scale of corporate tax abuse using the now well-established “misalignment methodology.” Almost all criticism raised against the State of Tax Justice has focused on the scale of hidden offshore wealth used in the report, however, which, as stated, is sourced from ECORYS.

This fundamental misunderstanding of the State of Tax Justice’s methodology unfortunately forms the basis of almost all the claims raised against the report. On top of this, many of the claims also attack assumptions that are simply not made, despite the actual assumptions being documented in the methodology paper.

Estimating the impacts of behaviour that is deliberately hidden is of course challenging, and we are always open to critical comments and inputs in good faith. We recently identified a coding error in our own analysis, for example, and have issued a full and prominent correction. We are committed to improving the technical quality of the analysis upon which policy debates are based. Having robust evidence is far too important to justify defending an error.

In the case of the current criticisms, however, the Tax Justice Network publicly responded some years ago, and demonstrated in detail that the criticisms were insubstantial and often based on an erroneous understanding of our methodology. Nonetheless, these debunked criticisms of our report continue to be repeated, and have even been used by lobbyists to misdirect media. One critic even linked to our previous detailed response while claiming we had never responded(!).

Most recently, Cayman Finance has quoted these criticisms in an attempt to discredit our research – something Cayman Finance has done in the past, and to which we also responded at the time.

In light of this, we are again providing below an explanation of the errors that underpin these claims. As always, we invite further discussion should there be substantive points.

Breakdown of claims

Claim: The State of Tax Justice’s calculation of the scale of hidden offshore wealth is too high.

Fact: The State of Tax Justice does not calculate the scale of hidden offshore wealth. The report calculates the distribution of hidden offshore wealth, that is, where the wealth hidden offshore should be declared for tax purposes, not how much wealth is hidden offshore. The estimate on the scale of hidden offshore wealth used in the report is sourced from a separate study commissioned by the European Commission and carried out by ECORYS.

The ECORYS study concludes that the scale of hidden offshore wealth is 11.4% of global GDP. The ECORYS study uses an established methodology initially developed by Gabriel Zucman, in his 2013 paper published in the Quarterly Journal of Economics, which is one of the most highly-ranked economics journals in the world. Zucman recently received for his work on tax the John Bates Clark medal, a major prize given to an economist under the age of forty who is judged to have made a significant contribution to economic thought and knowledge.

For estimates of GDP, the State of Tax Justice sources data from the World Bank. Where World Bank GDP data is not available for a country, GDP data is used from the UN. If UN data is also not available, GDP data is used from the CIA.

The State of Tax Justice applies its evaluation of the distribution of hidden offshore wealth to ECORYS’ calculation of the scale of hidden offshore wealth to determine how much tax loss each country suffers to offshore tax evasion.

While the estimates from ECORYS used in the State of Tax Justice report are widely regarded as the best available estimates on the scale of hidden offshore wealth, there remain a number of limitations in these estimates. These stem largely from the limited availability of data on secretive offshore practices. The State of Tax Justice discusses and take several steps to address these limitations in the methodology.

However, the criticisms raised by Dan Neidle and Richard Murphy do not address the limitations in ECORYS’s estimates nor Gabriel Zucman’s method, but stem from a gross misunderstanding of what the State of Tax Justice’s methodology is evaluating.

Claim: The State of Tax Justice makes several false assumptions in its methodology, which result in the report overestimating the scale of hidden offshore wealth.

Fact: The State of Tax Justice’s methodology does not make the assumptions it is accused of making, as is clearly evidenced by the methodology paper. These erroneous claims also mistake the State of Tax Justice’s methodology for evaluating the distribution of hidden offshore wealth, for a methodology for calculating the scale of hidden offshore wealth (which is actually calculated by ECORYS, and also does not make the claimed assumptions).

See claims on assumptions

Claim: The methodology ignores the impact of FATCA/CRS on hidden offshore wealth.

Fact: The methodology accounts for the impact FATCA/CRS, which ECORYS’s study finds had no material impact on the scale of hidden offshore wealth.

The Common Reporting Standard (CRS) and the US’s Foreign Account Tax Compliance Act (FATCA) are two forms of automatic exchange of information: a data sharing process designed to expose corporations and individuals whenever they hide money in foreign banks to appear less wealthy to their governments and underpay tax.

The CRS is based on a reciprocal exchange of information between countries, which more than 100 jurisdictions are participating in today. FATCA is based on a one-way flow of information, which sees countries share information with the US in return for ensuring their financial institutions retain access to US markets.

The Tax Justice Network was an early advocate for automatic exchange of information and continues to campaign for more robust and effectives forms of the transparency measure on a range of financial assets.

The CRS was approved in 2014, and exchanges between countries first began in 2018. FATCA was enacted by US Congress in 2010.

It has been claimed that the State of Tax Justice has failed to take into account the impact of CRS exchanges beginning in 2018.

This claim is based on the hypothesis that the start of CRS exchanges in 2018 resulted in the dramatic reduction in the scale of undeclared offshore wealth, to a level far below that used in the State of Tax Justice assessment.

This hypothesis, however, was already proved false in 2021. The scale of hidden offshore wealth in 2018 following the start of CRS exchanges remained at 11.4 per cent of global GDP, as estimated by ECORYS, compared to 11.6 per cent in 2017, as estimated by Alstadsaeter, Johannesen and Zucman in a study published in the highly-regarded Journal of Public Economics.

The ECORYS study looks specifically at the introduction of the CRS. In common with other studies, they find a relatively concentrated drop in the holdings of bank accounts in smaller “international financial centres” (for the EU, the volume of such bank deposits falls by 8 per cent between the first quarter of 2017, and the third quarter of 2019). It is the value of other offshore assets, and of equity holdings in particular, that results in ECORYS estimating much higher tax losses for EU countries in 2017 and 2018 than any year since their analysis begins in 2004.

While the evaluation of the distribution of country-level tax losses in the State of Tax Justice report follows a different methodology, the results are broadly consistent with the ECORYS finding that FATCA/CRS had had an immaterial impact on overall EU losses to offshore tax evasion. As ECORYS note, there are a multitude of asset types (including real estate and a range of financial assets) as well as ownership structures (including loans and equity through interposed companies) that are not subject to information exchange and are commonly used by wealthy individuals.

In short: the estimate on the scale of hidden offshore wealth calculated by ECORYS does include the impact of FATCA/CRS, and so these are accounted for by the State of Tax Justice. It’s just the impact has been minimal, at least up to the year of the data in question.

This weak impact is something that the Tax Justice Network and other researchers had warned of, and have explored and highlighted at some length. One reason is that the US does not participate in information exchange, and this has led to undisclosed bank deposits moving from smaller tax havens to the US as we predicted. Another is that the CRS is too limited in scope, and a lot of new financial products have been created to be non-reportable under FATCA and CRS.

If anything, it is possible that the narrowness of FACTA/CRS’s scope of coverage has increased the attraction of the portfolio assets covered by ECORYS, since these are not reportable. This is likely to include financial accounts (or very close substitutes) which have been specifically designed and marketed as non-reportable under FATCA and CRS. In defence of the CRS, the overall lack of impact in reducing tax losses does cover some reduction in undeclared offshore accounts; only that this is offset elsewhere, including by rising equity prices in 2017-18.

An academic paper by two Tax Justice Network researchers on the effectiveness of automatic exchange of information (AIE) arrives at three findings:

“First, we find that more secretive jurisdictions manage to keep more of the secrecy they supply to other countries uncovered by AIE via engaging in a strategy of selective resistance. Among those highly secretive jurisdictions, the OECD’s dependent territories play a crucial role. Second, we report that OECD countries are better than other countries at using AIE to target their most relevant secrecy jurisdictions. Third, we show that EU member states are better at targeting their most relevant secrecy jurisdictions with AIE rather than by means of blacklisting. Overall, our findings suggest that hypocrisy lies at the core of both the OECD AIE system and the EU’s blacklisting exercise.”

And on the effectiveness of global financial transparency more widely, an academic paper published this year by Petr Janský, Dariusz Wójcik and the Tax Justice Network’s Head of Research Miroslav Palanský finds:

“They [findings] do, however, show that while OECD countries are relatively more transparent, their former colonies, with continued links with and dependency on former colonial powers, exhibit little improvement. Put together, our findings show that while some progress towards global financial transparency has been achieved, it is shallow and very uneven, with convergence potentially replacing a race-to-the-bottom dynamic.” This is not to say that CRS has not been successful in providing some countries with transparency about certain types of financial accounts, and that is why the Tax Justice Network had long campaigned for the introduction of such multilateral measures. But the narrowness of the OECD approach, coupled with the noncompliance of the US and the effective exclusion of most lower income countries, means that a great deal of offshore wealth remains entirely hidden from tax authorities.

The methodology uses data from the Bank for International Settlements on offshore bank deposits to help determine the distribution of hidden offshore wealth. The Bank for International Settlement does not distinguish between personal deposits and corporate deposits in this data.

It has been claimed that the State of Tax Justice’s methodology does not make this clear about the data and instead assumes all deposits captured in this data to be personal deposits. This would mean the methodology treats all these bank deposits as belonging to individuals, and so overestimates the scale of wealth hidden offshore by individuals by lumping in bank deposits that actually belong to corporations.

The methodology, however, does explicitly explain that the data from the Bank for International Settlements does not distinguish between personal and corporate deposits, and goes on to explain how this data limitation is dealt with. The methodology is clear that the bank deposits captured in the data from the Bank for International Settlements do not all belong to individuals, and they are not treated as such by the report.

In addition, this data from the Bank for International Settlements is not used to calculate the scale of hidden offshore wealth, as it is claimed. The data is used to help determine the distribution of hidden offshore wealth, in other words, to attribute these bank deposits to their origin countries. While the data cannot readily indicate which offshore bank deposits belong to individuals and which belong to corporations, it does show which offshore destinations are most popular for wealth coming out of different countries, whether that wealth comes from individuals or corporations. This geographical pattern revealed by the data can be expected to be similar for both personal and corporate deposits as the pattern is often informed by regulations, treaties, service providers and legal structures in place in countries and in between countries. (We would welcome new research that identifies any specific patterns in relative shares of offshore deposits of individuals and corporations, by country of residence. At present, however, we do not see a basis to vary from the assumption that the ratio of individual to corporate deposits considered to be uniform across residence jurisdictions.)

The use of the data from the Bank for International Settlements in this way to determine distribution of hidden offshore wealth follows the method published in the highly-regarded Journal of Public Economics in 2018 by Alstadsaeter, Johannesen and Zucman.

Claim: The methodology does not recognise that there may be valid commercial reasons for some abnormal deposits.

Fact: The methodology allows for genuine commercial reasons by identifying only abnormally high levels of deposits that are associated with the highest levels of bank secrecy.

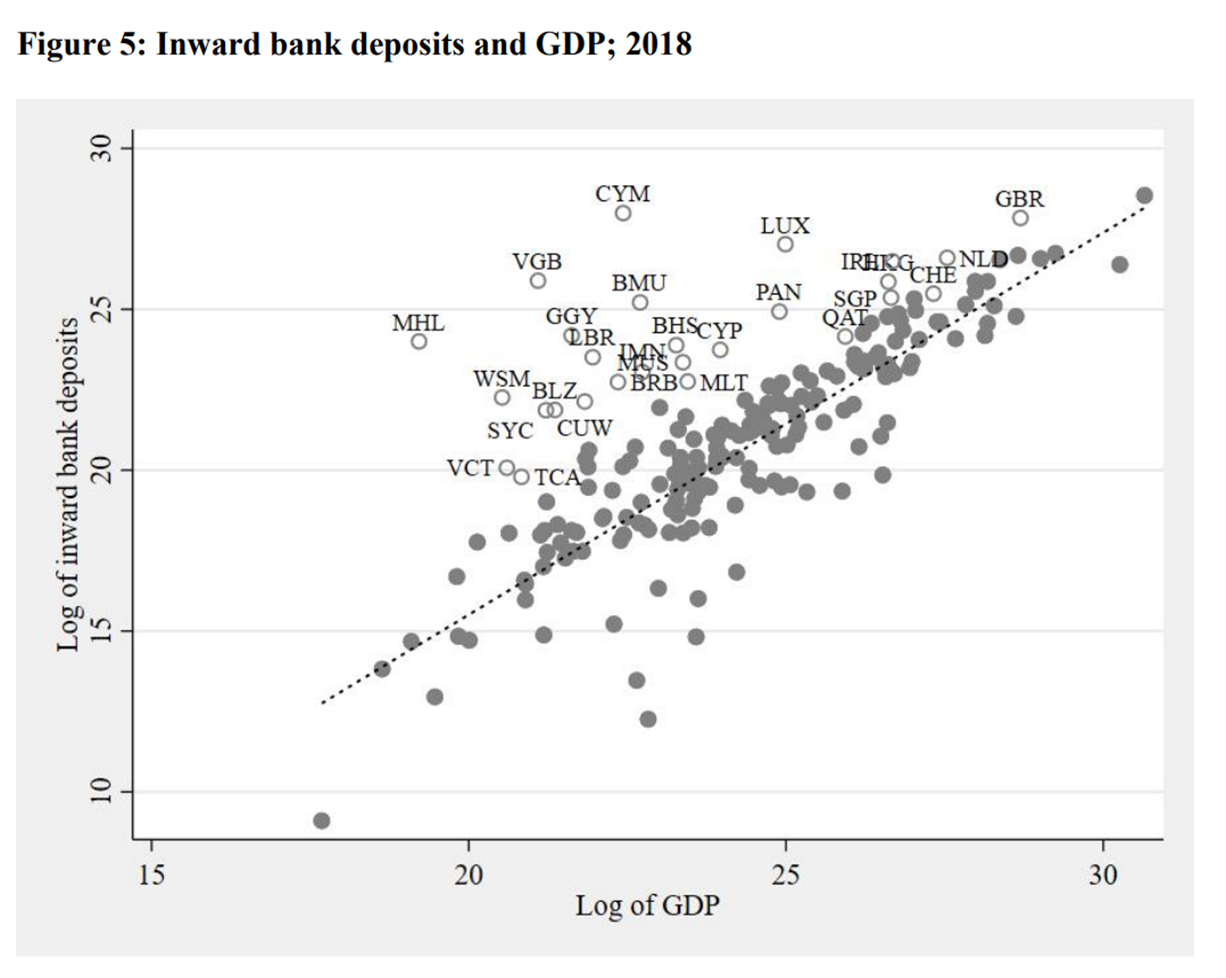

The State of Tax Justice does identify a pattern of “abnormal” bank deposits across jurisdictions. This means determining what share of the offshore bank deposits going into a jurisdiction can reasonably be explained by the level of genuine business activity going on in the country, and what share if any cannot.

We do not look only at the size of each jurisdiction’s economy, however (their GDP, or gross domestic product), but also at how secretive their regulations are. We identify 30 jurisdictions that are both relatively highly secretive, and also receive bank deposits far greater than can be readily explained by their economic activity. These 30 jurisdictions account for only 7 per cent of global GDP but are destinations for over 45 per cent of all offshore bank deposits.

We conduct a regression analysis on the rest of the jurisdictions in the world to determine a “normal”, or expected, relationship between bank deposits coming into a country and the country’s GDP, specifically in the case where the jurisdictions do not offer high bank secrecy.

This is shown in Figure 5, taken from the methodology. Jurisdictions with lower bank secrecy are shown as dark dots, and the strength of the relationship between deposits and GDP is clear (the dotted line shows the fitted model). Jurisdictions with high bank secrecy and abnormally high levels of deposits, are shown as clear circles and with 3-digit ISO codes (for example, CYM is Cayman and LUX is Luxembourg).

The regression allows us to identify a baseline for a normal level of offshore bank deposits coming into a country. The further jurisdictions offering bank secrecy appear above this line, the greater the probability we estimate that these deposits are undeclared to home country tax authorities. Because tax abuse is deliberately hidden, it is impossible to prove definitively that all deposits identified as abnormal here (exceeding this baseline) are undeclared. Some genuine economic activity may in fact be included. But bank secrecy is necessary to hide deposits, and the evidence here shows clearly that the provision of bank secrecy dominates the revealed pattern of abnormal deposits between jurisdictions. This supports the conclusion that this pattern of abnormal deposits provides a reasonable approximation for the distribution of undeclared offshore wealth.

Claim: The methodology assumes a 5% return on cash deposits.

Fact: The methodology does not assume a 5% return on cash deposits. The methodology assumes a 5% return on investments, in line with established research.

When calculating how much tax should have been paid on wealth hidden offshore by individuals, the methodology assumes hidden investments make a 5 per cent return. A personal income tax is then applied to this 5 per cent to determine how much tax was missed out on in the country where that offshore investment originally came from.

The assumption of a 5 per cent return on investments is directly sourced from a 2015 study by Gabriel Zucman. The methodology applies Zucman’s assumption of 5 per cent return to investments only. At no point does the methodology state otherwise. The methodology does not at any point specifically consider cash deposits.

The erroneous claim that State of Tax Justice’s methodology assumes a 5 per cent return on cash deposits, and that this contributes to an overestimating of the scale of offshore tax evasion, was made by Richard Murphy. Prof Murphy directly quotes our methodology when making this claim – even though the quoted line from our methodology clearly states the assumption relates to investments.

Screenshot from Richard Murphy’s 21 July 2021 blogLess detail▲

Claim: Corporate tax rates instead of personal income tax rates should be applied to some abnormal bank deposits.

Fact: The appropriateness of corporate tax rates is debatable and there is good reason to use personal income tax rates, as explained in our methodology.

When calculating how much tax countries lose to offshore tax evasion by individuals, we assume individuals would have paid personal income tax rates on the return they gain from the wealth they hid offshore.

Personal income tax rates are usually higher than other types of tax rates, like corporate tax rates and capital gains tax rates. It is possible that the return gained from wealth hidden offshore, if it were taxed instead of evaded, could have been taxed under a corporate tax rate if that return took the form of profit from a corporation or taxed under a capital gains tax rate if the government taxes dividends differently from personal income.

Using personal income tax rates it then follows to estimate how much tax countries lose to offshore tax evasion may put estimates on tax losses on the upper-end of the scale. The State of Tax Justice’s methodology considers this issue in detail.

Ultimately, we decide to use personal income tax rates for two reasons.

First, although in theory the methodology considers a full range of assets when looking at hidden offshore wealth, in practice the numbers are driven by financial account holdings, to which personal income tax rather than capital gains tax would generally apply.

Second, it can be argued that if the returns were actually declared for tax purposes, rather than hidden offshore, individuals would have an incentive to minimise their tax obligation by structuring their returns as capital gains rather than as individual income. In other words, when assuming what individuals would have paid if they did not evade tax, we should still they would have sought to abuse tax by utilising tax avoidance schemes. Therefore it is more appropriate to use a capital gains tax rate since this what would be applied under a tax minimising scheme. However, since the State of Tax Justice seeks to report how much tax countries would have collected if corporations and individuals paid the right amount of tax, in the right place and at the right time – in other words, if tax abuse and tax evasion was stopped – it is more appropriate to estimate how much tax would have been paid under personal income tax, rather than capital gains tax.

Lastly, it can also be argued that the existence of cases such as Italy where a lower rate than personal income tax would apply to income streams from declared offshore assets might suggest making more conservative adjustments on a country by country basis, and we will consider this for future work. We note, however, that even in such a case, the very existence of the hidden offshore wealth is the result of an originally undeclared income stream. For that reason, applying the higher personal income rate to a hypothetical income stream generated by the hidden offshore wealth – rather than to the original income stream that generated the hidden offshore wealth itself – will understate the total tax losses very substantially. (For comparison, the ECORYS study referred to above obtains a significantly higher estimate of tax losses, by evaluating a combination of tax evasion of taxes on capital income; of taxes on inheritance and wealth; and of personal income taxes on original income transferred offshore.)

Claim: The methodology’s calculation of the scale of hidden offshore wealth is based on undisclosed offshore bank deposits. These bank deposits would have actually been disclosed under FATCA/CRS and so the calculation is incorrect.

Fact: The estimate on the scale of hidden offshore wealth used in the report is sourced from ECORYS, which bases its estimate on a much wider range of assets than that covered by FATCA/CRS.

As has already been explained several times above, the estimate on the scale of hidden offshore wealth used in the report is sourced from a separate study commissioned by the European Commission and carried out by ECORYS. The estimates from ECORYS are widely regarded as the best available estimates on the scale of hidden offshore wealth.

ECORYS estimates that the scale of hidden offshore wealth stood at 11.4% of global GDP in 2018, which is US$9.9 trillion. GDP figures for 2018 here are sourced from the World Bank, the UN and CIA. ECORYS’s estimate of hidden offshore wealth is based wide range of financial assets, but primarily on undisclosed portfolio investments which are unlikely to be covered FATCA/CRS.

It has been claimed that this US$9.9 trillion figure is produced by the State of Tax Justice’s methodology and is based on wealth the methodology assumes to be hidden offshore in undisclosed bank accounts. This claim points to the US$16 trillion in previously hidden offshore bank deposits that have been disclosed following the introduction of FATCA/CRS. The claim argues that since the State of Tax Justice’s US$9.9 trillion figure is based on undisclosed bank deposits, it cannot be compatible with the US$16 trillion of now-disclosed bank deposits. Simply put, how can there be another US$10 trillion in undisclosed bank deposits out there beyond the US$16 trillion that have been disclosed and how could these escape reporting?

Again, the issue with this claim is that it is based on an incorrect understanding of the methodology. The US$9.9 trillion figure is sourced from an external study which assess a wide range of financial assets beyond those covered by FATCA/CRS, and takes into account the impact of these transparency measures by the year in question.

For this reason, the US$16 trillion recently disclosed under FATCA/CRS does not powerfully affect ECORYS’s estimate. If anything, it is possible that the narrowness of FACTA/CRS’s scope of coverage has increased the attraction of the portfolio assets covered by ECORYS, since these are not reportable. This is likely to include financial accounts (or very close substitutes) which have been specifically designed and marketed as non-reportable under FATCA and CRS. In addition, increases in equity prices increased the level of hidden offshore wealth quite separately from any changes in bank deposits.

Information exchanges under CRS began in 2018 and it has been hypothesised that this has dramatically reduced the scale of undisclosed offshore wealth to a level far below the US$9.9 trillion estimate assumed in the State of Tax Justice report.

This hypothesis, however, was already proved false in 2021. The scale of hidden offshore wealth in 2018 following the start of CRS exchanges remained at 11.4 per cent of global GDP, as estimated by ECORYS, compared to 11.6 per cent in 2017, as estimated by Alstadsaeter, Johannesen and Zucman in a study published in the highly-regarded Journal of Public Economics.

ECORYS’s 2021 study confirmed that FATCA/CRS had had an immaterial impact on the losses to offshore tax evasion monitored by the State of Tax Justice.

The estimate on the scale of hidden offshore wealth calculated by ECORYS takes into account the impact of FATCA/CRS, and so the impact of these transparency measures are accounted for by the State of Tax Justice. It’s just the impact has been minimal.

This is not to say that CRS has not been successful in providing some countries with transparency about certain types of financial accounts, and that is why the Tax Justice Network had long campaigned for the introduction of such multilateral measures. But the narrowness of the OECD approach, coupled with the noncompliance of the US and the effective exclusion of most lower income countries, means that a great deal of offshore wealth remains entirely hidden from tax authorities.

Where the State of Tax Justice does consider both undisclosed bank deposits and undisclosed portfolio investments is its evaluation of the distribution of hidden offshore wealth, not the scale of hidden offshore wealth, as repeatedly explained above. This evaluation is used to determine where the hidden offshore wealth estimated by ECORYS originated from.

Claim: The State of Tax Justice’s estimate on the scale of corporate tax abuse is based on a fictitious calculation of tax and is not a measure of profit shifting or tax abuse.

Fact: The State of Tax Justice’s estimate on the scale of corporate tax abuse is based on an established methodology in the field for estimating profit shifting known as the “misalignment methodology”. Similar use of misalignment methodology was made in a 2023 paper by economists Torslov, Wier and Zucman published in the Review of Economic Studies, as well as earlier studies including Cobham & Jansky in Development Policy Review, 2019, and Casella & Souillard in UNCTAD’s Transnational Corporations, 2022. The State of Tax Justice’s estimate on the scale of corporate tax abuse is in line with figures published by other organisations and leading researchers.

The misalignment method contrasts the share of reported profits in a jurisdiction with the share of economic activity in that jurisdiction. It contrasts how much profit a multinational corporation declares in a jurisdiction against how much genuine business activity it does in the jurisdiction (eg how many sales it makes there, how many people it employs there, how many stores, offices or factory it operates in the jurisdiction).

In theory, these two shares should be roughly similar, if our international tax system worked the way it was designed to. The arm’s length principle on which the international tax system is based in theory should take care of aligning reported profits with economic activity, but this principle is flawed and routinely abused by multinational corporations to shift profits to tax havens and underpay tax.

When the G20 group of countries first gave the OECD a mandate to reform international tax rules a decade ago, they agreed a single aim for the work: to reduce this misalignment between where multinationals declare their profits for tax purposes, and the location of their real economic activity. As such, the misalignment approach is the direct assessment of how far tax abuse means that this goal remains unreached.

The misalignment between reported profits and economic activity is overwhelmingly driven by tax rates: multinationals under the current rules are able often to report profits in low tax jurisdictions, while having significant economic activity in other countries. The alternative is to move to unitary taxation with formulary apportionment, which serves as the basic counterfactual in the misalignment methodology.

Unitary tax was also the alternative considered by the League of Nations a century ago, when they took the central decision to reject it in favour of the arm’s length approach that is now widely held to be unfit for purpose. The second OECD process began in 2019 with the organisation committing, finally, to go beyond arm’s length pricing.

Under unitary tax, multinational corporations pay tax based on where their economic activity takes place – ie where they make sales, employ people, produce goods and services – instead of where they report profits – ie instead of where they shift their profits to. Unitary tax requires a multinational corporation’s profits to be divvied up across the countries where it does business, so that each can tax their fair share. This makes tax havens redundant since multinational corporations don’t do much real business in tax havens.

This means when misalignment methodology is measuring the economic activity of multinational corporations across different jurisdictions to compare to where multinational corporations are reporting profit, misalignment methodology is not just estimating the losses the arise out of multinational corporations abusing the arm’s length principle, it’s also putting to practice the principles of unitary tax.

Dan Neidle claims that this approach to calculating corporate tax abuse is fictitious because unitary tax has not been adopted by law in the countries on which the State of Tax Justice reports. Mr Neidle states, “I’m not aware of any proposal that any country should tax on this basis.”

Unitary tax has been at the heart of international tax reform debate for over a hundred years. It now forms the key component of Pillar 1 of the OECD’s two-pillar proposal (multinationals’ profits are assessed at the global level and an element is apportioned according to the location, in this case, of their sales). One of three proposals for Pillar 1 that the OECD Inclusive Framework charged the secretariat with evaluating was the G-24 group of countries’ proposal for a full move to fractional apportionment, a close relation.

Unitary tax has also been gaining more support, for example, as part of the EU’s Common Consolidated Corporate Tax Base (CCCTB) proposals, which have been debated and explored over two decades, and now the Commission’s BEFIT proposals. Certain apportionment approaches are also allowed under even current OECD rules, and major countries including India make use of these without difficulty. In addition, the approach is also well established for use by subnational jurisdictions and has been in application for decades in countries including the United States, Canada and Switzerland.

While we regret that Mr Neidle says he has not heard of any of these proposals, we do not feel that this fact constitutes a substantive criticism of the approach in the State of Tax Justice. And it may only be that these proposals have slipped Mr Neidle’s mind. In 2018, for example, he interviewed the European Commission’s then-Director-General for Tax about the CCCTB. Mr Neidle published a reflection on their discussion, in which he concludes: “This is probably the moment advocates of unitary taxation have been waiting for. The press and public are more focused on tax than ever before. France and Germany are fully backing CCCTB…”.

Although unitary tax has yet to be legally implemented in full internationally, it is by design a solution to the failure of the arm’s length principle. The misalignment methodology captures the extent of this failure, and is the only possible measure of the single, stated goal given to the OECD for its policy reforms over the last decade by the G20 group of countries. As the academic research literature also confirms, this is an entirely appropriate basis on which to assess the scale of tax abuse.

Claim: The Tax Justice Network has ignored criticism of the State of Tax Justice’s methodology, particularly on the impact of FACTA/CRS.

Fact: The Tax Justice Network publicly responded to these criticisms in 2021, demonstrating at the time how FACTA/CRS had no material impact on the reports figures.

Dan Neidle claims, in a blog published 25 July 2023, that the Tax Justice Network has ignored criticism of its methodology. The Tax Justice Network publicly responded to these criticisms in 2021.

Despite claiming in his blog that the Tax Justice Network has ignored criticism, Mr Neidle actually links in Footnote 7 of his blog to our 2021 public response, contradicting his claim.

The footnote dismisses our 2021 public response and erroneously implies again that the estimation of the scale of hidden offshore wealth used in the report is calculated by the State of Tax Justice’s methodology, when it is actually sourced from the ECORYS study. Mr Neidle’s blog does not make any mention of the ECORYS study, nor its conclusions on the impact of FATCA and CRS on its assessment.

Footnote 7 in Dan’s blog states:

“Subsequently, TJN justified their conclusions on the basis that the data showed little change in offshore wealth since FATCA/CRS had been introduced. The obvious explanation is that TJN’s methodology has always been wrong, and FATCA/CRS merely reveals this. TJN, however, prefer to believe that their methodology is correct and the actual measurable outcomes of FATCA/CRS should be discarded.”

The document Mr Neidle links to is sufficient to show his error. The “actual, measurable outcomes of FATCA/CRS” are indeed accounted for and discussed in the ECORYS study which is the underlying source for our estimate.

We share the hope that these arrangements for automatic exchange of financial information will be improved sufficiently to yield a much more visible scale of benefits in reducing undeclared offshore deposits. Indeed, we would not have spent our first decade of existence as an organisation campaigning for this, in the face of OECD opposition, had we not believed in the potential for such progress, on the basis of careful analysis. That hope should not blind us to the fact that in the first year of CRS exchange, the estimates of ECORYS show that undeclared offshore wealth overall is likely to have grown.

Cayman Finance has similarly claimed this week that the Tax Justice Network has not addressed criticism of the State of Tax Justice: “The latest State of Tax Justice report has made no effort to correct any of the shortcomings of previous iterations.” We did respond to Cayman Finance’s criticisms when responding to Mr Neidle and Prof Murphy in 2021. Cayman Finance’s post this week mostly reiterates Dan Neidle’s and Richard Murphy’s criticisms, all of which have been addressed again in this blog.

Cayman Finance has also reiterated criticisms against the State of Tax Justice made in a report commissioned and published by Cayman Finance in 2021 – which we also responded to at the time. The report was written by Julian Morris, a senior fellow at the Reason Foundation. The Reason Foundation is a libertarian think-tank funded by Koch foundations and had as a trustee for 36 years the late US billionaire David Koch. Since the early 1990s, the Reason Foundation has repeatedly been criticised for taking money from fossil fuel companies and tobacco firms while publishing writings that align with those companies’ interests.

The Reason Foundation was one of 32 organisations with links to fossil fuel interests called out by US senators in July 2016 for their role in “perpetrating a sprawling web of misdirection and disinformation to block action on climate change.” Cayman Finance’s report takes a similar tone of misdirection and evidence-denialism. While we are always keen to engage with different views, we do not consider the erroneous and at time outlandish claims in Cayman Finance’s report to have been made in good faith. For this reason, we have chosen to not dedicate space in this blog to point out (yet again) the errors and misrepresentation in these claims. Our original public response to Cayman Finance’s report and wider criticisms is available here.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.

")